LECTURE 10 DECISION MAKING - Cloud Object...

12

LECTURE 10 – DECISION MAKING INTRODUCTION TO DECISION MAKING Characteristics of Decision Information Information accumulated for decision-making will include many characteristics, but also some that are specifically relevant to the decision-needs of managers. Cost Behaviour Many of the decision-making techniques rely on a clear understanding of the behaviour of costs. o For example, CVP analysis is based entirely on the separation of costs into their fixed and variable categories. o Also review the pitfalls of incorrectly using unit costs. If the cost we are dealing with is a fixed cost, then for most decision-making issues (product pricing is an exception) per unit fixed costs should not be used - the total amount of the fixed costs is the appropriate item. This is usually of interest when the firm is considering changing from what it is currently doing. If the cost will still be incurred if the firm makes the change, the cost is unavoidable. If the cost is not incurred if the firm makes the change, it is avoidable. o This means that avoidable costs will be relevant costs, and unavoidable costs will not be relevant costs. o Frequently, but not always, the avoidable costs are the variable costs and the unavoidable costs are the fixed costs.

Transcript of LECTURE 10 DECISION MAKING - Cloud Object...

LECTURE 10 – DECISION MAKING INTRODUCTION TO DECISION MAKING Characteristics of Decision Information

Information accumulated for decision-making will include many characteristics, but also some that are specifically relevant to the decision-needs of managers.

Cost Behaviour

Many of the decision-making techniques rely on a clear understanding of the behaviour of costs. o For example, CVP analysis is based entirely on the separation of costs into their fixed and variable

categories. o Also review the pitfalls of incorrectly using unit costs. If the cost we are dealing with is a fixed cost,

then for most decision-making issues (product pricing is an exception) per unit fixed costs should not be used - the total amount of the fixed costs is the appropriate item.

Opportunity Cost

Opportunity cost is the revenue foregone by the next-best alternative being considered. Sunk Costs

These are costs which have been incurred in the past. They do not affect future costs and cannot be changed by any current or future action.

Sunk costs are never relevant costs. A common error when doing decision-making problems is to include sunk costs in the analysis.

Marginal Costs

Marginal cost is the additional cost incurred to produce one additional unit. In accounting problems, marginal cost is frequently equated with variable cost.

Relevant Costs

A cost is a relevant cost only if the cost differs across the different alternatives being considered. o Relevant costs are also described as differential or incremental costs.

If a particular total cost is the same in both alternatives being considered, that cost does not influence the decision, and is therefore not relevant.

Whether an item is relevant or not depends on the particular decision being made. Therefore it is possible only to make one definitive rule, and for the remainder provide broad guidelines

Rule: o Past costs (sunk costs) have already been incurred and therefore are never relevant

Guidelines: o Variable costs are usually relevant costs o Sometimes fixed costs are relevant, sometimes they are not. If you are considering two alternatives, and the

total fixed costs are the same in each alternative, then fixed costs are not relevant. If they are different in the two alternatives, they are relevant.

Avoidable/Unavoidable Costs

This is usually of interest when the firm is considering changing from what it is currently doing.

If the cost will still be incurred if the firm makes the change, the cost is unavoidable.

If the cost is not incurred if the firm makes the change, it is avoidable. o This means that avoidable costs will be relevant costs, and unavoidable costs will not be relevant costs. o Frequently, but not always, the avoidable costs are the variable costs and the unavoidable costs are the

fixed costs.

Importance of the Contribution Margin

The contribution margin is an extremely important concept.

For many decisions (but as already stated, not all) the fixed costs will not change – they will be unavoidable. Therefore in many cases it is only necessary to consider whether the product/segment is contributing positively to the firm (i.e. has a positive contribution margin).

o If so, it is unlikely that the firm will be better off by dropping that product or segment. o However, each decision situation is different, and you must always consider the facts related to a

particular decision. Approaches to Quantitative Decision-Making Finance Economics Approach

A finance approach to decision-making applies discounted cash flow techniques (e.g. calculating the net present value of investment opportunities), taking into account the time value of money.

NPV analysis can be used for make-or-buy, add-or-drop, product mix decisions. o This approach provides a decision rule free from the limitations of many of the more traditional

management accounting techniques. The Management Accounting Approach

Despite the superiority of the finance approach to decision-making, the management accounting approach has some value for short term decision-making

The decision-making techniques covered in the unit are: o CVP o Product mix o Add/drop product or segment o Special order pricing o Sell at split-off or process further

In all cases care must be taken to collect all relevant quantitative data, and where appropriate, any qualitative data that is available. Often there is more than one way to approach a decision problem - Students would not be required to use

a particular method. VARIOUS DECISION MAKING SITUATIONS Product Mix Decisions

Management must continually examine operating data and decide which combination of products offers the greatest total long-run potential for the firm.

Where capacity constraints exist, the management accounting decision rule is that firms optimise income when they maximise the contribution margin earned per unit of constraining resource.

To select the most profitable mix, products are ranked by contribution margin per limiting factor and produced (subject to demand) until the scarce resource is used. The contribution margin per unit of scarce resource is calculated as follows: o Calculate the contribution margin per unit in the usual way. o Divide the contribution margin per unit by the number of units of scarce resource required to produce one unit.

Lecture Example Example: A firm produces products X, Y and Z with contribution margins of $4, $5 and $10 respectively. Machine hours required for each of the products X, Y and Z are 1 hr, 1 hr and 5 hrs respectively. The firm faces a constraint in terms of machine hours. For a particular period, machine hours available are 5,000 hours, and demand for the products is: X 1,000 Y 3,000 Z 2,000 How many units of each product will the firm produce?

WORK EXAMPLE PAGE 3 HERE

Make or Buy

The make or buy decision can be applied equally to products and services. For example, will the firm make a component part or buy it from outside; will the firm process its own payroll (MAKE) or outsource it (BUY).

Managers consider make or buy decisions for various reasons, such as: o to reduce costs o to use or free up capacity o to improve quality or delivery

The quantitative analysis consists of identifying: o Costs to buy o Costs to make o Selecting the lower cost option, though a firm is unlikely to change from one option to the other if the optimal

is only marginally superior.

Lecture Example Our firm currently makes a component, and requires 30,000 for the coming year’s production. Another supplier has offered the part at a delivered price of $3 per unit. It would cost us $3,000 to check purchased units for quality. Our unit costs for the past year were: DM $1.25 DL .60 Var OH .50 Fixed OH $1.00 $3.35 If the component was bought, fixed overhead would be reduced by $6,000, the cost of leasing specialised equipment. The space vacated by the equipment can be rented for $4,000 for the year. Consider relevant costs only. Which option is cheaper, and by how much? What is the correct decision?

WORK EXAMPLE ON PAGE 4 HERE. Indifference Point

The analysis above is of limited usefulness unless the firm always produces 30,000 units.

A more general decision rule could be obtained by using the “point of indifference”. This technique is useful where the options being considered include combinations of fixed and variable costs, as is the case here: o Costs of make are fixed $6,000 + variable $2.35 unit o Costs to buy are fixed -$1,000 + variable $3 unit

The point of indifference is the level of activity where the firm is indifferent between two options being considered. The firm would be indifferent at the point where profits or costs are the same under both.

At the point of indifference, any fixed costs are covered, which means that if activity is above the point of indifference, the firm incurs additional variable costs only, and no additional fixed costs. It is therefore possible to conclude that the firm will always prefer:

o The lower variable cost option if activity is above the point of difference o The lower fixed cost option if activity is below the point if indifference

In this example, “make” has the lower variable cost therefore would be selected for activity above the point of indifference. “Buy” has the higher variable cost and the lower fixed cost and would be selected for activity below the point of indifference.

Calculating the Indifference Point

WORK EXAMPLE PAGE 5 HERE

The qualitative analysis involves considering factors such as the following: o Buying increases uncertainty, in particular with respect to timely availability of the component or service o Buying also surrenders control over product and service design, quality etc. o Effect on employee morale if a decision to buy means putting off staff o Consideration re use of capacity. If we are going to change to “make” do we have the capacity? If we move

to “buy”, what use is to be made of existing capacity? etc. o Is there a need for particular expertise or specialised equipment? o Customer expectations, in particular if we currently “make” and are going to change to “buy” o If buying, analysis will have been made on a quoted price. How likely is it that the supplier will continue to

supply at that price? o How reliable is the supplier with respect to correcting faulty items? o Position of the firm after the period considered in the analysis. Most management accounting analyses of

this type are not into perpetuity, and therefore the firm must consider the cost of converting back to "make" if the "buy" option does not continue to be optimal.

Add/Drop Products/Segments

In this section we consider techniques used to decide whether the firm should: o Add a product/segment or retain existing number of products/segments, OR o Drop a product/segment or retain existing number of products/segments

Firms will benefit by the timely identification of products or entire business segments (i.e. an entire department/section/division) which should be eliminated or extended (added).

The discussion in this section focuses on dropping (as distinct from adding) an item however similar principles apply to adding products or segments.

Ideally, management should have access to data which would signal a product-line or service-line in trouble, such as:

o decreasing market share o reports of a superior competitive product o consistent lowering of sales price to maintain sales

While firms must be on the look-out for "non-performing" products, a product or service should not be discontinued merely because it reports a loss on the firm’s segment financial reports.

o The loss could result from allocated costs (usually, but not always, fixed costs) that will not be avoided by eliminating the product, and therefore those costs are irrelevant to a decision about whether to drop the product.

If, as is often the case, fixed costs will not be reduced by dropping the product, then fixed costs are not relevant, and the decision rule is if the product has a positive contribution margin, do not drop the product.

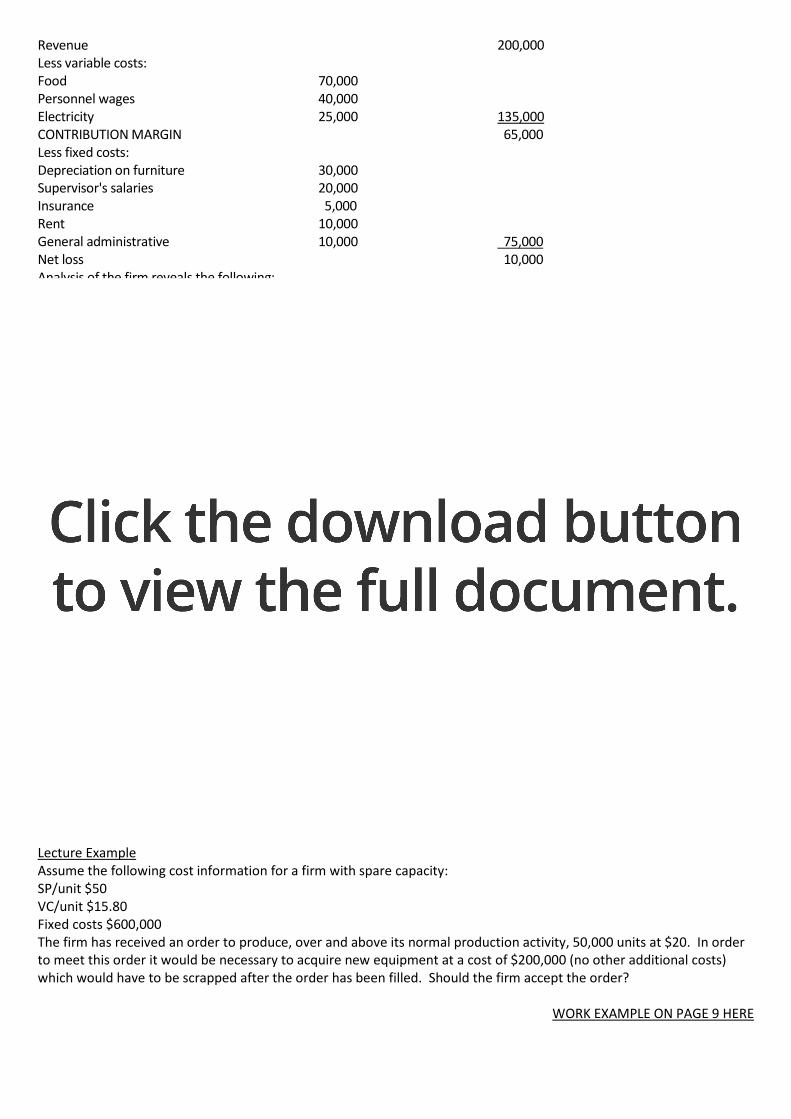

LECTURE EXAMPLE The managing director of Wallaby Airlines is concerned about the profitability of its World Hoppers Club (extract from profit statement shown below) and is considering closing it down: Questions: (a) Should the club close? (b) How much worse/better off would Wallaby Airlines be if the club closed?

Revenue 200,000 Less variable costs: Food 70,000 Personnel wages 40,000 Electricity 25,000 135,000 CONTRIBUTION MARGIN 65,000 Less fixed costs: Depreciation on furniture 30,000 Supervisor's salaries 20,000 Insurance 5,000 Rent 10,000 General administrative 10,000 75,000 Net loss 10,000 Analysis of the firm reveals the following: (1) If the Club was closed, some staff would be dismissed and others would be transferred to another section. This

would result in a reduction of half the staff costs in each salary type (personnel and supervisors) above. (2) Rent and general administrative costs have been allocated to the Club. The total amount of these items would not

change if the Club was closed. (3) All other costs will be avoided if the Club is closed down.

WORK EXAMPLE ON PAGE 7 HERE

Where the quantitative decision is in favour of dropping the product or division, a final decision should not be made without considering qualitative factors such as:

o the effect on other products (e.g. customers may prefer to buy from a supplier carrying all product lines) o alternative use of space o effect on the firm's image o effect on employee morale o potential openings for competitors o flexibility to re-introduce the product if future circumstances change

Product Pricing Special Order Pricing

The assumption behind this decision-making situation is that existing sales will continue. In such a case, fixed costs will only be relevant if they would increase because of the additional production required. Otherwise fixed costs will be covered by regular sales at the normal price, and so can be ignored.

In the following example the fixed costs are relevant, but in many cases of special-order pricing the only relevant costs will be the variable costs associated with the special order

The question will be phrased either as: (1) what price should we charge for the special order?, or

(2) should we accept the special order at this price?

If (1) the decision rule is: price the sale to cover incremental costs (usually variable but may include fixed as well).

If (2) the decision rule is: accept the sale at a reduced price if the firm earns a profit from the sale. Lecture Example Assume the following cost information for a firm with spare capacity: SP/unit $50 VC/unit $15.80 Fixed costs $600,000 The firm has received an order to produce, over and above its normal production activity, 50,000 units at $20. In order to meet this order it would be necessary to acquire new equipment at a cost of $200,000 (no other additional costs) which would have to be scrapped after the order has been filled. Should the firm accept the order?

WORK EXAMPLE ON PAGE 9 HERE

Sell at split-off or process further

In some manufacturing processes, firms have to choose between selling an item at split-off-point as an intermediate product, or processing it further and selling it in its refined state.

Lecture Example From the joint processes lecture example last week, Apple Juice had been sold at split-off-point for 70c litre. Assume the firm had used the physical measures of joint cost allocation, which resulted in a joint cost of 80c per litre being transferred to the product Apple Juice. Now assume the firm is investigating the processing Apple Juice further into Apple Juice Plus. This would cost an additional $.20 litre and would sell for $.95 litre. Should the firm sell at split-off, or process further?

WORK EXAMPLE ON PAGE 10 HERE

TUTORIAL QUESTIONS QUESTION 1 Determine the number of cartons sales of V1, V2 and V3 which will optimise profit for the firm, given the constraints of the following problem: Karl's Kitchens is experimenting with different vinegars for sale on the domestic market. The contribution margins per carton for three types (cleverly called V1, V2 and V3) are $120, $100 and $150 respectively. The firm is constrained in terms of labour hours, and the labour hours required per carton of each type of vinegar is 2 hours, 1.5 hours and 3 hours respectively. Assume the firm has 2,240 available labour hours per month, and the monthly demand is 1,200 cartons of V1, 800 cartons of V2 and 300 cartons of V3. QUESTION 2 The Mid-West Division of Ceebee Company currently manufactures all of the components of its product. As a cost reduction strategy it is investigating the possibility of outsourcing the provision of component MTR-2000. Marley Manufacturers will supply the 32,000 units required for year 2002 for $17.30 a unit. Current production costs for annual production of 30,000 units are: Direct materials $7 unit Direct labour $4.20 unit Factory rental space $84,000 Equipment leasing costs $36,000 Other manufacturing overhead $225,000 The facilities currently used to manufacture MTR-2000 are rented under a month to month agreement. If MTR-2000 is not manufactured in-house the firm would have no need for this space. Special equipment is required to produce MTR-2000. The equipment lease can be terminated by paying one month's lease payment for each year left on the lease. There would be 2 years left at the time of change should the firm decide to outsource. 40% of the other manufacturing overhead is variable and varies with the number of components produced. The fixed overhead will not change whether MTR is produced internally or outsourced. Required:

Calculate the relevant costs of the two options, and decide whether the firm should continue production or outsource.

Assume the firm is not certain of its level of output, and wants a more general decision rule. What will that decision rule be?

QUESTION 3 The most recent Profit and Loss Statement (in ‘000s dollars) for a firm follows:

Product A Product B

Sales 195 500 Less COGS: Variable 100 210 Fixed 45 90 Less selling costs: Advertising 15 40 Sales salaries 30 40 Less administrative costs: Office salaries 15 30 Depreciation 2 6 Rent 1 5 Bad debts 2 3 NET PROFIT (LOSS) (15) 76 Other information:

1. The salesperson for product A would be retrenched. Apart from the direct labour associated with product A, no other personnel changes would occur.

2. Bad debts are related directly to the product whose sale incurred the bad debt. 3. An analysis of advertising expenditure revealed that some costs were incurred specifically for a particular

product. These were $10,000 to Product A and $20,000 to Product B. The remaining advertising costs were not related to product, and were allocated arbitrarily.

4. Fixed overheads were allocated according to the direct labour hours spent on each product. Product B requires twice as much time as product A.

5. If Product A is dropped the firm will not be able to sub-lease the available floor space because of security risks. 6. It is not expected that any equipment used in manufacturing or administration will be retired if Product A is

dropped. Required: (a) Calculate the profit for the firm with product A, and without product A. (b) On the basis of your answer to (a), should the firm drop product A? (c) From the solution, indicate a simpler decision rule which results in the same decision as you arrived at in (b). (d) Students to work through on their own if they want to. Not to be covered in tutorial: Show an incremental

analysis to determine the financial effect of dropping product A.

PRACTICE QUESTIONS QUESTION 1 A firm is making a decision about whether to outsource its printing cost. The firm can incur the fixed costs of the function of $21,000 for the period. Alternatively the firm has an option of outsourcing the function at a cost of $3.50 per unit. At what level of units would the division be indifferent between the two proposals. Should the firm outsource the function? QUESTION 2 Details of three products produced by a firm follow:

Product CM per unit Machine hours required per unit Estimated demand in units

Lever Spring Pump

$20 $30 $10

5 hours 5 hours 1 hour

1,000 units 500 units 2,000 units

If the firm has a constraint of 9,000 machine hours available for the period, calculate the number of units of each product that would be produced to maximise profits. QUESTION 3 A firm produces multiple products. Total fixed costs of production are $10,000. Manufacturing costs per unit related to one of the firm’s products (a component part, used within the firm and also sold outside for a selling price of $20) are: DM $5 DL $4 V OH $3 F OH $2 The firm has received an offer from an external supplier to supply 1,000 units per period for a price of $12.25. If the firm accepts this offer, total fixed costs will be reduced by $500 (in other words, it is possible to identify $500 fixed costs associated with the production of the component being discussed.). (a) Calculate the price difference between continuing to manufacture, and outsourcing the 1,000 units. (b) Calculate the minimum selling price the firm would be prepared to set for the component as a special order

price, assuming the firm has spare capacity. (c) Calculate the point at which the firm is indifferent between making the product ourselves, or buying it from the

external supplier. (d) State your answer in terms of a decision rule for the firm, e.g. “above (the point of indifference) the firm would

prefer …., and below (etc)”.

QUESTION 4 Oldfield Engineering manufactures small engines used by manufacturers of lawn mowers and garden mulchers. The firm currently manufactures all the components used in these engines but is considering a proposal from an external supplier who wishes to supply the starter assemblies used in these engines. The starter assemblies are currently manufactured in Division 3 of Oldfield Engineering. The costs relating to the starter assemblies for the past 12 months were as follows:

Direct Materials $200, 000

Direct Labour 150,000

Overhead 400,000

Total $750,000

Production for the past year was 150,000 starter assemblies. The average cost for each starter assembly is $5 ($750,000 / 150,000). Other information: Of the total manufacturing overhead, only 25% is considered variable. Of the fixed portion, $150,000 is an allocation of general overhead that will remain unchanged for the firm as a whole if production of the starter assemblies is discontinued. A further $100,000 of the fixed overhead is avoidable if production of the starter assemblies is discontinued. The balance of the current fixed overhead, $50,000, is the division manager’s salary. If production of the starter assemblies is discontinued, the manager of Division 3 will be transferred to Division 2 at the same salary. This move will allow the company to save the $40,000 salary that would otherwise be paid to attract an outsider to this position. (a) The external supplier will supply starter assembly units at $4 per unit. Because this price is less than the current

average cost of $5 per unit, the vice president of manufacturing is eager to accept this offer. On the basis of financial considerations alone, should the outside offer be accepted? (You should consider that production output in the coming year may be different from production and output in previous years).

(b) How, if at all, would your response to requirement (a) change if the company could use the vacated plant space

for storage and thereby avoid $50,000 of outside storage charges currently incurred? Is this information relevant or irrelevant – explain.

TEXT QUESTIONS Ch.11, questions 34, 35

QUESTION 5 Paul’s Cycles produces all types of bicycles. This year’s expected production is 10,000 units. Currently, Paul’s makes the chains for its bicycles, and the following are costs for making the 10,000 bicycle chains:

Cost per Unit Costs for 10,000 Units

Direct materials $4.00 $ 40,000

Direct labour $2.00 $ 20,000

Variable overhead (power and utilities) $1.50 $ 15,000

Inspection, setup, materials handling $ 2,000

Machine rent $ 3,000

Allocated fixed costs of administration, taxes and insurance $ 30,000

Total Costs $110,000

Paul’s has received an offer from an outside vendor to supply any number of chains at $8.20 per chain. The following additional information is available:

Inspection, setup and materials-handling costs vary with the number of batches in which the chains are produced. Paul’s produces chains in batch sizes of 1,000 units. The 10,000 units will be produced in 10 batches.

Paul’s rents the machine used to make the chains. If chains are bought from the outside vendor, Paul’s does not need to rent this machine.

(a) Assume that if Paul’s purchases the chains from the outside supplier, the facility where the chains are currently made will remain idle. On the basis of financial considerations alone, should Paul’s accept the outside supplier’s offer at the anticipated production (and sales) volume of 10,000 units?

(b) Assume now that if the chains are purchased outside, the facilities where the chains are currently made will be used

to upgrade the bicycles by adding mud flaps and reflectors. As a consequence, the selling price of bicycles will be raised by $20. The variable cost per unit of the upgrade would be $18, and additional tooling costs of $16,000 would be incurred. On the basis of financial considerations alone, should Paul’s make or buy the chains, assuming that 10,000 units are produced and sold)? Show your calculations.

(c) Paul’s sales manager is concerned that the estimate of 10,000 units may be high and believes that only 6,200 units

will be sold. Production will be cut back, freeing up work space. This space can be used to add the mudflaps and reflectors whether Paul’s buys the chains or makes them in-house. At this lower output, Paul’s will produce the chains in eight batches of 775 units each. On the basis of financial considerations alone, should Paul’s purchase the chains from the outside vendor?

QUESTION 6 On the night of 1st August 1996, Kooyong Klassic Kompany’s premises were flooded, resulting in zero production activity for one week. You are required to select relevant information from the following, estimate the cost of the week’s loss of production, and briefly comment on the estimate you have calculated. Normal weekly production and sales was 500 units at a selling price of $20 per unit. Costs per unit were: Direct materials $6 Direct labour $2 Variable overheads 30cents

Selling costs 20cents Fixed overhead $5

Overhead rates are based on annual normal capacity of 24,000 units. An analysis of the fixed overhead revealed:

$4,000 of fixed overheads relate to straight-line depreciation of equipment which is not being used during the week

$40,000 is the salary of the plant supervisor who uses the week to provide training for employees in-house rather than sending them on an external course. The net savings of running the course in-house are $1,000

$50,000 relates to items such as rent, rates, insurances etc which are not related to production activity levels

Half of the remaining amount of fixed overhead , which it has been classified as fixed overhead, actually is a weekly charge for power. The weekly charge is only paid if production exceeds 100 units for the week

Other information: The nature of the awards in place are such that because the stoppage is for one week only, direct labour employees are paid their normal wage. They spend the week attending the training course discussed above.