Leveraging brand and an omnichannel platform to face the fintech challenge on retail banking

23

Leveraging brand and an omnichannel platform to face the fintech challenge in retail banking Daniel Ferretti CMO & Online Channels - Sicredi

-

Upload

daniel-ferretti -

Category

Business

-

view

183 -

download

0

Transcript of Leveraging brand and an omnichannel platform to face the fintech challenge on retail banking

Leveraging brand and an

omnichannel platform to

face the fintech challenge in

retail bankingDaniel FerrettiCMO & Online Channels - Sicredi

Quick overview: Brazil at a glance

• 8th largest economy in the world ($ 1.9 tri GDP / $ 3,6 tri PPP);

• Largest economy in Latin America;

• Total population 204 million (112 labor force);

• 108 million people have bank accounts (60% -US 71%);

• Amidst economic downturn ( 2,97% fcst GDP in 2015);

• Political crisis due to corruption charges (approval is 9%).

Estaiada bridge in São Paulo Beach in Rio de Janeiro Agribusiness in the Midwest

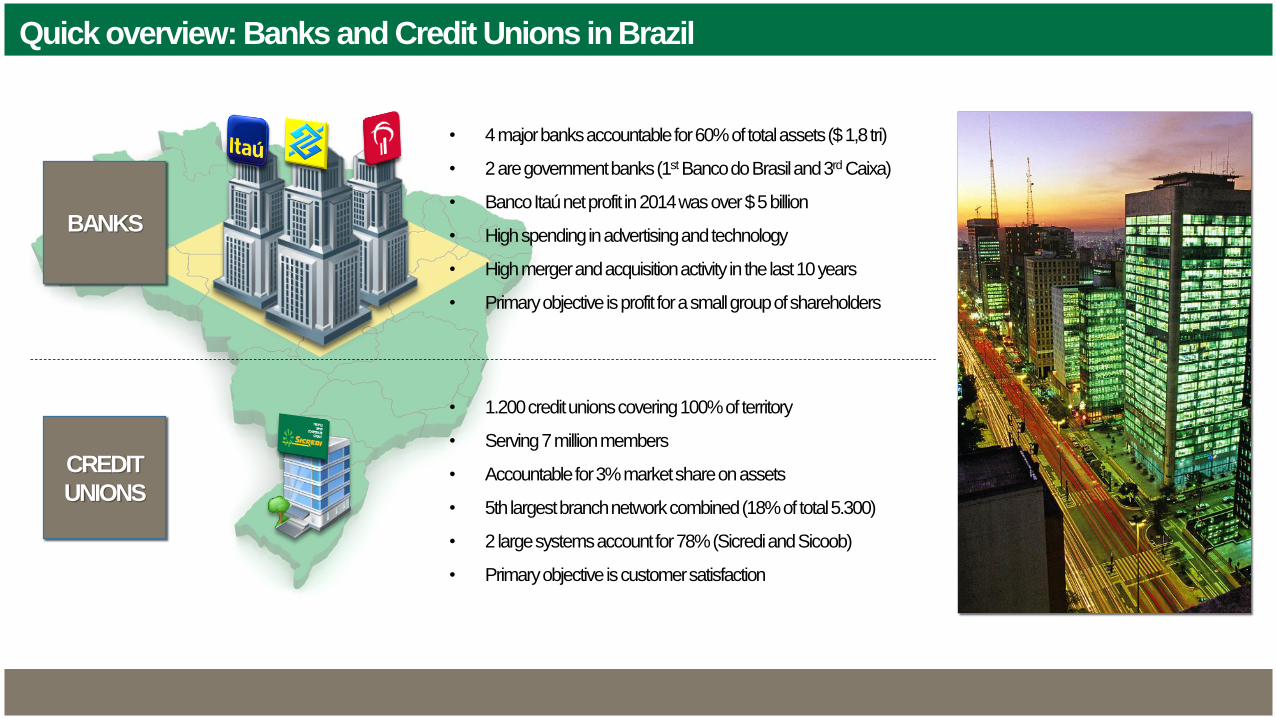

Quick overview: Banks and Credit Unions in Brazil

• 4 major banks accountable for 60% of total assets ($ 1,8 tri)

• 2 are government banks (1st Bancodo Brasiland 3rd Caixa)

• BancoItaúnet profit in 2014 was over $ 5 billion

• High spending in advertising and technology

• High merger and acquisition activity in the last 10 years

• Primary objective is profit for a small group of shareholders

• 1.200 credit unions covering 100% of territory

• Serving 7 million members

• Accountable for 3% market share on assets

• 5th largest branch network combined (18% of total 5.300)

• 2 large systems account for 78% (Sicrediand Sicoob)

• Primary objective is customer satisfaction

BANKS

CREDIT

UNIONS

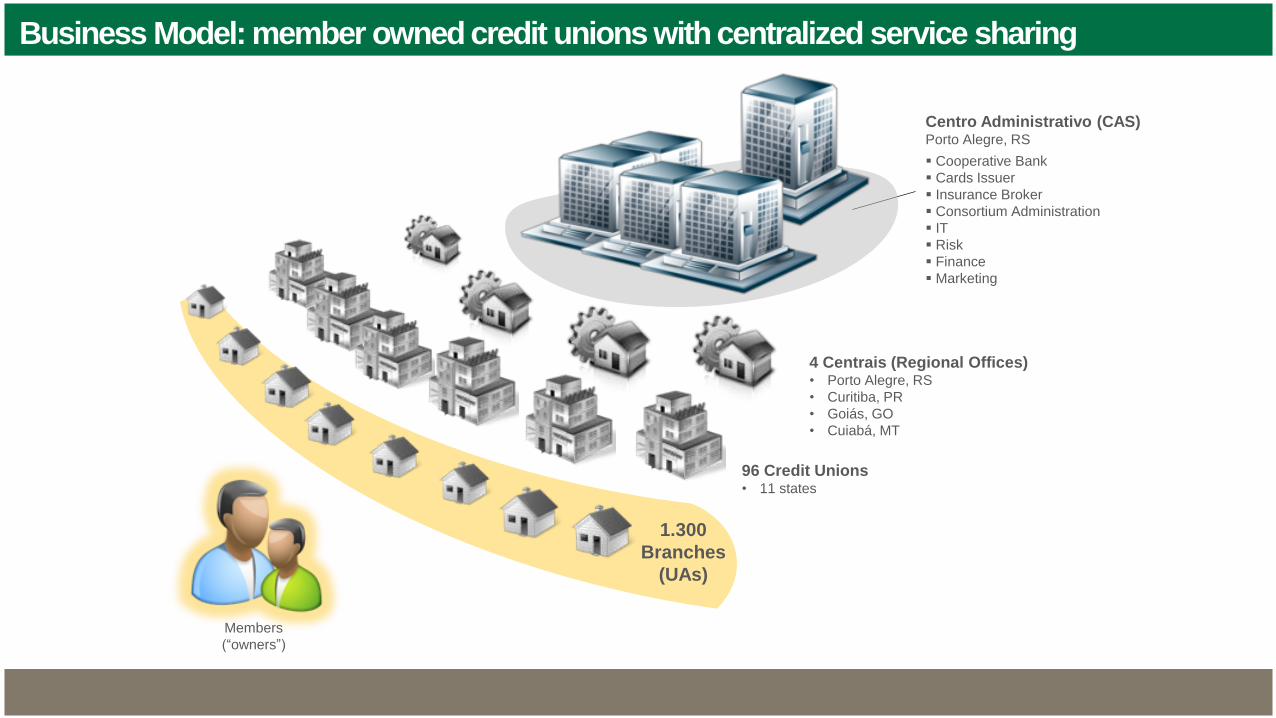

“People who cooperate grow“Administrative and operations office in Porto Alegre, RS

Quick overview: Sicredi

• 96 credit unions operating under a single brand

• 3 million members

• 1.370 branches in 11 states

• 18.000 employees

• US$ 18 bi in assets

• Centralized data center, operations and products

Inside Guaravera BranchJaniópolis Branch São Mateus do Sul Branch

1.300

Branches

(UAs)

4 Centrais (Regional Offices)• Porto Alegre, RS

• Curitiba, PR

• Goiás, GO

• Cuiabá, MT

Centro Administrativo (CAS)Porto Alegre, RS

Cooperative Bank

Cards Issuer

Insurance Broker

Consortium Administration

IT

Risk

Finance

Marketing

96 Credit Unions• 11 states

Members

(“owners”)

Business Model: member owned credit unions with centralized service sharing

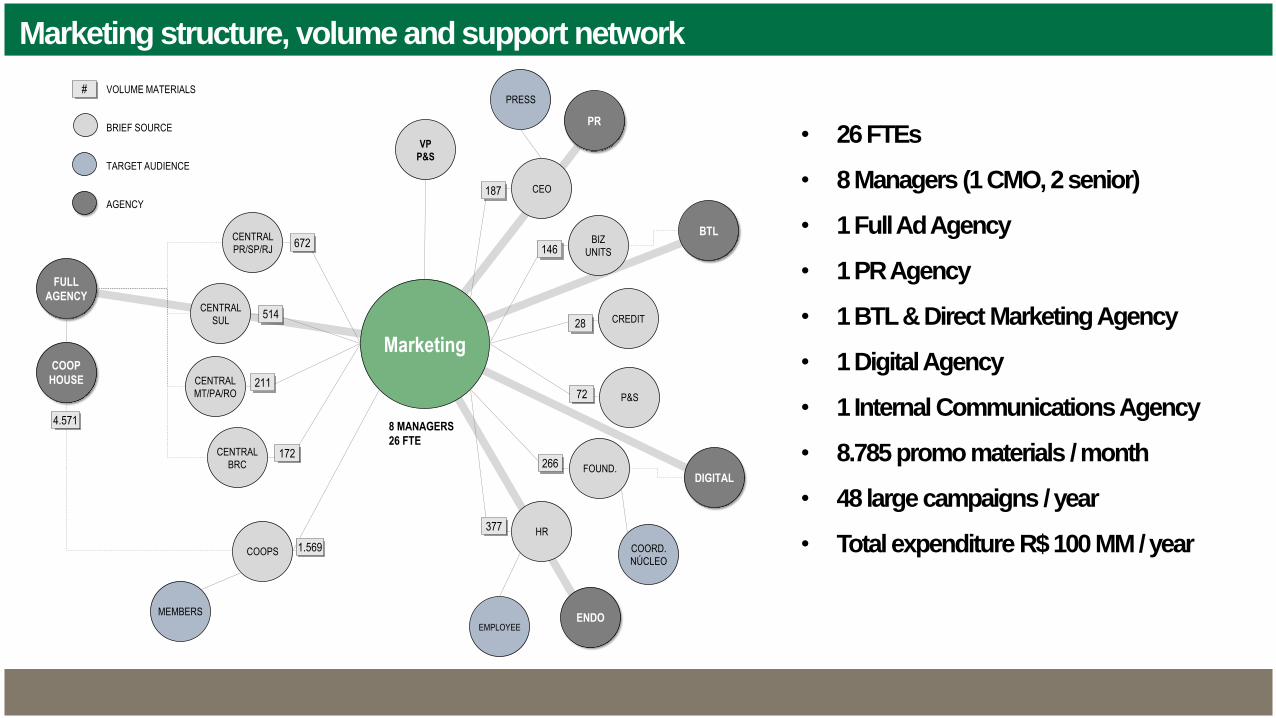

Marketing structure, volume and support network

Marketing

CENTRAL

MT/PA/RO

CENTRAL

BRC

CENTRAL

PR/SP/RJ

CENTRAL

SUL

P&S

FOUND.

BIZ

UNITS

CREDIT

CEO

HR

PRESS

COOPS

EMPLOYEE

MEMBERS

COORD.

NÚCLEO

FULL

AGENCY

COOP

HOUSE

ENDO

BTL

DIGITAL

PR

VP

P&S

672

514

211

172

1.569

377

187

146

28

72

266

4.571

# VOLUME MATERIALS

BRIEF SOURCE

TARGET AUDIENCE

AGENCY

8 MANAGERS

26 FTE

• 26 FTEs

• 8 Managers (1 CMO, 2 senior)

• 1 Full Ad Agency

• 1 PR Agency

• 1 BTL & Direct Marketing Agency

• 1 Digital Agency

• 1 Internal Communications Agency

• 8.785 promo materials / month

• 48 large campaigns / year

• Total expenditure R$ 100 MM / year

Brand performance 2013 to 2015

• Highest growth of brand

awareness among all financial

institutions (89%)

• 3rd ranked in inducted brand

recall

• 4th ranked in spontaneous in

brand recall

• Expenditure is 1/12 compared

to top 3 players average

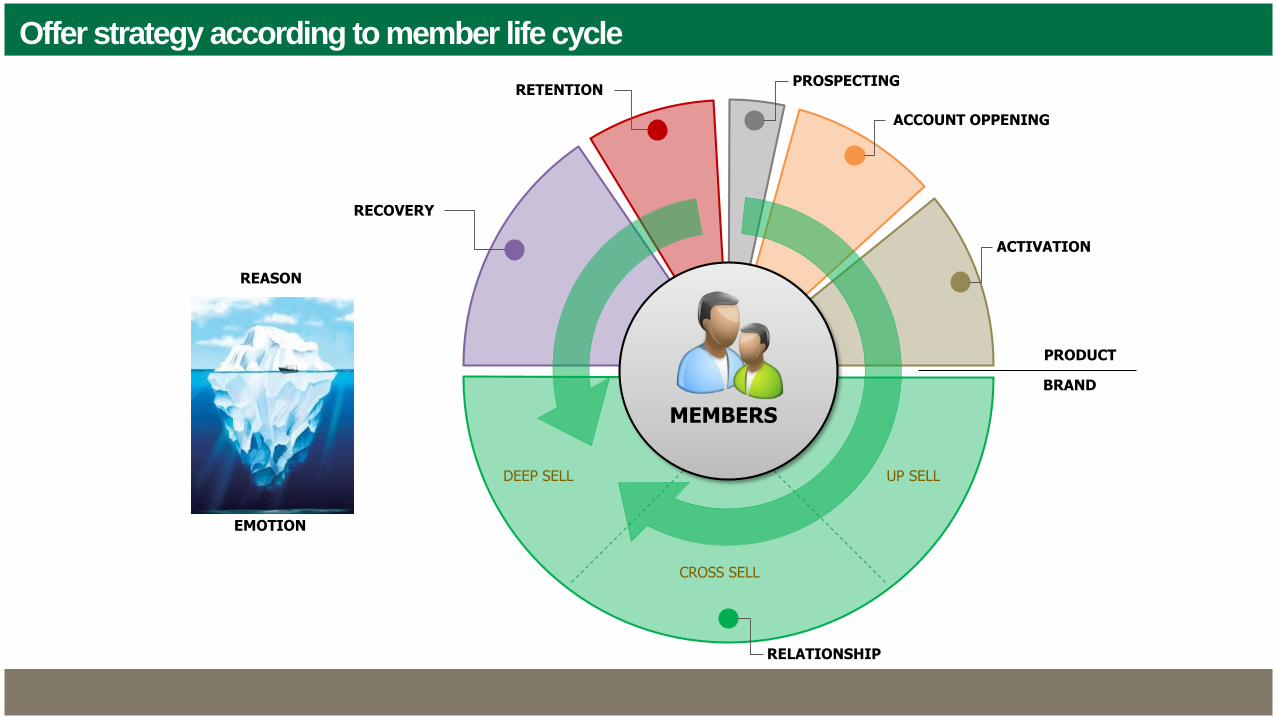

Offer strategy according to member life cycle

RELATIONSHIP

ACTIVATION

ACCOUNT OPPENING

PROSPECTING

RECOVERY

RETENTION

MEMBERS

UP SELL

CROSS SELL

DEEP SELL

REASON

EMOTION

BRAND

PRODUCT

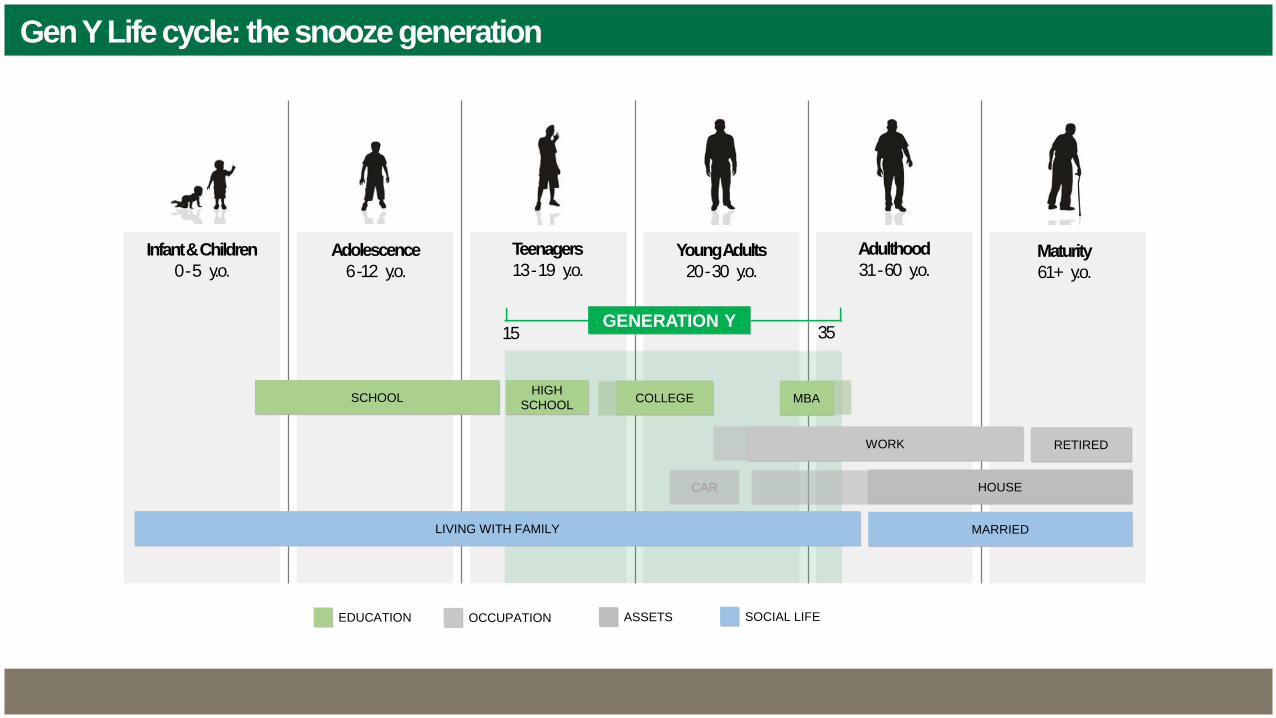

Gen Y Life cycle: the snooze generation

Infant & Children

0 -5 y.o.

Adolescence

6 -12 y.o.

Teenagers

13 -19 y.o.Young Adults

20 -30 y.o.

Adulthood

31 -60 y.o.Maturity

61+ y.o.

GENERATION Y15 35

SCHOOLHIGH

SCHOOLCOLLEGE MBA

MARRIEDLIVING WITH FAMILY

WORK RETIRED

HOUSECAR

EDUCATION OCCUPATION SOCIAL LIFEASSETS

Technology, alongside with market changes, transformed media in a profound way

1950 to1980 – “Broadcast Era” 1980 to2000 – “Clutter Era” 2000 to ... –“Network Era”

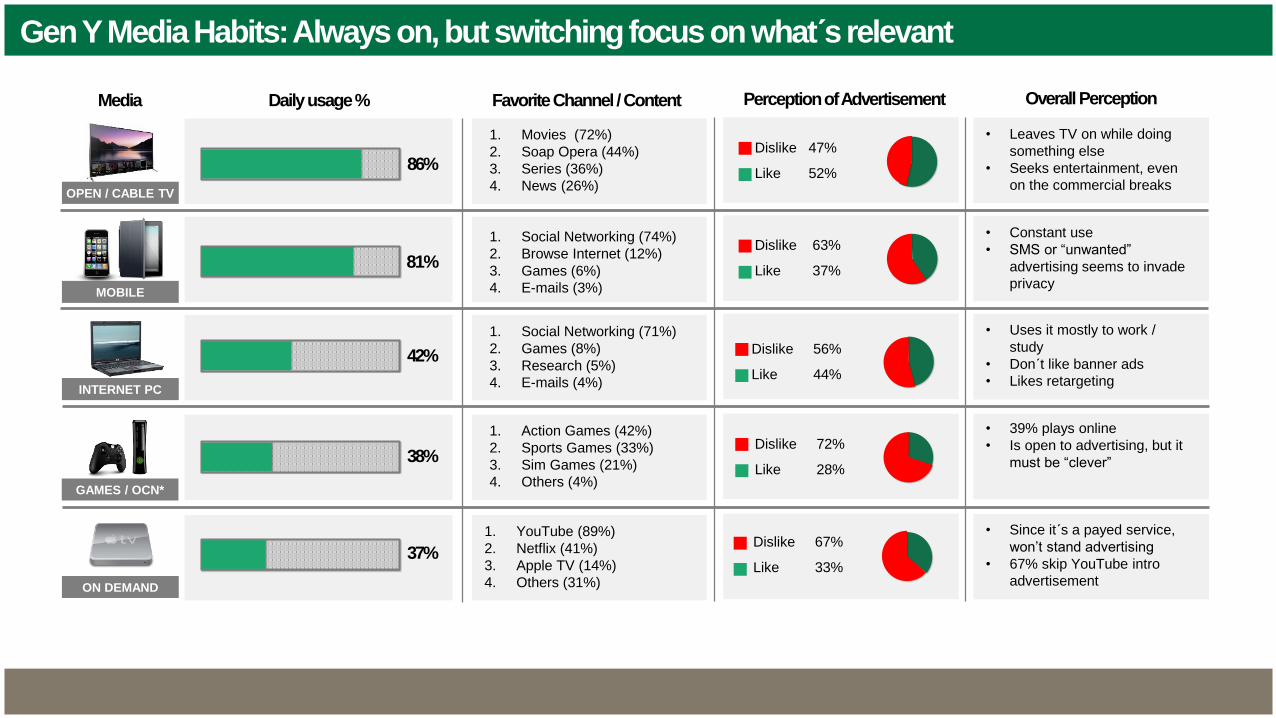

Gen Y Media Habits: Always on, but switching focus on what́ s relevant

OPEN / CABLE TV

INTERNET PC

MOBILE

ON DEMAND

GAMES / OCN*

86%

81%

42%

38%

37%

Daily usage % Favorite Channel / Content

1. Movies (72%)

2. Soap Opera (44%)

3. Series (36%)

4. News (26%)

1. Social Networking (74%)

2. Browse Internet (12%)

3. Games (6%)

4. E-mails (3%)

1. Social Networking (71%)

2. Games (8%)

3. Research (5%)

4. E-mails (4%)

1. Action Games (42%)

2. Sports Games (33%)

3. Sim Games (21%)

4. Others (4%)

1. YouTube (89%)

2. Netflix (41%)

3. Apple TV (14%)

4. Others (31%)

Perception of Advertisement

Dislike 47%

Like 52%

Dislike 63%

Like 37%

Dislike 56%

Like 44%

Dislike 72%

Like 28%

Dislike 67%

Like 33%

Overall Perception

• Leaves TV on while doing

something else

• Seeks entertainment, even

on the commercial breaks

• Constant use

• SMS or “unwanted”

advertising seems to invade

privacy

• Uses it mostly to work /

study

• Don´t like banner ads

• Likes retargeting

• 39% plays online

• Is open to advertising, but it

must be “clever”

• Since it´s a payed service,

won’t stand advertising

• 67% skip YouTube intro

advertisement

Media

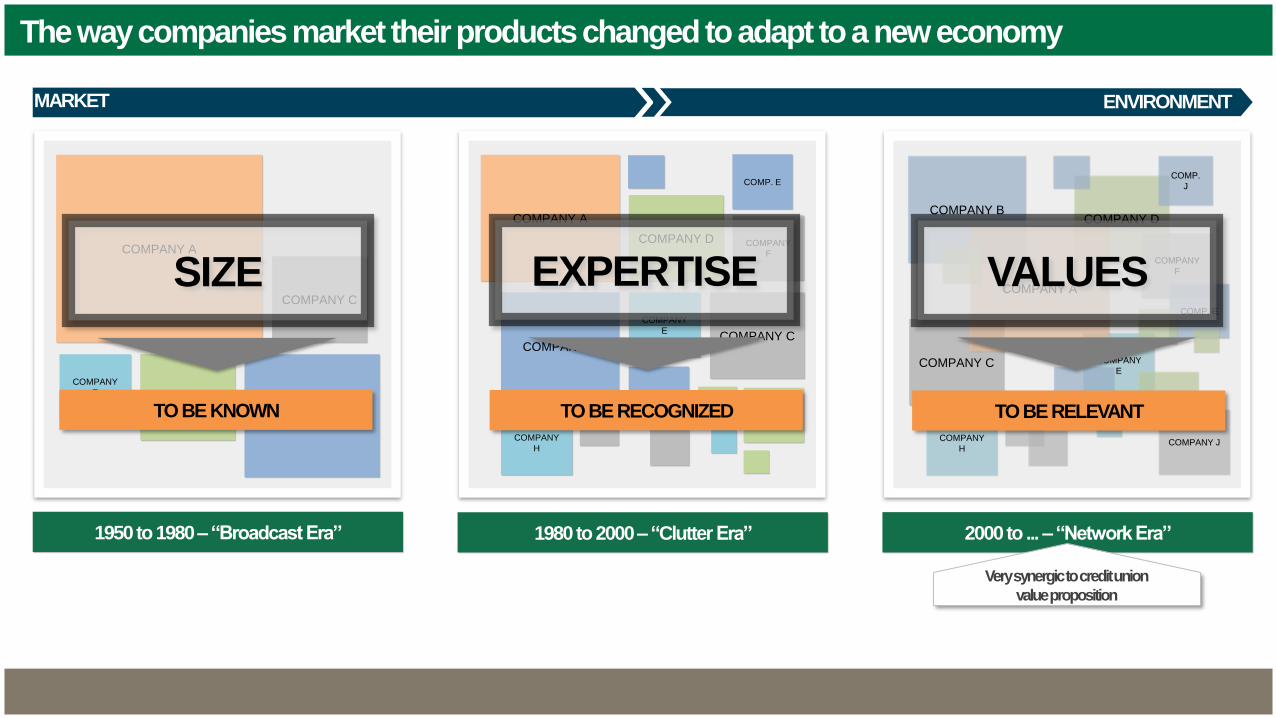

The way companies market their products changed to adapt to a new economy

COMPANY A

COMPANY B

COMPANY C

COMPANY D

COMPANY

E

1950 to1980 – “Broadcast Era”

COMPANY A

COMPANY BCOMPANY C

COMPANY D

COMPANY

E

COMPANY

F

COMPANY

H

COMP. E

COMP. E

COMP. G

1980 to2000 – “Clutter Era”

COMPANY B

COMPANY C

COMPANY D

COMPANY

E

COMPANY

F

COMPANY

H

COMP. E

COMP. E

COMP. G

COMPANY A

COMP.

J

COMPANY J

2000 to ... –“Network Era”

SIZE EXPERTISE VALUES

TO BE KNOWN TO BE RECOGNIZED TO BE RELEVANT

MARKET ENVIRONMENT

Very synergic to credit union

value proposition

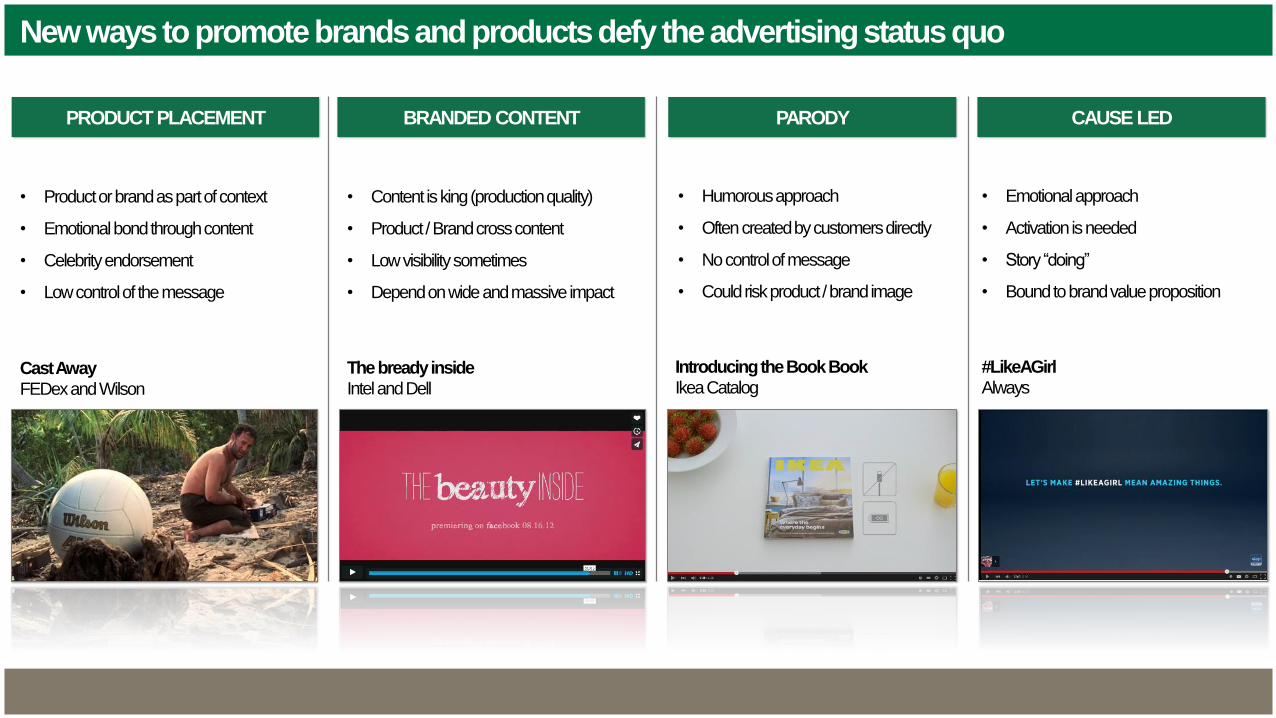

New ways to promote brands and products defy the advertising status quo

PRODUCT PLACEMENT BRANDED CONTENT PARODY CAUSE LED

Cast AwayFEDexand Wilson

The bready insideIntel and Dell

Introducing the Book BookIkea Catalog

#LikeAGirlAlways

• Product or brand as part of context

• Emotional bond through content

• Celebrity endorsement

• Low control of the message

• Content is king (production quality)

• Product / Brand cross content

• Low visibility sometimes

• Depend on wide and massive impact

• Humorous approach

• Often created by customers directly

• No control of message

• Could risk product / brand image

• Emotional approach

• Activation is needed

• Story “doing”

• Bound to brand value proposition

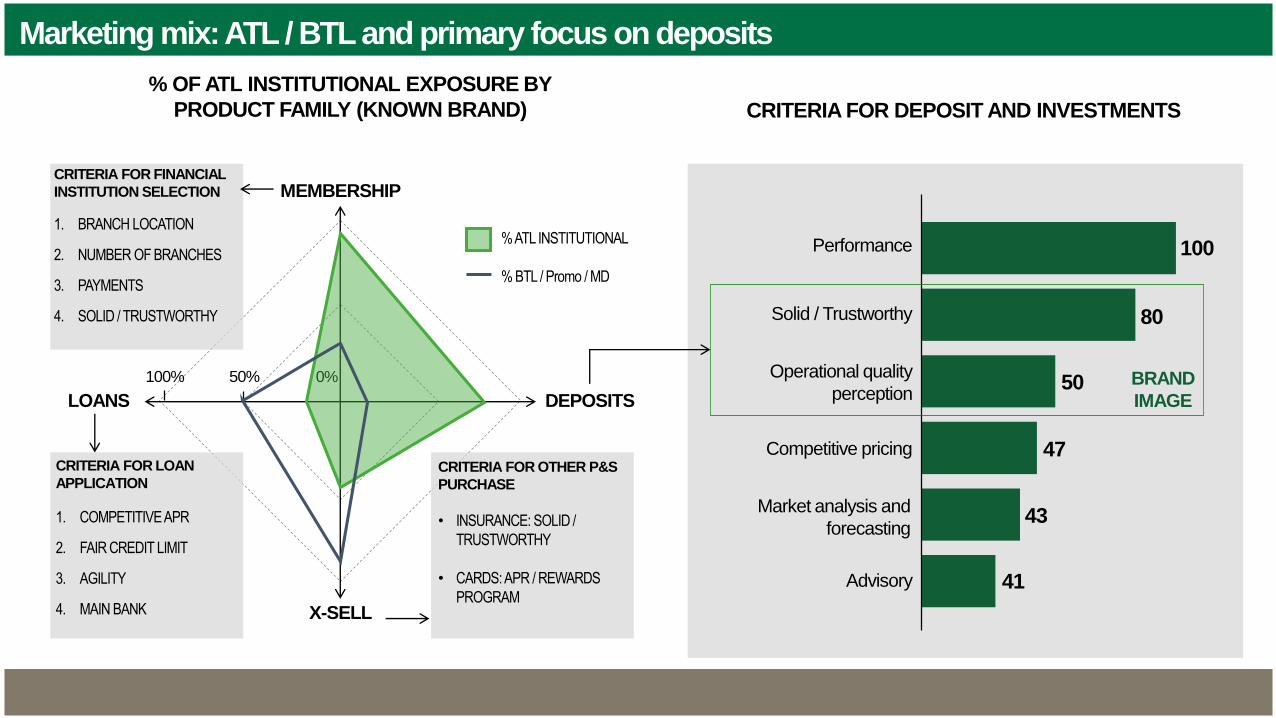

0%

MEMBERSHIP

X-SELL

DEPOSITSLOANS

% OF ATL INSTITUTIONAL EXPOSURE BY

PRODUCT FAMILY (KNOWN BRAND) CRITERIA FOR DEPOSIT AND INVESTMENTS

100Performance

Solid / Trustworthy

Operational quality

perception

Competitive pricing

Market analysis and

forecasting

Advisory

80

50

47

43

41

BRAND

IMAGE

100% 50%

CRITERIA FOR FINANCIAL

INSTITUTION SELECTION

1. BRANCH LOCATION

2. NUMBER OF BRANCHES

3. PAYMENTS

4. SOLID / TRUSTWORTHY

CRITERIA FOR LOAN

APPLICATION

1. COMPETITIVE APR

2. FAIR CREDIT LIMIT

3. AGILITY

4. MAIN BANK

CRITERIA FOR OTHER P&S

PURCHASE

• INSURANCE: SOLID /

TRUSTWORTHY

• CARDS: APR / REWARDS

PROGRAM

% ATL INSTITUTIONAL

% BTL / Promo / MD

Marketing mix: ATL / BTL and primary focus on deposits

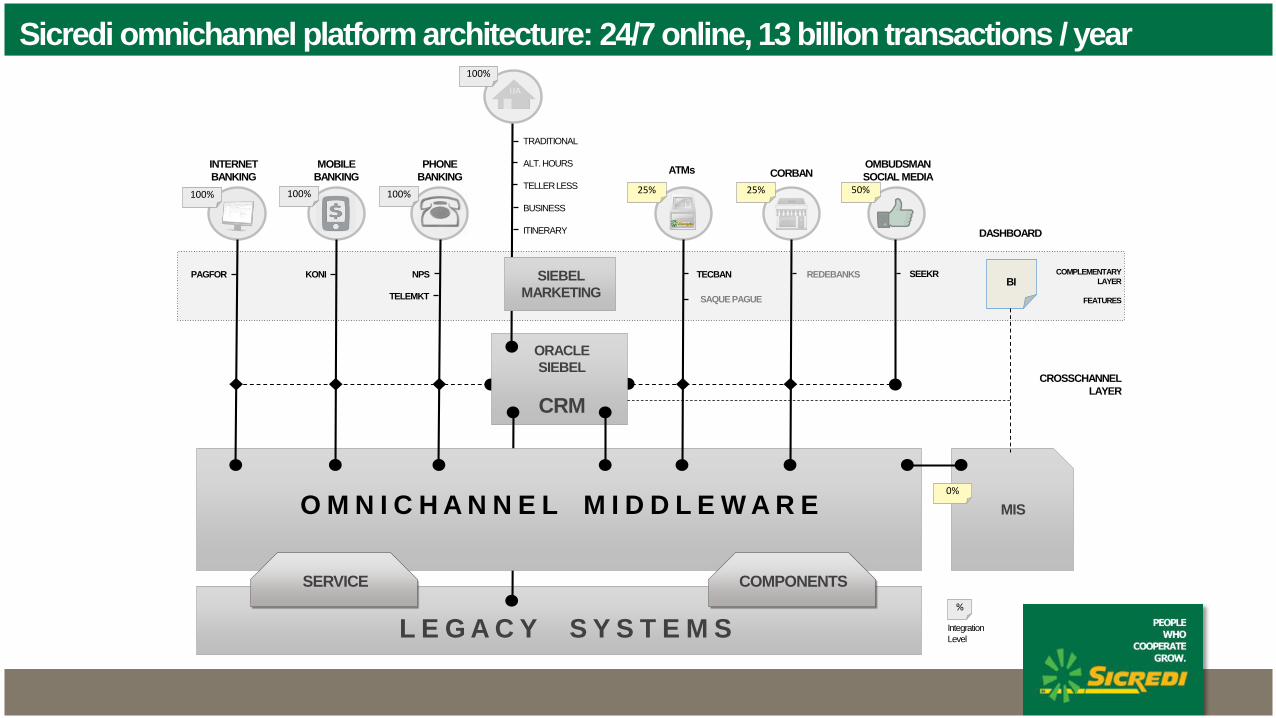

Achieving a standardized in branch experience: brand to commercial model

Business

Who am I?

Operations

Advertising

What do I have to

offer?Value Proposition

How do I deliver

my promise?Commercial Model

How do I become

efficient in doing

that?Operational Model

BRAND

PORTFOLIO

STAFF

BACK OFFICE

INTERNET

BANKING

MOBILE

BANKING

PHONE

BANKINGATMs CORBAN

OMBUDSMAN

SOCIAL MEDIA

ORACLE

SIEBEL

CRM

BRANCHES

SIEBEL

MARKETING

TECBAN

SAQUE PAGUE

PAGFOR KONI REDEBANKSNPS SEEKR

L E G A C Y S Y S T E M S

O M N I C H A N N E L M I D D L E W A R E

SERVICE COMPONENTS

MIS

BI

DASHBOARD

TRADITIONAL

ALT. HOURS

TELLER LESS

BUSINESS

ITINERARY

100% 100%

TELEMKT

100% 25% 25% 50%

100%

0%

%

Integration

Level

COMPLEMENTARY

LAYER

FEATURES

CROSSCHANNEL

LAYER

Sicredi omnichannel platform architecture: 24/7 online, 13 billion transactions / year

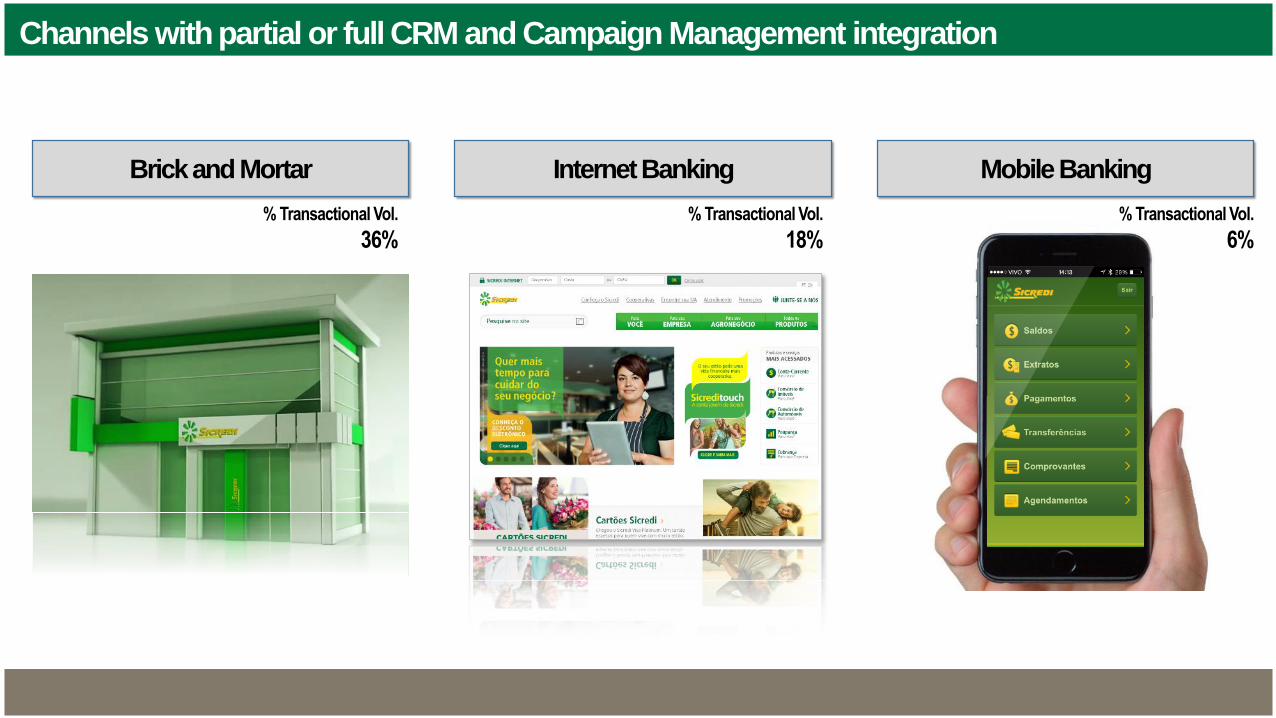

Channels with partial or full CRM and Campaign Management integration

Brickand Mortar Internet Banking Mobile Banking

% Transactional Vol.

6%% Transactional Vol.

18%% Transactional Vol.

36%

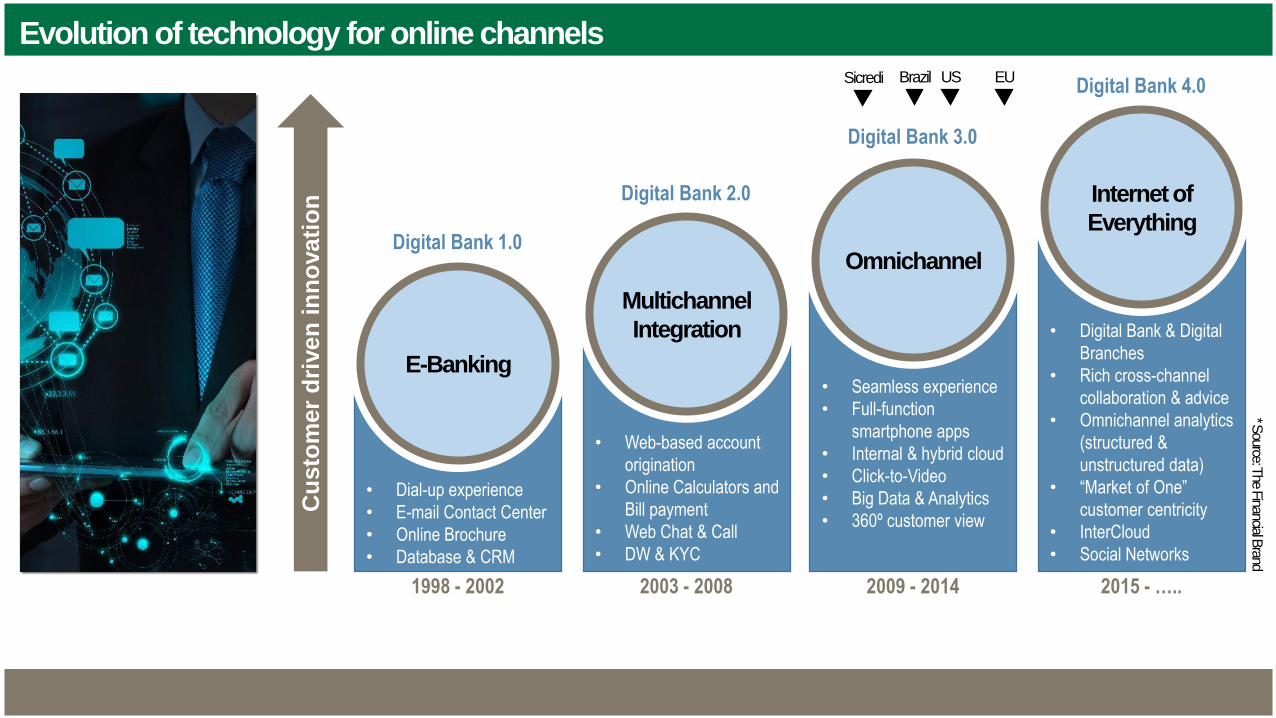

Evolution of technology for online channels

Internet of

Everything

Omnichannel

Multichannel

Integration

E-Banking

Cu

sto

mer

dri

ven

in

no

vati

on

Digital Bank 1.0

Digital Bank 2.0

Digital Bank 3.0

Digital Bank 4.0

1998 - 2002 2003 - 2008 2009 - 2014 2015 - …..

• Dial-up experience

• E-mail Contact Center

• Online Brochure

• Database & CRM

• Web-based account

origination

• Online Calculators and

Bill payment

• Web Chat & Call

• DW & KYC

• Seamless experience

• Full-function

smartphone apps

• Internal & hybrid cloud

• Click-to-Video

• Big Data & Analytics

• 360º customer view

• Digital Bank & Digital

Branches

• Rich cross-channel

collaboration & advice

• Omnichannel analytics

(structured &

unstructured data)

• “Market of One”

customer centricity

• InterCloud

• Social Networks

Sicredi Brazil US EU

* Source: T

he Financial B

rand

• Online customer onboarding

• Document scanning and biometric Id

• Social network linked

• Customizable look&feel

• PFM engine (Personal Finance Management)

• Campaign trigger offers and services

• Peer to peer interaction and transaction

• Easy to access (less security keys)

• No fees

• Integrated with e-payment tools

As brick and mortar branches become more rare, digital banking is growing in relevance due to enhanced customer experience, self-serving characteristic and low cost.

Credit Unions should be prepared to upgrade their online experience and face a new competitor: fintech startup companies

FinTech and Digital Banking 4.0

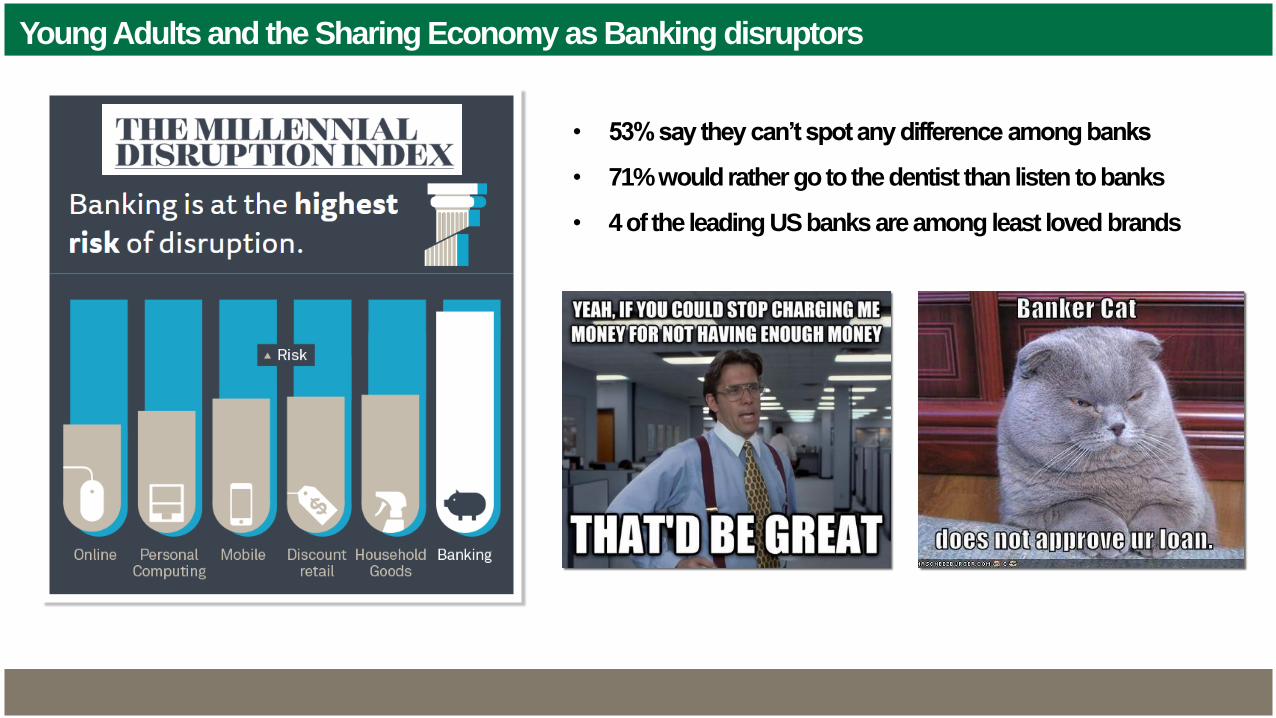

Young Adults and the Sharing Economy as Banking disruptors

• 53% say they can’t spot any difference among banks

• 71% would rather go to the dentist than listen to banks

• 4 of the leading US banks are among least loved brands

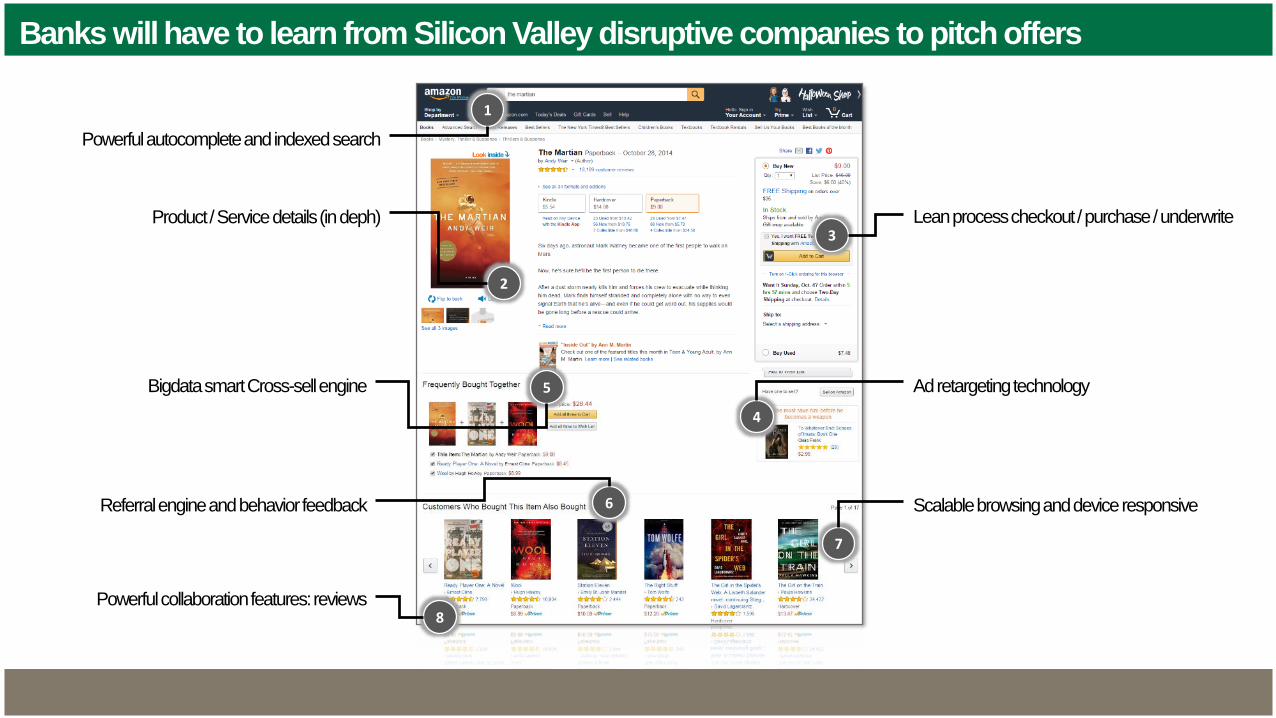

Banks will have to learn from Silicon Valley disruptive companies to pitch offers

Powerful autocomplete and indexed search

Product / Service details (in deph)

Bigdatasmart Cross-sell engine

Referral engine and behavior feedback Scalable browsing and device responsive

Ad retargeting technology

Lean process checkout / purchase / underwrite

Powerful collaboration features: reviews

1

2

3

4

5

6

7

8

Wrap up

• Sicredi is truly glo-cal: A national brand and standardized operations model with local presence;

• Despite branding efforts a solid campaign management engine is core to push for growth;

• Banks have been taking advantage of regulatory boundaries in place;

• Threat from FinTech startup and disruptive models pressure banks to move quicker;

• Young Adults don’t like banks, and they hope something disruptive will take place;

• Don’t listen to your COO: build a Digital Bank for your customer, not for your bank;

• Banks will need to be more transparent (no more hidden check boxes) and learn Big Data;

• Credit Unions have the advantage of beign 100% member centered. That will pay off in the future.