Latvia's Internal Adjustment and Lessons for Europe

26

Latvia’s internal adjustment and lessons for Europe May 24, 2012 Ilmārs Rimšēvičs Governor of the Bank of Latvia

-

Upload

global-interdependence-center -

Category

Documents

-

view

224 -

download

3

description

Ilmars Remsevics presentation at "Economies of Baltic Sea Regions and Their Capital Markets: A Sustainable Recovery?"

Transcript of Latvia's Internal Adjustment and Lessons for Europe

Latvia’s internal adjustment and

lessons for Europe

May 24, 2012

Ilmārs Rimšēvičs

Governor of the Bank of Latvia

Presentation outline

Setting the scene: some

developments before the crisis

How Latvia came through the

recent crisis?

What are the lessons learned and

implications for Europe?

Latvia’s economy was on a fast track during 2004-2007

However, if driving fast, one has to make sure

that the pace is sustainable

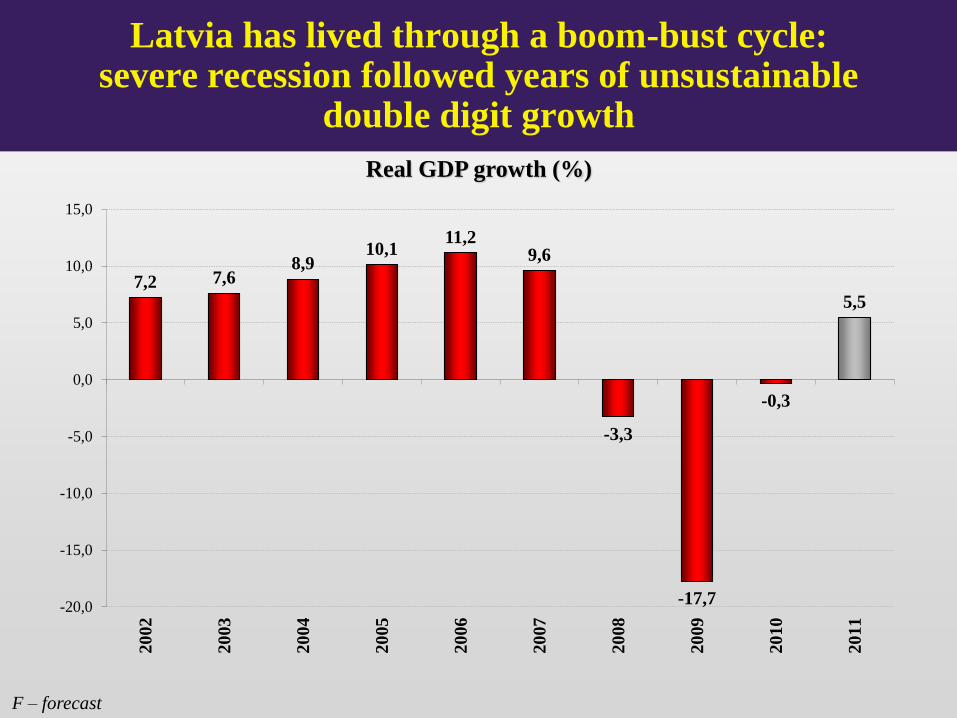

Latvia has lived through a boom-bust cycle: severe recession followed years of unsustainable

double digit growth

Real GDP growth (%)

F – forecast

7,2 7,6 8,9

10,1 11,2

9,6

-3,3

-17,7

-0,3

5,5

-20,0

-15,0

-10,0

-5,0

0,0

5,0

10,0

15,0

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Over the past boom Latvia was running enormous underlying fiscal gap

General Government budget balance (ESA’95), % of GDP

Source: Eurostat, F - BoL staff estimation

-0,4 -0,5 -0,4 -4,2 -9,8 -8,2 -3,5 -1,9

-18,6

-14,1

-5,6

-2,7 -3,3

-6,4

-8,5 -7,5

-5,5

-2,2

-0,8

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

2005 2006 2007 2008 2009 2010 2011 2012F

Consolidation effort Actual (targeted) balance

Fiscal gap Structural budget balance

Many suggested devaluation as a

way out of the crisis.

Why devaluation was not an

appropriate solution?

To be or not to be, was the question

in 2008

Latvia lost market access already at the outset of the recent crisis and the fiscal gap had to be closed quickly

by massive consolidation

Breakdown of budget consolidation measures, % of GDP

Source: Ministry of Finance; Bank of Latvia staff calculations

How Latvia managed to accomplish what initially was claimed being impossible?

Speed

A speedy consolidation can be compared to a timely

pruning an apple-tree – you earlier and richer harvest

How Latvia managed to accomplish what initially was claimed being impossible?

Ownership

How Latvia managed to accomplish what initially was claimed being impossible?

Commitment

How Latvia managed to accomplish what initially was claimed being impossible?

Solidarity

Latvia has regained its competitiveness: wage-productivity gap has been closed

Real hourly wage and labour productivity per hour (seasonally adjusted), 2005 Q1 = 100

80

90

100

110

120

130

140

150

200

4 Q

1

Q3

200

5 Q

1

Q3

200

6 Q

1

Q3

200

7 Q

1

Q3

200

8 Q

1

Q3

200

9 Q

1

Q3

201

0 Q

1

Q3

201

1 Q

1

Q3

Labour productivity Real wage

Source: CSB; Bank of Latvia staff calculations

Despite loud ex-ante warnings of protracted recession risks under internal adjustment scenario,

a strong “V” shaped recovery followed

Real GDP growth, %

5,5

-20

-15

-10

-5

0

5

10

15

2006 2007 2008 2009 2010 2011

Source: CSB; F – Bank of Latvia forecast

Indeed, Latvia and other Baltic countries have clearly benefited from getting through the internal adjustment at

an early stage

GDP growth in 2011, % y-o-y

Source: Eurostat

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

Est

on

ia

Lit

hu

an

ia

La

tvia

Po

lan

d

Sw

ed

en

Slo

vak

ia

Au

stri

a

Ger

ma

ny

Fin

lan

d

Ro

ma

nia

Ma

lta

Bel

giu

m

Bu

lgaria

Cze

ch R

epu

bli

c

Fran

ce

Hu

ng

ary

Net

her

lan

ds

Lu

xem

bo

urg

Den

ma

rk

Un

ited

Kin

gd

om

Irel

an

d

Sp

ain

Cy

pru

s

Ita

ly

Slo

ven

ia

Po

rtu

gal

Gre

ece

Despite problems in many European countries, GDP growth even accelerated in Latvia (the fastest

growing economy in Europe at the beginning of 2012)

GDP growth in Latvia, % y-o-y

Source: CSB;

+6.8%

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

2011 I II III IV 2012 I

Exports already well above the pre-crisis peak level;

Latvia ranges among the export leaders in Europe

85

72 71 71

55 53

44 44 43 43 42 38 35 34 34 33 33 32 31 30 29 29

26 23 21

10

2

0

10

20

30

40

50

60

70

80

90

Est

on

ia

Bu

lga

ria

La

tvia

Lit

hu

an

ia

Ro

ma

nia

Gre

ece

Cze

ch R

epu

bli

c

Ma

lta

Sw

ed

en

Cy

pru

s

Slo

vak

ia

Po

lan

d

Hu

ng

ary

Un

ited

Kin

gd

om

Po

rtu

gal

Slo

ven

ia

Net

her

lan

ds

Ger

ma

ny

Sp

ain

Au

stri

a

Bel

giu

m

Italy

Fin

lan

d

Fran

ce

Den

ma

rk

Irel

an

d

Lu

xem

bo

urg

Merchandise export revenue growth (2011 over 2009, %)

Source: Eurostat

General government gross debt, % of GDP

Source: Eurostat, F -Bank of Latvia forecast

Latvia has managed to stabilize debt at moderate level and to avoid initially expected debt explosion

19,8

36,7

44,7 42,6 43,4

0

5

10

15

20

25

30

35

40

45

50

2008 2009 2010 2011 2012F

Lessons

What are the lessons

learned?

This crisis has shown that

MORE is LESS and LESS is MORE

"One doesn't die from debt, one dies from not being able to borrow"

0

50

100

150

200

Gre

ece*

Irel

and

Ital

y

Po

rtu

gal US

Bel

giu

m

Fra

nce UK

EU

27

Ger

man

y

Sp

ain

Hu

ngar

y

Au

stri

a

Mal

ta

Cy

pru

s

Net

her

lan

ds

Po

lan

d

Slo

ven

ia

Fin

lan

d

Slo

vak

ia

Lat

via

Den

mar

k

Cze

ch R

ep.

Lit

hu

ania

Ro

man

ia

Sw

eden

Lux

embo

urg

Bu

lgar

ia

Est

on

ia

2005

General government gross debt, % of GDP

Rogoff & Reinhart

debt thresholds

for advanced and

emerging economies

Source: AMECO

"One doesn't die from debt, one dies from not being able to borrow"

0

50

100

150

200

Gre

ece*

Irel

and

Ital

y

Po

rtu

gal US

Bel

giu

m

Fra

nce UK

EU

27

Ger

man

y

Sp

ain

Hu

ngar

y

Au

stri

a

Mal

ta

Cy

pru

s

Net

her

lan

ds

Po

lan

d

Slo

ven

ia

Fin

lan

d

Slo

vak

ia

Lat

via

Den

mar

k

Cze

ch R

ep.

Lit

hu

ania

Ro

man

ia

Sw

eden

Lux

embo

urg

Bu

lgar

ia

Est

on

ia

2010

General government gross debt, % of GDP

Rogoff & Reinhart

debt thresholds

for advanced and

emerging economies

Source: AMECO

"One doesn't die from debt, one dies from not being able to borrow"

0

50

100

150

200

Gre

ece*

Irel

and

Ital

y

Po

rtu

gal US

Bel

giu

m

Fra

nce UK

EU

27

Ger

man

y

Sp

ain

Hu

ngar

y

Au

stri

a

Mal

ta

Cy

pru

s

Net

her

lan

ds

Po

lan

d

Slo

ven

ia

Fin

lan

d

Slo

vak

ia

Lat

via

Den

mar

k

Cze

ch R

ep.

Lit

hu

ania

Ro

man

ia

Sw

eden

Lux

embo

urg

Bu

lgar

ia

Est

on

ia

2013

General government gross debt, % of GDP

Rogoff & Reinhart

debt thresholds

for advanced and

emerging economies

Source: AMECO

Most Euro area countries suffering from high debt are still running large budget deficits

General government gross debt General government budget deficit

2000 2005 2010 2013 2000 2005 2010 2013

Greece* 104.4 101.2 144.9 198.5 -3.8 -5.6 -10.8 -6.8

Ireland 37.5 27.2 94.9 121.1 4.7 1.7 -31.3 -7.8

Italy 108.5 105.4 118.4 118.7 -0.9 -4.5 -4.5 -1.1

Portugal 48.5 62.8 93.3 112.1 -2.9 -5.9 -9.8 -3.2

Belgium 107.8 92.0 96.2 100.3 -0.1 -2.8 -4.2 -4.6

France 57.4 66.7 82.3 91.7 -1.5 -3.0 -7.1 -5.1

EU27 61.9 62.9 80.3 84.9 0.5 -2.5 -6.6 -3.2

Germany 60.2 68.6 83.2 79.9 1.1 -3.3 -4.3 -0.7

Spain 59.3 43.0 61.0 78.0 -1.0 1.3 -9.3 -5.3

Austria 66.2 64.2 71.8 73.7 -1.8 -1.8 -4.4 -2.9

Malta 55.0 69.7 69.0 71.5 -5.8 -2.9 -3.6 -3.6

Cyprus 59.6 69.4 61.5 70.9 -2.3 -2.4 -5.3 -4.7

Netherlands 53.8 51.8 62.9 66.0 2.0 -0.3 -5.0 -2.7

Slovenia 26.3 26.7 38.8 54.6 -3.7 -1.5 -5.8 -5.7

Finland 43.8 41.7 48.3 53.5 6.8 2.5 -2.8 -0.8

Slovakia 50.3 34.2 41.0 51.1 -12.3 -2.8 -7.7 -5.2

Luxembourg 6.2 6.1 19.1 20.3 6.0 0.0 -1.1 -0.9

Estonia 5.1 4.6 6.7 6.1 -0.2 1.6 0.3 -0.8

Euro area fiscal indicators, % of GDP

Source: AMECO

Latvia’s example shows that Speed, Ownership,

Commitment and Solidarity works

-20

-15

-10

-5

0

5

10

200

8 I II III

IV

200

9 I II III

IV

201

0 I II III

IV

201

1 I II III

IV

201

2 I

First large consolidation

implemented by Dombrovskis

government

Talks about

consolidation

and inability to

deliver

Real GDP growth, % y-o-y

Source: CSB