Leasing Industryin Poland

19

Leasing Industry in Poland Leasing Life European Conference Warsaw 2014 Mieczysław Woźniak Vice Chairman of the Polish Leasing Association

Transcript of Leasing Industryin Poland

Leasing Industry in PolandLeasing Life European ConferenceWarsaw 2014

Mieczysław Woźniak

Vice Chairman of the Polish Leasing Association

3.1 3.3

1.6

1.6 1.5

1.6

1.0

Leasing defined

in the Tax Law

Leasing defined

in the Accounting LawWorld economic crisis starts

New Business Forecast

Polish leasing market 1995 – 2013 milestones

Begining of 2007-2013 EU

budget perspective

1.5 2.5 4.06.0

8.0 7.8 6.3 7.510.5 11.8

13.7

19.6

29.6 29.8

20.9

25.729.5 29.8

33.7

40.0

1.0

1.7 1.21.4

0.8

0.61.9

2.5

2.02.1

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Movables Real Estate

Leasing defined

in the Civil Code

Year 1995 2013

New business PLN 1 500m PLN 35 300m

Ranking in the European Leasing Market 16 8

Share of leasing in investment financing 4,5% 14,4%

1995-2013 snapshot. Key changes & developments

No. of leasing companies 102 32

Top 10 companies (market share) 71,5% 66%

Bank-owned companies in Top 10 4/10 10/10

2,031

3,050 3,274

2,073

1,595

1,629 1,468

1,631

594

PLN 296,27bn

Almost PLN 300bn of investment was financed by leasingsince 2004

11,82213,716

19,630

29,597 29,791

20,923

25,69629,513 29,758

33,66930,4211,930

2,458

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 I-IX 2014

Movables Real Estate

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

Jan Jun Nov Apr Sep Feb Jul Dec May Oct Mar Aug Jan Jun Nov Apr Sep Feb

89,6 mld

49.856.6 56.5 54.9 53.4 55.3 55.9

61.1 60.8 61.5 62.1 64.571.4

1.8%

13.7%

-0.2%-2.8% -2.8%

3.6%0.9%

9.4%

-0.5%1.3% 0.9%

3.9%

10.7%

Jun Dec Jun Dec Jun Dec Jun Dec Jun Dec Jun Dec Jun

Leasing market O/S (Total market)O/S of investment loans

Importance of leasing vs. investment loans

07 07 07 08 08 09 09 09 10 10 11 11 12 12 12 13 13 14

Investment loans (mld PLN) Deposits/Loans ratio for companies

Jun '08

Dec '08

Jun '09

Dec '09

Jun '10

Dec '10

Jun '11

Dec '11

Jun '12

Dec '12

Jun '13

Dec '13

Jun '14

Total lease market (PLN bln) change as to the previous period

43.948.4 47.7 47.3 45.4 47.8 48.0

52.4 52.4 53.4 53.356.5

63.4

16.2%

10.2%-1.4% -0.9%

-3.9%

5.2%0.5%

9.1%

-0.1%2.0%

-0.3%

6.0%

12.2%

Jun '08

Dec '08

Jun '09

Dec '09

Jun '10

Dec '10

Jun '11

Dec '11

Jun '12

Dec '12

Jun '13

Dec '13

Jun '14

Leasing market O/S (Movables)

Movables lease market (PLN bln) change as to the previous period

5.9

8.2 8.8 7.6 8.0 7.5 7.9 8.7 8.4 8.1 8.8 8.0 8.0-47.0%

39.0%

7.3%

-13.6%

5.3%

-6.3%

5.3%10.1%

-3.4% -3.6%

8.6%

-9.1%0.0%

Jun '08

Dec '08

Jun '09

Dec '09

Jun '10

Dec '10

Jun '11

Dec '11

Jun '12

Dec '12

Jun '13

Dec '13

Jun '14

Leasing market O/S (Real Estate)

Real Estate lease market (PLN bln) change as to the previous period

Market structure by type of players

Akf leasing Polska S.A.

BGŻ Leasing Sp. z o. o.

BNP Paribas Lease Group Sp. z o. o.

BZ WBK Leasing S.A.

Caterpillar Financial Services Poland Sp. z o. o.

De Lage Landen Leasing Polska S.A.

Deutsche Leasing Polska S.A.

DnB Leasing Sp. z o. o.

Mercedes-Benz Leasing Polska Sp. z o.o.

Millennium Leasing Sp. z o.o.

mLeasing Sp. z o.o.

NOMA2 Sp. z o.o.

ORIX Polska S.A.

Pekao Leasing Sp. z o.o.

PKO Leasing S.A.

Polski Związek Wynajmu i Leasingu Pojazdów

15%

(by value of new business)

DnB Leasing Sp. z o. o.

Europejski Fundusz Leasingowy S.A.

Getin Leasing S.A.

Grupa Masterlease

Handlowy-Leasing Sp. z o. o.

Idea Leasing S.A.

IKB Leasing Polska Sp. z o. o.

Impuls-Leasing Polska Sp. z o. o.

ING Lease (Polska) Sp. z o. o.

Polski Związek Wynajmu i Leasingu Pojazdów

Raiffeisen-Leasing Polska Sp. z o.o.

Scania Finance Polska Sp. z o.o.

SG Equipment Leasing Polska Sp. z o.o.

SGB Leasing Sp. z o.o.

Siemens Finance Sp. z o.o.

VB Leasing Polska S.A.

VFS Usługi Finansowe Polska Sp. z o.o.

Volkswagen Leasing Polska Sp. z o.o.

85%

Captives Bank-owned

23%

31% 31% 32%

36%

Leasing share in Investments

22,0%

EUROPE 2013

Share of leasing in investment financing in Poland

2% 1% 1% 1% 1%

10.5%12.6% 13.1% 12.7%

14.4%

2009 2010 2011 2012 2013

Movables Real Estate Total

12,5%

1,5%

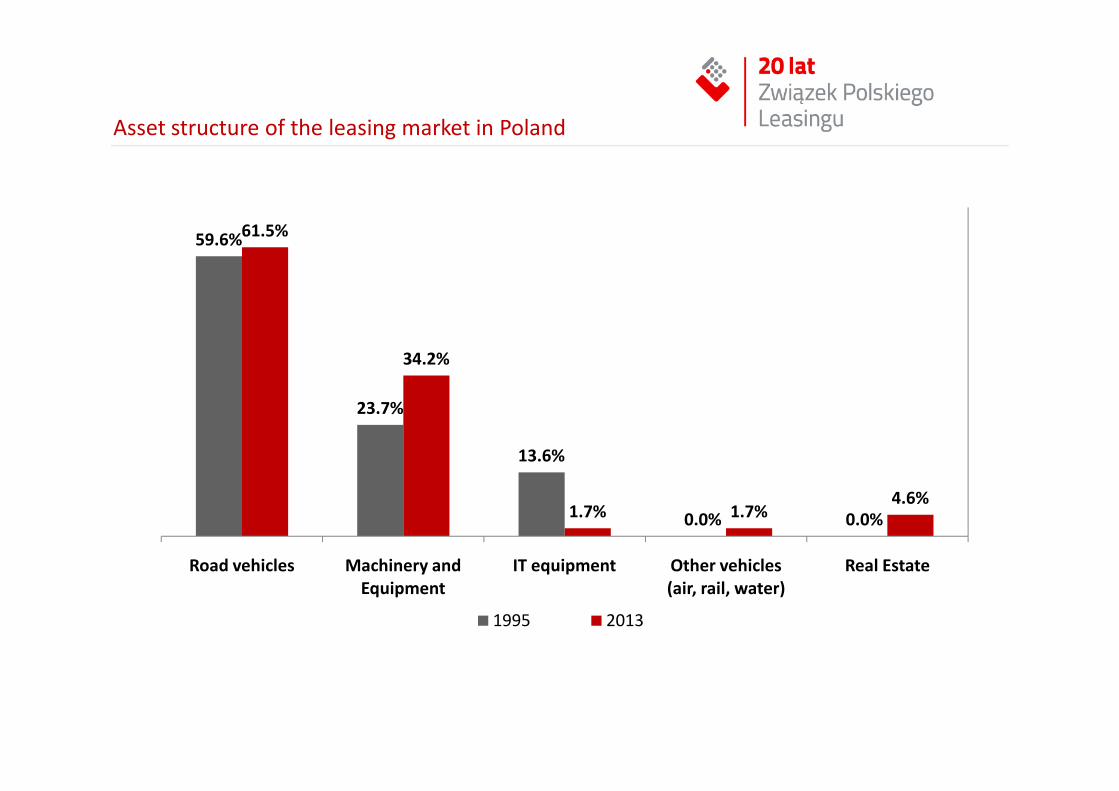

59.6%

23.7%

61.5%

34.2%

Asset structure of the leasing market in Poland

23.7%

13.6%

0.0% 0.0%1.7% 1.7%4.6%

Road vehicles Machinery and

Equipment

IT equipment Other vehicles

(air, rail, water)

Real Estate

1995 2013

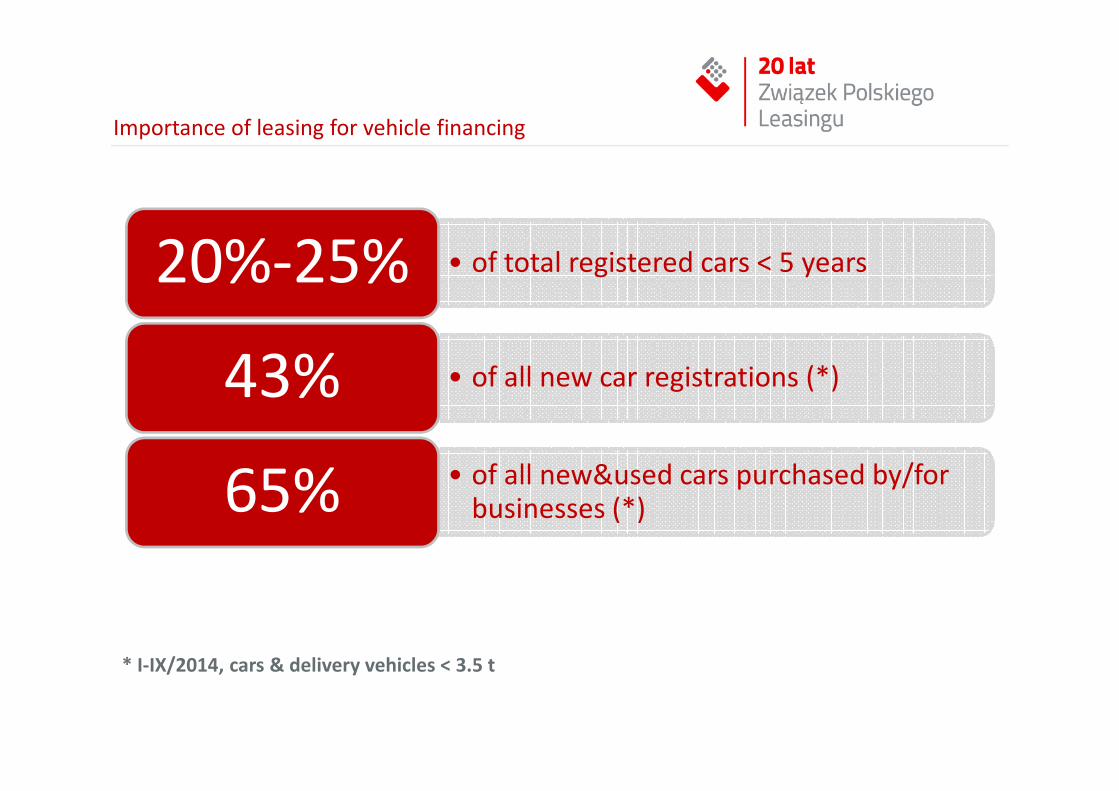

• of total registered cars < 5 years20%-25%

• of all new car registrations (*)43%

Importance of leasing for vehicle financing

43%

• of all new&used cars purchased by/for businesses (*)65%

* I-IX/2014, cars & delivery vehicles < 3.5 t

5.5%

14.0%

14.4%

27.9%

Medical

Construction

Plastics production and metalwork

Agricultural

(by type of machinery and equipment)

Structure of new leasing business for machinery & equipment

I-III Q 2014

26.9%

1.4%

2.9%

3.4%

3.6%

5.5%

Other

Catering

Food industry

Forklift trucks

Printing

Medical

31.2% 28.3%

16.7% 18.6%

15.5% 13.8%

Investment financed in 2010 and 2011, all SMEsCash/Equity Bank Loans

Leasing Other debt

Proportion of investment financed by:

The relevance of leasing financing in the European SME sector

36.7% 39.4%

2010 2011

Source: Oxford Economics/EFG

Facts and figures on SME financing in Europe:

� €224 bn total new business volume in 2011 with €110 bn fueling SMEs,� Representing roughly 19% of total investment finance for SMEs

302,449

381,830 373,616 355,376387,185 379,463

2008 2009 2010 2011 2012 2013

Number of clients

Source: GUS

Number of active leasing customers in Poland

28.4%

51.1%

64.3%

Micro Small Medium

Leasing penetration in SME segment (2009-2013)

Source: Monitoring kondycji sektora MMŚP w 2014 r (CBOS)

| 14

| 15

3.00%

3.50%3.45%

3.25%

3.00%

2014f 2015f 2016f 2017f 2018f

GDP Y/Y

0.20%

1.20%

2.00%

2.50% 2.50%

2014f 2015f 2016f 2017f 2018f

CPI (average)

Macroeconomics forecast – Poland

2.70%

-9.70%-6.30%

-0.10%

6.40% 6.5%

14.9%17.6%

9.6%

-1.2% -0.4%

8.5%

-1.6%-0.2%

7.0%8.7%

7.0% 6.0% 5.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014f 2015f 2016f 2017f 2018f

Investment Y/Y

2012 vs. 2014 Leaseurope Annual Convention concludingremarks

2012 Annual Convention

2014 Annual Convention2014 Annual Convention

Our concluding remarks Key challenges of the industryfor the years to come

• Megatrends (urbanisation, demographics, social & cultural changes, connectivity, integrated mobility & transport solutions)

• Technological changes (big data, 3-D printing, etc.)

• Increasing share of service solutions, service component, specialists

• Collaborative economy and sharing societies, crowdfunding, asset sharing

• Consumer leasing vs social and cultural changes

• Ability to absorb and retain talents

• Constantly increasing regulatory & compliance requirements

D z i ę k u j e m y z a u w a g ę

ul. Rejtana 17 lok 21,

02-516 Warszawa

tel.: +48 22 542 41 36

fax: +48 22 542 41 37

E-mail: [email protected]

www.leasing.org.pl