Kuali Financial Systems – Financial Administrator Development Series - October, 2006 Fund...

86

Kuali Financial Systems – Financial Administrator Development Series - October, 2006 Fund Accounting

-

Upload

jane-horton -

Category

Documents

-

view

216 -

download

0

Transcript of Kuali Financial Systems – Financial Administrator Development Series - October, 2006 Fund...

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Fund Accounting

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Summary of Today’s Topics

• Fund Accounting– Definitions– Value Added– Allowable Activity by Fund

• Function Codes

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

What is Fund Accounting?

Fund accounting is the procedure by which resources for various purposes are classified by accounting and reporting purposes in accordance with activities or objectives as specified by donors, in accordance with regulations, restrictions, or limitations imposed by sources outside the institution, or in accordance with directions issued by the governing board.

AICPA Audits of Colleges and Universities Industry Audit Guide

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Audit Guide Fund Groups

• Unrestricted Current Funds• Restricted Current Funds• Loan Funds• Endowment and Similar

Funds• Plant Funds• Other Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Fund Groups

General Funds

Designated Funds

Restricted Funds

Auxiliary Enterprises

Current Funds

Clearing Funds

Internal Agency

External Agency

Other Funds

Loan Funds

Endowment Funds

Plant Funds

Noncurrent Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Unrestricted Current Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Unrestricted Current Funds

Include those economic resources of the institution which are expendable for any purpose in performing the primary objectives of the institution, i.e. instruction, research, and public service and which have been designated by the governing board for other purposes.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

What is an Auxiliary?

An enterprise that furnishes goods or services to students, faculty, or staff and charged a fee directly related to, although not necessarily equal to, the cost of the goods or services. Basically, an entity managed as a self-supporting activity.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

What is a Service Fund?

An enterprise that furnishes goods or services to other internal university departments and charges a fee directly related to, and equal to, the cost of the goods or services. Basically, an entity managed as a self-supporting activity that is not allowed to make a profit.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Unrestricted Current Funds

• General Funds • Designated Funds

– Continuing Education – Public Service – Internal Research – Other - the Mighty Catch-all – Unrestricted Scholarships

• Auxiliary Enterprise Funds– Auxiliary – Service

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Grid Work

• General• Designated • Auxiliary Enterprises

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

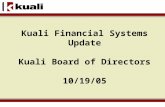

Unrestricted Current Funds – Additions

• State Appropriations• Student Fees• Sales and Services

– Academic, Auxiliary & Service

• Recovery of Indirect Cost

• Interest (Gains are questionable)

• Gifts• Rent, Dividends &

Royalties• Endowment Income –

if unrestricted• Other Sources• Transfers In

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Unrestricted Current Funds – Deductions

• Matching Expenditures– Salaries, Wages & Benefits– Supplies & Expense– Travel– Capital Expenditures– Note Payments (lease purchases)– Interest Expense (lease purchases)– Transfers Out

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Unrestricted Current Funds – Assets

• Cash• Investments• Accounts Receivable• Inventories• Prepaid Expenses• Due from Other Funds• Notes Receivable

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

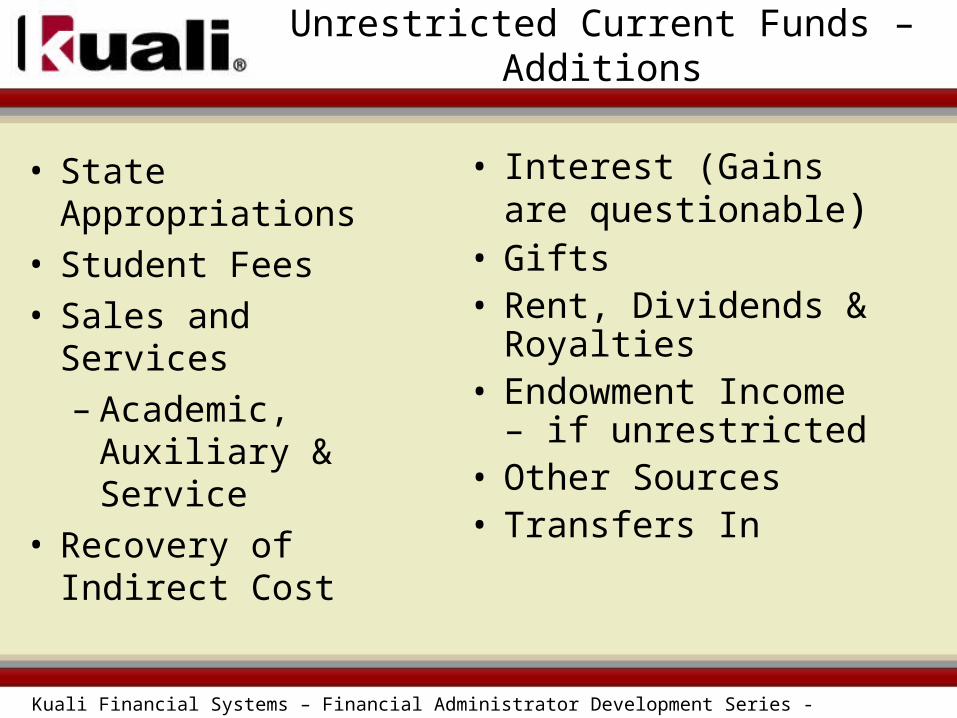

Unrestricted Current Funds – Liabilities

• Accounts Payable• Salaries Payable• Accrued Vacation

Liability• Deferred Revenue• Due to Other Funds• Notes Payable

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Restricted Current Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

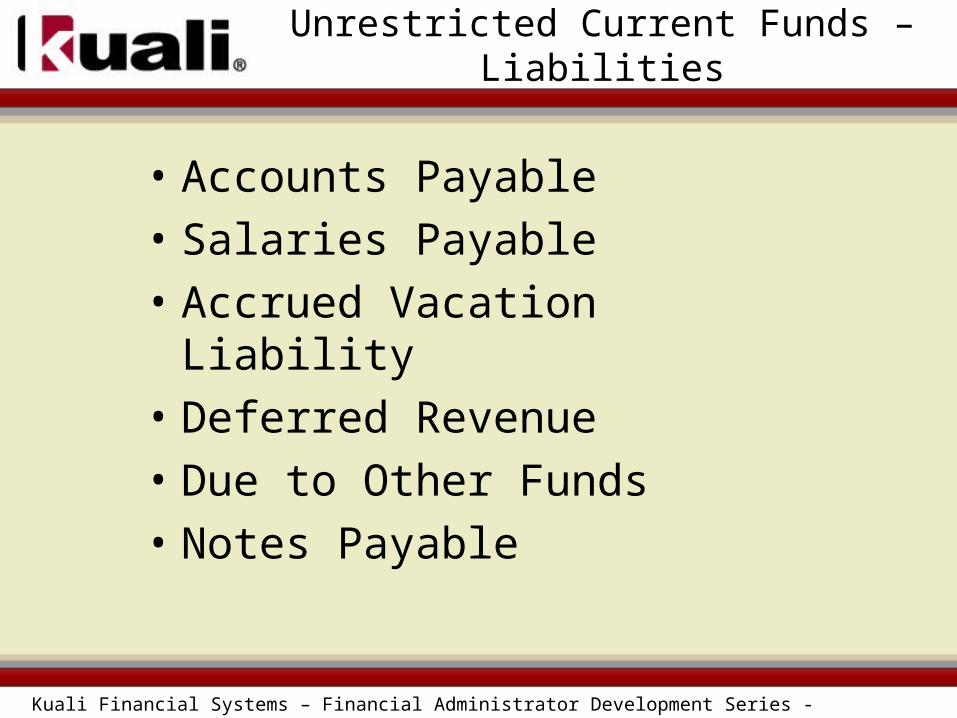

Restricted Current Funds

Those funds expendable for operating purposes but restricted by donors or other outside agencies as to the specific purpose for which they may be expended.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Restricted Current Funds

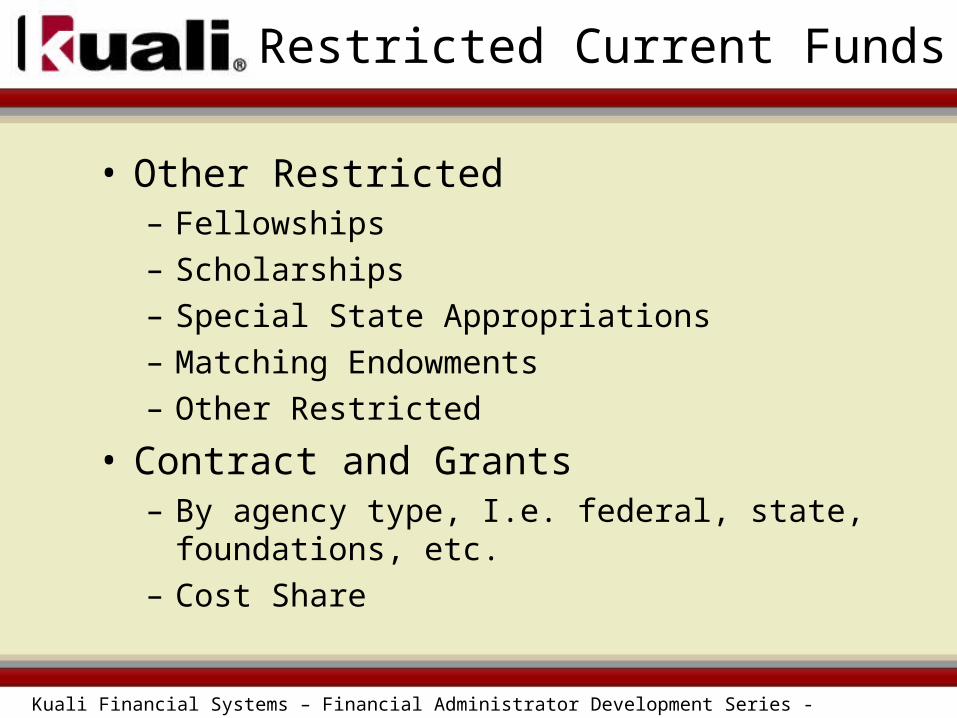

• Other Restricted– Fellowships – Scholarships – Special State Appropriations– Matching Endowments– Other Restricted

• Contract and Grants – By agency type, I.e. federal, state, foundations, etc.– Cost Share

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Grid Work

• Contracts & Grants

• Other Restricted

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Restricted Current Funds - Additions

• Sales & Services (program income)

• Interest & Gains

• Gifts

• Grants & Contracts

• Endowment Income

• Other Income (program income)

• Transfers In

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Restricted Current Funds – Deductions

• Matching Expenditures– Salaries, Wages & Benefits– Supplies & Expense– Travel– Indirect Cost Recovery– Capital Expenditures– Note Payments (lease purchases)– Interest Expense (lease purchases)– Transfers Out

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Restricted Current Funds – Assets

• Cash• Investments• Accounts Receivable• Inventories• Prepaid Expenses• Due from Other Funds• Notes Receivable

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Restricted Current Funds – Liabilities

• Accounts Payable• Salaries Payable• Deferred Revenue• Due to Other Funds• Notes Payable

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Loan Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Loan Funds

The loan funds group consists of loans to students, faculty, or staff, and of resources available for such purposes.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Loan Funds

• Gift Agreements specify revolving• Many are temporary and require

repayment of principal & interest• Some specify forgiveness of repayment

under certain conditions• Specific restrictions can exist

– Geographic– Financial status

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Grid Work

• Loans

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Loan Funds – Additions

• Interest • Gifts• Endowment Income• Other Sources

– Government advances

• Transfers In

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Loan Funds – Deductions

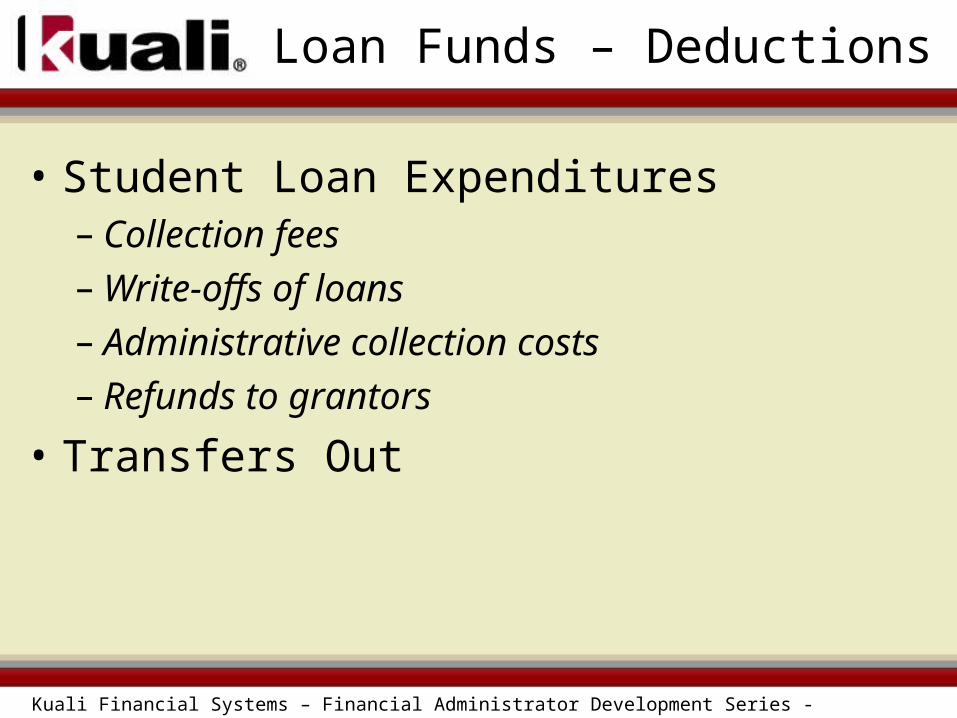

• Student Loan Expenditures– Collection fees– Write-offs of loans– Administrative collection costs– Refunds to grantors

• Transfers Out

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Loan Funds - Assets

• Cash• Investments – temporary• Due from other Funds• Notes Receivable

– Face value– Allowance for doubtful loans

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Loan Funds - Liabilities

• Accounts Payable– amounts due collection agencies for fees– Refundable loan amounts

• Due to other Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Endowment and Similar Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Endowment and Similar Funds

• Endowment Funds• Term Endowment Funds• Quasi-endowment Funds• Annuity and Life Income Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Endowment Funds

Endowment funds are funds with respect to which donors or other outside agencies have stipulated, as a condition of the gift instrument, that the principal is to be maintained inviolate and in perpetuity and invested for the purpose of producing present and future income which may either be expended or added to principal.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Term Endowment Funds

Term endowment funds are similar to endowment funds except that, upon the passage of a stated prior of time or the happening of a particular event, all or a part of the principal may be expended.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Quasi-endowment Funds

Sometimes called funds functioning as endowments, quasi-endowments are funds which the governing board of an institution, rather than a donor or other outside agency, has determined are to be retained and invested. Because they are internally designated, the governing board has the right to decide at any time to expend the principal.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Annuity and Life Income Funds

Funds contributed to an institution subject to the requirement that the institution periodically pay the income earned on the assets to designated beneficiaries.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Grid Work

• Endowments and Similar Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Endowments and Similar Funds – Additions

• Interest & Gains– Losses

• Gifts• Other Income

– Income from Asset – Farm Activity, Rental, etc.

• Transfers In

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Endowments and Similar Funds – Deductions

• Supplies & Expense – Payouts on life income funds

• Transfers Out

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Endowments and Similar Funds – Assets

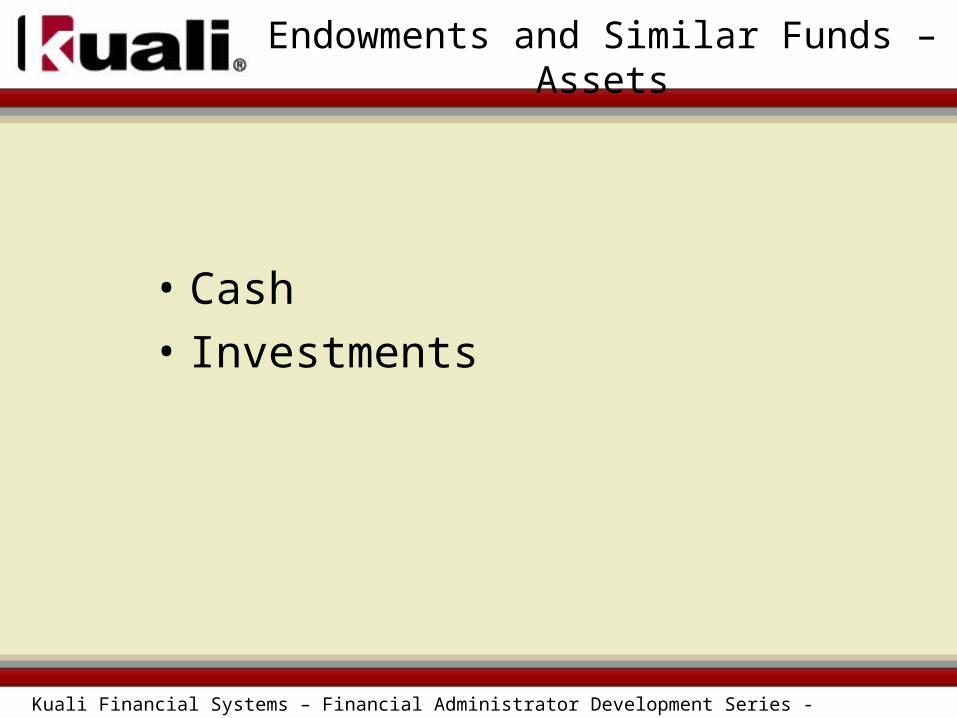

• Cash• Investments

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Endowments and Similar Funds - Liabilities

• NONE

The mission of these funds is to make money, not spend it. Therefore, there tends to be no liabilities since there are no deductions.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Endowments and Similar Funds

• Institutional spending policy• Endowment Income booked directly to

operating account– This is IU specific

• Industry calls for– Prudence– Rational and systematic formula

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Plant Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Plant Funds

• Construction• Retirement of Indebtedness• Renewal and Replacement• Investment in Plant

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Plant Fund Definitions

• Construction– Funds for acquisition of physical plant– Sometimes called Unexpended Plant

• Retirement of Indebtedness– Indebtedness incurred for plant expansion

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Plant Fund Definitions - continued

• Renewal & Replacement– Funds set aside for replacement of

renewable property• Desktop computer replacement

• Investment in Plant– Location of all assets that have been

capitalized and related to debt

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Grid Work

• Construction• Retirement of Indebtedness• Renewal & Replacement• Investment in Plant

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Construction - Additions

• Additions– State Appropriations– Interest & Gains

• Losses

– Gifts – Grants – federal and state– Bond Revenue– Transfers In

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Construction - Deductions

– Supplies & Expenditures

• Expendable equipment

– Capital Expenditures

• Predominantly building capitalization

– Transfers Out

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Construction – Assets

• Cash• Investments• Accounts Receivable• Prepaid Expense • Due from other Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Construction – Liabilities

• Accounts Payable• Due to other Funds• Notes Payable• Bonds Payable

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Retirement of Indebtedness – Additions

• Interest and gains– Losses

• Gifts• Grants• Transfers In

– Mandatory – Voluntary

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Retirement of Indebtedness - Deductions

• Supplies & Expense– Trustee’s fees and expenses

• Note Payments• Bond Payments• Interest Payments

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Retirement of Indebtedness - Assets

– Cash

– Investments

– Funds on deposit

– Accounts Receivable

– Due from other funds

– Notes receivable

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Retirement of Indebtedness - Liabilities

• NONE

Retirement of Indebtedness usually does not have any liabilities. Predominantly this is true because there are no operating expenditures involved in the fund group, nor any long term debt.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Renewal and Replacement Funds – Additions

• Interest and gains– Losses

• Gifts • Grants• Transfers In

– Mandatory– Voluntary

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Renewal and Replacement Funds - Deductions

• Supplies and Expense– Expendable Equipment– Maintenance of R&R Items

• Capital Expenditures• Transfers Out – very seldom

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Renewal and Replacement Funds - Assets

• Cash• Investments• Funds on Deposit • Accounts Receivable• Due from other Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Renewal and Replacement Funds – Liabilities

• Accounts Payable• Due to other Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Investment in Plant – Additions

• NONE

You will never see a revenue in Investment in Plant. There is never cash activity

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Investment in Plant – Deductions

• NONE

You will never see an expenditure in Investment in Plant.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Investment in Plant - Assets

• Capital Assets– Land

– Buildings

– Moveable Equipment

– Cataloged Library Acquisitions– Improvements to Land

• Accumulated Depreciation

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Investment in Plant – Liabilities

• Notes Payable• Bonds Payable

Only debt that matches the capital assets

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Other Funds

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Other Funds

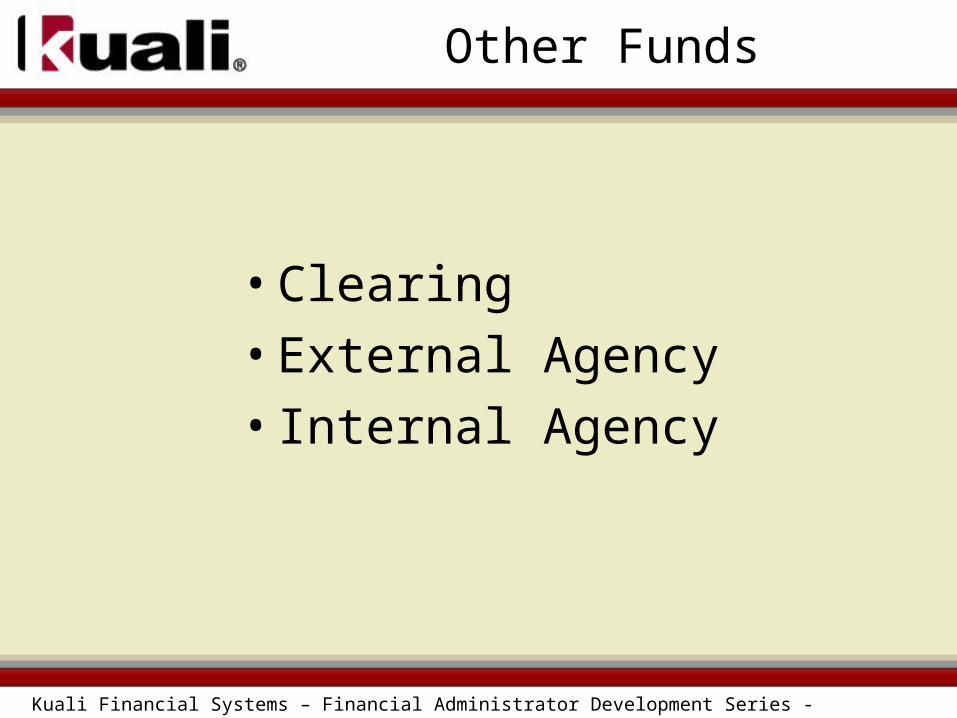

• Clearing• External Agency• Internal Agency

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

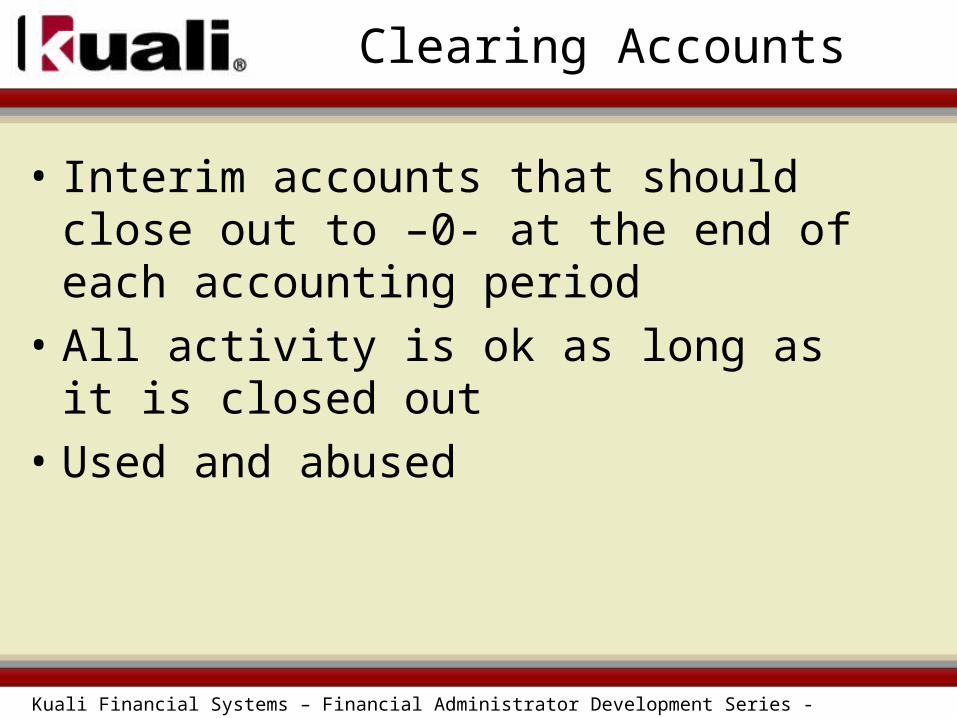

Clearing Accounts

• Interim accounts that should close out to –0- at the end of each accounting period

• All activity is ok as long as it is closed out• Used and abused

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

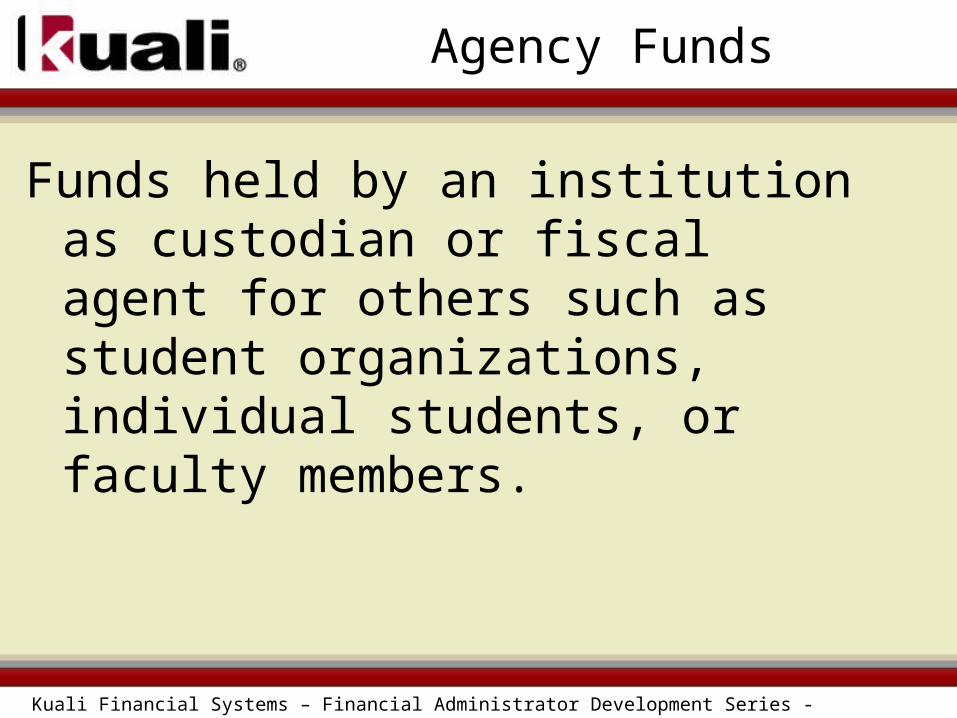

Agency Funds

Funds held by an institution as custodian or fiscal agent for others such as student organizations, individual students, or faculty members.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Internal Agency Funds

• Temporary Holding Accounts• Examples:

– FICA– Federal Taxes– State Taxes

• Reported as Unrestricted at June 30

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

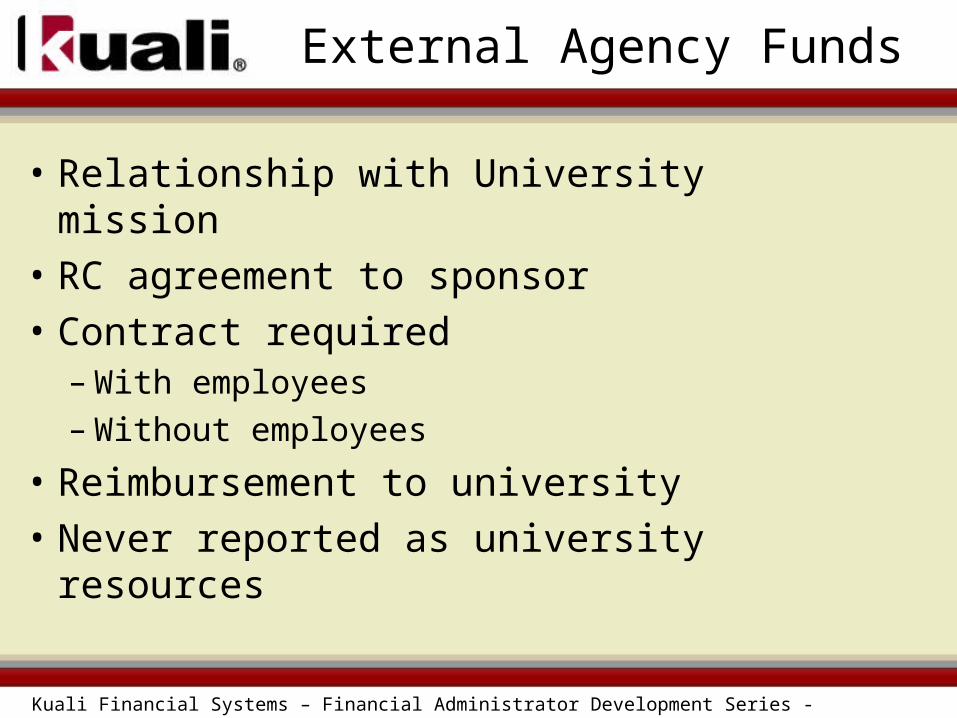

External Agency Funds

• Relationship with University mission• RC agreement to sponsor• Contract required

– With employees– Without employees

• Reimbursement to university• Never reported as university resources

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Questions

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Higher Education Function Codes

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

What are function codes needed for ?

• IPEDS

• Facilities and Administrative Rate

• Internal management of how dollars are spent

• Some states require reporting by function

• Institutions can report expenses in the operating statement by function instead of natural classification

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Educational and General Function Codes

• Instruction• Research• Public Service• Academic Support• Student Services• Institutional Support• Operation and Maintenance of Plant• Scholarships and Fellowships

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

INSTRUCTION

• General Academic

• Vocational/Technical

• Continuing Education

• Remedial

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

RESEARCH

• Individual

• Project

• Institutes and research centers

NOT equivalent to sponsored research

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

PUBLIC SERVICES

• Community service

• Cooperative extension services

• Public broadcasting services

– not primarily instructional

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

ACADEMIC SUPPORT

• Libraries

• Museums and galleries

• Educational media

• Academic computing

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

ACADEMIC SUPPORT Cont’d

• Ancillary support

• Academic administration

• Academic personnel development

• Course and curriculum development

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

STUDENT SERVICES

• Student services administration

• Financial aid administration

• Student records

• Admissions

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

STUDENT SERVICES, con’t

• Counseling and career guidance

• Social and cultural development

• Student health services

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

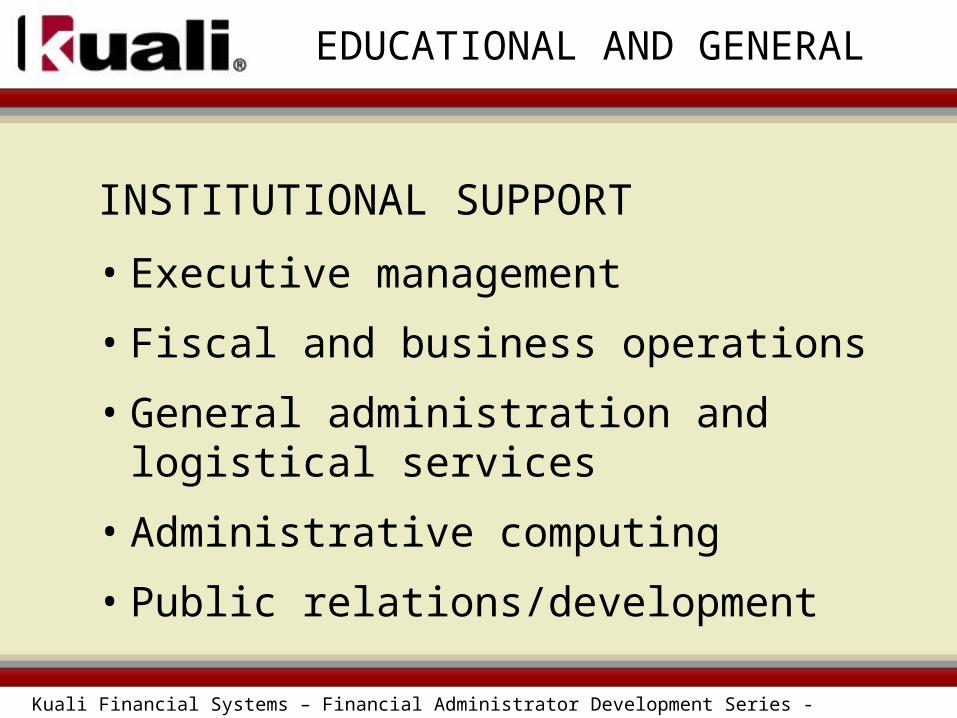

INSTITUTIONAL SUPPORT

• Executive management

• Fiscal and business operations

• General administration and logistical services

• Administrative computing

• Public relations/development

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

OPERATION AND MAINTENANCE OF PLANT

• Physical plant administration (and planning)

• Building maintenance

• Custodial services

• Utilities Cont’d

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

OPERATION AND MAINTENANCE OF PLANT

• Landscape and grounds maintenance

• Major repairs and renovations

Note: Not an expenditure category for private, must allocate out to all other functions.

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

EDUCATIONAL AND GENERAL

SCHOLARSHIPS AND FELLOWSHIPS• Grants• Trainee stipends• Prizes and awards• Tuition and fee waivers

NO exchange of services, used as designated by donor

Kuali Financial Systems – Financial Administrator Development Series - October, 2006

Questions on Function Codes?