Lehman Brothers Strategy

47

Sovereign Strategy A Framework for Analysis Kaushik Rudra February 2002 Confidential

-

Upload

ishtmeet-singh -

Category

Documents

-

view

230 -

download

0

Transcript of Lehman Brothers Strategy

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 1/47

Sovereign StrategyA Framework for Analysis

Kaushik Rudra

February 2002

Confidential

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 2/47

The Framework

for Analysis

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 3/47

3

Framework for Analysis

A combination of top down and bottom up analysis

Fundamental, credit, political and technical analysis

Globally unified view disseminated via a total rate of return

Model Portfolio Inter- and intra-country relative value ideas disseminated via a

relative value portfolio

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 4/47

4

Top Down Analysis

Global themes

G7 themes (US/EU/Japan)

Emerging market themes (e.g. Argentina)

Crossover market themes Exogenous shock (September 11)

Global liquidity conditions

Asset class valuation

Relative richness or cheapness of EM asset class versus HighGrade and High Yield

Strong emphasis on global political analysis

Geopolitical events analysis

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 5/47

5

Bottom Up Analysis

Fundamental analysis

Real sector analysis

Public sector financing analysis

External financing analysis Debt dynamics exercise

External support (private and public sector)

Reform and privatization effort

Multilateral support Geopolitical and strategic considerations

Access to foreign capital (direct & portfolio)

Question 1: Capacity to Service Debt?

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 6/47

6

Capacity to Service DebtMacroeconomic Fundamentals

Income levels (GDP/capita)

Income distribution

Unemployment

GDP composition Dependence on commodity prices

Share of exports

Growth trends & prospects

Sources of growth Domestic savings/investment rate

Export potential

FDI inflows

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 7/477

Capacity to Service DebtEconomic Policy

Fiscal policy

Tax Policy

Monetary policy

Exchange rate policy Interest rate policy

Credit policy

Commitment to market reforms

Support from multilateral organizations

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 8/478

Capacity to Service DebtFiscal and Monetary Policy

Effectiveness – impact on growth, inflation, FX rate

Purpose of government spending

Ability to raise taxes

Economy‟s sensitivity to interest rates Commitment to price stability

Key indicators

Budget deficit/GDP

Primary deficit/GDP Public debt/GDP

Level of real interest rates

Inflation trend

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 9/479

Capacity to Service DebtCurrency Regime

FX – free-floating; pegged against a currency basket;currency board

Will the Central Bank use reserves to defend FX?

Contagion Risk of devaluation

Impact on country‟s ability to service foreign debt

Reserves coverage (Reserves/Imports)

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 10/4710

Capacity to Service DebtCommitment to Market Reforms

Privatization

Pace, scale, price

Ability to attract strategic investors

Trade liberalization Banking sector restructuring

Labor reforms

Public support

Legal/regulatory framework

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 11/4711

Capacity to Service DebtSupport from Multilateral Organizations

Official lending: IMF, World Bank, EBRD, etc.

Often covers a substantial portion of funding needs

IMF program in place

Availability of contingency funds Signaling mechanism for private lenders

Track record

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 12/4712

Capacity to Service DebtBalance of Payments

Typical EMG economy

Current account deficit (trade deficit; interest payments onexternal debt)

Dependency on foreign capital inflows Large current account deficit

May exert pressure on FX

Not necessarily negative

Differentiating factor

Funding sources FDIs - long-term investments into real economy

Portfolio flows – short-term; subject to changes ininvestor sentiment

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 13/47

13

Capacity to Service DebtBalance of Payments

Trade Balance

Exports

• Growth catalyst

• Competitiveness Imports

• Consumption vs Capital

Services Balance

Tourism, Transportation, Interest Payments Capital Account

Direct and Portfolio investment

External Debt

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 14/47

14

Financing Requirements Financing Sources

2000 2001F 2002F 2000 2001F 2002F

Current Account 676 725 670 Capital Account 823 350 500

Amortizations 547 792 806 Direct Investments 1,002 500 600

Multilateral 209 338 319 Portfolio Investments -179 -150 -100

Bilateral 195 278 159 Disbursements 951 1,121 1,080

Private Sector & Other 143 176 328 Multilateral 449 381 450IMF

(3)274 66 150

World Bank (4)

71 150 150

Other 104 165 150

Bilateral 142 120 130

Private Sector & Other(5)

360 620 500

Total 1,223 1,517 1,476 Total 1,774 1,471 1,580

Capacity to Service Debteg. Bulgaria – Estimating Financing Gap/Surplus

Bulgaria Financing Equation (US$ million)(1,2)

Source: Lehman Brothers, Bulgarian National Bank, IMF(1) Assumes no change in reserves, no capital flight and no errors and omissions(2) Excludes short-term debt, which we assume will get rolled over(3) Includes a one year IMF program (US$150 million) in 2002(4) Assumes disbursement of US$150 million in 2002. According to the new CAS drawn up by the

world bank, Bulgaria will receive between US$250 – 750 million between 2002 – 04(5) Includes euro-denominated (300 million) eurobond in 2002

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 15/47

15

Capacity to Service DebtWhat determines the scale of FDIs?

Stable political regime

Natural wealth export potential

Sizable home market

Low labor costs Geographic location/cultural ties

Developed infrastructure

Stable legal/regulatory framework

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 16/47

16

Capacity to Service DebtExternal Debt Profile

Level of external debt

debt/GDP; debt/exports

Debt service ratio

debt service/imports Maturity profile/amortization schedule

ability to refinance

Composition (public/private)

probability of debt restructuring Level of international reserves

i i b

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 17/47

17

Capacity to Service DebtSovereign Credit Ratings

Moody‟s & S&P

Issuer rating = Foreign currency rating

Domestic currency rating

Domestic currency debt typically rated higher for EMG countries Government can print money/raise taxes

Rating differential wider for lower-rated countries

Sovereign ceiling

Government‟s ability to introduce FX & capital controls

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 18/47

18

Bottom Up Analysis

Political analysis

Lehman Brothers analysis

Eurasia Group analysis

• Strong “in-field” contacts • Eurasia‟s approach to political risk analysis is very different

from the traditional “Street” approach

• Scientific rigor, quantitative approach to political science

Mapping of economics (LB) with politics (EG)

Question 2: Willingness to Service Debt?

Willi f S i D b

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 19/47

19

Willingness of Service DebtPolitical Stability

Stable, transparent government

Political continuity

Election years

“Western” orientation Degree of consensus and public support

Presence of domestic/external conflicts

Regional developments/relations with neighbors

Level of integration with the global economy Too big to fail?

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 20/47

20

Bottom Up Analysis

Answers to questions 1 and 2…plus

Technical considerations

Holders of debt

Relative allocation of debt Index considerations

Other considerations

• Buybacks

• Debt restructuring• Issuance/supply

Question 3: Will the Credit Outperform?

Will h C di O f

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 21/47

21

Will the Credit OutperformTechnical Factors

Risk appetite for the asset class

Correlation with the market and the risk of contagion

Type of investors

Inclusion in the index

Short/long positions

New supply/debt exchange

Market and asset liquidity

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 22/47

Investment Outperformance Through

Exposure to Sovereign Markets

I t f th A t Cl

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 23/47

23

Importance of the Asset ClassContagion and Crossover

Current Yield/Total Return Enhancement

Why Invest in Sovereign Markets?

Fi d I A t Cl

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 24/47

24

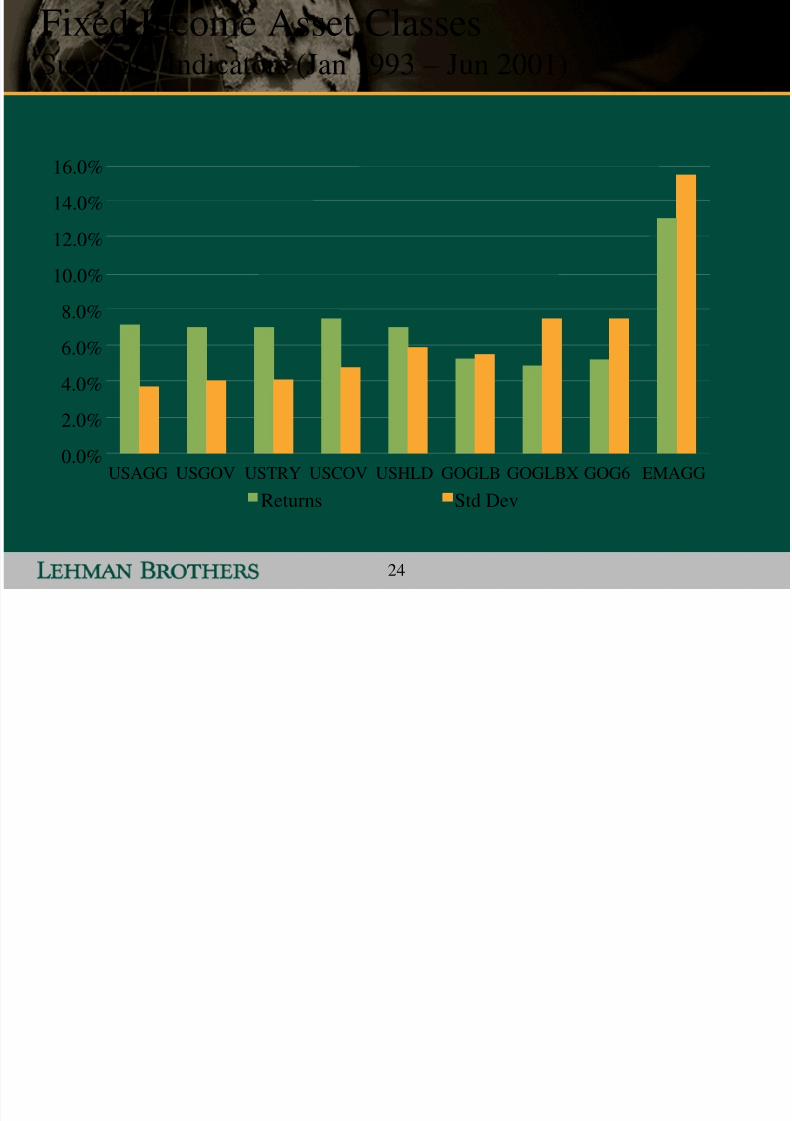

Fixed Income Asset ClassesSummary Indicators (Jan 1993 – Jun 2001)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

USAGG USGOV USTRY USCOV USHLD GOGLB GOGLBX GOG6 EMAGG

Returns Std Dev

I t f th A t Cl

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 25/47

25

Importance of the Asset Class:Contagion and Crossover

Current Yield/Total Return Enhancement

Diversification

Why Invest in Sovereign Markets?

Fi d I A t Cl

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 26/47

26

January 1993 – June 2001

Fixed Income Asset ClassesCross-correlation Matrix

USAGG USGOV USCOR USHLD GOGLB GOG6 EMAGG

USAGG 100%

USGOV 98% 100%

USCOR 97% 93% 100%

USHLD 41% 30% 54% 100%

GOGLB 51% 54% 47% 15% 100%

GOG6 25% 28% 22% 1% 95% 100%

EMAGG 20% 13% 30% 52% -3% -9% 100%

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 27/47

27

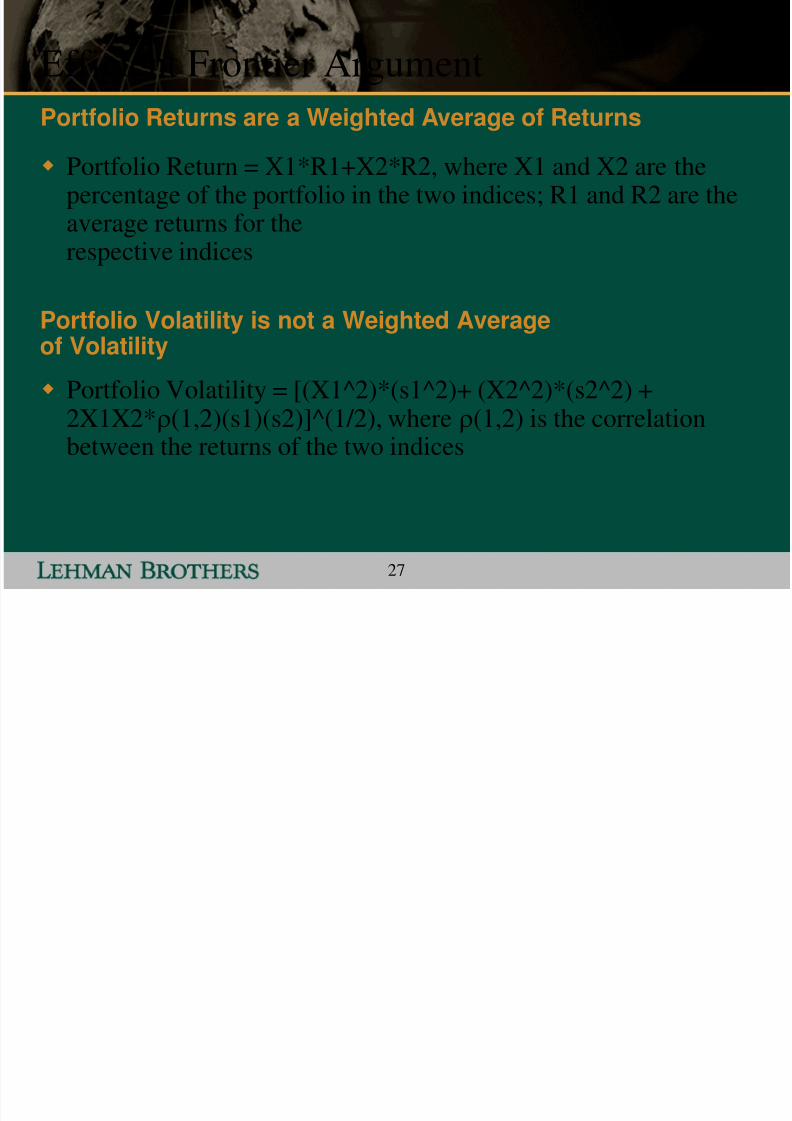

Efficient Frontier Argument

Portfolio Return = X1*R1+X2*R2, where X1 and X2 are thepercentage of the portfolio in the two indices; R1 and R2 are theaverage returns for therespective indices

Portfolio Volatility = [(X1^2)*(s1^2)+ (X2^2)*(s2^2) +

2X1X2*(1,2)(s1)(s2)]^(1/2), where (1,2) is the correlationbetween the returns of the two indices

Portfolio Returns are a Weighted Average of Returns

Portfolio Volatility is not a Weighted Averageof Volatility

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 28/47

28

Efficient Frontier Analysis

Examples

USAGG with EMAGG: = 20%, Limited Benefits

GOG6 with EMAGG: = -9%, Significant Benefits

Correlation Coefficient ()

-1 0 +1

Increasing Benefit

from Diversification

Limited to No Benefit

from Diversification

As a result:

Efficient Frontier Anal sis E amples USAGG

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 29/47

29

Efficient Frontier Analysis Examples USAGG

with EMAGG

Lehman US Aggregate with Lehman EMG Aggregate; Monthly(Jan 1993-Jun 2001)

Efficient Frontier

6%

8%

10%

12%

14%

3% 6% 9% 12% 15% 18%

Annualised Volatility

98% US Aggregate,

2% EMG Aggregate100% US Aggregate

100% EMG Aggregate

Annualised Return

Efficient Frontier Analysis Examples

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 30/47

30

Efficient Frontier Analysis ExamplesGOG6 with EMAGG

Lehman Government Global (G6) with Lehman EMG Aggregate;Monthly (Jan 1993-Jun 2001)

Efficient Frontier

6%

8%

10%

12%

14%

5% 8% 11% 14% 17%

Annualised Volatility

Annualised Return

79% Govt. Global (G6),

21% EMG Aggregate

100% Govt. Global (G6)

100% EMG Aggregate

Importance of the Asset Class

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 31/47

31

Importance of the Asset ClassContagion and Crossover

Current Yield/Total Return Enhancement

Diversification

The Potential Crossover Stories

Why Invest in Sovereign Markets?

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 32/47

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 33/47

33

200

300

400

500

600

700

800

900

1,000

3-Aug-98 17-Nov-98 3-Mar-99 17-Jun-99 2-Oct-99 16-Jan-00 1-May-00

C a s h f l o w Y i e l d M o d e l

S p r e a d ( b p )

United Mexican States 16 United Mexican States 26

200

300

400

500

600

700

800

900

1,000

3-Aug-98 17-Nov-98 3-Mar-99 17-Jun-99 2-Oct-99 16-Jan-00 1-May-00

C a s h f l o w Y i e l d M o d e l

S p r e a d ( b p )

United Mexican States 16 United Mexican States 26

The Crossover Story (Part II)

Mexico – In Anticipation of an Investment Grade Rating

Russian Crisis

2-Feb-00:

Moody‟s changes

outlook to positive

(Ba1/Positive)

7-Mar-00:Moody‟s raises Mexico‟s

rating to Investment

Grade (Baa3)

Importance of the Asset Class

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 34/47

34

Importance of the Asset ClassContagion and Crossover

Current Yield/Total Return Enhancement

Diversification

The Potential Crossover Stories

Convergence Plays

Why Invest in Sovereign Markets?

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 35/47

35

Convergence Virtuous Cycle

Adherence to

Reforms

Improved Credit

Outlook

EU Norms &

Targets Accession Process

on Track

Improved

Ratings

Improved

InvestorSentiment

Increased

Capital Inflows

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 36/47

Applying the Approach

View for 2002

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 37/47

37

Total Return Model Portfolio

Benchmark – LB Emerging Markets Index

Components of the Model Portfolio

EM top down view (regional breakdown)

EM bottom up view (country selection)

Asset selection

• Duration view (based on overall country view)

• US treasury yield curve view (fixed versus floating)

• Collateralized versus non-collateralized

Risk Profile – tracking error analysis Yield curve

Credit spreads

Issuer selection

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 38/47

38

Themes for 2002

5 Themes

High beta countries will outperform in H1‟02

Commodity and oil prices

• Demand factors may dominate – countries that can sustainlow oil prices will outperform

Limited financing requirements

• Watch current account/current account dynamics

Argentina: has it completely decoupled?

Politics – Implication of a war in Iraq and continued conflictin Israel/Palestine

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 39/47

39

Themes for 2002

1. Emerging Markets as a Yield Play

Emerging Markets remain attractive from a yield standpointin H1 „02

• Outlook for EM ex-Argentina still robust (fundamentals strong,

financing requirements limited) Assumption: Global growth conditions remain weak in H1 ‟02; pick up

in H2 ‟02

• Fed bias in Q1 (and probably Q2) towards growth – bias will changeto inflation in Q2 and beyond

• Watch for strong economic data as a precursor to a change in bias Current trade: EM cheap (relative to treasury) begins to get reversed…

• Relative yield differential declines as Fed begins to act on inflation

H1 ‟02: High beta names (Russia, Brazil etc.) do well

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 40/47

40

Themes for 2002

2. Commodity prices: A play on global growth

Oil prices, commodity prices remain soft to low as long globalgrowth remains weak

• LB oil forecast for 2002: $17 p/b

If V-shaped recovery does not play out, oil prices remain soft for alonger period

Russia will be ok – strong reserve build up, stabilization fund,changed geopolitical environment

Venezuela will be more worrisome

• Deteriorating fiscal situation, troubling politics

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 41/47

41

Themes for 2002

3. Financing Requirements Current Account, Capital Account: will it change in 2002? Major EM Countries – Limited gross external financing

requirements Multilateral (especial IMF) flushed with liquidity

Brazil: Net financing requirement $12 billion, of which public sectorwill need at most $6 billion

Russia: Zero financing requirement (even if oil remains atlow levels)

Turkey: Moral Hazard at play Argentina: Covered?….but other more important issues to consider

Relative to available cash, overall financing requirements seemfairly innocuous

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 42/47

42

EMG Bonds

Overall Market (projections for 2002): Total Interests plusPrincipal coming due: $39.6 billion

($ billion)

0.01.0

2.0

3.0

4.0

5.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cash Flow Analysis

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 43/47

43

EMG Bonds

Overall Market Issuance Requirement ($27.8 billion) comparesfavorably to projected redemption ($39.6 billion)

Issuance to Redemption Analysis

Emerging Markets – Cash to Supply Dynamic, 2002 (US$ billion)

2002 Of which:

Financing Requirement (1) US$ €uro(2)

Argentina US$0.0 billion US$0.0 billion US$0.0 billionBrazil US$5.0 billion US$4.0 billion US$1.0 billionMexico US$3.2 billion US$2.5 billion US$0.7 billionRussia US$0.0 billion US$0.0 billion US$0.0 billionTurkey US$4.0 billion US$2.0 billion US$2.0 billionPhilippines US$1.5 billion US$1.5 billion US$0.0 billionOthers US$14.1 billion US$8.9 billion US$5.2 billion

Total Issuance US$27.8 billion US$18.9 billion US$8.9 billionTotal Available Funds US$40.0 billion US$32.0 billion US$8.0 billion

Differential +US$12.2 billion +US$13.1 billion – US$0.9 billion

Source: Lehman Brothers(1) Need to access international capital markets(2) Total available funds on the euro side under-estimate the total cash available. Index definition

used to calculate cash flow

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 44/47

44

Themes for 2002

4. Argentina: has it decoupled completely?

Recent price action suggests market has decoupled from Argentina

• Potentially more downside for Argentina

• Rest of the market: limited contagion fears

• Only exception: Brazil (potential peso devaluation could put

pressure on the real/interest rates/growth debt dynamics)

Buy opportunities for the rest of the Market

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 45/47

45

Themes for 2002

5. Politics

Geopolitical Considerations

• Security remains of paramount importance

• Attack on Iraq?

• Negative for Turkey, Qatar, Egypt etc.• Political implications for Russia and Turkey

• Conflict between Israel and Palestine: broader implication for theregion and global politics?

Domestic Politics

• Elections in Brazil• Venezuela: The Chavez Drama

• Nothing significant in Asia and Europe

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 46/47

46

An Example of Lehman Analysis

Moral Hazard Trade at Play

Debt rollover and domestic financing gap covered

Positive implications for currency, deposit composition and debtdynamics

It is not about the money, it is all about confidence Currency and deposit switch

Debt dynamics

Rollover flexibility

Confidence and investor sentiment will improve only if authoritiesundertake credible and strong implementation of the reform agenda

Will Turkey Outperform in 2002?

7/31/2019 Lehman Brothers Strategy

http://slidepdf.com/reader/full/lehman-brothers-strategy 47/47

An Example of Lehman Analysis

Risks on the Horizon

Challenging economic environment

Challenging global environment

Domestic political risks

A war with Iraq? Are the spreads too tight?

At 200 bps tight to the overall index and 300 bps to Brazil, Turkeyoffers limited near-term upside

Strong performance since beginning of September (has

outperformed regional peers incl.. Russia) Although attractive from a diversification standpoint, near-term out-

performance is conditional on significant and credible progress onthe reform agenda – especially banking sector

Will Turkey Outperform in 2002?

![[Lehman Brothers] Structured Credit Strategy - Annual 2004](https://static.fdocuments.net/doc/165x107/5533a0f15503464f7d8b4973/lehman-brothers-structured-credit-strategy-annual-2004.jpg)