Legislative Budget and Finance...

35

SENATORS ROBERT B. MENSCH Chairman JAMES R. BREWSTER Vice Chairman MICHELE BROOKS THOMAS McGARRIGLE CHRISTINE TARTAGLIONE JOHN N. WOZNIAK REPRESENTATIVES ROBERT W. GODSHALL Secretary VACANT Treasurer STEPHEN E. BARRAR JIM CHRISTIANA SCOTT CONKLIN PETER SCHWEYER JAKE WHEATLEY EXECUTIVE DIRECTOR PHILIP R. DURGIN Impact of Act 2012-207 on Access to Retail Pharmacies and Cost of Prescription Medications Conducted Pursuant to Act 2012-207 April 2015 Legislative Budget and Finance Committee A JOINT COMMITTEE OF THE PENNSYLVANIA GENERAL ASSEMBLY Offices: Room 400 Finance Building, 613 North Street, Harrisburg Mailing Address: P.O. Box 8737, Harrisburg, PA 17105-8737 Tel: (717) 783-1600 • Fax: (717) 787-5487 • Web: http://lbfc.legis.state.pa.us

Transcript of Legislative Budget and Finance...

SENATORS

ROBERT B. MENSCH Chairman JAMES R. BREWSTER Vice Chairman MICHELE BROOKS THOMAS McGARRIGLE CHRISTINE TARTAGLIONE JOHN N. WOZNIAK REPRESENTATIVES

ROBERT W. GODSHALL Secretary VACANT Treasurer STEPHEN E. BARRAR JIM CHRISTIANA SCOTT CONKLIN PETER SCHWEYER JAKE WHEATLEY EXECUTIVE DIRECTOR

PHILIP R. DURGIN

Impact of Act 2012-207 on Access to Retail Pharmacies and Cost of Prescription Medications

Conducted Pursuant to Act 2012-207

April 2015

Legislative Budget and Finance Committee

A JOINT COMMITTEE OF THE PENNSYLVANIA GENERAL ASSEMBLY Offices: Room 400 Finance Building, 613 North Street, Harrisburg

Mailing Address: P.O. Box 8737, Harrisburg, PA 17105-8737 Tel: (717) 783-1600 • Fax: (717) 787-5487 • Web: http://lbfc.legis.state.pa.us

i

Table of Contents

Page

Summary and Conclusions ............................................................... S-1

I. Introduction ........................................................................................ 1

II. Findings .............................................................................................. 3

A. Eight States, Including Pennsylvania, Have Attempted to Limit Required Use of Mail Order Pharmacies. ............................................... 3

B. The Pennsylvania Insurance Department Has Received Relatively Few Complaints Concerning Act 2012-207 ............................................ 7

C. Half of the Retail Pharmacies Applying to Offer Act 207 Dispensing Were Not Approved or Elected to Withdraw Their Applications .............. 11

III. Appendices ......................................................................................... 23

A. Act 2012-207 .......................................................................................... 24

B. Act 2012-207’s Impact on Access to and Cost of Prescription Drugs Questionnaire for Pennsylvania Retail (Independent and Chain) Pharmacies ............................................................................................. 26

S-1

Summary and Conclusions

In 2012, the Pennsylvania General Assembly enacted Act 2012-207 prohibit-ing state-licensed health insurance plans from requiring their consumers to obtain prescription medications through mail order pharmacies. Act 207 was enacted in an effort to provide greater consumer access to retail pharmacies and a “level play-ing field” between mail order and retail pharmacies. To accomplish such goals, it required state-licensed health insurers that offer a prescription drug benefit to pro-vide such benefits with copayments and coinsurance that are the same for mail or-der and retail pharmacies if the retail pharmacy agrees to the same terms and con-ditions that are in place for the plan’s mail order pharmacy.

The act also directed the Legislative Budget and Finance Committee

(LB&FC) to evaluate the impact of this program on access to prescription drugs at independent and chain retail pharmacies and to evaluate whether its provisions had a material impact on the cost of prescription medications for consumers and health care plans. The act required the LB&FC to commence the evaluation by September 2014 (i.e., 18 months after the effective date of the act1) and issue a re-port nine months after commencing the evaluation.

We found:

Pennsylvania is one of eight states that have attempted to limit required

use of mail order pharmacies, according to the National Community Pharmacists Association. Such laws are applicable to state-licensed in-surers in five states (Connecticut, Hawaii, Maryland, New York, and Pennsylvania); employers in two states (Arkansas and Louisiana) and cer-tain state benefit plans in one state (Texas). Four (Hawaii, New York, Pennsylvania, and Texas) states require that

consumer copayments or coinsurance be comparable for mail order and retail pharmacies and that the retail pharmacy agrees to the same terms and conditions as those established for the mail order pharmacy.

Representatives of state pharmacy associations in Connecticut and New York with whom we spoke indicate their state laws have had minimum impact because of their limited applicability. As in Pennsyl-vania, their laws apply to state licensed health insurers, but not “health coverage” benefits available through self-insured trusts, legally permitted employer welfare arrangements, and federal Medicare and Medicaid programs, which are governed under various federal laws.

1 The Act was approved November 1, 2012, and took effect 120 days after (March 2013).

S-2

Nationwide, 61 percent of covered workers in private, public, and pri-vate not-for-profit firms that receive health care through their employ-ers receive coverage through such plans, according to the Kaiser Fam-ily Foundation and Health Research and Educational Trust, Employer Health Benefits, 2013 Annual Survey.

The Pennsylvania Insurance Department has received relatively few

consumer complaints (i.e., 36) since the Act was implemented in March 2013, and notes there is considerable misunderstanding of the Act and the role of the Department. In many instances, according to PDI, the complaints were not covered by Act 207 since:

The filer of the complaint was enrolled in a plan not covered by Act 207. For example, consumers asked if Medicare was covered by the act, or if the law applied to self-funded plans. In other cases, the retail pharmacy reported that it could not meet the conditions or pricing offered by the mail order pharmacy, and thus Act 207 would not apply in those instances….

The limited volume of complaints may also be due to the absence of wide-

spread participation in the Act 207 program. One major health plan reported that six months after the Act’s initial implementation date “… no retail pharmacy has expressed interest in nor executed a contract…[with the insurer’s pharmacy benefit manager] to participate as a mail service pharmacy.” Another advised a consumer one year after the Act’s implementation that no pharmacy in Pennsylvania had ac-cepted the contract for 90-day dispensing at retail under the same price, terms, and conditions as mail order. As of late 2014, at least two major health insurers advised LB&FC staff that they had not received completed applications from retail pharma-cies seeking to participate under Act 207.

To assess the impact of Act 2012-207 on access to retail pharmacies and the cost of prescription medications, we provided an opportunity for retail pharmacies2 to share their experiences with the implementation of the Act. We obtained such in-put through a web-based survey conducted in August and September 2014 with the support of the Pennsylvania Pharmacists Association and the Pennsylvania Associ-ation of Chain Drug Stores. Our survey3 found:

Three-quarters (101 of 132) of our survey respondents, including all chain pharmacy respondents, applied to insurers and pharmacy benefit

2 As of November 2013, the Pennsylvania Department of State licensed over 3,300 pharmacies. Such licenses include retail pharmacies, along with hospital, long-term care, and specialty pharmacies. Based on the availa-ble state licensure data, it is not possible to determine the exact number of independent and chain retail phar-macies in Pennsylvania. 3 We received 132 survey responses, including five responses from chain pharmacies that reported operating over 920 pharmacies in Pennsylvania.

S-3

managers to offer medication dispensing under Act 207; but only about half (55 of 101) of those that applied were approved or chose to offer dispensing under Act 207. Typically those not approved reported they did not meet the insurer’s mail order pharmacy network requirements. Several, however, reported withdrawing their applications after becoming familiar with the insurer or the insurer’s benefit manager’s requirements for Act 207 dispensing.

Just over half of those participating in Act 207 dispensing, including two chain pharmacy respondents, think consumer out-of-pocket costs have remained the same or decreased. In contrast, only 20 percent of those not participating in Act 207 thought consumer out-of-pocket costs have remained the same or decreased after the passage of Act 207. LB&FC staff also asked major insurers if they had incurred material costs with the implementation of Act 207. None of the major insurers reported that they had incurred such costs. One noted that costs associated with implementation typically involve the provider credentialing process, which is in place and would occur with or without Act 207.

Over 80 percent of those providing Act 207 dispensing planned to con-tinue such dispensing, including the approved chain respondents.4 The primary reasons offered by the six respondents who indicated they would not continue are the failure of the program to cover the pharmacy’s drug acquisition and drug dispensing costs.

For the most part, independent pharmacists expressed disappointment with the implementation of the Act in view of its original legislative in-tent to encourage consumer choice. Pharmacists responding to our sur-vey typically indicated that the Act, while well intentioned, was ignored, “lacked teeth,” or was not enforced.

One independent pharmacist involved in the drafting of the initial versions of

the Act and the compromises that were reached to obtain its passage advised us:

Unfortunately…health insurers, government programs and pharmacy benefit managers have taken advantage of the legislation’s failure to more clearly address a number of issues by interpreting the revised legislation in a manner that prevented it from having any appreciable impact on the availability of retail pharmacy services to Pennsylvania consumers.

4 One of our chain pharmacy survey respondents dispensed 90-day supplies of medication prior to Act 207 and planned to continue such dispensing after Act 207 was implemented. The pharmacy applied but subsequently decided it would not provide such dispensing under Act 207’s terms and conditions.

S-4

Specific factors associated with such an outcome, according to the independent pharmacist, include, for example:

Requirements that pharmacies already enrolled in the insurer’s pro-vider network be approved for admittance into new provider networks to participate in Act 207.

Discriminatory requirements for admission into provider networks

that either effectively block participation by retail pharmacies or make their participation in networks unreasonably burdensome.

The general refusal of pharmacy benefit managers affiliated with mail

order pharmacies to include payments received from insurers and drug manufacturers in amounts paid to retail pharmacies.

The lack of effective efforts by the Pennsylvania Insurance Department

to enforce the law in a manner consistent with the legislative intent.

The absence of widespread implementation of Act 207 provides little oppor-tunity to fully assess the impact of the act, either positively or negatively on the cost of medication services. There is, however, no evidence thus far that it has imposed material costs on insurers or consumers.

Throughout our work to evaluate the impact of Act 207, we received several

suggestions as to how to improve the implementation of Act 207. Some independent pharmacists see the need for analysis of the legality of the tactics and strategies of pharmacy benefit managers and insurers, and possibly amendments to the act. Others are concerned about the ability of the act to realize its goals given the many health benefits that are provided through coverage outside of the scope of the state’s regulatory authority. A chain pharmacy representative suggested that the number of pharmacies participating in Act 207 might be increased if insurers and pharmacy benefit managers offered community pharmacies “a reasonable rate that would not result in the community pharmacy losing money filing prescriptions” and if the scope of the act could be expanded to include the federally authorized health cover-age plans. The Insurance Department suggests that it be involved initially and throughout any process to revise the Act in view of the complexity of health insur-ance laws at the state and federal levels.

1

I. Introduction Act 2012-207 (Appendix A) directed the Legislative Budget and Finance Com-mittee (LB&FC) to evaluate the impact of its provisions on access to prescription drugs at independent and chain retail pharmacies and whether its provisions had a material positive or negative impact on the cost of prescription medications for con-sumers and health care plans. It further directed the LB&FC commence the evalu-ation by September 2014 (i.e., 18 months after the effective date of the Act1) and is-sue a report nine months after commencing the evaluation.

Act 207 was intended to prohibit health insurance plans providing prescrip-tion medications from requiring that such drugs be obtained only through mail or-der pharmacies. For this to occur, participating retail pharmacies had to be willing to accept insurer and pharmacy benefit manager pricing, terms, conditions, and other requirements associated with mail order prescriptions.

Study Scope and Objectives Specifically, this study seeks to:

1. Identify the extent to which Act 207 has been implemented, and any chal-lenges associated with its implementation.

2. Determine the added costs or savings, if any, for prescription drugs expe-rienced by consumers and health plans as a result of Act 207’s consumer choice provision.

3. Assess the extent to which Pennsylvania’s experience compares to other states that provide for consumer choice when filling prescriptions.

To identify the extent to which Act 207 has been implemented and challenges associated with its implementation, we spoke with representatives of independent community and chain retail pharmacies. With the assistance of the Pennsylvania Pharmacists Association and the Pennsylvania Association of Chain Drug Stores, we made a web-based survey available to their members in August and September 2014 to provide them with an opportunity to share their experiences with the act. Appendix B provides a copy of the LB&FC’s questionnaire for Pennsylvania retail (independent and chain) pharmacies. We met with Pennsylvania Insurance Department officials involved with the implementation of Act 207, and reviewed materials prepared by the Pennsylvania Pharmacists Association with input from the Pennsylvania Insurance Department concerning the Act’s implementation. We also spoke with and reviewed materials 1 The act was approved November 1, 2012, and took effect 120 days after (March 2013).

2

prepared by independent pharmacy consultants identifying specific problems and concerns associated with Act 207’s implementation. To determine the added costs or savings, if any, for prescription drugs experi-enced by consumers we asked pharmacies responding to our survey and participat-ing in Act 207 dispensing about such costs and savings. We also spoke with key in-surers to identify any material added costs they may have encountered as a result of Act 207’s implementation. Four major insurers responded to our request, with all four noting they had not incurred material added costs as a result of Act 207. Two of the four major insurers also noted they had not received any completed applica-tions from pharmacies seeking to provide Act 207 dispensing. To assess the extent to which Pennsylvania’s experience compares with other states that have legislation prohibiting insurers from adopting mandatory mail or-der pharmacy benefit requirements, we reviewed legislation adopted in states with such requirements. In particular, we considered the types of restrictions imposed, those required to comply, and how such laws were enforced. We also spoke with state pharmacy associations and officials involved in implementing “mandatory mail order” legislation in their states about their experiences following the adoption of state legislation.

Acknowledgements LB&FC staff completed this study with consultation and assistance from the Pennsylvania Pharmacists Association and the Pennsylvania Association of Chain Drug Stores. We thank the Pennsylvania Insurance Department and its staff for their valuable assistance throughout the study. In particular, we thank Arthur McNulty, Deputy Insurance Commissioner for Market Regulation; Carmen DiCello, R.Ph., the Director of Government and Public Affairs for the Value Drug Company; Patricia Epple, CAE, CEO of the Pennsylvania Pharmacists Association; and Drew Lyons, who represents the Pennsylvania Association of Chain Drug Stores.

Important Note

This report was developed by Legislative Budget and Finance Committee staff. The release of this report should not be construed as indicating that the Committee members endorse all the report’s findings and recommendations. Any questions or comments regarding the contents of this report should be di-rected to Philip R. Durgin, Executive Director, Legislative Budget and Finance Com-mittee, P.O. Box 8737, Harrisburg, Pennsylvania 17105-8737.

3

II. Findings

A. Eight States, Including Pennsylvania, Have Attempted to Limit Required Use of Mail Order Pharmacies

Eight states (Arkansas, Connecticut, Hawaii, Louisiana, Maryland, New York, Pennsylvania, and Texas) have enacted legislation intended to limit the re-quired use of mail order pharmacies, according to the National Community Phar-macists Association. Such legislation is enacted to allow consumers the choice of ob-taining prescription drugs from a community retail pharmacy or a mail order phar-macy.

The eight states, however, differ in who they require to comply, the nature of the limitations and restrictions, and provisions for penalties and enforcement. In most ways, Pennsylvania’s law is similar to those of other states; however, it has certain unique features not found in most state laws.

Limitations on Use of Mail Order Pharmacies

Who Must Comply: Typically, state laws prohibiting required use of mail or-der pharmacies are applicable to state-licensed health insurers that provide pre-scription drug coverage. As shown in Exhibit 1, five (Connecticut, Hawaii, Mary-land, New York, and Pennsylvania) of the eight states, including Pennsylvania, place limits on state licensed insurers’ use of mail order pharmacies.

In addition to covering state-licensed health insurers, Exhibit 1 shows Penn-sylvania’s legislative restrictions apply to certain state programs. Such programs include the Pharmacy Assistance Program for the Elderly (PACE), which has al-ways had the same copayment for retail and mail order pharmacies in its program.1 Pennsylvania’s legislation also explicitly states its limitations apply only to the ex-tent they are not preempted by federal law.

Two (Arkansas and Louisiana) of the eight states impose limitations on em-ployers rather than insurers. One (Texas) of the eight states limits its mail order restrictions to health benefit plans administered by the State Employee Retirement System and the State Teacher Retirement System.

Restrictions: Typically, state laws limiting use of mail order pharmacies in-clude all mail order pharmacies. One (Arkansas) of the eight states, however, ap-plies its prohibitions only to out-of-state mail order pharmacies.

As shown in Exhibit 1, states typically require that copayments and coinsur-ance2 for prescription drugs be equivalent for mail order and retail pharmacies.

1 Only 1.3 percent of PACE’s total claims are for mail order dispensing. 2 Copayments, or “copays” are a form of consumer out-of-pocket cost sharing that requires the consumer to pay a fixed dollar amount for the medical service provided. Coinsurance is also a form of consumer out-of-pocket cost sharing. It requires the consumer to pay a percentage of the cost of the medical service provided.

Exh

ibit

1

Sta

tes

Wit

h L

egis

lati

on

Lim

itin

g R

equ

ired

Use

of

Mai

l Ord

er P

har

mac

y

Sta

te

Wh

o M

ust

Co

mp

ly

Res

tric

tio

ns

Co

pay

men

t, C

oin

sura

nce

,or

Oth

er F

ees

Sp

ecif

ical

ly Id

enti

fied

Exc

lusi

on

s E

nfo

rcem

ent

and

Pen

alti

es

Ark

ansa

s E

mpl

oyer

s pr

ovid

ing

pre-

scrip

tion

drug

cov

erag

e P

rohi

bits

em

ploy

ers

from

req

uirin

g th

e us

e of

an

out-

of-s

tate

mai

l ord

er p

har-

mac

y.

Cop

aym

ent a

nd o

ther

ret

ail p

har-

mac

y pr

escr

iptio

n co

nditi

ons

mus

t be

the

sam

e as

thos

e fo

r m

ail o

r-de

r ph

arm

acy.

Em

ploy

ers

who

allo

w e

mpl

oyee

s to

ch

oose

whe

re th

ey h

ave

thei

r pr

escr

ip-

tions

fille

d.

Yes

, vio

lato

rs

ma

y be

fine

d be

-tw

een

$100

and

$1

,000

. C

onne

cti-

cut

Hea

lth in

sura

nce

polic

ies

issu

ed b

y ho

spita

l and

m

edic

al s

ervi

ce c

orpo

ra-

tions

, (su

ch a

s B

lue

Cro

ss

and

Blu

e S

hiel

d) a

nd

heal

th c

are

cent

ers

Insu

red

bene

ficia

ries

cann

ot b

e re

-qu

ired

to u

se a

mai

l ord

er p

harm

acy.

N

ot s

peci

fied

N

one

spec

ified

N

one

spec

ified

Haw

aii

Pre

scrip

tion

drug

and

he

alth

ben

efit

plan

s, m

utua

l be

nefit

soc

ietie

s, p

harm

acy

bene

fit m

anag

ers

Ret

ail p

harm

acie

s w

hich

acc

ept p

har-

mac

y be

nefit

man

ager

(P

BM

) te

rms

and

cond

ition

s m

ust b

e al

low

ed to

par

-tic

ipat

e in

the

PB

M’s

net

wor

k.

Cop

aym

ent a

nd o

ther

ret

ail p

har-

mac

y pr

escr

iptio

n co

nditi

ons

mus

t be

the

sam

e as

thos

e fo

r m

ail o

r-de

r ph

arm

acy.

Com

mun

ity r

eta

il ph

arm

acie

s de

sig-

nate

d as

rur

al p

harm

acie

s pu

rsua

nt to

fe

dera

l law

Yes

, vio

lato

rs

ma

y be

ass

esse

d a

fine

up to

$1

0,00

0 an

d be

re

quire

d to

take

co

rrec

tive

actio

n.

Loui

sian

a E

mpl

oyer

s pr

ovid

ing

pre-

scrip

tion

drug

cov

erag

e P

rohi

bits

em

ploy

ers

from

req

uirin

g us

e of

mai

l ord

er p

harm

acy.

C

opay

men

t and

oth

er r

etai

l pha

r-m

acy

pres

crip

tion

cond

ition

s m

ust

be th

e sa

me

as th

ose

for

mai

l or-

der

phar

mac

y.

Exc

lude

s al

l em

ploy

ers

who

sh

ow t

hat

thei

r he

alth

ben

efits

are

not

reg

ulat

ed

by

the

sta

te.

Yes

, vio

lato

rs

ma

y be

fine

d up

to

$50

0.

Mar

ylan

d In

sure

rs, n

onpr

ofit

heal

th

serv

ice

plan

s, H

MO

s P

olic

ies

and

cont

ract

s m

ay

not

esta

b-lis

h th

e am

ount

of r

eim

burs

emen

t for

a

phar

mac

eutic

al p

rodu

ct to

the

insu

red

base

d on

who

the

auth

oriz

ed p

re-

scrib

er is

.

Cop

aym

ent a

nd o

ther

ret

ail p

har-

mac

y pr

escr

iptio

n co

nditi

ons

mus

t be

the

sam

e as

thos

e fo

r m

ail o

r-de

r ph

arm

acy.

Hea

lth s

ervi

ces

prov

ided

by

plan

s or

co

ntra

cts

issu

ed to

an

empl

oye

r un

der

a co

llect

ive

barg

aini

ng a

gree

men

t.

Non

e sp

ecifi

ed

New

Yor

k H

ealth

insu

ranc

e co

mpa

-ni

es, h

ealth

ser

vice

s an

d ho

spita

l cor

pora

tions

, med

-ic

al e

xpen

se in

dem

nity

cor

-po

ratio

ns

Pol

icie

s m

ust a

llow

insu

red

to o

btai

n pr

escr

iptio

n dr

ugs

from

eith

er r

etai

l or

mai

l ord

er p

harm

acy

if th

e re

tail

phar

-m

acy

acce

pts

the

sam

e te

rms

and

cond

ition

s as

mai

l ord

er p

harm

acie

s.

Cop

aym

ent a

nd o

ther

ret

ail p

har-

mac

y pr

escr

iptio

n co

nditi

ons

mus

t be

the

sam

e as

thos

e fo

r m

ail o

r-de

r ph

arm

acy

if un

der

the

sam

e pr

ogra

m, p

olic

y, o

r co

ntra

ct.

Exc

lude

s a

colle

ctiv

e ba

rgai

ning

ag

reem

ent b

etw

een

an e

mpl

oye

r an

d a

reco

gniz

ed o

r ce

rtifi

ed e

mpl

oyee

or-

gani

zatio

n.

Non

e sp

ecifi

ed

Pen

nsyl

-va

nia

Sta

te li

cens

ed in

sure

rs, t

he

stat

e M

edic

aid

prog

ram

, th

e st

ate

Chi

ldre

n’s

Hea

lth

Insu

ranc

e P

rogr

am, a

nd

the

Pha

rmac

eutic

al A

ssis

-ta

nce

Pro

gram

for

the

El-

derly

Pol

icie

s an

d pr

ogra

ms

mus

t allo

w in

-su

red

and

part

icip

ants

to o

btai

n pr

e-sc

riptio

n dr

ugs

from

eith

er r

etai

l or

mai

l or

der

phar

mac

y if

the

reta

il ph

arm

acy

acce

pts

the

sam

e te

rms

and

cond

ition

s as

mai

l ord

er p

harm

acie

s.

Cop

aym

ents

and

oth

er r

etai

l pha

r-m

acy

pres

crip

tion

cond

ition

s m

ust

be th

e sa

me

for

com

mun

ity r

eta

il ph

arm

acie

s an

d m

ail o

rder

pha

r-m

acie

s.

Spe

cific

ally

exc

lude

s ac

cide

nt o

nly,

fix

ed in

dem

nity

, lim

ited

bene

fit, c

redi

t, de

ntal

, vis

ion,

spe

cifie

d di

seas

e, M

edi-

care

sup

plem

ent,

Civ

ilian

Hea

lth a

nd

Med

ical

Pro

gram

of t

he U

nifo

rm S

er-

vice

s (C

HA

MP

US

) su

pple

men

t, lo

ng-

term

car

e or

dis

abili

ty in

com

e, w

orke

rs’

com

pens

atio

n or

aut

omob

ile m

edic

al

paym

ent i

nsur

ance

.

Non

e sp

ecifi

ed

Tex

as

Hea

lth b

enef

it pl

ans

adm

in-

iste

red

by th

e S

tate

T

each

er R

etire

men

t and

th

e S

tate

Em

ploy

ee R

etire

-m

ent S

yste

ms

Pro

hibi

ts r

equi

ring

grou

p be

nefit

par

tic-

ipan

ts to

pur

chas

e pr

escr

iptio

n dr

ug

bene

fits

thro

ugh

a m

ail o

rder

pro

gram

an

d re

quire

s pl

ans

to a

llow

a p

artic

i-pa

nt to

obt

ain

a m

ultip

le-m

onth

sup

ply

of d

rugs

from

eith

er a

ret

ail o

r m

ail o

r-de

r ph

arm

acy

if th

e re

tail

phar

mac

y ag

rees

to th

e sa

me

term

s as

a m

ail o

r-de

r ph

arm

acy.

Cop

aym

ents

, ded

uctib

les,

coi

nsur

-an

ce a

nd o

ther

cos

t-sh

arin

g ob

li-ga

tions

mus

t be

the

sam

e fo

r co

m-

mun

ity r

etai

l pha

rmac

ies

and

mai

l or

der

phar

mac

ies.

Hea

lth b

enef

it pl

ans

othe

r th

an th

ose

adm

inis

tere

d by

the

Sta

te T

each

er R

e-tir

emen

t and

the

Sta

te E

mpl

oyee

Re-

tirem

ent S

yste

ms

Non

e sp

ecifi

ed

Sou

rce:

Dev

elop

ed

by

LB&

FC

sta

ff ba

sed

on

revi

ew

of p

ertin

ent s

tate

legi

slat

ion.

4

5

Seven states (Arkansas, Hawaii, Louisiana, Maryland, New York, Pennsylvania, and Texas) include such provisions in their laws. Only one state (Connecticut) does not.

Four (Hawaii, New York, Pennsylvania, and Texas) of those seven states, in-cluding Pennsylvania, require copayment/coinsurance comparability between retail and mail order pharmacies if the retail pharmacy agrees to the same terms and con-ditions as those established by the health insurer for the mail order pharmacy. Spe-cially, Pennsylvania’s law requires that copayment/coinsurance comparability:

shall apply only if the retail pharmacy is willing to accept from the in-surer the same pricing, terms, conditions or requirements related to the cost of the prescriptions and the cost and quality of dispensing pre-scriptions that the insurer has established for a mail-order pharmacy and any of such pharmacy’s affiliates, including any affiliated phar-macy benefit manager, pursuant to the health insurance policy.3

Exclusions: Most of the states explicitly specify parties not covered by their

state law. Three (Louisiana, Maryland, and New York) of the eight states, for ex-ample, specify that certain employer-based plans are not covered. Pennsylvania also lists insurers that are covered under the state’s insurance law,4 but are not cov-ered by Act 2012-207’s limitations concerning pharmacy mail order. As discussed in Finding B, however, there are important forms of health coverage available in Pennsylvania that are not governed by the state’s insurance law, and therefore not affected by Act 207’s provisions.

Enforcement: Most states, including Pennsylvania, do not include penalties

or enforcement provisions in their statutes. Three states (Arkansas, Hawaii, and Louisiana), however, do. In Arkansas, any person or entity violating its state law provisions is guilty of a misdemeanor and upon conviction can be fined between $100 to $1,000. In Hawaii, the Insurance Commissioner may assess a fine of up to $10,000 for each violation by a pharmacy benefit manager or prescription drug ben-efit plan provider. The statute further allows the Insurance Commissioner to order pharmacy benefit managers to take specific affirmative corrective action or make restitution.5 In Louisiana, a person convicted of violating the provisions of the act can be fined up to $500.

LB&FC staff spoke with representatives of the state pharmacy associations

in New York and Connecticut. Connecticut’s legislation has been in place since

3 40 P.S. §764l(b). 4 40 P.S. §764l(d)(2)(iii). 5 By March 31st of each year entities affected by Hawaii’s law must file with the Insurance Commissioner a re-port for the preceding year stating they are in compliance with the law. The report is intended to fully disclose the amount, terms and conditions relating to copayments reimbursement options, and other payments associ-ated with the drug benefit plan.

6

1989, and New York’s since 2011. Representatives of both state associations indi-cated their state legislation had minimal impact in preventing mail order only re-quirements because of its limited applicability. Specifically, both state associations noted their legislation did not apply to various employer-based plans that are not subject to state insurance regulation. New York also noted that its statute was inef-fective because it did not specifically identify the “terms and conditions” that are and are not permitted under the program.

7

B. The Pennsylvania Insurance Department Has Received Relatively Few Complaints Concerning Act 2012-207

The Pennsylvania Insurance Department is responsible for investigating complaints from consumers concerning unfair insurance practices, including unfair practices of health insurers. Its Office of Consumer Services also responds to in-quiries that are brought to its attention. Based on information provided by the In-surance Department and the Pennsylvania Pharmacists Association, the Depart-ment of Insurance has received relatively few complaints and inquiries from either consumers or others concerning Act 207. Act 207 Complaints Filed With the PA Insurance Department From March 2013 through mid-November 2014, the Department received:

36 consumer complaints and

9 inquires. The Department investigated each complaint and inquiry, and as appropriate re-sponded to the request. According to the Department:

In many instances, the complaint was not covered by Act 207 since the filer of the complaint was enrolled in a plan not covered by Act 207. For example, consumers asked if Medicare was covered by the act, or if the law applied to self-funded plans. In other cases, the retail phar-macy reported that it could not meet the conditions or pricing offered by the mail order pharmacy, and thus Act 207 would not apply in those instances as well.

The Department advised LB&FC staff that certain health “coverage” is outside of the scope of Act 207. According to Department legal staff:

…With regard to situations where Act 207 does not apply, some con-cern has been expressed as to how Act 207 defines ‘insurer,’ which in turn references ‘health insurance policy.’ Both definitions are critical in determining what situations trigger application of the act. Notably, this is a standard approach in legislation enacted by the General As-sembly: use of exact definitions of ‘health insurance policy’ and ‘in-surer’ can be found in a number of laws, and in essence, clarifies that those laws only apply to policies of insurance issued by licensed com-mercial companies and the four Blue plans. In other words Act 207—like many laws—would not apply to many situations where a person, erroneously believing they have insurance, might conclude that it does apply. That is because coverage through a variety of sources such as

8

self-insured trusts, legally permitted employer welfare arrangements,1 Medicare and Medicaid, is not insurance, but rather coverage subject to one of several laws. Those federal laws preempt state regulations, so it would be superfluous for the legislation to have included them in Act 207’s definitions….

To protect consumer confidential information, the Department did not pro-vide us with a list identifying each complaint and its disposition. From other sources, however, we obtained copies of letters sent in response to complainants. Such letters confirm the Department’s overall characterization of the complaints it received. Exhibit 2 provides a few examples of responses provided by the Pennsyl-vania Insurance Department.

The complaint information we reviewed, as well as information provided by

major health insurers, further confirms the results of our survey (see Finding C) that there is not widespread participation of retail pharmacies in Act 207 dispens-ing. One major health plan noted six months after the Act’s initial implementation date that “to date, no retail pharmacy has expressed interest in nor executed a con-tract…[with the insurer’s pharmacy benefit manager] to participate as a mail ser-vice pharmacy.” Another advised a consumer one year after the Act’s implementa-tion that no pharmacy in Pennsylvania had accepted the contract for 90-day dis-pensing at retail under the same price, terms, and conditions as mail order. As of late 2014, moreover, at least two major health insurers advised LB&FC staff that they had not received completed applications from retail pharmacies seeking to par-ticipate under Act 207.

As shown in Exhibit 2, some of those filing complaints with the Insurance De-

partment did not have a clear understanding of the Act and its coverage. Some of those filing complaints, for example, incorrectly thought that Act 207 provided for “Any Willing Provider” legislation, i.e., any interested pharmacy could become part of a plan or pharmacy benefit network’s provider network. Others, inaccurately un-derstood Act 207 to permit them to operate a “specialty” pharmacy without meeting the plan’s unique credentialing requirements for such pharmacies.

Several of the practices of concern to those considering or filing complaints

are practices that are allowed in the federal Medicare Part D prescription drug pro-gram. As the Insurance Department noted above, however, the Medicare Part D

1 Nationwide 61 percent of covered workers in private, public, and private not-for-profit firms that receive health care through their employers receive coverage through such plans, according to the Kaiser Family Foun-dation and Health Research and Educational Trust, Employer Health Benefits, 2013 Annual Survey.

9

Exhibit 2

Examples of Pennsylvania Insurance Department Responses to Consumer Act 207 Complaints

Example 1:

Thank you for contacting the Pennsylvania Insurance Department with your concern. Act 207, also known as SB 201, is a newly enacted Pennsylvania law that prohibits a Pennsylvania health insurance policy or government program providing prescription ben-efits from charging an individual using a retail pharmacy a copayment, deductible fee, limitation or other condition or requirement not otherwise imposed on the covered indi-vidual using a mail order pharmacy. The individual cost similarity created by the Act, however, only applies if the retail phar-macy is willing to accept from the insurer the same pricing, terms, conditions or require-ments related to the cost of the prescription and the cost and quality of dispensing pre-scriptions that the insurer has established for a mail order pharmacy and its affiliates. Act 207 does not provide guidance on how the insurer and/or its prescription benefit manager will reach this agreement with the retail pharmacist. The Pennsylvania Insurance Department has worked closely with the Pennsylvania Pharmacists Association on this legislation. Please copy and paste the below URL into your browser to learn additional information about Act 207, compliance with the Act, and Act 207 complaints with the Pennsylvania Insurance Department. http://www.papharmacists.com/diplaycommon.cfm?an=18subarticlenbr=35

Thank you for providing this opportunity to respond. Please do not hesitate in contacting me with your additional concerns.

Example 2:

Thank you for writing our Department to share your concerns about…denial of your re-quest to become a network provider. I do understand your concern over this situation. At present time, Pennsylvania has not enacted an ‘Any Willing Provider’ law, which would require an insurance company to ac-cept all medical providers wishing to participate with that company. The Pennsylvania Insurance Department does not have jurisdiction over the contractual relationship between a medical provider and an insurance company. This is a business relationship and either party can elect not to enter into this relationship. Please understand that Act 207 does not [emphasis in the original] require insurers to accept any retail pharmacy into their network. I regret that I am unable to provide you with any relief in this unfortunate situation. You may want to discuss your concerns with your State Senator and Representative to deter-mine if Legislation should be introduced to address this problem….

Source: Developed by LB&FC staff.

10

program is not subject to Act 207. The Medicare Part D program, for example, re-quires plan sponsors to form pharmacy networks with participating pharmacies, and such pharmacies must agree to meet all of the sponsor’s standard terms and conditions. Medicare, moreover, requires plan sponsors to include in their networks any pharmacy willing to accept their standard contracting terms and conditions. It, however, allows plans to vary their terms and conditions for different types of phar-macies as long as the same standards and conditions apply to all pharmacies within a given pharmacy type. As a result, Medicare Part D plan sponsors have separate and differing standards and conditions for mail and retail pharmacies.

Like Act 207, Medicare Part D calls for “a level playing field” between mail-

order and retail pharmacies. When a plan sponsor includes a mail order pharmacy that provides extended supplies (e.g., a 90-day supply) of covered drugs within its network, Medicare Part D plans must allow network retail pharmacies to offer ex-tended day supplies of medications. Medicare, however, permits plan sponsors to require consumers who elect to use a retail pharmacy for extended day supplies of medications to pay any additional costs associated with such dispensing.

Given the complexities of health benefit coverage and prescription medication

benefits across the various types of health coverage and health programs, it is not surprising that the Pennsylvania Insurance Department staff have concluded that there is misunderstanding about Act 207. This misunderstanding exists among both consumers and the industry, according to the Department.

11

C. Half of the Retail Pharmacies Applying to Offer Act 207 Dispensing Were Not Approved or Elected to Withdraw Their Applications

In 2013, nationwide, according to Drug Channels:1

mail order pharmacies accounted for 15.2 percent of the number of pre-scriptions dispensed through retail channels,

independent pharmacies 17.2 percent, chain stores 55.2 percent, and supermarkets with pharmacies 12.5 percent.

Mail order pharmacies routinely offer extended medication dispensing (i.e., 90-day medication supplies). Retail pharmacies can also provide such dispensing. The cost to the consumer, however, may be greater at the retail pharmacy if the consumer’s drug benefit plan has a higher retail pharmacy copayment or coinsurance than the mail order pharmacy for the same medication. For example, if the consumer’s drug plan has a $10 copayment for a 90-day supply of medication from the plan’s mail or-der pharmacy and the consumer has a $30 dollar copayment for the same supply from a retail pharmacy, the consumer has a strong incentive to have the medication dispensed from the mail order pharmacy.

Act 207 was enacted in an effort to provide greater consumer access to retail pharmacies and a “level playing field” between mail order and retail pharmacies. To accomplish such goals, it required state-licensed health insurers that offer a pre-scription drug benefit to provide such benefits with copayments and coinsurance that are the same for mail order and retail pharmacies if the retail pharmacy agrees to the same terms and conditions that are in place for the plan’s mail order phar-macy.

To assess the impact of Act 2012-207 on consumer access to retail pharmacies and the cost of prescription medications, the Legislative Budget & Finance Commit-tee provided opportunity for retail pharmacies to share their experiences with the implementation of Act 207. We obtained their input through a web-based survey conducted in August and September 2014 with the assistance of the Pennsylvania Pharmacists Association and the Pennsylvania Association of Chain Drug Stores, who made the survey available to their members. Appendix B provides a copy of the LB&FC’s retail pharmacy survey questionnaire. As shown in Table 1, independent retail pharmacies accounted for the largest number of our survey respondents. Five retail chain pharmacies, however, also

1 The Drug Channels Institute is a provider of specialized management education and computer-based training for and about the pharmaceutical industry.

12

participated in the survey. While not shown in Table 1, these chains reported oper-ating over 920 Pennsylvania drug stores.2 Two-thirds of those responding to our survey were from eastern Pennsylvania, as shown in Table 2.

Table 1

Retail Pharmacy Respondents

Type of Pharmacy Number of Responses

Independent Pharmacy .................... 117

Regional Independent Pharmacy ..... 8

Chain ................................................ 5

Did not identify type of pharmacy ..... 2

Total: .............................................. 132 Source: Developed by LB&FC staff from survey responses.

Table 2

Location of Survey Respondents*

Region Number of

Respondents Percent

Northeast .................. 39 30%

Northwest ................. 4 3

North Central ............ 10 8

Southeast ................. 48 37

Southwest ................. 18 14

South Central ............ 11 9 _________________ *N = 130 of 132. Source: Developed by LB&FC staff from survey responses.

2 As of November 2013, the Pennsylvania Department of State licensed over 3,300 pharmacies. Such licenses include retail pharmacies, hospital, long-term care, and specialty pharmacies. Based on the available state li-censure data, it is not possible to determine the exact number of independent and chain retail pharmacies in Pennsylvania.

13

As shown in Table 3, just over three-quarters (101 of 132) of our survey re-spondents, including all chain pharmacy respondents, reported applying to insurers and pharmacy benefit managers3 to offer dispensing under Act 207. Fifteen per-cent (21 of 132) reported they did not apply.

Table 3

Applications for Act 207 Dispensing*

Respondent Type Applied Did not Apply

Independent ........... 96 21

Chain ...................... 5 0

Total ..................... 101 21 _______________ *N = 122 of 132. Source: Developed by LB&FC staff from survey responses.

Reasons Applications for Act 207 Dispensing Were Not Approved

As shown in Table 4, just over half (55 of 101) of respondents that applied

were not approved for Act 207 dispensing. Those not approved included one chain pharmacy, which offered extended medication dispensing prior to Act 207, and planned to continue such dispensing outside of Act 207.

Table 4

Outcome for Applications to Provide Act 207 Dispensing*

Respondent Type Applied Approved Not Approved

Independent ... 96 42 54

Chain .............. 5 4 1

Total .............. 101 46 55 _______________ *N = 101 of 132. Source: Developed by LB&FC staff from survey responses.

3 Employers and plans sponsors often hire pharmacy benefit managers (PBMs) to design and administer plans for prescription drug benefits, including plan drug formularies. PBMs are often selected for their industry knowledge, and their negotiating power (given their large patient base) to secure rebates and discounts from drug manufacturers and pharmacies. PBMs also provide electronic claims processing, pharmacy networks, ge-neric substitution, and patient services. They adjudicate approximately 80 percent of all prescriptions pro-cessed today, with three large PBMs handling 65 percent of outpatient prescription volume. Some PBMs are organizationally affiliated with prescription mail order companies. Currently, PBMs are not regulated in Penn-sylvania or in most states.

14

We asked those respondents who applied and were not approved to provide Act 207 medication dispensing the reason(s) offered for their non-approval. As shown in Table 5, almost three-quarters (19 of 26) of those not approved who pro-vided a reason for their non-approval indicated they did not meet the insurer’s mail order pharmacy network requirements. As one respondent noted:

[the insurers’ Pharmacy Benefit Manager] requires us to be open from 8 A.M. to 10:00 P.M. Monday thru Friday and Saturdays from 8:00 A.M. to 4:00 P.M. Our normal hours are 9-7 Monday through Friday, Satur-day 9-2 and Sunday 10-2. They would not allow us to participate even though we have a pharmacist who is on call after our normal hours….

Table 5 also shows that almost one-third (8 of 26) of those that applied and reported a reason for non-approval indicated they had withdrawn their applications after be-coming familiar with the insurer’s or pharmacy benefit manager’s requirements for Act 207 dispensing. While not shown in Table 5, a sizeable portion (22 of 55) of respondents that applied and were not approved, and did not check a reason for their denial from the list of reasons identified on the questionnaire (see question 8 on the survey ques-tionnaire in Appendix B), provided comments concerning their non-approval. Just over half (12 of 22) of such respondents indicated the insurers or the insurers’ phar-macy benefit managers whom they contacted gave no response or reason for their non-approval.

Table 5

Reasons for Non-Approved Act 207 Applications*

Reason Unduplicated Responsesa

1. Retail pharmacy did not demonstrate that it met all of the insurer’s mail order pharmacy network requirements ........................................................................ 14

2. Retail pharmacy did not meet the insurer’s minimum volume requirement ....... 1

3. Retail pharmacy decided to withdraw and did not pursue its application after review of the insurer’s network requirements and other conditions. .................. 6

Multiple Reasons Reported

1 and 2 above ........................................................................................................ 3

1 and 3 above ........................................................................................................ 2 _______________ *N = 26 of 55. Twelve respondents also indicated the insurer provided no reasons for their non-approval. Source: Developed by LB&FC staff from survey responses.

15

Act 207’s Impact on Consumer Prescription Drug Out-of-Pocket Costs Our survey asked respondents who were approved to provide dispensing un-der Act 207 if consumer out-of-pocket prescription medication costs had declined fol-lowing Act 207’s enactment—one of the General Assembly’s desired outcomes for the Act. As shown in Table 6, just over 50 percent (24 of 46) of the respondents par-ticipating in Act 207’s dispensing, including two chain respondents, think consumer out-of-pocket costs have remained the same (10 of 46) or decreased (14 of 46).

The remainder (22 of 46) reported consumer out-of-pocket costs increased. The reasons offered for such increases, however, are not necessarily related to Act 207. Changes in a prescription drug plan’s deductibles and coinsurance may ac-count for some of the reported consumer prescription drug cost increases.

While not shown in Table 6, typically over half (12 of 22) of those reporting

increases in consumer out-of-pocket costs, including one chain, reported increases under $10, and just under half (10 of 22) increases greater than $10. Only nine of the survey respondents approved to offer Act 207 dispensing reported the amount by which consumer out-of-pocket costs have decreased. Three of the nine reported decreases under $10 and six of the nine reporting decreases greater than $10.

Table 6

Perception of Consumer Extended Medication Copayment Costs After Act 207’s Enactment*

(Those Approved to Offer Act 207 Dispensing)

How Consumer Costs Were Affected

Unduplicated Responses

Independents

Unduplicated Responses

Chains

Consumer out-of-pocket costs have increased due to, for example, higher copayments, coinsurance, and deducti-bles introduced by the insurer for both retail and mail order customers ............................................................................. 20 2

Consumer out-of-pocket costs have decreased due to, for example, Act 207’s establishment of copayments, coinsur-ance, and deductibles equal to those encountered through use of mail order pharmacies ............................................... 10 0

Consumer out-of-pocket costs have neither increased nor decreased ............................................................................. 12 2

_______________ *N = 46 of 46. Source: Developed by LB&FC staff from survey responses.

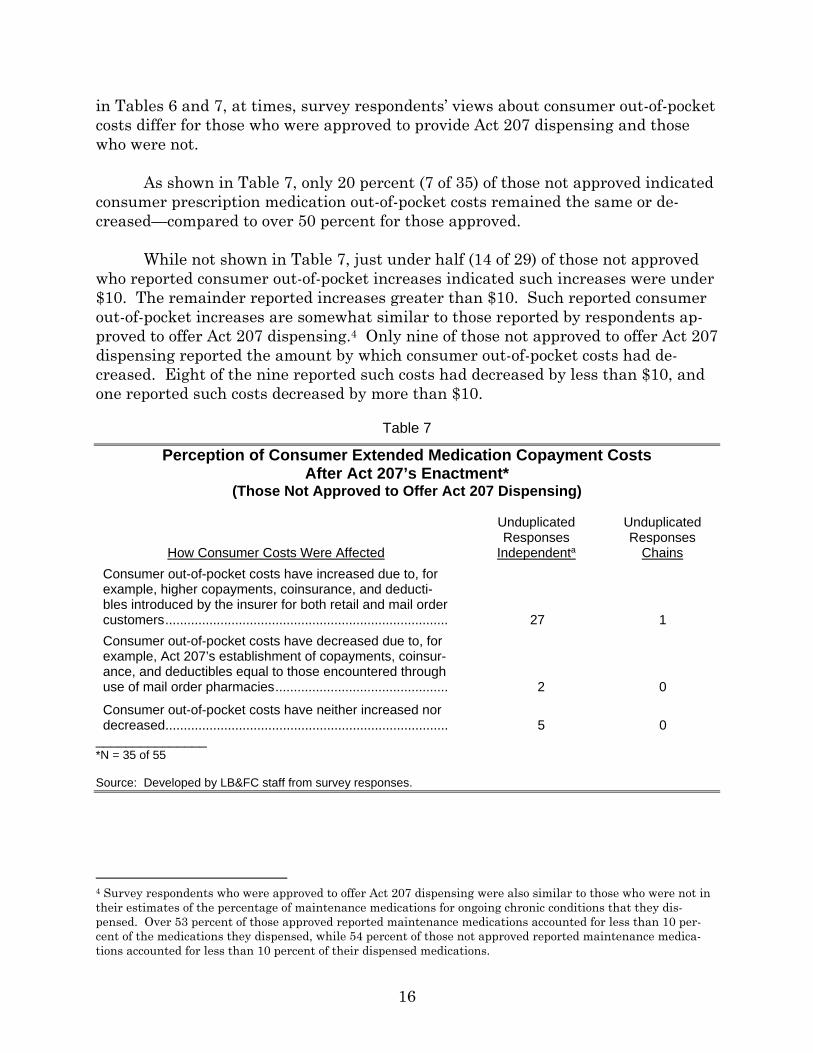

Our survey did not ask those who applied and were not approved to provide Act 207 dispensing their perceptions of consumer out-of-pocket prescription drug costs after Act 207’s enactment. Many (35 of 55), however, offered them. As shown

16

in Tables 6 and 7, at times, survey respondents’ views about consumer out-of-pocket costs differ for those who were approved to provide Act 207 dispensing and those who were not.

As shown in Table 7, only 20 percent (7 of 35) of those not approved indicated consumer prescription medication out-of-pocket costs remained the same or de-creased—compared to over 50 percent for those approved.

While not shown in Table 7, just under half (14 of 29) of those not approved

who reported consumer out-of-pocket increases indicated such increases were under $10. The remainder reported increases greater than $10. Such reported consumer out-of-pocket increases are somewhat similar to those reported by respondents ap-proved to offer Act 207 dispensing.4 Only nine of those not approved to offer Act 207 dispensing reported the amount by which consumer out-of-pocket costs had de-creased. Eight of the nine reported such costs had decreased by less than $10, and one reported such costs decreased by more than $10.

Table 7

Perception of Consumer Extended Medication Copayment Costs After Act 207’s Enactment*

(Those Not Approved to Offer Act 207 Dispensing)

How Consumer Costs Were Affected

Unduplicated Responses

Independenta

Unduplicated Responses

Chains

Consumer out-of-pocket costs have increased due to, for example, higher copayments, coinsurance, and deducti-bles introduced by the insurer for both retail and mail order customers ............................................................................. 27 1

Consumer out-of-pocket costs have decreased due to, for example, Act 207’s establishment of copayments, coinsur-ance, and deductibles equal to those encountered through use of mail order pharmacies ............................................... 2 0

Consumer out-of-pocket costs have neither increased nor decreased ............................................................................. 5 0

_______________ *N = 35 of 55 Source: Developed by LB&FC staff from survey responses.

4 Survey respondents who were approved to offer Act 207 dispensing were also similar to those who were not in their estimates of the percentage of maintenance medications for ongoing chronic conditions that they dis-pensed. Over 53 percent of those approved reported maintenance medications accounted for less than 10 per-cent of the medications they dispensed, while 54 percent of those not approved reported maintenance medica-tions accounted for less than 10 percent of their dispensed medications.

17

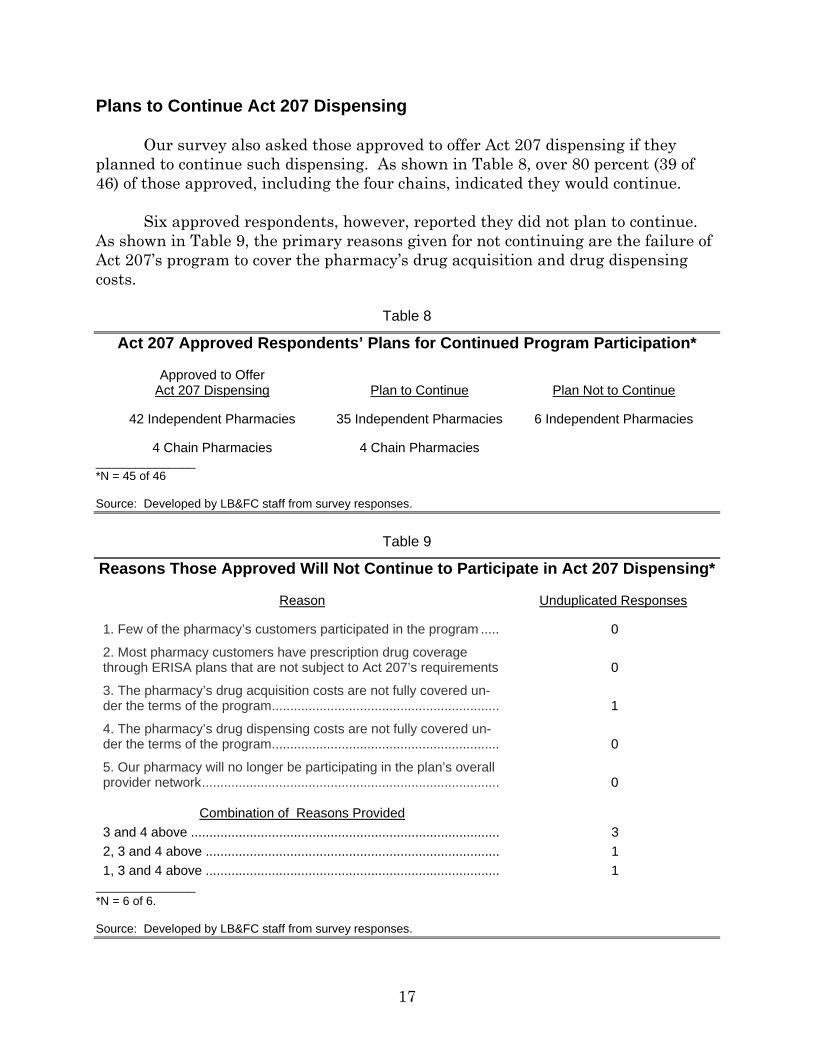

Plans to Continue Act 207 Dispensing Our survey also asked those approved to offer Act 207 dispensing if they planned to continue such dispensing. As shown in Table 8, over 80 percent (39 of 46) of those approved, including the four chains, indicated they would continue. Six approved respondents, however, reported they did not plan to continue. As shown in Table 9, the primary reasons given for not continuing are the failure of Act 207’s program to cover the pharmacy’s drug acquisition and drug dispensing costs.

Table 8

Act 207 Approved Respondents’ Plans for Continued Program Participation*

Approved to Offer Act 207 Dispensing Plan to Continue Plan Not to Continue

42 Independent Pharmacies 35 Independent Pharmacies 6 Independent Pharmacies

4 Chain Pharmacies 4 Chain Pharmacies _______________ *N = 45 of 46 Source: Developed by LB&FC staff from survey responses.

Table 9

Reasons Those Approved Will Not Continue to Participate in Act 207 Dispensing*

Reason Unduplicated Responses

1. Few of the pharmacy’s customers participated in the program ..... 0

2. Most pharmacy customers have prescription drug coverage through ERISA plans that are not subject to Act 207’s requirements 0

3. The pharmacy’s drug acquisition costs are not fully covered un-der the terms of the program .............................................................. 1

4. The pharmacy’s drug dispensing costs are not fully covered un-der the terms of the program .............................................................. 0

5. Our pharmacy will no longer be participating in the plan’s overall provider network ................................................................................. 0

Combination of Reasons Provided

3 and 4 above .................................................................................... 3

2, 3 and 4 above ................................................................................ 1

1, 3 and 4 above ................................................................................ 1 _______________ *N = 6 of 6. Source: Developed by LB&FC staff from survey responses.

18

Our survey provided opportunity for retail pharmacists to provide comments about Act 207 and its implementation. Exhibit 3 provides some of the key com-ments about Act 207 offered by pharmacies responding to our survey.

Those providing comments typically indicated the Act, while well intentioned, was ignored, “lacked teeth,” or was not enforced. They also often noted concerns about the practices of pharmacy benefit managers (PBMs) with the way in which drug prices are established, and differences in the way in which prices are deter-mined for retail and mail order pharmacies by drug manufacturers and pharmacy benefit managers. While some of the respondents’ concerns are outside of the scope of Act 207 (e.g., how drug prices are established) and the current statutory author-ity of the of the state Insurance Department (see Finding B for additional infor-mation about the authority of the Pennsylvania Insurance Department with respect to “health insurers” and Act 207), they have been included in Exhibit 3 in view of their importance to retail pharmacies.

Our survey responses are also consistent with insights shared by an inde-pendent pharmacist involved in drafting the initial versions of Act 207 and the com-promises that were reached to obtain its passage. This independent pharmacist, for example, advised the LB&FC:

The retail pharmacy community agreed to revisions to the legislation in the hope that the legislation, while not perfect and intentionally not addressing a number of issues, would nonetheless significantly increase access to retail community pharmacy services and pave the way for future constructive dia-logue. Unfortunately…health insurers, government programs and pharmacy benefit managers have taken advantage of the legislation’s failure to more clearly address a number of issues by interpreting the revised legislation in a manner that prevented it from having any appreciable impact on the availa-bility of retail pharmacy services to Pennsylvania consumers.

19

Exhibit 3

Retail Pharmacists’ Comments About the Impact of Act 207 on Access to and Cost of Prescription Drug Coverage

Act 207 had made no changes. Because of the copay structure, consumers are forced to use

mail order pharmacies.

We need a law with teeth. This was a good first step.

It has no “teeth” so to speak. There are too many ways left open for plans to exclude or restrict independent pharmacies.

The act has been totally ignored by PBMs [pharmacy benefit managers]. I don’t think I have re-tained one patient due to ACT 207. I continue to lose patients on a monthly if not weekly basis to mandatory mail order or exclusive chain contracts.

…While Act 207 was initiated with well intentions, it has NOT [emphasis in the original] accom-plished anything, the PBMs [pharmacy benefit managers] still do whatever they want to regard-less of this act and things will never change until there is transparency in their corrupt system.

While I answered the above positively [i.e., the respondent has been approved to participate in at least one plan under Act 207], the option to be in these plans is very limited. There are still some main plans in my market that I do not/cannot participate in.

The largest problem with extended medication dispensing is the reimbursement of medication and dispensing costs. Some plans reimburse at costs below any of our suppliers’ charge for medication. It is not possible to remain in business when there are reimbursements below our WAC [Wholesale Acquisition Cost].a

Most patients are locked into mail order suppliers through employer provided insurance, and are not able to utilize our pharmacy services to benefit them. The answer we get when we try to submit the claims to insurance is that it is not their fault. The employer selected the mail order option but they do not mention the fact about the better deal they offer to employers if their em-ployees utilize the PBM mail order services. Mail Order facilities are inflating AWPs [Average Wholesale Prices]b on repackaged medications causing their plan sponsors to pay more. Spread pricingc is also costing plan sponsors more money while PBM profits flourish. Most plans still excluding Independent Pharmacies from participating—such as Caremark insisting the use of mail-order or CVS stores only. Mandates to participate are not realistic. PBMs take 3 months to update manufacturer price increases, but are able to update price decreases within 1 day. Patients prefer dealing with their local independent Pharmacy especially senior citizens & handi-capped individuals. We have also found those people where English is their second language have problems communicating with mail-order. Three months supplies are in many cases wasteful. Mail-order automatic deliveries are even more wasteful as drugs are sent to patients that have passed on for months after their passing. We are being asked to fill Rx’s at a loss with many of the plans because of MAC [Maximum Allowable Cost] pricingd while Mail-Order con-tracts do not use MAC pricing. Nobody seems concerned that profits do not cover expenses in Community Pharmacy—Cost of dispensing surveys are being ignored. Professional Fee of $0.25/Rx are a disgrace and has become the norm. It was $2.50 in the 70s.

As a business owner, I cannot continue to accept below cost reimbursement. We lost $110 on one generic prescription today!!!!! No other business in the world has to deal with this on a daily basis!

How could plan sponsors mail out letters to PA residing members mandating MAIL ORDER [em-phasis in the original] for maintenance drugs.

20

Exhibit 3 (Continued) The intent of the law has been, in my opinion, ignored by the majority, if not all, PBMs and insur-

ance companies. We have been offered, and in some cases, accepted extended prescription benefits (as a courtesy to our patients/customers). BUT [emphasis in the original] we have been shut out from any attempt to provide extended benefits at the same terms and conditions—be it on the copay end or the reimbursement end. That is, we are offered lower rates [for drug acqui-sition costs] and patients pay higher copays [than they would for mail order]. The intent of the law was to allow access to lower copays at retail under the same payment terms and conditions. Retail pharmacy providers have been denied reimbursement at the same terms and conditions. We were originally excited by Act 207 because we thought it would level the playing field for all pharmacies. But we have not been accepted into any of the 90 day plans. In addition the PBMs all tell us the law does not apply to Specialty medications and they continue to restrict us from every network that involves Specialty medications. It has not helped us at all.

The manufacturer’s steep price increases, sometimes 1000% overnight and lack of payors re-sponse to those increases have made pharmacy a very difficult business to be in. In my opinion there seems to be no end in sight for drug pricing increases by manufacturers and ignorance by payors. PBMs are quick to drop reimbursement on medications but super slow to raise the MACs, and when they do it is often raised for a short time, then dropped again days or weeks later. Dispensing fees are comical, plans insult us with … reimbursement fees that are a joke and make completing these cases a full time job. Soon health care will be a ‘you get what you pay for’ type business. Good pharmacies and pharmacists will shift their attention to more re-warding less bureaucratic business models which will leave consumer wondering what hap-pened. It is a crime that our elected officials do not do more for our small businesses in this country!

Only one insurance has dealt with us according to Act 207, the other insurances (PBMs) have totally ignored Act 207 by not even giving us a contract to let us choose to join or not. Patients in the one contract that let us in are very happy to be able to deal with their local pharmacist for quick service and answered questions instead of wondering if the drugs by mail would be deliv-ered on time.

The Insurance Department doesn’t seem interested in upholding this law.

Until the Insurance Dept. starts enforcing 207, nothing much will change.

We need an Act to provide for Fair pricing of meds and fair reimbursements to all pharmacies!! ____________ a Wholesale Acquisition Cost (WAC) is the price paid by a wholesaler for drugs purchased from the wholesaler’s sup-plier, typically the manufacturer of the drug. Publicly disclosed or listed WAC amounts may not reflect all available discounts. b Average Wholesale Price (AWP) is recognized as retail list price and is currently used by some public and private third-party payers as the basis for reimbursement (e.g. AWP minus 5 or 25 percent). AWP has been widely criticized as a price that is not reflective of the true market price and easily manipulated, according to the Kaiser Family Foun-dation. c Spread pricing refers to the practice of pharmacy benefit managers (PBMs) billing health plans or employers more for the drug than the PBM pays the local pharmacist. For example, the PBM pays the pharmacy $100 for filling a pre-scription for a 30-day supply of a drug. The PBM then bills the health insurance plan sponsor or employer or union, $110 when an insured’s prescription is filled. d MAC lists are designed to cap reimbursement for certain generic and multi-source brand products. States and pri-vate payers with MAC programs typically publish lists of selected generic and multi-source brand drugs along with the maximum price at which the program will reimburse for those drugs. In general, pharmacies will receive payment no higher than the MAC price when billing for drugs on an MAC list. Source: Developed by LB&FC staff from survey responses.

21

This independent retail pharmacist further noted:

A number of factors, most of which are an outgrowth of the changes to Senate Bill 201 and House Bill 511 have prevented Act 207 from improving access to retail community pharmacy services as intended by the sponsors of the legis-lation. These factors include:

requirements that pharmacies already enrolled in the provider net-works of insurance companies by pharmacy benefit managers must ap-ply for and be approved for admittance into new provider networks to enjoy the benefits of Act 207;

discriminatory requirements for admission into provider networks that

either effectively block participation by retail pharmacies or make their participation in networks unreasonably burdensome;

a lack of transparency regarding the pricing terms and conditions be-

ing paid to mail-order pharmacies coupled with demands that such pricing terms be accepted without adequate disclosure;

the general refusal of pharmacy benefit managers affiliated with mail

order pharmacies to include payments received from insurers and drug manufacturers in amounts paid to retail pharmacies;

assertions that self-funded employee benefit plans created by collective

bargaining agreements for Pennsylvania government employees are not subject to Act 207;

the failure of the Pennsylvania Insurance Department to apply the re-

quirements of Act 207 to pharmacy benefit managers acting as risk-bearing preferred provider organizations (PPOs), including pharmacy benefit managers providing services to employee benefit plans subject to the federal Employment Retirement Income Security Act (ERISA); and

the lack of effective efforts by the Pennsylvania Insurance Department

to enforce the law in a manner consistent with the legislative objec-tives.

The absence of widespread implementation of Act 207 has provided little oppor-tunity for the Act to impact (either positively or negatively) the cost of prescription medication services, according to this independent retail pharmacist—a conclusion consistent with our own based on data reported by LB&FC survey respondents and several major insurers.

22

During the course of our study, we received several suggestions on steps to improve the implementation of Act 207. The independent pharmacist recommends:

…a careful analysis of the legality of the tactics and strategies used by phar-macy benefit managers and insurance companies to impede implementation of Act 207 and the adoption of regulatory policies, and perhaps amendments to Act 207, to ensure that the legislation achieves its intended goals and ob-jectives.

A chain pharmacy representative advised the LB&FC that to increase the

number of pharmacies participating in Act 207, the insurers and PBMs need to offer community pharmacies a “reasonable rate that would not result in the community pharmacy losing money filing prescriptions,” as can occur with Act 207’s require-ment that a community pharmacy accept the same “terms and conditions” as a mail order pharmacy. In addition, the limited scope of Act 207 would need to be ad-dressed to increase utilization by community pharmacies.

The Pennsylvania Insurance Department advised us that it was not actively

involved in the drafting of Act 207. It suggested that should the Pennsylvania Gen-eral Assembly plan to revise the statute, PDI be involved initially and throughout the process in view of the complexity of health insurance in Pennsylvania and na-tionally.

23

III. Appendices

24

APPENDIX A INSURANCE COMPANY LAW OF 1921 - COVERAGE OF PRESCRIPTIONS

SB 201

Act of Nov. 1, 2012, P.L. 1670, No. 207 Session of 2012

No. 2012-207

AN ACT

Cl. 40

Amending the act of May 17, 1921 (P.L.682, No.284), entitled "An act relating to insurance; amending, revising, and consolidating the law providing for the incorporation of insurance companies, and the regulation, supervision, and protection of home and foreign insurance companies, Lloyds associations, reciprocal and inter-insurance exchanges, and fire insurance rating bureaus, and the regulation and supervision of insurance carried by such companies, associations, and exchanges, including insurance carried by the State Workmen's Insurance Fund; providing penalties; and repealing existing laws," in health and accident insurance, providing for coverage of prescriptions.

The General Assembly of the Commonwealth of Pennsylvania

hereby enacts as follows:

Section 1. The act of May 17, 1921 (P.L.682, No.284), known as The Insurance Company Law of 1921, is amended by adding a section to read:

Section 635.6. Coverage of Prescriptions.--(a) A health insurance policy or government program providing benefits for prescriptions shall not impose on a covered individual utilizing a retail pharmacy a copayment, deductible, fee, limitation on benefits or other condition or requirement not otherwise imposed on the covered individual when using a mail-order pharmacy.

(b) Subsection (a) shall apply only if the retail pharmacy is willing to accept from the insurer the same pricing, terms, conditions or requirements related to the cost of the prescriptions and the cost and quality of dispensing prescriptions that the insurer has established for a mail-order pharmacy and any of such pharmacy's affiliates, including any affiliated pharmacy benefit manager, pursuant to the health insurance policy.

(c) Beginning eighteen months after the effective date of this section, the Legislative Budget and Finance Committee shall conduct an evaluation of the impact of this section regarding the access to prescription drugs at both independent and chain retail pharmacies and whether the provisions of this section have had a material positive or negative impact upon the cost of prescription medications to

25

Appendix A (Continued)

consumers and health care plans and shall issue a report to the General Assembly within nine months of the commencement of the study regarding its findings and recommendations.

(d) As used in this section: (1) "Government program" means any of the following: (i) The Commonwealth's medical assistance program

established under the act of June 13, 1967 (P.L.31, No.21), known as the "Public Welfare Code."

(ii) The Children's Health Care Program established under Article XXIII.

(iii) The program of pharmaceutical assistance for the elderly established under Chapter 5 of the act of August 26, 1971 (P.L.351, No.91), known as the "State Lottery Law."

(2) "Health insurance policy" means a group or individual health or sickness or accident insurance policy, subscriber contract or certificate issued by an entity subject to any one of the following:

(i) This act. (ii) The act of December 29, 1972 (P.L.1701, No.364),