Knoll, Inc. -...

25

Knoll, Inc. 2008 Investor Presentation Andrew Cogan, CEO Barry McCabe, EVP, CFO

Transcript of Knoll, Inc. -...

Knoll, Inc. 2008 Investor Presentation

Andrew Cogan, CEOBarry McCabe, EVP, CFO

© 20072

DisclaimerThe following information includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements regarding Knoll, Inc.’s expected future financial position, results of operations, cash flows, business strategy, budgets, projected costs, capital expenditures, products, competitive positions, growth opportunities, plans, goals and objectives of management for future operations, as well as statements that include words such as "anticipate," "if," "believe," "plan," "estimate," "expect," "intend," "may," "could," "should," "will," and other similar expressions are forward-looking statements. Such forward-looking statements are inherently uncertain, and readers must recognize that actual results may differ materially from the expectations of Knoll management. Knoll does not undertake a duty to update such forward-looking statements. Factors that may cause actual results to differ materially from those in the forward-looking statements include, without limitation, corporate spending and service-sector employment, price competition, acceptance of Knoll’s new products, the pricing and availability of raw material and components, foreign exchange pressures, transportation costs, demand for high quality, well designed office furniture solutions, changes in the competitive marketplace, changes in the trends in the market for office furniture and other risks identified in Knoll’s Annual Report on Form 10-K and other filings with the Securities and Exchange Commission. Many of these factors are outside of Knoll’s control.

© 20073

For 70 Years, Knoll Has Used Modern Design to Connect People With Their Work, Their Lives and Their World• A product portfolio by prominent, internationally acknowledged architects and designers• Recognized as a design leader with a premier brand identity• Products noted for their high quality and sophisticated aesthetics

Ludwig Mies van der Rohe

Hans andFlorence

Eero Saarinen

Formway Design

FrankGehry

Shelton Mindel

© 20074

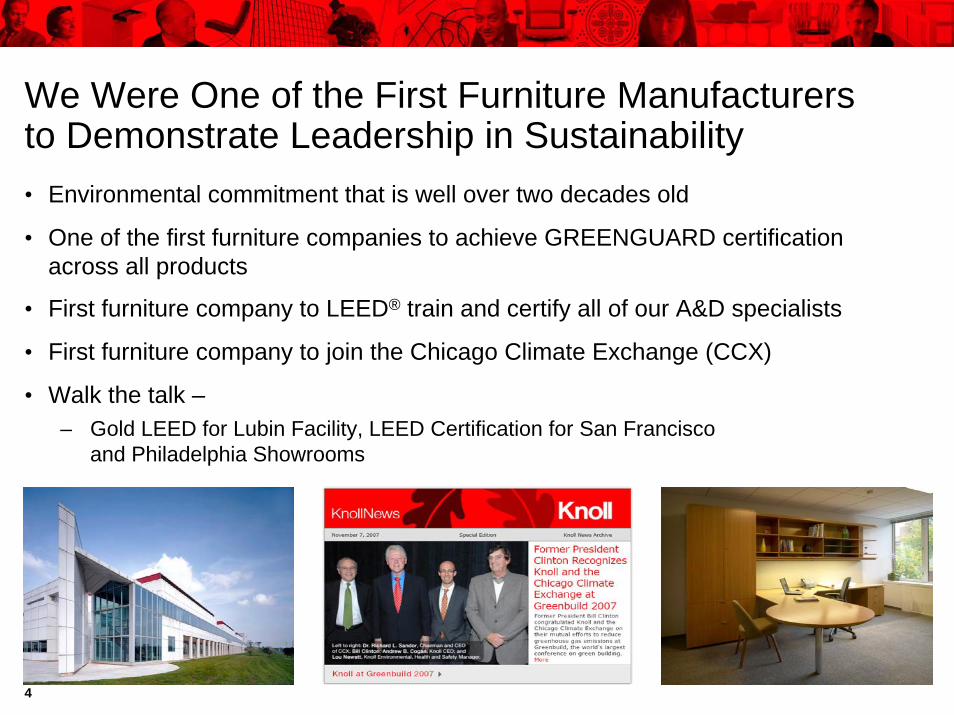

We Were One of the First Furniture Manufacturers to Demonstrate Leadership in Sustainability• Environmental commitment that is well over two decades old

• One of the first furniture companies to achieve GREENGUARD certification across all products

• First furniture company to LEED® train and certify all of our A&D specialists

• First furniture company to join the Chicago Climate Exchange (CCX)

• Walk the talk –– Gold LEED for Lubin Facility, LEED Certification for San Francisco

and Philadelphia Showrooms

© 20075

Premier Brand IdentityKnoll Targets the Middle to Upper End of the Market Where Image, Performance and Customer Service are Key Differentiating Factors

Pric

e R

a nge

High

Mid-High

Mid-Low

Budget

North America Market Share¹ 17.6%14.0% 18.5%8.4%

(1) Based on LTM December 31, 2007 North America or U.S. publicly reported segments as a percent of LTM December 31, 2007 BIFMA U.S. industry shipments.

© 20076

(5)%

0%

5%

10%

15%

20%

25%

2000 2001 2002 2003 2004 2005 2006 2007

Ope

ratin

g M

argi

n

Knoll Herman Miller Steelcase

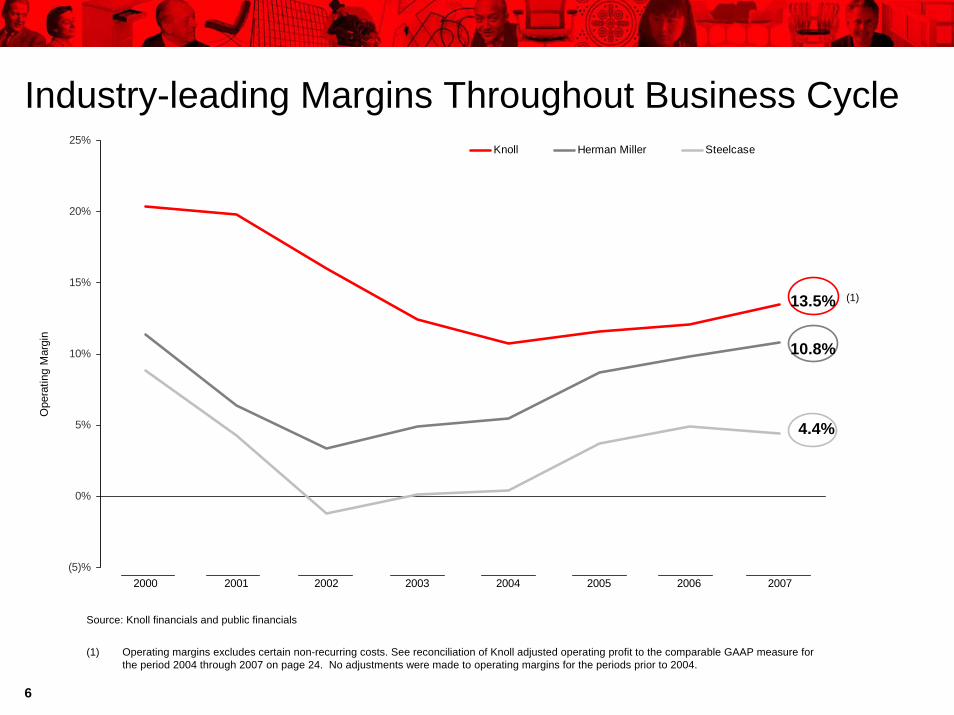

Industry-leading Margins Throughout Business Cycle

Source: Knoll financials and public financials

(1) Operating margins excludes certain non-recurring costs. See reconciliation of Knoll adjusted operating profit to the comparable GAAP measure for the period 2004 through 2007 on page 24. No adjustments were made to operating margins for the periods prior to 2004.

13.5%

10.8%

4.4%

(1)

© 20077

Our Growth from our 2004 IPO through 2007 49.5 % Sales Growth (millions)

$706.4$808.0

$982.2$1,055.8

$0.00

$200.00

$400.00

$600.00

$800.00

$1,000.00

$1,200.00

2004 2005 2006 2007

Knoll Vs BIFMA Growth 2004 through 2007

49.5%

27.8%

0%

10%

20%

30%

40%

50%

60%

Perc

enta

ge S

ales

Incr

ease

(%)

Knoll GrowthBIFMA Growth

Gross Margin

34.1%

33.7%

32.5%

34.6%

31.0%

31.5%

32.0%

32.5%

33.0%

33.5%

34.0%

34.5%

35.0%

2004 2005 2006 2007

Operating Margins Increased 340 Basis Points

10.1%

11.5%11.9%

13.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2004 2005 2006 2007

© 20078

Our Growth from our 2004 IPO through 2007 (cont.)

95% Adjusted EBITDA Growth (2) (millions)

$87.7

$114.6

$142.1

$170.9

$-

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

$160.0

$180.0

2004 2005 2006 2007

Leverage Ratio (3)4.48

2.762.46

2.18

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2004 2005 2006 2007

123% Adjusted EPS Growth (1)

$0.66

$0.80

$1.17

$1.47

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

2004 2005 2006 2007

Debt Level $ (millions)

$392.90

$316.00

$350.30$368.60

$0.00

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

$450.00

12/31/2004 12/31/2005 12/31/2006 12/31/2007

(1) Adjusted EPS exclude certain non-recurring costs. For a reconciliation of these non-GAAP measures to the comparable GAAP measure, see page 24.

(2) For details of the EBITDA calculation, including a reconciliation of EBITDA to GAAP Net Income, see “Leverage Ratio” on page 25.

(3) Leverage Ratio is calculated by dividing the outstanding debt by EBITDA. For details of the leverage ratio calculation, see page 25.

© 20079

Free Cash Flow (thousands) (1)

$35,552

$48,564

$69,632

$82,312

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2004 2005 2006 2007

FREE CASH FLOW

Cash Returned to Shareholders $ (2)

$15,956

$128,627

$70,420

$0.00

$20,000.00

$40,000.00

$60,000.00

$80,000.00

$100,000.00

$120,000.00

$140,000.00

2005 2006 2007

Diluted Weighted Average Shares (millions)

48.3

52.9

51.2

49.2

48.0

49.0

50.0

51.0

52.0

53.0

54.0

12/04 12/05 12/06 12/07

Debt Levels $316 $332 $324 $375 $350 $329$357

125% Dividend Growth $

$0.20

$0.25

$0.41

$0.45

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

$0.50

2004 2005 2006 2007

Our Growth from our 2004 IPO through 2007 (cont.)

(1) Free Cash Flow is defined as Net Income plus depreciation and amortization and non-cash stock compensation less capital expenditures. For details of the free cash flow calculation, see page 25.

(2) Cash returned to shareholders includes dividends paid and shares repurchased.

© 200710

Trends We Watch

-1000

-500

0

500

1000

1500

1991 1993 1995 1997 1999 2001 2003 2005 2007

American Institute of Architects Billings Index

40

50

60

2000 2001 2002 2003 2004 2005 2006 March2007

June2007

Sept.2007

Dec.2007

Inde

x

Absorption and Vacancy Rates

(40)

(30)

(20)

(10)

-

10

20

30

40

Net

Abs

orpt

ion

(mill

ions

sq.

ft.)

7.5%

10.0%

12.5%

15.0%

17.5%

20.0%

% Vacancy

Net Absorption Vacancy %

2002 2003 2004 2005 2006 20071997 1998 1999 2000

Billings Index = The nine to twelve months lag between architecture billings and construction spending

Change In Office Employment

BIFMA Shipments 1980 -2008F

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 0708

(F)

x

Ship

men

ts -

mill

ions

of U

S$

$8.9

0$1

0.98

$8.5

1

$3.3

3$3

.75

$4.1

5$4

.56

$5.7

4$6

.41

$6.6

8

$7.3

3$7

.45

$7.8

3$7

.86

$7.7

1

$8.1

6$8

.85

$9.4

4$1

0.04

$11.

46

$12.

35

8.5%12.6%10.7%

9.8%

25.9%

11.8%4.1%

9.8% 1.7%5.1%0.4%

-8.1%

6.7% 5.8%

8.5%6.6%

6.4%

14.1%

7.8% -0.9%

8.5%

-17.4%

-19.0%-4.3%

$7.2

3

$12.

24

$13.

28

$8.9

4

5.1%

12.7%

$10.

1

7.4%

$10.

8

5.5%

$11.

4

-0.90%

$11.

3

Source: Grubb & Ellis Source: BIFMA

Source: American institute of Architects Billings indexSource: McGraw Hill Construction

© 200711

Growth Strategy • Leverage our leading Office System offerings to capture market share in

underpenetrated seating, storage and casegoods categories.

• Drive high margin high growth Specialty businesses through expanded product offerings, distribution channels and sales and marketing programs.

• Increase International presence and results.

• Position Knoll as the supplier of choice for companies seeking to attract the next generation of office workers by creating dynamic workplaces that respond to emerging workstyles and trends.

© 200712

We Still Have Significant Market Share Opportunity in Underpenetrated Categories

$75m

28%26%

20%

12%

18%

4% 3%

1%0

5

10

15

20

25

30

Office Systems Seating Storage Casegoods

Cat

egor

y Sh

are

(%)2

Category Share of Total Industry Shipments¹Knoll Category Share

$3,117

$552

$2,948

$114

$2,273

$81

$1,306

+$300 M

1. Percent of LTM 9/30/07 industry shipments of $11.3 billion, as reported by BIFMA2. As of LTM 9/30/07

© 200713

Today approximately 98% of Our Sales Come from Less Than 50% of the Global Market

¹ EstimateMarket Opportunity North AmericaMarket Opportunity Knoll EuropeMarket Opportunity Knoll International

$10.9B(1)

$6.4B(1)

$15.0B(1)

Knoll North America8.41%

Knoll International

0.15%

Knoll Europe1.05%

Implementing a Geographic Segmentation of the Business to Raise Visibility and Focus on $15BInternational Opportunity

(1)

© 200714

We Are Building a Design-driven Portfolio Less Dependent on NA Office Cycles• Significantly Decreased Exposure

to Office Systems Category

• Strengthened and Expanded Complimentary Seating, Storage, and Casegood Offerings

• Aggressively Increased Specialty Sales, Distribution, and Marketing Efforts

• Acquired Edelman Leather our 5th

Specialty Business

68%

12% 13%

7%

53%

19% 19%

10%

0

10

20

30

40

50

60

70

80

Office Systems Complimentary Specialty Europe/International

Cat

egor

y Sh

are

(%)2

% Sales YTD December 31, 2000% Sales YTD December 31, 2007

© 200715

Engaged Leading Design Talent Around the Globe to Address the Needs of the Modern Workplace and Home Just as Hans and Florence Did 70 Years Ago

© 2007

Financial Performance

© 200717

Contribution Margin Shows Good ProgressKNOLL, INC.YTD 2007

DECEMBER, YEAR TO DATE2007 2006 VARIANCE

SALES 1,055,814 982,152 73,662% YEAR OVER YEAR GROWTH 7.5% 21.6%

COST OF GOODS SOLD 690,689 663,115 27,574

GROSS MARGIN 365,125 319,037 46,08834.6% 32.5% 2.1 PTS

CONTRIBUTION MARGIN 62.6%

OPERATING EXPENSES 222,937 202,097 20,84021.1% 20.6% 0.5 PTS

ADJ OPERATING PROFIT (1) 142,188 118,440 23,74813.5% 12.1% 1.4 PTS

CONTRIBUTION MARGIN 32.2%

ADJ EARNINGS PER SHARE (1) $1.47 $1.17 $0.30% GROWTH 25.6% 46.3%

(1) Adjusted operating profit and adjusted EPS exclude certain non-recurring costs. For a reconciliation of these non-GAAP measures to the comparable GAAP measure, see page 24.

© 200718

We Have Made Excellent Progress Towards Our Mid-term Goal of Achieving 35% Gross Margins

GM as a % of Sales

34.1%

33.7%

34.1%34.3%

34.7%

35.1%

32.5%

31.0%

31.5%

32.0%

32.5%

33.0%

33.5%

34.0%

34.5%

35.0%

35.5%

2004 2005 2006

• Pricing– Realizing price and stabilizing

discount

• Global Sourcing– Expanding opportunities

• Factory Initiatives– Absorption and efficiencies improving

• Inflation– Moderating

Q107

• Fuel Costs• Foreign Exchange

– Canadian dollar strengthening

POSITIVES NEGATIVES

Q207 Q307 Q407

© 200719

And to Our Goal of Achieving 15% Operating Margins

10.7%11.6%

12.4%

13.8% 13.5% 14.0%

12.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2004 2005 Q1072006

• Continue Leveraging Our SG&A

– Selectively invest in our support infrastructure

– Where possible, keep costs variable

– Keep SG&A at 21-22% of sales

Q207 Q307 Q407

Adjusted Operating Margins as a % of Sales

(1) Adjusted operating margins exclude certain non-recurring costs. For a reconciliation of adjusted operating profit to the comparable GAAP measure, see page 24. No adjustments were made to operating margins for the periods of 2007.

(1)

© 200720

5%

18%19%

20%

16%

12%

10%12% 12% 12%

14% 14%14%

17%

20%

0%

6%

13%

19%

25%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Q107 Q207 Q307 Q407

Our Margin Performance is Approaching its Historical Average

Adjusted Operating Margins(1) Adjusted Operating margins exclude certain non-recurring costs. For a reconciliation of adjusted operating profit to the comparable GAAP measure for the periods 2004 through 2007 see

page 24. No adjustments were made to operating margins for the periods prior to 2004.

1996–2006 Avg.: 15%

(1)

© 200721

Allocation of Free Cash Flow• Invest in Focused Initiatives to Drive Top-line

Growth and Improve Margins– Complementary acquisitions

– New and enhanced products

– Look at factory machinery and equipment for efficiencies and cost improvements

• Pay Dividends to Shareholders

• Share Repurchase (8.5 million shares since December 2004)

• Target 2.0 – 2.5x Debt / EBITDA

© 200722

Thank You

www.knoll.com

© 200723

Reconciliation of Adjusted EPS 2004 through 2007

2004 2005 2006 2007Earnings per Share - Diluted 0.55$ 0.68$ 1.14$ 1.45$

Add back: Write off of deferred financing fees 0.03 0.05 - 0.02 Public offering expense 0.08 - 0.03 - Restructuring charges - 0.01 - - Taxes related to repatriation of foreign earnings - 0.06 - -

Adjusted Earnings per Share Diluted 0.66$ 0.80$ 1.17$ 1.47$

© 200724

Reconciliation of Adjusted Operating Profit and Adjusted Earnings per Share

FY 2007 FY 2006 FY 2005 FY 2004

Operating Profit ($mm) 142.2$ 116.9$ 92.8$ 71.3$

Add back:

Restructuring charges - - 0.8 - Public offering expenses - 1.5 (1) - 4.4

Adjusted Operating Profit 142.2$ 118.4$ 93.6$ 75.7$

Net Sales 1,055.8$ 982.2$ 808.0$ 706.4$

Operating Margin 13.5% 12.1% 11.6% 10.7%

Earnings per Share (Diluted) 1.45$ 1.14$ 0.68$ 0.55$

Add back:

Restructuring charges - - 0.01 - Public offering expenses - 0.03 - 0.08 Write-off of deferred financing fees 0.02 - 0.05 0.03 Taxes related to repatriation of foreign earnings - - 0.06 -

Adjusted Earnings per Share 1.47$ 1.17$ 0.80$ 0.66$

(1) Includes costs associated with our two secondary stock offerings, the buyback of 3.9mm shares from Warburg Pincusand fees incurred in connection with the amendment of our credit facility.

© 200725

2004 2005 2006 2007

Net Income 26,744$ 35,909$ 58,633$ 71,443$

Add: Depreciation 20,080 18,721 19,194 19,655

Amortization 1,692 626 663 1,604

Stock compensation expense 167 4,052 4,504 5,902

Less:

Capital expenditures (13,131) (10,744) (13,362) (16,292)

Free Cash Flow 35,552$ 48,564$ 69,632$ 82,312$

( in t ho usand s)

(1) Non-recurring costs include public offering expenses, write-off of deferred financing fees, restructuring charges and additionaltaxes from the repatriation of foreign earnings

(2) Non cash items include stock compensation expense, unrealized gains/losses on derivatives and the write-off of deferred financing fees

(3) Includes an annualized proforma EBITDA for Edelman Leather, which was acquired on October 1, 2007.

12/31/04 12/31/05 12/31/06 12/31/2007

Debt Levels 392.9$ 316.0$ 350.0$ 368.6$

LTM Net Income ($mm) 26.7$ 35.9$ 58.7$ 71.4$ LTM Adjustments

Interest 19.5 23.7 23.7 24.6

Taxes 19.8 27.9 35.4 41.4

Depreciation and Amortization 20.0 18.7 19.2 21.3

Non-cash items(2) 1.7 8.4 5.1 12.2 (3)

LTM EBITDA 87.7$ 114.6$ 142.1$ 170.9$

Leverage Ratio 4.48 2.76 2.46 2.18

Free Cash Flow Leverage Ratio