LAW UNION AND ROCK INSURANCE PLCnse.com.ng/Financial_NewsDocs/Law Union AND Rock - 2016...

104

LAW UNION AND ROCK INSURANCE PLC ANNUAL REPORT AND FINANCIAL STATEMENTS 31 DECEMBER 2016

Transcript of LAW UNION AND ROCK INSURANCE PLCnse.com.ng/Financial_NewsDocs/Law Union AND Rock - 2016...

LAW UNION AND ROCK INSURANCE PLC

ANNUAL REPORT AND FINANCIAL STATEMENTS 31 DECEMBER 2016

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

Table of Contents

Directors Report

Financial Highlights

Corporate Information 1

Statement of Directors’ Responsibilities

3

3

3

Risk Management Statement 4

Report of Statutory Audit Committee 6 Report of Statutory Audit Committee

Independent Auditor’s Report 7

Summary of Significant Accounting Policies 11

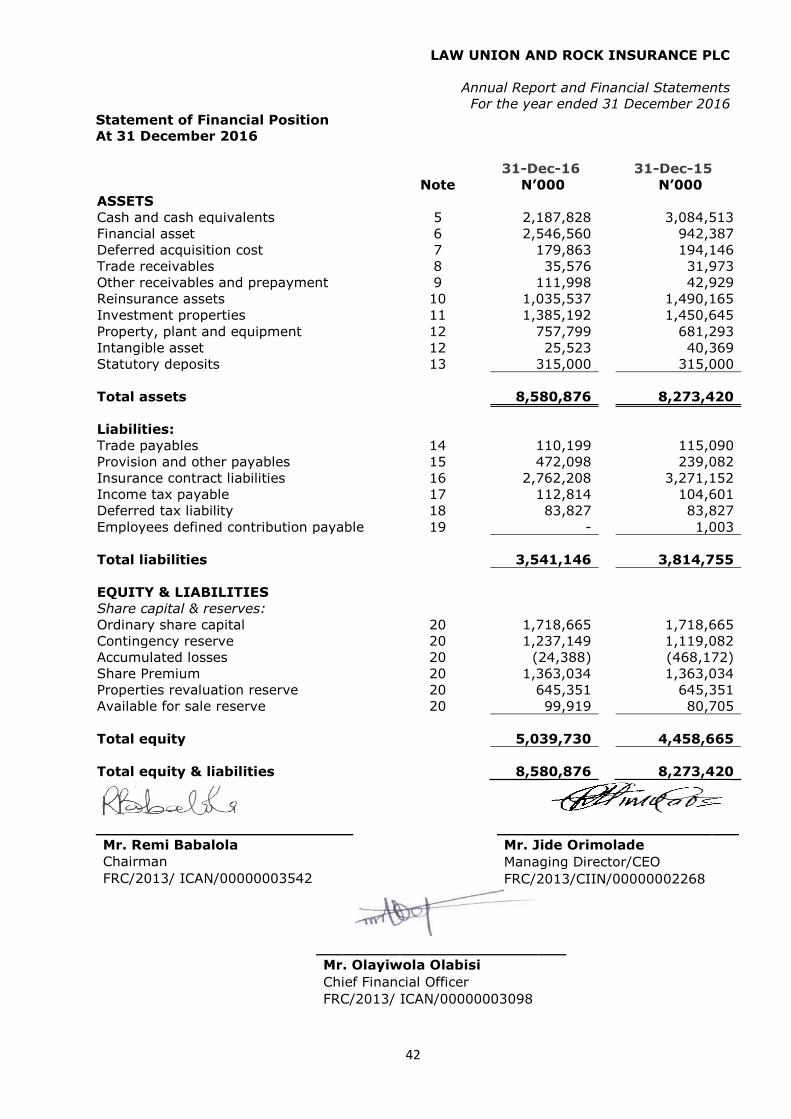

Statement of Financial Position 42

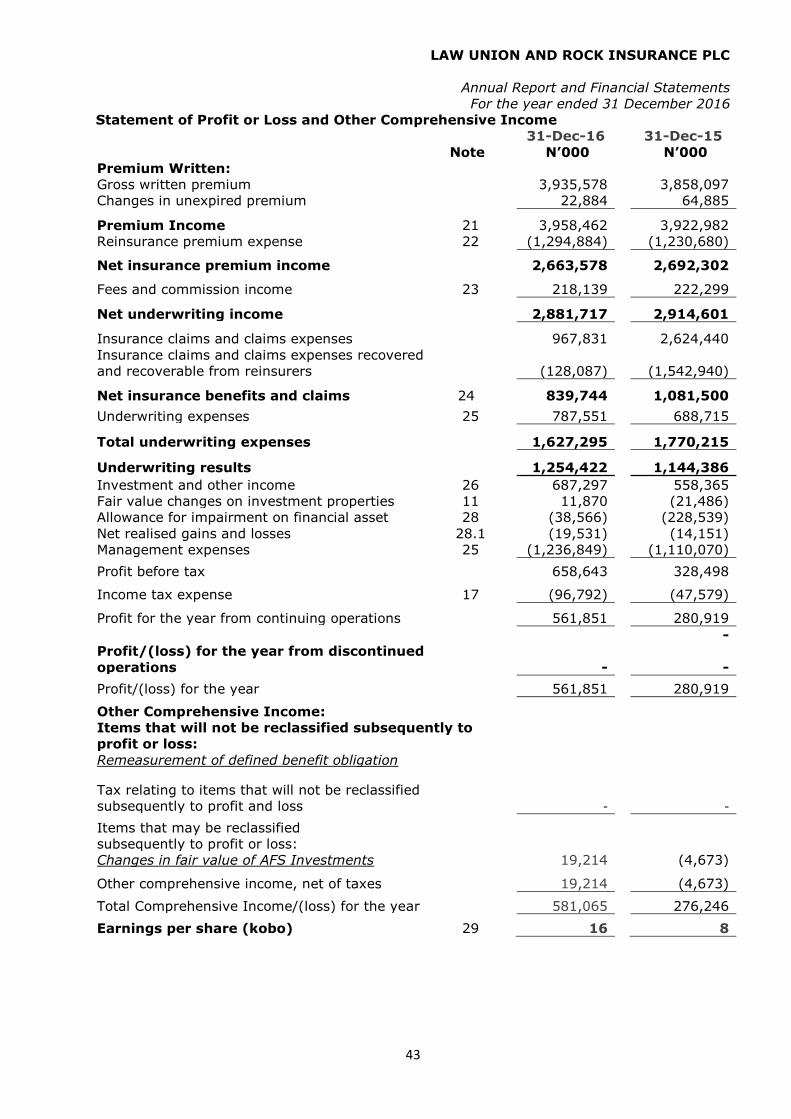

Statement of Profit or Loss and Other Comprehensive Income 43

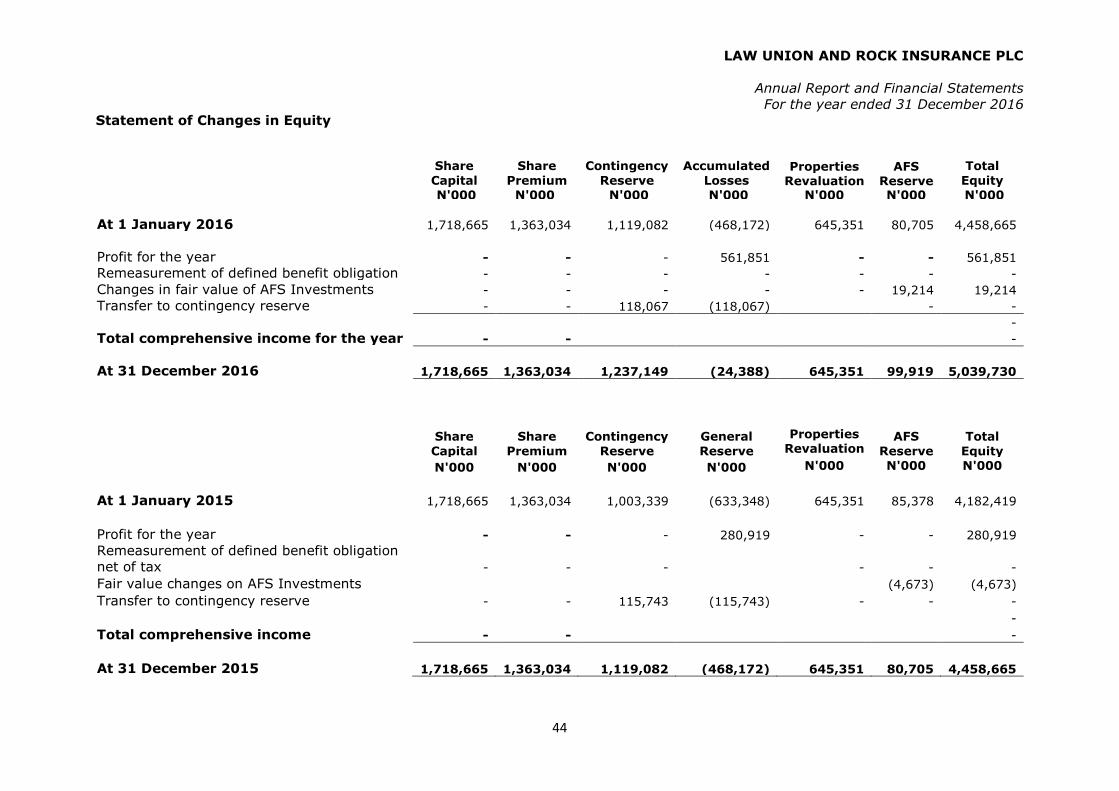

Statement of Changes in Equity 44

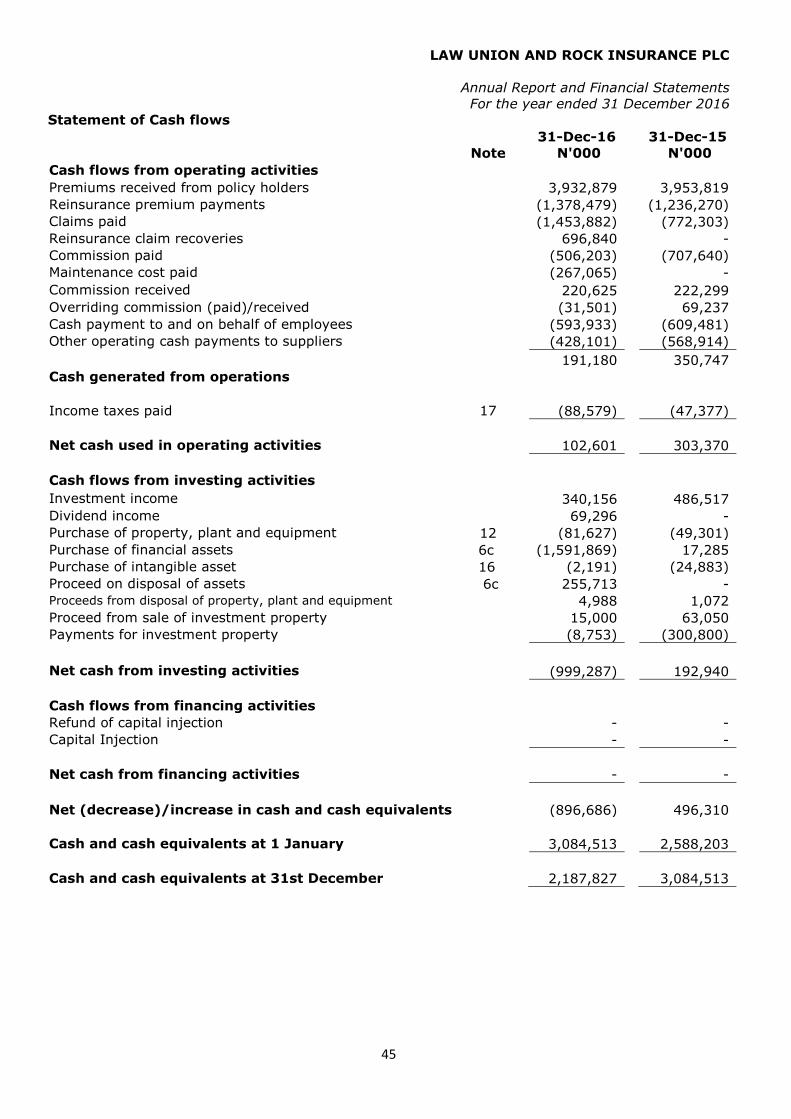

Statement of Cash Flows 45

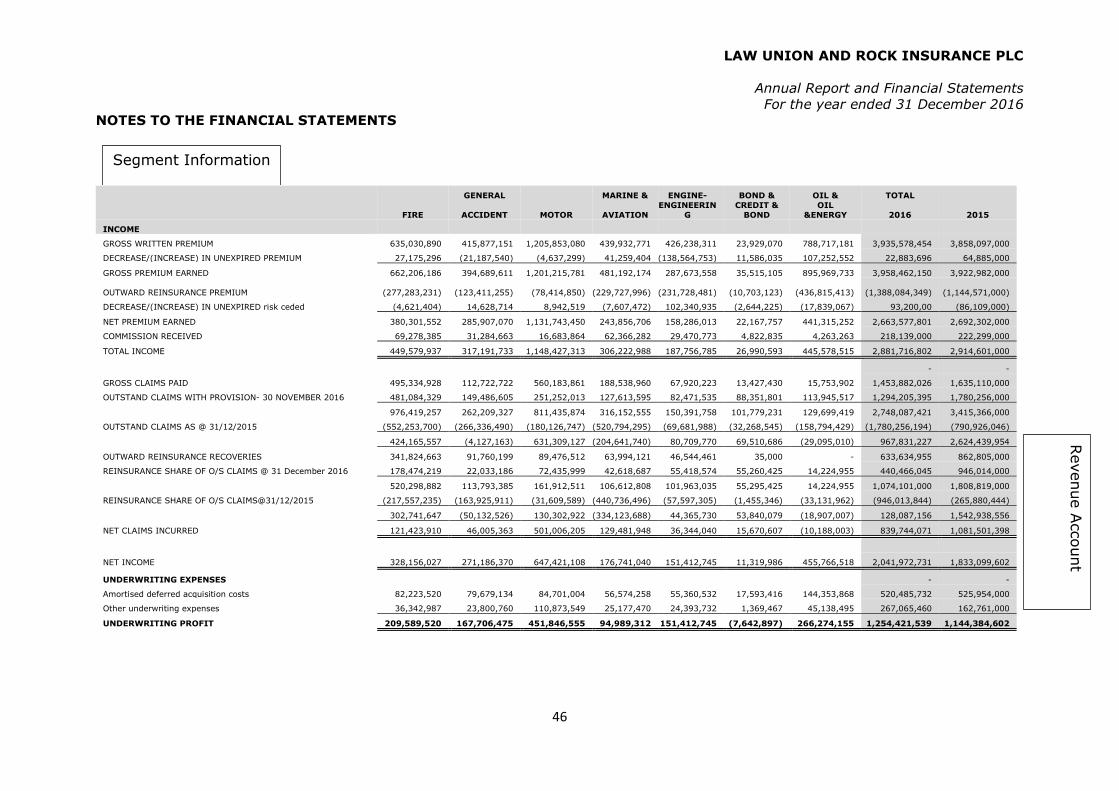

Notes to the Financial Statements 46

Statement of Value Added 95

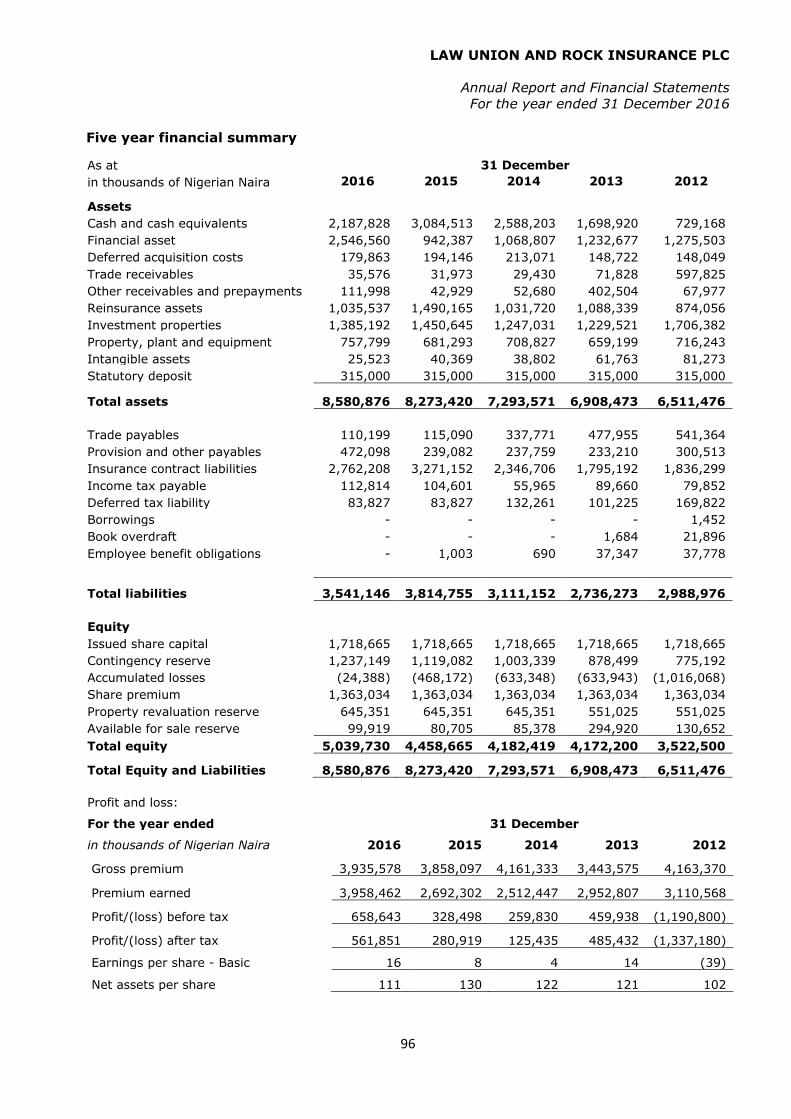

Financial Summary 96

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

i

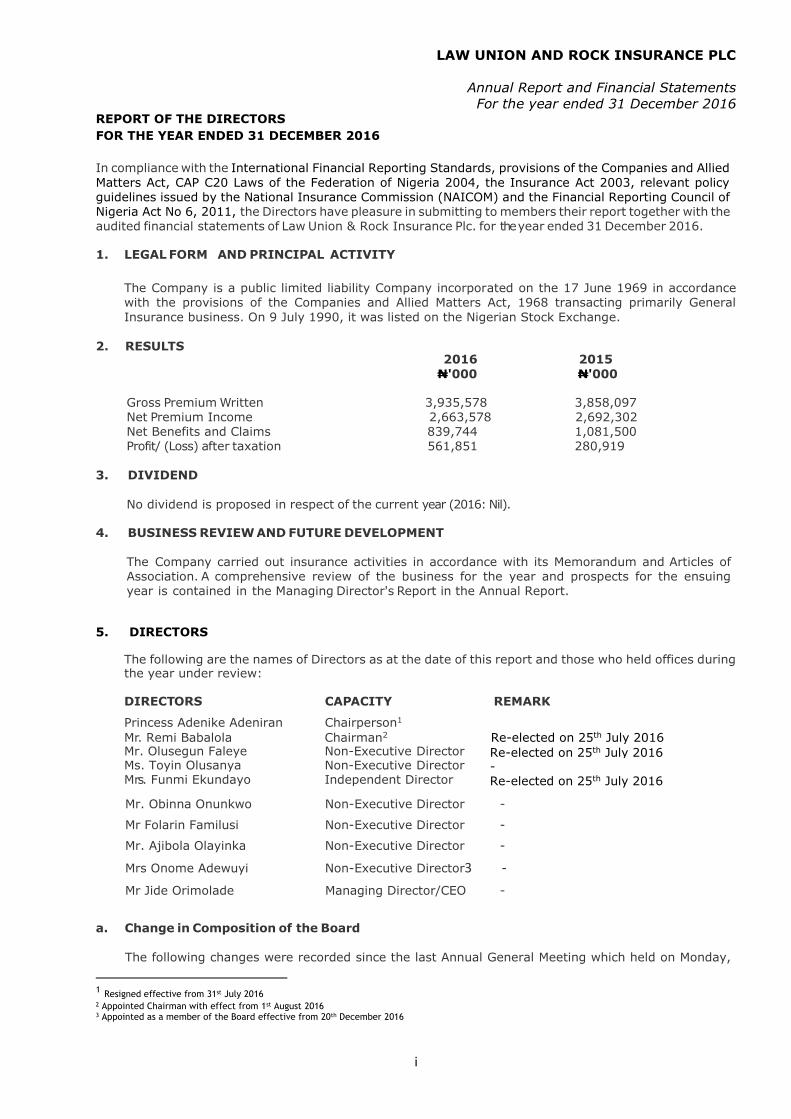

REPORT OF THE DIRECTORS

FOR THE YEAR ENDED 31 DECEMBER 2016

In compliance with the International Financial Reporting Standards, provisions of the Companies and Allied

Matters Act, CAP C20 Laws of the Federation of Nigeria 2004, the Insurance Act 2003, relevant policy guidelines issued by the National Insurance Commission (NAICOM) and the Financial Reporting Council of Nigeria Act No 6, 2011, the Directors have pleasure in submitting to members their report together with the audited financial statements of Law Union & Rock Insurance Plc. for the year ended 31 December 2016.

1. LEGAL FORM AND PRINCIPAL ACTIVITY

The Company is a public limited liability Company incorporated on the 17 June 1969 in accordance with the provisions of the Companies and Allied Matters Act, 1968 transacting primarily General

Insurance business. On 9 July 1990, it was listed on the Nigerian Stock Exchange.

2. RESULTS 2016 2015

N'000 N'000

Gross Premium Written 3,935,578 3,858,097 Net Premium Income 2,663,578 2,692,302 Net Benefits and Claims 839,744 1,081,500 Profit/ (Loss) after taxation 561,851 280,919

3. DIVIDEND

No dividend is proposed in respect of the current year (2016: Nil).

4. BUSINESS REVIEW AND FUTURE DEVELOPMENT

The Company carried out insurance activities in accordance with its Memorandum and Articles of Association. A comprehensive review of the business for the year and prospects for the ensuing year is contained in the Managing Director's Report in the Annual Report.

5. DIRECTORS

The following are the names of Directors as at the date of this report and those who held offices during the year under review:

DIRECTORS CAPACITY REMARK

Princess Adenike Adeniran Chairperson1

Mr. Remi Babalola Chairman2 Re-elected on 25th July 2016 Mr. Olusegun Faleye Non-Executive Director Re-elected on 25th July 2016 Ms. Toyin Olusanya Non-Executive Director - Mrs. Funmi Ekundayo Independent Director Re-elected on 25th July 2016

- Mr. Obinna Onunkwo Non-Executive Director -

Mr Folarin Familusi Non-Executive Director -

Mr. Ajibola Olayinka Non-Executive Director -

Mrs Onome Adewuyi Non-Executive Director3 -

Mr Jide Orimolade Managing Director/CEO -

a. Change in Composition of the Board

The following changes were recorded since the last Annual General Meeting which held on Monday,

1 Resigned effective from 31st July 2016 2 Appointed Chairman with effect from 1st August 2016 3 Appointed as a member of the Board effective from 20th December 2016

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

ii

25th July 2016: Princess Adenike Adeniran resigned from the Board of Directors with effect from 31st July 2016; Mr Remi Babalola was appointed as the Chairman of the Board with effect from 1st August 2016;

Mr Olusegun Faleye was appointed as the Vice Chairman of the Board with effect from 1st August 2016; and

By a resolution of the Board dated 20th December 2016, Mrs Onome Adewuyi was appointed as a member of the Board.

Board Committees were reconstituted during the period.

b. Directors Retiring by Rotation

In accordance with the Company’s Article of Association and S259(1) and (2) of the Companies and Allied Matters Act 1990, the following Directors, Mr Folarin Familusi, Mr Ajibola Olayinka and Ms Toyin

Olusanya will retire by rotation, and being eligible, offer themselves for re-election. Pursuant to the

provision of S259 (3) of Companies and Allied Matters Act 1990, a resolution will be proposed at the Annual General Meeting for their re-election.

c. Directors' Interest

The names of the Directors and their interests in the issued share capital of the Company as recorded in the Register of Directors' Shareholdings as at 31 December 2016 are as follows:

DIRECTORS NAME Number of Ordinary Shares held (2016)

Number of Ordinary Shares held (2015)

Princess Adenike Adeniran

Indirect (1) - 1,031,133,728 (Swanlux Solutions and Services Limited) Indirect (2) – 10,147,700 (Nikal Nigeria Limited)

Indirect (1) - 1,031,133,728 (Swanlux Solutions and Services Limited) Indirect (2) – 10,147,700 (Nikal Nigeria Limited)

Mr. Remi Babalola

Indirect – 1,031,133,727 (Alternative Capital Partners)

Indirect – 1,031,133,727 (Alternative Capital Partners)

Mr. Victor Olusegun Faleye

Indirect – 1,031,133,728 (Swanlux Solutions and Services Limited)

Indirect – 1,031,133,728 (Swanlux Solutions and Services Limited)

Ms. Toyin Olusanya

Indirect – 1,031,133,727 (Alternative Capital Partners)

Indirect – 1,031,133,727 (Alternative Capital Partners)

Mr. Ajibola Olayinka

Indirect – 1,031,133,727 (Alternative Capital Partners)

Indirect – 1,031,133,727 (Alternative Capital Partners)

Mr. Folarin Familusi Direct – 1,000,000 Indirect – 1,031,133,728 (Swanlux Solutions and Services Limited)

Direct – 1,000,000 Indirect – 1,031,133,728 (Swanlux Solutions and Services Limited)

Mr. Obinna Onunkwo Indirect – 1,031,133,727 (Alternative Capital Partners)

Indirect – 1,031,133,727 (Alternative Capital Partners)

Mrs Funmi Ekundayo Nil Nil

Mr Jide Orimolade Nil Nil

Mrs Onome Adewuyi Indirect – 1,031,133,728 (Swanlux Solutions and Services Limited)

Nil

None of the Directors has notified the Company for the purposes of Section 277 of the Companies and Allied Matters Act, CAP C20 Laws of the Federation Nigeria 2004 of any disclosable interests in contracts in which the Company was involved as at 31 December 2016 other than the one disclosed in note 32.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

iii

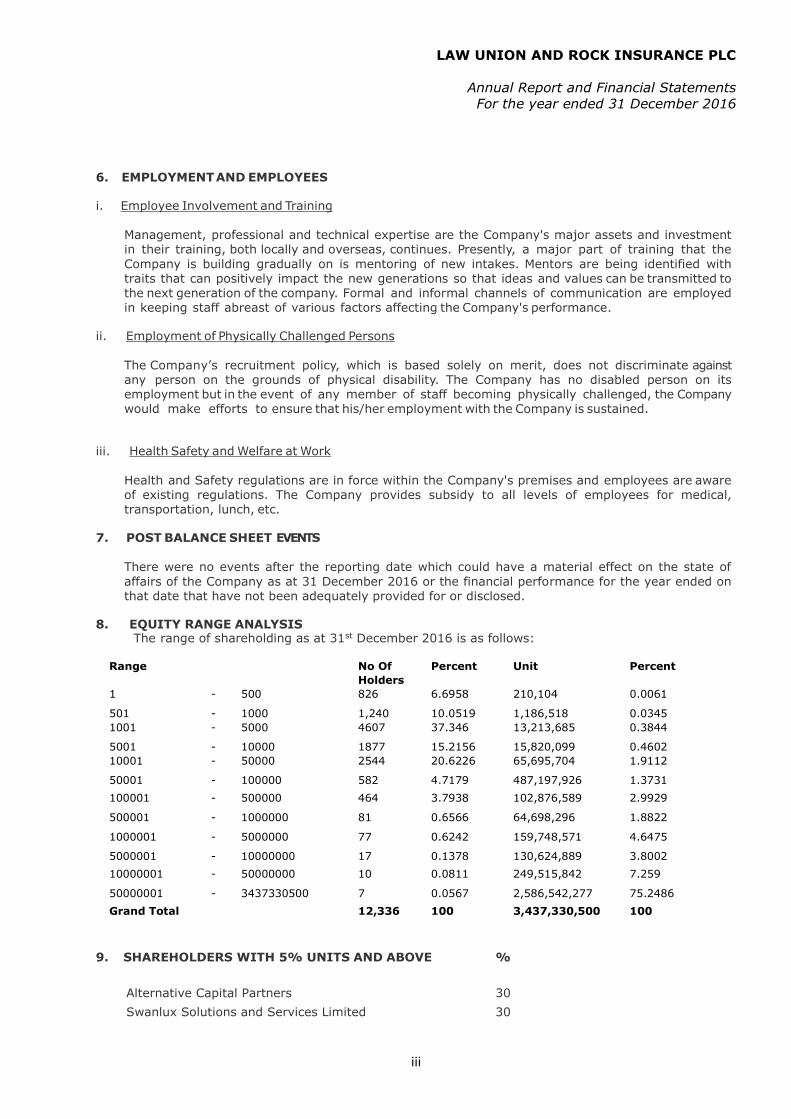

6. EMPLOYMENT AND EMPLOYEES

i. Employee Involvement and Training

Management, professional and technical expertise are the Company's major assets and investment in their training, both locally and overseas, continues. Presently, a major part of training that the

Company is building gradually on is mentoring of new intakes. Mentors are being identified with traits that can positively impact the new generations so that ideas and values can be transmitted to the next generation of the company. Formal and informal channels of communication are employed in keeping staff abreast of various factors affecting the Company's performance.

ii. Employment of Physically Challenged Persons

The Company’s recruitment policy, which is based solely on merit, does not discriminate against any person on the grounds of physical disability. The Company has no disabled person on its employment but in the event of any member of staff becoming physically challenged, the Company would make efforts to ensure that his/her employment with the Company is sustained.

iii. Health Safety and Welfare at Work

Health and Safety regulations are in force within the Company's premises and employees are aware of existing regulations. The Company provides subsidy to all levels of employees for medical, transportation, lunch, etc.

7. POST BALANCE SHEET EVENTS

There were no events after the reporting date which could have a material effect on the state of

affairs of the Company as at 31 December 2016 or the financial performance for the year ended on that date that have not been adequately provided for or disclosed.

8. EQUITY RANGE ANALYSIS The range of shareholding as at 31st December 2016 is as follows:

Range No Of

Holders

Percent Unit Percent

1 - 500 826 6.6958 210,104 0.0061

501 - 1000 1,240 10.0519 1,186,518 0.0345

1001 - 5000 4607 37.346 13,213,685 0.3844

5001 - 10000 1877 15.2156 15,820,099 0.4602

10001 - 50000 2544 20.6226 65,695,704 1.9112

50001 - 100000 582 4.7179 487,197,926 1.3731

100001 - 500000 464 3.7938 102,876,589 2.9929

500001 - 1000000 81 0.6566 64,698,296 1.8822

1000001 - 5000000 77 0.6242 159,748,571 4.6475

5000001 - 10000000 17 0.1378 130,624,889 3.8002

10000001 - 50000000 10 0.0811 249,515,842 7.259

50000001 - 3437330500 7 0.0567 2,586,542,277 75.2486

Grand Total 12,336 100 3,437,330,500 100

9. SHAREHOLDERS WITH 5% UNITS AND ABOVE %

Alternative Capital Partners 30

Swanlux Solutions and Services Limited 30

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

iv

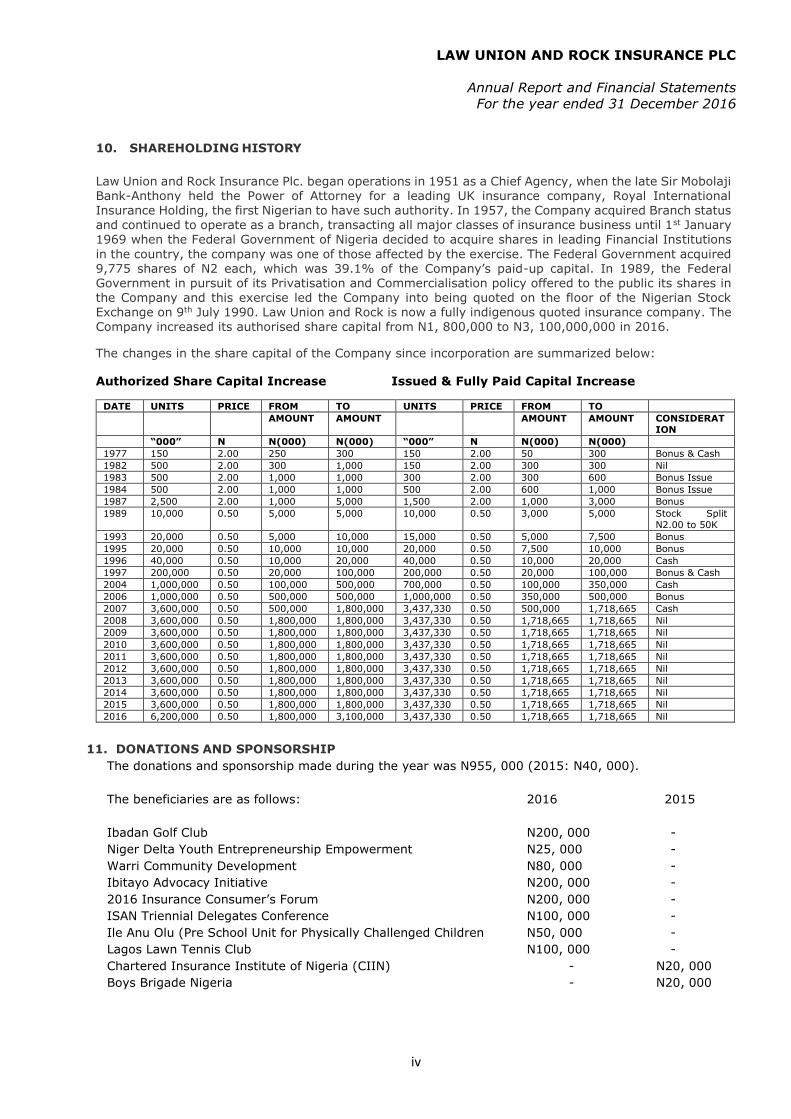

10. SHAREHOLDING HISTORY

Law Union and Rock Insurance Plc. began operations in 1951 as a Chief Agency, when the late Sir Mobolaji Bank-Anthony held the Power of Attorney for a leading UK insurance company, Royal International Insurance Holding, the first Nigerian to have such authority. In 1957, the Company acquired Branch status and continued to operate as a branch, transacting all major classes of insurance business until 1st January 1969 when the Federal Government of Nigeria decided to acquire shares in leading Financial Institutions

in the country, the company was one of those affected by the exercise. The Federal Government acquired 9,775 shares of N2 each, which was 39.1% of the Company’s paid-up capital. In 1989, the Federal Government in pursuit of its Privatisation and Commercialisation policy offered to the public its shares in the Company and this exercise led the Company into being quoted on the floor of the Nigerian Stock Exchange on 9th July 1990. Law Union and Rock is now a fully indigenous quoted insurance company. The

Company increased its authorised share capital from N1, 800,000 to N3, 100,000,000 in 2016. The changes in the share capital of the Company since incorporation are summarized below:

Authorized Share Capital Increase Issued & Fully Paid Capital Increase

DATE UNITS PRICE FROM TO UNITS PRICE FROM TO

AMOUNT AMOUNT AMOUNT AMOUNT CONSIDERAT

ION

“000” N N(000) N(000) “000” N N(000) N(000)

1977 150 2.00 250 300 150 2.00 50 300 Bonus & Cash

1982 500 2.00 300 1,000 150 2.00 300 300 Nil

1983 500 2.00 1,000 1,000 300 2.00 300 600 Bonus Issue

1984 500 2.00 1,000 1,000 500 2.00 600 1,000 Bonus Issue

1987 2,500 2.00 1,000 5,000 1,500 2.00 1,000 3,000 Bonus

1989 10,000 0.50 5,000 5,000 10,000 0.50 3,000 5,000 Stock Split

N2.00 to 50K

1993 20,000 0.50 5,000 10,000 15,000 0.50 5,000 7,500 Bonus

1995 20,000 0.50 10,000 10,000 20,000 0.50 7,500 10,000 Bonus

1996 40,000 0.50 10,000 20,000 40,000 0.50 10,000 20,000 Cash

1997 200,000 0.50 20,000 100,000 200,000 0.50 20,000 100,000 Bonus & Cash

2004 1,000,000 0.50 100,000 500,000 700,000 0.50 100,000 350,000 Cash

2006 1,000,000 0.50 500,000 500,000 1,000,000 0.50 350,000 500,000 Bonus

2007 3,600,000 0.50 500,000 1,800,000 3,437,330 0.50 500,000 1,718,665 Cash

2008 3,600,000 0.50 1,800,000 1,800,000 3,437,330 0.50 1,718,665 1,718,665 Nil

2009 3,600,000 0.50 1,800,000 1,800,000 3,437,330 0.50 1,718,665 1,718,665 Nil

2010 3,600,000 0.50 1,800,000 1,800,000 3,437,330 0.50 1,718,665 1,718,665 Nil

2011 3,600,000 0.50 1,800,000 1,800,000 3,437,330 0.50 1,718,665 1,718,665 Nil

2012 3,600,000 0.50 1,800,000 1,800,000 3,437,330 0.50 1,718,665 1,718,665 Nil

2013 3,600,000 0.50 1,800,000 1,800,000 3,437,330 0.50 1,718,665 1,718,665 Nil

2014 3,600,000 0.50 1,800,000 1,800,000 3,437,330 0.50 1,718,665 1,718,665 Nil

2015 3,600,000 0.50 1,800,000 1,800,000 3,437,330 0.50 1,718,665 1,718,665 Nil

2016 6,200,000 0.50 1,800,000 3,100,000 3,437,330 0.50 1,718,665 1,718,665 Nil

11. DONATIONS AND SPONSORSHIP

The donations and sponsorship made during the year was N955, 000 (2015: N40, 000).

The beneficiaries are as follows: 2016 2015

Ibadan Golf Club N200, 000 -

Niger Delta Youth Entrepreneurship Empowerment N25, 000 -

Warri Community Development N80, 000 -

Ibitayo Advocacy Initiative N200, 000 -

2016 Insurance Consumer’s Forum N200, 000 -

ISAN Triennial Delegates Conference N100, 000 -

Ile Anu Olu (Pre School Unit for Physically Challenged Children N50, 000 -

Lagos Lawn Tennis Club N100, 000 -

Chartered Insurance Institute of Nigeria (CIIN) - N20, 000

Boys Brigade Nigeria - N20, 000

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

v

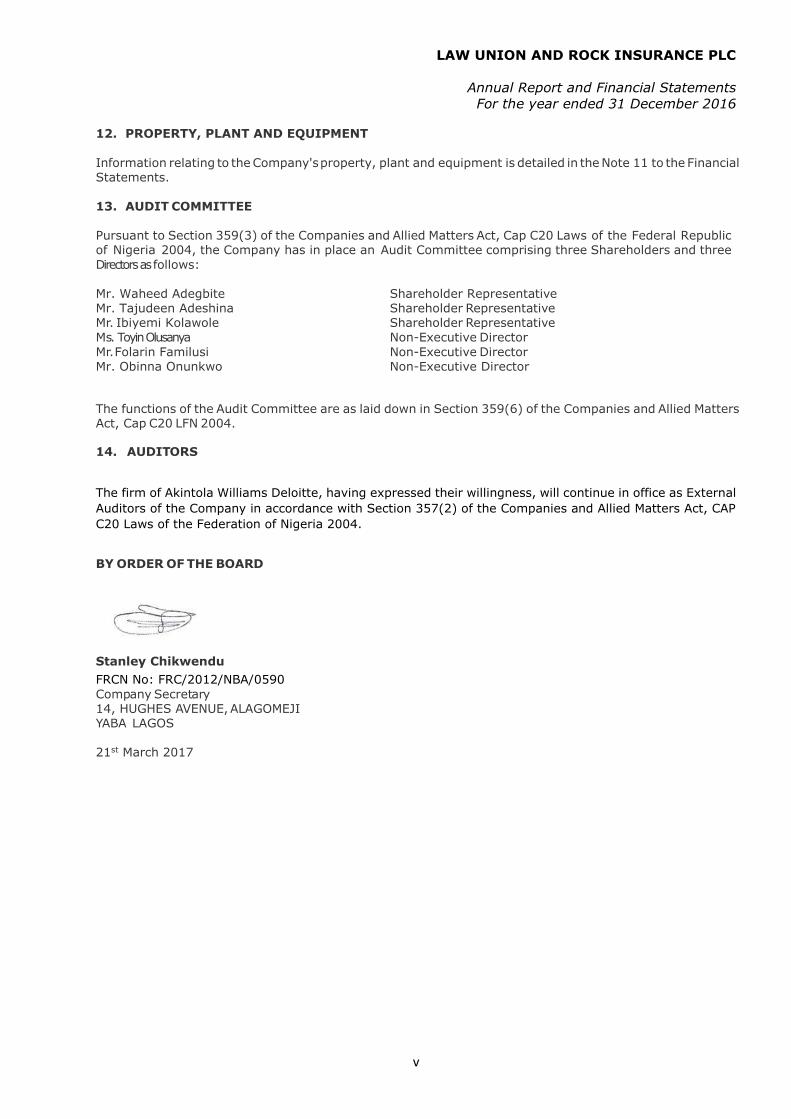

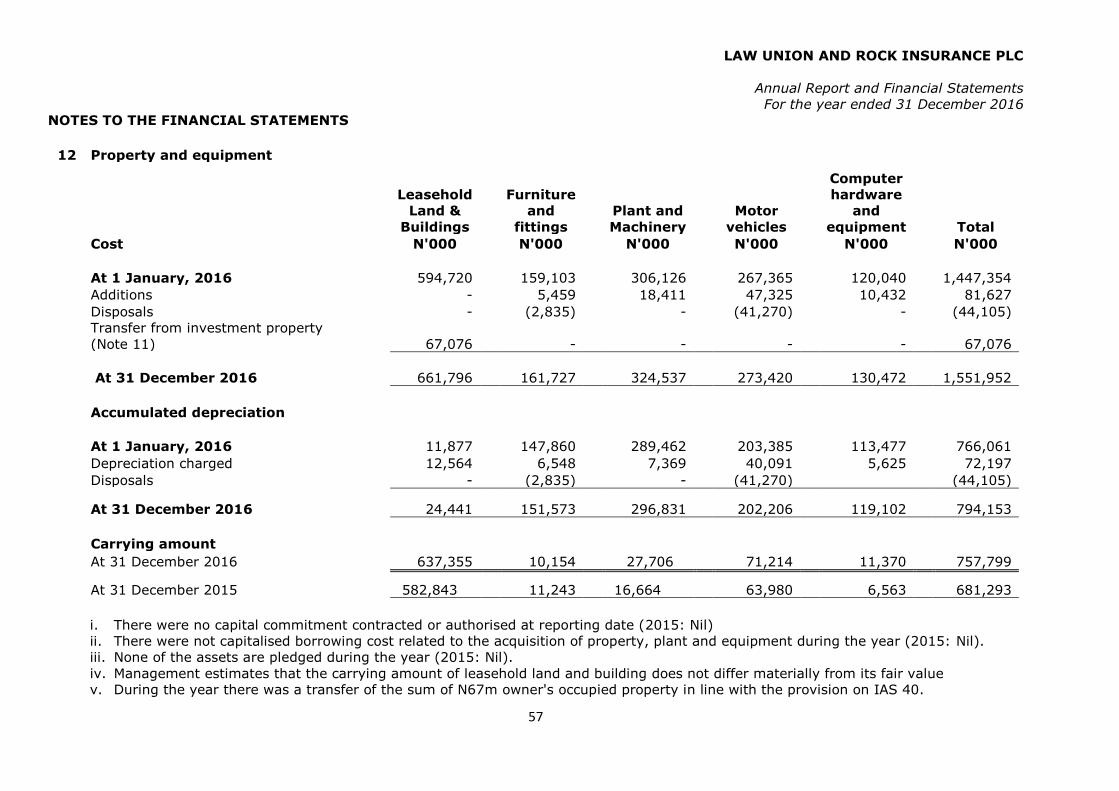

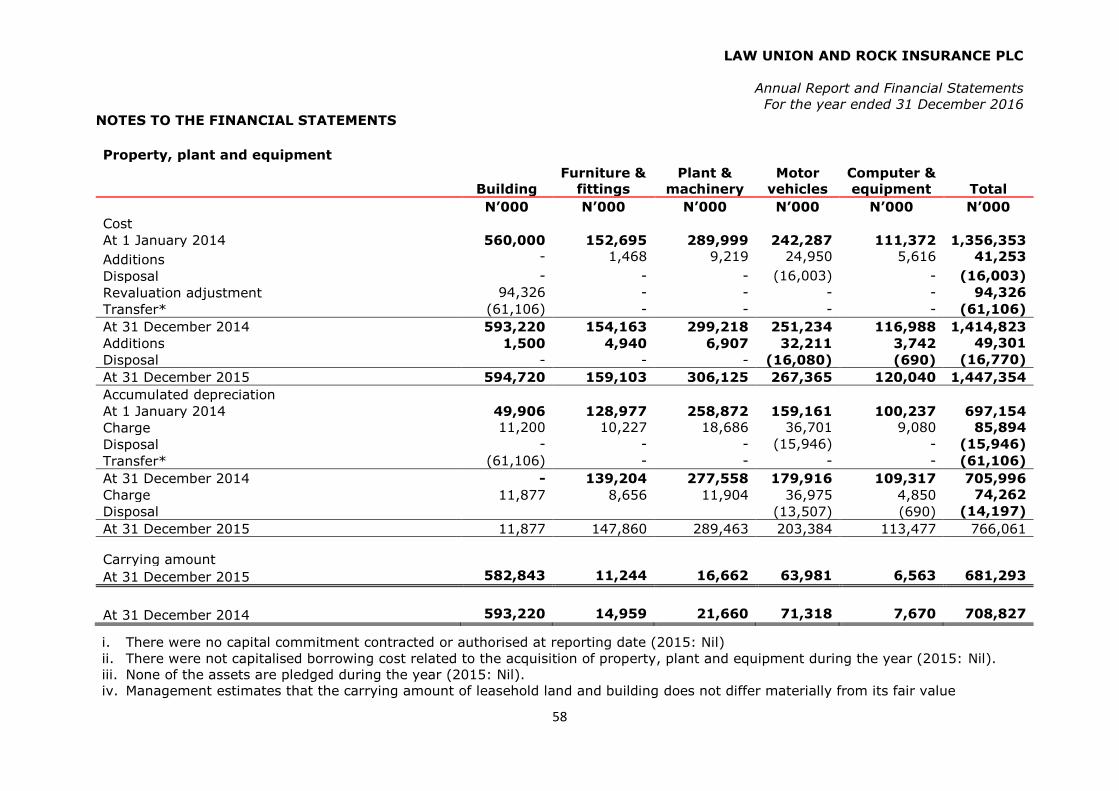

12. PROPERTY, PLANT AND EQUIPMENT

Information relating to the Company's property, plant and equipment is detailed in the Note 11 to the Financial Statements. 13. AUDIT COMMITTEE

Pursuant to Section 359(3) of the Companies and Allied Matters Act, Cap C20 Laws of the Federal Republic of Nigeria 2004, the Company has in place an Audit Committee comprising three Shareholders and three

Directors as follows: Mr. Waheed Adegbite Shareholder Representative Mr. Tajudeen Adeshina Shareholder Representative Mr. Ibiyemi Kolawole Shareholder Representative

Ms. Toyin Olusanya Non-Executive Director

Mr. Folarin Familusi Non-Executive Director Mr. Obinna Onunkwo Non-Executive Director

The functions of the Audit Committee are as laid down in Section 359(6) of the Companies and Allied Matters Act, Cap C20 LFN 2004.

14. AUDITORS

The firm of Akintola Williams Deloitte, having expressed their willingness, will continue in office as External

Auditors of the Company in accordance with Section 357(2) of the Companies and Allied Matters Act, CAP

C20 Laws of the Federation of Nigeria 2004.

BY ORDER OF THE BOARD

Stanley Chikwendu

FRCN No: FRC/2012/NBA/0590

Company Secretary 14, HUGHES AVENUE, ALAGOMEJI YABA LAGOS 21st March 2017

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

vi

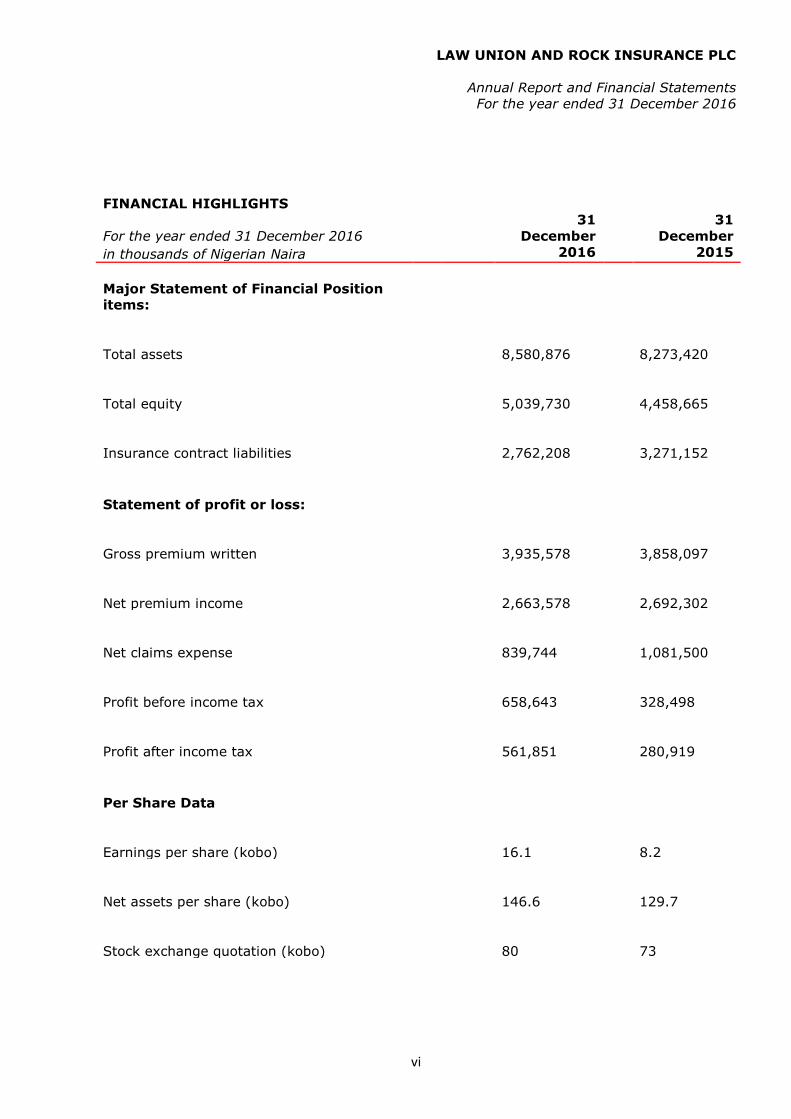

FINANCIAL HIGHLIGHTS

For the year ended 31 December 2016

31

December

31

December

in thousands of Nigerian Naira 2016 2015

Major Statement of Financial Position

items:

Total assets

8,580,876

8,273,420

Total equity

5,039,730

4,458,665

Insurance contract liabilities

2,762,208

3,271,152

Statement of profit or loss:

Gross premium written

3,935,578

3,858,097

Net premium income

2,663,578

2,692,302

Net claims expense

839,744

1,081,500

Profit before income tax

658,643

328,498

Profit after income tax

561,851

280,919

Per Share Data

Earnings per share (kobo)

16.1

8.2

Net assets per share (kobo)

146.6

129.7

Stock exchange quotation (kobo)

80

73

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

1

CORPORATE INFORMATION

DIRECTORS APPOINTMENT DATE Mr. Remi Babalola 1/6/2012 Mr. Ajibola Olayinka 24/07/2014 Mr. Victor Faleye 1/6/2012 Mrs. Funmi Ekundayo 16/08/2012 Mr. Obinna Onunkwo 4/26/2013 Ms Toyin Olusanya 1/6/2012 Mr. Akinjide Orimolade 21/10/2014 Mrs. Funmi Ekundayo 16/08/2012 Mr. Folarin Familusi 24/07/2014

SECRETARY: Stanley Chikwendu Date of Appointment 15 October, 2012 RC No. RC.6286 FRC No. FRC/2012/NBA/0590

REGISTERED OFFICE: 14, Hughes Avenue, Alagomeji, Yaba, Lagos.

BANKERS Skye Bank Plc

Zenith Bank Plc

Ecobank Plc

Diamond Bank

Unity Bank

Union Bank

Auditors: Akintola Williams Deloitte

Civic Towers, Plot GA 1

Ozumba Mbadiwe Avenue

Victoria Island, Lagos

Nigeria

REINSURERS: Munich Reinsurance Company Of Africa Ltd

African Reinsurance Corporation

Continental Reinsurance Plc

Waica Reinsurance Corporation

Aveni Reinsurance Co Ltd

Nigeria Reinsurance Corporation

REPORTING ACTUARY HR Nigeria Limited

7th Floor, AIICO Plaza, Afribank Street, Victoria Island, Lagos.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

2

BRANCH OFFICES ADRRESS Ikeja Adol House (1st Floor), Plot 15 CIPM Road, Central Business

District, Alausa Ikeja, Lagos.

Festac PIN Plaza, 1st Avenue, Festac Town, Lagos.

Victoria Island/Lekki 209 Muri Okunola, Behind Ajose Adeogun, Victoria Island, Lagos.

Ibadan 2nd Floor Broking House, 1 Alhaji Jimoh Odutola Road, Dugbe,

Ibadan, Oyo State.

Kano Office Skye Bank PLC, 4E, Bello road, Kano, Kano State.

Kaduna Office Oando Building, 4 Constitution Road, Kaduna

Oshogbo

Jesus Court, 2nd Floor (Left Wing), 6 Isiaka Adeleke Freeway,

Okefia, Oshogbo.

Port Harcourt Skye Bank Building , 89, Aba Road, Garrison Junction, Port

Harcourt, Rivers State.

Calabar (Retail Office) Skye Bank Plc, 41 Muritala Mohammed Way, Calabar.

Uyo 164, Oron Road, Uyo.

Warri 60 Effurun/Sapele Road, Effurun, Warri, Delta State.

Benin (Retail Office) Skye Bank Building, 1 Forestry Road, Benin City.

Onitsha (Retail Office) Skye Bank Plc, Head Bridge Branch, 42 Port Harcourt Road, Fegge

Onitsha, Anambra State.

Abuja Block B, Suite 3, 1st Floor, 79 Adetokunbo Ademola Crescent,

Wuse II Abuja, FCT.

Kano Skye Bank PLC, 23 Bello road, Kano, Kano State.

Kaduna Oando Building, 4 Construction Road, Kaduna.

Minna 1 Saidu Yabagi/Bosso Road, Opposite Muritala Park, P. O. Box

1369, Minna.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

3

STATEMENT OF DIRECTORS’ RESPONSIBILITIES

The Companies and Allied Matters Act, Cap C20 Laws of the Federation of Nigeria 2004, requires

the Directors to prepare financial statements for each financial year that present fairly, in all

material respects, state of financial affairs of the Company at the end of the year and of its profit

or loss. The responsibilities include ensuring that the Company:

a. keeps proper records that disclose, with reasonable accuracy, the financial position of the

Company and comply with the requirements of International Financial Reporting Standards,

provisions of the Companies and Allied Matters Act, Cap C20 Laws of the Federation of

Nigeria 2004, the Insurance Act 2003, relevant policy guidelines issued by the National

Insurance Commission (NAICOM) and the Financial Reporting Council of Nigeria Act No. 6,

2011;

b. establishes adequate internal controls to safeguard assets and to prevent and detect fraud

and other irregularities; and

c. prepares its financial statements using suitable accounting policies supported by reasonable

and prudent judgments and estimates, and are consistently applied.

The Directors accept responsibility for the annual financial statements, which have been

prepared using appropriate accounting policies supported by reasonable and prudent judgments

and estimates, in conformity with the International Financial Reporting Standards, provisions of

the Companies and Allied Matters Act Cap C20 Laws of the Federation of Nigeria 2004, the

Insurance Act 203, relevant policy guidelines issued by the National Insurance Commission

(NAICOM) and the Financial Reporting Council of Nigeria Act No.6, 2011.

The Directors are of the opinion that the financial statements present fairly, in all material

respects, the state of the financial affairs of the Company and of its profit or loss. The Directors

further accept responsibility for the maintenance of accounting records that may be relied upon

in the preparation of the financial statements, as well as adequate systems of internal financial

control.

Nothing has come to the attention of the Directors to indicate that the Company will not remain

a going concern for at least twelve months from the date of this statement.

_________________________ __________________________

Remi Babalola Jide Orimolade

Chairman Managing Director /CEO

FRC/2013/ICAN/00000003542 FRC/2013/CIIN/2268

Approved on 21st March 2017

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

4

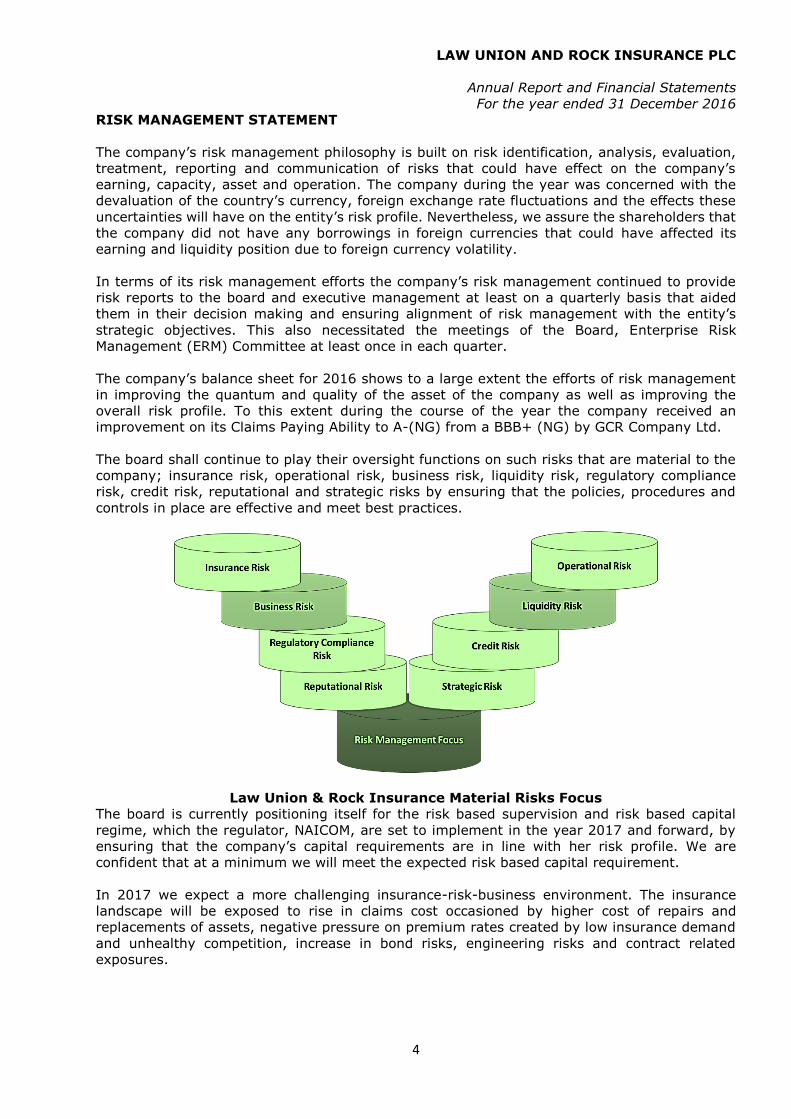

RISK MANAGEMENT STATEMENT

The company’s risk management philosophy is built on risk identification, analysis, evaluation,

treatment, reporting and communication of risks that could have effect on the company’s

earning, capacity, asset and operation. The company during the year was concerned with the

devaluation of the country’s currency, foreign exchange rate fluctuations and the effects these

uncertainties will have on the entity’s risk profile. Nevertheless, we assure the shareholders that

the company did not have any borrowings in foreign currencies that could have affected its

earning and liquidity position due to foreign currency volatility.

In terms of its risk management efforts the company’s risk management continued to provide

risk reports to the board and executive management at least on a quarterly basis that aided

them in their decision making and ensuring alignment of risk management with the entity’s

strategic objectives. This also necessitated the meetings of the Board, Enterprise Risk

Management (ERM) Committee at least once in each quarter.

The company’s balance sheet for 2016 shows to a large extent the efforts of risk management

in improving the quantum and quality of the asset of the company as well as improving the

overall risk profile. To this extent during the course of the year the company received an

improvement on its Claims Paying Ability to A-(NG) from a BBB+ (NG) by GCR Company Ltd.

The board shall continue to play their oversight functions on such risks that are material to the

company; insurance risk, operational risk, business risk, liquidity risk, regulatory compliance

risk, credit risk, reputational and strategic risks by ensuring that the policies, procedures and

controls in place are effective and meet best practices.

Law Union & Rock Insurance Material Risks Focus

The board is currently positioning itself for the risk based supervision and risk based capital

regime, which the regulator, NAICOM, are set to implement in the year 2017 and forward, by

ensuring that the company’s capital requirements are in line with her risk profile. We are

confident that at a minimum we will meet the expected risk based capital requirement.

In 2017 we expect a more challenging insurance-risk-business environment. The insurance

landscape will be exposed to rise in claims cost occasioned by higher cost of repairs and

replacements of assets, negative pressure on premium rates created by low insurance demand

and unhealthy competition, increase in bond risks, engineering risks and contract related

exposures.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

5

The company shall continually ensure that risk methodologies utilized in assessing and

appraising her risks are continually upgraded and that her risk uncertainties are reduced to an

appreciable level (its risk appetite) through proper risk treatments options.

Furthermore, the board and executive management shall work proactively to ensure that

governance, risk and compliance objectives and tailored towards principled performance. This

will believe is intrinsic in creating a sustainable shareholders’ value.

_______________________________

Mr. Obinna Onunkwo

Chairman, Board ERM Committee

FRC/2013/IODN/00000003520

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

6

REPORT OF THE STATUTORY AUDIT COMMITTEE

To the members of Law Union & Rock Insurance Plc.

In accordance with the International Financial Reporting Standards, provisions of the Companies

and Allied Matters Act, Cap C20 Laws of the Federation of Nigeria, 2004, the Insurance Act 2003,

relevant policy guidelines issues by the National Insurance Commission (NAICOM) and the

Financial Reporting Council of Nigeria Act No. 6, 2011, the members of the Statutory Audit

Committee of Law Union & Rock Insurance Plc. hereby report as follows:

We have exercised our statutory functions under Section 359(6) of the Companies and

Allied Matters Act, Cap C20, Laws of the Federation of Nigeria 2004 and we acknowledge

the co-operation of management and staff in the conduct of these responsibilities.

We confirm that the accounting and reporting policies of the Company are in accordance

with legal requirements and agreed ethical practices and that the scope and planning of

both the external and internal audits for the year ended 31st December 2016 were

satisfactory, and reinforce the Company’s internal control systems.

We have deliberated with external auditors, who have confirmed that necessary co-

operation was received from management in the course of their statutory audit and we are

satisfied with the management’s response to the external auditors’ recommendations on

accounting and internal control matters and with the effectiveness of the Company’s

system of accounting and internal control.

21st March 2017

Members of the Audit Committee are:

1. Mr. Waheed Adegbite – Chairman

2. Mr. Tajudeen Adeshina

3. Mr. Ibiyemi Kolawole

4. Mr. Folarin Familusi

5. Ms Toyin Olusanya

6. Mr. Obinna Onunkwo

Secretary to the Committee

Mr. Stanley Chikwendu

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

8

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

9

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

10

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

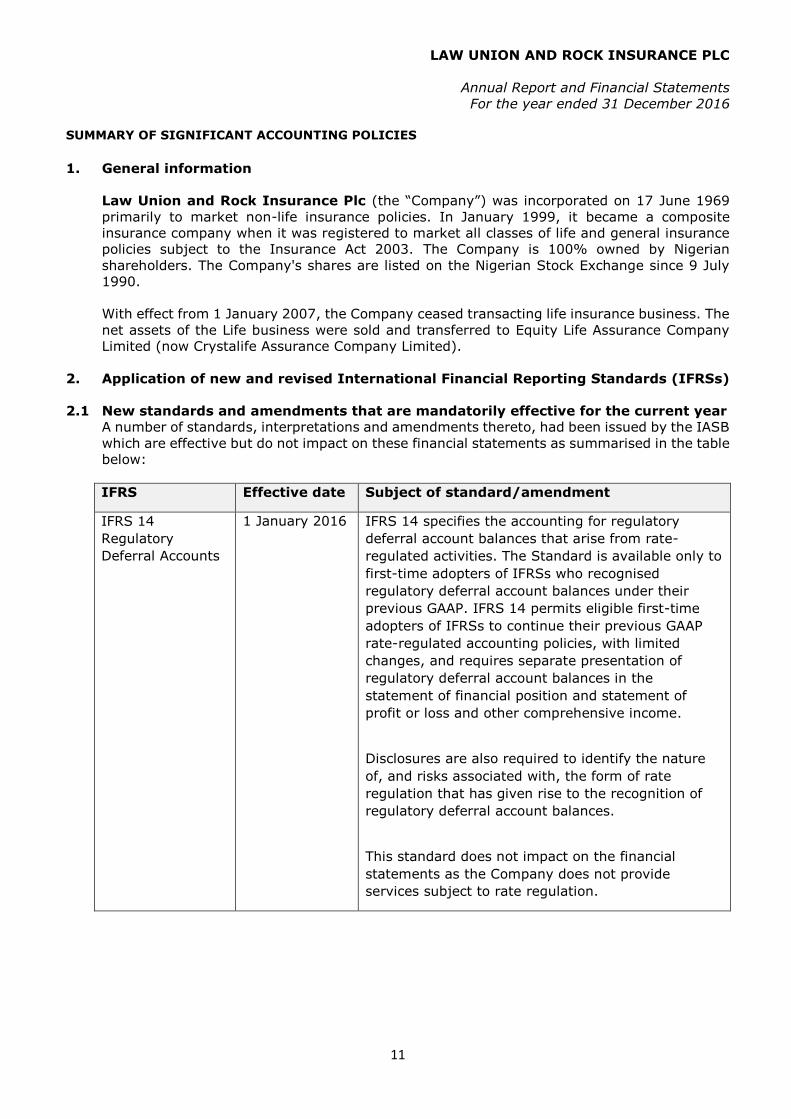

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

11

1. General information

Law Union and Rock Insurance Plc (the “Company”) was incorporated on 17 June 1969

primarily to market non-life insurance policies. In January 1999, it became a composite

insurance company when it was registered to market all classes of life and general insurance

policies subject to the Insurance Act 2003. The Company is 100% owned by Nigerian

shareholders. The Company's shares are listed on the Nigerian Stock Exchange since 9 July

1990.

With effect from 1 January 2007, the Company ceased transacting life insurance business. The

net assets of the Life business were sold and transferred to Equity Life Assurance Company

Limited (now Crystalife Assurance Company Limited).

2. Application of new and revised International Financial Reporting Standards (IFRSs)

2.1 New standards and amendments that are mandatorily effective for the current year

A number of standards, interpretations and amendments thereto, had been issued by the IASB

which are effective but do not impact on these financial statements as summarised in the table

below:

IFRS Effective date Subject of standard/amendment

IFRS 14

Regulatory

Deferral Accounts

1 January 2016 IFRS 14 specifies the accounting for regulatory

deferral account balances that arise from rate-

regulated activities. The Standard is available only to

first-time adopters of IFRSs who recognised

regulatory deferral account balances under their

previous GAAP. IFRS 14 permits eligible first-time

adopters of IFRSs to continue their previous GAAP

rate-regulated accounting policies, with limited

changes, and requires separate presentation of

regulatory deferral account balances in the

statement of financial position and statement of

profit or loss and other comprehensive income.

Disclosures are also required to identify the nature

of, and risks associated with, the form of rate

regulation that has given rise to the recognition of

regulatory deferral account balances.

This standard does not impact on the financial

statements as the Company does not provide

services subject to rate regulation.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

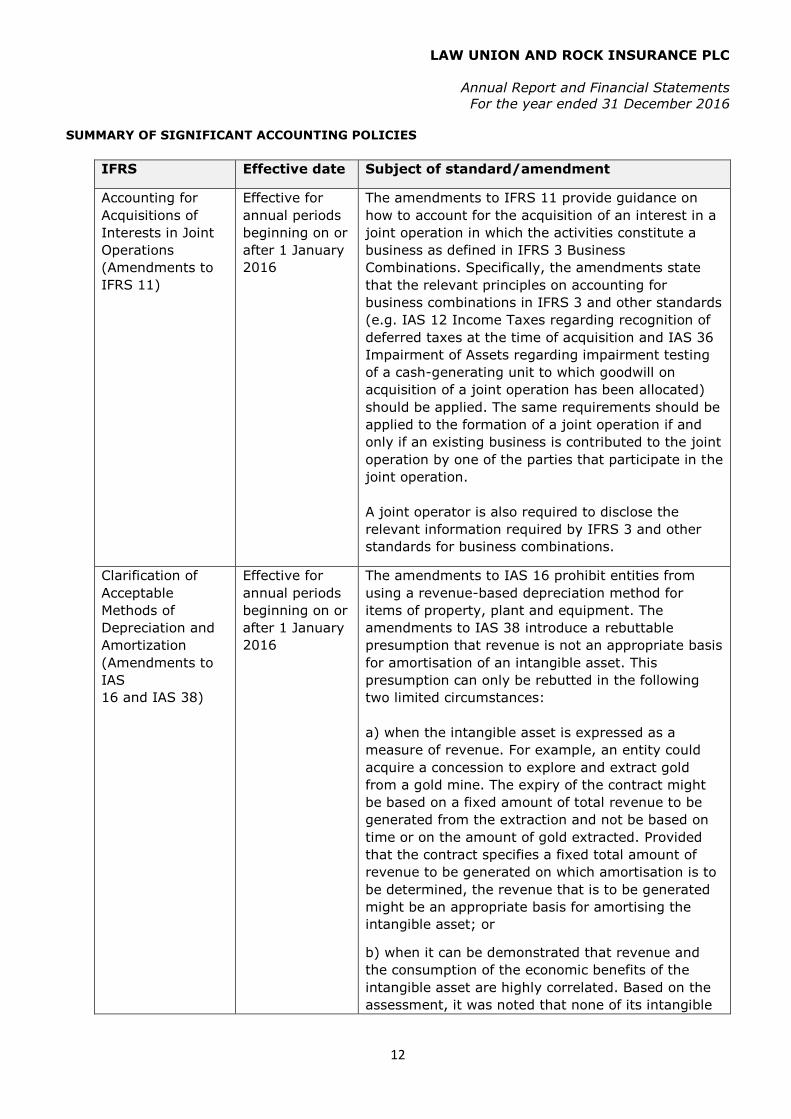

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

12

IFRS Effective date Subject of standard/amendment

Accounting for

Acquisitions of

Interests in Joint

Operations

(Amendments to

IFRS 11)

Effective for

annual periods

beginning on or

after 1 January

2016

The amendments to IFRS 11 provide guidance on

how to account for the acquisition of an interest in a

joint operation in which the activities constitute a

business as defined in IFRS 3 Business

Combinations. Specifically, the amendments state

that the relevant principles on accounting for

business combinations in IFRS 3 and other standards

(e.g. IAS 12 Income Taxes regarding recognition of

deferred taxes at the time of acquisition and IAS 36

Impairment of Assets regarding impairment testing

of a cash-generating unit to which goodwill on

acquisition of a joint operation has been allocated)

should be applied. The same requirements should be

applied to the formation of a joint operation if and

only if an existing business is contributed to the joint

operation by one of the parties that participate in the

joint operation.

A joint operator is also required to disclose the

relevant information required by IFRS 3 and other

standards for business combinations.

Clarification of

Acceptable

Methods of

Depreciation and

Amortization

(Amendments to

IAS

16 and IAS 38)

Effective for

annual periods

beginning on or

after 1 January

2016

The amendments to IAS 16 prohibit entities from

using a revenue-based depreciation method for

items of property, plant and equipment. The

amendments to IAS 38 introduce a rebuttable

presumption that revenue is not an appropriate basis

for amortisation of an intangible asset. This

presumption can only be rebutted in the following

two limited circumstances:

a) when the intangible asset is expressed as a

measure of revenue. For example, an entity could

acquire a concession to explore and extract gold

from a gold mine. The expiry of the contract might

be based on a fixed amount of total revenue to be

generated from the extraction and not be based on

time or on the amount of gold extracted. Provided

that the contract specifies a fixed total amount of

revenue to be generated on which amortisation is to

be determined, the revenue that is to be generated

might be an appropriate basis for amortising the

intangible asset; or

b) when it can be demonstrated that revenue and

the consumption of the economic benefits of the

intangible asset are highly correlated. Based on the

assessment, it was noted that none of its intangible

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

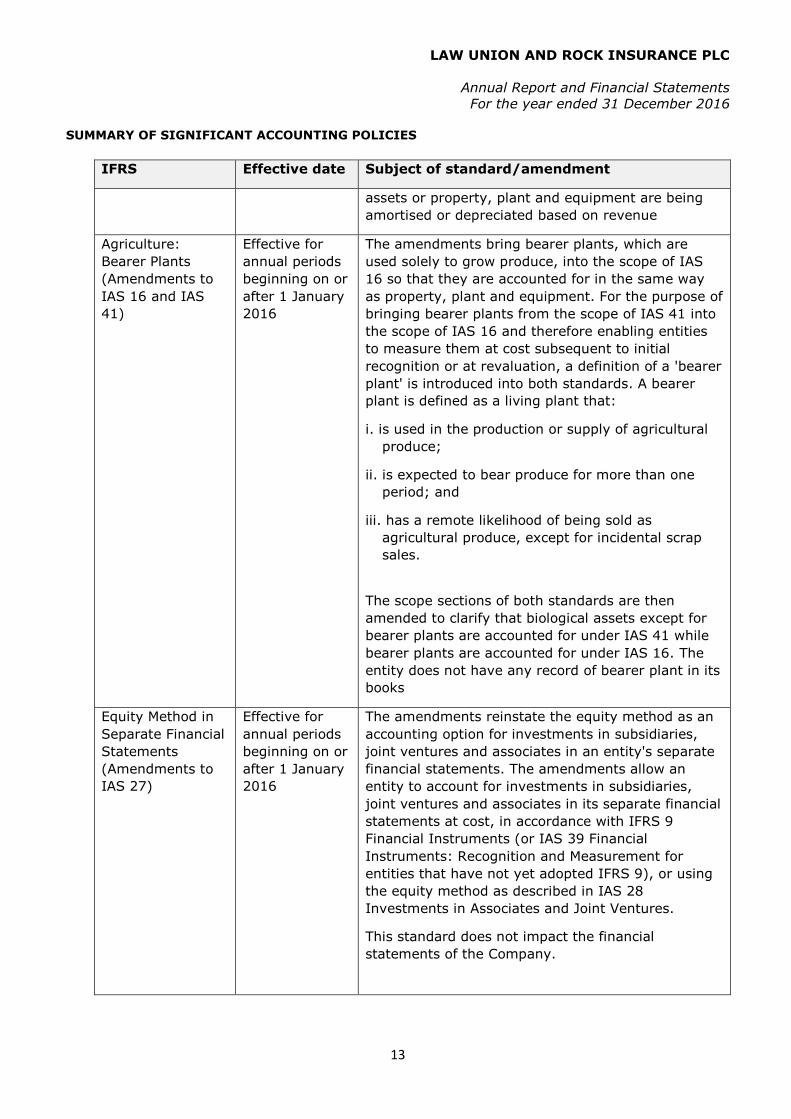

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

13

IFRS Effective date Subject of standard/amendment

assets or property, plant and equipment are being

amortised or depreciated based on revenue

Agriculture:

Bearer Plants

(Amendments to

IAS 16 and IAS

41)

Effective for

annual periods

beginning on or

after 1 January

2016

The amendments bring bearer plants, which are

used solely to grow produce, into the scope of IAS

16 so that they are accounted for in the same way

as property, plant and equipment. For the purpose of

bringing bearer plants from the scope of IAS 41 into

the scope of IAS 16 and therefore enabling entities

to measure them at cost subsequent to initial

recognition or at revaluation, a definition of a 'bearer

plant' is introduced into both standards. A bearer

plant is defined as a living plant that:

i. is used in the production or supply of agricultural

produce;

ii. is expected to bear produce for more than one

period; and

iii. has a remote likelihood of being sold as

agricultural produce, except for incidental scrap

sales.

The scope sections of both standards are then

amended to clarify that biological assets except for

bearer plants are accounted for under IAS 41 while

bearer plants are accounted for under IAS 16. The

entity does not have any record of bearer plant in its

books

Equity Method in

Separate Financial

Statements

(Amendments to

IAS 27)

Effective for

annual periods

beginning on or

after 1 January

2016

The amendments reinstate the equity method as an

accounting option for investments in subsidiaries,

joint ventures and associates in an entity's separate

financial statements. The amendments allow an

entity to account for investments in subsidiaries,

joint ventures and associates in its separate financial

statements at cost, in accordance with IFRS 9

Financial Instruments (or IAS 39 Financial

Instruments: Recognition and Measurement for

entities that have not yet adopted IFRS 9), or using

the equity method as described in IAS 28

Investments in Associates and Joint Ventures.

This standard does not impact the financial

statements of the Company.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

14

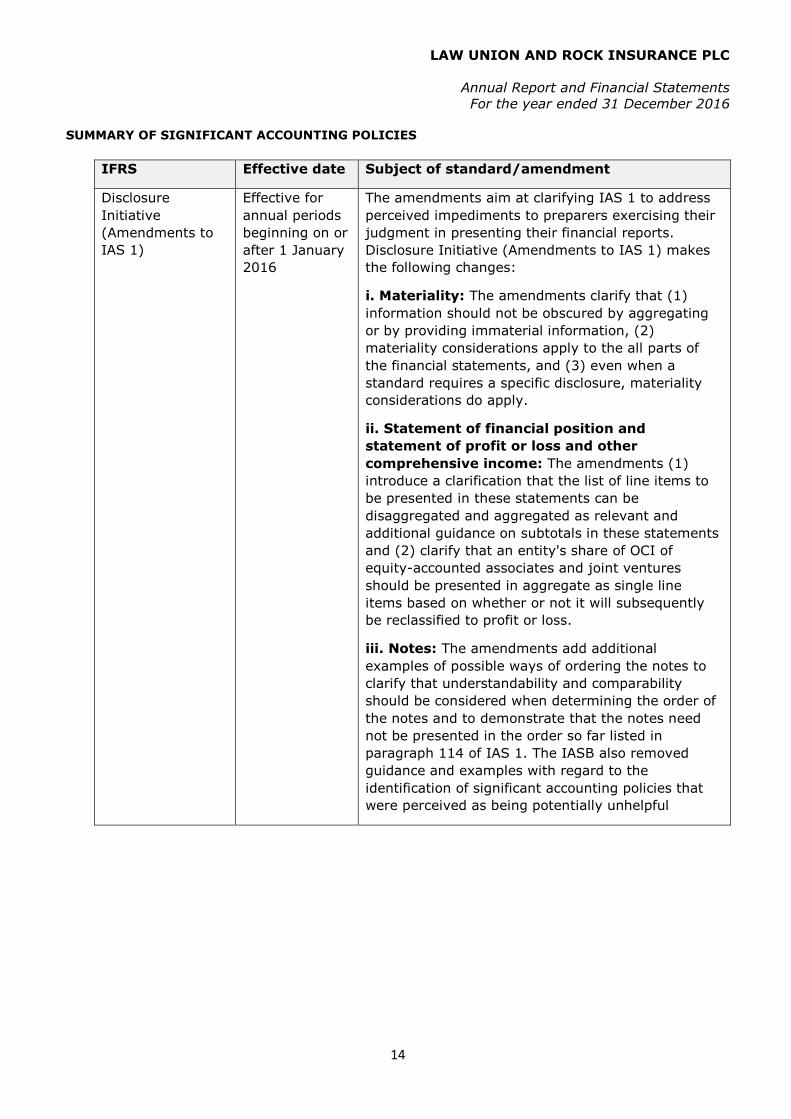

IFRS Effective date Subject of standard/amendment

Disclosure

Initiative

(Amendments to

IAS 1)

Effective for

annual periods

beginning on or

after 1 January

2016

The amendments aim at clarifying IAS 1 to address

perceived impediments to preparers exercising their

judgment in presenting their financial reports.

Disclosure Initiative (Amendments to IAS 1) makes

the following changes:

i. Materiality: The amendments clarify that (1)

information should not be obscured by aggregating

or by providing immaterial information, (2)

materiality considerations apply to the all parts of

the financial statements, and (3) even when a

standard requires a specific disclosure, materiality

considerations do apply.

ii. Statement of financial position and

statement of profit or loss and other

comprehensive income: The amendments (1)

introduce a clarification that the list of line items to

be presented in these statements can be

disaggregated and aggregated as relevant and

additional guidance on subtotals in these statements

and (2) clarify that an entity's share of OCI of

equity-accounted associates and joint ventures

should be presented in aggregate as single line

items based on whether or not it will subsequently

be reclassified to profit or loss.

iii. Notes: The amendments add additional

examples of possible ways of ordering the notes to

clarify that understandability and comparability

should be considered when determining the order of

the notes and to demonstrate that the notes need

not be presented in the order so far listed in

paragraph 114 of IAS 1. The IASB also removed

guidance and examples with regard to the

identification of significant accounting policies that

were perceived as being potentially unhelpful

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

15

IFRS Effective date Subject of standard/amendment

Investment

Entities: Applying

the Consolidation

Exception

(Amendments to

IFRS 10, IFRS 12

and IAS 28)

Effective for

annual periods

beginning on or

after 1 January

2016

The amendments address issues that have arisen in

the context of applying the consolidation exception

for investment entities. Investment Entities: The

amendments confirm that the exemption from

preparing consolidated financial statements for an

intermediate parent entity is available to a parent

entity that is a subsidiary of an investment entity,

even if the investment entity measures all of its

subsidiaries at fair value. It also states that a

subsidiary that provides services related to the

parent's investment activities should not be

consolidated if the subsidiary itself is an investment

entity. In addition, when applying the equity method

to an associate or a joint venture, a non-investment

entity investor in an investment entity may retain

the fair value measurement applied by the associate

or joint venture to its interests in subsidiaries. In

addition, an investment entity measuring all of its

subsidiaries at fair value must provide the

disclosures relating to investment entities as

required by IFRS 12.This standard does not have

impact on the operation of the company.

The above standards does not have impact on the operation of the company during the year.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

16

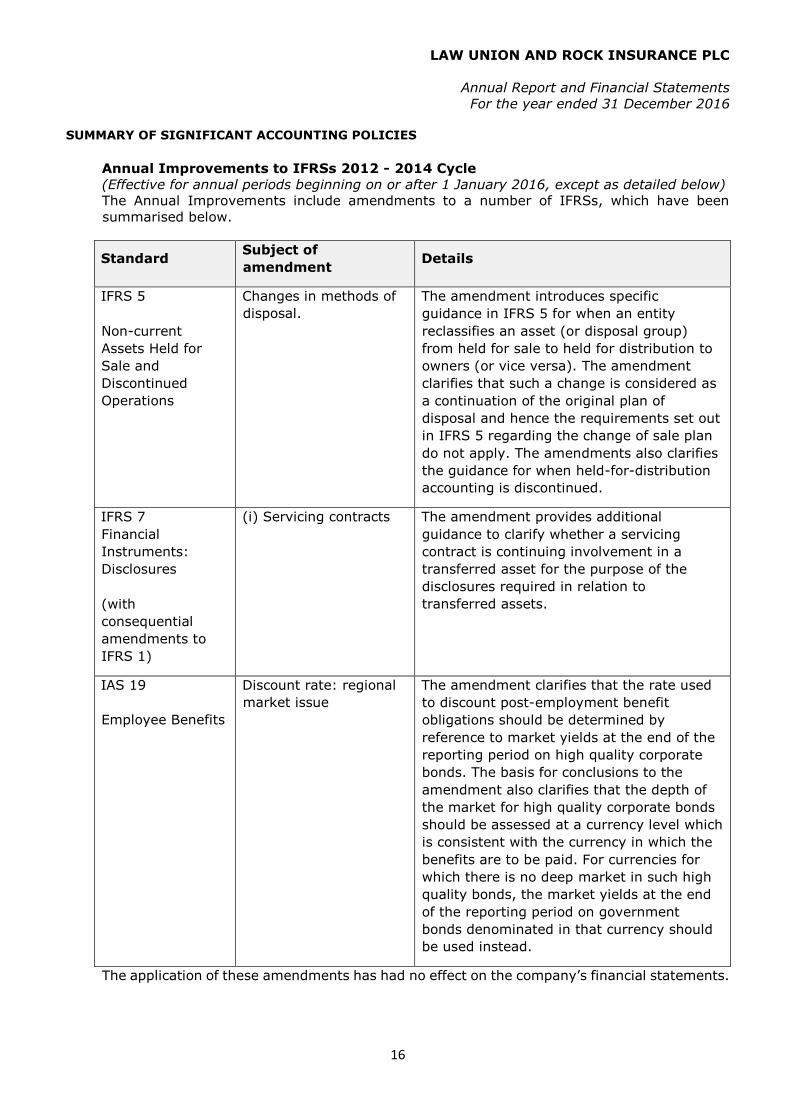

Annual Improvements to IFRSs 2012 - 2014 Cycle

(Effective for annual periods beginning on or after 1 January 2016, except as detailed below)

The Annual Improvements include amendments to a number of IFRSs, which have been

summarised below.

Standard Subject of

amendment Details

IFRS 5

Non-current

Assets Held for

Sale and

Discontinued

Operations

Changes in methods of

disposal.

The amendment introduces specific

guidance in IFRS 5 for when an entity

reclassifies an asset (or disposal group)

from held for sale to held for distribution to

owners (or vice versa). The amendment

clarifies that such a change is considered as

a continuation of the original plan of

disposal and hence the requirements set out

in IFRS 5 regarding the change of sale plan

do not apply. The amendments also clarifies

the guidance for when held-for-distribution

accounting is discontinued.

IFRS 7

Financial

Instruments:

Disclosures

(with

consequential

amendments to

IFRS 1)

(i) Servicing contracts

The amendment provides additional

guidance to clarify whether a servicing

contract is continuing involvement in a

transferred asset for the purpose of the

disclosures required in relation to

transferred assets.

IAS 19

Employee Benefits

Discount rate: regional

market issue

The amendment clarifies that the rate used

to discount post-employment benefit

obligations should be determined by

reference to market yields at the end of the

reporting period on high quality corporate

bonds. The basis for conclusions to the

amendment also clarifies that the depth of

the market for high quality corporate bonds

should be assessed at a currency level which

is consistent with the currency in which the

benefits are to be paid. For currencies for

which there is no deep market in such high

quality bonds, the market yields at the end

of the reporting period on government

bonds denominated in that currency should

be used instead.

The application of these amendments has had no effect on the company’s financial statements.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

17

2.2 New and revised IFRSs in issue that are not mandatorily effective (but allow early

application) for the year ended 31 December 2016

The company has not applied the following new and revised IFRSs that have been issued but

are not yet effective:

i. IFRS 9 Financial Instruments;

ii. IFRS 15 Revenue from Contracts with Customers;

iii. Amendments to IFRS 10 and IAS 28 Sale or Contribution of Assets between an Investor

and its Associate or Joint Venture

iv. IFRS 16 Leases

v. Amendments to IAS 12 Recognition of Deferred Tax Assets for Unrealised Losses

vi. Amendments to IAS 7 Additional disclosure on changes in financing activities

vii. Amendments to IFRS 2 Classification and Measurement of Share-based Payment

Transactions

viii. Amendments to IFRS 4 upon applying IFRS 9

2.2.1 IFRS 9 Financial Instruments

(Effective for annual periods beginning on or after 1 January 2018)

In July 2014, the IASB finalised the reform of financial instruments accounting and issued

IFRS 9 (as revised in 2014), which contains the requirements for a) the classification and

measurement of financial assets and financial liabilities, b) impairment methodology, and c)

general hedge accounting. IFRS 9 (as revised in 2014) will supersede IAS 39 Financial

Instruments: Recognition and Measurement upon its effective date.

Phase 1: Classification and measurement of financial assets and financial liabilities

With respect to the classification and measurement, the number of categories of financial

assets under IFRS 9 has been reduced; all recognised financial assets that are currently

within the scope of IAS 39 will be subsequently measured at either amortised cost or fair

value under IFRS 9. Specifically:

a debt instrument that (i) is held within a business model whose objective is to collect

the contractual cash flows and (ii) has contractual cash flows that are solely payments

of principal and interest on the principal amount outstanding must be measured at

amortised cost (net of any write down for impairment), unless the asset is designated

at fair value through profit or loss (FVTPL) under the fair value option.

a debt instrument that (i) is held within a business model whose objective is achieved

both by collecting contractual cash flows and selling financial assets and (ii) has

contractual terms that give rise on specified dates to cash flows that are solely

payments of principal and interest on the principal amount outstanding, must be

measured at FVTOCI, unless the asset is designated at FVTPL under the fair value

option.

all other debt instruments must be measured at FVTPL.

all equity investments are to be measured in the statement of financial position at fair

value, with gains and losses recognised in profit or loss except that if an equity

investment is not held for trading, an irrevocable election can be made at initial

recognition to measure the investment at FVTOCI, with dividend income recognised in

profit or loss.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

18

IFRS 9 also contains requirements for the classification and measurement of financial liabilities

and derecognition requirements. One major change from IAS 39 relates to the presentation of

changes in the fair value of a financial liability designated as at FVTPL attributable to changes

in the credit risk of that liability. Under IFRS 9, such changes are presented in other

comprehensive income, unless the presentation of the effect of the change in the liability’s

credit risk in other comprehensive income would create or enlarge an accounting mismatch in

profit or loss. Changes in fair value attributable to a financial liability’s credit risk are not

subsequently reclassified to profit or loss. Under IAS 39, the entire amount of the change in

the fair value of the financial liability designated as FVTPL is presented in profit or loss.

Phase 2: Impairment methodology

The impairment model under IFRS 9 reflects expected credit losses, as opposed to incurred

credit losses under IAS 39. Under the impairment approach in IFRS 9, it is no longer necessary

for a credit event to have occurred before credit losses are recognised. Instead, an entity

always accounts for expected credit losses and changes in those expected credit losses. The

amount of expected credit losses should be updated at each reporting date to reflect changes

in credit risk since initial recognition.

Phase 3: Hedge accounting

The general hedge accounting requirements of IFRS 9 retain the three types of hedge

accounting mechanisms in IAS 39. However, greater flexibility has been introduced to the

types of transactions eligible for hedge accounting, specifically broadening the types of

instruments that qualify as hedging instruments and the types of risk components of non-

financial items that are eligible for hedge accounting. In addition, the effectiveness test has

been overhauled and replaced with the principle of an ‘economic relationship’. Retrospective

assessment of hedge effectiveness is no longer required. Far more disclosure requirements

about an entity’s risk management activities have been introduced.

The work on macro hedging by the IASB is still at a preliminary stage - a discussion paper was

issued in April 2014 to gather preliminary views and direction from constituents with a

comment period which ended on 17 October 2014. The project is under redeliberation at the

time of writing.

Transitional provisions

IFRS 9 (as revised in 2014) is effective for annual periods beginning on or after 1 January

2018 with earlier application permitted. If an entity elects to apply IFRS 9 early, it must apply

all of the requirements in IFRS 9 at the same time, except for those relating to:

1. the presentation of fair value gains and losses attributable to changes in the credit risk

of financial liabilities designated as at FVTPL, the requirements for which an entity may

early apply without applying the other requirements in IFRS 9; and

2. hedge accounting, for which an entity may choose to continue to apply the hedge

accounting requirements of IAS 39 instead of the requirements of IFRS 9.

An entity may early apply the earlier versions of IFRS 9 instead of the 2014 version if the

entity’s date of initial application of IFRS 9 is before 1 February 2015. The date of initial

application is the beginning of the reporting period when an entity first applies the

requirements of IFRS 9.

IFRS 9 contains specific transitional provisions for i) classification and measurement of financial

assets; ii) impairment of financial assets; and iii) hedge accounting. Please see IFRS 9 for

details.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

19

2.2.2 IFRS 15 Revenue from Contracts with Customers

(Effective for annual periods beginning on or after 1 January 2018)

IFRS 15 establishes a single comprehensive model for entities to use in accounting for

revenue arising from contracts with customers. It will supersede the following revenue

Standards and Interpretations upon its effective date:

IAS 18 Revenue;

IAS 11 Construction Contracts;

IFRIC 13 Customer Loyalty Programmes;

IFRIC 15 Agreements for the Construction of Real Estate;

IFRIC 18 Transfers of Assets from Customers; and

SIC 31 Revenue-Barter Transactions Involving Advertising Services.

As suggested by the title of the new revenue Standard, IFRS 15 will only cover revenue

arising from contracts with customers. Under IFRS 15, a customer of an entity is a party that

has contracted with the entity to obtain goods or services that are an output of the entity's

ordinary activities in exchange for consideration.

Unlike the scope of IAS 18, the recognition and measurement of interest income and dividend

income from debt and equity investments are no longer within the scope of IFRS 15. Instead,

they are within the scope of IAS 39 Financial Instruments: Recognition and Measurement (or

IFRS 9 Financial Instruments, if IFRS 9 is early adopted).

As mentioned above, the new revenue Standard has a single model to deal with revenue

from contracts with customers. Its core principle is that an entity should recognise revenue

to depict the transfer of promised goods or services to customers in an amount that reflects

the consideration to which the entity expects to be entitled in exchange for those goods or

services.

The new revenue Standard introduces a 5-step approach to revenue recognition and

measurement:

Step 1: Identify the contract with a customer

Step 2: Identify the performance obligations in the contract

Step 3: Determine the transaction price

Step 4: Allocate the transaction price to the performance obligations in the contract

Step 5: Recognise revenue when (or as) the entity satisfies a performance obligation.

Far more prescriptive guidance has been introduced by the new revenue Standard:

Whether or not a contract (or a combination of contracts) contains more than one

promised good or service, and if so, when and how the promised goods or services

should be unbundled.

Whether the transaction price allocated to each performance obligation should be

recognised as revenue over time or at a point in time. Under IFRS 15, an entity

recognises revenue when a performance obligation is satisfied, which is when ‘control’

of the goods or services underlying the particular performance obligation is transferred

to the customer. Unlike IAS 18, the new Standard does not include separate guidance

for 'sales of goods' and 'provision of services'; rather, the new Standard requires entities

to assess whether revenue should be recognised over time or a particular point in time

regardless of whether revenue relates to 'sales of goods' or 'provision of services'.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

20

When the transaction price includes a variable consideration element, how it will affect

the amount and timing of revenue to be recognised. The concept of variable

consideration is broad; a transaction price is considered variable due to discounts,

rebates, refunds, credits, price concessions, incentives, performance bonuses, penalties

and contingency arrangements. The new Standard introduces a high hurdle for variable

consideration to be recognised as revenue – that is, only to the extent that it is highly

probable that a significant reversal in the amount of cumulative revenue recognised will

not occur when the uncertainty associated with the variable consideration is

subsequently resolved.

When costs incurred to obtain a contract and costs to fulfil a contract can be recognised

as an asset.

2.2.3 Amendments to IFRS 10 and IAS 28 Sale or Contribution of Assets between an

Investor and its Associate or Joint Venture

The amendments clarify that the exemption from preparing consolidated financial statements

is available to a parent entity that is a subsidiary of an investment entity, even if the

investment entity measures all its subsidiaries at fair value in accordance with IFRS 10.

Consequential amendments have also been made to IAS 28 to clarify that the exemption

from applying the equity method is also applicable to an investor in an associate or joint

venture if that investor is a subsidiary of an investment entity that measures all its

subsidiaries at fair value.

The amendments further clarify that the requirement for an investment entity to consolidate

a subsidiary providing services related to the former’s investment activities applies only to

subsidiaries that are not investment entities themselves.

Moreover, the amendments clarify that in applying the equity method of accounting to an

associate or a joint venture that is an investment entity, an investor may retain the fair value

measurements that the associate or joint venture used for its subsidiaries.

Lastly, clarification is also made that an investment entity that measures all its subsidiaries

at fair value should provide the disclosures required by IFRS 12 Disclosures of Interests in

Other Entities.

The amendments apply retrospectively for annual periods beginning on or after 1 January

2016 with earlier application permitted.

2.2.4 IFRS 16 Leases

IFRS 16 Leases was issued, it specifies how an IFRS reporter will recognize, measure, present

and disclose leases. The standard provides a single lessee accounting model, requiring

lessees to recognize assets and liabilities for all leases unless the lease term is 12 months or

less or the underlying asset has a low value. Lessors continue to classify leases as operating

or finance, with IFRS 16's approach to lessor accounting substantially unchanged from its

predecessor, IAS 17.

Effective date of this standard is 1 January 2018

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

21

2.2.5 Amendments to IAS 12 Recognition of Deferred Tax Assets for Unrealised Losses

IAS 12 Income Taxes was amended to clarify the following aspects: Unrealized losses on

debt instruments measured at fair value and measured at cost for tax purposes give rise to

a deductible temporary difference regardless of whether the debt instrument's holder expects

to recover the carrying amount of the debt instrument by sale or by use. The carrying amount

of an asset does not limit the estimation of probable future taxable profits. Estimates for

future taxable profits exclude tax deductions resulting from the reversal of deductible

temporary differences. An entity assesses a deferred tax asset in combination with other

deferred tax assets. Where tax law restricts the utilization of tax losses, an entity would

assess a deferred tax asset in combination with other deferred tax assets of the same type.

Effective date of the amendment is 1 January, 2017

2.2.6 Amendments to IAS 7 Additional disclosure on changes in financing activities

IAS 7 was amended to clarify that entities shall provide disclosures that enable users of

financial statements to evaluate changes in liabilities arising from financing activities.

2.2.7 Amendments to IFRS 2 Classification and Measurement of Share-based Payment

Transactions

IFRS 2 was amended to clarify the standard in relation to the accounting for cash-settled

share-based payment transactions that include a performance condition, the classification of

share-based payment transactions with net settlement features, and the accounting for

modifications of share-based payment transactions from cash-settled to equity-settled.

Effective date is 1 January 2018

3. Basis of preparation

The financial statements of the Company have been prepared in accordance with

International Financial Reporting Standards (IFRS), as issued by the International Accounting

Standards Board (IASB).

The financial statements values are presented in Nigeria Naira (N) rounded to the nearest

thousand (N000), unless otherwise indicated.

Financial assets and financial liabilities are offset and the net amount reported in the

statement of financial position only when there is a current legally enforceable right to offset

the recognized amounts and there is an intention to settle on a net basis, or to realize the

assets and settled the liability simultaneously.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

22

3.1 Revenue recognition

3.1.1 Gross premiums

Gross general insurance written premiums comprise the total premiums receivable for the

whole period of cover provided by contracts entered into during the accounting period. They

are recognised on the date on which the policy commences.

3.1.2 Net premiums

Premiums include any adjustments arising in the accounting period in respect of reinsurance

contracts incepting in prior accounting periods.

Unearned reinsurance premiums are those proportions of premiums written in a year that

relate to periods of risk after the reporting date. Unearned reinsurance premiums are

deferred over the term of the underlying direct insurance policies for risks-attaching

contracts and over the term of the reinsurance contract for losses occurring contracts.

Reinsurance commission income

Reinsurance commission income represents commission received on direct business and

transactions ceded to re-insurance during the year. It is recognized over the cover provided

by contracts entered into the period and are recognized on the date on which the policy

incepts.

3.3.3 Investment income

Interest income is recognized in the profit or loss as it accrues and is calculated by using the

effective interest rate method. EIR is the rate that exactly discounts the estimated future

cash payments or receipts over the expected life of the financial instrument or a shorter

period, where appropriate, to the net carrying amount of the financial asset or liability. Fees

and commissions that are an integral part of the effective yield of the financial asset or

liability are recognized as an adjustment to the effective interest rate of the instrument.

Investment income also includes dividends when the right to receive payment is established.

For listed securities, this is the date the security is listed as ex-dividend.

3.3.4 Realized gains and losses

Realized gains and losses recorded in the profit or loss on investments include gains and

losses on financial assets and investment properties.

Gains and losses on the sale of investments are calculated as the difference between net

sales proceeds and the original or amortized cost and are recorded on occurrence of the sale

transaction.

3.4 Claims and expenses recognition

3.4.1 Gross claim

General insurance claims include all claims occurring during the year, whether reported or

not, related internal and external claims handling costs that are directly related to the

processing and settlement of claims, a reduction for the value of salvage and other

recoveries, and any adjustments to claims outstanding from previous years.

3.4.2 Reinsurance claims

Reinsurance claims are recognized when the related gross insurance claim is recognized

according to the terms of the relevant contract.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

23

3.4.3 Underwriting expenses

Underwriting expenses comprise acquisitions costs and other underwriting expenses.

Acquisition costs comprise all direct and indirect costs arising from the writing of insurance

contracts. These costs also include fees and commission expense. Other underwriting

expenses are those incurred in servicing existing policies and contracts. They are recognized

in the statement of profit or loss over the tenor of the insurance cover.

3.4.4 General administrative expenses

These are expenses other than claims and underwriting expenses. They include employee

benefits, professional fees, depreciation expenses and other non-operating expenses.

Management expenses are accounted for on accrual basis and recognized in the statement

of profit or loss upon utilization of the service or at the date of origination.

3.4.5 Finance costs

Interest expense is recognized in the profit or loss as it accrues and is calculated by using

the effective interest rate method. Accrued interest is included within the carrying value of

the interest bearing financial liability.

3.5 Cash and cash equivalents

Cash and cash equivalents comprise cash at bank and on hand and short-term deposits with

an original maturity of three months or less in the statement of financial position.

For the purpose of the statement of cash flows, cash and cash equivalents consist of cash

and cash equivalents as defined above, net of outstanding bank and book overdrafts.

3.6 Financial assets

Initial recognition and measurement

Financial assets within the scope of IAS 39 are classified as financial assets at fair value

through profit or loss, loans and receivables, held-to-maturity investments, available-for-

sale financial assets, as appropriate.

The Company determines the classification of its financial assets at initial recognition.

Financial assets are recognized initially at fair value plus, in the case of investments not at

fair value through profit or loss, directly attributable transaction costs.

The classification depends on the purpose for which the investments were acquired or

originated. Financial assets are classified as at fair value through profit or loss where the

Company’s documented investment strategy is to manage financial investments on a fair

value basis, because the related liabilities are also managed on this basis. The available-for-

sale and held-to-maturity categories are used when the relevant liability (including

shareholders’ funds) is passively managed and/or carried at amortized cost.

Purchases or sales of financial assets that require delivery of assets within a time frame

established by regulation or convention in the marketplace (regular way trades) are

recognized on the trade date, i.e., the date that the Company commits to purchase or sell

the asset.

The Company’s financial assets include cash and short-term deposits, trade and other

receivables, loan and other receivables, quoted and unquoted financial instruments.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

24

Subsequent measurement

The subsequent measurement of financial assets depends on their classification as follows:

Available-for-sale financial assets

Available-for-sale financial investments include equity and debt securities. Equity

investments classified as available-for-sale are those that are neither classified as held for

trading nor designated at fair value through profit or loss. Debt securities in this category

are those that are intended to be held for an indefinite period of time and which may be sold

in response to needs for liquidity or in response to changes in the market conditions.

After initial measurement, available-for-sale financial assets are subsequently measured at

fair value, with unrealized gains or losses recognized in other comprehensive income in the

available- for-sale reserve.

Interest earned whilst holding available-for-sale investments is reported as interest income

using the Effective Interest Rate (EIR). Dividends earned whilst holding available-for-sale

investments are recognised in the profit or loss as ‘Investment income’ when the right of the

payment has been established. When the asset is derecognised the cumulative gain or loss

is recognised in other operating income. When it is determined to be impaired, the

cumulative loss is recognised in the profit or loss in finance costs and removed from the

available-for-sale reserve.

The Company evaluates its available-for-sale financial assets to determine whether the

ability and intention to sell them in the near term would still be appropriate. In the case

where the Company is unable to trade these financial assets due to inactive markets and

management’s intention significantly changes to do so in the foreseeable future, the

Company may elect to reclassify these financial assets in rare circumstances. Reclassification

to loans and receivables is permitted when the financial asset meets the definition of loans

and receivables and management has the intention and ability to hold these assets for the

foreseeable future or until maturity. The reclassification to held-to-maturity is permitted only

when the entity has the ability and intention to hold the financial asset until maturity.

For a financial asset reclassified out of the available-for-sale category, any previous gain or

loss on that asset that has been recognised in equity is amortised to profit or loss over the

remaining life of the investment using the EIR. Any difference between the new amortised

cost and the expected cash flows is also amortised over the remaining life of the asset using

the EIR. If the asset is subsequently determined to be impaired then the amount recorded

in equity is reclassified to the profit or loss.

Investments in equity instruments that do not have a quoted market price in an active

market and whose fair value cannot be reliably measured are measured at cost.

Available-for-sale financial assets in the Company include investment in equity instruments

(both quoted and unquoted), investments in mutual funds and investment in debt securities

(bonds) issued by state governments and other corporate entities.

Loans and other receivables

Loans and receivables are non-derivative financial assets with fixed or determinable

payments that are not quoted in an active market. These investments are initially recognized

at cost, being the fair value of the consideration paid for the acquisition of the investment.

All transaction costs directly attributable to the acquisition are also included in the cost of

the investment. After initial measurement, loans and receivables are measured at amortized

cost, using the EIR, less allowance for impairment. Amortized cost is calculated by taking

into account any discount or premium on acquisition and fee or costs that are an integral

part of the EIR. The EIR amortization is included in ‘investment income’ in the profit or loss.

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

25

Gains and losses are recognized in the profit or loss when the investments are derecognized

or impaired, as well as through the amortization process.

Loans and receivables in the Company include deposits with bank and other financial

institutions having maturity of more than three months, loans to employees and receivable

under finance lease in which the Company is a lessor.

Held-to-maturity financial assets

Non-derivative financial assets with fixed or determinable payments and fixed maturities are

classified as held-to-maturity when the Company has the intention and ability to hold until

maturity. After initial measurement, held-to-maturity financial assets are measured at

amortized cost, using the EIR, less impairment. The EIR amortization is included in

‘investment income’ in the profit or loss. Gains and losses are recognized in the profit or loss

when the investments are derecognized or impaired, as well as through the amortization

process.

Derecognition of financial assets

A financial asset (or, when applicable, a part of a financial asset or part of a Company of

similar financial assets) is derecognized when:

· The rights to receive cash flows from the asset have expired

Or

· The Company retains the right to receive cash flows from the asset or has assumed an

obligation to pay the received cash flows in full without material delay to a third party

under a ‘pass- through’ arrangement; and either:

· The Company has transferred substantially all the risks and rewards of the asset

Or

· The Company has neither transferred nor retained substantially all the risks and rewards

of the asset, but has transferred control of the asset.

When the Company has transferred its right to receive cash flows from an asset or has

entered into a pass-through arrangement, and has neither transferred nor retained

substantially all the risks and rewards of the asset nor transferred control of the asset, the

asset is recognized to the extent of the Company’s continuing involvement in the asset.

Continuing involvement that takes the form of a guarantee over the transferred asset is

measured at the lower of the original carrying amount of the asset and the maximum amount

of consideration that the Company could be required to repay.

In that case, the Company also recognizes an associated liability. The transferred asset and

the associated liability are measured on a basis that reflects the rights and obligations that

the Company has retained.

3.7 Impairment of financial assets

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

26

The Company assesses at each reporting date whether there is any objective evidence that

a financial asset or group of financial assets is impaired. A financial asset or a group of

financial assets is deemed to be impaired if, and only if, there is objective evidence of

impairment as a result of one or more events that has occurred after the initial recognition

of the asset (an incurred ‘loss event’) and that loss event has an impact on the estimated

future cash flows of the financial asset or the group of financial assets that can be reliably

estimated. Evidence of impairment may include indications that the debtors or a group of

debtors is experiencing significant financial difficulty, default or delinquency in interest or

principal payments, the probability that they will enter bankruptcy or other financial

reorganization and where observable data indicate that there is a measurable decrease in

the estimated future cash flows, such as changes in arrears or economic conditions that

correlate with defaults.

Financial assets carried at amortized cost

For financial assets carried at amortized cost, the Company first assesses individually

whether objective evidence of impairment exists individually for financial assets that are

individually significant, or collectively for financial assets that are not individually significant.

If the Company determines that no objective evidence of impairment exists for an

individually assessed financial asset, whether significant or not, it includes the asset in a

group of financial assets with similar credit risk characteristics and collectively assesses them

for impairment. Assets that are individually assessed for impairment and for which an

impairment loss is, or continues to be, recognized are not included in a collective assessment

of impairment.

If there is objective evidence that an impairment loss on assets carried at amortized cost

has been incurred, the amount of the loss is measured as the difference between the carrying

amount of the asset and the present value of estimated future cash flows (excluding future

expected credit losses that have not been incurred) discounted at the financial asset’s original

effective interest rate. If a loan has a variable interest rate, the discount rate for measuring

any impairment loss is the current effective interest rate.

The carrying amount of the asset is reduced through the use of an allowance account and

the amount of the loss is recognized in the profit or loss. Interest income continues to be

accrued on the reduced carrying amount and is accrued using the rate of interest used to

discount the future cash flows for the purpose of measuring the impairment loss. The interest

income is recorded as part of investment income in the profit or loss. Loans together with

the associated allowance are written off when there is no realistic prospect of future recovery

and all collateral has been realized or has been transferred to the Company. If, in a

subsequent year, the amount of the estimated impairment loss increases or decreases

because of an event occurring after the impairment was recognized, the previously

recognized impairment loss is increased or reduced by adjusting the allowance account.

If a future write-off is later recovered, the recovery is credited to the ‘investment income’ in

the profit or loss.

For the purpose of a collective evaluation of impairment, financial assets are grouped on the

basis of the Company’s internal credit grading system, which considers credit risk

characteristics such as asset type, industry, geographical location, collateral type, past-due

status and other relevant factors.

Future cash flows on a group of financial assets that are collectively evaluated for impairment

are estimated on the basis of historical loss experience for assets with credit risk

LAW UNION AND ROCK INSURANCE PLC

Annual Report and Financial Statements

For the year ended 31 December 2016

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

27

characteristics similar to those in the group. Historical loss experience is adjusted on the

basis of current observable data to reflect the effects of current conditions on which the

historical loss experience is based and to remove the effects of conditions in the historical

period that do not exist currently. Estimates of changes in future cash flows reflect, and are

directionally consistent with, changes in related observable data from year to year (such as

changes in unemployment rates, payment status, or other factors that are indicative of

incurred losses in the group and their magnitude). The methodology and assumptions used

for estimating future cash flows are reviewed regularly to reduce any differences between

loss estimates and actual loss experience.

Available-for-sale financial investments

For available-for-sale financial investments, the Company assesses at each reporting date

whether there is objective evidence that an investment or a group of investments is impaired.

In the case of equity investments classified as available-for-sale, objective evidence would

include a ‘significant or prolonged’ decline in the fair value of the investment below its cost.

‘Significant’ is to be evaluated against the original cost of the investment and ‘prolonged’

against the period in which the fair value has been below its original cost. The Company

treats ‘significant’ generally as 20% and ‘prolonged’ generally as greater than six months.

Where there is evidence of impairment, the cumulative loss – measured as the difference

between the acquisition cost and the current fair value, less any impairment loss on that