Landlord’s Buildings and Contents - MS Amlin plc · Welcome to your Landlord’s buildings and...

38

Landlord’s Buildings and Contents Insurance Policy 1 AOD112-20170302 – SME E trade

Transcript of Landlord’s Buildings and Contents - MS Amlin plc · Welcome to your Landlord’s buildings and...

Landlord’s Buildings and Contents Insurance Policy

1 AOD112-20170302 – SME E trade

Welcome to your Landlord’s buildings and contents insurance policy.

Important Telephone Number and Voucher Code applicable to Section 5 – Legal expenses Counselling assistance 0333 000 2082

For an employee (including family members permanently living with them) needing confidential help and advice, our qualified counsellors are available to provide telephone support on any matter that is causing your employee upset or anxiety, from personal problems to bereavement.

Landlords legal services Register today at www.araglegal.co.uk and enter the voucher code EC426C378CB8 to access the law guide and download tenancy agreements, legal notices to repossess and other legal documents to help with landlord and tenant legal matters.

If you need to make a claim

If you need to make a claim under this policy, please telephone us on 01245 396688 and we will be pleased to advise you of the steps to take. It will assist if you have details of your policy and cover available when telephoning.

In all communications with us please quote your policy number. To make a Legal expenses claim under Section 5 please telephone ARAG on 0117 917 1698 or download a claim form at www.arag.co.uk/newclaims.

We would refer you also to the claims conditions of this policy set out on page 13.

In some cases all or part of your claim may be handled on our behalf by one of our trusted partners. You can rest assured that we will strive to ensure you are provided with exceptional service from MS Amlin and our trusted partners.

2 AOD112-20170302 – SME E trade

Index

If you need to make a claim 2 Important telephone number and voucher code applicable to Section 5 – Legal expenses 2 Important information:

The duty of fair presentation 4 The contract of insurance 4 Changes to your circumstances 4 How to cancel your policy 4 Cancellation instalments 5 Registration and regulatory information 5

Financial Services Compensation Scheme (FSCS) 5 Tax 5 Sanction limitation 5 How to make a complaint 5 Privacy Notice 6 Employers’ Liability tracing Office 7 Contracts (Rights of Third Parties) Act 1999 8 Choice of law 8

General definitions 9 Claims conditions 14 Section 1 – Buildings 17 Section 2 – Contents 22 Section 3 – Landlord legal liability 26 Section 4 – Employers’ liability 27 Section 5 – Legal expenses 28 General conditions applicable to all sections of the policy 32 General exclusions applicable to all sections of the policy 37

3 AOD112-20170302 – SME E trade

Important information

The duty of fair presentation By entering into this insurance contract we accept that you have made a reasonably clear and accessible presentation of the risk, in accordance with Section 3(3)(b) of the Insurance Act 2015. The Contract of Insurance This is your Landlord’s buildings and contents insurance policy. It sets out the details of your insurance contract with us. This document, any endorsements, certificates and the schedule must be read together as one contract as they form your policy. In return for payment of the premium shown in the schedule, we agree to insure you against: • loss or damage you sustain; and • loss resulting from interruption or interference

with the business following damage,

during the period of insurance and in accordance with the terms and conditions contained in or endorsed on this policy. Please read the whole document carefully and keep it in a safe place. You should take the time to read all its terms, especially the conditions which you have to fulfil to ensure your insurance remains valid and what you have to do when making a claim. It is important that you: • check that the sections you have requested are

included in the schedule; • check that the information you have given us is

accurate; and • comply with your duties under each section and

under the insurance as a whole. If this policy does not meet your requirements, or if your requirements change, you should contact your insurance agent at your earliest opportunity.

Changes to your circumstances Please tell your insurance agent as soon as reasonably practicable if there are any changes to your circumstances which could affect your insurance. Please refer to General Conditions 2 of this policy. If your circumstances change and you do not tell your insurance agent, you may find that you are not covered if you need to claim. How to cancel your policy You have a statutory right to cancel your policy within 14 days from the day of purchase or renewal of the contract or the day on which you receive your policy or the renewal documentation, whichever is the later. If you wish to cancel and the insurance cover has not yet commenced, you will be entitled to a full refund of the premium paid. Alternatively, if you wish to cancel and the insurance cover has already commenced, provided you have not made a claim, you will be entitled to a refund of the premium paid, less a proportional deduction for the time we have provided cover. If you do not exercise your right to cancel your policy, it will continue in force and you will be required to pay the premium.

For cancellation outside of this statutory cooling off period you can cancel this insurance at any time by telephoning or writing (by e-mail, fax or letter) to us.

If this insurance is cancelled outside the statutory cooling off period, provided you have not made a claim and there hasn't been an incident that could give rise to a claim, you will be entitled to a refund of any premium paid, less a deduction for any time for which you have been covered. This will be calculated on a proportional basis. For example, if you have been covered for 6 months, the deduction for the time you have been covered will be half the annual premium.

If we pay any claim, in whole or in part, then no refund of premium will be allowed.

4 AOD112-20170302 – SME E trade

Important information

Cancellation – instalment payments

Time is of the essence in relation to your payment of the premium. If you pay your premium by direct debit and there is any default in payment, we will contact you to request payment by a given date, which will be 14 days from the date we contact you. If payment is still not received by this date, we may then cancel this policy. No refund or credit of premium will be due when cancellation takes place in these circumstances. For our rights to cancel your policy please refer to General condition 1. Registration and regulatory information Amlin UK is a trading name of Amlin UK Limited. Amlin UK Limited is wholly owned by and an appointed representative of MS Amlin Underwriting Limited which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority under reference number 204918. Amlin UK Limited is registered in England No. 02739220. Registered office: Leadenhall Building, 122 Leadenhall Street, London, EC3V 4AG. Financial Services Compensation Scheme (FSCS) Lloyd’s insurers are covered by the Financial Services Compensation Scheme. You may be entitled to compensation from the Scheme if a Lloyd’s insurer is unable to meet its obligations to you under this policy. If you were entitled to compensation from the Scheme, the level and extent of the compensation would depend on the nature of this policy. Further information about the Scheme is available from the Financial Services Compensation Scheme (10th Floor, Beaufort House, 15 St. Botolph Street, London EC3A 7QU) and on their website www.fscs.org.uk Tax You will pay any tax due on the premium in accordance with current legislation.

Sanction limitation This policy will not provide any insurance cover or benefit and we will not pay any sum if doing so would mean that we are in breach of any sanction, prohibition or restriction imposed by any laws or regulations. How to make a complaint Our aim is to ensure that all aspects of your insurance are dealt with promptly, efficiently and fairly. At all times we are committed to providing you with the highest standard of service. If you have any questions or concerns about your policy or the handling of a claim you should, in the first instance, contact your insurance agent. If you remain dissatisfied and wish to make a complaint, you can do so at any time. Making a complaint does not affect any of your legal rights. For all sections except 5: Our contact details are: Post: Complaints, MS Amlin Underwriting Limited, The Leadenhall Building, 122 Leadenhall Street, EC3V 4AG. Telephone: +44 (0) 20 7746 1300 Fax: +44 (0) 20 7746 1001 Email: [email protected] Website: www.msamlin.com For section 5 please contact ARAG plc (the administrator): Post: ARAG plc, Customer Relations Department,

9 Whiteladies Road, Clifton, Bristol, BS8 1NN Telephone: +44 (0) 117 917 1561 Email: [email protected] Website: www.arag.co.uk If your complaint cannot be resolved within two weeks, or if you have not received a response within two weeks you are entitled to refer the matter to Lloyd’s. Lloyd’s will then conduct a full investigation of your complaint and provide you with a written final response. Lloyd’s contact details are:

5 AOD112-20170302 – SME E trade

Important information

Post: Complaints, Lloyd’s Fidentia House, Walter Burke Way, Chatham Maritime, Chatham Kent ME4 4RN

Telephone: +44 (0) 20 7327 5693 Fax: +44 (0) 20 7327 5225 Email: [email protected]

Details of Lloyd’s complaints procedures are set out in a leaflet “Your Complaint – How We Can Help” available at www.lloyds.com/complaints and are also available from the above address. If you remain dissatisfied after Lloyd’s has considered your complaint, or if you have not received a written final response within eight weeks from the date your complaint was received, you may be entitled to refer your complaint to the Financial Ombudsman Service who will independently consider your complaint free of charge. Their contact details are: Post: The Financial Ombudsman Service,

Exchange Tower, London E14 9SR Telephone: (Fixed): 0800 0234567l (Mobile): 0300 1239123 (Outside UK): +44 (0) 20 7964 0500 Fax: +44 (0)20 7964 1001 Email: complaint.info@financial- ombudsman.org.uk Website: www.financial-ombudsman.org.uk

Alternatively, if you have bought a product or service online you may have the right to register your complaint with the European Commission’s on-line dispute resolution (ODR) platform. The ODR platform will redirect your complaint to the appropriate alternative dispute resolution body.

For further details visit http://ec.europa.eu/odr Please note: • You must refer your complaint to the Financial

Ombudsman Service within six months of the date of Lloyd’s final response.

The Financial Ombudsman Service will normally only consider a complaint from private individuals or from a business that has an annual turnover of less than 2 million Euros and fewer than 10 employees.

Privacy Notice Information we process You should understand that information you provide, have provided and may provide in future will be processed by us, in compliance with UK data privacy laws for the purpose of providing insurance, handling claims and/or responding to complaints. Information containing personal and sensitive personal information Information we process may be defined as personal and/or sensitive personal information. Personal information is information that can be used to identify a living individual e.g. name, address, driving licence or national insurance number. Personal information is also information that can identify an individual through a work function or their title. In addition, personal information may contain sensitive personal information; this can be information about your health and/or any criminal convictions. We will not use personal and/or sensitive personal information except for the specific purpose for which you provide it and to carry out the services as set out within this notice. Collecting electronic information If you contact us via an electronic method, we may record your internet electronic identifier i.e. your internet protocol (IP) address. Your telephone company may also provide us with your telephone number. How we use your information Your personal and/or sensitive personal information may be used by us in a number of ways, including to: • arrange and administer an application for

insurance; • manage and administer the insurance; • investigate, process and manage claims;

and/or • prevent fraud. Who we share your information with We may pass your personal and/or sensitive personal information to industry related third parties, including authorised agents; service providers; reinsurers; other insurers; legal advisers; loss adjusters; and claims handlers. We may also share your personal and/or sensitive personal information with law enforcement, fraud detection, credit reference and debt collection

6 AOD112-20170302 – SME E trade

Important information

agencies and within the MS Amlin Group of companies to: • assess financial and insurance risks; • recover debt; • to prevent and detect crime; and/or • develop products and services. We will not disclose your personal and/or sensitive personal information to anyone outside the MS Amlin Group of companies except: • where we have your permission; • where we are required or permitted to do so by

law; • to other companies who provide a service to

us or you; and/or • where we may transfer rights and obligations

under the insurance.

Why it is necessary to share information Insurance companies share claims data to: • ensure that more than one claim cannot be

made for the same personal injury or property damage;

• check that claims information matches what was provided when the insurance was taken out;

• act as a basis for investigating claims when we suspect that fraud is being

attempted; and/or respond to requests for information from law enforcement agencies.

The transferring of information outside the European Economic Area In providing insurance services, we may transfer your personal and/or sensitive personal information to other countries including countries outside the European Economic Area. If this happens we will ensure that appropriate measures are taken to safeguard your personal and/or sensitive personal information. Access to your information You have a right to know what personal and/or sensitive personal information we hold about you. If you would like to know what information we hold, please contact the MS Amlin Data Privacy Officer at the address listed within this notice, stating the reason for your enquiry. We may write back requesting you to confirm your identity, we may also charge a fee of £10 for processing your enquiry. If we do hold information about you, we will: • give you a description of it; • tell you why we are holding it; • tell you who it could be disclosed to; and

• let you have a copy of the information in an intelligible form.

If some of your information is inaccurate, you can ask us to correct any mistakes by contacting our Data Privacy Officer. Providing consent to process your information By providing us with your personal and/or sensitive personal information, you consent to your information being used, processed, disclosed, transferred and retained for the purposes set out within this notice. If you supply us with personal information and/or sensitive personal information of other people, please ensure that you have fairly and fully obtained their consent for the processing of their information. You should also show this notice to the other people. You should understand that if you do not consent to the processing of your information or you withdraw consent, we may be unable to provide you with insurance services. Changes to this Notice We keep our privacy notice under regular review. This notice was last updated on the 20th October 2015. Contacting us If you have any questions relating to the processing of your information, please write to The MS Amlin Data Privacy Officer, The Leadenhall Building, 122 Leadenhall Street, London EC3V 4AG.

You can also email: [email protected] For information about the MS Amlin Group of companies please visit www.msamlin.com.

7 AOD112-20170302 – SME E trade

Important information

Employers’ Liability Tracing Office By entering into this insurance policy you will be deemed to specifically consent to the use of your insurance policy data in the following way and for the following purposes. 1. Certain information relating to your insurance

policy including, without limitation:

a) the policy number(s); b) employers’ names and addresses

(including subsidiaries and any relevant changes of name);

c) dates of cover; d) employer’s reference numbers provided

by Her Majesty’s Revenue and Customs; and

e) Companies House reference numbers (if

relevant), will be provided to the Employers’ Liability

Tracing Office (ELTO) and added to an electronic database.

2. This information will be made available by us

to ELTO in a specified and readily accessible form as required by the Employers’ Liability Insurance: Disclosure by Insurers Instrument 2011. This information will have regular periodic updating and certification and will be audited on an annual basis.

3. The database will assist individual consumer

claimants who have suffered an employment related injury or disease arising out of their course of employment in the UK for employers carrying on or who carried on business in the UK and who are covered by the employers’ liability insurance of their employers (claimants):

a) to identify which insurer (or insurers)

provided employers’ liability cover during the relevant periods of employment; and

b) to identify the relevant employers’ liability insurance policies. 4. The database will be managed by ELTO. 5. The database and the data stored on it may

be accessed and used by claimants, their appointed representatives, insurers with potential liability for UK commercial lines employers’ liability insurance cover and any other persons or entities permitted by law.

Contracts (Rights of Third Parties) Act 1999 A person or company who was not party to this policy has no right under the Contracts (Rights of Third Parties) Act 1999 to enforce any term of this policy but this condition does not affect any right or remedy of a third party which exists or is available other than by virtue of this Act and any further amendment to it.

Choice of law and jurisdiction In the absence of any agreement to the contrary, the laws of England and Wales will apply and this policy will be subject to the exclusive jurisdiction of the courts of England unless, at the start of the period of insurance, you are either: a) a resident of; or

b) a business with its registered office or

principal place of business is situated in;

Scotland, Northern Ireland, the Channel Islands or the Isle of Man, in which case (in the absence of agreement to the contrary) the law of that country, crown protectorate or dependency will apply and this policy will be subject to the exclusive jurisdiction of the courts of that country, crown protectorate or dependency.

8 AOD112-20170302 – SME E trade

General definitions

The following definitions apply in all sections of this policy unless otherwise stated. Each time one of the words below is used it will have the same meaning wherever it appears in the policy or schedule. To help identify these words they will appear in bold in the policy wording.

Bodily injury Death, injury, illness, disease or nervous shock. Buildings The buildings at the premises shown in your schedule including:

a) landlord’s fixtures and fittings; b) outbuildings, annexes, private garages,

gangways, foundations or footings, swimming pools, tennis courts, squash courts, gymnasia used by residents for domestic and leisure purposes;

c) walls, gates, fences and hedges; d) roadways, paths, yards and car parks; e) underground pipes and cables belonging to

you or which you are responsible for; f) tenants improvements which you are

responsible for; g) street furniture, lampposts, fanlights,

skylights and partitions; h) telecommunications aerials, aerial fittings,

masts and closed circuit television (CCTV); i) solar panels and wind turbines attached to

the building;

j) cess pits, septic tanks, pavements, paved terraces, patios, drives; and

k) contents of communal areas, situated in the territorial limits. Business The business stated in the schedule.

Contents of communal areas a) Carpets, furniture and furnishings and

gardening equipment other than valuables belonging to you or for which you are responsible whilst contained within the building or within any office but not within any premises.

b) Garden furniture in the open or within the building.

Costs and expenses (Applicable to sections 3 and 4) a) claimants costs and expenses arising for

any claim against you which may be the subject of cover under this policy; and

b) all cost and expenses incurred by you with

our written consent for any claim against you which may be the subject of cover under this policy.

Damage Loss or destruction of or damage to property insured by this policy. Denial of service attack Any actions or instructions constructed or generated with the ability to damage, interfere with or otherwise affect the availability of networks, network services, network connectivity or information systems. Denial of service attacks include, but are not limited to, the generation of excess traffic into network addresses, the exploitation of system or network weaknesses and the generation of excess or non-genuine traffic between and amongst networks. Deposit The sum paid by the tenant to you or the managing agent under the terms of the tenancy agreement for the purpose of providing you with an reimbursement or partial reimbursement against losses arising from the tenant’s breach of any of the terms of the tenancy agreement.

9 AOD112-20170302 – SME E trade

General definitions

Employee Any person who is: a) under a contract of service with you; or b) self-employed and working for you and

under your control. Excess This is the first part of any claim that you will have to pay after the application of all other terms and conditions of the policy. Hacking Unauthorised access to any computer or other equipment or component or system or item which processes stores or retrieves data, whether your property or not. Land Land belonging to the premises. Landlord’s contents’ a) Computer equipment;

b) Contents – Landlord’s: being household

goods and furnishings, appliances and satellite dishes and receiving aerials for which you are responsible and contained within the buildings. Examples include demountable partition systems, telephone systems, CCTV systems, edge-fitted and loose-laid carpets, blinds, curtains and curtain rails, paintings or mirrors that are not bolted but hung or screwed to a wall, notice boards, beds/sofas and other free standing items of furniture or equipment, lamps and lampshades, potted plants and shrubs (in containers);

c) Contents – Other: being contents at the premises which do not belong to you as landlord of the premises;

d) White Goods: being washing machines,

tumble dryers, washer dryers; built-in washing machines and tumble dryers, dishwashers and built-in dish washers, fridge freezers, freezers, fridges, chest freezers, American style fridge freezers, wine coolers, under counter fridges and built-in fridge freezers, fridges, freezers and larders. Under counter freezers, under counter wine coolers and under counter larders. Ovens, hobs, range cookers, microwaves, cookers, cooker hoods and extractor fans, built-in microwaves, oven hobs, cookers and cooker hoods. Compact ovens, microwaves and slow cookers.

Valuables, clothings and pedal cycles are not included. Landlord’s fixtures and fittings Include items which are owned by you and are reasonably permanent and affixed to the property through the application of plaster, cement, bolts, screws, nuts, or nails. Examples include fixed partitions and doors, electrical installations, electric sockets, light fittings, security alarm systems, television aerials and satellite dishes, fires and fire surrounds, central-heating boilers and radiators, plumbing installations, bathroom suites and other sanitaryware installations, vanity furniture, cubicles/ shower screens, kitchen units, sinks, adhered floor finishes, door furniture, built-in furniture, worktops, built in wardrobes/ cupboards/ shelf units, wall paintings and plants and shrubs [rooted] in land belonging to the property. Legal charge A legal document held by the Land Registry showing who has a claim on a property. Limit of liability The maximum amount we will pay in respect of any one loss or series of losses arising from the same original incident.

10 AOD112-20170302 – SME E trade

General definitions

Offshore From the time of embarkation by an employee onto a conveyance at the point of final departure to an offshore rig or offshore platform until disembarkation by that employee from a conveyance on to land upon return from an offshore rig or offshore platform. Period of insurance The period from the effective date shown in the schedule until midnight on the expiry date shown in the schedule. Phishing

Any access or attempted access to data or

information made by means of misrepresentation or deception. Pollution Pollution or contamination by naturally occurring or man-made substances, forces, organisms or any combination of them whether permanent or transitory and all loss, damage or injury, caused by pollution or contamination. Premises The private residence owned by you and let to tenants as detailed in your schedule. Principal The other party to a contract or agreement for whom you are undertaking work or services where that party is responsible for setting out the terms of the contract or agreement. Reinstatement 1. the rebuilding or replacement of property

lost or destroyed which, provided our liability is not increased, may be carried out in any manner suitable to you or on another site; or

2. the repair or restoration of property

damaged

in either case to a condition equal to but not better or more extensive than its condition when new. Remediation Remedying the effects of pollution.

Rent arrears Money owed to you by an accepted tenant under a tenancy agreement (less the deposit or the balance of the deposit following sight of accounted receipts relating to dilapidations caused to the premises by the tenant/s). Roadways, paths, yards and car parks Roads, paths, yards and car parks which are on your land which form part of the property insured. Sum insured the amount of money that we are obligated to cover in the event of a covered loss. Tenancy agreement a) A tenancy agreement in writing made between

you and the tenant which is an Assured Shorthold Tenancy Agreement within the meaning of the Housing Acts 1988 and 1996or a Short Assured tenancy or an Assured Tenancy as defined in the Housing (Scotland) Act 1988. In Northern Ireland the Agreement between you and the tenant to let the premises must not be a Protected Tenancy or a Statutory Tenancy within the meaning of the Rent (NI) Order 1978 nor a Protected Shorthold Tenancy within the meaning of Housing (NI) Order 1983.Tenancy Agreements in which the tenant is a limited company or a tenancy agreement or lease of commercial premises are not included in this definition.

b) Any other residential tenancy as agreed and accepted by us in writing (excluding agricultural holdings or tied accommodation).

Tenant A person occuping your premises by virtue of a tenancy agreement. Territorial limits England, Scotland, Wales, Northern Ireland, the Channel Islands and Isle of Man.

11 AOD112-20170302 – SME E trade

General definitions

Terrorism a) acts of persons acting on behalf of, or in

connection with, any organisation which carries out activities directed towards the overthrowing, by force or violence, of Her Majesty’s government in the United Kingdom or any other legitimate government or accepted (illegitimate) government;

b) any action in controlling, preventing, suppressing, retaliating against or responding to any act or preparation for action or threat of action described in a) above.

Uninhabitable Not in a sufficient condition to be lived in. Unoccupied Any building or part of any building that is not in use by you or any authorised person. Valuables Articles of precious metals, jewellery, watches, stamps, medals, money, photographic equipment, furs, unusual objects, works of art and home computer equipment. Vermin Various small animals or insects, (for example brown or black rats, cockroaches, house or field mice, wasps or hornets), that are destructive, annoying or present a health hazard. Virus or similar mechanism Program code, programming instruction or any set of instructions intentionally constructed with the ability to damage, interfere with or otherwise adversely affect computer programs, data files or operations, whether involving self-replication or not. The definition of virus or similar mechanism includes but is not limited to Trojan horses, worms and logic bombs.

We/us/our Lloyd’s Syndicate 2001 managed by MS Amlin Underwriting Limited through its appointed representative Amlin UK Limited. You/your The policyholder named in the schedule

12 AOD112-20170302 – SME E trade

General definitions

The following definitions only apply to Section 5 – Legal Expenses Appointed adviser The solicitor, accountant, mediator or other suitably qualified person, who has been appointed by us to act for you in accordance with the terms of this policy. Collective conditional fee agreement A legally enforceable agreement entered into on a common basis between the appointed adviser and us to pay their professional fees on the basis of “no-win no-fee Conditional fee agreement A legally enforceable agreement between you and the appointed adviser for paying their professional fees on the basis of “no-win no-fee”. Costs and expenses a) Reasonable legal costs, fees and

disbursements reasonably and proportionately incurred by the appointed adviser on the standard basis and agreed in advance by us;

b) In civil claims, the other side's costs, fees and disbursements where you have been ordered to pay them or you pay them with our consent

Insured property a) buildings owned by you which are let or

which you intend to let to tenants for residential purposes and/or

b) accommodation which is owned by you and which you let or intend to let to guests as holiday accommodation for leisure purposes under the terms of a written agreement,

located within England, Scotland, Wales or Northern Ireland. Property Material property or land.

Reasonable prospects of success a) You must have a greater than fifty percent

chance of successfully pursuing or defending your claim and if you are seeking damages, a greater than fifty percent chance of enforcing any judgement that might be obtained.

.

b) In all claims involving an appeal there must be a greater than fifty percent chance that you will be successful.

Small claims court A court in: a) England and Wales that hears a claim falling

under the small claims track in the County Court as defined by Section 26.6 (1) of the Civil Procedure Rules 1999;

b) Scotland that uses the small claims procedure as set out by the Court Reform Act (Scotland) 2014;

c) Northern Ireland where the sum in dispute is less than £3,000.

Standard basis The basis of assessment of costs where the court only allows recovery of costs which are proportionate to the claim and which have been reasonably incurred.

13 AOD112-20170302 – SME E trade

Claims conditions

1. Arbitration

If we agree to pay your claim and you disagree with the amount to be paid it may be referred to an arbitrator who is jointly appointed. Whether we or you bear the costs of the arbitration, or these are shared by us and you, will be determined at the discretion of the arbitrator. Alternatively, depending on the size of your business, you may be able to refer your case to the Financial Ombudsman Service (FOS). In either case, this will not affect your right to take action against us over the disagreement.

2. Claims co-operation

You must provide all help, assistance and co-operation reasonably required by us in connection with any claim.

3. Claims procedures

If you need to make a claim you must comply with the following conditions. If you fail to do so, we may not pay your claim, or any payment could be reduced.

a) You must notify your insurance agent as

soon as reasonably practicable giving full details of what has happened.

b) You must provide your insurance agent with any other information we may reasonably require.

c) You must forward to your insurance agent as soon as reasonably practicable, if a claim for liability is made against you, any letter, claim, writ, summons or other legal document you receive.

d) You must inform the police as soon as reasonably practicable following any loss caused by malicious acts, violent disorder, riots or civil commotion, theft, attempted theft or lost property.

e) You must not admit liability or offer or agree to settle any claim without our written permission.

f) You must take practical steps to prevent further damage or bodily injury, recover property lost and otherwise minimise the claim.

4. Discharge of liability

Where in our opinion, the limit of liability or the sum insured of any claim may exceed the available limit of liability or sum insured we will be entitled at our discretion, to discharge our liability by paying the available limit of liability or sum insured to you or on your behalf and pay defence costs up to the date of that payment. In this situation, if at the time of payment we are conducting the defence of the claim, we will also relinquish that conduct.

5. Fraudulent claims

If you or anyone acting on your behalf makes a fraudulent claim under your policy, including providing fraudulent information or documentation, we may: a) refuse to pay the claim; b) seek to recover any of costs already

incurred by us relating to the fraudulent claim;

c) also have the option to cancel the policy

from the date of the discovery of the fraud; and

d) keep any premium paid to us. This will not affect claims already made unless they too were fraudulent. If your policy covers more than one insured and a fraudulent claim is made by one of those insureds, we will treat that claim in accordance with the above, but the rights of the other insured(s) under the policy will not be affected.

6. Other insurance

If you have any other insurance which covers the same loss, damage or liability, we will only pay our pro rata share of any claim.

7. Salvage

We may enter the premises where damage has occurred and take possession of or require to be delivered to us any property insured and deal with it in a reasonable manner but property may not be abandoned to us.

14 AOD112-20170302 – SME E trade

Claims conditions

8. Subrogation

We are entitled to:

a) take over and conduct the defence orsettlement of any claim in your name or onyour behalf at our discretion; and

b) take steps to enforce rights against anyother party before or after payment is madeby us.

Claims conditions which only apply to Section 5 – Legal expenses We have appointed Arag Plc to act on our behalf for all claims arising under Section 5 - Legal expenses.

1. Barrister’s opinion

We may require you to obtain and pay for an opinion from a barrister if a dispute arises regarding the merits or value of the claim. If the opinion supports you, then we will reimburse the reasonable costs of that opinion. If that opinion conflicts with advice obtained by us, then we will pay for a final opinion which will be binding on you and us. This does not affect your right under Arbitration, Claims condition 1.

2. Claims Procedures

If you need to make a claim you must notify ARAG plc as soon as possible.

a) Under no circumstances should you instructyour own lawyer or accountant as we will notpay any costs incurred without ouragreement.

b) You can request a claim form between 9amand 5pm Monday to Friday (except bankholidays) by telephoning 0117 917 1698 oranytime by downloading one atwww.arag.co.uk/newclaims;

c) Where you are making a claim to repossessan insured property, you must have issuedthe necessary notices informing your tenantof your intention to repossess the insuredproperty;

d) We will issue you with a writtenacknowledgement within one working day ofreceiving their claim form.

e) Within five working days of receiving all theinformation needed to assess the availabilityof cover under this section of the policy, wewill write to you either:

i) confirming the appointment of a qualifiedrepresentative who will promptlyprogress the claim for them; or

ii) if the claim is not covered, explaining infull why and whether we can assist inanother way.

When a lawyer is appointed they will try to resolve your dispute without delay, arranging mediation whenever appropriate. Matters cannot always be resolved quickly particularly if the other side is slow to cooperate or a legal timetable is decided by the courts.

3. Consent

You must agree to us having sight of the appointed adviser’s file relating to your claim. You are considered to have provided consent to us or our appointed agent to have sight of the appointed adviser’s file for auditing and quality and cost control purposes.

4. Freedom to choose an appointedadviser

a) In certain circumstances, as set out in 7.b)below, you may choose an appointedadviser. In all other cases no such rightexists and we will choose the appointedadviser.

b) If:

i) we agree to start proceedings orproceedings are issued against you; or

ii) there is a conflict of interest,

you may choose a qualified appointed adviser except where your claim is to be dealt with by the Employment Tribunal or small claims court where we will always choose the appointed adviser.

c) Where your wishes to exercise your right tochoose, they must write to us (by e-mail, faxor letter) with their preferred representative’scontact details. Where you chooses to usetheir preferred representative we will not paymore than we agree to pay a solicitor fromour panel.

15 AOD112-20170302 – SME E trade

Claims conditions

d) If you dismisses the appointed adviser without good reason, or withdraws from the claim without our written agreement or if the appointed adviser refuses with good reason to continue acting for you cover under section 5 will end immediately for Section 5.

5. Settlement

a) We can settle the claim by paying the reasonable value of your claim.

b) You must not negotiate, settle the claim or agree to pay costs and expenses without our written agreement.

If you refuses to settle the claim following a reasonable offer or advice to do so from the appointed adviser, we reserve the right to refuse to pay further costs and expenses.

6. Your responsibilities

You must:

a) cooperate fully with us, give the

appointed adviser any instructions we require, and keep them updated with progress of the claim and not hinder them;

b) take reasonable steps to recover costs and expenses and pay them to us;

c) keep costs and expenses as low as possible;

d) allow us at any time to take over and conduct in your name, any settlement or defence of any claim or to prosecute for our own benefit any claim for indemnity or compensation or otherwise and have full discretion in the conduct of any proceedings and in settlement of any claim, proceeding or investigation.

16 AOD112-20170302 – SME E trade

Section 1 – Buildings cover

(This section only applicable if shown as being included or insured/covered on the schedule). Important Note: Any successful claim for buildings will be liable to the excess as stated on the schedule.

What is covered What is not covered We cover your buildings against damage caused by the following:

1. Fire, explosion, lightning, or earthquake.

a)

b)

Damage caused by smog, industrial or agricultural output; damage caused by riot, civil commotion or subterranean fire.

2. Smoke. a)

b)

Damage caused by smog, industrial or agricultural output; damage caused by riot, civil commotion or subterranean fire.

3. Storm or flood.

a)

b)

c)

Damage caused by frost, subsidence, ground leave or slip or lightning; damage to domestic fixed fuel-oil tanks in the open, drives, patios and terraces, gates and fences, swimming pools, tennis courts; damage caused by rising water table levels.

4. Escape of water or oil from any fixed water or heating installation, apparatus and pipes.

a)

b)

c) d)

Damage whilst the buildings are unoccupied for 30 days or more; damage to the apparatus and/or pipes from which water or oil has escaped; damage caused by gradual emission; The first £250 of every claim unless otherwise specified in your schedule.

5. Freezing or forcible or violent bursting of any fixed water or heating installation, apparatus or pipes.

a) Damage whilst the buildings are unoccupied for 30 days or more.

6. Theft or attempted theft caused by violent and forcible entry or exit.

a)

b)

c)

Damage by any tenant or person lawfully on the premises; damage whilst the buildings are unoccupied for 30 days or more; damage caused by deception unless deception is used solely to gain entry to your premises.

7. Riot, strike, civil commotion, labour and political disturbances.

a) Damage in Northern Ireland.

17 AOD112-20170302 – SME E trade

Section 1 – Buildings cover

What is covered What is not covered 8. Malicious damage or vandalism.

a) b)

Damage whilst the buildings are unoccupied for 30 days or more; damage by any tenant or person lawfully on the premises.

9. Subsidence, landslip or heave of the site upon which the buildings stand.

a) b) c) d) e) f) g) h) i)

Damage caused by erosion of the coast or riverbank; damage to domestic fixed fuel-oil tanks, swimming pools, tennis courts, drives, patios and terraces, walls, gates and fences unless the main building is damaged at the same time; damage caused by structural repairs, alterations, demolitions or extensions; damage arising from faulty or defective workmanship, designs or materials; normal settlement, shrinkage or expansion; the first £1,000 of every claim unless otherwise specified in your schedule; damage that originated before the start of this insurance; damage caused by the movement of solid floors unless the foundations beneath the floor are damaged at the same time and by the same cause; damage to buildings caused by the action of chemicals or by the reaction of chemicals with any material which forms part of the buildings.

10. Collision or impact by any animal, vehicle, aircraft or aerial devices and including items dropped from them.

11. Falling trees and branches, telegraph poles, lamp-posts.

a)

Damage caused by maintenance to trees.

12. Falling satellite dishes, receiving aerials and their fittings and masts.

a) Damage caused to them.

13. Damage to fixed glass, sanitary fixtures and ceramic hobs forming part of the property.

a) b) c)

Damage whilst the buildings are unoccupied, for 30 days or more; damage caused by chipping, denting or scratching; damage to ceramic hobs in free–standing cookers.

14. Damage to underground pipes, cables and services for which you are responsible.

a) b)

Damage due to wear and tear or gradual deterioration; damage caused by faulty materials, design, workmanship or as a consequence of any alterations, renovations or repairs.

18 AOD112-20170302 – SME E trade

Section 1 – Buildings cover

What is covered What is not covered 15. Accidental damage to the buildings which is not covered under Insured Events listed in paragraphs 1 to 12 of this section.

Damage: a) domestic pets; b) whilst the buildings are unoccupied for 30 days or more; c) cost of normal maintenance; d) caused by wet or dry rot; faulty workmanship or design; e) as a result of any building alterations, renovations or repairs; f) if previously specifically excluded from cover. g) The first £250 of each claim arising under

this Insured Event.

16. Clearing of drains, gutters and sewers.

a) Any amount in excess of £2,500 any one loss.

17. Loss of rent and/or cost of alternative accommodation incurred by you as a result of the buildings becoming uninhabitable following loss or damage caused by any of the Insured Events listed in Section 1.

a) b)

Any amount exceeding 25% of the limit of liability on the buildings damaged and for losses incurred in a period exceeding 12 months from the date the buildings became uninhabitable, unless stated otherwise in the schedule; any claim where damage under Section 1 has not been accepted by us.

18. Increased metered water charges incurred by you resulting from escape of water and/or a further claim under Insured Event 3.

a)

Any amount exceeding £1,000 in any period of insurance.

19. Expenses incurred by you as a result of removal of debris; compliance with Government or Local Authority requirements; architects’ and surveyors’ fees incurred in the reinstatement of the building following loss or damage caused by any of the Insured Events listed in Section 1.

a) Any fees charged in the preparation of a claim.

20.Trace and Access - We will pay up to £25,000 for the costs with our written consent in locating the source of any damage resulting from the escape of water from fixed domestic water services or heating installations including the cost of repairs to walls, floors ceilings.

a) b)

Any damage to the heating or water system from which water or oil has escaped; any amount exceed £25,000 for any one loss.

21. Emergency Access - We will provide cover for damage to the buildings caused by forced access by the fire, police or ambulance services as a result of an emergency, at the premises.

a) Any amount in excess of £1,000 for any one loss.

19 AOD112-20170302 – SME E trade

Section 1 – Buildings cover

What is covered What is not covered

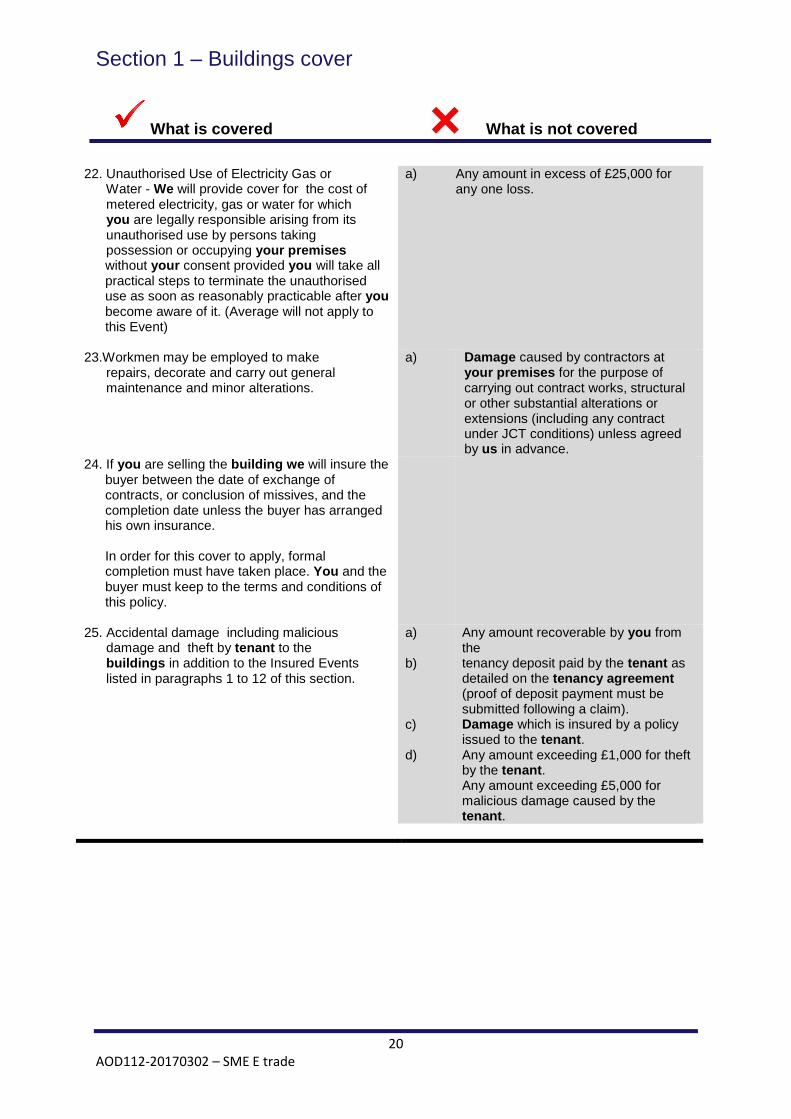

22. Unauthorised Use of Electricity Gas or Water - We will provide cover for the cost of metered electricity, gas or water for which you are legally responsible arising from its unauthorised use by persons taking possession or occupying your premises

without your consent provided you will take all practical steps to terminate the unauthorised use as soon as reasonably practicable after you become aware of it. (Average will not apply to this Event)

a) Any amount in excess of £25,000 for any one loss.

23.Workmen may be employed to make repairs, decorate and carry out general maintenance and minor alterations.

a) Damage caused by contractors at your premises for the purpose of carrying out contract works, structural or other substantial alterations or extensions (including any contract under JCT conditions) unless agreed by us in advance.

24. If you are selling the building we will insure the buyer between the date of exchange of contracts, or conclusion of missives, and the completion date unless the buyer has arranged his own insurance.

In order for this cover to apply, formal completion must have taken place. You and the buyer must keep to the terms and conditions of this policy.

25. Accidental damage including malicious damage and theft by tenant to the buildings in addition to the Insured Events listed in paragraphs 1 to 12 of this section.

a) b) c) d)

Any amount recoverable by you from the tenancy deposit paid by the tenant as detailed on the tenancy agreement (proof of deposit payment must be submitted following a claim). Damage which is insured by a policy issued to the tenant. Any amount exceeding £1,000 for theft by the tenant. Any amount exceeding £5,000 for malicious damage caused by the tenant.

20 AOD112-20170302 – SME E trade

Section 1 – Buildings cover

Conditions applicable to this Section 1 – Buildings cover Average Wherever a sum insured is stated to be in accordance with average, if at the time of any damage the sum insured on any item of the buildings is less than the total value of the property, you will be considered as being your own insurer for the difference and will bear a rateable share of the loss accordingly. Basis of claims settlement Following damage to the buildings, we will pay the full cost of reinstatement as long as the buildings are maintained in a good state of repair and they are insured for the full cost of reinstatement. If the buildings have not been maintained in a good state of repair, we will make a deduction for wear and tear or gradual deterioration. For any claim made under this policy, our liability will: 1. not exceed the proportion that the limit of liability bears to the full cost of reconstruction of your buildings as stated in the schedule; 2. not exceed the limit of liability for the buildings as stated in the schedule. It is your responsibility to ensure at all times the buildings sum insured reflects the total cost of reinstatement and associated fees including the proportionate share of communal parts and the structure of the building for which you are legally responsible. We will not be liable for any additional costs incurred for delays resulting from the co-ordination of repairs with other property owners (and/or their Insurers) within the block. Following an insured incident to any part of the premises not occupied by you but for which you are legally responsible we will only pay the proportion of that loss as the limit of liability bears to the reinstatement value of the building. We will not pay for the cost of replacing or repairing any undamaged part(s) of the building which forms part of a pair, set, suite or part of a common design. We will not reduce the limit of liability under this section following a claim provided that you agree to carry out our recommendations to prevent further damage.

Index-linking clause The sums insured under this section may be adjusted each month in accordance with the following indices: • The House Rebuilding Costs Index, issued by the Royal Institute of Chartered Surveyors; No additional premium will be charged for each monthly increase but at each renewal the premium will be calculated on the revised sums insured and will be shown on your renewal schedule.

21 AOD112-20170302 – SME E trade

Section 2 – Contents cover

This section is provided as a core cover Important Note: Any successful claim for landlord’s contents’ will be liable to the excess as stated on the schedule.

What is covered What is not covered We will cover your landlord’s contents’ up to £25,000 any one loss against damage caused by the following Insured Events:

1. Fire, explosion, lightning, or earthquake.

a) b)

Damage caused by smog, industrial or agricultural output; damage caused by riot, civil commotion or subterranean fire.

2. Smoke. a) b)

Damage caused by smog, industrial or agricultural output; damage caused by riot, civil commotion or subterranean fire.

3. Storm or flood.

a) b) c) d)

Damage caused by frost, subsidence, ground leave or slip or lightning; damage to domestic fixed fuel-oil tanks in the open, drives, patios and terraces, gates and fences, swimming pools, tennis courts; damage caused by rising water table levels; landlord’s contents’ in the open.

4. Escape of water or oil from any fixed water or heating installation, apparatus and pipes.

a) b) c) d)

Damage whilst the buildings are unoccupied for 30 days or more; damage to the apparatus and/or pipes from which water or oil has escaped; damage caused by gradual emission; the first £250 of every claim unless otherwise specified in your schedule.

5. Theft or attempted theft caused by violent and forcible entry or exit.

a) b) c) d)

Damage by any tenant or person lawfully on the property; damage whilst the buildings are unoccupied for 30 days or more; any amount exceeding £500 for landlord’s contents’ contained within detached domestic outbuildings and garages; damage of any item whilst in the open.

6. Riot, strike, civil commotion, labour and political disturbances.

a) Damage in Northern Ireland.

7. Malicious damage or vandalism.

a) b)

Damage whilst the buildings are unoccupied for 30 days or more; damage by any tenant or person lawfully on the property.

22 AOD112-20170302 – SME E trade

Section 2 – Contents cover

What is covered What is not covered 8. Subsidence, landslip or heave of the site

upon which the buildings stand. a) b) c) d) e) f) g) h) i)

Damage: caused by erosion of the coast or riverbank; to domestic fixed fuel-oil tanks, swimming pools, tennis courts, drives, patios and terraces, walls, gates and fences unless the main building is damaged at the same time; caused by structural repairs, alterations, demolitions or extensions; arising from faulty or defective workmanship, designs or materials; that originated before the start of this insurance; caused by the movement of solid floors unless the foundations beneath the floor are damaged at the same time and by the same cause; to landlord’s contents’’ caused by the action of chemicals or by the reaction of chemicals with any material which forms part of the buildings; Normal settlement, shrinkage or expansion; The first £1,000 of every claim unless otherwise specified in your schedule;

9. Collision or impact by any animal, vehicle, aircraft or aerial devices and including items dropped from them.

10. Falling trees and branches, telegraph poles, lamp-posts.

a)

Damage caused by maintenance to trees.

11. Falling satellite dishes, receiving aerials and their fittings and masts.

a) Damage caused to them.

12. Accidental damage to the landlord’s contents in addition to the Insured Events listed in paragraphs 1 to 11 of this section.

Damage: a) whilst the buildings are unoccupied for 30 days or more; b) cost of normal maintenance; d) caused by faulty workmanship or design; e) as a result of any building alterations, renovations or repairs; f) damage if specifically excluded from cover.

13. Clearing of drains, gutters and sewers up to £2,500 any one loss.

23 AOD112-20170302 – SME E trade

Section 2 – Contents cover

What is covered What is not covered 14. Loss of rent and/or cost of alternative accommodation incurred by you as a result of the buildings becoming uninhabitable following loss or damage caused by any of the Insured Events listed in Section 1.

a) b)

Any amount exceeding 20% of the limit of liability applicable to landlord’s contents’ on the buildings damaged and for losses which have occurred in a period exceeding 12 months from the date the property became uninhabitable, unless stated otherwise in the schedule; any claim where damage under Section 1 has not been accepted by us.

15. Loss of keys – for replacing necessary locks and keys of:

a) alarms and safes installed in the premises; and

b) external doors and windows of the premises following loss or theft of the keys.

a) Any amount exceeding £250 for any one loss.

16. Legal Liability to the public – limit of liability £2,000,000 any one loss. All sums for which you are legally liable as the owner of the landlord’s contents to pay as compensation for bodily injury to any person, or loss or damage to third party property including resulting defence costs and

expenses incurred with our consent in respect of any claim against you which is the subject of cover under this Insured Event.

a) b) c) d) e) f) g) h)

Bodily injury or death to any employee or a member of your family or household; liability arising out of the transmission of any communicable disease; damage to property under your custody or control; liability arising out of any profession, occupation or business other than through private letting of the buildings; liability arising out of the ownership, possession or operation of: i) any mechanically propelled vehicle other than a private garden vehicle operated within your premises; ii) any power-operated lift; iii) any aircraft or watercraft; iv) a caravan whilst being towed; v) any dogs designated as dangerous under the Dangerous Dogs Act 1991; liability arising out of pollution; if you are entitled to cover under any other insurance; any cost or expense not agreed by us in writing.

17. Accidental damage including malicious damage and theft by a tenant to the landlord’s contents’ in addition to the Insured Events listed in paragraphs 1 to 11 of this section.

a) b) c) d)

Any amount recoverable by you from the tenancy deposit paid by the tenant as detailed on the tenancy agreement (proof of deposit payment must be submitted following a claim); damage which is insured by a policy issued to the tenant; any amount exceeding £1000 any one loss for theft by the tenant; any amount exceeding £5000 any one loss for malicious damage caused by the tenant.

24 AOD112-20170302 – SME E trade

Section 2 – Contents cover

Conditions applicable to this Section 2 – Contents cover Average Wherever a sum insured is stated to be in accordance with average, if at the time of any damage the sum insured on any item of the landlord’s contents’ is less than the total value of the property, you will be considered as being your own insurer for the difference and will bear a rateable share of the loss accordingly. Basis of claims settlement Following damage to the landlord’s contents’ we will replace the damaged landlord’s contents’ as new provided that the sum insured is at least equal to the cost of replacing all the landlord’s contents’. At our option, we may either pay the cost of replacing the lost or damaged item as new or pay the cost of repairing the item. For any claim made under this policy, our liability will: 1. not exceed the proportion that the limit of liability bears to the full cost of replacement of your landlord’s contents’ as stated in the schedule; 2. not exceed the limit of liability for landlord’s contents’ as stated in the schedule. It is your responsibility to ensure at all times the landlord’s contents’ sum insured reflects the total cost of replacement as new. We will not pay for the cost of replacing or repairing any undamaged part(s) of the landlord’s contents’ which forms part of a pair, set, suite or part of a common design. We will not reduce the limit of liability under this section following a claim provided that you agree to carry out our recommendations to prevent further damage.

Index-linking clause The sums insured under this section may be adjusted each month in accordance with the following indices: • The Consumer Durable section of the General Index of Retail Prices or its equivalent No additional premium will be charged for each monthly increase but at each renewal the premium will be calculated on the revised sums insured and will be shown on your renewal schedule.

25 AOD112-20170302 – SME E trade

Section 3 – Landlord’s legal liability

(This section only applicable if shown as being included or insured/covered on the schedule). Important Note: Any successful claim for landlord’s legal liability will be liable to the excess as stated on the schedule.

What is covered What is not covered This section includes your landlord’s legal liability under Section 3 of the Defective Premises Act 1972 or Article 5 of the Defective Premises (Northern Ireland) Order 1975 for injury to a third party or loss or damage to third party property arising from a defect in your premises including defence costs that we have agreed to pay in writing. Up to £2,000,000 unless stated otherwise on your schedule for which you are legally liable to pay as compensation for bodily injury to any person or loss or damage to third party property arising directly as a consequence of your ownership of the premises, including defence costs and expenses incurred with our consent.

a) b) c) d) e) f) g) h)

Bodily injury to employees, or is a member of your family or household; Arising out of the transmission of any communicable disease; damage to property under your custody or control; arising out of any profession, occupation or business other than through private letting of the premises; Arising out of the ownership, possession or operation of: i) any mechanically propelled vehicle other than a private garden vehicle operated within your premises; ii) any power-operated lift; iii) any aircraft or watercraft; iv) a caravan whilst being towed; v) any dogs designated as dangerous under the Dangerous Dogs Act 1991; arising out of ownership or use of any land or building not situated within the buildings as specified in the schedule; arising out of pollution; if you are entitled to cover under any other insurance.

26 AOD112-20170302 – SME E trade

Section 4 – Employers’ liability

(This section only applicable if shown as being included or insured/covered on the schedule).

What is covered What is not covered Employers’ liability compulsory insurance The cover granted by this section is in accordance with the provisions of any law enacted in the territorial limits, relating to compulsory insurance of liability to employees. If, however, we pay any sum which would not have been paid but for the provisions of this law then you will repay that sum to us. We will cover you against: 1. all sums which you will become legally liable to pay as damages; and 2 costs and expenses, in the event of bodily injury sustained by any employee which arises out of and in the course of their employment by you in the business and which is occurs in the territorial limits. The maximum we will pay to any claimant or any number of claimants for any one occurrence or all events of a series attributable to one original cause will not exceed the amount specified in the schedule and will include costs and expenses. We will cover you against liability for bodily injury assumed by you to the extent that any contract or agreement entered into by you with any principal requires provided that: a) the liability arises out of the performance by

you of a contract or agreement; b) the conduct and control of claims is vested in

us; c) the cover granted will apply only for

liability to any employee; and d) nothing in this extension will increase our

liability to pay any amount in excess of the limit of liability under this section.

We will also pay solicitors’ fees incurred with our written consent for: a) representation at any coroners’ inquest or fatal

injury inquiry for any death; and b) defending in any court of summary jurisdiction

any proceedings for any act or omission causing or relating to any event, which may be the subject of cover under this section.

1. 2. 3. 4. 5.

We will not cover you under this section against: liability for bodily injury to an employee:

a) in circumstances where compulsory

insurance or security is required by Road Traffic Act legislation;

b) for any employee undertaking the following activities: i) tree felling and lopping; ii) window cleaning, painting or

similar operations carried out from cradles and/or hoists;

iii) the provision of, erection of, dismantling of or addition to new or existing buildings.

liability arising offshore. liability arising from the manufacture, mining, processing, distribution, testing, remediation, removal, storage, disposal, sale, use or exposure to asbestos or materials or products containing asbestos in excess of £5,000,000 for any one loss. liability arising out of terrorism in excess of £5,000,000 for any one loss. fines or penalties of any kind.

27 AOD112-20170302 – SME E trade

Section 5 – Legal expenses

This section is provided as a core cover For the covers described in 1 – 4 of this section, we will pay your costs and expenses up to £100,000 for all claims related by time or original cause including the cost of appeals. Provided that your claim occurs within the territorial limits; and

a) always has reasonable prospects of success; b) is reported to us:

i) during the period of insurance; and

ii) as soon as is practicably possible after you become aware of the circumstances which could give rise to a claim under this policy; and

iii) within 60 days of rent falling into arrears where you wish to recover unpaid rent or are seeking repossession

What is covered What is not covered 1. Repossession of residential property

a) Pursuit of your legal rights to repossess your insured

property provided you: A. give the tenant the correct notices for the

repossession; and

B. will try to get repossession under: i) Schedule 2, Part 1 (grounds 1 to 8) of the

Housing Act 1988 as amended by the Housing Act 1996; or

ii) Schedule 5, Part 1 (grounds 1 to 8) of the Housing Act (Scotland) 1988; or

iii) Part 1, Section 21 of the Housing Act 1988 amended by the Housing Act 1996; or

iv) Part 2, Section 33 of the Housing Act (Scotland) 1988.

b) Pursuit of your legal rights to repossess your insured

property that you have let in accordance with the Private Tenancies (Northern Ireland) Order 2006.

28 AOD112-20170302 – SME E trade

Section 5 – Legal expenses

What is covered What is not covered 2. Recovery of rent arrears

Pursuit of your legal right to recover rent owed to you by: a) your tenant or ex-tenant of insured property;

b) guest(s) staying at your insured property which is

used as holiday accommodation.

3. Property damage, nuisance and trespass

a) An event which causes visible damage to your insured property and/or material property owned by you at your insured property.

b) A public or private nuisance or a trespass relating to your insured property.

Provided that if your insured property is used as holiday accommodation:

i) you can provide a detailed inventory of its

condition and contents which has been signed by your guest(s) and

ii) a dilapidations deposit has been paid in cash or payment has cleared in your bank account.

We will not pay for: i) damage or loss arising from a

contract between you and a third party who is not a tenant, ex-tenant; or guest staying at the insured property you have let out as holiday accommodation;

ii) the compulsory purchase of, or of, or demolition, restrictions, controls or permissions placed on land or material property by any government, local or public authority;

iii) a dispute with any party other than the party who caused the damage, nuisance or trespass;

iv) any nuisance or trespass claim under 3. b) that arises from a contract, lease, licence or tenancy agreement between you and the third party (including trespass by your ex-tenant);

v) an excess of £250 applies to b) except where you bring a claim against a person who is living at the insured property without your permission (squatters). We will ask you to pay the excess when we accept your claim.

29 AOD112-20170302 – SME E trade

Section 5 – Legal expenses

1. unless there is a conflict of interest, you alwaysagree to use the appointed adviser chosen byus in any claim;

a) to be heard by an Employment Tribunalor small claims court; and/or

b) before proceedings have been or needto be issued;

2. any dispute will be dealt with by a court, tribunal,Advisory Conciliation and Arbitration Service(ACAS) or a relevant regulatory or licensingbody in the territorial limits.

3. A claim is considered to be reported to us when we have received your fully completed claim form.

4. Holiday homes contract disputes

A dispute that arises from:

a) a written agreement which you have entered into to let outthe premises as holiday accommodation that is nototherwise covered by 2. Recovery of rent arrears or 4.Property damage, nuisance & trespass above;

b) a contract you have entered into to buy or hire goods orservices for the benefit of the premises which you have letor intend to let to guests as holiday accommodation.

We will not pay for:

i) goods or services which exceed£6,000 (including VAT) in value;

ii) loans and mortgages;

iii) an employment contract;

iv) a settlement due under aninsurance policy.

Conditions applicable to this Section 5 – Legal expenses cover

30 AOD112-20170302 – SME E trade

General conditions applicable to all sections of the policy These are the conditions of the cover and apply throughout your policy. There are additional conditions under each section of cover. If you do not comply with these conditions you may not receive payment for a claim, a claim may be reduced, or you may lose all right to cover under your policy. If you are unsure about any of these conditions or whether you need to notify us about any matter, please contact your insurance agent. 1. Cancellation – our rights

We may cancel this policy or any section by giving 30 days’ notice in writing by registered letter to you at your last known address and in this case you will be entitled to a proportionate return of premium for the unexpired term of this policy (other than in circumstances where we invoke the Fraudulent claims condition under the Claims conditions section). Reasons we may decide to cancel your policy include if: a) there is a material change in

your business;

b) there is reasonable suspicion of fraud or where there has been a deliberate or reckless misrepresentation of material facts and/or other non-disclosure;

c) you do not co-operate or supply information or documentation that we request which materially affects our ability to process this policy or our ability to defend our interests;

d) following a survey at any of your properties or sites we have required you to make risk improvements and you have not completed these within a reasonable period of time advised by us;

e) the first or renewal premium

has not been paid;

f) you or anyone acting on your behalf threatening or abusive behaviour or the use of threatening or abusive language, intimidation or bullying of our staff or suppliers; and

g) you do not exercise your duty

of care as required under General condition 4 – Maintenance and reasonable precautions contained in this policy and failing to put this right when we ask you by sending you 7 days’ written notice to your last known address.

Where a claim has been made during the current period of insurance, the full annual premium will still be payable despite cancellation of cover and we reserve the right to deduct this from any claim payment.

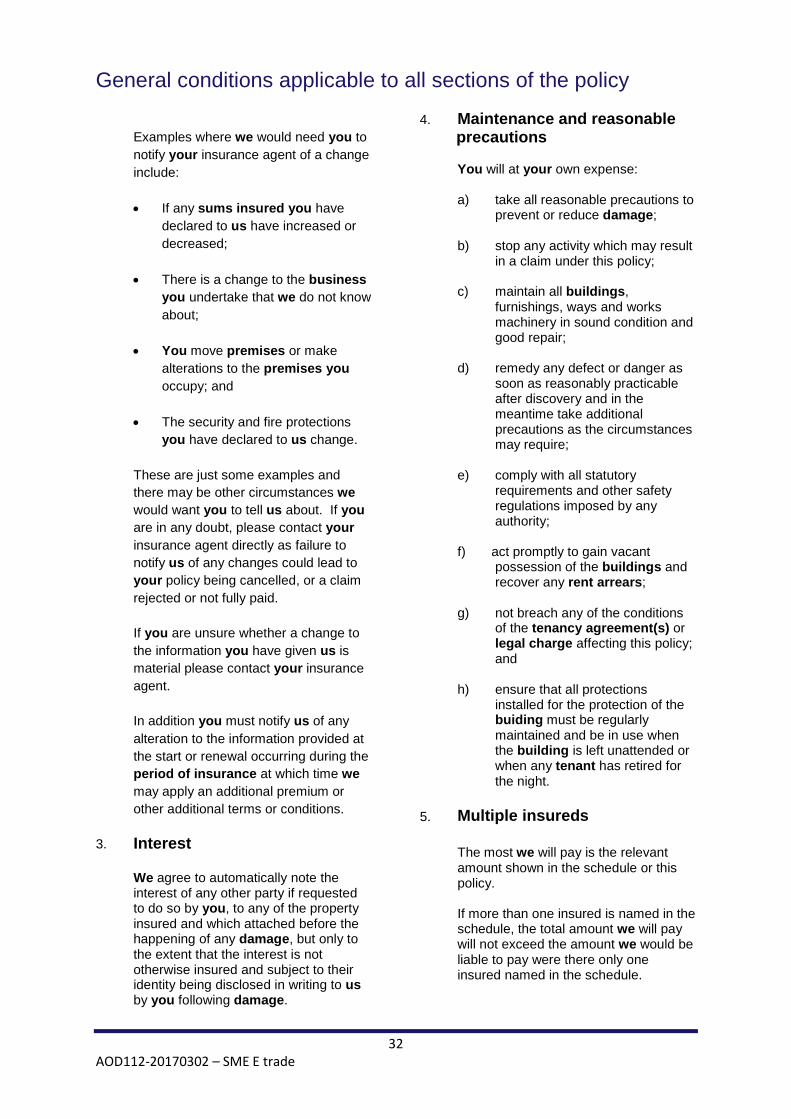

2. Change in circumstances or

alteration to the risk

If you would like to make changes to your policy please contact your insurance agent. If you are aware of any material changes to the information provided or if you become aware of any material changes you must tell your insurance agent about those changes. You must take care when answering any questions we ask by ensuring that all information provided is accurate and complete. If you need to change the information you have given us please contact your insurance agent as soon as reasonably practicable on becoming aware of that change.

31 AOD112-20170302 – SME E trade

General conditions applicable to all sections of the policy

Examples where we would need you to notify your insurance agent of a change include: • If any sums insured you have

declared to us have increased or decreased;

• There is a change to the business you undertake that we do not know about;

• You move premises or make alterations to the premises you occupy; and

• The security and fire protections

you have declared to us change. These are just some examples and there may be other circumstances we would want you to tell us about. If you are in any doubt, please contact your insurance agent directly as failure to notify us of any changes could lead to your policy being cancelled, or a claim rejected or not fully paid. If you are unsure whether a change to the information you have given us is material please contact your insurance agent. In addition you must notify us of any alteration to the information provided at the start or renewal occurring during the period of insurance at which time we may apply an additional premium or other additional terms or conditions.

3. Interest

We agree to automatically note the interest of any other party if requested to do so by you, to any of the property insured and which attached before the happening of any damage, but only to the extent that the interest is not otherwise insured and subject to their identity being disclosed in writing to us by you following damage.

4. Maintenance and reasonable precautions

You will at your own expense:

a) take all reasonable precautions to

prevent or reduce damage; b) stop any activity which may result

in a claim under this policy; c) maintain all buildings,

furnishings, ways and works machinery in sound condition and good repair;

d) remedy any defect or danger as

soon as reasonably practicable after discovery and in the meantime take additional precautions as the circumstances may require;

e) comply with all statutory

requirements and other safety regulations imposed by any authority;

f) act promptly to gain vacant

possession of the buildings and recover any rent arrears;

g) not breach any of the conditions

of the tenancy agreement(s) or legal charge affecting this policy; and

h) ensure that all protections

installed for the protection of the buiding must be regularly maintained and be in use when the building is left unattended or when any tenant has retired for the night.

5. Multiple insureds

The most we will pay is the relevant amount shown in the schedule or this policy. If more than one insured is named in the schedule, the total amount we will pay will not exceed the amount we would be liable to pay were there only one insured named in the schedule.

32 AOD112-20170302 – SME E trade

General conditions applicable to all sections of the policy

You agree that if there is more than one insured named in the schedule, the first insured listed is authorised to receive all notices and agree any changes to this policy.

6. Notice of building works

You must notify us before starting of any structural building work (for example conversions and extensions) to any buildings.

7. Remedies following a breach in

your duty of fair presentation

A non-disclosure or misrepresentation is “deliberate or reckless” if:

a) in the case of a misrepresentation,

you knew it was untrue or misleading, or did not care whether it was untrue or misleading

b) in the case of a non-disclosure, you

knew that the matter to which the non-disclosure related was material to us, or did not care whether or not it was material to us.

The burden will be on us to prove all matters set out in this condition.

Deliberate or reckless breach of the duty of fair presentation If you deliberately or recklessly breach your duty of fair presentation of the risk this policy will be avoided from its start date and no premium will be returned. Breach of the duty of fair presentation which is neither deliberate nor reckless If your breach of the duty of fair presentation of the risk was neither deliberate nor reckless, and had we known the information which led to the breach from the start of the policy or at the time of its renewal, we:

a) would not have entered into the

contract:

we will:

i) charge an additional premium

calculated from the start of the period of insurance (the amount charged will be proportionate with the increase in risk);

ii) apply additional terms from the date we discover the breach;

Provided you have paid the additional premium we requested and agreed in writing to the additional terms, we will also:

a. pay any valid claims notified to us

before the date of the discovery of the breach, including any valid claim which led to the discovery of the breach;

b. continue to cover you on the revised basis for the remaining period of insurance, but we may not continue insuring you once the policy reaches its renewal date.

However there may be certain circumstances where we will cancel the policy from the start date. These circumstances will include where the breach means we or our parent company will suffer reputational harm in either the insurance market, the media or amongst our customers or trading partners. If we do cancel your policy from the start date because of the above all premiums paid will be returned.

b) would have applied different terms we will apply those different terms from the date of the discovery. Any claims already made will not be affected by our discovery; c) would have charged a higher premium we will charge an additional premium calculated from the start of the policy. Any claims already made will not be affected by our discovery;

33 AOD112-20170302 – SME E trade

General conditions applicable to all sections of the policy d) would have applied different terms and charged a higher premium we will charge the additional premium (calculated from the start of the policy) and apply additional terms from the date of discovery. Any claims already made will not be affected by our discovery. We or your insurance agent will write to you if we intend to apply one of the above proportional remedies. 8. Statutory conditions and

regulations a) If the property is let, you must