Key results from the survey on organic agriculture worldwide 2011 Part 3: Organic agriculture in the...

73

Key results from the survey on organic agriculture worldwide 2011 Part 3: Organic agriculture in the regions 2009 Research Institute of Organic Agriculture FiBL, Frick, Switzerland, in cooperation with the International Federation of Organic Agriculture Movements IFOAM Supported by: Swiss State Secretariat of Economic Affairs, International Trade Centre, NürnbergMesse Data as published February 2011 in The World of Organic Agriculture. Statistics and Emerging Trends 2011 For updates check www.organic-world.net Contact: Helga Willer, Research Institute of Organic Agriculture, FiBL, Frick, Switzerland, [email protected] £http://www.organic-world.net/presentations-2011.html Version: 30.5.2011

-

Upload

eleanor-morris -

Category

Documents

-

view

215 -

download

0

Transcript of Key results from the survey on organic agriculture worldwide 2011 Part 3: Organic agriculture in the...

Key results from the survey on organic agriculture worldwide 2011 Part 3: Organic agriculture in the regions 2009

Research Institute of Organic Agriculture FiBL, Frick, Switzerland, in cooperation with the International Federation of Organic Agriculture Movements IFOAM

Supported by: Swiss State Secretariat of Economic Affairs, International Trade Centre, NürnbergMesse

Data as published February 2011 in The World of Organic Agriculture. Statistics and Emerging Trends 2011For updates check www.organic-world.net

Contact: Helga Willer, Research Institute of Organic Agriculture, FiBL, Frick, Switzerland, [email protected]£http://www.organic-world.net/presentations-2011.html

Version: 30.5.2011

www.fibl.org

The Global Survey on Organic Agriculture: Supporters

› International Trade Centre, Geneva

› The Swiss State Secretariat of Economic Affairs SECO, Berne

› Nürnberg Messe, the organizers of the BioFach Organic Trade Fair

www.fibl.org

The World of Organic Agriculture 2011

› The 12th edition of ‚The World of Organic Agriculture‘, was published by FiBL and IFOAM in February 2011.*

› Contents:› Results of the survey on organic agriculture

worldwide;› Organic agriculture in the regions and country

reports;› Armenia, Australia, Canada, Chile, China,

Costa Rica, Indonesia, Kazakhstan, Republic of Korea, Pacific Islands, Switzerland, Tunisia, Uganda, United States and Ukraine.

› Chapters on the global market, standards & legislations, voluntary standards and organic beekeeping

› Numerous tables and graphs. › The book can be ordered via IFOAM.org and

shop.FiBL.org. › *Willer, H, and Kilcher, L. (2011) The World of

Organic Agriculture. Statistics and Emerging Trends 2011. IFOAM, Bonn, and FiBL, Frick

www.fibl.org

Website www.organic-world.net

› Detailed statistics in excel format (in progress)

› Graphs & Maps› Data revisions› News and

background information

www.fibl.org

About this presentation

› This presentations summarizes the key results of the FiBL/IFOAM survey on organic agriculture worldwide 2011 (data 2009). In addition key results on crop and on regional data are presented.

› More information is available at the password area of www.organic-world.net

› The presentations has 4 main chapters:1. Data background and key data on organic agriculture: Land,

producers, market data 2009

2. Organic agriculture in developing countries 2009

3. Land use and key crops in organic agriculture 2009

4. Organic agriculture in the regions

www.fibl.org

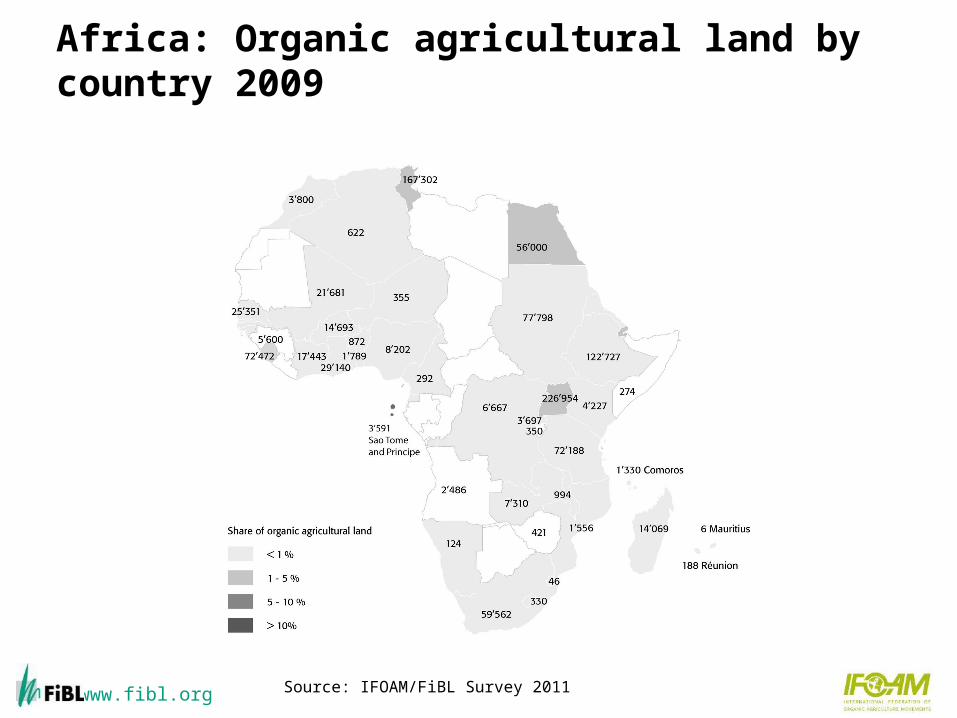

Africa: Organic agricultural land by country 2009

Source: IFOAM/FiBL Survey 2011

www.fibl.org

Organic agriculture in Africa 2009

› In Africa, there are slightly more than one million hectares of certified organic agricultural land (data 2009).

› This constitutes about three percent of the world’s organic agricultural land.

› 500’000 producers were reported. › The countries with the most organic land are Uganda (226'954

hectares), Tunisia (167'302 hectares), and Ethiopia (122'727 hectares). › The highest shares of organic land are in Sao Tome and Prince (6.5

percent), Sierra Leone (1.8 percent), and Uganda (1.7 percent). › The majority of certified organic produce in Africa is destined for export

markets; in Uganda the export value for organic products was 37 million US dollars in 2009/2010.

› The European Union, as the major recipient of these exports, is Africa’s largest market for agricultural produce. Tunisia was accepted under the EU’s Third Country List in 2009.

Source: IFOAM/FiBL Survey 2011

www.fibl.org

Africa: Development of organic agricultural land 1999-2009

0.23 0.

32 0.36

0.52

0.49

0.68

0.86

0.86

1.03

0.05

0.05

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Hec

tare

s

Source: IFOAM, FiBL and SOEL, surveys 2000-2011

www.fibl.org

Africa: The ten countries with the most organic agricultural land 2009

25'351

29'140

56'000

59'562

72'188

72'472

77'798

122'727

167'302

226'954

0 100'000 200'000

Senegal

Ghana

Egypt

South Africa

Tanzania, United Republic of

Sierra Leone

Sudan

Ethiopia

Tunisia

Uganda

Hectares

IFOAM/FiBL Survey 2011, based on data from governments, the private organic sector and certifiers

www.fibl.org

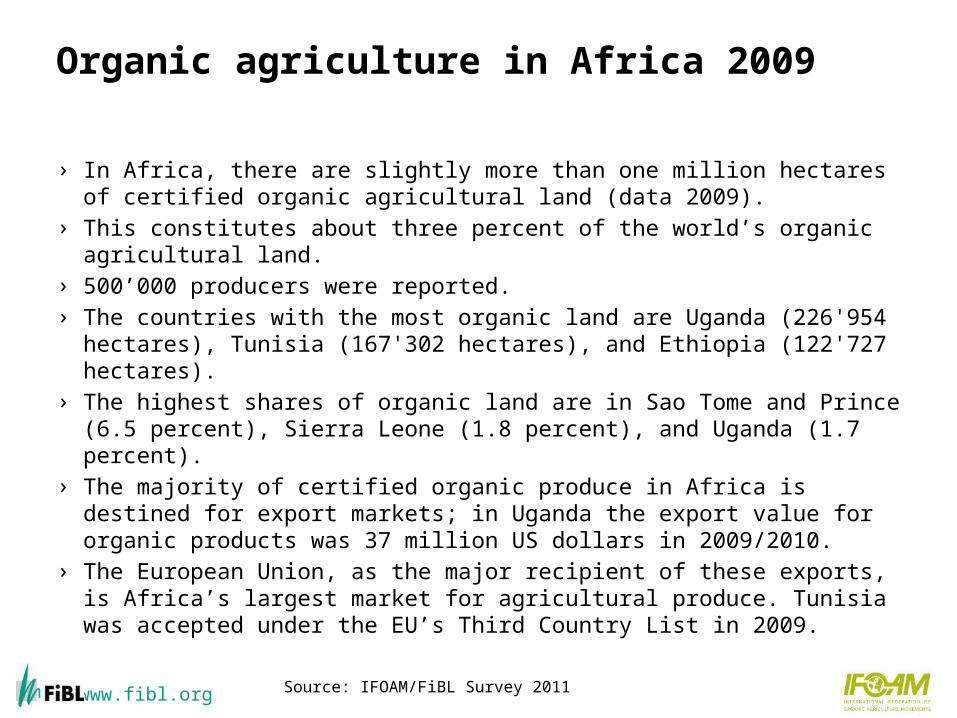

Africa: Distribution of organically managed agricultural land by country 2009 (total: 1.03 mio ha)

22%

16%

12%

50%

Uganda

Tunisia

Ethiopia

Rest

IFOAM/FiBL Survey 2011, based on data from governments, the private organic sector and certifiers

www.fibl.org

Africa: The ten countries with the highest shares of organic agricultural land 2009

0.2%

0.3%

0.4%

0.5%

0.9%

1.6%

1.7%

1.7%

1.8%

6.5%

0% 1% 2% 3% 4% 5% 6% 7%

Tanzania, United Republic of

Senegal

Ethiopia

Réunion (France)

Comoros

Egypt

Tunisia

Uganda

Sierra Leone

Sao Tome and Principe

IFOAM/FiBL Survey 2011, based on data from governments, the private organic sector and certifiers

www.fibl.org

Africa: Distribution of shares of organic land 2009

2%10%

88%

Countries with 5.0 to9.9 % organic land

Countries with 1 to4.9 % organic land

Countries with lessthan 1 % organicland

Source: FiBL/IFOAM Survey 2011

www.fibl.org

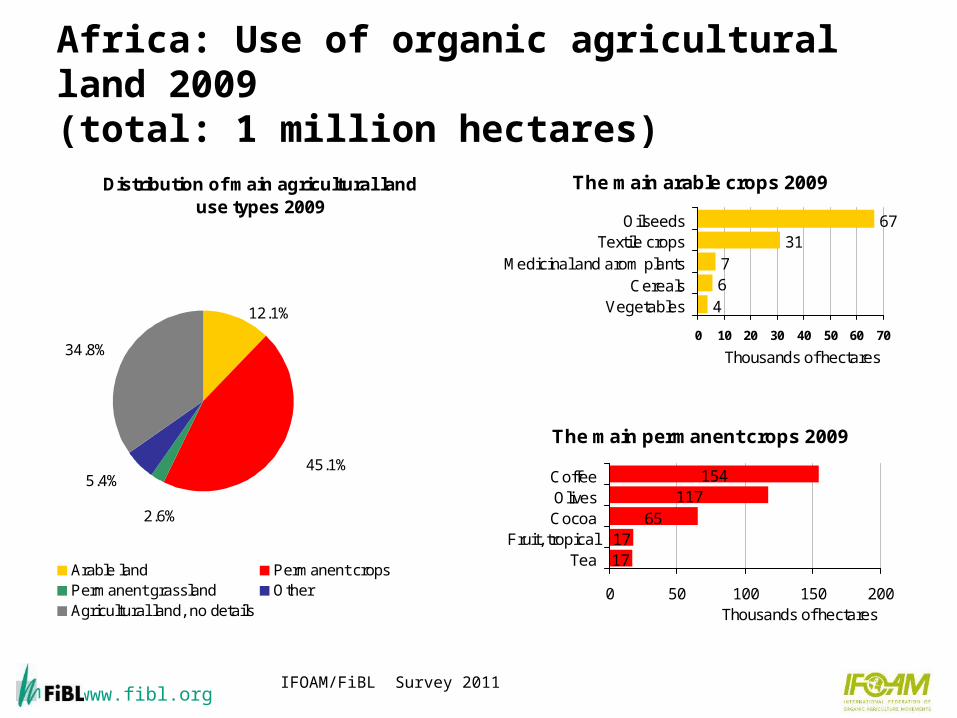

Africa: Use of organic agricultural land 2009 (total: 1 million hectares)

Distribution of main agricultural land use types 2009

12.1%

2.6%

45.1%5.4%

34.8%

Arable land Permanent cropsPermanent grassland OtherAgricultural land, no details

The main arable crops 2009

467

3167

0 10 20 30 40 50 60 70

VegetablesCereals

Medicinal and arom plantsTextile crops

Oilseeds

Thousands of hectares

The main permanent crops 2009

1717

65117

154

0 50 100 150 200

TeaFruit, tropical

CocoaOlivesCoffee

Thousands of hectares

IFOAM/FiBL Survey 2011

www.fibl.org

Articles about Africa in the 2011 Edition of "The World of Organic Agriculture"

› Organic Farming in Africa Hervé Bouagnimbeck

› Tunisia: Country Report Lukas Kilcher and Samia Maamer Belkhiria

› Uganda: Country Report Charity Namuwoza and Hedwig Tushemerirwe

14

www.fibl.org

Asia: Organic agricultural land by country 2009

Source: FiBL/IFOAM Survey 2011, based on national sources

www.fibl.org

Organic Agriculture in Asia – Key Figures 2009

› The total organic agricultural area in Asia is nearly 3.6 million hectares.

› This constitutes ten percent of the world’s organic agricultural land.

› There were 731'315 producers reported. › The leading countries by area are China (1.9 million

hectares) and India (1.2 million hectares). › Timor-Leste has the most organic agricultural area as a

proportion of total agricultural land (almost seven percent).

16

www.fibl.org

Organic Agriculture in Asia – Key Figures 2009

› The region hosts a wide range of organic sector development scenarios, from early development to highly regulated. Far from the marginal position it held previously, organic is now an accepted concept and growing market trend in the region.

› Whilst export remains the dominant feature of sector development in the majority of developing countries in the region, local markets have emerged and are gaining ground.

› Primarily a market driven sector, government policy is an emerging and significant sector development factor today in many countries. Although domestic market size is still relatively small, the high value and profile associated with organic has led to civil society (consumer) calls and governments’ interest to regulate the sector. Seven markets have implementedorganic labeling regulations (i.e., China, India, Japan, South Korea, Philippines, Taiwan, and Malaysia). Others, Sri Lanka and Nepal have established government competent authorities.

› A major event— The 17th IFOAM Organic World Congress —will be held in Korea in autumn 2011.

17

www.fibl.org

Asia: Development of organic agricultural land 2000-2009

47.9%48.1%

4.0%

Europe North America

Others

Source: FiBL /IFOAM Survey 2011The increase of organic agricultural land in 2004 is due to a major expansion in China, partly due to government support. Much of these areas were grazing areas which, however, ceased to be certified in 2005, hence the drop of the organic agricultural area in Asia in that year.

www.fibl.org

Asia: Distribution of organic agricultural land by country 2009; total: 3.6 million hectares

51%

33%

12%

4%

China

India

Kazakhstan

Others

FiBL/IFOAM Survey 2011, based on data from governments, the private organic sector and certifiers

www.fibl.org

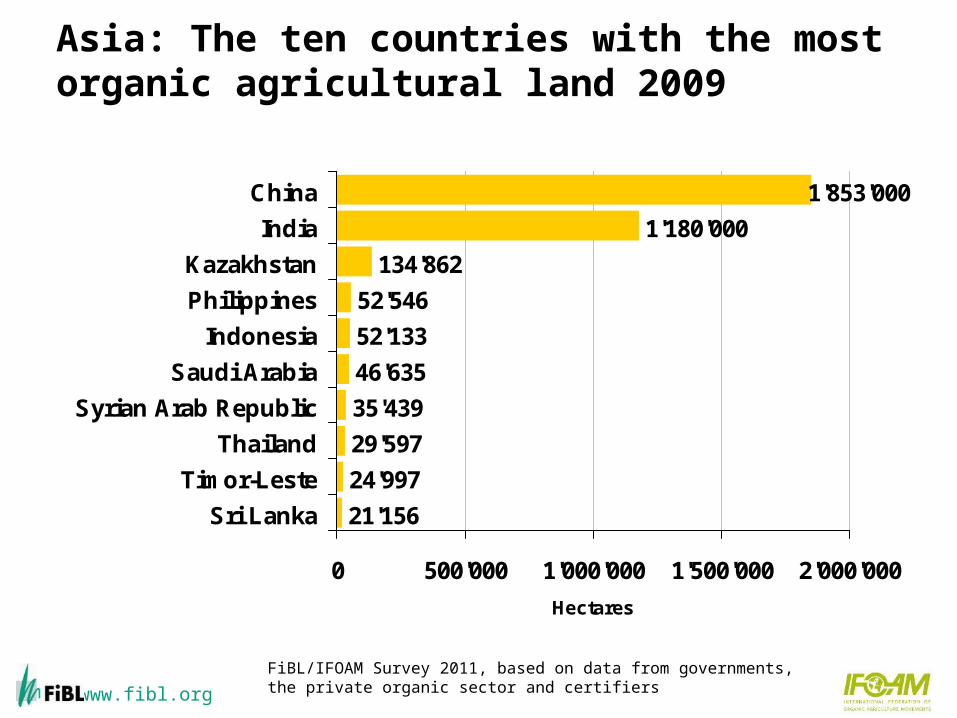

Asia: The ten countries with the most organic agricultural land 2009

21'156

24'997

29'597

35'439

46'635

52'133

52'546

134'862

1'180'000

1'853'000

0 500'000 1'000'000 1'500'000 2'000'000

Sri Lanka

Timor-Leste

Thailand

Syrian Arab Republic

Saudi Arabia

Indonesia

Philippines

Kazakhstan

India

China

Hectares

FiBL/IFOAM Survey 2011, based on data from governments, the private organic sector and certifiers

www.fibl.org

Asia: Distribution of shares of organic land 2009

94%

3%3% Countries with 5.0 to

9.9 % organic land

Countries with 1 to4.9 % organic land

Countries with lessthan 1 % organicland

Source: FiBL/IFOAM Survey 2011

www.fibl.org

Asia: The ten countries/territories with the highest shares of organic agricultural land 2009

0.3%

0.4%

0.4%

0.5%

0.5%

0.7%

0.7%

0.8%

1.4%

6.7%

0% 1% 2% 3% 4% 5% 6% 7% 8%

China

Taiwan

Azerbaijan

Philippines

Lebanon

India

Korea, Republic of

Sri Lanka

Israel

Timor-Leste

FiBL/IFOAM Survey 2011, based on data from governments, the private organic sector and certifiers

www.fibl.org

Asia: Use of organic agricultural land 2009(total: 3.6 million hectares)

Distritbution of main agricultural land use types 2009

6%5%

31%

17%

41%

Arable land Permanent cropsCropland, no details Permanent grasslandAgricultural land, no details

The main arable crops 2009

311

2128

3283

0 20 40 60 80 100

Field fodder cropsVegetables

Medicinal and arom plantsTextile crops

OilseedsCereals

Thousands of hectares

The main permanent crops 2009

14

28

28

31

60

0 20 40 60 80

Nuts

Fruit, tropical andsubtropical

Coconuts

Tea

Coffee

Thousands of hectares

Source: FiBL & IFOAM Survey 2011

www.fibl.org

Articles about Asia in the 2011 Edition of "The World of Organic Agriculture"

› Organic Asia 2010 Ong Kung Wai

› Organic Agriculture in Armenia Nune Darbinyan

› Organic Agriculture Development in China Yuhui Qiao

› Indonesia: Country Report › Lidya Ariesusanty › Kazakhstan: Country Report

Evgeniy Klimov › South Korea: Country Report

Dong-Geun Choi

www.fibl.org

Europe: Organic agricultural land by country 2009

Source: FiBL Survey 2011, revision of May 15, 2011

www.fibl.org

Organic agriculture in Europe: Key data/indicators 2009

› 9.2 million hectares of agricultural land are organic (including in conversion areas).

› This constitutes 1.9 percent of the agricultural land in Êurope.

› The organic agricultural land increased by one million hectares or twelve percent in 2009 .

› 260’000 producers were reported.

Source: FiBL Survey 2011, revision of May 15, 2011

www.fibl.org

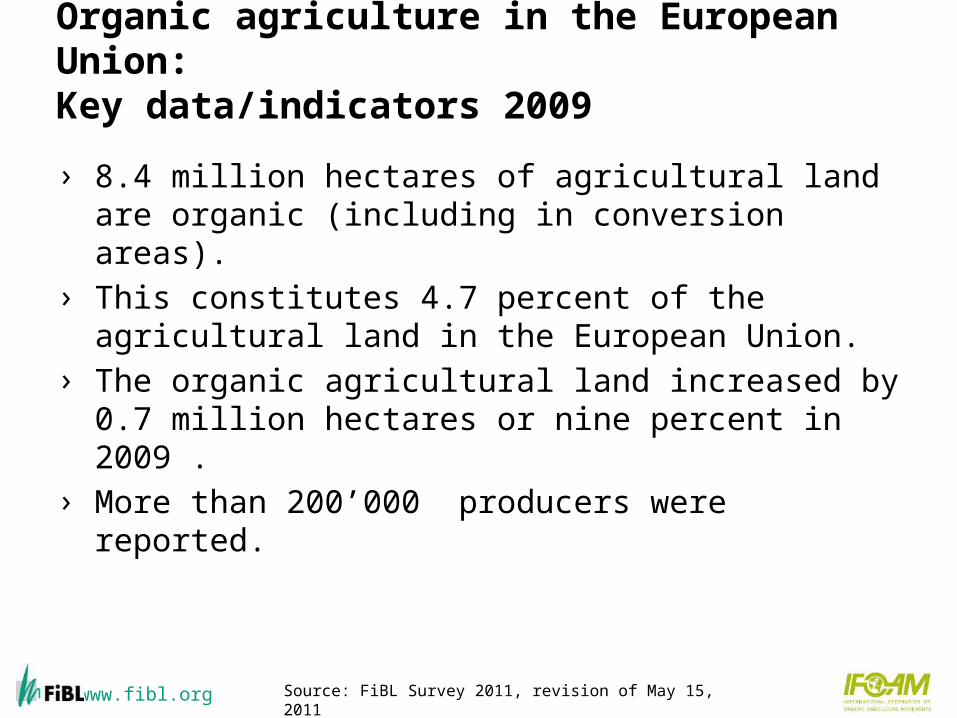

Organic agriculture in the European Union: Key data/indicators 2009

› 8.4 million hectares of agricultural land are organic (including in conversion areas).

› This constitutes 4.7 percent of the agricultural land in the European Union.

› The organic agricultural land increased by 0.7 million hectares or nine percent in 2009 .

› More than 200’000 producers were reported.

Source: FiBL Survey 2011, revision of May 15, 2011

www.fibl.org

Organic agriculture in Europe: Key data/indicators 2009

› The market was 18.4 billion euros, an increase of roughly five percent compared with 2009. The market grew at smaller rates than in previous years even though some countries like France and Sweden showed strong growth.

› The largest market for organic products in 2009 was Germany with a turnover of 5’800 million euros, followed by France (3'041 million euros) and the UK (2'065 million euros).

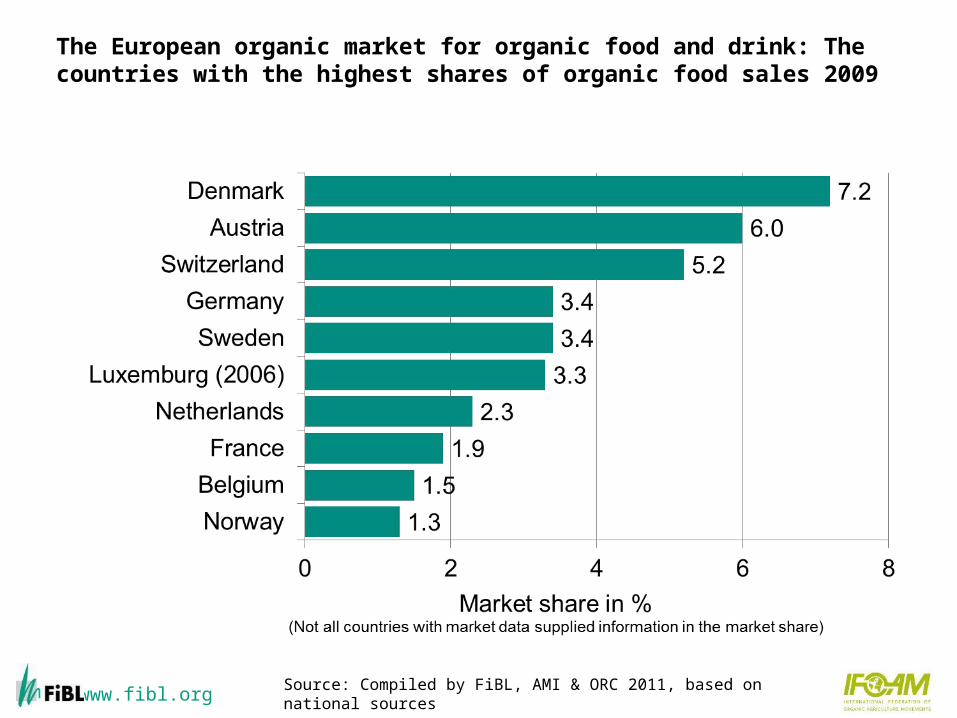

› As a portion of the total market share, the highest levels have been reached in Denmark, Austria and Switzerland, with five percent or more for organic products. The highest per capita spending is also in these countries.

› Support for organic farming in the European Union and neighboring countries includes grants under rural development programs, legal protection, and the European as well as national action plans. An updated overview of European action plans shows that currently 26 action plans (including regional action plans) are in place.

www.fibl.org

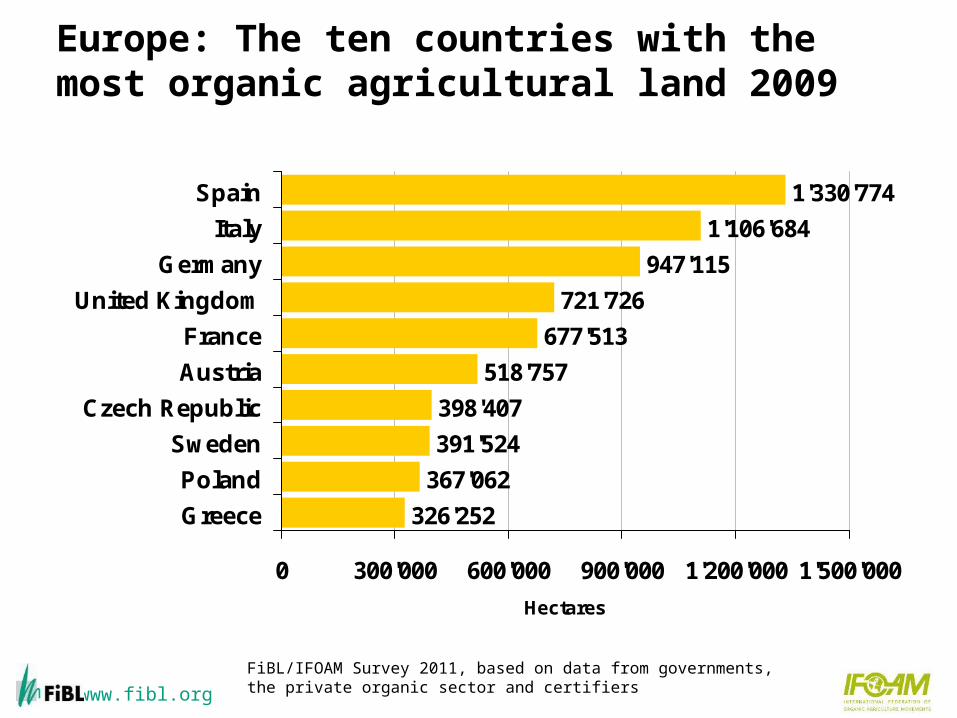

Europe: The ten countries with the most organic agricultural land 2009

326'252

367'062

391'524

398'407

518'757

677'513

721'726

947'115

1'106'684

1'330'774

0 300'000 600'000 900'000 1'200'000 1'500'000

Greece

Poland

Sweden

Czech Republic

Austria

France

United Kingdom

Germany

Italy

Spain

Hectares

FiBL/IFOAM Survey 2011, based on data from governments, the private organic sector and certifiers

www.fibl.org

Europe: Distribution of organically managed agricultural land by country 2009 (Total: 9.3 million hectares)

1'106'684ha; 12%

1'330'774ha; 14%

5'878'424 ha; 64%

947'115 ha; 10%

Spain

Italy

Germany

Rest

Source: Data based on information of Eurostat, ministries, certification bodies and the private sector. Compiled by FiBL 2011

www.fibl.org

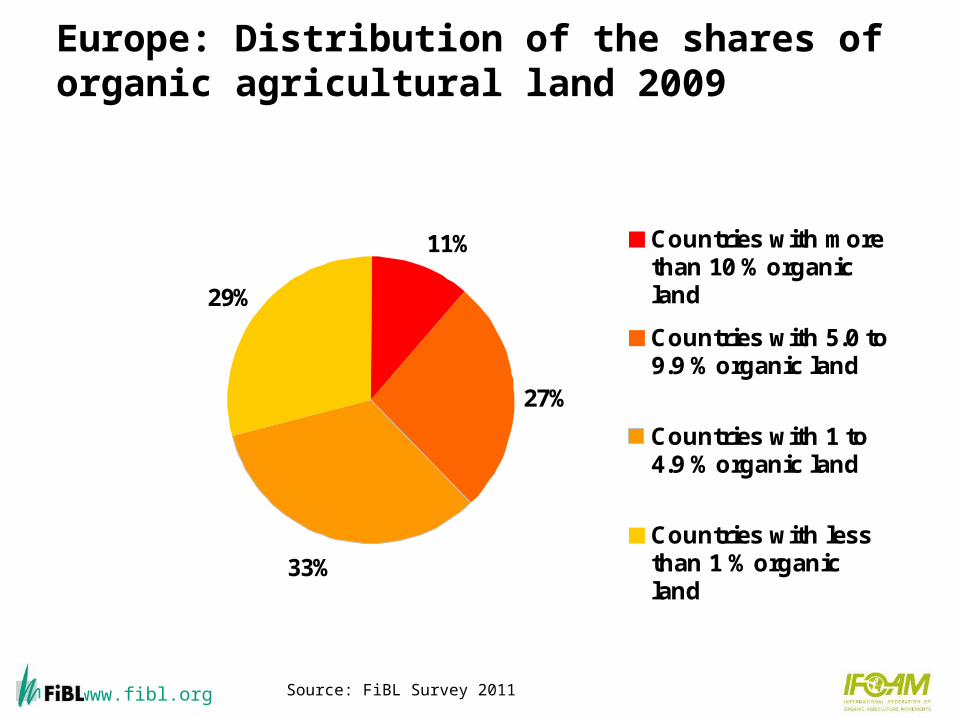

Europe: Distribution of the shares of organic agricultural land 2009

11%

27%

33%

29%

Countries with morethan 10 % organicland

Countries with 5.0 to9.9 % organic land

Countries with 1 to4.9 % organic land

Countries with lessthan 1 % organicland

Source: FiBL Survey 2011

www.fibl.org

Europe: The ten countries with the highest shares of organic agricultural land 2009

7.3%

7.5%

8.7%

9.0%

9.4%

10.5%

10.8%

12.6%

18.5%

26.9%

0% 5% 10% 15% 20% 25% 30%

Finland

Slovakia

Italy

Latvia

Czech Republic

Estonia

Switzerland

Sweden

Austria

Liechtenstein

Source: FiBL Survey 2011, based on national sources

www.fibl.org

Development of the organic agricultural land in Europe 1985-2009(Revision April 26, 2011)

0.10.10.10.20.20.30.50.60.8 11.4

1.82.3

2.9

3.7

4.5

5.45.86.16.4

6.87.3

7.88.3

9.2

0

1

2

3

4

5

6

7

8

9

10

La

nd a

rea

in m

illio

n he

cta

res

Source: FiBL, Aberystwyth University, AMI/ZMP

www.fibl.org

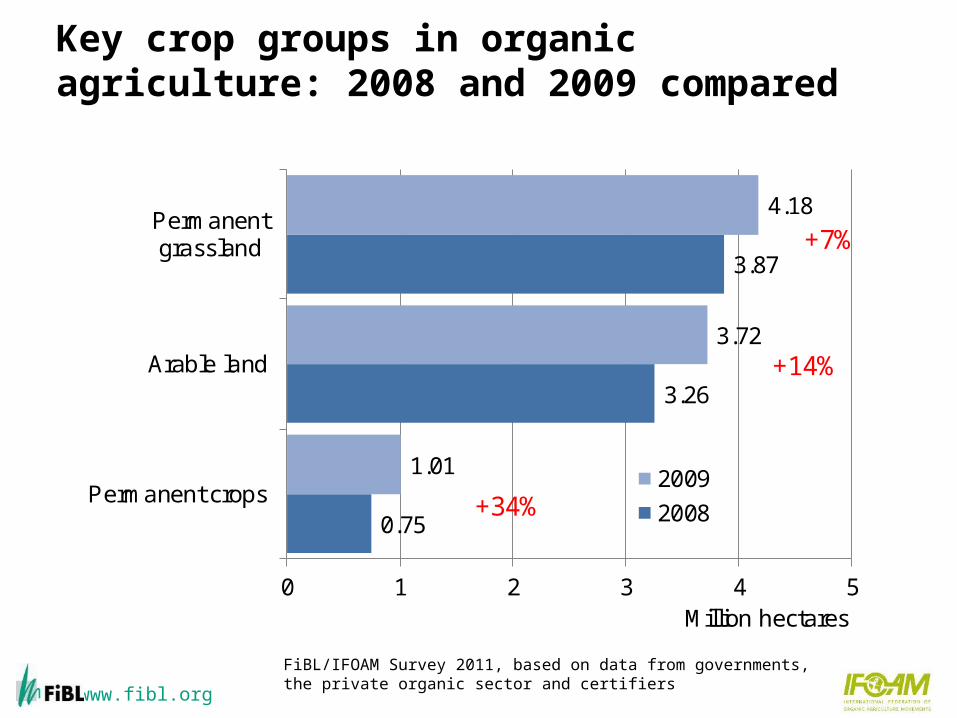

Key crop groups in organic agriculture: 2008 and 2009 compared

0.75

3.26

3.87

1.01

3.72

4.18

0 1 2 3 4 5

Permanent crops

Arable land

Permanentgrassland

Million hectares

2009

2008+34%

+14%

+7%

FiBL/IFOAM Survey 2011, based on data from governments, the private organic sector and certifiers

www.fibl.org

Europe: Use of organic agricultural land 2009 (total: 9.3 million hectares)

Distritbution of main agricultural land use types 2009

40%

11%

3%

46%

Arable land Permanent cropsPermanent grassland Other

The main arable crops 2009

103153162

1'3941'740

0 500 1'000 1'500 2'000

VegetablsOilseeds

Protein cropsField fodder crops

Cereals

Thousands of hectares

The main permanent crops 2009

4071

160167

366

0 100 200 300 400

Citrus fruitFruit, temperate

NutsGrapes

Olives

Thousands of hectares

Source: FiBL Survey 2011

www.fibl.org

Europe: Development of the European Market for Organic Food 2004-2009

10'79212'103

13'536

15'483

17'26018'400

0.0

5'000.0

10'000.0

15'000.0

20'000.0

2004 2005 2006 2007 2008 2009

Mill

ion

Eur

os

Source: FiBL, AMI & ORC 2006 -2011

www.fibl.org

The European organic market for organic food and drink: Growth rates for selected countries 2009

-12.9

0.0

+19.0

-15 -10 -5 0 5 10 15 20 25

UK

Germany

France

Market growth 2009 in %

Source: Soil Association, AMI and Agence Bio 2010

www.fibl.org

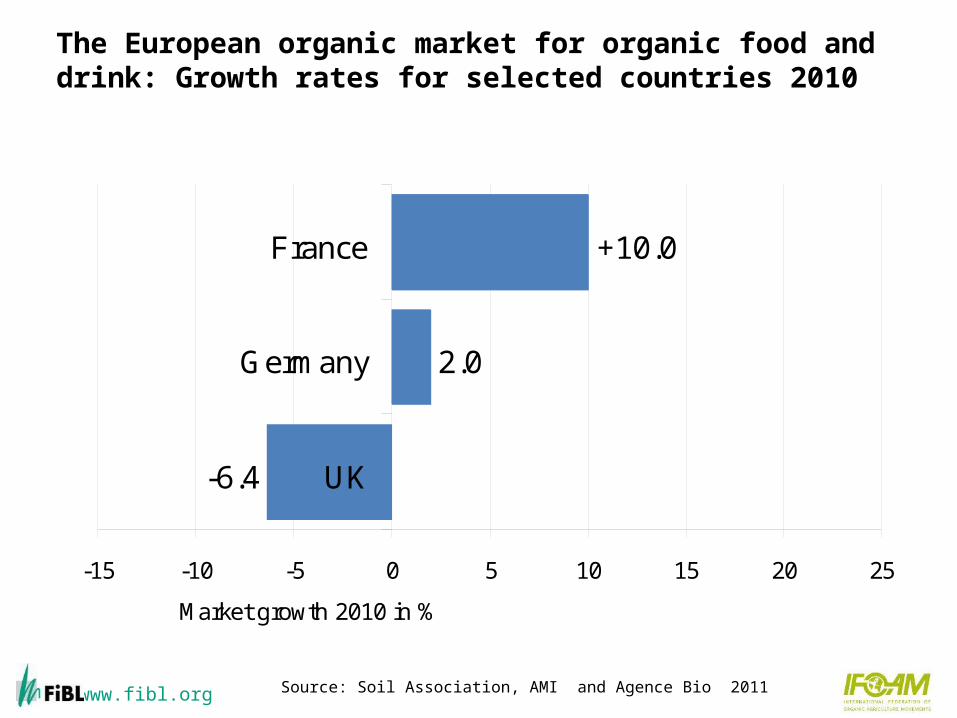

The European organic market for organic food and drink: Growth rates for selected countries 2010

-6.4

2.0

+10.0

-15 -10 -5 0 5 10 15 20 25

UK

Germany

France

Market growth 2010 in %

Source: Soil Association, AMI and Agence Bio 2011

www.fibl.org

Europe: Distribution of sales of organic food and drink by country 2009 (total: 18.4 billion Euros)

Source: FiBL, AMI, ORC Survey 2011, based on national sources

www.fibl.org

The European market for organic food and drink: The countries with the highest sales 2009

Source: Compiled by FiBL, AMI and ORC 2011, based on national sources

www.fibl.org

The European organic market for organic food and drink: The countries with the highest shares of organic food sales 2009

Source: Compiled by FiBL, AMI & ORC 2011, based on national sources

www.fibl.org

The European market for organic food: The countries with the highest per capita consumption 2009

Source: Compiled by FiBL, AMI and ORC 2011, based on national sources

www.fibl.org

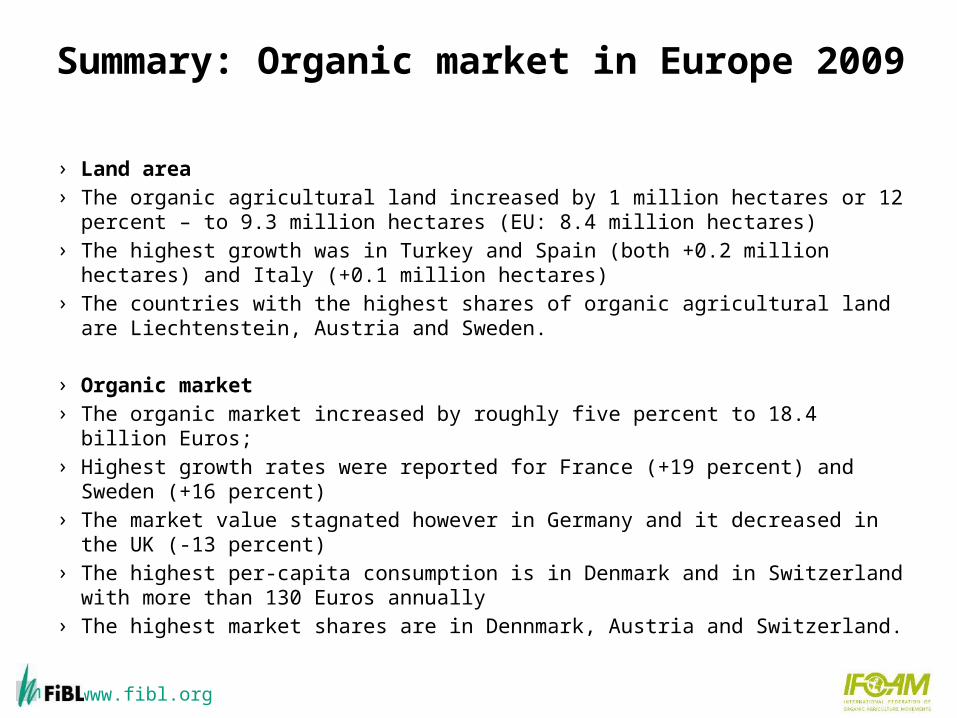

Summary: Organic market in Europe 2009

› Land area› The organic agricultural land increased by 1 million hectares or 12 percent – to 9.3

million hectares (EU: 8.4 million hectares)› The highest growth was in Turkey and Spain (both +0.2 million hectares) and Italy

(+0.1 million hectares)› The countries with the highest shares of organic agricultural land are

Liechtenstein, Austria and Sweden.

› Organic market› The organic market increased by roughly five percent to 18.4 billion Euros;› Highest growth rates were reported for France (+19 percent) and Sweden (+16

percent)› The market value stagnated however in Germany and it decreased in the UK (-13

percent) › The highest per-capita consumption is in Denmark and in Switzerland with more

than 130 Euros annually› The highest market shares are in Dennmark, Austria and Switzerland.

www.fibl.org

Articles about Europe in the 2011 Edition of "The World of Organic Agriculture"

› Organic Agriculture in Europe: Overview Helga Willer

› The Organic Market in Europe Diana Schaack, Helga Willer, and Susanne Padel

› Organic Action Plans in Europe in 2010 Victor Gonzálvez, Otto Schmid and Helga Willer

› Switzerland: Country Report Lukas Kilcher

› Ukraine Country Report Natalie Prokopchuk and Tobias Eisenring

www.fibl.org

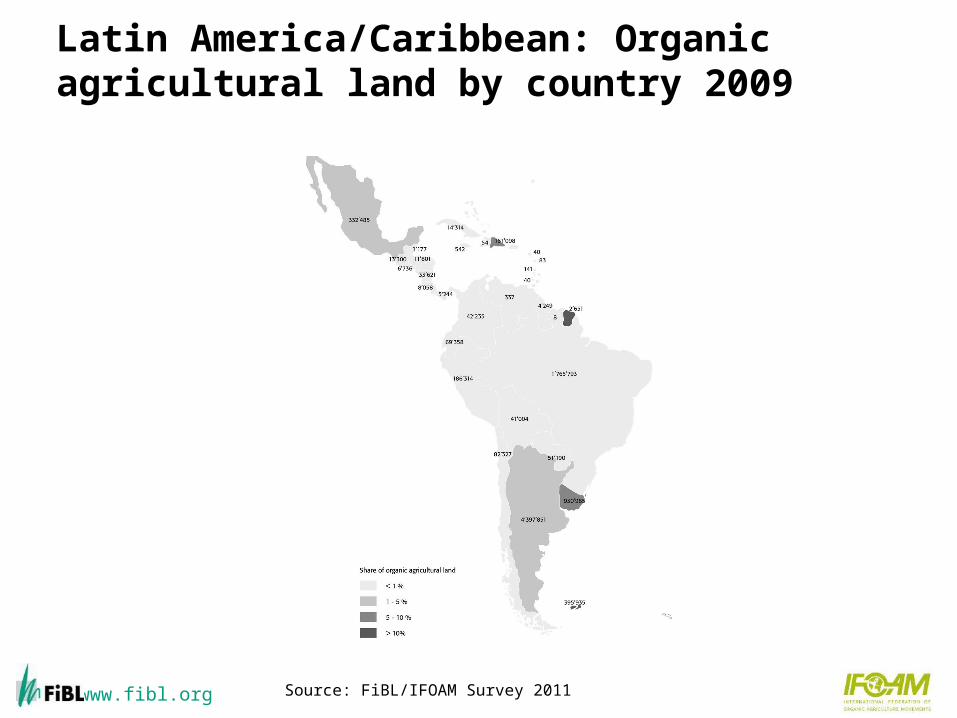

Latin America/Caribbean: Organic agricultural land by country 2009

Source: FiBL/IFOAM Survey 2011

www.fibl.org

Latin America: Key figures 2009

› In Latin America, more than 280’000 producers managed 8.6 million hectares of agricultural land organically in 2009.

› This constitutes 23 percent of the world’s organic land and 1.4 percent of the regions agricultural land.

› The leading countries are Argentina (4.4 million hectares), Brazil (1.8 million hectares), and Uruguay (930'965 hectares).

› The highest shares of organic agricultural land are in the Falkland Islands/Malvinas (35.7 percent), the Dominican Republic (8.3 percent), and Uruguay (6.3 percent).

www.fibl.org

Latin America: Key figures 2009

› Most organic products from Latin American countries are sold on the European, North American or Japanese markets. Popular goods are especially those that cannot be produced in these regions, as well as off-season products. Thus, the development of robust local markets is still a major challenge, without which the sustainability of organic production cannot be achieved. Important crops are tropical fruits, grains and cereals, coffee, cocoa, sugar, and meats. Most organic food sales in the domestic markets of the countries occur in major cities.

› Eighteen countries have legislation on organic farming, and five additional countries are currently developing organic regulations. Costa Rica and Argentina have both attained Third Country status according to the EU regulation on organic farming.

› The types of support in Latin American countries range from organic agriculture promotion programs to market access support by export agencies.

47

www.fibl.org

Latin America/Caribbean: Distribution of organically managed agricultural land by country 2009 (total: 8.6 million hectares)

51%

21%

17%

11%

Argentina

Brazil (2007)

Uruguay (2007)

Others

Source: FiBL Survey 2011

www.fibl.org

Latin America/Caribbean: The ten countries with the most organic agricultural land 2009

51'190

69'358

82'327

161'098

186'314

332'485

395'935

930'965

1'765'793

4'397'851

0 2'000'000 4'000'000 6'000'000

Paraguay (2007)

Ecuador

Chile

Dominican Republic

Peru

Mexico (2008)

Falkland Islands (Malvinas)

Uruguay (2006)

Brazil (2007)

Argentina

HectaresArgentina and Uruguay: Only fully converted area

Source: FiBL/IFOAM Survey 2011

www.fibl.org

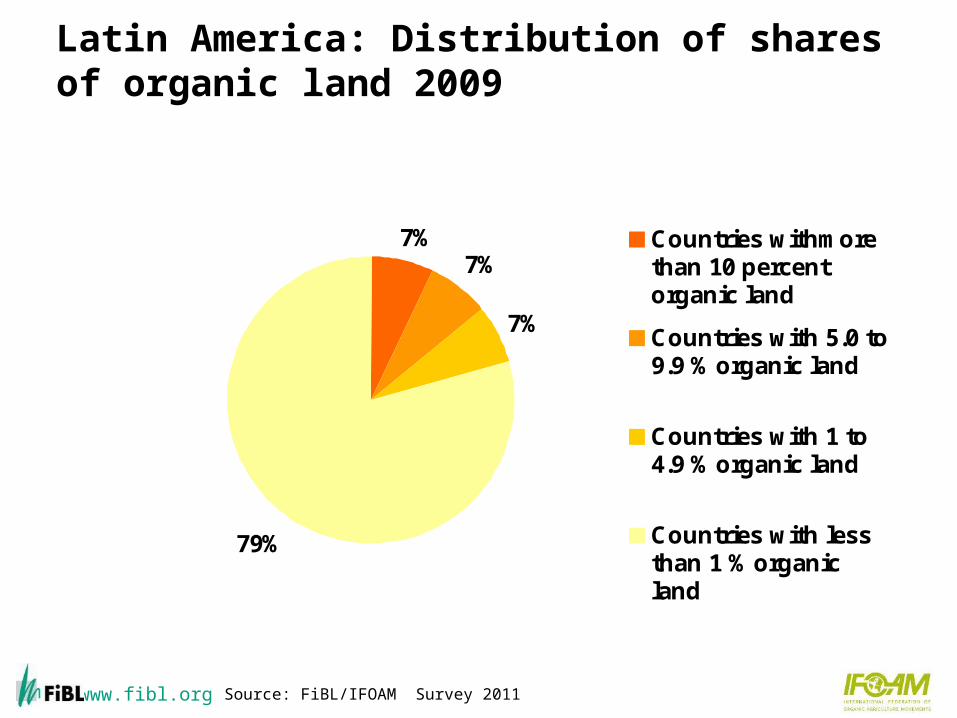

Latin America: Distribution of shares of organic land 2009

7%7%

7%

79%

Countries withmorethan 10 percentorganic land

Countries with 5.0 to9.9 % organic land

Countries with 1 to4.9 % organic land

Countries with lessthan 1 % organicland

Source: FiBL/IFOAM Survey 2011

www.fibl.org

Latin America: The ten countries with the highest shares of organic agricultural land 2009

0.7%

0.8%

0.9%

0.9%

2.4%

3.3%

6.3%

8.3%

11.7%

35.7%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Brazil

Belize

Peru

Ecuador

Mexico

Argentina

Uruguay

Dominican Republic

French Guiana (France)

Falkland Islands (Malvinas)

FiBL/IFOAM Survey 2011, based on data from governments, the private organic sector and certifiers

www.fibl.org

Latin America: Development of organically managed agricultural land 2000-2009

1.2

4.8

5.8 6.0

5.2

5.1

5.0

6.4

8.1 8.

6

3.9

0

1

2

3

4

5

6

7

8

9

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Mil

lio

n h

ecta

res

Source: FiBL/IFOAM/SOEL Surveys 1999-2011

www.fibl.org

Latin America: Use of organic agricultural land 2009 (total: 8.6 million hectares)

Distritbution of main agricultural land use types 2009

2% 8%

0%

62%

28%

Arable land Permanent cropsCropland, no details Permanent grasslandAgricultural land, no details

The main arable crops 2009

2

6

25

39

51

0 20 40 60

Protein crops

Medicinal and arom. Plants

Cereals

Vegetables

Sugarcane

Thousands of hectares

The main permanent crops 2009

1214

98197

330

0 100 200 300 400

Citrus fruitCoconut

Fruit, tropicalCocoaCoffee

Thousands of hectares

Source: FiBL & IFOAM Survey 2011

www.fibl.org

Articles about Latin America and the Caribbean in the 2011 Edition of "The World of Organic Agriculture"

› Organic Farming in Latin America and the Caribbean Salvador V. Garibay, Roberto Ugas, and Patricia Flores Escudero

› Chile: Country Report Pilar Eguillor Recabarren

› Costa Rica: Country Report Roberto Azofeifa

› All in Willer/Kilcher (Eds.) 2011: The World of Organic Agriculture. Statistics and Emerging Trends 2011. IFOAM and FiBL, Bonn and Frick

54

www.fibl.org

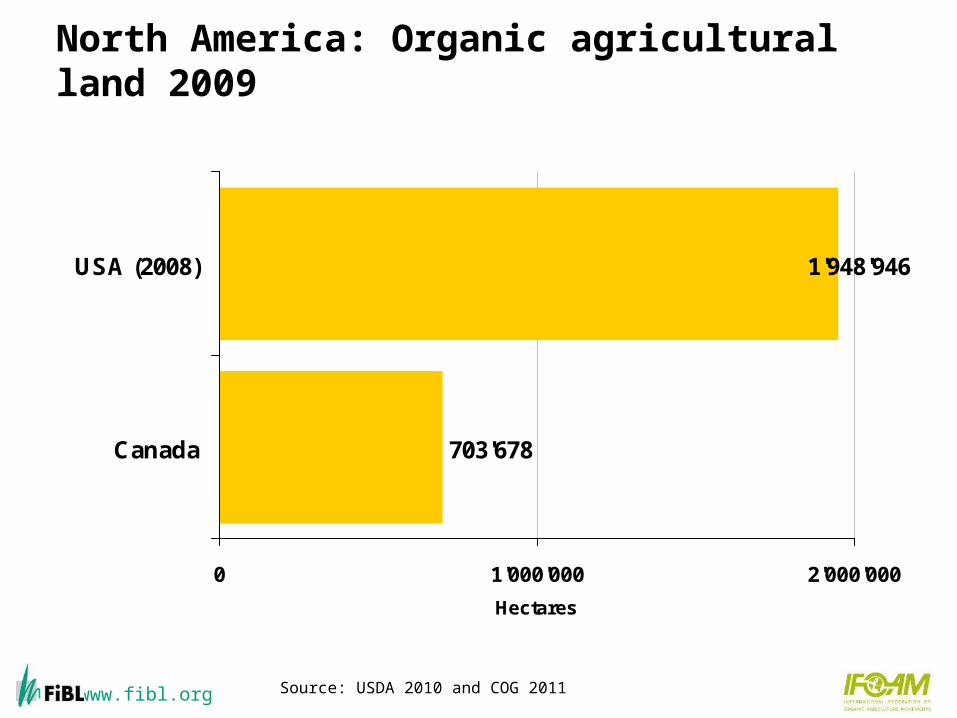

North America: Organic agricultural land by country 2009

Source: USDA and COG 2011

www.fibl.org

Organic Agriculture in North America: Key figures 2009

› In North America, almost 2.7 million hectares are managed organically, of these nearly two million in the United States and 0.7 million in Canada.

› This represents approximately 0.7 percent of the total agricultural area in the region and 7 percent of the world’s organic agricultural land.

› US sales of organic products continued to grow during 2009 despite the distressed state of the economy. In fact, organic product sales in 2009 grew by 5.3 percent overall, to reach 26.6 billion US dollars.

› Of that figure, 24.8 billion US dollars represented organic food or 3.7 percent of the food market. The remaining 1.8 billion were sales of organic non-foods.

› Projections for 2010 and beyond indicate higher growth rates for organic sales in North America.

www.fibl.org

Organic Agriculture in North America: Key figures 2009

› In Canada, Agriculture and Agri-Food Canada in 2010 released a new report on the Canadian organic sector’s trade data and retail sales. Analyzing the 2008 sales of organic foods, the report concludes that the total Canadian organic market is worth 2 billion Canadian dollars annually.

› Regarding legislation, representatives from the Canada Organic Office and the US National Organic Program have completed a full peer review, in order to monitor and evaluate how the US-Canada organic equivalence arrangement is being applied.

www.fibl.org

North America: Organic agricultural land 2009

703'678

1'948'946

0 1'000'000 2'000'000

Canada

USA (2008)

Hectares

Source: USDA 2010 and COG 2011

www.fibl.org

North America: Distribution of organic agricultural land by country 2009; total: 2.7 million hectares

73%

27%

USA Canada

Source: USDA 200 and Canadian Organic Growers 2011

www.fibl.org

North America: Shares of organic agricultural land 2009

0.6%

1.0%

0% 0% 0% 1% 1% 1% 1%

USA (2008)

Canada

Source: Canadian Organic Growers 2010 and USDA 2010

www.fibl.org

North America: Development of organically managed agricultural land 2000-2009

0.7

1.3

1.3 1.

4

1.7

2.2

1.8

2.3

2.6 2.7

1.1

0

1

1

2

2

3

3

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Mil

lio

n h

ecta

res

Source: USDA and Canadian Organic Growers 1999-2011

For the US, no data are available for 2009.

www.fibl.org

North America: Use of organic agricultural land 2009* (total: 2.65 million hectares)

Distritbution of main agricultural land use types 2009

50%

2%

4%

43%

1%

0%

Arable land Permanent cropsCropland, no details Permanent grasslandOther Agricultural land, no details

The main arable crops 2009

3965

169445

575

0 200 400 600 800

Protein cropsVegetables

OilseedsField fodder crops

Cereals

Thousands of hectares

The main permanent crops 2009

46

810

12

0 2 4 6 8 10 12 14

BerriesCitrus fruit

Fruit, temp.Nuts

Grapes

Thousands of hectares

Source: FiBL/IFOAM Survey 2011 *US data from 2008

www.fibl.org

US: Organic food sales 2000-2009

2000 2001 2002 2003 2004 2005 2006 2007 2008 20090

5,000

10,000

15,000

20,000

25,000

0%

1%

2%

3%

4%

6,1

00

7,3

60

8,6

35

10

,38

1

12

,00

2

14

,22

3

17

,22

1

20

,41

0

23

,60

7

24

,80

3

1.2%1.4%

1.6%

1.9%

2.2%

2.5%

2.9%

3.2%

3.6% 3.7%

Turnover in million US Dollars Share of total market (%)

Tu

rno

ver

Sh

are

of t

ota

l ma

rke

t

Source: OTAOrganic Trade Association’s 2010 Organic Industry Survey conducted 1/21/2010 – 3/3/2010. Available on http://www.ota.com/pics/documents/2010OrganicIndustrySurveySummary.pdf

www.fibl.org

Articles about North America in the 2011 Edition of "The World of Organic Agriculture"

› North American Overview Barbara Fitch Haumann

› United States: Country Report Barbara Fitch Haumann

› Canada: Country Report Matthew Holmes and Anne Macey

› All in Willer/Kilcher (Eds.) 2011: The World of Organic Agriculture. Statistics and Emerging Trends 2011. IFOAM and FiBL, Bonn and Frick

www.fibl.org

Oceania: Organic agricultural land by country 2009

FiBL/IFOAM Survey 2011

www.fibl.org

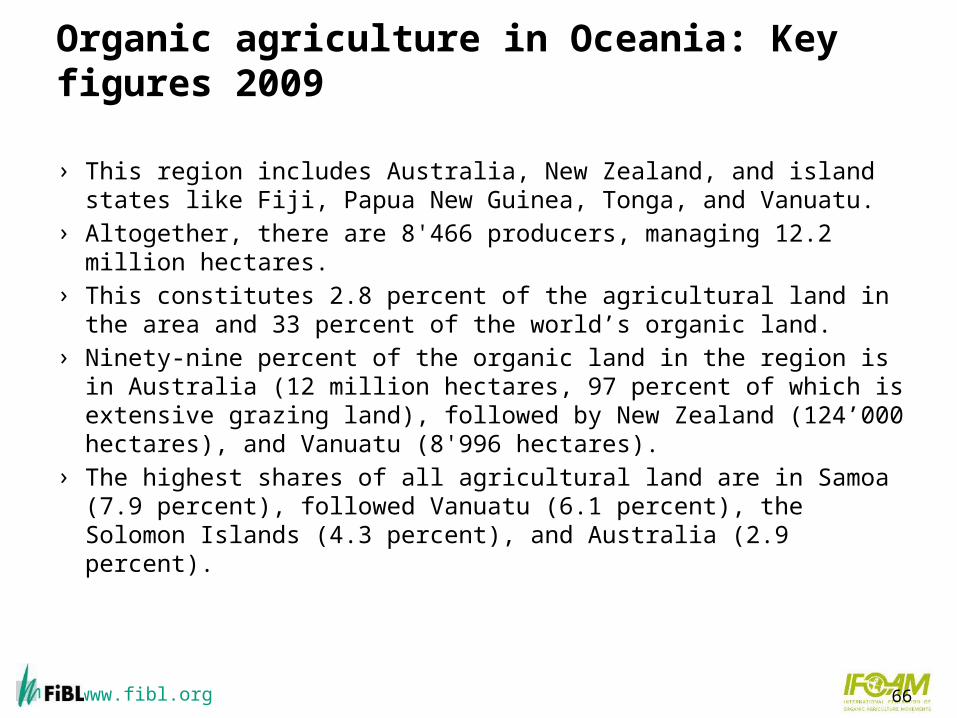

Organic agriculture in Oceania: Key figures 2009

› This region includes Australia, New Zealand, and island states like Fiji, Papua New Guinea, Tonga, and Vanuatu.

› Altogether, there are 8'466 producers, managing 12.2 million hectares.

› This constitutes 2.8 percent of the agricultural land in the area and 33 percent of the world’s organic land.

› Ninety-nine percent of the organic land in the region is in Australia (12 million hectares, 97 percent of which is extensive grazing land), followed by New Zealand (124’000 hectares), and Vanuatu (8'996 hectares).

› The highest shares of all agricultural land are in Samoa (7.9 percent), followed Vanuatu (6.1 percent), the Solomon Islands (4.3 percent), and Australia (2.9 percent).

66

www.fibl.org

Organic agriculture in Oceania: Key figures 2009

› Growth in the organic industry in Australia, New Zealand and the Pacific Islands has been strongly influenced by rapidly growing overseas demand; domestic markets are, however, also growing. In Australia it was at 947 Australian dollars in 2009 and in New Zealand at 350 million New Zealand dollars.

› The biggest change in the Australian domestic market over 2009 was that the Australian Standard for Organic and Biodynamic Products was adopted and published by Standards Australia.

› The year 2010 marked a milestone for the Pacific Region: The International Organic Accreditation Service (www.ioas.org) assessed the Pacific Organic Standard (POS) and found it to be equivalent to the standards requirements of the European Union’s organic regulations.

www.fibl.org

Oceania: Development of organic agricultural land 1999-2009

Source: USDA and Canadian Organic Growers 1999-2011

For the US, no data are available for 2009,

www.fibl.org

Oceania: Shares of organic agricultural land 2009

Source: FiBL/IFOAM Survey 2011, based on data from governments, the private organic sector and certifiers.

www.fibl.org

Oceania: Shares of organic land 2009

Source: FiBL/IFOAM Survey 2011

www.fibl.org

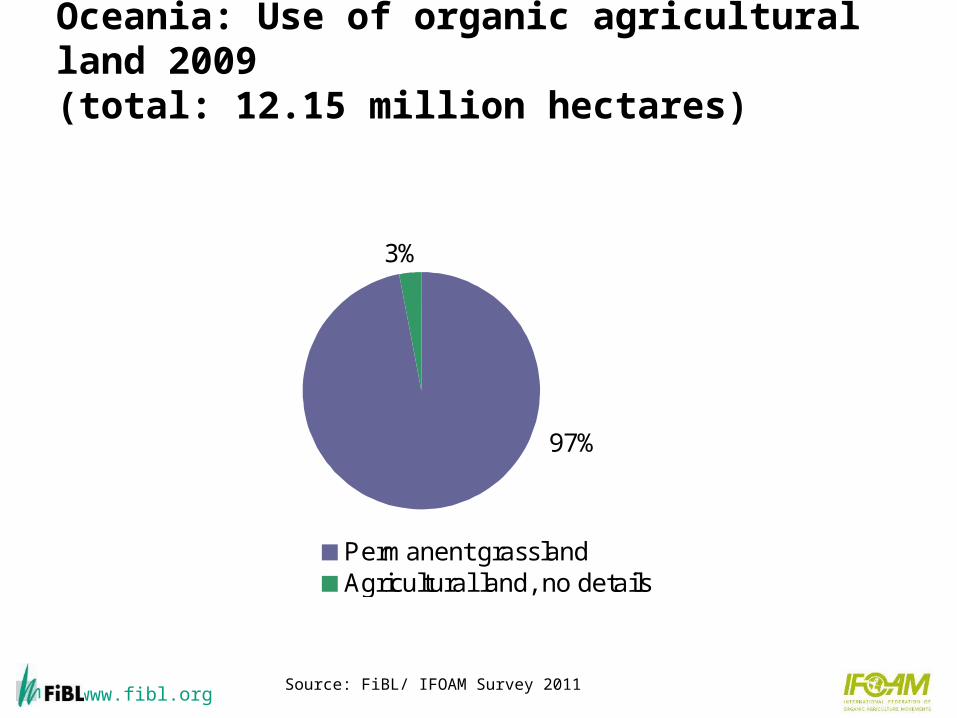

Oceania: Use of organic agricultural land 2009 (total: 12.15 million hectares)

3%

97%

Permanent grasslandAgricultural land, no details

Source: FiBL/ IFOAM Survey 2011

www.fibl.org

Articles about Oceania in the 2011 Edition of "The World of Organic Agriculture"

› Organic Farming in Australia Els Wynen, Alexandra Mitchell, and Paul Kristiansen

› The Pacific Islands Karen Mapusua

› All in Willer/Kilcher (Eds.) 2011: The World of Organic Agriculture. Statistics and Emerging Trends 2011. IFOAM and FiBL, Bonn and Frick

www.fibl.org

Abbreviations

› AMI: Agrarmarkt Informations-Gesellschaft mbH (AMI, information service for organic markets), www.ami-informiert.de

› COG: Canadian Organic Growers – www.cog.ca› FiBL: Research Institute of Organic Agriculture, Switzerland› IFOAM: International Federation of Organic Agriculture

Movements, Germany, www.ifoam.org› ORC: Organic Research Centre Elm Farm, UK, www.efrc.com› RUTA: Unidad Regional de Asistencia Técnica (RUTA;

Regional Unit for Technical Assistance), Costa Rica, www.ruta.org

› USDA: United States Department of Agriculture (USDA), www.usda.gov