Comparing Credit Risk in Islamic and Conventional Banking ...

Upload

brendan-conleyCategory

view

224download

2

Lecture 2

Conventional Banking and Islamic Banking Systems

1

BANKis a financial institution and a financial intermediary that

accepts deposits and channels those deposits into lending activities, either directly by loaning or indirectly through capital markets. A bank links together customers that have capital deficits and customers with capital surpluses.

2

Types of BanksThere are various types of banks. The

necessity for the variety among these banks is because each bank is specialized in their own field. Each bank has its own principles and policies. Different rates of interests are also noted among these banks.

3

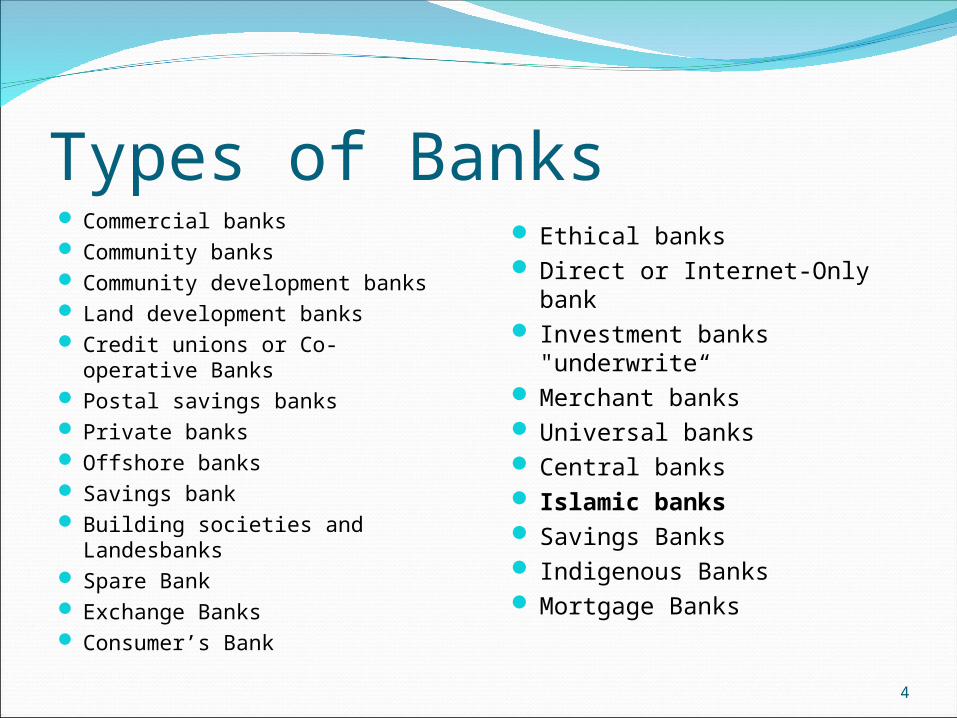

Types of Banks Commercial banks Community banks Community development banks Land development banks Credit unions or Co-operative Banks Postal savings banks Private banks Offshore banks Savings bank Building societies and Landesbanks Spare Bank Exchange Banks Consumer’s Bank

Ethical banks Direct or Internet-Only bank Investment banks "underwrite“ Merchant banks Universal banks Central banks Islamic banks Savings Banks Indigenous Banks Mortgage Banks

4

Types of BanksSavings Banks – these banks are suited for employees with a

monthly salary. Low waged people may open an account in the savings bank.

Commercial Banks – These bank collects money from people in various sectors and gives the same as a loan to business men and make profits in interests these business men pay. Since the loan is large the interest rates are also high.

Industrial Development Bank – these banks are committed towards enhancing the growth of industries by providing loans for a very long period of time. This is vital for the long term growth of the industries.

Land Development’s Bank – these banks promote growth in the food sector, by giving loans to farmer at a relatively lower interest rate. The loan is usually given on the basis of land. If a farmer has lots of agricultural fields then the more will be the loan provided.

5

Types of Banks Indigenous Banks – native banks. They are normal moneylenders; only

this time, handling huge amounts of money. They collect money from the community and provide loans to business men and industrialists for a short amount of time.

Mortgage Banks – these banks are specialized in providing mortgage loans alone. In order to sell loans they depend solely on the secondary market.

Spare Bank – these banks are present in Norway. They promote both savings and commercial facilities to the both people and organizations in Norway.

Federal or National Banks – these banks control the principles and policies of other banks across the country. These banks are managed and run by the government. This bank provides benchmarks which other banks should follow.Co operative banks: co operative banks as the name suggests gets money from the general community without any bias and provide loans to all sections of people in the neighborhood. Their motto is not profit alone, but service.

6

Types of Banks Exchange Banks – these banks will be available in more than a

single country. They provide services for the buying and selling of gold and silver; transactions will be in foreign currencies.

Consumer’s Bank – these are consumer friendly banks; they encourage the consumer in buying commercial products and provide options for easy repay of the loan amount.

Community Development Banks – these banks provide services to the community; where there has been nothing or very little development over the years.

Credit Unions – they act just like a co operative bank except that they provide services to only one employee union in the community. Low interest rates and easy installment paybacks are features of this bankPostal savings bank: these banks are oriented with postal services. People save money for a defined period of time and are paid with standard interest rates.

7

Types of BanksOffshore Banks – they are also private banks except that

they have little tax to pay for their transactions; there is very little regulation for this bank.

Ethical Banks – as the name implies ethical banks promote candid transactions; between various customers of the bank. Policies and rules are transparent in nature.

Internet Bank – provides banking facilities only via internet. There will be no physical contact with the bank. All transactions are permitted only through online.

Investment Banks – these banks are pertinent to large organization’s investment ventures across the industry. They provide advice in the investments and promote corporate transactions.

8

Types of Banks Private Banks – these banks are not for the general public or

community. They serve entirely for private personnel’s assets and transactions alone.

Merchant Banks – these banks exist for a long time. They promote investing in organizations that reap huge benefits for a long time rather than brand new organizations.

Universal Banks – these banks have a wide spectrum of financial assistances to provide. Insurances to stocks, they promote everything across all countries around the globe.

Islamic Banks – these banks are based on the principles of the religion Islam. There are no interests for loans acquired from this bank. Service charges may apply. This means that all operations of Islamic bank mast be based on regulations and rules of Islam.

9

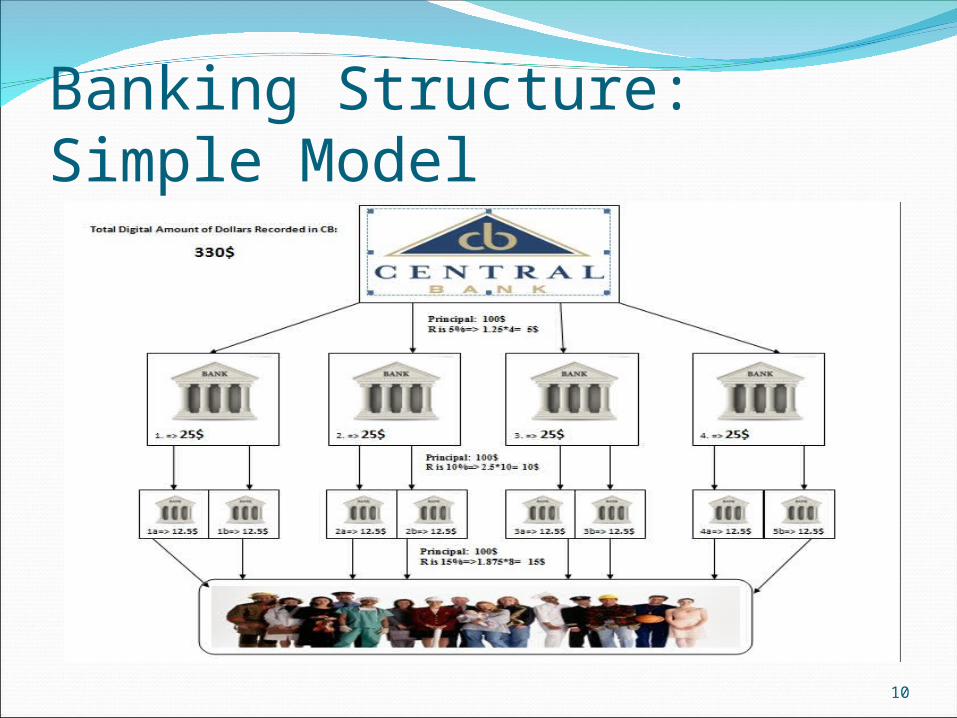

Banking Structure: Simple Model

10

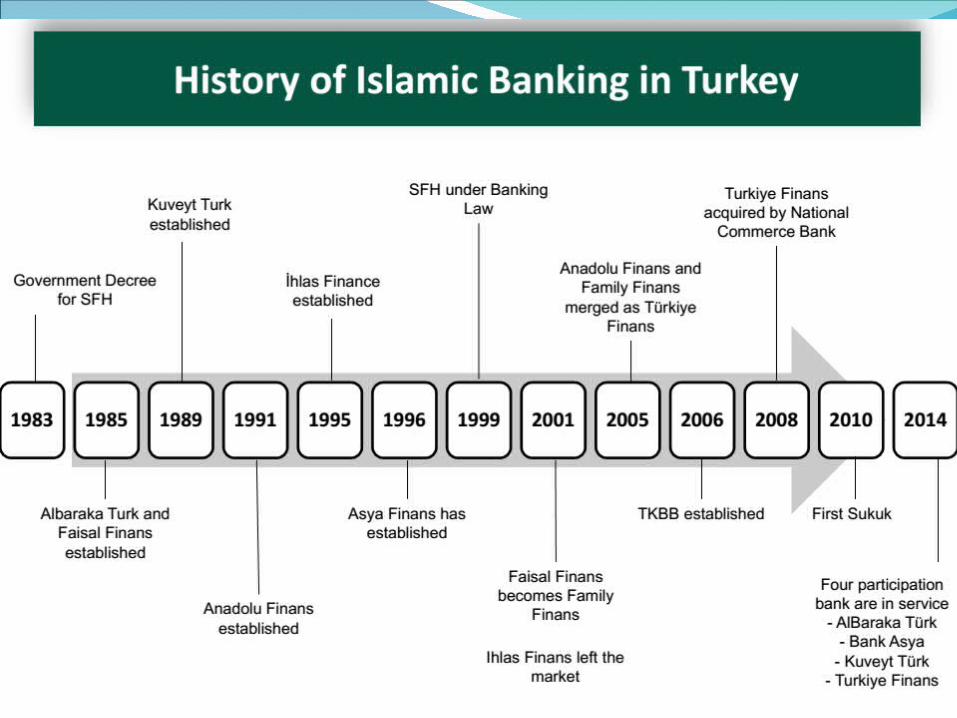

History of Islamic Banking Islam is not a new religion; it is the same truth that God

revealed through all His prophets. All religions are the same in essence, whether given, for example, to Noah, Abraham, Moses, or Jesus, or to the holy Prophet of Islam. For a fifth of the world’s population, Islam is both a religion and a complete code of life.

Economic growth is the main transmission channel for development. Islam does not contradict growth; it promotes sustainable development and growth.

Modern conventional banking system came into existance nearly 427 years ago-Banco Della Pizza in Venice 1587

11

History of Islamic BankingThe term Islamic banking became common in the 1960's, but the

mechanisms and concepts of the system were implied and used since the birth of Islam. Many studies and researches have shown that Islamic finance mechanisms were used in the Muslim world throughout the Middle Ages; in conducting trade and business activities.

Early experiments with Islamic Banking took place in Malaysia in the mid 1940s, in Pakistan in the late 1950s and Egypt’s Mit Ghamr Savings Bank (1963) and Nasser Social Bank (1971).

In the Arab world the 1st modern experiment with Islamic banking was undertaken in Mit Ghamr, Egypt in 1963. The experiment combined the idea of German Savings banks with the principle of rural cooperative banking within the general framework of Islamic financing, to cater for those unwilling, for religious reasons, to deal with the conventional banks.

12

History of Islamic Banking In fact, in 1976, Mit Ghamr Savings bank was closed and its

operation taken over by the National Bank of Egypt and made interest based.

Similar political antagonism to Islamic financial institutions, occurred elsewhere in the Muslim world; Iraq, Oman, Syria and even Saudi Arabia. Two institutions that however survived this early period were the Nasser Social Bank established in 1971 in Egypt and Tabung Hajj, established in 1963 in Malaysia.

From the mid 70s a new era was witnessed in the history of Islamic Banking in the wake of oil wealth. Energy price rises provided the financial capital to support an expansion of both conventional and Islamic Banks and oil resources enabled a wide range of institutions to participate in the social and economic development of Muslim countries, the result was a change in the political climate in many Muslim countries hence largely dispensing the need to operate Islamic financial institutions under cover.

13

History of Islamic Banking A visible achievement arising from oil-related resource boosting is

the establishment of the Islamic Development Bank (IDB) in 1975. An important development in the 80s is the restructuring of the

whole financial system of Iran, Sudan and Pakistan to accord with Islamic precepts:- Iran in March 1984, Sudan in July 1984 and Pakistan a gradual transition from 1977.

Another important development in the 80s is the establishment of two groups of companies; Dar al-maal al-Islam in 1981 and Al-Baraka group in 1982. Dar al-maal al-Islam was founded in Bahamas, headquartered in Geneva and operates 10 Islamic banks, 7 Islamic investment companies, 7 trading companies and 3 Takaful (Islamic Insurance) companies in 15 countries around the world while Al-Baraka group was established in Saudi Arabia in 1982 and currently has activities in 43 countries. It has over 2000 companies including 15 Islamic banks and several Islamic insurance companies.

14

History of Islamic BankingThe IMF issued first study on Islamic banking

in 1987. since then more research papers have come.

Traditional banks opened Islamic unitsMajor conventional banks establishing

Islamic branches dealing exclusively with Islamic products.

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Islamic Banking Activities in accordance with Shariah:Different Accounts in IBMusharakahMudarabahMurabahahIjarahQard HassanSalam and Istisna SukukZakat

29

Different Accounts in IB

In Islamic banking each customer is a partner with the Islamic Financial Institution (IFI). This relationship is classified as a Mudarib Partnership. Profits resulting from the account are divided between the parties. An IFI receives a certain percentage of the net profits, as a return for the amounts deposited in different investment accounts as its share, being a Mudarib, as agreed between the customer, who is the investment account holder, and the IFI.

30

Current AccountsCurrent accounts are an interest-free loan by

the account holder to the Islamic bank, which maintains these funds and pays them to the customer on demand. These accounts are similar to a loan in guarantee and the payment of the same amount. An IB has the right to invest the funds it is holding in current accounts without the customer bearing any loss. For this reason, the customer does not get any profit on this type of account, but he also does not bear any loss.

31

Investment Savings AccountsMany Islamic banks offer savings accounts to

their customers. This account allows the account holder to place funds in a safe environment till such time when they may wish to withdraw them. Profits and losses under investment savings accounts accrue on the minimum monthly balance. Profits are paid, or losses are deducted, after the expiry of the financial year and the net profits are determined.

32

Musharakah

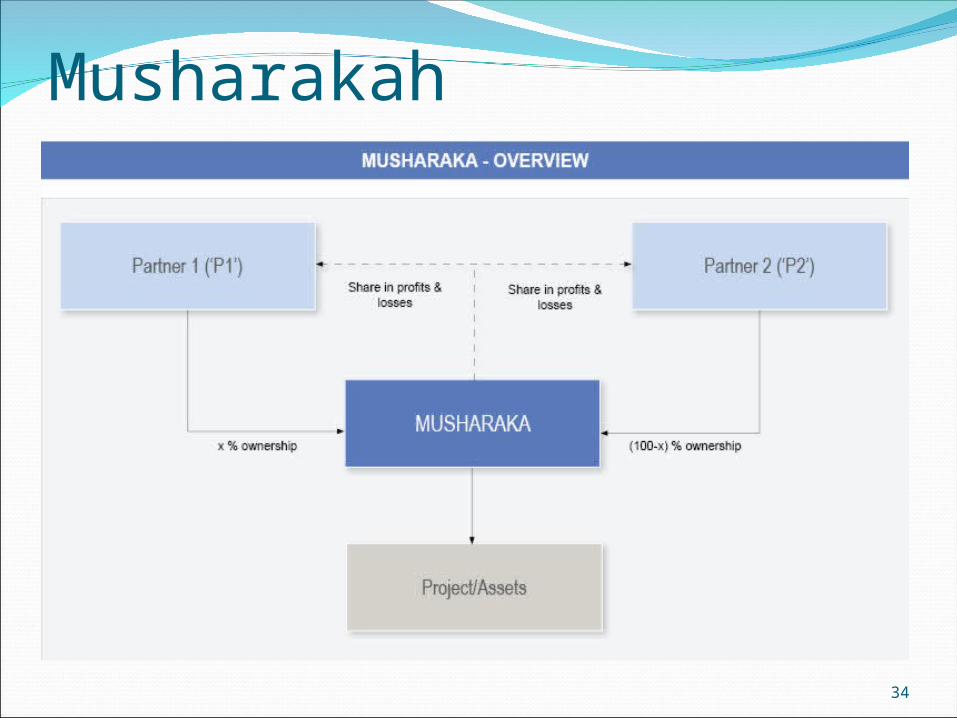

Musharakah is an Islamic mode of financing in the form of a partnership between the bank and its client whereby each party contributes to the capital of the partnership in equal or varying degrees either to establish a new project or share in an existing project.

The accruing profit is divided between the partners pre-agreed formula, while losses are shared on pro rata basis.

The word Musharakah is derived from the Arabic word Sharikah meaning partnership. Islamic jurists point out that the legality and permissibility of Musharakah is based on the injunctions of the Qur'an, Sunnah, and Ijma (consensus) of the scholars.

33

Musharakah

34

MudarabahMudarabah is an Islamic mode of financing between the bank,

providing a specified amount of capital, and the Mudarib, providing management for carrying out the venture, trade or service with a view to earning profit. It is a special kind of partnership where one partner gives money to another for investing it in a commercial enterprise. The former is called Rabb - ul - mal and the latter is called Mudharib.

Thus, Mudarabah is a contract between those who have capital and those who have expertise, where the first party provides capital and the other party provides the expertise with the purpose of earning Halal (lawful) profit which will be shared in a mutually agreed upon proportion. This type of business venture serves the interest of the capital owner and the Mudarib (agent).

35

Mudarabah

36

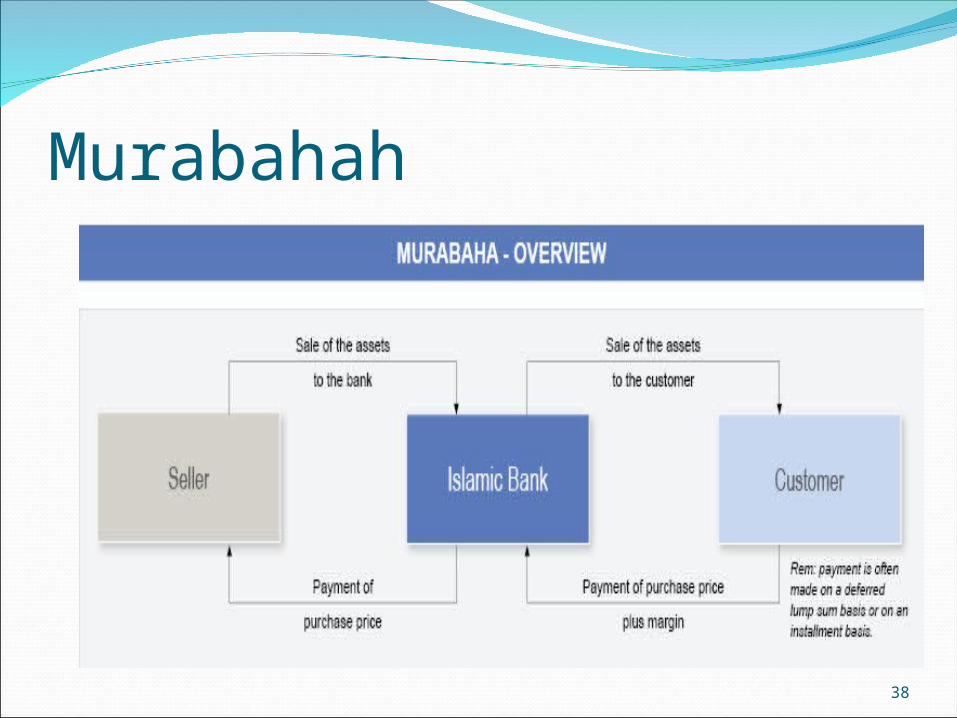

Murabahah Murabaha is one of the Islamic Finance modes and it is

very popular worldwide nowadays. Murabaha; sometimes referred to as “Murabahah” is also known as “corporate asset support”. The concept of murabaha can be summed up as; “Bank finances the needed purchase, buys it, and resells it with a mark – up”. murabaha financing means, “cost plus financing”.

Murabaha is an Islamic finance instrument which of course does not include interest (usury – riba) in it. The philosophy laying in the roots of murabaha financing is to supply a needed service, good or commercial right. Bank; Islamic bank in this situation, buys that needed property or service in advance with cash money than resells it to the client with an added profit as deferred payment base

37

Murabahah

38

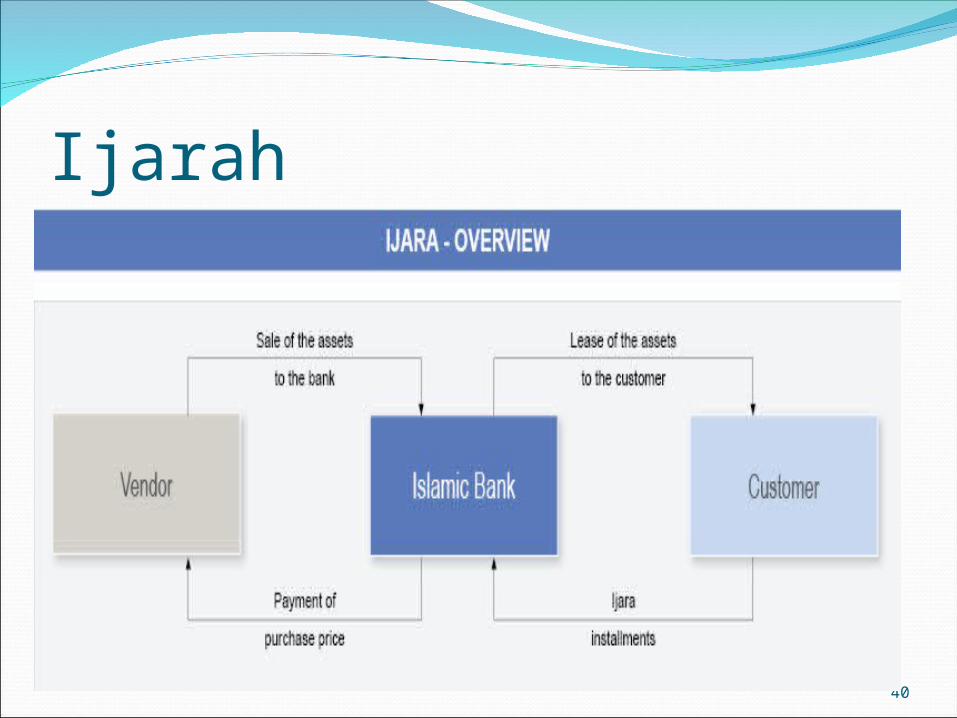

IjarahIjarah is an operating lease contract whereby

the bank avails assets to the customer against a periodic rental fee for a specified period of time. The asset continues to be owned by the bank, and will revert back to the bank at the end of the lease contract. Ijarah is commonly used for the finance of expensive equipment.

39

Ijarah

40

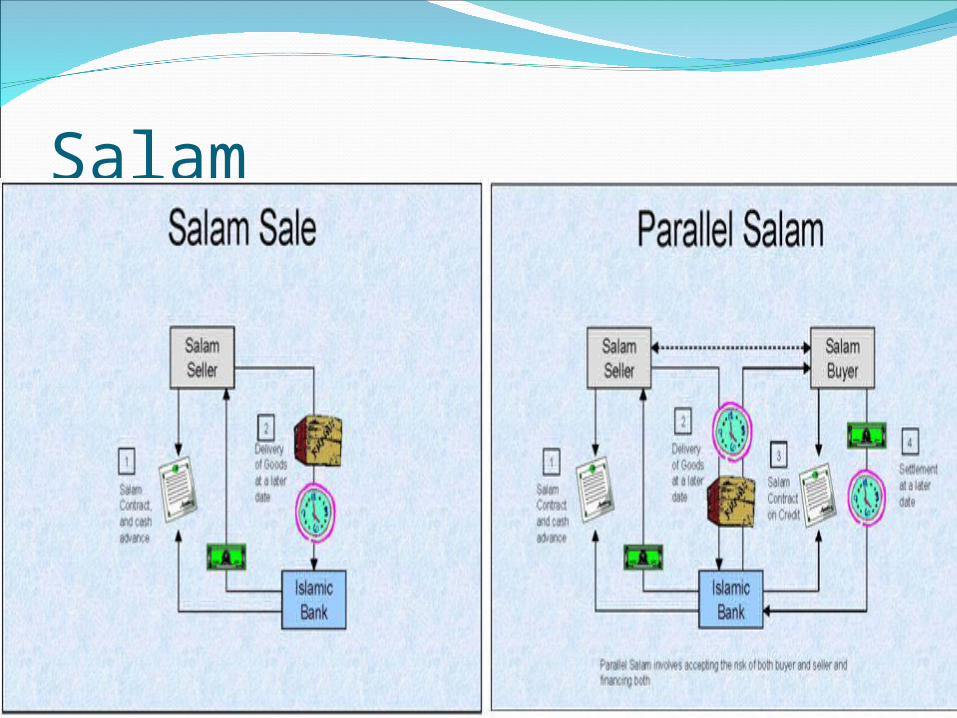

SalamSalam is a future contract. It is the purchase or sale of a

commodity according to defined specifications and conditions for deferred delivery on a specified date in the future in exchange for immediate payment.

Parallel Salam allows the bank to buy a product through a Salam contract with one customer for deferred delivery, extending the cash immediately to the customer so that they can procure or produce the product, and sell the same product for future delivery on another contract to another customer.

41

SalamThis is allowed provided the two contracts are not legally

related. The bank would thus have facilitated a deal between two customers by availing funds immediately to the producer/seller while providing a form of guarantee to the buyer towards the fulfillment of the sale. Like Istisna’, Salam can be combined with other Islamic financing products to form a derivative that allows for the financing of the full production/procurement – sale cycle.

42

Salam

43

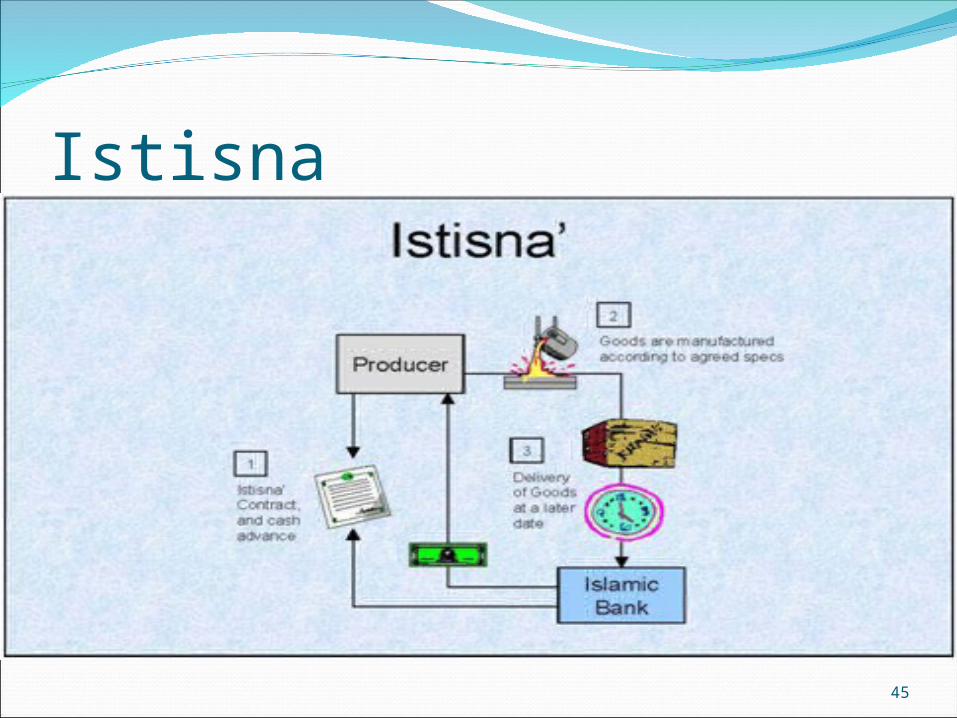

Istisna Istisna’ is a contract whereby the purchaser asks the seller

to manufacture a specifically defined product using the seller’s raw materials at a given price. The contract is a future contract by nature, in that it allows for the sale of a product that is not available at the time of sale. The price may be paid on credit.

Istisna’ has many uses, and can be applied in construction contracting and manufacturing finance. It can also be combined with other Islamic financing products to form a derivative that allows for the financing of the full production – sale cycle.

44

Istisna

45

ZakatA term used in Islamic finance to refer to the

obligation that an individual has to donate a certain proportion of wealth each year to charitable causes. Zakat is a mandatory process for Muslims in order to physically and spiritually purify their yearly earnings that are over and above what is required to provide the essential needs of a person or family.

46

ZakatThere are comprehensive descriptions in

religious texts describing minimum amounts of zakat with regards to farm produce, cattle, business activities, paper currency and precious metals such as gold and silver.

The most common level of zakat on wealth from cash, equities and gold is 2.5% of the total value.

47

What is Shariah?

48

SunnahQuran

QiyasIjmah

SHARIAHQURAN – holy book of Islam and understood

by Muslims literature word of God.SUNNAH- sayings, actions and approvals of

prophet Muhammed (pbuh).IJMAH- this is consensus reached on

particular issue by Islamic Scholars.QIYAS- analogy, simply to say decisions made

by Islamic scholars on particular issue by comparing with similar situations may have happened before.

49

Islamic Banking and Finance Basic PrinciplesContracts are considered to be permissible

assuming no Shariah violation is provedTherefore Shariah is not restricted to any

specific forms of contracts.Shariah made changes to the prevailing

contracts of that time by adding additional conditions.

Any arrangement leading to a prohibited practice is also prohibited.

50

Main Prohibitions

51

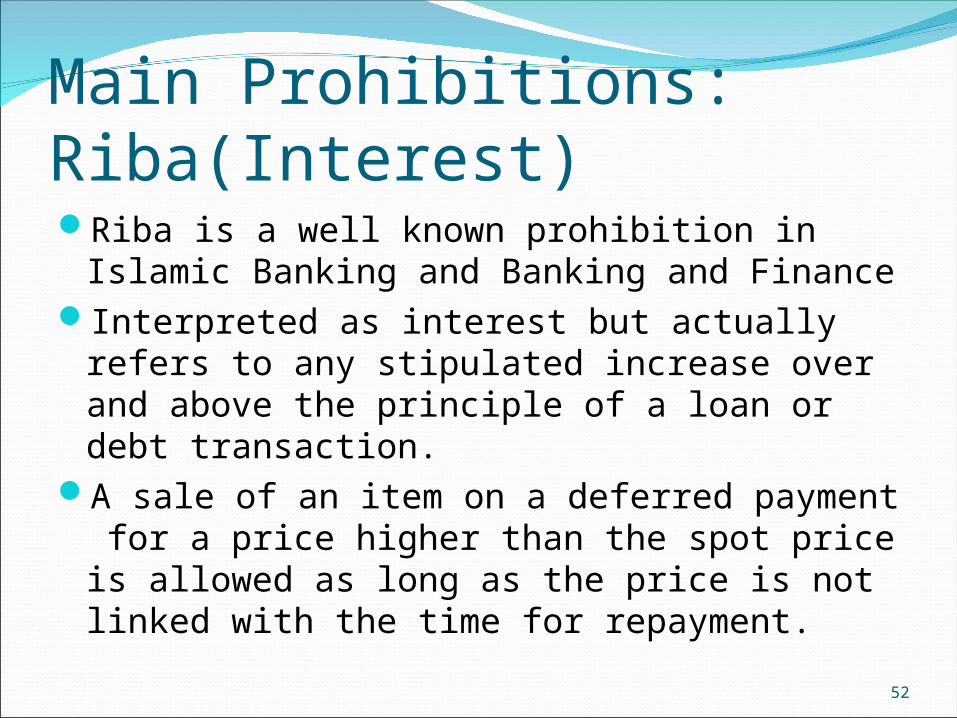

RIBA(interest)

Impermissible

ActivitiesGHARAR

(uncertainty)

Main Prohibitions: Riba(Interest)Riba is a well known prohibition in Islamic

Banking and Banking and FinanceInterpreted as interest but actually refers to

any stipulated increase over and above the principle of a loan or debt transaction.

A sale of an item on a deferred payment for a price higher than the spot price is allowed as long as the price is not linked with the time for repayment.

52

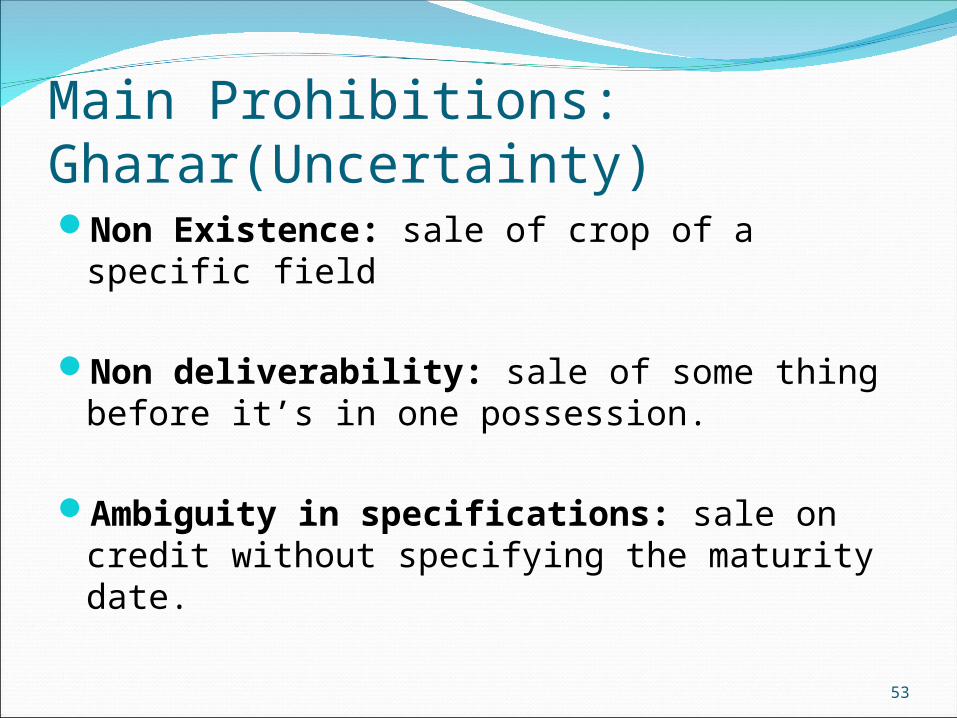

Main Prohibitions: Gharar(Uncertainty) Non Existence: sale of crop of a specific

field

Non deliverability: sale of some thing before it’s in one possession.

Ambiguity in specifications: sale on credit without specifying the maturity date.

53

Main Prohibitions: Impermissible Activities INSURANCE: conventional insurers.BANKING: banks and organizations whose principal

activity is conventional finance.ALCOHOL: producers, distributers, liquor stores,

businesses that derive income from these area(hotels).NON HALAL FOOD: producers, distributers, meat

stores, companies that are involved with handling non halal products.

GAMBLING: casinos, betting clubs and other companies that are involved in gambling.

ADULT ENTERTAINMENT: companies involved in the production or distribution of pornography.

54

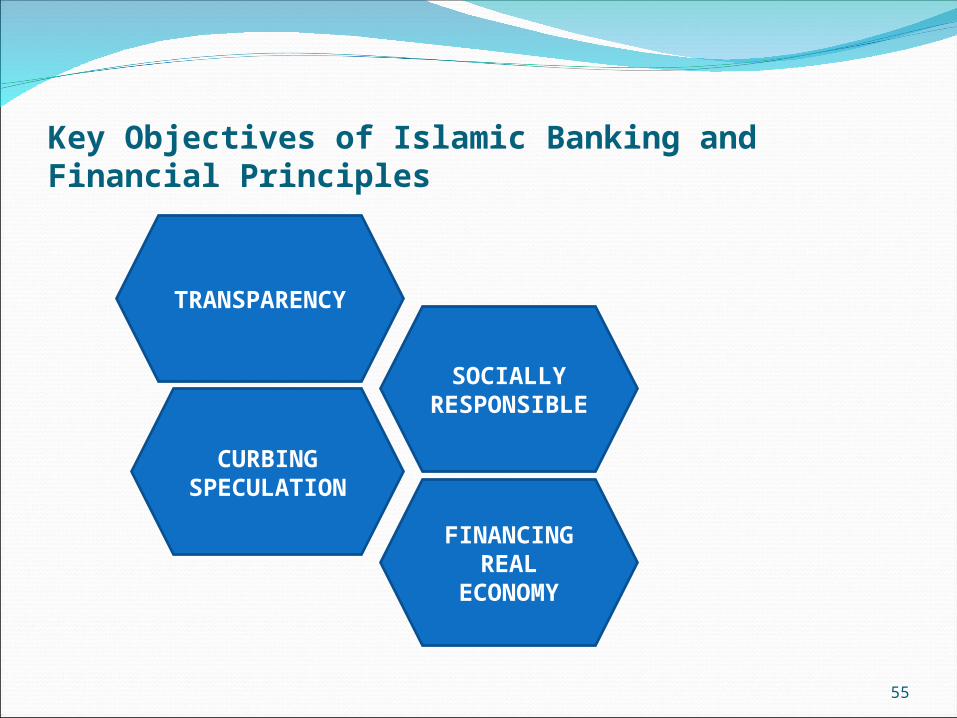

Key Objectives of Islamic Banking and Financial Principles

55

TRANSPARENCY

FINANCING REAL

ECONOMY

SOCIALLY RESPONSI

BLECURBING

SPECULATION

![10. Islamic vs. Conventional Banking[1]](https://static.fdocuments.net/doc/165x107/577ca6bd1a28abea748c0194/10-islamic-vs-conventional-banking1.jpg)