Kingspan Interim Results 22nd August 2011

30

Kingspan Interim Results 22 nd August 2011

Transcript of Kingspan Interim Results 22nd August 2011

Kingspan Interim Results 22nd August 2011

Disclaimer

Forward Looking Statements This presentation contains certain forward-looking statements. Actual results may differ materially from those projected or implied in such forward-looking statements. Such forward-looking information involves risks and uncertainties that could affect expected results.

2

Full Year Results 2010 28th February 2011

2011 Interim Management Report

Key Highlights Gene Murtagh CEO

Financial Review Geoff Doherty CFO

Business Review Gene Murtagh CEO

Strategy & Outlook Gene Murtagh CEO

Q&A 3

Revenue up 32% to €736m

Trading Profit up 24% to €44.2m

Insulated Panels divisional sales up 22% with growth across all key regions

Insulation Boards divisional sales up 86%, or up 14% excluding the acquisition of CIE, with increased geographic balance following the acquisition

Environmental & Renewables divisional sales up 17% reflecting buoyant European sales

Access Floors divisional sales down 5% overall with strong datacentre volumes partially offsetting a decrease in office activity

Raw material inflation of approximately €40m in H1 2011 with recovery effort fully on track

Key development highlight was acquisition and integration of CIE in the period

Excellent headway on R&D initiatives, notably Powerpanel ® and Next Generation Insulation

Continuing progress demonstrated across the Group on its conversion agenda

4

Key Highlights

5

2011 Interim Management Statement

FINANCIAL REVIEW

Financial Highlights

6

Revenue €736.0m +32% +16% like-for-like*

Trading Profit** €44.2m +24% +17% like-for-like*

Trading Margin 6.0% -0.4%

Profit after tax €29.2m +37%

Basic EPS 17.3c +38%

Free cash flow €32.4m +13%

* Like-for-like comparisons exclude the impact of the CIE acquisition and currency movements ** Pre-intangible amortisation

€32.4m Interim dividend 4.5c +12.5%

0

100

200

300

400

500

600

700

800

Revenue H1 10 Currency Volume Price/Mix Acquisition Revenue H1 11

558.7

736.0

0.6

55.5

36.7

85.7 €

m

7

Sales Bridge

Margin %

H1 11 H1 10 FY 10

Insulated Panels 6.2% 4.8% 5.6%

Insulation Boards 6.5% 9.0% 6.7%

Environmental & Renewables 1.2% 1.1% 0.5%

Access Floors 10.4% 15.0% 13.8%

Group 6.0% 6.4% 6.0%

8

Trading Profit Growth

0.0

0.0

0.0

0.0

0.0

0.1

H1 2010 H1 2011

35.7

44.2

€m

Trading Profit

9

Trading Profit* Bridge

0.0

10.0

20.0

30.0

40.0

50.0

60.0

EBIT H1 10 Currency Volume Margin Operatingcosts

Acquisition EBIT H1 11

35.7

44.2

17.4

0.1

15.6

7.8

2.4

€m

* Pre- intangible amortisation

H1 2011 Trading Profit: Like-for-like % growth

10

Like-for-like growth

Acquisitions/ disposals

Reporting Currency

Reported Growth

Insulated Panels +56.9% - +1.5% +58.4%

Insulation Boards +11.4% +23.1% +1.0% +35.5%

Environmental & Renewables +19.4% - +0.6% +20.0%

Access Floors -31.4% - -2.6% -34.0%

Group +16.6% +6.9% +0.3% +23.8%

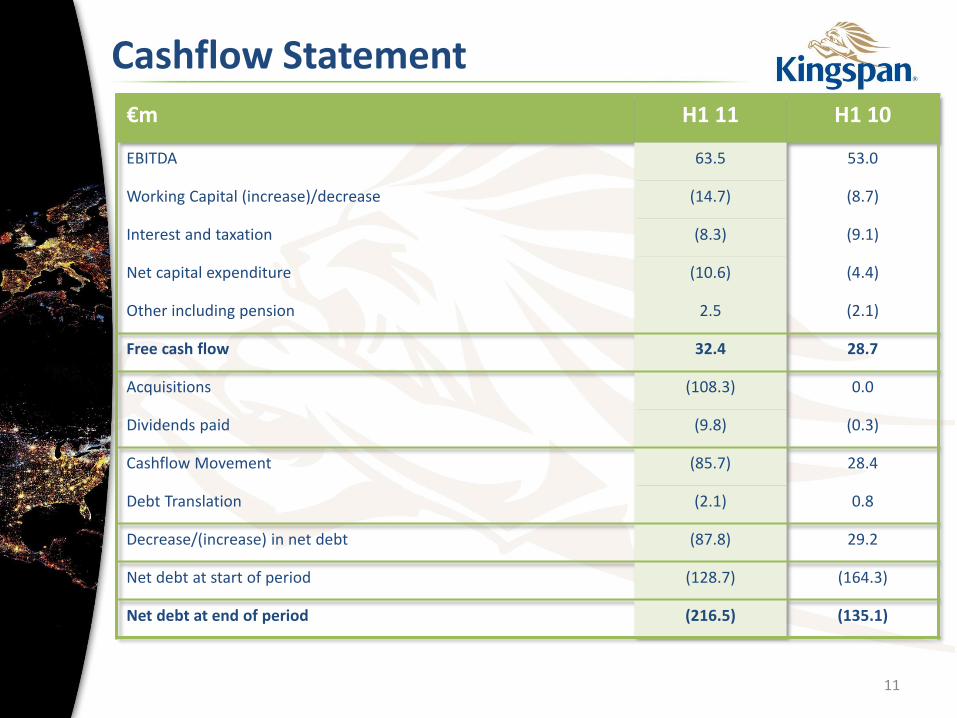

€m H1 11 H1 10

EBITDA 63.5 53.0

Working Capital (increase)/decrease (14.7) (8.7)

Interest and taxation (8.3) (9.1)

Net capital expenditure (10.6) (4.4)

Other including pension 2.5 (2.1)

Free cash flow 32.4 28.7

Acquisitions (108.3) 0.0

Dividends paid (9.8) (0.3)

Cashflow Movement (85.7) 28.4

Debt Translation (2.1) 0.8

Decrease/(increase) in net debt (87.8) 29.2

Net debt at start of period (128.7) (164.3)

Net debt at end of period (216.5) (135.1)

11

Cashflow Statement

Key Ratios

12

Key Ratios H1 11 H1 10 FY 10

Gearing (Net Debt: Shareholders Funds) 32.1% 20.8% 19.3%

Net Debt/EBITDA 1.83 1.28 1.2

Interest Cover 12.2 10.5 11.9

ROCE 9.1% 8.4% 8.4%

Working Capital as % of Sales 12.5% 12.1% 12.8%

H1 2011 Net Debt €216.5m – headroom c. €434m

Revolving Credit Facility of €330m

2005 Private placement €151mn (USD200m)

2011 Private placement €139m (USD200m)

Significant headroom on covenants

Max 3.5x net debt:EBITDA; actual 1.83 x

Min 4.0x interest cover; actual 12.2 x

Weighted average maturity of net debt of 5.5 years post August 2011 Private Placement

13

Debt Facilities

0

50

100

150

200

250

300

350

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

330

119

32

139

Profile of Available Facilities €m

RCF Private Placement

14

2011 Interim Management Statement

BUSINESS REVIEW & OUTLOOK

€mn H1 11 H1 10 % Change at Constant

Rates

YoY % Change

Republic of Ireland 36.2 32.4 +12% +12%

Britain & Northern Ireland 308.1 248.5 +24% +24%

Mainland Europe 258.6 147.6 +75% +75%

Americas 100.0 93.9 +11% +6%

Australasia 27.1 22.0 +13% +23%

Other 6.0 14.3 -59% -58%

Group Sales 736.0 558.7 +32% +32%

6%

44%

26%

17%

4% 3%

H1 2010

Republic of Ireland Britain & Northern Ireland

Mainland Europe Americas

Australasia Other

5%

42%

35%

13%

4% 1%

H1 2011

15

Sales by Geography

€m H1 11 H1 10 % Change at Constant

Rates

YoY % Change

Insulated Panels 350.4 287.0 +22% +22%

Insulation Boards 222.6 119.9 +85% +86%

Environmental & Renewables 97.9 83.4 +17% +17%

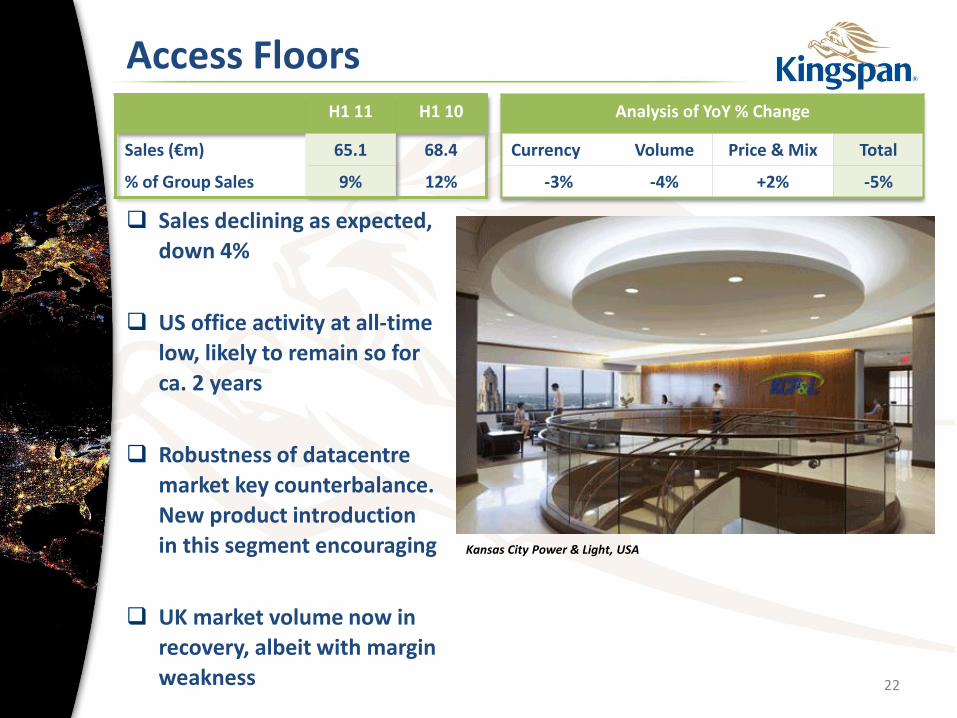

Access Floors 65.1 68.4 -2% -5%

Group Sales 736.0 558.7 +32% +32%

0

50

100

150

200

250

300

350

400

Insulated Panels Insulation Environmental &Renewables

Access Floors

€’m

n

H1 2011

H1 2010

16

Sales by Product Group

Strong volume growth in all markets

UK +16%

Benelux +7%

Ireland +8%

Australia/NZ +52%

Order intake positive, up 8% across the business unit

Raw material recovery on track

Powerpanel® launch

Progress on Benchmark® architectural panels

H1 11 H1 10

Sales (€m) 201.0 160.1

% of Group Sales 28% 29%

Analysis of YoY % Change

Currency Volume Price & Mix Total

+1% +16% +9% +26%

17

Insulated Panels UK, IRL, WE

Abbertay University, Dundee, UK

Mixed sales pattern across the territory but strong volume growth overall

Germany +13%

Turkey +40%

Poland -21%

Czech -8%

Order intake positive overall

Up 9%

Good progress in Russia

H1 11 H1 10

Sales (€m) 88.5 73.7

% of Group Sales 12% 13%

Analysis of YoY % Change

Currency Volume Price & Mix Total

+1% +13% +6% +20%

Note: The above figures include Germany and Turkey

18

Insulated Panels CEMEI

Interfruct C&C food warehouse, Budapest, Hungary

Robust volume growth in H1

US +5%

Canada +14%

Overall Order Intake -8%

Commercial and Industrial volumes strong

Coldstore volumes strong but margin pressure

Architectural disappointing sales but strong intake

US/Canada integration working very well

H1 11 H1 10

Sales (€m) 60.9 53.2

% of Group Sales 8% 10%

Analysis of YoY % Change

Currency Volume Price & Mix Total

-4% +7% +12% +15%

19

Insulated Panels North America

Print Innovators, Fredricksberg, Virginia, USA

CIE integration on track, WE strong in PIR

Robust underlying performance in UK & WE

Chemical increases a significant challenge. Recovery underway and ongoing in Q3

Phenolic conversion on track in all markets

Australia/New Zealand solid performance and improving through Q2

H1 11 H1 10

Sales (€m) 222.6 119.9

% of Group Sales 30% 21%

Analysis of YoY % Change

Currency Volume Price & Mix Acquisition Total

+1% +4% +9% +72% +86%

ExCel, London, UK

20

Insulation

Solid performance

throughout the business

unit

Continental Europe

strong, particularly

France

Solarthermal growth in

UK, US & Ireland.

Borealis case complete.

Ruling expected Jan 2012

H1 11 H1 10

Sales (€m) 97.9 83.4

% of Group Sales 13% 15%

Analysis of YoY % Change

Currency Volume, Price & Mix Total

0% +17% +17%

21

Environmental & Renewables

George Washington University, Washington DC, USA

Sales declining as expected,

down 4%

US office activity at all-time

low, likely to remain so for

ca. 2 years

Robustness of datacentre

market key counterbalance.

New product introduction

in this segment encouraging

UK market volume now in

recovery, albeit with margin

weakness

H1 11 H1 10

Sales (€m) 65.1 68.4

% of Group Sales 9% 12%

Analysis of YoY % Change

Currency Volume Price & Mix Total

-3% -4% +2% -5%

22

Access Floors

Kansas City Power & Light, USA

23

Strategy

Drive conversion to high

performance solutions

Increase penetration

Extend and develop new territories

Continuous R&D e.g. Powerpanel®

Capitalise NetZero energy → a

significant and tangible opportunity

for building occupiers over time

aided by Kingspan solutions

Haletra, The Netherlands

Orderbook likely to support a favourable H2 in most markets

Pace of growth eased in Q2 and likely to moderate further in H2

Raw material cost stability for H2, reductions are a possibility

Uncertain global macro environment

24

Outlook

Indescon Court, UK

25

2011 Interim Management Statement

ADDITIONAL INFORMATION

Trends in Thermal Regulations

26

This graph shows the permitted consumption of energy in KW/H per m2 of domestic dwelling space and its historic and planned evolution, as a percentage of the permitted 2000 levels.

28

Performance vs Construction Macro’s US Panels

Growth in penetration *Source: McGraw Hill Construction

29

Performance vs Construction Macro’s UK Insulation

“Conversion” enabling out-performance

Penetration Potential

2005A 2010A 2015F

Insulated Panels UK 55% 62% 75%

Insulated Panels NA 5% 8% 11%

UK Insulation 30% 34% 38%

Germany External Wall 0% 2% 10%

CEE Insulation Board 0% 0.7% 6%

30

General improvement in UK residential and low rise commercial likely to continue in the near term. Office construction anticipated to fall further, and state-funded projects will decline

Insulated Panels and Insulation expect solid H12011, stable in the UK, growth in Mainland Europe and North America

Growth in refurbishment globally. Many exciting initiatives, including the UK’s “Green Deal”

Rising steel prices and contracting Access Floors activity will present margin challenges across the Group through 2011

Outlook

31