Kuntal Dave, CA Budget 2007 – Income Tax proposals affecting non-residents Court proposes,...

35

Kuntal Dave, CA Budget 2007 – Income Tax proposals affecting non- residents Court proposes, Government disposes Date: March 5, 2007 Venue: SNDT Hall, Mumbai Group Chairman: Porus Kaka Group Leader: Kuntal Dave

-

Upload

ashlee-barrett -

Category

Documents

-

view

214 -

download

0

Transcript of Kuntal Dave, CA Budget 2007 – Income Tax proposals affecting non-residents Court proposes,...

Kuntal Dave, CA

Budget 2007 – Income Tax proposals affecting non-residents

Court proposes, Government disposes

Date: March 5, 2007

Venue: SNDT Hall, Mumbai

Group Chairman: Porus Kaka

Group Leader: Kuntal Dave

Kuntal Dave, CA

Contents

• Rate of tax (surcharge and education cess)

• Definition of ‘India’ (section 2(25A))

• Explanation to section 9

• Exemption for the Interest from banks (u/s 10(15)(iv))

• Income for venture capital company (u/s 10 (23FB))

• MAT for units covered u/s 10A or 10B

• Time limit for completion of assessment by TPO

• Procedure to be adopted by A.O. for consideration of the order of TPO

• Distribution tax on income distributed on units of Mutual Funds u/s 115R

• Appeal against TDS u/s 195

Kuntal Dave, CA

Definition of ‘India’

Section 2(25A)

• Before Amendment– India shall be deemed to include the Union territories of Dadra and

Nagar Haveli, Goa, Daman and Diu, and Pondicherry,

• as respects any period, for the purposes of section 6 ; and

• as respects any period included in the previous year, for the purposes of making any assessment for the assessment year commencing on the 1st day of April, 1963, or for any subsequent Year

• After Amendment (effective 25 Aug 1976)– India means the territory of India as referred to in article 1 of the

constitution, its territorial waters, seabed and subsoil underlying such waters, continental shelf, exclusive economic zone or any other maritime zone as refereed to in the territorial waters, continental Shelf , exclusive economic zone and other maritime zone act, 1976, and the air space above its territory and territorial waters.

Kuntal Dave, CA

General Definition (under treaty)

The term India means the territory of India and includes the territorial sea and the air space above it, as well as any other maritime zone in which India has sovereign rights, other rights and jurisdictions, according to the Indian law and in accordance with international law

An attempt to disregard order of HC – retrospective amendment

Definition of ‘India’

Section 2(25A) – cont’d

Kuntal Dave, CA

Explanation to section 9

Income deemed to accrue or arise in India

● Before Amendment

Retrospective amendment (from 1st June, 1976) has been proposed by inserting an explanation in Section 9 so as to tax income in the nature of interest, royalty and technical services earned in India by a Non-Resident, whether or not he has residence or place of business or business connection in India.

Under the existing provisions of section 9, income earned by a Non - Resident in the nature of interest, royalty and technical services are subject to tax in India under the 'Source Rule'.

● After Amendment

Kuntal Dave, CA

Explanation to section 9 – cont’d

Income deemed to accrue or arise in India

● Rationale for amendment – as explained

Source rule

Courts have misunderstood

Interest, royalty and fees for technical services at

par

Kuntal Dave, CA

• Consortium was

established

• Turnkey Project

• Setting up a Liquefied

natural gas receiving

storage and

degasification facility

• Role and responsibility of

consortium member

separately specified

• Separate payments

specified

• To develop, design, reengineer and

procure equipment/ material / supplies.

• To erect and constitute storage tanks

• Marine facility for transmission & supply

of LNG to purchaser

• To test and commission the facilities

relating to receipt and unloading,

storage and re-gasification of LNG

• To send out re-gasified LNG

Explanation to section 9 – cont’d

Background for proposed amendment

Kuntal Dave, CA

Description of scope In Indian rupees In US Dollars

Offshore supply Nil 81,711,877

Offshore services Nil 19,756,225

Onshore supply *** 1,869,978,658 Nil

Onshore services *** 1,774,353,282 12,780,467

Construction and erection ***

3,958,464,384 36,795,623

Total

*** - not a subject matter before AAR

7,602,796,324 151,044,192

Explanation to section 9 – cont’d

Kuntal Dave, CA

Explanation to section 9 – cont’d

Advance Authority Rulings - propositions

Scenario Taxability in India

Sale of goods simpliciter No income accrue or arise in India

Not taxable

Sale of goods as a part of composite contract involving various operations within and outside India

If it accrues or arises in India

taxable

Business of which all operations are not carried out in India

Income attributable to part of operation carried out in India

taxable

Business connection in India or/and whether all operations of the business are not carried out in India

Depends on the facts of the case

Kuntal Dave, CA

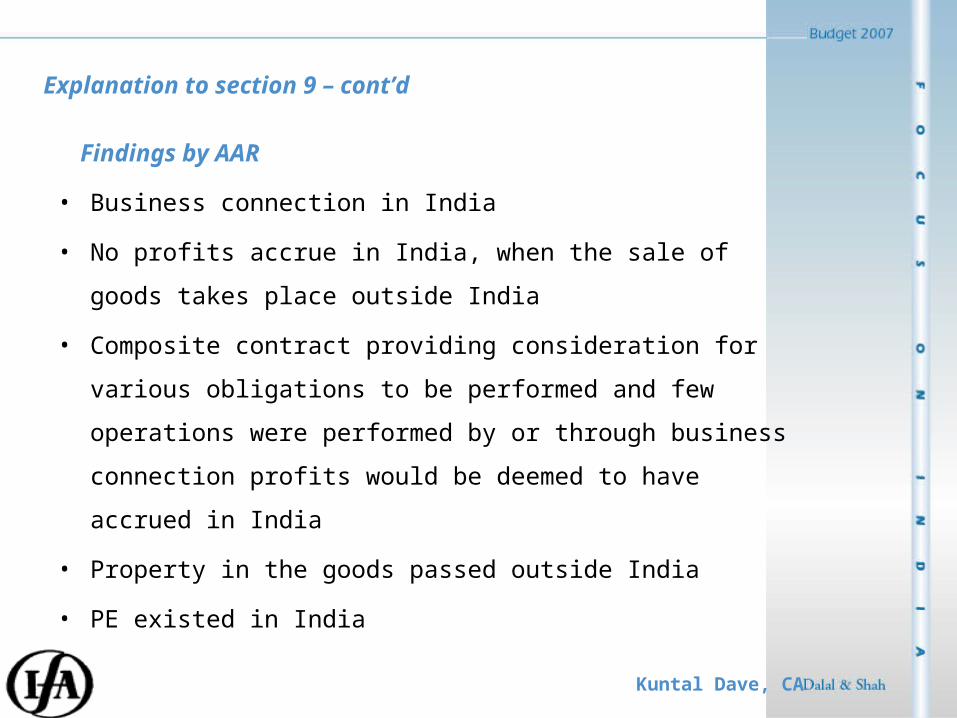

• Business connection in India

• No profits accrue in India, when the sale of goods takes

place outside India

• Composite contract providing consideration for various

obligations to be performed and few operations were

performed by or through business connection profits would

be deemed to have accrued in India

• Property in the goods passed outside India

• PE existed in India

Findings by AAR

Explanation to section 9 – cont’d

Kuntal Dave, CA

Explanation to section 9 – cont’d

Advance Authority Rulings

Description of scope taxability Amount subject to tax

Offshore supply Taxable Profit attributable to the operations

Offshore services Taxable 20 per cent on gross basis

Onshore supply *** N A N A

Onshore services *** N A N A

Construction and erection ***

N A N A

Kuntal Dave, CA

Explanation to section 9 – cont’d

Before SC – Department’s contentions

• Composition of contract – based on facts (linkeage with onshore

activities, dominant objective, point of time and place where

title of goods not relevant)

• All the activities were to ensure completion of entire contract

• Breach would result for the entire contract and not just the

particular obligation

• Turnkey project shall be PE

• Business connection in India and offshore supply/services

interlinked with the entire project

• DTAA facilitates the allocation of income amongst the

jurisdiction

• Offshore supply/services attributable to turnkey project and

taxable in terms of article 7

Kuntal Dave, CA

Explanation to section 9 – cont’d

Before SC – Appellant’s contention

• Payments in US$, title of the goods passed on outside India and services rendered outside India

• Contact important and not where was it signed (converse situation)

• Consideration was not for construction or like project• Fees effectively connected to contract but not

attributable to PE• Scope of 5(2) – income accrues or arises or deemed to

accrue or arise in India or received or deemed to be received

• No part of income received in India• All operations in connection with offshore supply carried

outside India• No consideration for certain services (like unloading,

port clearance, etc.)• Activities in India were independent of offshore services• DTAA – no tax in India on offshore supply

Kuntal Dave, CA

Explanation to section 9 – cont’d

• Income attributable to operations carried out in India• No tax in India – all parts of the transactions outside

India• Territorial jurisdiction to be followed• Contract where signed not important• PE is different from Business connection• As per Explanation 1(a) to S. 9(1)(i) only such part of

the income as is attributable to the operations carried out in India, are taxable in India.

• Permanent establishment does not constitute sufficient 'business connection', and the permanent establishment would be the taxable entity.

• There is a difference between the existence of a business connection and the income accruing or arising out of such business connection.

• Involvement of PE is important for attributing profits

SC - Offshore supply

Kuntal Dave, CA

• Sufficient territorial nexus between the rendition of services and

territorial limits of India is necessary to make the income taxable.

• The entire contract would not be attributable to the operations in

India

• Act not wide import to include the income received by non-resident

outside India for the services rendered outside India

• ‘Residence’ qua the tax payer and not the recipient of the services

• Services to be utilized within India and must be rendered in India

• The terms 'effectively connected' and 'attributable to' are to be

construed differently even if the offshore services and the permanent

establishment were connected

SC - Offshore services

Explanation to section 9 – cont’d

Kuntal Dave, CA

• Section 9(1)(vii)(c) of the Act would not apply as there is

nothing to show that the income derived by a non-resident

company irrespective of where rendered, was utilized in India.

• No profit can be attributable to PE in India in terms of Article 7

• Applying the principle of apportionment to composite

transactions which have some operations in one territory and

some in others, is essential to determine the taxability of

various operations.

• The location of the source of income within India would not

render sufficient nexus to tax the income from that source

• Distinction exists for connection between the Indian and

foreign operations and apportionment of income

• The services are inextricably linked to the supply of goods,

and it must be considered in the same manner

SC - Offshore services

Explanation to section 9 – cont’d

Kuntal Dave, CA

SC - several observations independent of Section 9

• Turnkey project would not mean that taxability of entire

contract should be considered to be an integrated

• Specification of different supply of equipment and services

points that liability of tax would be different

• Execution of contract in India would not make the entire income

derived from the contract taxable in India.

• A contract must be construed keeping in view the intention of

the parties

• Where different severable parts of the composite contract are

performed in different places, the principle of apportionment

can be applied to determine which fiscal jurisdiction can tax that

particular part of the transaction

• Income that was attributable to the operations carried out in

India would be taxable in India

• Territorial nexus doctrine upheld (entire income cannot be

regarded as accruing or arising in each of jurisdictions)

Explanation to section 9 – cont’d

Kuntal Dave, CA

SC - several observations independent of Section 9

• CBDT instructions of September 21, 1989 in case of hydro

electric power project was upheld

• Principle of apportionment of is recognized under Act – goods

manufactured and sold outside India??

• 9(1)(vii)(c) – requires two conditions to be met (rendered in

India as well as utilized in India)

• 9(1)(vii) must be read with section 5

• Territorial nexus for the purpose of determining the tax liability

is an internationally accepted principle

• Whatever is payable by a resident to a non-resident by way of

fees for technical services would not always come within the

purview of section 9(1)(vii)

• Agree to the view of Prof Klaus Vogel

Explanation to section 9 – cont’d

Kuntal Dave, CA

Issues

• Whether the proposed amendment would reverse the

SC decision?

• Whether the proposed amendment can be regarded as

unconstitutional?

• International Law on the suo motto amendment to the

domestic law by a state (especially to such retrospective

amendment)

Explanation to section 9 – cont’d

Kuntal Dave, CA

Exemption for the Interest from Banks

Section 10(15)(iv) (fa)

● Amendment

Consequential to amendment to section 36(1)(vii)

Kuntal Dave, CA

Income for venture capital company

Section 10 (23FB)

o Any income of a Venture Capital Company or Venture Capital Fund, set up to raise funds for investments in Venture Capital undertaking is exempt from tax

o Venture capital undertaking means a venture capital undertakingreferred to in the Securities and Exchange Board of India (VentureCapital Funds) Regulations, 1996 made under the Securities and Exchange Board of India Act, 1992 and notified as such in the Official Gazette by the Board

● Before Amendment

Kuntal Dave, CA

● After Amendment

o Any income of a Venture Capital Company or Venture Capital Fund, from investments in Venture Capital undertaking is exempt from tax

o Venture capital undertaking means such domestic company whose shares are not listed in a recognised stock exchange in India and which is engaged in certain specified business or industries

Income for venture capital company – cont’d

Section 10 (23FB)

Kuntal Dave, CA

● Specified Business

− Nanotechnology,− Information technology relating to hardware and

software development,− Seed research and development, − Bio-technology,− Research and development of new chemical entities in

the pharmaceutical sector, − Production of bio-fuels− Building operating composite hotel-cum convention

centre with seating capacity of more than three thousand.

● Specified Industries

− Dairy− poultry

Income for venture capital company – cont’d

Section 10 (23FB)

Kuntal Dave, CA

• Set up to raise funds for investments v/s from investments

• Definition of VCU

– ‘Deserving sectors’

– SEBI (VCF) Regulations and role of VC industry internationally

– Earlier proviso to cl (b) to sub-section (1) to 112

Income for venture capital company – cont’d

Section 10 (23FB)

Kuntal Dave, CA

• 10 (23F) and 10 (23FA) not to apply to investments made after 31

March 99/00

• What about the income arising to VCC for investments made prior to

31 March 07 or from other business/industry?

• What if VCU changes the business?

• Income arising after VCU get listed?

• Whether it will make any difference to the tax incidence, after

proposed amendment?

Income for venture capital company – cont’d

Section 10 (23FB)

Kuntal Dave, CA

Income for venture capital company – cont’d

Section 10 (23FB)

Kuntal Dave, CA

Income for venture capital company – cont’d

Section 10 (23FB)

Kuntal Dave, CA

MAT for units covered u/s 10A or 10B

Section 115JB

For the purposes of section 115JB, book profit means − the net profit as shown in the profit and loss account for

the relevant previous year prepared under sub-section (2), asincreased by

− the amount or amounts of expenditure relatable to any income to which section 10[(other than the provisions contained in clause (23G) thereof)] or section 10A or section 10B or section 11 or section 12 apply [explanation (f) ]

● Before Amendment

● After Amendment

● Income to be included in book profit for the purpose of MAT

Change of domestic law by the state – Foreign Company can take shelter of international law?

Kuntal Dave, CA

Time limit for completion of assessment by TPO and role of AOSection 92CA (4)

o TPO to arrive at ALP – no time limit prescribedo Where an arms length price is determined by the

Assessing Officer under sub-section (3), the Assessing Officer may compute the total income of the assessee having regard to the arms length price so determined

● Before Amendment

o TPO to arrive at ALP – time limit prescribedo Where an arms length price is determined by the

Assessing Officer under sub-section (3), the Assessing Officer may compute the total income of the assessee in conformity with the arms length price so determined

● After Amendment

Kuntal Dave, CA

Time limit for completion of assessment by TPO and role of AOSection 92CA (4)

o Assessee deprived of dual opportunity of substantiating

the transfer price

o Decision of Delhi HC in the case of Sony India – will it make

department’s case weak now?

o Practical difficulties (to facilitate the completion of

assessment during the month of October)

● Issues

Kuntal Dave, CA

Distribution tax on income distributed on units of Mutual Funds Section 115R

Income Distributor Rate of distribution tax

Money market Mutual Fund / liquid fund

Existing rate Proposed rate

Recipient – Individual/HUF Others

12.5 25

20 25

Other Mutual fund Existing rate Proposed rate

Recipient – Individual/HUF Others

12.5 12.5

20 20

Kuntal Dave, CA

Distribution tax on income distributed on units of Mutual Funds Section 115R

• SEBI (MF) Regulations

• Whether amendment to the proviso to section

10(35) necessary?

• Information to the investors?

Kuntal Dave, CA

Appeal against TDS

Under Section 195

− Any person after deducting and making the payment of tax in accordance with the provision of section 195 and 200 is eligible to make appeal to the CIT (A) challenging such liability to deduct tax at source.

− In such situation the person making the payment (the deductor) shall claim claim the refund of tax deducted and paid by him in addition to theNon -Resident from whose income the tax has been deducted as such.

● Before Amendment

− where under an agreement or other arrangement, the tax deductible on any income, other than interest, under section 195 is to be borne by the person by whom the income is payable, and

− such person having paid such tax to the credit of the Central Government, claims that no tax was required to be deducted on such income, he mayappeal to the Commissioner (Appeals) for a declaration that no tax wasdeductible on such income

● After Amendment

Kuntal Dave, CA

• Issues

– Appeal only when the tax has been paid by the person

– will it cover TDS?

– Appeal within 30 days from the date of payment of tax

– practical difficulties for a non-resident, especially in

case of TDS?

– Time limit for disposal of application u/s 195(2)/(3)?

Appeal against TDS

Under Section 195

Kuntal Dave, CA

Thank Thank YouYou

![MKCL RLC Mumbai, DU SNDT WU e-Suvidha Implementation 2013-14 Online Admission Process for College [ DU SNDT WU ]](https://static.fdocuments.net/doc/165x107/56649c745503460f94926a26/mkcl-rlc-mumbai-du-sndt-wu-e-suvidha-implementation-2013-14-online-admission.jpg)