Lease the Illinois Tollway? Public Ownership is BetterWhite+Paper... · Lease the Illinois Tollway?...

23

Lease the Illinois Tollway? Public Ownership is Better Transportation for Illinois Coalition White Paper ____________ January 2008

Transcript of Lease the Illinois Tollway? Public Ownership is BetterWhite+Paper... · Lease the Illinois Tollway?...

Lease the Illinois Tollway?Public Ownership is Better

Transportation for Illinois CoalitionWhite Paper____________January 2008

Lease the Illinois Tollway?Public Ownership is Better

Transportation for Illinois CoalitionWhite Paper

Researched & Written byLinda WheelerFormer Director of the Office of Planning &Programming for the Illinois Department of Transportation

________________________

Contents

Executive Summary ................................................................. 2Overview ................................................................................... 5Public Policy Issues .................................................................. 6Analysis by Credit Suisse ...................................................... 10Critical Factors Affecting Lease Value ................................ 12Comparison: Public Opinion Vs. Privatization .................. 19Conclusion .............................................................................. 21

The Transportation for Illinois Coalition is a diverse group of statewide and regional business,organized labor, industry, governmental and not-for-profit organizations that has joined together ina united and focused effort to support a strong transportation alliance for Illinois. The coalitiontakes a comprehensive approach and seeks to speak with one voice for all of Illinois regardingtransportation funding needs at both the state and federal levels. The coalition believes thattransportation is critical to the economy of Illinois. This comprehensive approach involves allmodes of transportation, including rail, air, water, highways and mass transit.

1

ExecutiveSummary

Executive SummaryOverviewPublic Policy IssuesAnalysisCritical FactorsComparisonConclusion

Executive Summary2

ith the growing need for transportationimprovements outstripping availableresources, there has been nationwide interestin innovative funding methods. One of those

methods is public/private partnerships. In Illinois, attentionhas been given to the possibility of leasing the IllinoisTollway as a means to raise money for the state.

In examining that concept, the Transportation for IllinoisCoalition (TFIC) has identified a series of policy issueswhich would need to be resolved, has reviewed the tollwayprivatization study prepared for the Illinois Commission onGovernment Forecasting and Accountability (CGFA), andhas assessed additional factors not included in that study.

While leasing the tollway to a private partner could raisesubstantial amounts, such sums would require very longleases and continuous toll increases throughout the leaseperiod. Further, the proceeds from a lease could besubstantially less if various options were included, such as:a toll freeze for a portion of the lease period; not allowing anon-compete clause; or adding a requirement for theprivate partner to fund future toll road improvementsincluding reconstruction, additional lanes and extensions.Finally, TFIC has analyzed a public option, i.e., keepingthe toll road public but raising tolls in the same manner asthe privatization option would. TFIC has concluded thatthis public option is more efficient in that it would generategreater funding for transportation improvements. Orconversely, through more modest toll increases, the publicoption can generate substantial amounts for neededtransportation improvements.

Based on all these factors, TFIC has concluded that publicownership of the existing toll road system is a betteroption.

Key points from the TFIC review include:

■ The Illinois Tollway is a critical component of thestate’s and especially northeast Illinois’ transporta-tion network, stretching for 274 miles and serving1.3 million drivers every day. No action should beallowed which would put at risk the continuedefficient operation of this vital asset.

■ Any funds which are generated from the toll roadmust be used for transportation purposes.Illinois toll roads were paid for by the users;their payments should not be diverted tonon-transportation purposes.

■ It appears that leasing the toll road to a privatepartner could generate as much as $5 billion to$18 billion for the state, after outstanding bondswere defeased. Tempering these sizeable estimatesare the following factors:

— To generate such amounts, leases would haveto last for at least 50 years; the $18 billionestimate required a 75-year lease.

— To generate such amounts, toll increases wouldhave to begin immediately and occur everyyear; the $18 billion estimate required a 50%toll increase every 20 years plus a 3% increaseannually.

— These estimates do not include any funding formajor capital improvements beyond thosecurrently underway as part of the toll roads

Executive Summary 3

Congestion-Relief Program (CRP). During a50 or 75-year lease term, needed majorimprovements to the toll road not accounted forin these lease estimates include reconstruction,adding lanes, and building extensions, such aswestern access to O’Hare. Including theseimprovements in the lease would reduce itsvalue by as much as $4.5 billion. (It should benoted that once the first toll road segment wasin place, the construction of all subsequent tollroads and extensions has been cross-subsidizedby toll revenues from the existing system. Akey concern of any lease discussion has beenthe need to preserve this financing method forfuture toll road needs.)

— These estimates do not include any provisionfor a toll rate freeze during the early years ofthe lease. While some have suggested includ-ing such a freeze, it also would reduce thevalue of any lease payments - by as much as$3.2 billion for a 10-year freeze. Further, at theend of the freeze period, tolls would have to beraised by as much as 100% to reach the levelthe tolls would have been had they beenincreased annually.

— These estimates assume a non-competeclause, under which the region would haverestrictions on expanding or constructingnearby facilities which could draw trafficfrom the toll road. But, northeast Illinoishas a continuing need to expand its transitand highway facilities to serve growingtransportation demand. A non-competeclause could jeopardize such projects.

— These estimates assume a one-time upfrontpayment. Extending the payments throughthe life of the lease would ensure anongoing revenue source for transportationimprovements. Further, it would avoid asituation where motorists continued to seeannual toll increases long after the upfrontlease payment had been spent. With themost aggressive toll increase regime (the$18 billion lease scenario), such annualpayments would amount to $550 million,assuming the lease included a 10-year tollfreeze and funding for future major tollroad improvements.

— If the toll road were to stay public and toadopt the same aggressive toll increaseschedule as a private partner, it couldgenerate as much as $97 billion (net presentvalue) for additional transportation im-provements over a 75-year period. Whilethe Illinois Tollway would be very unlikelyto adopt such an aggressive toll increaseschedule, it has adopted modest increases asnecessary for toll road improvements. Themost recent of these increases, which wentinto effect in 2005, is funding a $5.3 billionCongestion-Relief Program, including thenewly-constructed I-355 extension.

If the toll road were to staypublic and to adopt the sameaggressive toll increaseschedule as a private partner,it could generate as much as$97 billion (net present value)for additional transportationimprovements over a 75-yearperiod.

Executive Summary4

■ Keeping the toll road public would:

— Avoid the continuous toll increases necessaryfor a private lease arrangement; although, withsuch increases, public sector could generateeven more funding than private sector fortransportation improvements.

— Avoid the loss of direct control for the 50 to75-year lease term. Because it is impossible toforesee what transportation changes orimprovements would be needed during such alengthy time, it would be important for anylease to include potentially expensive provi-sions for re-opening and modifying thecontract.

— Assure that user fees were re-invested in thetransportation system and not diverted to otheruses.

— Assure that the toll road continued to complywith current (and future) statutes on labor,environment, competitive bidding, etc. Whilesuch compliance could be included in a lease,it would affect the value of the lease to aprivate partner.

— Assure that the toll road continued to bemanaged as an integral part of the overalltransportation network, including coordi-nated planning, coordinated scheduling ofmaintenance and construction activities,cooperation with transit operations andextensions, and other activities to supportnortheast Illinois’ overall transportationgoals. That also would include the consid-eration of traffic diversions that wouldresult from toll increases. The larger thetoll increase, the greater the potential fortraffic diversions, which could pose aproblem for congested local and arterialroads in northeast Illinois.

— Avoid the conflict between the public’sright to know and private sector’s need tokeep information confidential that typicallyoccurs in negotiating a privatization deal.

While leasing toll roads to a private partner may workin some locations, for the Illinois Tollway it is thewrong option – creating numerous policy challenges,likely to be costly to consumers and likely to be lessefficient than keeping the toll road publicly operated.

OverviewExecutive SummaryOverviewPublic Policy IssuesAnalysisCritical FactorsComparisonConclusion

Overview 5

ationwide, as transportation capital costs haveovertaken available funding, a number ofareas are considering innovative ways togenerate additional revenue. One of those

ways is through the lease of an existing transportationasset to a private partner. In exchange for payments fromthe private partner, the public agency enters into a long-term concession or lease arrangement giving the privateentity the right to operate the facility, to raise and collecttolls on it and to keep the profits from the operation. Thatis what the City of Chicago did with the Chicago Skywayand what Indiana did with the Indiana Toll Road.

In Illinois, there has been discussion about the possibilityof entering into a public/private partnership to lease theIllinois Tollway. During 2006, there were legislativehearings on the issue; state legislation was proposed toallow public/private partnerships; and the IllinoisCommission on Government Forecasting andAccountability (CGFA) commissioned a study by CreditSuisse which examined privatizing the Illinois Tollway.

This paper examines the issue of leasing the IllinoisTollway to a private entity. It includes the followingsections:

■ Public Policy Issues: Identifies 11 public policyissues that need to be examined when considering atoll road lease; decisions on these issues wouldhave significant impact on the value of a lease to aprivate partner.

■ Analysis by Credit Suisse: Describes themethodology and results of the CGFA study onprivatizing the Illinois Tollway.

■ Critical Factors Affecting Lease Value: Reviewsfactors which could significantly change thevalue of a toll road lease.

■ Comparison: Public Option Vs. Privatization:Compares the revenue generated byprivatization with the revenue generated bykeeping the toll road in public operation.

■ Conclusion: Concludes that leasing the IllinoisTollway is not a good idea given the following:

— Privatizing the toll road would posenumerous public policy challenges whichcould limit the value of the lease.

— Privatizing the toll road would be costly toconsumers, requiring annual toll increaseswhich were not linked to toll road improve-ments.

— It would be less efficient than keeping thetoll road publicly operated given the policychallenges and the fact that more revenuecould be generated for transportationimprovements by keeping the toll road inpublic operation than by leasing it to aprivate partner.

Public Policy Issues6

Public Policy IssuesExecutive SummaryOverviewPublic Policy IssuesAnalysisCritical FactorsComparisonConclusion

he 274-mile Illinois Tollway system is not adiscrete, stand-alone element of Illinois’transportation network. Rather, passingthrough 12 counties and serving 1.3 million

drivers daily, the Illinois toll road is critical for themovement of people and goods in and through Illinois.With commuters comprising 75% of its traffic, the tollwayhas a daily impact on the people of northern Illinois.

Given the importance of the toll road system to Illinois,TFIC has identified 11 public policy questions whichwould have to be resolved prior to any lease agreement.These questions fall into three broad categories: financial,policy, and transportation. How each of these questionswould be decided would have significant impact on thevalue of the lease to any potential private partner. Each ofthese issues is detailed below.

Financial Issues

■ Ability to Finance New Toll Road AdditionsOne of the traditional benefits of Illinois’ tollwaysystem is the ability to use the success of completedsegments to help build new segments. The first tollroad segment built, the Tri-State, had to pay foritself. All extensions since that time have beenfinanced using the system as a whole since no newextension could cover its initial construction oroperating costs. First the Northwest was financedusing the base system, then the East-West, then theNorth-South in DuPage County and now I-355 inWill County. Leasing the system to a private partner

would likely eliminate the ability for “cross-subsidiz-ing” the construction of new segments. It might bepossible to fashion a lease agreement that wouldrequire the use of toll revenues for constructingadditions to the system, but that would significantlyreduce the lease payment from the private partner.

■ Use of Lease RevenuesA long-term lease of the tollway has the potential togenerate significant dollars. The Skyway lease inChicago generated $1.8 billion, and the lease of theIndiana Toll Road generated $3.8 billion. In Indianathese moneys are to be used for highway purposes,while in Chicago they are not. In the public discus-sions of an Illinois toll road lease held during 2006,there were many ideas for how potential proceedscould be used. But TFIC believes this is critical:Illinois’ toll roads were paid for by the users; anyfunds generated for the public sector through alease should be used for the benefit of the users.

A related question deals with whether the public isbest served by a one-time payment of benefits or bypayments stretched over many years. With a one-timepayment to the public sector, funding can be quicklyput to work and improvements realized, but thepartnership provides no ability to generate funds forfuture needs. When payments to the public sector arestretched out over the life of the agreement, futureneeds can also be met. However, the amount of theannual payments could seem relatively modest incomparison to a single up-front payment.

■ Increased Costs to UsersIn a lease arrangement, a private partner needs togenerate enough revenue from tolls to cover thecost of the up-front payment to the public owner aswell as to provide a return on equity to investors. Inorder to protect the public, partnership agreementsgenerally will index future toll increases to an indexlike the Consumer Price Index (CPI). For example,the Skyway agreement allows 7.9% average annualtoll increases through 2017 and toll increases afterthat at the greater of 2% per year, inflation, ornominal gross domestic product per capita.

Public agencies, on the other hand, only raise tollswhen it is necessary to meet increased costs orexpansion needs that have to be justified andpresented to the public before approval. Typicallypublic owner toll increases do not keep pace withthe CPI. In fact, for I-Pass users, tolls on the Illinoissystem have risen only 33% in nearly 50 years.

In summary, what are the costs to the highway userfor private as opposed to public financing andoperation? Should the public have any input intofuture toll increase commitments? If so, how couldthat be accomplished within the framework of apublic/private partnership?

■ Flexibility to Increase Other TransportationResourcesIllinois has a strong record of support for periodictransportation funding increases. However, thepromises of additional money from a lease arrange-ment, without raising state highway user fees, couldmake future support for raising fees more difficult.Legislators who might be nervous about feeincreases can point to private partnerships as areason that public initiatives are unnecessary. Topass initiatives in the General Assembly, all parts ofthe state must benefit from the program. Focusingon just a toll road lease could make it more difficultto reach legislative consensus on a package thatmeets all of the state’s transportation needsincluding rural widening/resurfacing and bridges,public transportation, passenger and freight rail,and other infrastructure investments.

Illinois’ unfunded transportation needs are exten-sive. This year, TFIC recommended a $5 billionannual increase in Illinois’ highway, transit, rail andairport programs. How could a toll road leaseagreement be structured to enhance future publicinitiatives or to be part of overall transportationfunding strategies?

Policy Issues

■ Flexibility to Modify/Terminate AgreementPrivatization concepts look at very long lease times— 75 years in the case of the Indiana Toll Road and99 years for the Chicago Skyway. Unforeseencircumstances can arise during that time which maynecessitate the modification or termination of theagreement.

For example, if the Illinois Tollway were leased, itis expected that the partnership agreement wouldinclude provisions for annual toll increases, to be

Public Policy Issues 7

Illinois’ unfundedtransportation needs areextensive. This year, TFICrecommended a $5 billionannual increase in Illinois’highway, transit, rail andairport programs.

Public Policy Issues8

imposed by the private partner, in order for theprivate sector to make a profit. Most of the tolls arepaid by Suburban Cook and Collar Countyresidents. If the proceeds from the lease were usedto benefit downstate and /or Chicago and the tollincreases were perceived as “too high,” it might bepolitically necessary to modify or terminate theagreement. In fact controversies did arise, fairlyearly in the lease period, concerning public/privatetoll roads in Toronto and in Orange County,California. In Toronto’s case, the matter was incourt for several years, with the courts ruling infavor of the private concessionaire. In California,Orange County was able to terminate its agreement,but at a cost of more than $200 million paid to theprivate partner.

Additionally, flexibility is needed to respond tochanging transportation circumstances during thelife of the lease. Today we cannot foresee whatneeds our transportation systems will have 30 or 40years from now, and certainly not in 70 or 80 years.

How could a lease be structured to preserve theflexibility to respond to changing future circum-stances?

■ Public Disclosure of Agreement DetailsWhile public agencies are supposed to be transpar-ent, private businesses strive to be opaque toprotect proprietary information and maintaincompetitive advantages. As public/private partner-ships are considered around the country, conflictshave arisen regarding the extent of the public’s“right to know” before agreements are finalized.

■ Extent of Administrative DiscretionIt is important to consider how much administrativediscretion should be given to transportation

agencies to negotiate and commit to public/private partnerships. The Chicago City Councilhad to approve the Skyway agreement. TheIndiana state legislature had to approve theIndiana Toll Road agreement. What level ofoversight or approval should be required forpublic/private partnership commitments? Howmuch administrative discretion should begranted?

■ Compliance with Current Statutes on Labor,Environment, Competitive Bidding, etc.Public agencies are required to adhere to statestatutes and regulations with respect to numer-ous areas that are designed to protect the broadgeneral public interest. These include:

— Disadvantaged business enterprise law— Prevailing wage law— State procurement code requirements,

including competitive bidding forconstruction

— Qualification-based selection law for hiringengineering and design firms

— Providing for an adequately staffed tollwaysystem

— Ensuring tollway employees have the rightto join a union and bargain collectively forwages and benefits

How would a private entity ensure that some or all ofthese public policy goals were met?

Transportation Issues

■ Use of Non-Compete ProvisionsThe inclusion of “non-compete” provisionsincreases the amount a private partner would bewilling to pay for a long-term lease since theprivate sector’s risk is reduced by removing the

Public Policy Issues 9

possibility of future transportation improvementsbeing constructed in or near the corridor. While theSkyway agreement does not include a non-competeclause, the Indiana Toll Road agreement has alimited non-compete clause.

If included in a contract with a private partner, non-compete provisions could prohibit state, local andtransit agencies from making future improvementsin or near the corridor. In the case of the IllinoisTollway, there are a number of highway and transitimprovements currently under consideration,including the O’Hare Western Bypass, completionof the Elgin-O’Hare Expressway, the Illinois 53corridor in Lake County, the Illiana corridor, andthe Metra Star line. Preserving state and localpower to make these improvements (and otherimprovements which could arise during a long-termlease) is critical to maintaining a strong transporta-tion system for the future.

■ Ability to Manage Road Network as a SystemIt is difficult enough today to coordinate andmanage the transportation system in the Chicagoarea with IDOT and the Tollway managing theInterstate system; CTA, Metra and Pace operatingthe public transportation system; and six countiesand hundreds of municipalities managing the localroad system. Careful consideration would beneeded as to how to integrate a private partner intothe system.

A private partner would manage its facilities tomaximize returns to shareholders and investors, notto maximize public benefit. Frequently public andprivate goals are consistent, but not always. Forexample, increased use of public transit — a publicpolicy goal — may not be compatible with the goalof maximizing toll revenues. Or, goals could differ

with respect to the scheduling of major roadconstruction. This scheduling should be coordinatedamong all transportation agencies in order to diverttraffic from construction zones. But there is noincentive for a private owner to want to schedulework on its system so there is an alternate routeavailable to the public during construction.

■ Impact of Traffic DiversionsAs noted earlier, in order for the private partner torecoup investment and make a profit, public/privatepartnerships require ongoing toll increases.However, when tolls are increased significantly, asmall portion of traffic will divert to other road-ways, including local roads. Many roads innortheast Illinois are already congested or have notbeen constructed to carry traffic more appropriatelyhandled by an expressway. Any consideration of along-term lease should consider the likely extentand impact of traffic diversions due to increasedtolls, including the type of traffic (truck vs. auto)that would divert and the roads that would receivethe additional traffic (local streets, arterials, etc.).

Conclusion

The eleven issues detailed above must be reviewed as partof any toll road lease discussion. While it is likely that alease agreement could be structured to deal with the issues,those decisions would play a large role in determining thevalue of the lease to a private partner.

Analysis10

Analysis byCredit Suisse

Executive SummaryOverviewPublic Policy IssuesAnalysisCritical FactorsComparisonConclusion

he public discussions that occurred in 2006 onleasing the Illinois Tollway focused quicklyon the amount of money the state mightrealize from such a lease. The Illinois

Commission on Government Forecasting andAccountability (CGFA) hired Credit Suisse (CS) toperform a financial analysis of the potential value ofprivatizing the tollway. The Credit Suisse study, releasedin August of 2006, examined various lease and saleoptions, estimated the revenues generated by each, andoffered guidelines as to the manner in which a potentialdeal could be structured. (The “sale” option generated nosupport since it did not result in greater income to the statethan the lease option and, unlike the lease option, wouldmean the permanent transfer of the facility from public toprivate ownership. Therefore, this summary will focusonly on the lease option.)

Credit Suisse analyzed seven lease scenarios, based onthree variables: the length of the lease; the timing and sizeof toll increases and estimated future traffic growth.

■ Length of Lease: The lease lengths in the studyvaried from 25 to 75 years. The 25-year leasescenario was not financially viable.

■ Timing and Size of Toll Increases: The tollincreases varied from a low of 3% annuallybeginning in the year 2031 to a high of 50% every20 years beginning in 2007 coupled with annualincreases of 3% a year. The 3% annually beginningin 2031 was not financially viable.

■ Estimated Future Traffic Growth: For all but onescenario, the study used forecasts through the year2030 which were prepared by Wilbur SmithAssociates (WSA) and included in an IllinoisTollway bond prospectus dated May 25, 2006; andfor the period after 2030, the study used annualtraffic growth of 1%. One scenario increased annualtraffic growth at 1.5% above the Wilbur Smithprojections, beginning in 2007.

Credit Suisse calculated estimated lease values using twomethodologies: the Discounted Cash Flow (DCF) methodand the Internal Rate of Return (IRR) method. The DCFmethod derives the value by computing the present valueof the free cash flow using a weighted average cost ofcapital. (Free cash flow is the amount left over after allexpenses have been paid.) Credit Suisse used a range of6.0% to 6.9% for the weighted average cost of capital. TheIRR method sets the value based on a desired rate of returnfor the investors.

The Credit Suisse study,released in August of 2006,examined various lease andsale options, estimated therevenues generated by each,and offered guidelines as tothe manner in which apotential deal could bestructured.

Analysis 11

The following table below summarizes the Credit Suissescenarios. Since the two valuation methodologies yieldedsimilar ball park results, the table uses the middle of therange given for the proceeds under the Discounted CashFlow method. Finally, the CS report did not reduce theestimated lease proceeds by the amount needed to defeaseoutstanding Illinois Tollway bonds, although CS noted

that this would have to be done and would cost around$2 billion. Therefore, the table shows net lease proceedsafter paying $2 billion for bond defeasance althoughtoday’s costs could be higher. (According to their 2007Budget, the Illinois Tollway had $2.3 billion in debtoutstanding at the beginning of the year, and expected tosell another $700 million in bonds during 2007.)

Estimated NetProceeds After

Required Toll Traffic Bond DefeasanceScenario Increase Lease Term Projections ($ Billion)

#1. 3% annually 75 years Per WSA forecasts ($0.5)starting 2031

#2. 3% annually 75 years Per WSA forecasts $5.1starting 2007

#3. 3% annually 75 years 1.5% annually $11.1starting 2007 above WSA forecasts

#4. 25% every 75 years Per WSA forecasts $10.120 years starting2007 plus 3% inall other years

#5. 50% every 75 Years Per WSA forecasts $18.320 years starting

2007 plus 3%in all other years

#6. 50% every 50 years Per WSA forecasts $11.120 years starting

2007 plus 3%in all other years

#7. 3% annually 25 years Per WSA forecasts ($0.1)starting 2007

While the above table shows substantial potential fundingfrom a toll road lease, there are several factors notincluded which would greatly diminish the value of anylease. Also, in order to estimate the value of a lease, it is

important to compare private lease scenarios to a scenarioin which the toll road remained public. These TFICconcerns are discussed in the following sections of thispaper.

Summary: Illinois Tollway Lease ScenariosFrom Credit Suisse Report

Critical FactorsAffecting Lease Value

Executive SummaryOverviewPublic Policy IssuesAnalysisCritical FactorsComparisonConclusion

Critical Factors12

here are several major variables which cancause significant changes, both up and down,in the dollar value of a tollway lease. Thesevariables include: future toll increases, length

of the lease, establishment of an endowment orstabilization fund to cushion toll increases, required futureconstruction, weighted average cost of capital used in thefinancial analysis, and non-compete provisions. Each ofthese variables is discussed in this section.

Additionally, the Credit Suisse report only quantifiedpossible lease proceeds as a single upfront payment.However, rather than a single payment, the payments couldbe structured to be made through the life of the lease inorder to support ongoing transportation improvements.This section also analyzes the “annual payment” option.

Toll Increases

Guaranteed toll increases are a required element of anyconcession agreement if payment is to be made by aprivate partner to the state. As noted earlier, Credit Suisseused four different toll regimes to estimate the value of atollway lease. These four were:

■ Scenario #1 - Annual increases of 3%,starting in 2031

■ Scenario #2 - Annual increases of 3%,starting in 2007

■ Scenario #4 - 25% increase every 20 years,starting in 2007; 3% increase in all other years

■ Scenario #5 - 50% increase every 20 years,starting in 2007; 3% increase in all other years

(Scenarios #3 & #7 used the same toll regime as #2, but #3had more aggressive traffic growth and #7 had a muchshorter lease. Scenario #6 used the same toll regime as #5,but with a shorter lease.)

The graph on the next page shows historic toll rates plusthe rates under each of the four toll increase regimes. Asthe graph illustrates, historic rates have been relativelyflat, and the toll increase regimes would be a significantdeparture from past practice. In the case of the mostaggressive regime — 50% increase every 20 years plus3% in other years — the tolls would rise from the current$0.40 for I-Pass users to more than $16.00 by 2079.

Guaranteed toll increasesare a required element ofany concession agreement ifpayment is to be made by aprivate partner to the state.

Critical Factors 13

Credit Suisse Toll Rate Assumptions

The revenues generated by these guaranteed toll increase scenarios are quite large. The following table, using estimatesmade by TFIC, shows how substantial these revenues could be in the future.

Scenario Status Quo #1. #2. #4. #5.

Required Toll None 3% Annual 3% Annual 25% Every 50% EveryIncrease Starting 2031 Starting 2007 20 Yrs. Plus 20 Yrs.

3% Annual Plus 3% Annual

Toll Revenues $1.0 $1.0 $1.8 $2.4 $3.2in 2030

Toll Revenues $1.2 $2.1 $3.9 $6.2 $9.6in 2050

Estimated Toll Revenues($ Billion)

To put these revenue numbers in perspective, the state’s largest riverboat casino revenue generator is Elgin with revenues of$407 million annually.

Critical Factors14

Length of Lease

As noted earlier, leases in public/private partnershiparrangements can be very long — 99 years for the ChicagoSkyway and 75 years for the Indiana Toll Road. Whenlease terms are shortened, the value of the lease to theprivate sector, and hence the lease payment to the publicsector, go down. This is illustrated in the following table.

Est. Net ProceedsLease Term After Bond Defeasance

($ Billion)

75 Years* 18.3

50 Years* 11.1

25 Years** 3.6

*Credit Suisse Estimate**TFIC Estimate

Lease Value at 20% Toll IncreaseEvery 20 Yrs. Plus 3% Annual

Establishment of an EndowmentFund to Cushion Toll Increases

It has been suggested that the guaranteed toll increasescould be mitigated for a period of time by taking part ofthe proceeds and depositing them into a fund to pay theprivate partner annually for revenues lost due to a tollfreeze. Deferring toll increases could make legislativepassage of a toll road lease politically easier. However,there are several disadvantages:

■ The cost of establishing an endowment/tollstabilization fund reduces proceeds from theconcession agreement.

■ Fund investments may not achieve targets increas-ing the state’s risk since the private partner must bereimbursed an agreed amount.

■ When the toll freeze ended, a large toll increasewould be necessary to bring tolls up to guaranteedlevels.

Endowment/Toll Stabilization Fund 10-Year Freeze($ Billion)

The following table shows the fund size necessary for a 10-year toll freeze assuming a 5.2% earnings rate for theendowment fund.

Scenario #2 #4 #5

Required Toll Increase 3% Annual 25% Every 20 Yrs. 50% Every 20 Yrs.Starting 2007 Plus 3% Annual Plus 3% Annual

Required Fund Size $0.7* $1.7* $3.2**

2017 Required 38%* 68%* 102%*Toll Increase

*TFIC Estimate**Credit Suisse Estimate

Critical Factors 15

It should be noted that, in lieu of an endowment fund, theprivate partner could simply reduce the upfront leasepayment to the state, based on deferring any toll increasesfor a chosen period of time.

Future Construction Requirements

Credit Suisse made the following assumptions on capitalspending for improvements to the Tollway to be requiredby the concession agreement:

■ Completion of the Tollway’s current $5.3 billionCongestion-Relief Program (CRP)

■ Annual maintenance of $175 million through 2011,$200 million through 2020, 3% annual growththereafter.

The annual maintenance assumptions are reasonable.However, no provision is included in the estimates for

Additional Capital Expenses Needed Over Credit Suisse Report(2006 $ Billion)

Lease Term: 50 Years Lease Term: 75 Years

Existing System Capacity Expansion $1.0; Year 25 $1.0; Year 25

New System Extensions $1.5; Years 15 & 30 $1.5; Years 15, 30 & 65

O’Hare Western Access $2.0; Year 10 $2.0; Year 10

CRP Magnitude Program $0 $5.3; Year 50

Inclusion of these amounts will reduce the proceeds to the state. TFIC does not have the financial models used by CreditSuisse and can only estimate the present value of these additional expenses.

Present Value Additional Construction Expenses($ Billion)

Lease Term: 50 Years Lease Term: 75 Years

Existing System Capacity Expansion $0.4 $0.4

New System Extensions $1.5 $1.7

O’Hare Western Access $1.4 $1.4

CRP Magnitude Program 0 $1.0

Total $3.3 $4.5

needed pavement/bridge reconstruction or for additionallanes and new interchanges in future years after completionof the current CRP. Nor did they assume construction ofany new additions to the system such as the most recent IL355 extension down to I-80.

While this is not an issue for the 25-year lease termanalysis, it is a major shortcoming for the 50 and 75-yearlease analysis. Credit Suisse noted the need for a CRP-sized program after 45 years for lease terms of over 85years, but CS only analyzed shorter lease terms. Thus, theCS analysis did not include any funding for additionalmajor capital needs beyond those in the currentCongestion-Relief Program. The following capitalassumptions should be added if the Tollway is to continueto be a vital part of the northeastern Illinois transportationnetwork into the future.

Critical Factors16

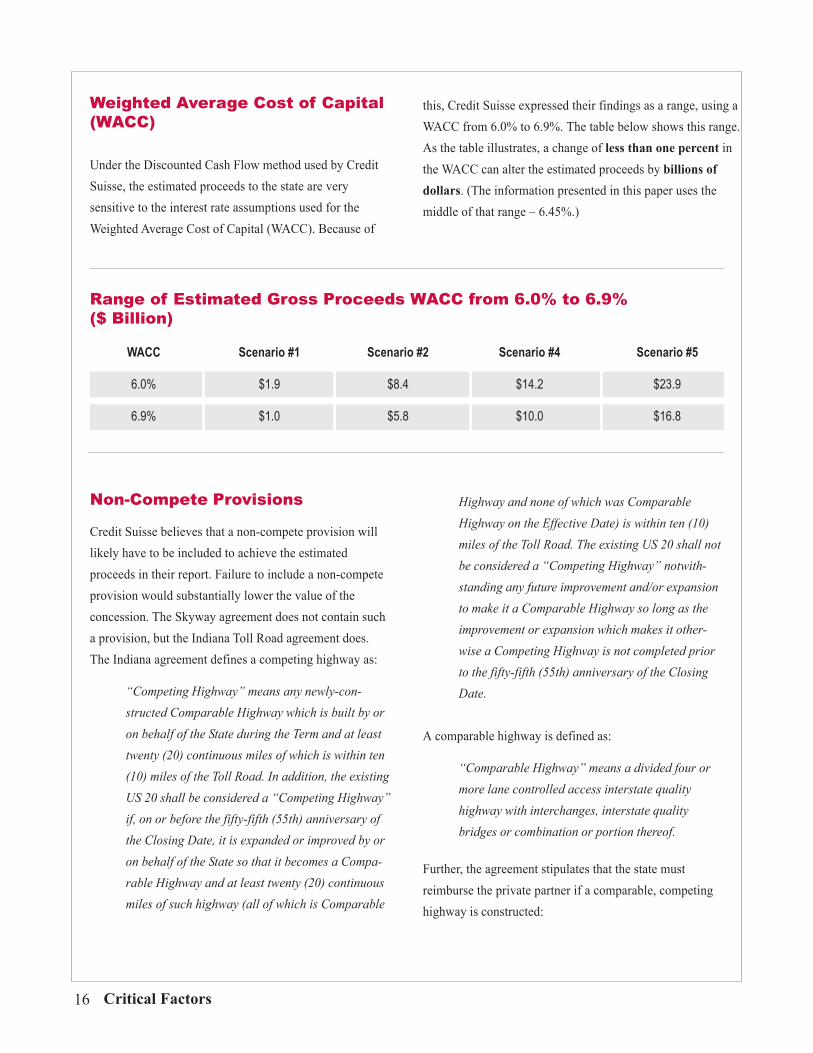

Weighted Average Cost of Capital(WACC)

Under the Discounted Cash Flow method used by CreditSuisse, the estimated proceeds to the state are verysensitive to the interest rate assumptions used for theWeighted Average Cost of Capital (WACC). Because of

Range of Estimated Gross Proceeds WACC from 6.0% to 6.9%($ Billion)

WACC Scenario #1 Scenario #2 Scenario #4 Scenario #5

6.0% $1.9 $8.4 $14.2 $23.9

6.9% $1.0 $5.8 $10.0 $16.8

this, Credit Suisse expressed their findings as a range, using aWACC from 6.0% to 6.9%. The table below shows this range.As the table illustrates, a change of less than one percent inthe WACC can alter the estimated proceeds by billions ofdollars. (The information presented in this paper uses themiddle of that range – 6.45%.)

Non-Compete Provisions

Credit Suisse believes that a non-compete provision willlikely have to be included to achieve the estimatedproceeds in their report. Failure to include a non-competeprovision would substantially lower the value of theconcession. The Skyway agreement does not contain sucha provision, but the Indiana Toll Road agreement does.The Indiana agreement defines a competing highway as:

“Competing Highway” means any newly-con-structed Comparable Highway which is built by oron behalf of the State during the Term and at leasttwenty (20) continuous miles of which is within ten(10) miles of the Toll Road. In addition, the existingUS 20 shall be considered a “Competing Highway”if, on or before the fifty-fifth (55th) anniversary ofthe Closing Date, it is expanded or improved by oron behalf of the State so that it becomes a Compa-rable Highway and at least twenty (20) continuousmiles of such highway (all of which is Comparable

Highway and none of which was ComparableHighway on the Effective Date) is within ten (10)miles of the Toll Road. The existing US 20 shall notbe considered a “Competing Highway” notwith-standing any future improvement and/or expansionto make it a Comparable Highway so long as theimprovement or expansion which makes it other-wise a Competing Highway is not completed priorto the fifty-fifth (55th) anniversary of the ClosingDate.

A comparable highway is defined as:

“Comparable Highway” means a divided four ormore lane controlled access interstate qualityhighway with interchanges, interstate qualitybridges or combination or portion thereof.

Further, the agreement stipulates that the state mustreimburse the private partner if a comparable, competinghighway is constructed:

Critical Factors 17

(e) …The opening of a Competing Highway shallconstitute a Compensation Event with respect towhich Concession Compensation shall be payableon or before March 15 in an amount equal to theactual decrease in net income suffered by theConcessionaire during the preceding calendar yearas a sole and direct result of the CompetingHighway.

It is unknown what type of non-compete provision mightbe included in a proposed Illinois Tollway lease. However,the inclusion of a non-compete provision is likelynecessary to achieve significant proceeds for the state.

What is known is that there are many locations throughoutnortheastern Illinois where future improvements on routesnear the Tollway will be required over the next 50 to 75years. Preserving state and local power to make theseimprovements will be critical to maintaining a goodtransportation system for the future. A few examples ofthese needed improvements are:

O’Hare Western BypassElgin-O’Hare completionIllinois 53 corridor in Lake CountyIllinois 59 corridorIlliana corridorMetra Star line

Summary of Critical Factors

Following is a table which summarizes the critical factors discussed in this section.

Scenario #2 Scenario #4 Scenario #5 Scenario #6Key Variables Includedin CS ReportRequired Toll 3% Annual 25% Every 20 Yrs. 50% Every 20 Yrs. 50% Every 20 Yrs.Increase Starting 2007 Plus 3% Annual Plus 3% Annual Plus 3% AnnualLease Term 75 Yrs. 75 Yrs. 75 Yrs. 50 Yrs.

Est. Lease Proceeds(after bond defeasance) $5.1 Billion $10.1 Billion $18.3 Billion $11.1 Billion

Est. Cost of VariablesNot In CS Report10-Yr. Toll Freeze $0.7 Billion $1.7 Billion $3.2 Billion $3.2 BillionEndowmentPresent Value of Add’l $4.5 Billion $4.5 Billion $4.5 Billion $3.3 BillionConstruction Needed

Est. Net Lease Proceeds ($0.1 Billion) $3.9 Billion $10.6 Billion $4.6 Billion

Other Variables0.45% Change in WACC +/-$1.3 Billion +/-$2.1 Billion +/-$3.6 Billion +/-$1.7 BillionAcceptable Non- ? ? ? ?Compete Provision

Potential Lease Payouts Stretched Over Time

Critical Factors18

Structure of Lease Payments

The Credit Suisse analysis estimated the lease proceeds asa single upfront payment. However, another option wouldbe to apply the net proceeds to a Transportation CapitalTrust Fund which could provide funding annually fortransportation programs throughout the term of the lease asopposed to spending all of the proceeds in a short period oftime.

Advantages of this approach include:

■ The additional funding would not run out until thelease expired, at which time the revenues from theasset would again be available to the state - to returnto its role as operator or to lease it again.

■ The lease proceeds would not be depleted in a fiveor ten-year period, leaving decades where tolls wereincreased but motorists received no transportationbenefits.

■ Stretching the proceeds over the term of the leasewould avoid committing the state to either asubstantial tax increase or large transportationcapital program reduction when the proceeds weredepleted.

Disadvantages include:

■ There would be no big short-term program.■ Steady annual payments would be eroded signifi-

cantly over the years by inflation.

The following table estimates the new transportation fundsavailable annually if all the net proceeds were dedicated toa Transportation Trust Fund for the full life of the lease orfor a period of 10 years. The table assumes the trust fundwould earn 5.2%.

*Net proceeds after defeasing bonds, funding needed additional construction identified in this section, and setting up10-year toll freeze endowment fund.

Scenario #2 Scenario #4 Scenario #5 Scenario #6Required Toll 3% Annual 25% Every 20 Yrs. 50% Every 20 Yrs. 50% Every 20 Yrs.Increase Starting 2007 Plus 3% Annual Plus 3% Annual Plus 3% Annual

Lease Term 75 Yrs. 75 Yrs. 75 Yrs. 50 Yrs.

Net Proceeds* ($0.1 Billion) $3.9 Billion $10.6 Billion $4.6 Billion

Payout Over n/a $0.2 Billion $0.55 Billion $0.26 BillionLife of LeaseEst. Annual Amount

Payout Over 10 Yrs. n/a $0.51 Billion $1.36 Billion $0.60 BillionEst. Annual Amount

Comparison 19

Comparison:Public Option Vs. Privatization

Executive SummaryOverviewPublic Policy IssuesAnalysisCritical FactorsComparisonConclusion

ather than lease the Tollway to a privatepartner, the Tollway board could raise tolls ina manner identical to a private partner. Theadditional toll revenue could be used to

support new bonds, with the proceeds of the bondsdedicated to additional transportation improvements.

To analyze such an option, the following assumptionswere used:

■ Same operating and capital expenditures as thoseused by Credit Suisse for a private partner

■ ISTHA’s Congestion-Relief Program (CRP) paidfor with current toll revenues

■ No toll freeze or additional expansion costs overCredit Suisse assumptions

■ Revenue growth used to support new bonds forcapital improvements

■ 1.3 coverage ratio for new debt service■ 25-year term for new bonds

The following table compares the tollway lease scenariosto a public option. As the table illustrates, the publicoption yields as much as $97 billion (net present value) foradditional capital spending. Thus, if the toll increaseregime required for private lease options wereimplemented by public sector, much more funding wouldbe available for capital improvements.

Keeping the Tollway Public:Additional Tollway Capital Spending 2007-2081

Scenario #2 Scenario #4 Scenario #5

Toll Increase 3% Annual 25% Every 20 Yrs. 50% Every 20 Yrs.Plus 3% Annual Plus 3% Annual

Private Option: $5.1 Billion $10.1 Billion $18.3 BillionEst. Lease Proceeds(after bond defeasance)

Public Option: $23.4 Billion $52.3 Billion $97.2 BillionNew Tollway Bonds(net present value)

Comparison20

It is highly unlikely that the Tollway board would adoptthe same aggressive toll increase schedule as a privatepartner would require. Typically, toll road increases areproposed when needed to fund specific capitalimprovements and are adopted only after public scrutiny.This contrasts sharply with the private partner toll increasemodel of annual increases for 50 or 75 years, includingsizeable increases every 20 years, with no public scrutinyand with no linkage to toll road improvements.

The Illinois Tollway’s most recent toll increase, effectivein 2005, was adopted only after public hearings; wasrelatively modest; and is funding a $5.3 billion majorreconstruction and expansion of the system, including the$730 million I-355 extension. Thus, it should be possibleto generate the funds for needed transportationimprovements, through the public option, with smaller tollincreases.

Conclusion

Executive SummaryOverviewPublic Policy IssuesAnalysisCritical FactorsComparisonConclusion

Conclusion 21

tretching for 274 miles and serving around 8billion vehicles miles of travel a year, theIllinois Tollway is an invaluable asset to thestate and particularly to the people ofnortheast Illinois. It is critical that nothing be

done to jeopardize this vital component of Illinois’transportation network.

TFIC believes that privatization of the Illinois Tollwaywould present many public policy challenges, wouldprovide only a limited short-term funding fix, and wouldnot generate as much funding for future capital needs ascontinued public sector control. Factors that led to thisconclusion are:

■ Many tough policy issues complicate any privatelease option for the toll road, including how tofinance future improvements currently cross-subsidized by existing toll revenues, the size of tollincreases, the length of the lease, required non-compete provisions, employee rights, and otherissues. Decisions on these issues would likely beginto limit the value of the toll road to a private partner,and could also limit the full potential of the toll roadto function as an integrated, coordinated componentof northeastern Illinois’ transit/highway network.

■ Based on the toll road study commissioned byIllinois’ Commission on Government Forecasting

and Accountability (CGFA), a successful toll roadlease would require a long lease term (50 to 75years) and an annual toll increase scheduledramatically different from Illinois’ history ofinfrequent and small increases.

■ The CGFA study did not make any provision forfunding future major toll road improvements(beyond those underway today), such as recon-struction and additional lanes on the existingsystem as well as toll road extensions. Providingfunding for these improvements would signifi-cantly reduce lease proceeds.

■ Allowing the existing tollway board to implementfare increases like those required to attract aprivate partner would actually result in morefunding for capital improvements than would a tollroad lease. Or, the existing tollway board couldprovide transportation improvement funds asneeded by adopting more modest fare increasesthan a private lease would require.

While leasing toll roads to a private partner may work insome locations, for the Illinois Tollway it is the wrongoption — creating numerous policy challenges, likely tobe costly to consumers and likely to be less efficient thankeeping the toll road publicly operated.

22

Transportation for Illinois Coalition Members

STEERING COMMITTEELocal/Regional OrganizationsChamber of Commerce for Decatur & Macon CountyChampaign County Chamber of Commerce/Champaign AllianceChampaign-Urbana Mass Transit DistrictChicago Metropolis 2020Chicago Southland Economic Development Corp.Chicago Transit AuthorityChicago & Vicinity District Council of Iron WorkersCorridor 67, Inc.Egyptian Contractors AssociationElgin Area Chamber of CommerceGreater Springfield Chamber of CommerceHeartland PartnershipKane CountyLake County Division of TransportationLake County Transportation AllianceMetraMetroLINKNaperville Area Chamber of CommerceQuincy Area Chamber of CommerceRegional Transportation Authority (RTA)Rockford Winnebago County Better Roads Assn.Route 51 CoalitionSouthern Illinois Construction Adv. Program

SUPPORTING MEMBERSBuilders Assn. of Greater ChicagoChicago Federation of Labor (AFL-CIO)Chicago Southland Chamber of CommerceChicagoland Chamber of CommerceGreater Aurora Chamber of CommerceHighway 34 CoalitionIllinois Automobile Dealers AssociationIllinois Highway Users AssociationIllinois Petroleum CouncilIllinois Public Airports AssociationIllinois Quad City Chamber of CommerceJacksonville Area Chamber of CommerceLeadership Council of SW IllinoisMacomb Area Chamber (MACCDDC)McLean County ChamberMetropolitan Planning CouncilMid-Central Illinois Regional Council of CarpentersNorthwestern Illinois Contractors AssociationSouthwestern IL Bldg. & Constr. Trades Council

STEERING COMMITTEEStatewide OrganizationsAmerican Concrete Pavement Asso. – IL Chapter, Inc.American Council of Engineering Cos. of IllinoisAssociated General Contractors of IllinoisIllinois AFL-CIOIllinois Asphalt Pavement AssociationIllinois Association of Aggregate ProducersIllinois Association of County EngineersIllinois Chamber of CommerceIllinois Municipal LeagueIllinois Road & Transportation Builders AssociationIllinois State Branch of Operating EngineersPrecast/Prestressed Producers of IL & WIUnderground Contractors AssociationUnited Transportation Union

PARTICIPATING MEMBERS336 CoalitionAAA – Chicago Motor ClubAmerican Society of Civil Engineers - IL SectionAssociated Equipment DistributorsDuPage County – Dept. of Economic Dev. & PlanningGreater Peoria Contractors & Suppliers AssnGrowth Association of Southwestern ILIllinois Concrete Pipe AssociationIllinois Construction Industry CommitteeIllinois Professional Land SurveyorsIllinois Public Transportation AssociationIllinois Society of Professional EngineersIllinois Valley Contractors AssociationMid-West Truckers AssociationStructural Engineers Association of IllinoisTownship Officials of Illinois

The Transportation for Illinois Coalition is a diverse group of statewide and regional business, organized labor, industry,governmental and not-for-profit organizations that has joined together in a united and focused effort to support a strongtransportation alliance for Illinois. The coalition takes a comprehensive approach and seeks to speak with one voice for

all of Illinois regarding transportation funding needs at both the state and federal levels. The coalition believes thattransportation is critical to the economy of Illinois. This comprehensive approach involves all modes of

transportation, including rail, air, water, highways and mass transit.