L & T Resurgent India Corporate Band Fund

20

L&T Resurgent India Corporate Bond Fund (An open-ended income scheme) NFO opens: 22 nd January 2015 NFO closes: 30 th January 2015 For product labeling please refer to slide 19

-

Upload

girish-kodashettar -

Category

Economy & Finance

-

view

82 -

download

2

Transcript of L & T Resurgent India Corporate Band Fund

L&T Resurgent India Corporate Bond Fund

(An open-ended income scheme)

NFO opens: 22nd January 2015

NFO closes: 30th January 2015

For product labeling please refer to slide 19

Indian economy is on the verge of a turnaround…

Indian economy has seen a significant slowdown since 2010-11 on account of slowing

global growth, lack of domestic policy action and inflationary pressure

However, the new stable government’s thrust on policy actions & focus on

infrastructure & allied sectors is expected to drive the economic recovery going forward

RBI’s focus on maintaining a stable monetary policy to control retail inflation coupled

with benign commodity prices have led to significant improvement in country’s macro

fundamentals

With inflation largely under control, we are now likely to see RBI’s focus shifting

towards boosting sustainable growth while still keeping inflation under check

In a global context, we believe India is uniquely positioned to enjoy favorable

growth-inflation dynamics

2

How this could influence fixed income market?

2014 2015 2016 2017 2018

Macro outlook

• Falling inflation, gradual pick-up in economic growth • Credit growth to pick-up only gradually due to slow turnaround in capex cycle and banks’ balance sheet issues

• Growth acceleration likely from 2016 • Credit growth also likely to gain momentum with rising economic activity

Interest Rates

• Expect RBI to cut rates by 50-100bps over the next 8-12 months. • As a result 10 yr G-Sec could move to 7.0% - 7.50% range

• Expect inflation to stabilize in 5 to 6% range • With a real rate of 1.5-2.0% indicated by RBI, limited room for further policy easing in 2016

Credit

• Credit environment likely to improve gradually with economic recovery • However, one needs to be cautious given high leverage & lack of cash flow visibility in certain sectors

• Better visibility on business with sustained economic recovery leading to balance sheet deleveraging & improving cash flow trajectory

• Bias towards credit upgrades likely

3 The aforesaid views are of L&T Investment Management . Before relying on these views please consult your financial

adviser.

So for investors with medium term investment

horizon (~ 3 years), what are the fixed income

investment options available to capitalize on the

prevailing conducive environment?

4

12.50%

9.20%8.12%

0%2%4%6%8%

10%12%14%

Year 1 Year 2 Year 3

Cumulative annualised returnat the end of...

Option 1: Dynamic Bond Funds

Assume a dynamic bond fund investing predominantly in government securities

and highly rated corporate bonds and typically maintaining high duration in the

softening rate environment and then moving towards more conservative

positioning

While these funds could deliver strong near term performance, over a 3 year period cumulative performance could taper sharply on account of lower yield

accrual in 2nd / 3rd year and lack of further capital appreciation

Possible scenario

Fund type Current gross yield

Mod Duration in falling interest rate environment

Mod Duration in rising / flat interest rate environment

Dynamic Bond Fund 8.50% 6 2

The above calculations are based on various assumptions and actual performance may vary depending on the market conditions and actual change in the shape of the yield curve. This is for illustration purpose only. Please consult your financial advisor before taking any investment decisions. Annualized return shown above is assuming a total expense ratio (TER) of 150 bps. 5

-1.2%

-1.0%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0 1 2 3

Yie

ld m

ove

me

nt

Year

Interest rate movement

Option 2: Accrual / high yielding funds

Assume an accrual fund investing predominantly in higher yielding corporate bonds

including those in sensitive sectors like real estate and loan against shares and

typically maintaining modified duration of 2-3 years

Higher yield accruals could help these funds outperform in a flat / rising interest rate environment but due to their low duration they may be unable to capitalize

adequately in a falling rate environment

Possible scenario

Fund type Current gross yield

Mod Duration in falling interest rate environment

Mod Duration in rising / flat interest rate environment

Accrual Fund 10.25% 2.5 2.5

-1.2%

-1.0%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0 1 2 3

Yie

ld m

ove

me

nt

Year

Interest rate movement

10.75%9.24% 8.74%

0%2%4%6%8%

10%12%

Year 1 Year 2 Year 3

Cumulative annualised returnat the end of...

6

The above calculations are based on various assumptions and actual performance may vary depending on the market conditions and actual change in the shape of the yield curve. This is for illustration purpose only. Please consult your financial advisor before taking any investment decisions. Annualized return shown above is assuming a total expense ratio (TER) of 150 bps.

Option 3: Invest in long duration bond fund in falling rate

environment and switch to accrual fund when rates stabilize

Assume an investment strategy where investor invests in a long duration fund in a falling interest

rate environment and then switches to accrual / high yielding fund once interest rates stabilize

Likely to be the most inefficient strategy - Investments held for < 3 years attract short term capital gains tax impacting the return. Also timing the switch may be difficult.

Possible scenario

Fund type Current gross yield

Mod Duration in falling interest rate

environment

Fund Type Gross yield at the time of

switch

Mod Duration in rising / flat interest rate

environment

Duration Fund 8.50% 6.0 Accrual Fund 9.25% 2.5

-1.2%

-1.0%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0 1 2 3

Yiel

d m

ove

men

t

Year

Interest rate movement

The above calculations are based on various assumptions and actual performance may vary depending on the market conditions and actual change in the shape of the yield curve. This is for illustration purpose only. Please consult your financial advisor before taking any investment decisions. Annualized return shown above is assuming a total expense ratio (TER) of 150 bps. Tax paid at the end of 1st year assumed to be 30.90%. Short term capital gains tax on investments in accrual fund not considered assuming investor will continue to stay invested for at least another year.

Switch from duration fund to accrual fund after 1 year

7

8.64%

8.19% 8.05%3.86%

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%

Year 1 Year 2 Year 3

Cumulative annualised returnat the end of...

Impact of STCG tax

In summary…

The above calculations are based on various assumptions and actual performance may vary depending on the market conditions and actual change in the shape of the yield curve. This is for illustration purpose only. Please consult your financial advisor before taking any investment decisions. Annualized return shown above is assuming a total expense ratio (TER) of 150 bps. In the 3rd strategy (first bond fund and then switch to accrual fund), tax paid at the end of 1st year assumed to be 30.90% ; However, short term capital gains tax on investments in accrual fund not considered assuming investor will continue to stay invested for at least another year.

8.12%8.74%

8.05%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Dynamic Bond Fund Accrual Fund First bond fund and then switch to accrual fund

-1.2%

-1.0%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0 1 2 3

Yie

ld m

ove

me

nt

Year

Interest rate movement

Likely 3-year returns scenario in such environment

8

Strategy Duration Multiplier

Attractiveness of portfolio yield

Tax efficient?

Dynamic bond funds High Low Yes

Accrual funds Low High Yes

Strategy to switch from duration to accrual Moderate to High Moderate to high No

How can an investor benefit from best of both worlds

to maximize post tax returns?

Duration + accrual strategy

L&T Resurgent India Corporate Bond Fund*

A fund that aims to combine best of duration and accrual

strategy to deliver superior medium term performance

Introducing…

* For product labeling please refer to slide 19 10

Resurgent India Corporate Bond Fund^

Duration Fund

- Capitalize on the interest rate rally

- But low underlying yields

- High liquidity

- Predominantly AAA/ Sovereign category

Accrual Fund

- High underlying yields

- But difficult to build high duration

-Low liquidity

- Predominantly AA to A category

Resurgent India Corporate Bond Fund (Duration +

accrual)

- Mod duration: closer to long bond funds (~4-5)*

- Yields closer to accrual funds (AAA+~125-150 bps in current environment)

- Moderate to high liquidity

- Predominantly AAA /AA category

^ For product labeling please refer to slide 19. * As per the scheme information document, the scheme could have

modified duration of up to 6 years. 11

Portfolio positioning in the current environment

Duration Fund Accrual Fund

High Low

7 2

8.25% 10.25%

Rating AAA

Rating A

Resurgent India

Corporate Bond Fund

(RICBF)^

Gross YTM:~125-150 bps over AAA in current environment

(closer to accrual funds)

Duration: ~4.5 to 5 years*

(closer to duration funds)

Credit quality: Predominantly AAA / AA category

(closer to duration funds)

Liquidity: Moderate to High

(closer to duration funds)

The above portfolio positioning is based on the current assessment of the market environment. The actual portfolio positioning may be different from what has been shown here and the actual YTM of the portfolio could vary accordingly. ^ For product labeling please refer to slide 19. * As per the scheme information document, the scheme could have modified duration of up to 6 years.

12

Enablers for executing the strategy

Maturity / Duration

Yie

ld t

o M

atu

rity

Low Medium High

13

Low

High Loan against shares

Real estate loans

Operating co / NBFCs

G-secs / SDLs*

Highest quality PSU / corporate

bonds

High quality

structured papers

Perpetual bonds

CMBS

Bank capital instruments

RICBF^ would look to predominantly

invest in this segment

Strategy in current environment would be to add duration while keeping credit risks at moderate levels without compromising much on portfolio yield

The strategy indicated above is based on the current assessment of the market environment and the actual portfolio positioning may be different from what has been shown here. ^ For product labeling please refer to slide 19. * please note that RICBF would not invest in g-secs and SDLs except as mentioned in the scheme information document.

AAA category

AA category

A category

Provides yield kicker

High duration help capitalize when interest rates fall

Help benefit from higher yields and also capitalize when interest rates fall

In the current environment, the fund would look to

predominantly invest in…

High Quality Long Tenor Bonds

Bank Tier I perpetual under Basel III

• Adequate universe of strong public and private sector banks

• Rating category: AA to AAA

Duration: 5.5-6 years

YTM: 9.5%-10%

Perpetual bonds of Corporates

• Issued by some of the large corporates like Tata Steel and Tata Power

• Rating category: AA

Duration: 5-6 years

YTM: 10%-10.5%

Commercial Mortgage Backed Securities

(CMBS)

• Fully operational commercial properties with strong corporate tenants

• Rating category: AAA

Duration: 2.5-3 years

YTM: 9.5%-10%

High Quality Structured Products / Bonds

• Sponsored by strong corporates like IOCL, HPCL, NHAI etc

• Rating category: AA to AAA

Duration: 4 - 6 years

YTM: 9.5%-10%

~20-30% ~15-25% ~15-25% ~20-30%

The above information is provided based on the current assessment of the market environment and the actual allocations and portfolio may be different from what has been shown here. * The actual YTM of the portfolio could vary accordingly. ^ As per the scheme information document, the scheme could have modified duration of up to 6 years.

Predominantly AAA/AA rated portfolio with YTM of 125-150* bps over AAA ; Duration of 4.5-5^ years

14

However once interest rates stabilize, the fund would look to

trim duration exposure

2014 2015 2016 2017 2018

Macro outlook

• Falling inflation, gradual pick-up in economic growth • Expect RBI to ease monetary policy

• Growth acceleration and stable inflation • Limited room for further policy easing

15

• Focus on generating returns using

combination of capital appreciation and yield

accruals

• Portfolio YTM of ~ 125-150* bps over AAA

• Modified Duration of 4.5-5 years

• Focus on return generation through yield

accruals while limiting interest rate risk by

lowering duration

• Portfolio YTM of ~ 150-200* bps over AAA

• Modified Duration of 2-3 years

The above information is provided based on the current assessment of the market environment and the actual allocations and portfolio may be different from what has been shown here. * The actual YTM of the portfolio could vary accordingly.

8.12%

8.40% 8.46%

8.74%

8.39%

9.24%

9.47% 9.51%

9.98%

7%

8%

9%

10%

Scenario 1 Scenario 2 Scenario 3

Scenario analysis

3-year scenario analysis

16

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0 1 2 3

Yie

ld m

ove

me

nt

Year

Scenario # 1

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0 1 2 3

Yie

ld m

ove

me

nt

Year

Scenario # 2

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0 1 2 3

Yie

ld m

ove

me

nt

Year

Scenario # 3

Dynamic Bond Accrual Duration + accrual strategy

The above calculations are based on various assumptions and actual performance may vary depending on the market conditions and actual change in the shape of the yield curve. This is for illustration purpose only. Please consult your financial advisor before taking any investment decisions. Annualized return shown above is assuming a total expense ratio (TER) of 150 bps. Beginning YTM for dynamic bond fund, accrual fund and duration + accrual strategy is assumed to be 8.50%, 10.25% and 10% respectively and initial modified duration is assumed to be 6, 2.5 and 5 respectively. At the end of 1 year, it is assumed that modified duration of dynamic bond and duration + accrual strategy are revised to 2 and 2.5 respectively. The numbers shown above are based on a 3 year investment horizon and they could vary for different investment time periods.

An

nu

aliz

ed 3

yea

r p

erfo

rman

ce

L&T Resurgent India

Corporate Bond Fund

Adequate duration exposure

• Adequate duration to capture upside potential in falling interest rate environment ; flexibility to cut back duration once rates stabilize

Why L&T Resurgent India Corporate Bond Fund*?

* For product labeling please refer to slide no 19. The above information is provided based on the current assessment of the market environment and the actual allocations may be different from what has been shown here. ^ The actual YTM of the portfolio could vary accordingly. 17

Tax efficient • A combination of

duration and accrual strategy in one product allows investors to stay invested for over 3 years to earn better post tax returns

Stable investor base

• Exit load for 3 years to ensure stability of flows / avoid abrupt flows which can impact existing investors

A strategy that can: • Maintain high duration to capitalize on softening interest rate trend • Strategically lower duration once interest rates stabilize • Own securities which provide adequate yield pick-up over AAA • Offer tax efficient returns

Attractive portfolio yields

• Portfolio that would aim to have portfolio yield of 125-150^ bps over AAA

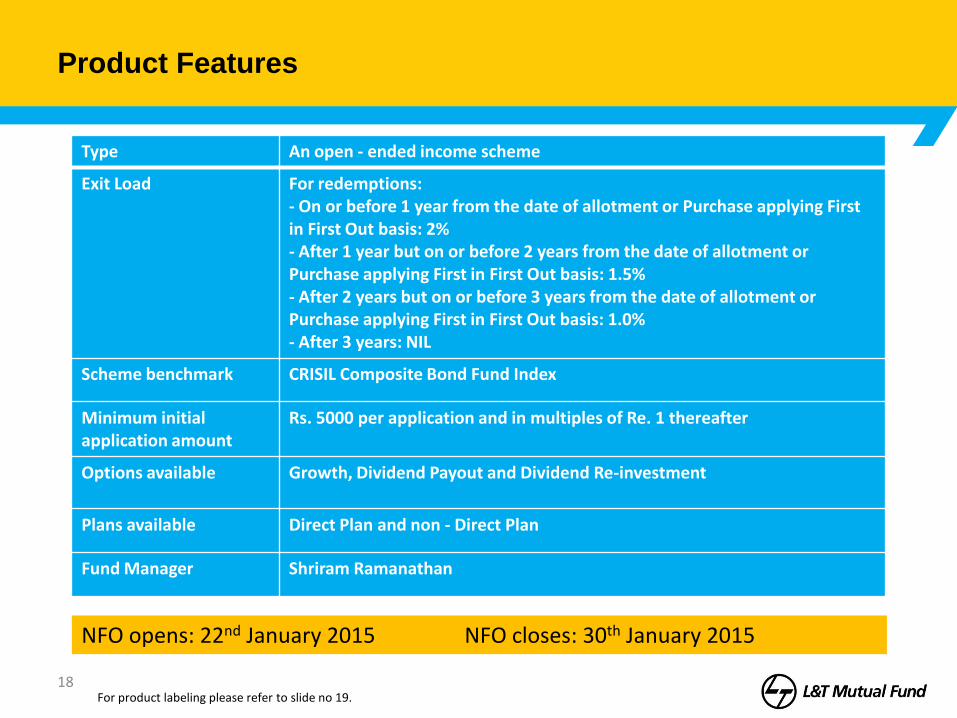

Product Features

Type An open - ended income scheme

Exit Load For redemptions: - On or before 1 year from the date of allotment or Purchase applying First in First Out basis: 2% - After 1 year but on or before 2 years from the date of allotment or Purchase applying First in First Out basis: 1.5% - After 2 years but on or before 3 years from the date of allotment or Purchase applying First in First Out basis: 1.0% - After 3 years: NIL

Scheme benchmark CRISIL Composite Bond Fund Index

Minimum initial application amount

Rs. 5000 per application and in multiples of Re. 1 thereafter

Options available Growth, Dividend Payout and Dividend Re-investment

Plans available Direct Plan and non - Direct Plan

Fund Manager Shriram Ramanathan

NFO opens: 22nd January 2015 NFO closes: 30th January 2015

18 For product labeling please refer to slide no 19.

Important Information

This presentation is for general information only and does not have regard to specific investment objectives, financial

situation and the particular needs of any specific person who may receive this information. The views expressed herein

are solely of L&T Investment Management Limited. The data/information used/disclosed in this presentation is only for

information purposes and not guaranteeing / indicating any returns. Recipient of this presentation should understand

that statements made herein regarding future prospects may not be realized. He/ She should also understand that any

reference to the securities/ sectors / indices in the document is only for illustration purpose and are NOT

recommendations from the author or L&T Investment Management Limited, the asset management company of L&T

Mutual Fund or any of its associates. Neither this presentation nor the units of L&T Mutual Fund have been registered

in any jurisdiction. The distribution of this presentation in certain jurisdictions may be restricted or totally prohibited and

accordingly, persons who come into possession of this presentation are required to inform themselves about, and to

observe, any such restrictions. Please consult your investment adviser before making investments.

Mutual Fund investments are subject to market risks, read all scheme related documents

carefully.

CL01501

This product is suitable for investors who are seeking:*

• Generation of income over medium to long term

• Investment primarily in debt and money market securities of fundamentally strong corporates/ companies in growth sectors which

are closely associated with the resurgence of domestic economy

• Low risk (BLUE)

Note: Risk may be represented as: (BLUE) investors understand that their principal will be at low risk; (YELLOW)

investors understand that their principal will be at medium risk; (BROWN) investors understand that their principal will be at

high risk.

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

19

Thank You!!!