Law of Banking and Security DR. ZULKIFLI HASAN 27th September 2011 Week III.

21

Law of Banking Law of Banking and Security and Security DR. ZULKIFLI HASAN DR. ZULKIFLI HASAN 27th September 2011 27th September 2011 Week III Week III

-

Upload

jonathan-singleton -

Category

Documents

-

view

216 -

download

3

Transcript of Law of Banking and Security DR. ZULKIFLI HASAN 27th September 2011 Week III.

Law of Banking Law of Banking and Securityand SecurityDR. ZULKIFLI HASANDR. ZULKIFLI HASAN

27th September 201127th September 2011

Week IIIWeek III

ContentsContents

The Banker-Customer RelationshipThe Banker-Customer Relationship Definition of ’Banker’ and ’Customer’Definition of ’Banker’ and ’Customer’ Nature of Banker-Customer Nature of Banker-Customer

RelationshipRelationship Agent & Principal RelationshipAgent & Principal Relationship Fiduciary relatFiduciary relationshipionship Debtor-Creditor RelationshipDebtor-Creditor Relationship Constructive Trustee and Beneficiary Constructive Trustee and Beneficiary

RelationshipRelationship

Definition of bankerDefinition of banker

Common lawCommon law Text books/profound scholarsText books/profound scholars StatutesStatutes Judicial InterpretationJudicial Interpretation

Common lawCommon law

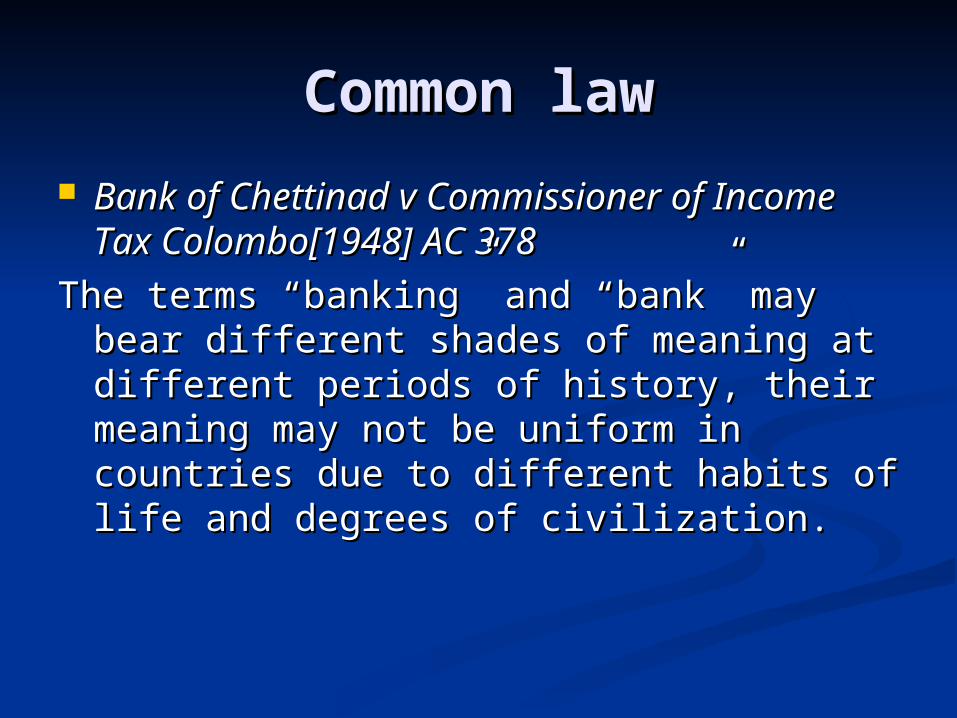

Bank of Chettinad v Commissioner of Bank of Chettinad v Commissioner of Income Tax Colombo[1948] AC 378Income Tax Colombo[1948] AC 378

The terms “banking” and “bank” may bear The terms “banking” and “bank” may bear different shades of meaning at different different shades of meaning at different periods of history, their meaning may not periods of history, their meaning may not be uniform in countries due to different be uniform in countries due to different habits of life and degrees of civilization.habits of life and degrees of civilization.

Bank of New South Wales v Commonwealth Bank of New South Wales v Commonwealth [1948] 76 CLR 1 334- Dixon J:[1948] 76 CLR 1 334- Dixon J:

““Banking should have ascribed to it Banking should have ascribed to it anything but a wide meaning and a matter anything but a wide meaning and a matter forming part of the commercial, economic forming part of the commercial, economic and social organization of the community”.and social organization of the community”.

Varied from age to age and country to Varied from age to age and country to country.country.

Commonwealth v Bank of New South WalesCommonwealth v Bank of New South Wales [1950] ac 235 303.[1950] ac 235 303.

“ “the creation and transfer of credit, the the creation and transfer of credit, the making of loans, the purchase and disposal making of loans, the purchase and disposal of investments and other kindred activities”.of investments and other kindred activities”.

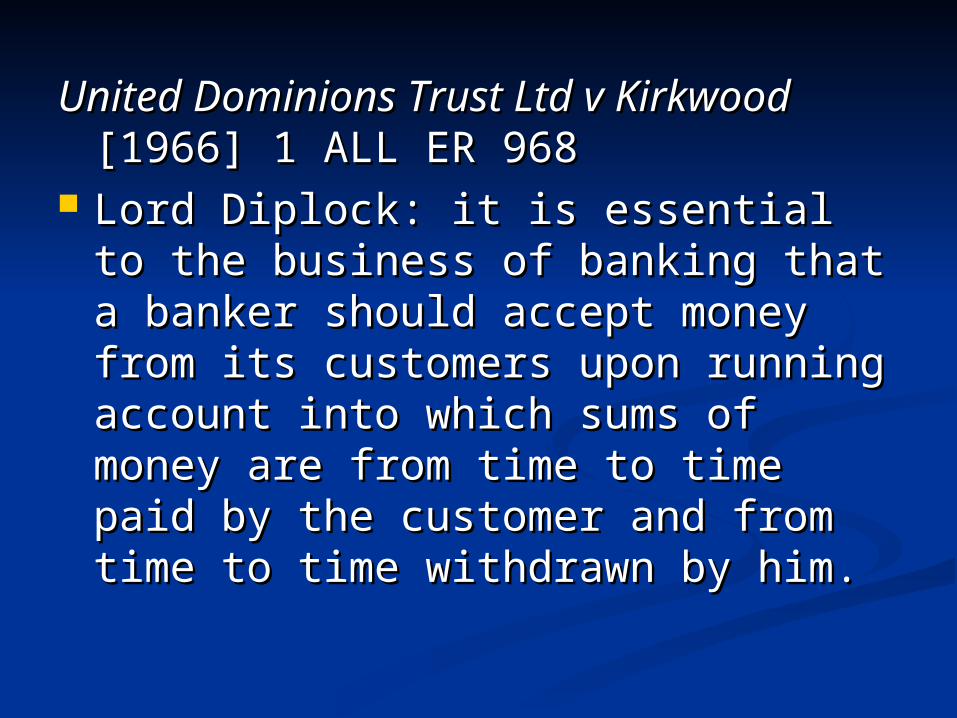

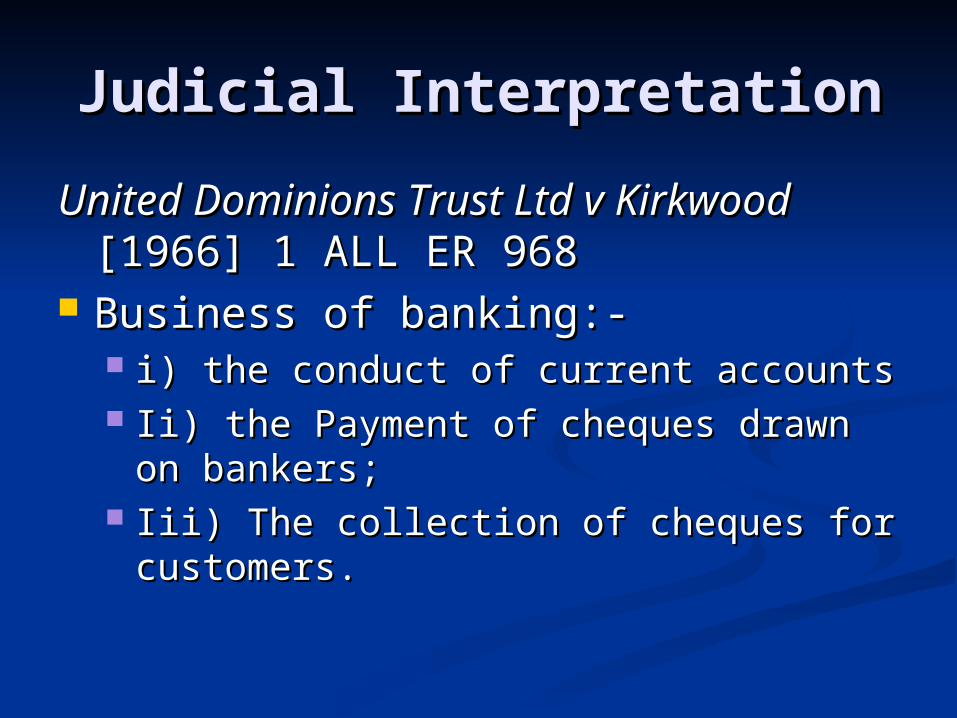

United Dominions Trust Ltd v United Dominions Trust Ltd v KirkwoodKirkwood [1966] 1 ALL ER 968 [1966] 1 ALL ER 968

Lord Diplock: it is essential to the Lord Diplock: it is essential to the business of banking that a banker business of banking that a banker should accept money from its should accept money from its customers upon running account customers upon running account into which sums of money are from into which sums of money are from time to time paid by the customer time to time paid by the customer and from time to time withdrawn by and from time to time withdrawn by him.him.

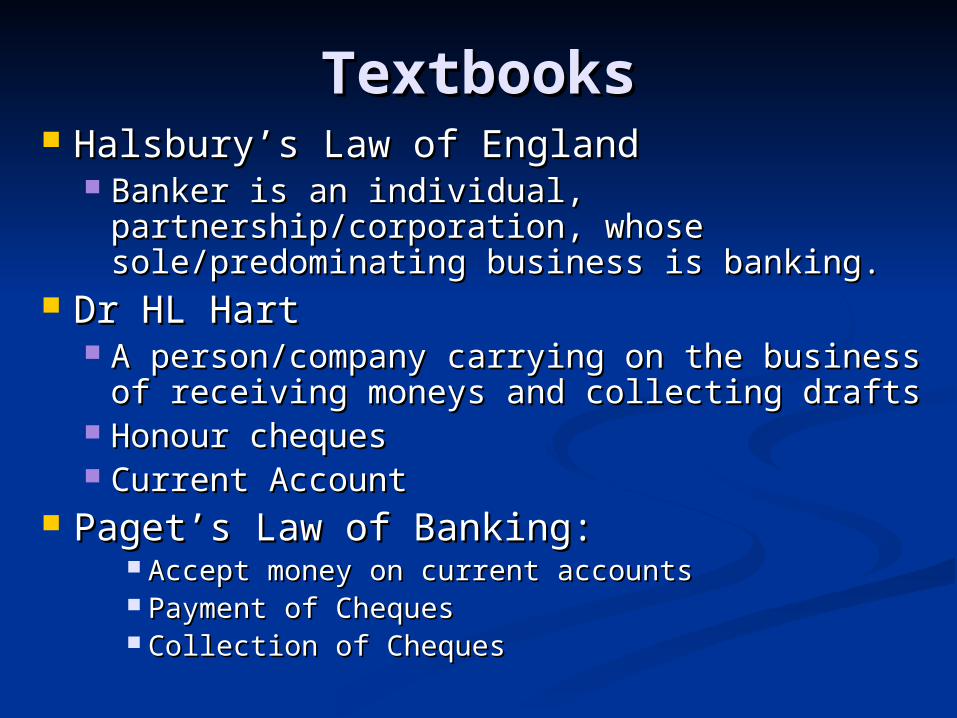

TextbooksTextbooks Halsbury’s Law of EnglandHalsbury’s Law of England

Banker is an individual, Banker is an individual, partnership/corporation, whose partnership/corporation, whose sole/predominating business is banking.sole/predominating business is banking.

Dr HL HartDr HL Hart A person/company carrying on the business A person/company carrying on the business

of receiving moneys and collecting draftsof receiving moneys and collecting drafts Honour chequesHonour cheques Current AccountCurrent Account

Paget’s Law of Banking: Paget’s Law of Banking: Accept money on current accountsAccept money on current accounts Payment of ChequesPayment of Cheques Collection of ChequesCollection of Cheques

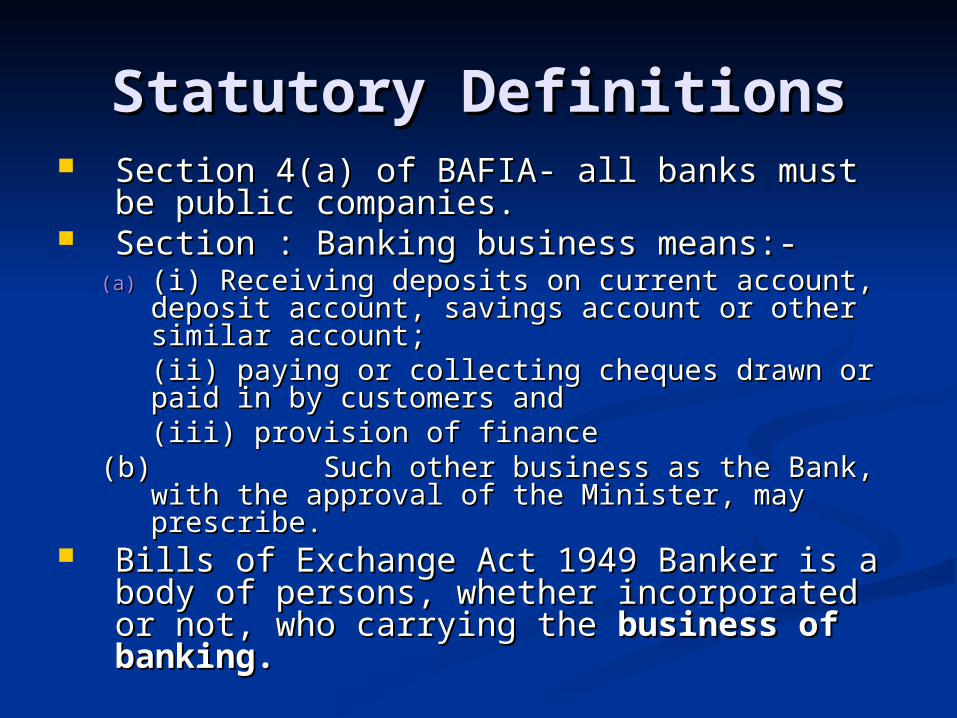

Statutory DefinitionsStatutory Definitions Section 4(a) of BAFIA- all banks must be Section 4(a) of BAFIA- all banks must be

public companies.public companies. Section : Banking business means:-Section : Banking business means:-

(a)(a) (i) Receiving deposits on current account, (i) Receiving deposits on current account, deposit account, savings account or other deposit account, savings account or other similar account;similar account;(ii) paying or collecting cheques drawn or paid (ii) paying or collecting cheques drawn or paid in by customers andin by customers and(iii) provision of finance(iii) provision of finance

(b)(b) Such other business as the Bank, with the Such other business as the Bank, with the approval of the Minister, may prescribe. approval of the Minister, may prescribe.

Bills of Exchange Act 1949 Banker is a Bills of Exchange Act 1949 Banker is a body of persons, whether incorporated or body of persons, whether incorporated or not, who carrying the not, who carrying the business of business of banking.banking.

Judicial InterpretationJudicial Interpretation

United Dominions Trust Ltd v United Dominions Trust Ltd v KirkwoodKirkwood [1966] 1 ALL ER 968 [1966] 1 ALL ER 968

Business of banking:- Business of banking:- i) the conduct of current accountsi) the conduct of current accounts Ii) the Payment of cheques drawn on Ii) the Payment of cheques drawn on

bankers;bankers; Iii) The collection of cheques for Iii) The collection of cheques for

customers.customers.

Recover Debts Recover Debts

Bank of China v Lee Kee Pin [1961] Bank of China v Lee Kee Pin [1961] MLJ 40MLJ 40

HC: A bank which was refused a HC: A bank which was refused a license could still recover debts license could still recover debts because it does not amount to because it does not amount to carrying on banking business.carrying on banking business.

Foreign Bank Acquiring Foreign Bank Acquiring and Accepting Charges of and Accepting Charges of

LandLand Koh Kim Chai v Asia Commercial Koh Kim Chai v Asia Commercial

Banking Corporation LimitedBanking Corporation Limited [1984] [1984] 1 MLJ 3221 MLJ 322

FC: the transaction of acquiring and FC: the transaction of acquiring and accepting charges of land in accepting charges of land in Malaysia could not be said to come Malaysia could not be said to come within the ambit of banking business within the ambit of banking business in Malaysiain Malaysia

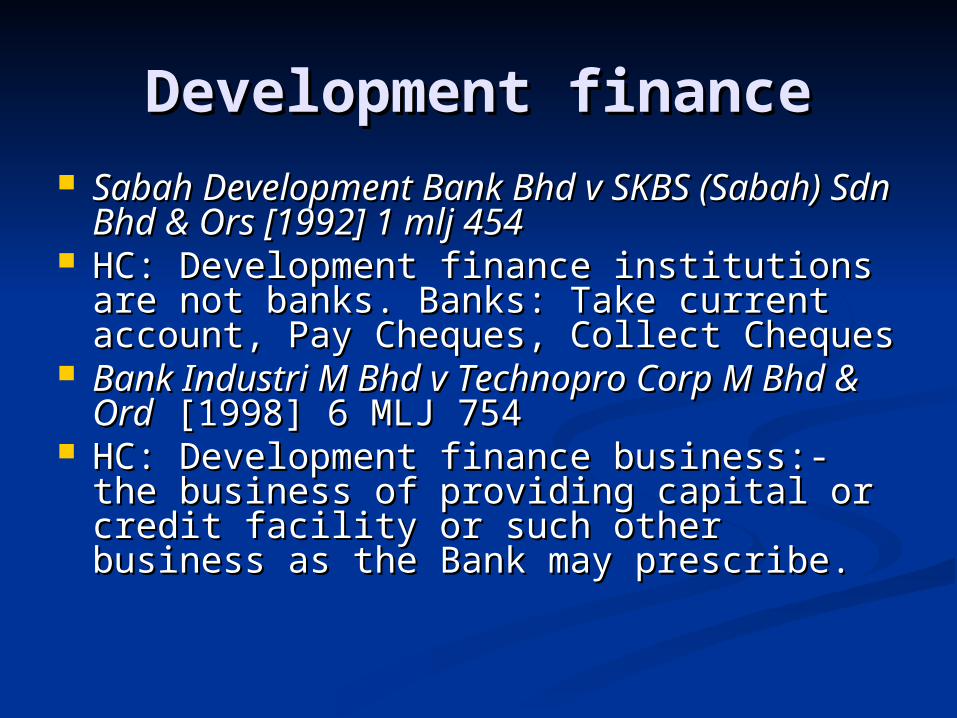

Development financeDevelopment finance Sabah Development Bank Bhd v SKBS Sabah Development Bank Bhd v SKBS

(Sabah) Sdn Bhd & Ors [1992] 1 mlj 454(Sabah) Sdn Bhd & Ors [1992] 1 mlj 454 HC: Development finance institutions are HC: Development finance institutions are

not banks. Banks: Take current account, not banks. Banks: Take current account, Pay Cheques, Collect ChequesPay Cheques, Collect Cheques

Bank Industri M Bhd v Technopro Corp M Bank Industri M Bhd v Technopro Corp M Bhd & OrdBhd & Ord [1998] 6 MLJ 754 [1998] 6 MLJ 754

HC: Development finance business:- the HC: Development finance business:- the business of providing capital or credit business of providing capital or credit facility or such other business as the Bank facility or such other business as the Bank may prescribe. may prescribe.

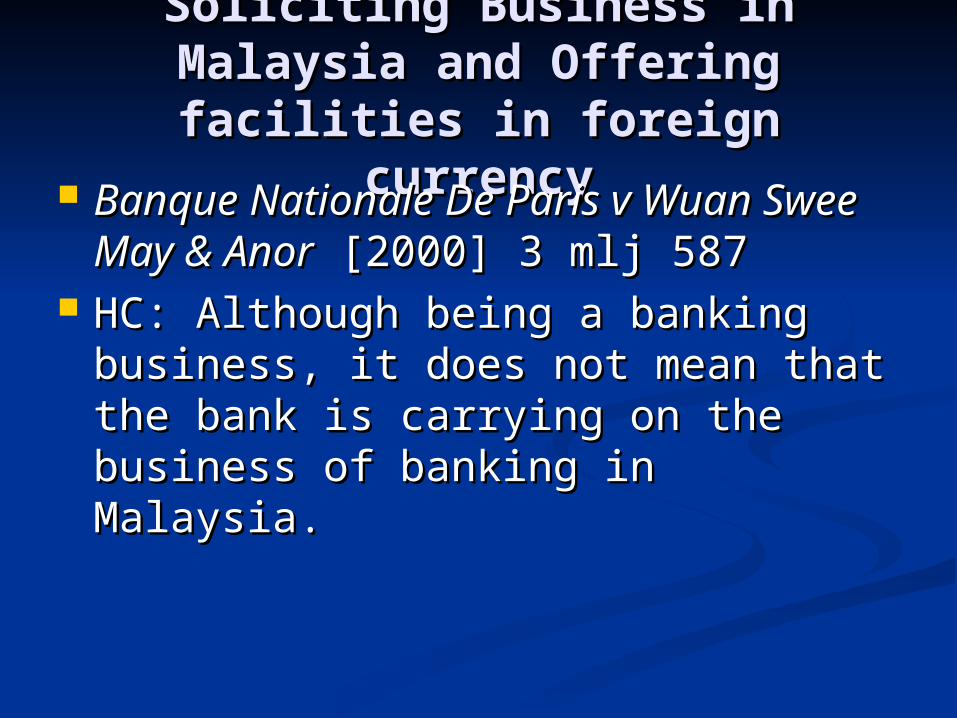

Soliciting Business in Malaysia Soliciting Business in Malaysia and Offering facilities in and Offering facilities in

foreign currencyforeign currency Banque Nationale De Paris v Wuan Banque Nationale De Paris v Wuan

Swee May & AnorSwee May & Anor [2000] 3 mlj 587 [2000] 3 mlj 587 HC: Although being a banking HC: Although being a banking

business, it does not mean that the business, it does not mean that the bank is carrying on the business of bank is carrying on the business of banking in Malaysia.banking in Malaysia.

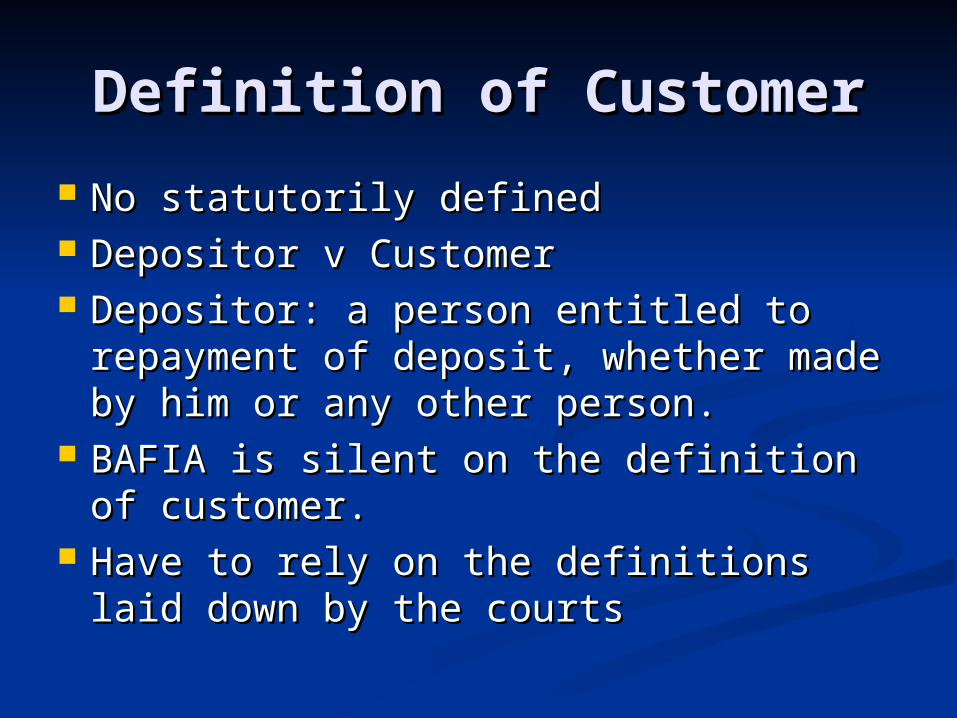

Definition of CustomerDefinition of Customer

No statutorily definedNo statutorily defined Depositor v Customer Depositor v Customer Depositor: a person entitled to Depositor: a person entitled to

repayment of deposit, whether made repayment of deposit, whether made by him or any other person.by him or any other person.

BAFIA is silent on the definition of BAFIA is silent on the definition of customer.customer.

Have to rely on the definitions laid Have to rely on the definitions laid down by the courtsdown by the courts

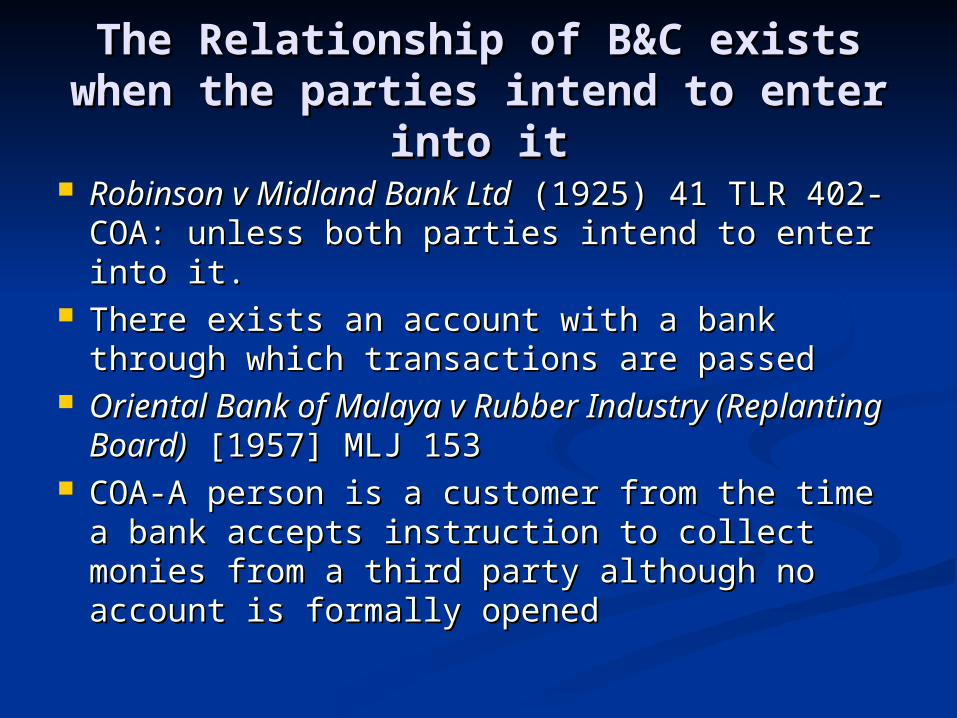

The Relationship of B&C exists The Relationship of B&C exists when the parties intend to enter when the parties intend to enter

into itinto it Robinson v Midland Bank LtdRobinson v Midland Bank Ltd (1925) 41 TLR (1925) 41 TLR

402- COA: unless both parties intend to enter 402- COA: unless both parties intend to enter into it.into it.

There exists an account with a bank through There exists an account with a bank through which transactions are passedwhich transactions are passed

Oriental Bank of Malaya v Rubber Industry Oriental Bank of Malaya v Rubber Industry (Replanting Board)(Replanting Board) [1957] MLJ 153 [1957] MLJ 153

COA-A person is a customer from the time a COA-A person is a customer from the time a bank accepts instruction to collect monies bank accepts instruction to collect monies from a third party although no account is from a third party although no account is formally openedformally opened

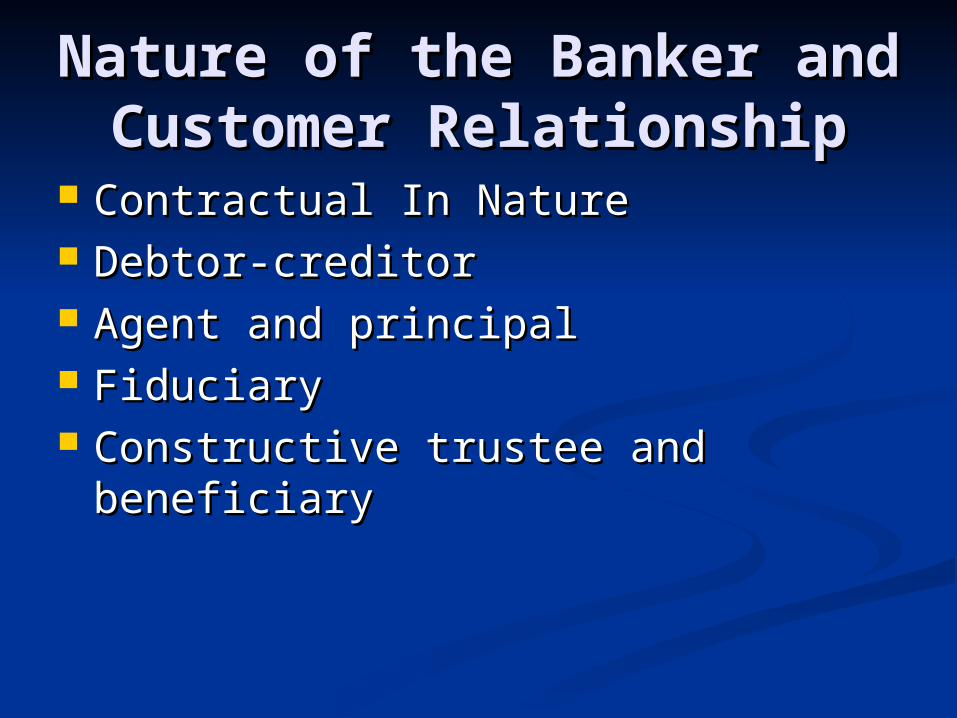

Nature of the Banker and Nature of the Banker and Customer RelationshipCustomer Relationship

Contractual In NatureContractual In Nature Debtor-creditorDebtor-creditor Agent and principalAgent and principal Fiduciary Fiduciary Constructive trustee and beneficiary Constructive trustee and beneficiary

Contractual in nature Contractual in nature

Joachimson v Swiss Bank Corporation Joachimson v Swiss Bank Corporation [1921] 3 KB 110[1921] 3 KB 110

The bank undertakes to receive money and The bank undertakes to receive money and to collect bills- the bank borrows the to collect bills- the bank borrows the proceeds and undertakes to repayproceeds and undertakes to repay

Bank Pertanian Malaysia v Mohd Gazzali Bank Pertanian Malaysia v Mohd Gazzali Mohd Ismail Mohd Ismail [1997]- Zaleha Zahari JC[1997]- Zaleha Zahari JC HC: Express term of the loan. A demand is HC: Express term of the loan. A demand is

absolute necessity as stipulated in the absolute necessity as stipulated in the agreement.agreement.

Debtor-Creditor Debtor-Creditor RelationshipRelationship

Foley v Hill (1848] 2 HL Cas 28 Foley v Hill (1848] 2 HL Cas 28 The trade of a banker is to receive The trade of a banker is to receive

money and use it as if it were his money and use it as if it were his own, he becoming a debtor to the own, he becoming a debtor to the person who has lent or deposited person who has lent or deposited with him the money to use as his with him the money to use as his own.own.

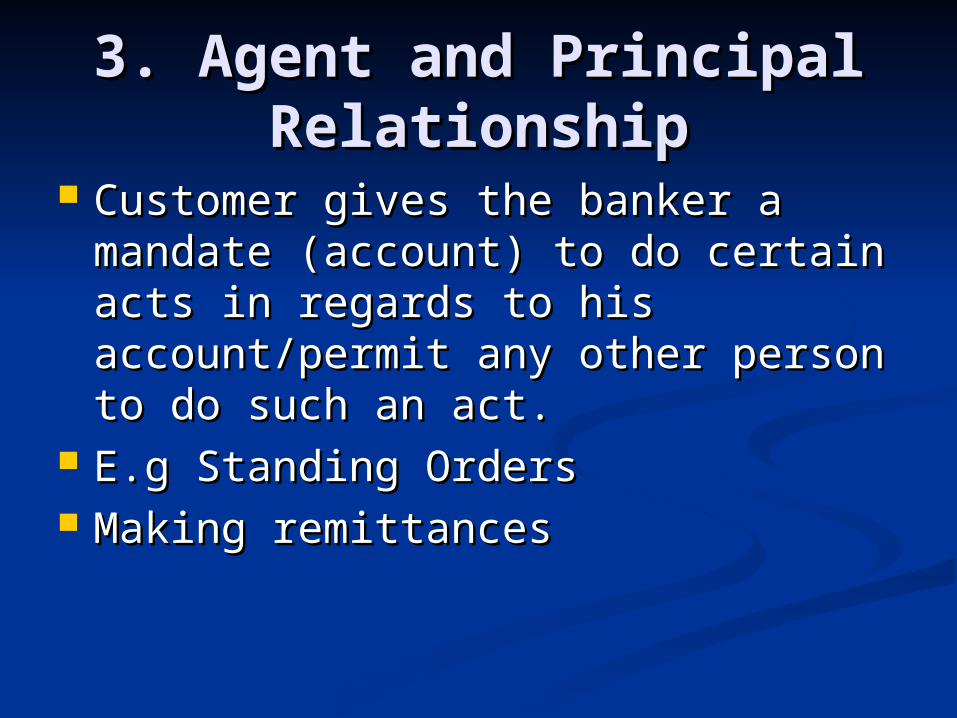

3. Agent and Principal 3. Agent and Principal RelationshipRelationship

Customer gives the banker a Customer gives the banker a mandate (account) to do certain acts mandate (account) to do certain acts in regards to his account/permit any in regards to his account/permit any other person to do such an act.other person to do such an act.

E.g Standing OrdersE.g Standing Orders Making remittancesMaking remittances

4. Fiduciary Relationship4. Fiduciary Relationship

Banker as trustee over trust funds.Banker as trustee over trust funds. Equity imposes a duty on a bank not Equity imposes a duty on a bank not

to take undue advantage over a to take undue advantage over a customercustomer Woods v Martin Bank Ltd & Anor Woods v Martin Bank Ltd & Anor

[1959][1959] Avoid conflict of interestAvoid conflict of interest

5. Constructive Trustee 5. Constructive Trustee and beneficiary and beneficiary

RelationshipRelationship Banker is subject to constructive Banker is subject to constructive trust- look at the breach and liabilitytrust- look at the breach and liability

See Barnes v Addy (1874)See Barnes v Addy (1874) The bank offered assistanceThe bank offered assistance Had actual or constructive knowledgeHad actual or constructive knowledge There was dishonest and fraudulent There was dishonest and fraudulent

design or intentiondesign or intention

![[XLS]xa.yimg.comxa.yimg.com/kq/groups/24779538/2009471176/name/SKUSES... · Web viewNOR SHAHIRAH BINTI ZULKIFLI 990605146244 ZULKIFLI BIN HASAN BASRI 0142256692 YASMAINI BINTI SYUIB](https://static.fdocuments.net/doc/165x107/5ae41dce7f8b9a0d7d8e9008/xlsxayimgcomxayimgcomkqgroups247795382009471176nameskusesweb-viewnor.jpg)