LABUAN IBFC · PDF fileWhere is Labuan? Off the coast of Sabah, Malaysia Governed by Malaysia...

48

LABUAN IBFC: ASIA’S PREFERRED CAPTIVE DOMICILE 19 MAY 2016 TOKYO MARRIOTT HOTEL, JAPAN

Transcript of LABUAN IBFC · PDF fileWhere is Labuan? Off the coast of Sabah, Malaysia Governed by Malaysia...

LABUAN IBFC: ASIA’S PREFERRED CAPTIVE DOMICILE

19 MAY 2016 TOKYO MARRIOTT HOTEL, JAPAN

WELCOME REMARKS

Annie Undikai Managing Director, Brighton Management Limited

AN INTRODUCTION TO LABUAN INTERNATIONAL BUSINESS

AND FINANCIAL CENTRE

Farah Jaafar-Crossby Director, Market Intelligence and Strategic Communications

ASIA PACIFIC’S

MIDSHORE INTERNATIONAL BUSINESS

AND FINANCIAL CENTRE

Where is Labuan?

Off the coast of Sabah, Malaysia Governed by Malaysia A Duty free island 100,000 pop. well educated English Speaking Same time zone with major Asian cities One of best wreck diving spots in the region

5

What is Labuan IBFC?

• An International Business and Financial Centre

• A tax-efficient jurisdiction to facilitate cross border businesses,

trading, investments through financial services and legal structures

• Well-balanced : Legal and Regulatory Framework vs. Ease of Doing Business

Our Vision To be Asia Pacific’s leading midshore international business and financial centre

Striking an ideal balance between client confidentiality and international best standards

7

Rise of a ‘Midshore’ Jurisdiction

Global cross-border financial transactions, investments and fund flows are facing mounting international scrutiny. The ‘Midshore’ jurisdiction is emerging as a new breed of financial centre, combining the best attributes of both onshore and offshore.

Labuan IBFC : Asia’s

Midshore Jurisdiction

“Connecting Asia’s

Economies”

So what is Midshore? A jurisdiction with a business-friendly, efficient tax system yet has a robust regulatory and supervisory framework akin to an onshore financial centre, stands out as a midshore jurisdiction.

8

Striking the Midshore Balance

Confidentiality

• Separate laws to Malaysian “onshore” environment, except in AMLA/CTF

• No disclosure of beneficiaries

• Registration of trusts and private funds not mandatory

• No “fishing expeditions” allowed

• Audits only mandatory for licensed entities

Compliance with International Standards

• “White Listed” by OECD and EU

• Committed to Base Erosion Profit Shifting initiative, Common Reporting Standard and FATCA

• Wide Tax Treaty network

• Common law

• Member of international agencies in respect to Anti-Money Laundering activity

• Robust supervisory stance

9

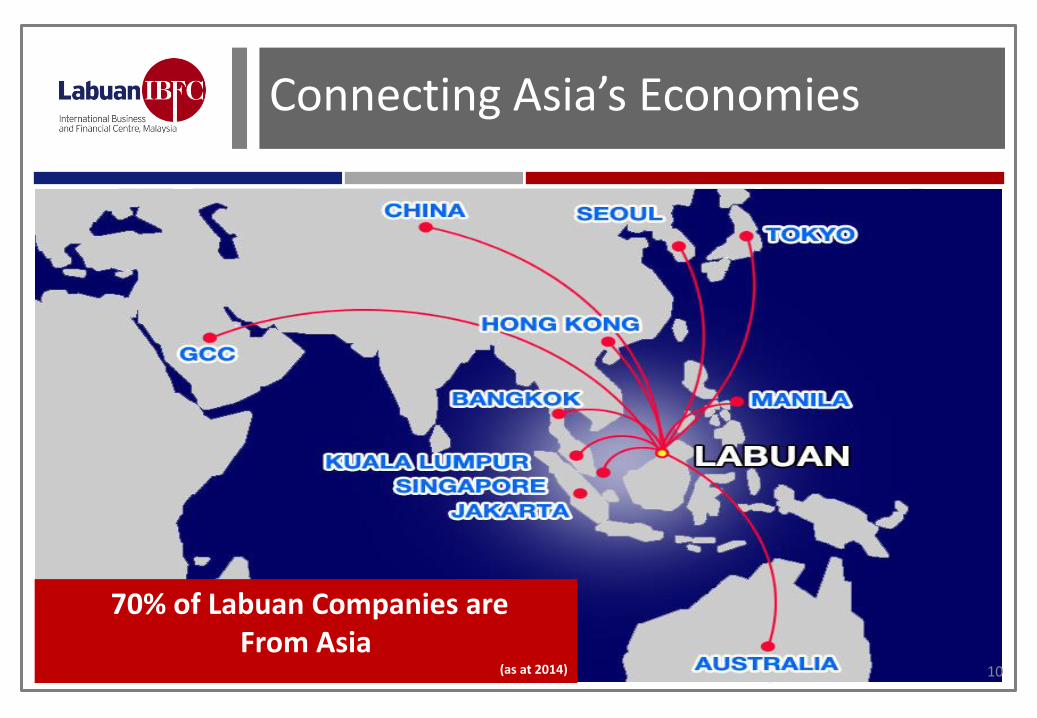

Connecting Asia’s Economies

70% of Labuan Companies are From Asia

(as at 2014) 10

Internationally Recognised

Group of International Finance Centre Supervisors (GIFCS) Member since 1999

International Organisation of Securities Commissions (IOSCO) Member since 2003

Group of International Insurance Centre Supervisors (GIICS) Member since 1999

International Association of Insurance Supervisors (IAIS) Member since 1998

Islamic Financial Services Board (IFSB) Member since 1998

Asia/Pacific Group on Money Laundering (APG) Member since 2000

Labuan IBFC Adheres to OECD’s International Standards and Best Practices in Tax Transparency

International Islamic Financial Market (IIFM) Member since 2002

11

Comprehensive Legislation

Labuan Financial Services and Securities Act 2010

Labuan Islamic Financial Services and Securities Act 2010

Labuan Foundations Act 2010

Labuan Limited Partnerships and Limited Liability Partnerships Act 2010

Labuan Business Activity Tax Act 1990

Labuan Financial Services Authority Act 1996

Labuan Trusts Act 1996

Labuan Companies Act 1990

12

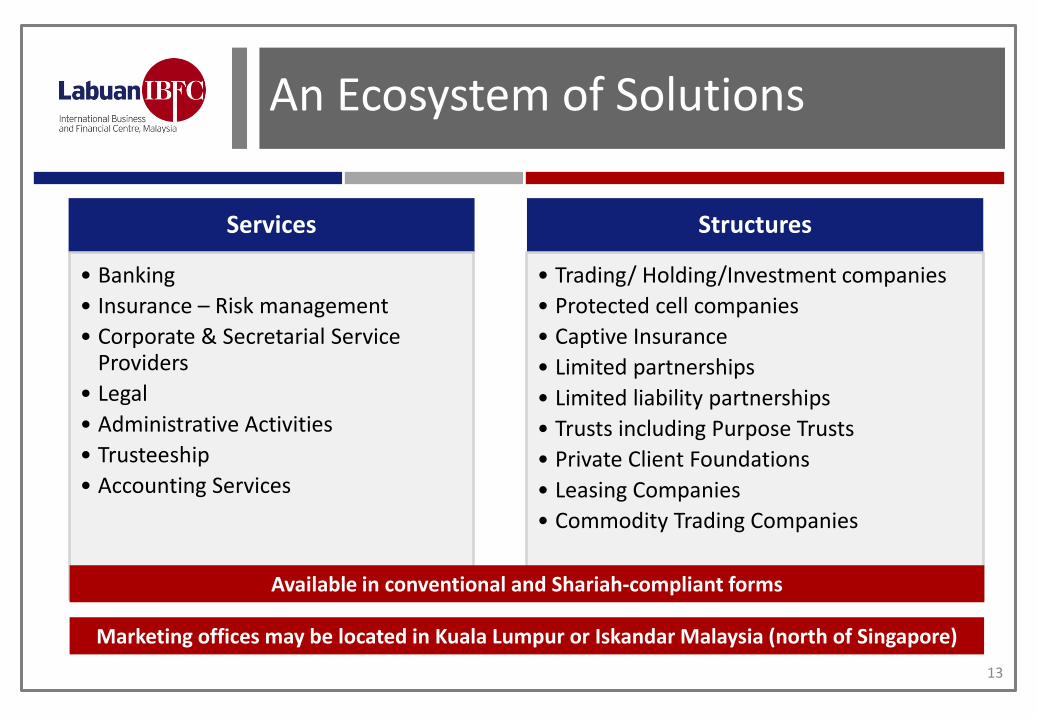

An Ecosystem of Solutions

Services

• Banking

• Insurance – Risk management

• Corporate & Secretarial Service Providers

• Legal

• Administrative Activities

• Trusteeship

• Accounting Services

Structures

• Trading/ Holding/Investment companies

• Protected cell companies

• Captive Insurance

• Limited partnerships

• Limited liability partnerships

• Trusts including Purpose Trusts

• Private Client Foundations

• Leasing Companies

• Commodity Trading Companies

Available in conventional and Shariah-compliant forms

Marketing offices may be located in Kuala Lumpur or Iskandar Malaysia (north of Singapore)

13

Business Activities

Source: Statistics from Labuan FSA’s Annual Report 2014

Banking (57)

•Wholesale banking

•Investment banking

•Loans/deposit

•Financial guarantees

•Trade finance

Leasing (359)

Companies (11,630)

• Investment holding

• Trading

•Life/general

•Broking

•Captives

•Re-insurance

Insurance (209)

•Company incorporation

•Company administration

•Corporate secretarial

•Trustee services

Trust Cos. (39)

•Aviation

•Shipping

•Heavy machinery

Wealth Management

(more than 300)

Commodity Trading

(39)

•Business succession

•Estate management

•Legacy planning

•Oil and gas

•Agriculture

•Minerals

14

A Tax Efficient Regime

No indirect tax

No capital gains tax

No withholding tax

No inheritance or wealth tax

No stamp duty

Access to a wide network of DTAs as part of Malaysia

No foreign exchange control

No foreign ownership limitation 15

Labuan Tax

Flexibility

Labuan Tax Act 1990

0%

Investment Holding

Non Trading

Labuan Tax Act 1990

3%

Labuan Tax Act 1990

RM 20,000

Malaysia Income Tax Act 1967

24%

Irrevocable Election

0% foreign source income

Trading Income

16

Double Taxation Agreements (80 Ratified)

ALBANIA ARGENTINA AUSTRALIA AUSTRIA BAHRAIN BANGLADESH BELGIUM

CROATIA

IRAN IRELAND ITALY JAPAN JORDAN KAZAKHSTAN KOREA KUWAIT KYRGYZ LAOS LEBANON LUXEMBOURG

MALTA MAURITIUS MONGOLIA MOROCCO MYANMAR NAMIBIA NETHERLANDS

POLAND QATAR ROMANIA RUSSIA

BOSNIA HERZEGOVINA

BRUNEI CANADA CHILE CHINA

DENMARK EGYPT FIJI FINLAND FRANCE GERMANY HONG KONG HUNGARY INDIA INDONESIA CZECH REPUBLIC

NEW ZEALAND

NORWAY PAKISTAN PAPUA NEW GUINEA

PHILIPPINES

SAN MARINO

SAUDI ARABIA

SEYCHELLES SINGAPORE SOUTH AFRICA

SPAIN SRI LANKA SUDAN

SWEDEN SWITZERLAND SYRIA THAILAND TURKEY TURKMENISTAN UAE UK USA UZBEKISTAN VENEZUELA VIETNAM 17

Why Labuan IBFC?

• Developed legal framework providing a wide array of products and services

• Tax efficiency and flexibility; e.g. Labuan or onshore tax option

• Malaysia is ranked 18th/ 189 - World Bank's Ease of Doing Business Report 2015

• Cost effective, One third the cost of Singapore/Hong Kong

• Professional expertise and services

• Re domiciliation to or from Labuan IBFC of companies and structures allowed

• Ability to create economic substance on Labuan island or Malaysia, onshore

• Same time zone as all key Asian cities, including Tokyo, Singapore, Hong Kong

• Labuan Companies accepted as a listing vehicle on: National Stock Exchange of Australia, Hong Kong Stock Exchange and Singapore Stock Exchange

18

Why Not?

19

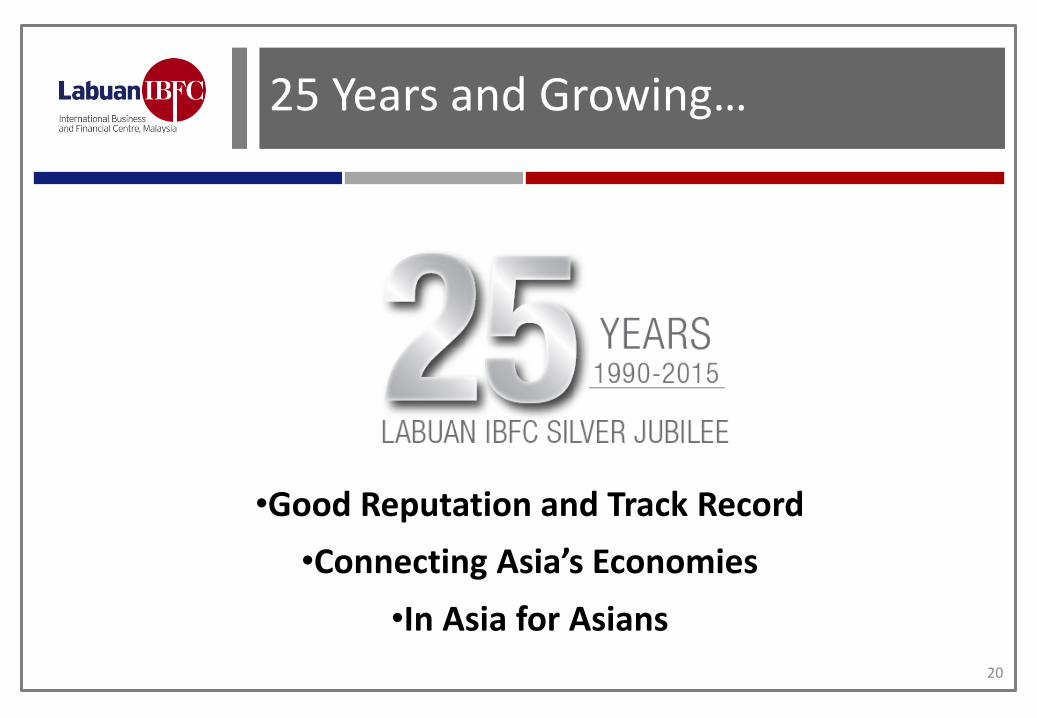

25 Years and Growing…

•Good Reputation and Track Record

•Connecting Asia’s Economies

•In Asia for Asians

20

LABUAN IBFC: ASIA’S PREFERRED CAPTIVE DOMICILE

Anthony Egerton Principal Officer, Huntington Underwriting Limited

Regulatory Definition

“an insurance or reinsurance entity created and owned, directly or

indirectly, by one or more industrial, commercial or financial entities, the purpose of which is to provide insurance or reinsurance cover for

risks of the entity or entities to which it belongs, or for entities connected to those entities and only a small part if any of its risk

exposure is related to providing insurance or reinsurance to other parties”

Issues Paper on the Regulation and Supervision of Captive Insurance Companies International Association of Insurance Supervisors (“IAIS”) - October 2006

22

What is a Captive Insurance Company?

• Essentially, a wholly-owned insurance company that insures the assets, liabilities and other risks of its parent company

• Usually located in a jurisdiction where taxation, solvency and reporting requirements are less onerous

• Often managed by specialist companies that act as accountants and administrators

• However, much of the decision-making around • how the risk is retained by the subsidiary company and

• how much is transferred to the conventional insurance market

is undertaken by the parent company

• 75% of the world’s Fortune 500 companies are parent owners of captive insurance companies

• Total captive premium income exceeds US$14 billion with more than 5,000 captives established worldwide

23

Why Labuan IBFC for Risk Management?

• Robust and internationally recognised regulatory framework

• Facilitative and Business-friendly legislation

• Wide choice of risk management entities

• Tax efficiency, access to more than 70 double taxation agreements

• Same time zone with major Asian cities

• Access to Malaysia’s strong direct insurance market

• Preferential treatment due to domestic insurance tiering

• Cost efficiency, provides for substance creation

24

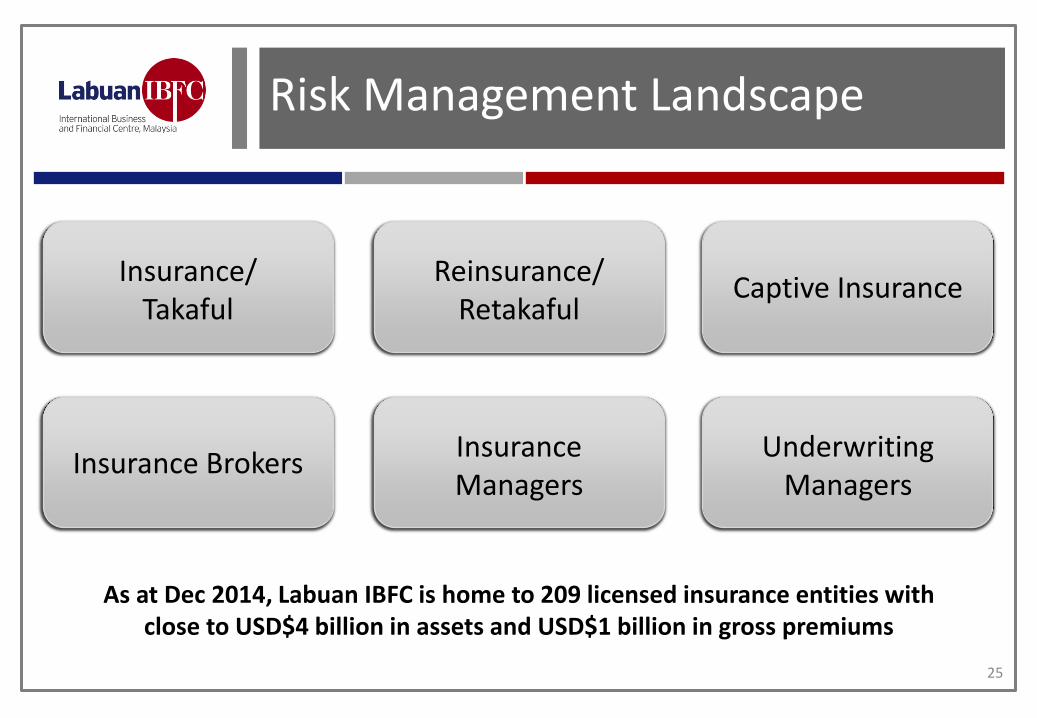

Risk Management Landscape

Insurance/ Takaful

Reinsurance/ Retakaful

Captive Insurance

Insurance Brokers Insurance Managers

Underwriting Managers

As at Dec 2014, Labuan IBFC is home to 209 licensed insurance entities with close to USD$4 billion in assets and USD$1 billion in gross premiums

25

Cost Efficient

• RM300,000

Capitalisation of Captive Company

• Processing fee: RM1,000 (one off)

• Annual licence fee: RM10,000 per annum

Regulatory Fees

• 3% of net audited profits or RM20,000 upon election, alternatively 25% for a Labuan Company electing to be taxed under the Malaysian Income Tax Act 1967

Tax

RM1: 28 Yen as at 26 April 2016 26

Our Captives

As at December 2014, there are 40 captives in Labuan IBFC

Plants & Facilities

Warisan Captive Incorporated (M)

Tune Insurance (Labuan) Ltd (M)

QSR Captive Insurance Limited (M)

Genting (Labuan) Limited (M)

Delima Insurance (Labuan) Ltd

Energas Insurance (L) Limited (M)

Sime Darby Insurance Pte. Ltd. (M)

Sunway Captive Insurance Ltd. (M)

Employees’ Benefits & Food Outlets

International & Local Properties

Aviation, Hull, Liabilities & Travel

Aviation, Hull, Liabilities & Travel

Refineries & Facilities; Onshore, Offshore

International & Local Properties

International & Local Properties

Something Group Japan

27

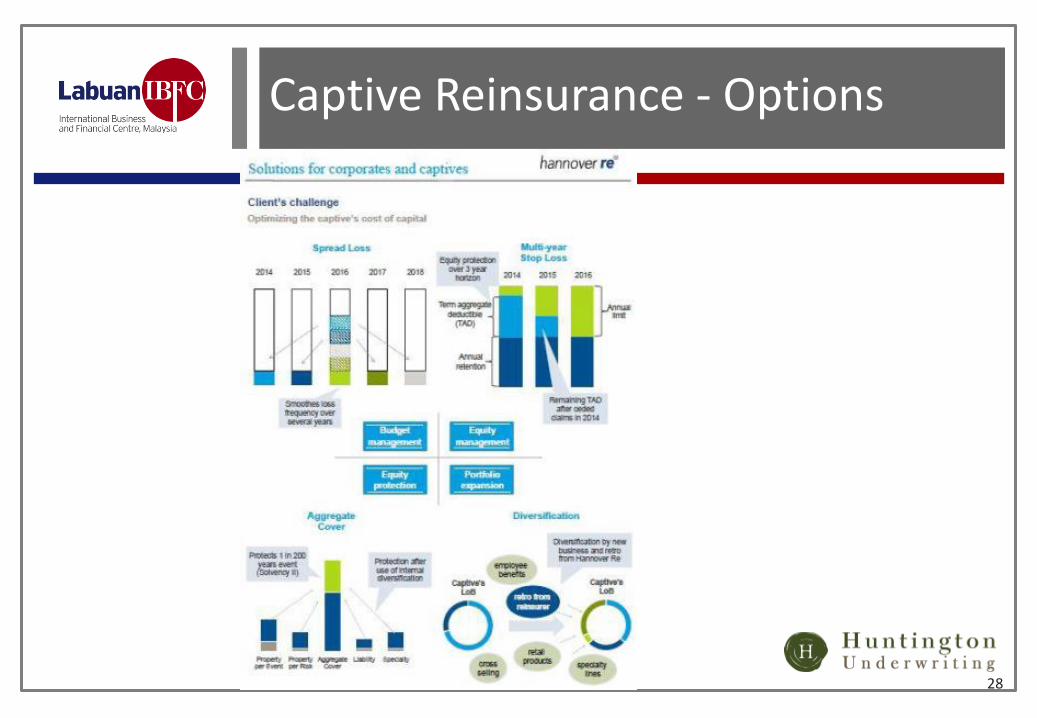

Captive Reinsurance - Options

28

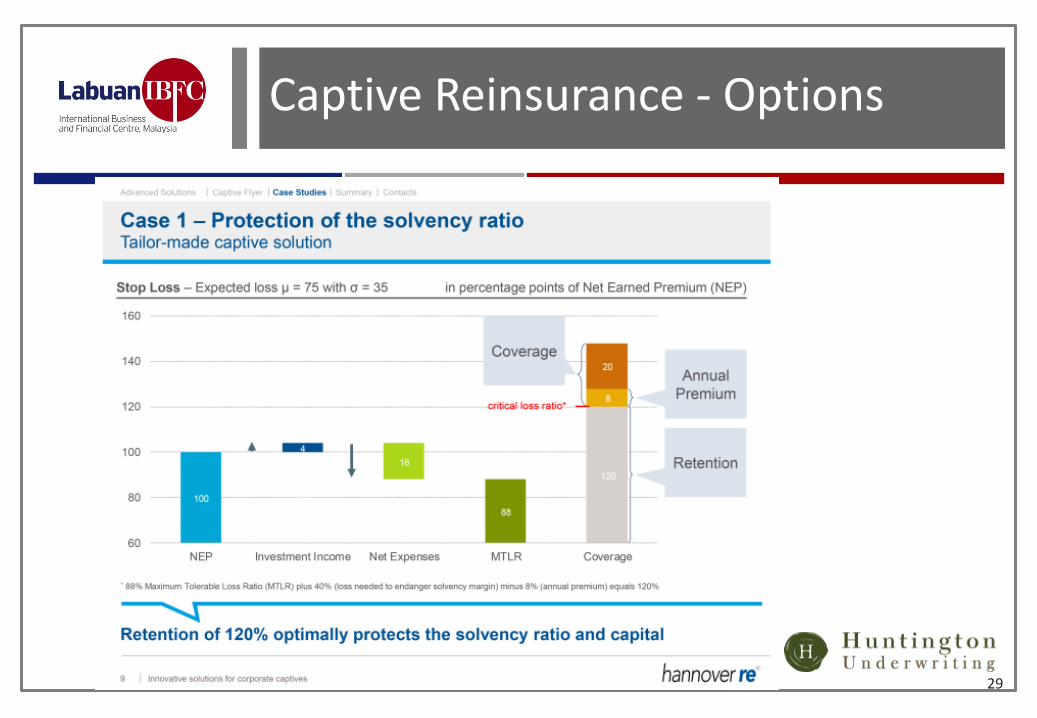

Captive Reinsurance - Options

29

Captive Reinsurance - Options

30

Captive Reinsurance - Options

31

Selecting a Jurisdiction

Robust & Efficient Regulatory Environment

“Substance” Creation

Access to double taxation agreements

Cost Efficient

CHOSEN JURISDICTION 32

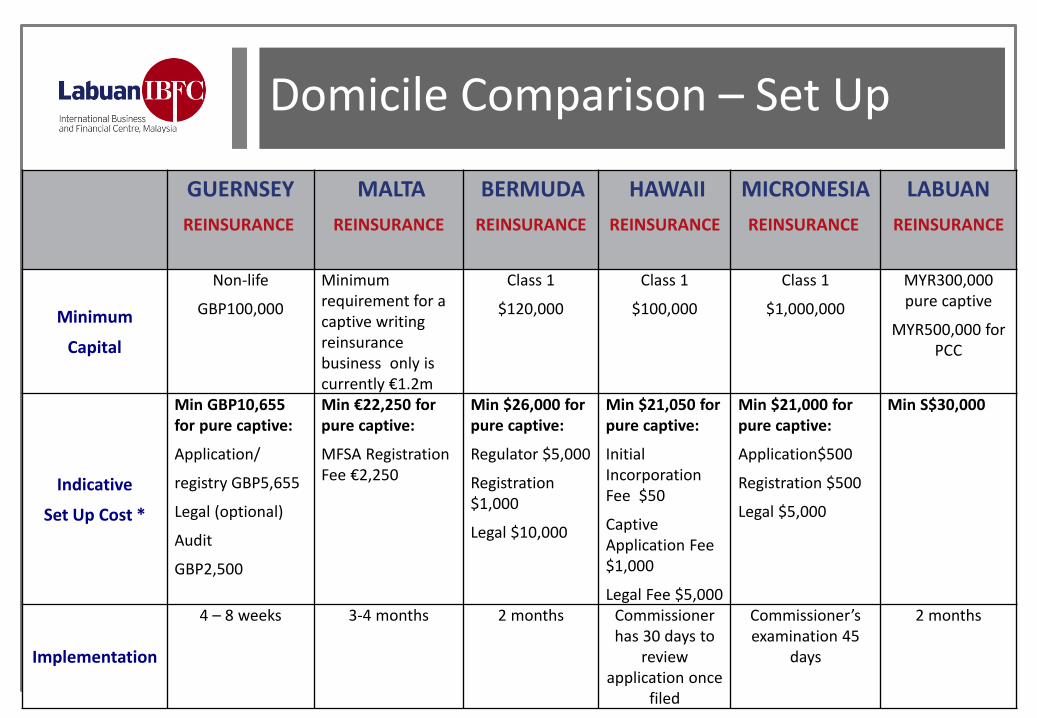

Domicile Comparison – Set Up

33

GUERNSEY

REINSURANCE

MALTA

REINSURANCE

BERMUDA

REINSURANCE

HAWAII

REINSURANCE

MICRONESIA

REINSURANCE

LABUAN

REINSURANCE

Minimum

Capital

Non-life

GBP100,000

Minimum requirement for a captive writing reinsurance business only is currently €1.2m

Class 1

$120,000

Class 1

$100,000

Class 1

$1,000,000

MYR300,000 pure captive

MYR500,000 for PCC

Indicative

Set Up Cost *

Min GBP10,655 for pure captive:

Application/

registry GBP5,655

Legal (optional)

Audit

GBP2,500

Min €22,250 for pure captive:

MFSA Registration Fee €2,250

Min $26,000 for pure captive:

Regulator $5,000

Registration $1,000

Legal $10,000

Min $21,050 for pure captive:

Initial Incorporation Fee $50

Captive Application Fee $1,000

Legal Fee $5,000

Min $21,000 for pure captive:

Application$500

Registration $500

Legal $5,000

Min S$30,000

Implementation

4 – 8 weeks 3-4 months 2 months Commissioner has 30 days to

review application once

filed

Commissioner’s examination 45

days

2 months

Domicile Comparison - Solvency

34

GUERNSEY

REINSURANCE

MALTA

REINSURANCE

BERMUDA

REINSURANCE

HAWAII

REINSURANCE

MICRONESIA

REINSURANCE

LABUAN

REINSURANCE

Solvency

Margin

OSCA (Own Solvency Capital Assessment), a risk based capital assessment;

Subject to minimum solvency capital requirement (MCR) currently 18% of premium up to GBP5m plus 16% of premium excess of GBP5m

Currently based on Premium and Losses. (Solvency I (EU) requirement). If short-tail risk programme such as PD/BI, Marine, Trade Credit then 27% of premium written would apply (50% buffer over 18% min). Further credit/discount available for outwards reinsurance placement.

Class 1 - 20% of net premium up to $6M.

10% of net premium over $6M

Net Worth to Loss Reserves:

Class 1 - 10% of loss reserves

No specific guidelines. Based on captive’s business plan.

Minimum margin of solvency is the balance of total amount of assets less total amount of liabilities which should be greater of :

(1) $100,000

(2) 20% of net premium income; or

(3) 5% of sum of unexpired risk reserve and loss reserves.

20% of prior year net written premium

Domicile Comparison – Running Costs

GUERNSEY

REINSURANCE

MALTA

REINSURANCE

BERMUDA

REINSURANCE

HAWAII

REINSURANCE

MICRONESIA

REINSURANCE

LABUAN

REINSURANCE

Indicative Annual Cost *

Min. GBP65k for pure captive:

Regulator (GBP5,655)

Director (GBP5,000)

Audit (GBP5,000)

Min. €114,500:

Regulator (€6,500) - sliding scale based on premium income

Non Exec Director x2 (€18,000) - negotiable

Audit (€15,000)

Min $$87,000:

Regulator ($5,000)

Company secretarial

($7,000)

Audit ($20,000)

Min $95,500 for pure captive:

License & Regulatory Fees $500

Audit/Tax Return $20,000

Legal $5,000

Actuary $10,000

Min $95,500 for pure captive:

License $500

Audit/Tax Return $20,000

Legal $5,000

Actuary $10,000

Min S$75,000

35

Cost Efficiency

36

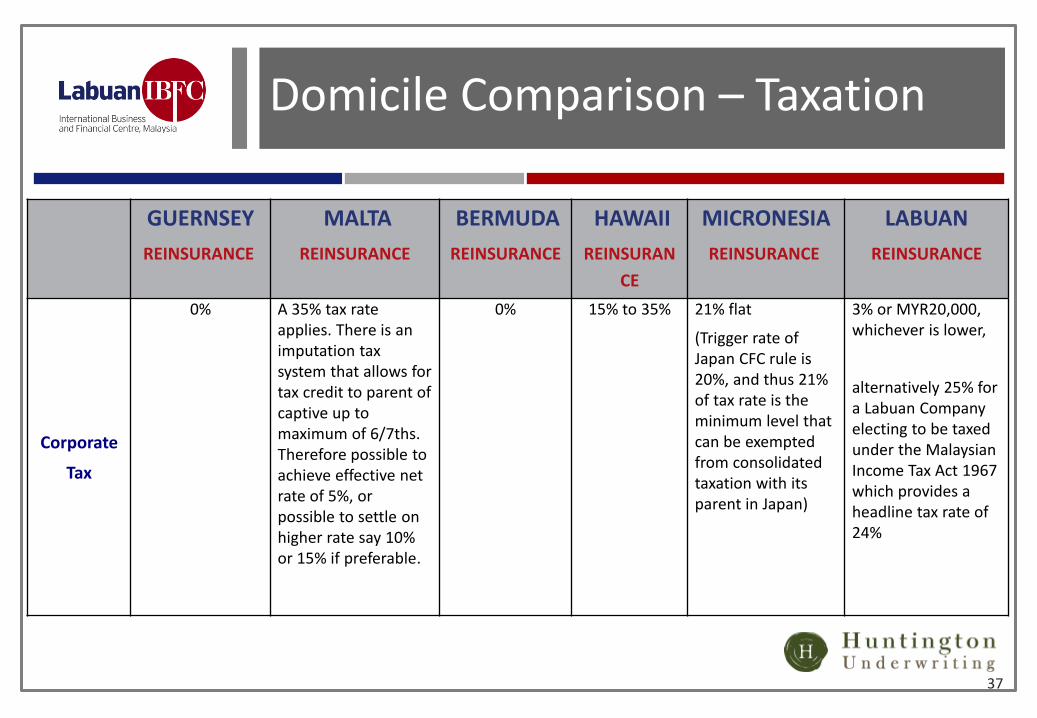

Domicile Comparison – Taxation

GUERNSEY

REINSURANCE

MALTA

REINSURANCE

BERMUDA

REINSURANCE

HAWAII

REINSURAN

CE

MICRONESIA

REINSURANCE

LABUAN

REINSURANCE

Corporate

Tax

0% A 35% tax rate applies. There is an imputation tax system that allows for tax credit to parent of captive up to maximum of 6/7ths. Therefore possible to achieve effective net rate of 5%, or possible to settle on higher rate say 10% or 15% if preferable.

0% 15% to 35% 21% flat

(Trigger rate of Japan CFC rule is 20%, and thus 21% of tax rate is the minimum level that can be exempted from consolidated taxation with its parent in Japan)

3% or MYR20,000, whichever is lower,

alternatively 25% for a Labuan Company electing to be taxed under the Malaysian Income Tax Act 1967 which provides a headline tax rate of 24%

37

'Substance over Form' Principle

"The effect is to ascertain the tax consequences of a transaction or arrangement by determining the economic substance of such transaction or arrangement rather than its strict legal form."

"In 1961, it was proposed that a general provision in relation to substance in the National General Administration Law be enacted, but the proposal had (sic) never been accepted. As a result, the Japanese tax statues (sic) do not provide for a general provision of taxation on the basis of the substance of a transaction. However, in practice, it is acknowledged that the "substance over form approach" shall be applied as a general principle…"

"What is clear from the Japanese case law and practice is that the Japanese tax authorities will challenge transactions or structures based on the substance grounds. Taxpayers should ensure that there are sound commercial reasons with proper documentation for undertaking a particular transaction or using a particular structure."

Source: PricewaterhouseCoopers - Asia Pacific Tax Notes 2010

38

Meeting 'Substance' Requirements

• Hold Annual General Shareholders' and Board of Directors' meetings in the domicile

• Perform Directors’ duties in the domicile

• Prepare and maintain accounting books and records in the domicile

• Participate in the management as a resident of the domicile

• Et cetera

Source: Tokyo Kyodo Accounting Office

www.tkao.com

39

Base Erosion & Profit Shifting

• G20 leaders committed in November 2015 to implementing Base Erosion and Profit Shifting (BEPS) framework

• OECD initiative has since been expanded to a further 80 countries

• Aims to close gaps that allow corporate profits to ‘disappear’ or be artificially shifted to low- or no-tax environments

• Captives and international insurance and reinsurance arrangements not only been caught up in BEPS, they have been singled out

• First meeting of Committee on Fiscal Affairs - Kyoto, Japan 30 June & 1 July 2016

Source: Commercial Risk Europe – Friday 22 April 2016

http://www.oecd.org/tax/beps.htm

40

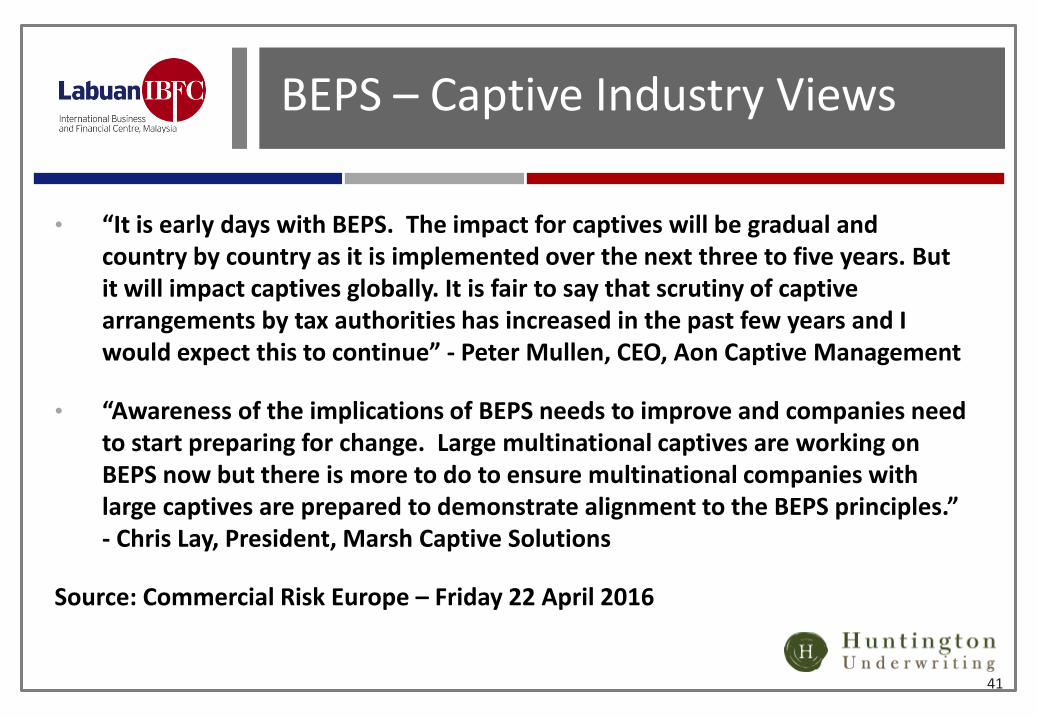

BEPS – Captive Industry Views

• “It is early days with BEPS. The impact for captives will be gradual and country by country as it is implemented over the next three to five years. But it will impact captives globally. It is fair to say that scrutiny of captive arrangements by tax authorities has increased in the past few years and I would expect this to continue” - Peter Mullen, CEO, Aon Captive Management

• “Awareness of the implications of BEPS needs to improve and companies need to start preparing for change. Large multinational captives are working on BEPS now but there is more to do to ensure multinational companies with large captives are prepared to demonstrate alignment to the BEPS principles.” - Chris Lay, President, Marsh Captive Solutions

Source: Commercial Risk Europe – Friday 22 April 2016

41

BEPS – Captive Industry Impact

• “There are four aspects of BEPS that are particularly relevant for captives;-

• the need to justify the commercial rationale for transactions;

• the substance of the captive, its governance and economic activity;

• transfer pricing rationale and premium allocation; and

• the transparency and reporting of information to tax authorities.”

• “While much of the work will focus on documentation and being able to demonstrate the rationale and substance of captive arrangements, many companies may need to make operational and governance changes.”

- Chris Lay, President, Marsh Captive Solutions

Source: Commercial Risk Europe – Friday 22 April 2016

42

Labuan IBFC as a Domicile

• Cost Efficient and easy for “substance” to be established

• Enjoys access to Malaysia’s more than 70 DTAs

• Offers a comprehensive range of sophisticated structures, both conventional and shariah-compliant

• “Abstract Labuan” where investors/companies can set-up a Labuan company and conduct legitimate offshore business anywhere in the world

• Has a business friendly regulatory environment with a modern and well-developed infrastructure

43

Labuan IBFC as an Insurance Centre

As at December 2014

Total No. of Insurance Licence 209

No. of Captives (Including PCCs) 40

No. of Underwriting Managers 21

No. of Insurance Managers 3

Total Assets (USD Mil) 3,923.2

Total Gross Premiums (USD Mil) 1,429.5

44

Why Labuan IBFC?

Flexibility through co-location Attractive alternative for Labuan Insurance and Takaful licensees to establish offices in Peninsular Malaysia to leverage of infrastructure, facilities and human capital

Competitive advantage With potential growth in Asian multinationals, increased awareness and better risk management, more companies are ‘THINKING CAPTIVE’

Leading jurisdiction in Islamic Finance Introduction of Shariah-compliant captives to take advantage of the global retakaful market and world’s first comprehensive omnibus legislation governing Islamic Finance products and services

Cost-effective approach Low operational costs in the jurisdiction without sacrificing quality with access to expertise in the insurance industry and world class infrastructure

45

DIALOGUE SESSION

Annie Undikai Managing Director, Brighton Management Limited

Farah Jaafar-Crossby

Director, Market Intelligence and Strategic Communications, Labuan IBFC

Anthony Egerton

Principal Officer, Huntington Underwriting Limited

Disclaimer

This presentation should not be regarded as offering a complete explanation of the matters referred to and is subject to changes in law. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Labuan IBFC cannot accept any responsibility for loss occasional to any person acting or refraining from action as a result of any material in this presentation. The republication, reproduction or commercial use of any part of this presentation in any manner whatsoever, including electronically, without the prior written permission from Labuan IBFC Inc. is strictly prohibited.

LABUAN IBFC INC SDN BHD IS THE OFFICIAL AGENCY ESTABLISHED BY GOVERNMENT OF MALAYSIA TO POSITION LABUAN IBFC AS THE PREFERRED INTERNATIONAL BUSINESS AND FINANCIAL CENTRE IN ASIA PACIFIC

Thank You