Koenen en Co is lid van Nexia International, het wereldwijde netwerk van onafhankelijke accountants-...

15

Koenen en Co is lid van Nexia International, het wereldwijde netwerk van onafhankelijke accountants- en advieskantoren Debt vs Equity in the Netherlands mr. Giovanni Armino Tax Partner at Koenen en Co Sittard, the Netherlands

-

Upload

marion-marsh -

Category

Documents

-

view

214 -

download

0

Transcript of Koenen en Co is lid van Nexia International, het wereldwijde netwerk van onafhankelijke accountants-...

Koenen en Co is lid van Nexia International, het wereldwijde netwerk van onafhankelijke accountants- en advieskantoren

Debt vs Equity in the Netherlands

mr. Giovanni ArminoTax Partner at Koenen en Co Sittard, the Netherlands

2

1A. Thin Cap Rules Article 10d Corporate tax law)

1.A.1 Only applicable for tax purposes 1.A.2 Not limited to intercompany loans but restriction cannot

exceed interest paid to affiliated parties

3

A. The ratio’s 1.A.3 Ratio’s

1:3 Ratio: Too much debt if:

debt is more than 3x equity ánd the debt exceeds € 500.000

Concern Ratio: Too much debt if:

Average debt of taxpayer is more than: Average debt group x groupfactor (=debt-equity

ratio of the group)

4

1A. Case (1)

1.A.4 Fiscal

1 jan 31 dec Average

Equity -450.000 -450.000 1

Total receivables 0 0 0

Loans affiliated parties 15.000.000 15.000.000

Loans non-affiliated parties 5.000.000 5.000.000

Total debts 20.000.000 20.000.000 20.000.000

Total receivables and debts 20.000.000 20.000.000 20.000.000

5

1A. Case (2) 1:3 Ratio1.A.4

Factor 3 multiplied with equity 3

Franchise € 500.000 500.000

Permitted debt 500.003

Too much debt 19.499997

Too much debt in percentage 97,50%

6

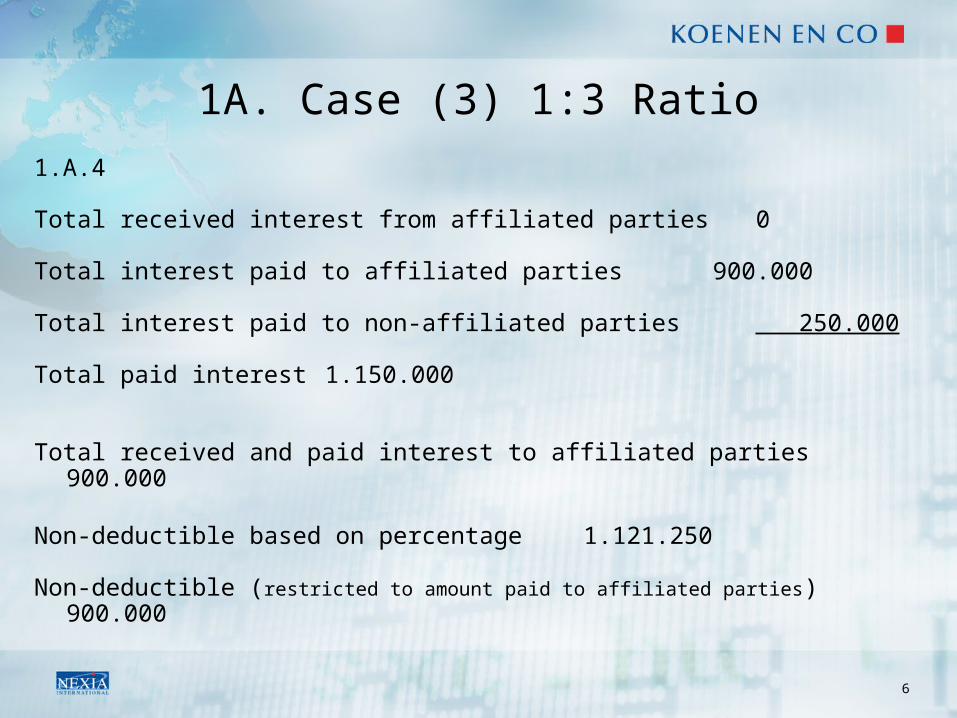

1A. Case (3) 1:3 Ratio

1.A.4

Total received interest from affiliated parties 0

Total interest paid to affiliated parties 900.000

Total interest paid to non-affiliated parties 250.000

Total paid interest 1.150.000

Total received and paid interest to affiliated parties 900.000

Non-deductible based on percentage 1.121.250

Non-deductible (restricted to amount paid to affiliated parties) 900.000

7

1B. Reclassification of loan

1.B Negative equity does not lead to an automatic reclassification of the intercompany loans

8

1C. Deductability of the interest

1.C.1 In the case percentage too much debt is 97,5% but restricted to amount paid to affiliated companies

(in case € 900.000) 1.C.2 No difference between intercompany interest and bank

interest 1.C.3 No standardisation on basis of transfer pricing

principle’s

9

1D. Other interest restrictions

1.D

Loans can (based on case law) qualify as equity instead of debt

Interest on debts which are related to an equity refund or a capital distribution to a related party are not deductible

Restrictions on interest deductibilty on - Interest free (or low interest bearing) loans with long

maturity - loans for the acquisition of own shares

10

1E. Depreciation of the value of the claim

When Parent Company decides to depreciate the value: 1.E No consequences for subsidiary (condition:

depreciation done for business reasons)

11

1F. Waive the loan

Parent Company decides to fully or partial waive the loan 1.F This leads to a profit but a exemption may be be

applicable (waiving the loan only possible if done for business reasons)

12

1G. Conversion of the loan into equity

When Parent-company decides to convert the loan into equity: 1.G No consequences for the subsidiary, except Thin cap

calculation: increasing equity

13

2A. Writing down the loan

2.A Writing down is possible if loan is (partial) deficient due to losses of the subsidiary

2.B Writing down is deductable 2.C Writing down only possible if classified as loan

Important: anti abuse rule if the loan (which is written down) is transfered to related party

14

2B. Waive the loan

2.A.1 Loss leads to a deductable expense 2.B.2 Not relevant whether the loan is already (partial)

written down

15

2C. Conversion of loan into equity

2.C.1 Conversion has no consequences 2.C.2 If it concerns a depreciated loan than anti-abuse rule for

parent-company is applicable: depreciation is added to profit