Key Issues and Policy Recommendations - Welcome to National

25

Mierta Capaul Program Manager, Corporate Governance Policy Practice Corporate Governance Department The World Bank Group Key Issues and Policy Recommendations India Corporate Governance ROSC Assessment Varsha Marathe Financial Specialist Finance and Private Sector Unit- South Asia Region The World Bank October 18, 2004 New Delhi

Transcript of Key Issues and Policy Recommendations - Welcome to National

Mierta CapaulProgram Manager, Corporate Governance Policy PracticeCorporate Governance DepartmentThe World Bank Group

Key Issues and Policy Recommendations

India

Corporate Governance ROSC Assessment

Varsha MaratheFinancial SpecialistFinance and Private Sector Unit- South Asia RegionThe World Bank

October 18, 2004

New Delhi

2

Overview

Who we areWhy corporate governance?The role of the World BankCorporate governance ROSC assessmentsSummary of the corporate governance ROSC assessment in IndiaKey issues and policy recommendationsContact information

3

Corporate Governance DepartmentA joint WB/IFC Department

Who we are…

IFC Investor and Corporate

Practice

• Multi-donor trust fund• Awareness raising• Sponsor research• Promotes government

reform and private sector self-help

• Develops toolkit

• Evaluates client companies

• Uses methodology & set of tools and

practices• Helps clients implement

best practice• Technical assistance

• ROSC assessments• IFA / OECD liaison• Cross-support• Operational work• Best Practice papers • Implementation design

WB Corporate Governance

Policy Practice

Global Corporate

Governance Forum

4

Why corporate governance?

Protection of shareholder rightsPublic policy rationale Access to finance Crisis prevention and financial stability Protection of pension savings for retirement

5

Corporate Governance and World Bank Strategy

Investment Climate One of the World Bank’s strategic pillars Macro-stabilization and micro policy reforms Laws, regulations, public institutions & civic habits Importance of diagnostics – ICA, FIAS, DB, CG

A conducive investment climate is crucial for economic growth and poverty reduction

6

Overview of Corporate Governance ROSC Assessments

Corporate governance is one of 12 standards and codes assessed by IMF and World Bank

• Data Dissemination • Fiscal Transparency • Monetary and Financial Policy Transparency • Banking Supervision • Securities Regulation (IOSCO)• Insurance Supervision • Payments Systems Corporate Governance Accounting Auditing Insolvency and Creditor Rights• Anti-Money Laundering

}

7

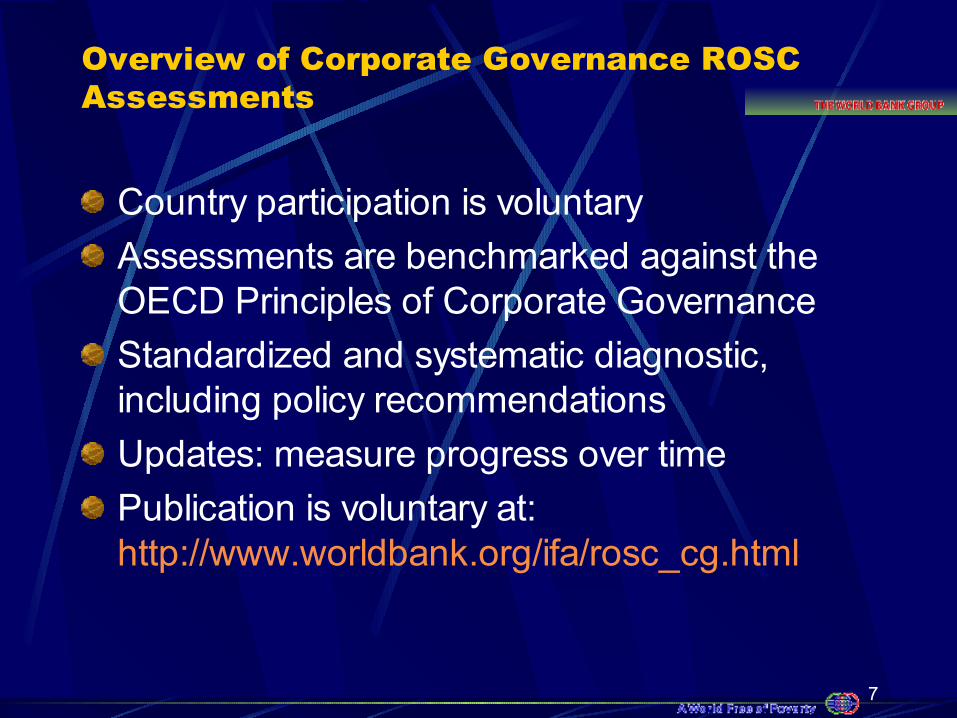

Overview of Corporate Governance ROSC Assessments

Country participation is voluntaryAssessments are benchmarked against the OECD Principles of Corporate Governance Standardized and systematic diagnostic, including policy recommendationsUpdates: measure progress over timePublication is voluntary at: http://www.worldbank.org/ifa/rosc_cg.html

8

Overview of World Bank Corporate Governance Assessments

Published 30Completed (not yet published) 8Ongoing 4Planned ’05 6

10

8

10

10

10

0 10 20 30 40 50

FY01

FY02

FY03

FY04

FY05

Assessments by Year

9

Overview of Corporate Governance ROSC Assessments

Assessments through FY04 by Region

AFR (3)

EAP (5)

ECA (17)

LCR (7)

MNA (4)

SAR (2)

10

Overview of World Bank Corporate Governance Assessments

2001 2002 2003 2004 2005 Brazil Georgia Mauritius Egypt 2 Poland2 Croatia Czech Rep. 2 Brazil 2 Slovenia Thailand Czech Rep. Lithuania Hungary Russia Armenia Egypt Bulgaria Ukraine India 2 Brazil3 India Latvia Korea Peru Vietnam Malaysia Morocco Hong Kong Romania 2 Macedonia Philippines Romania Chile Indonesia Ghana Poland South Africa Mexico Jordan Bangladesh Turkey Slovakia Moldova Lebanon? Zimbabwe Colombia Panama CFA Zone? Pakistan? Notes: Assessments in bold are in process. Assessments in italics have not been published.

11

Corporate Governance Assessment in India

Summary of assessment

Key issues and policy recommendations

12

India ROSC – Key country features

Over 9,500 listed companies in 200369 GDRs, 11 ADRs, 5 companies bothSOEs account for 32 % of market capIncreasing importance of equity finance Promoters own at least 26 % of firmBusiness groups are common

13

Corporate Governance Assessment in India: Summary of Assessment

Strong assessment: 10 Principles “Observed” 6 Principles “Largely Observed” 6 Principles “Partially Observed” 1 Principle “Materially Not Observed” No principle was “Not Observed”

Improvement from previous assessment in 2000 with only 5 observed, 9 partially observed and the rest materially not, not observed or information not sought Update reflects progress over time including Company Act amendments, SEBI regulations and “Clause 49”, the “comply and explain” clause in the listing agreement. Awareness due to reporting in the press.

14

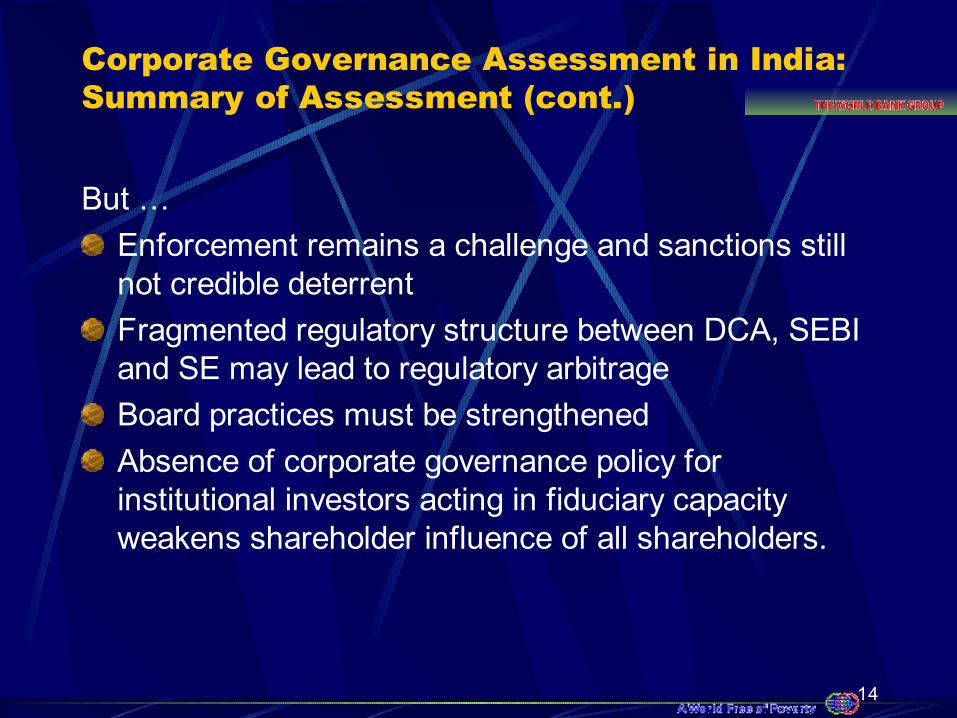

Corporate Governance Assessment in India: Summary of Assessment (cont.)

But …Enforcement remains a challenge and sanctions still not credible deterrent Fragmented regulatory structure between DCA, SEBI and SE may lead to regulatory arbitrageBoard practices must be strengthenedAbsence of corporate governance policy for institutional investors acting in fiduciary capacity weakens shareholder influence of all shareholders.

15

Key Issues and Policy Recommendations

• Institutional Framework• Board Structure• Fiduciary Duties• Create a Director Training Organization• Institutional Investors• Improve Disclosure- Issuers• Improve Audit Quality and Oversight• Strengthen Sanctions and Enforcement• Next Steps

16

1. Institutional Framework

The institutional framework guides the implementation and enforcement of rules and practices. The three-tiered regulatory system creates potential for regulatory arbitrage and weakens enforcement.

An in-depth revision of regulatory system regarding respective roles and responsibilities of the involved institutions and their supervisory functions necessary.• Keeping in mind the size of the equity market

17

2. Board Structure

1/3 of the board of directors: permanent directors Promoters, Executive Directors, Nominee Directors

2/3 of the board rotational – i.e. elected at AGM1/3 of the board independent directors If CEO is chairman, then 50% of board independent

Audit committee: majority independent

Should shareholders elect entire board? Do nominee directors have necessary specialized knowledge? Should terms for independent directors be capped?

18

3. Fiduciary Duties

Company dominated by promoter rather than BODBOD may delegate special powers to “executive directors”or “full time directors”Audit committee’s recommendations are binding on the board

The Company Act should clearly define duties and liabilities for all directors of the board• No different standard of care & diligence for full time and

independent directors, for audit committee and board Clearly defined board procedures and

responsibilities allow board to exercise its function

19

4. Create a Director Training Organization

Director training is considered essential to upgrading a country’s corporate governance.Director training provides directors with an understanding of their role and duties, and educates them in financial, business, and industry practices.Director training will expand the pool of competent independent director candidates, especially for audit committees.

20

5. Institutional Investors

SOE insurance companies and UTI are the most important institutional investors Traditionally characterized by voting apathyNominee board positions on portfolio companies’ boards

Institutional investors acting as fiduciaries should be encouraged to formulate and disclose a comprehensive CG and voting policy: Institutional investors should disclose how they manage

conflicts of interest Institutional investors should consider nominating

independent directors to boards of portfolio companies instead of automatically awarding positions to current/retired employees

21

6. Improve disclosure compliance- Issuers

Currently: Compliance emphasis on form rather than content Wide range of penalties for non-compliance: from

monetary penalty to imprisonment. However these are not credible deterrents.

Reforms: Sanctions (fines and civil liability) for non-disclosure

should be reviewed SEBI’s role as disclosure regulator- Selective review of

content versus form Stock Exchange Surveillance: Monitoring of financial

media needs to be supplemented with market surveillance on unusual price movements or trading volumes

22

7. Improve Audit Quality and Oversight

Currently: Ineffective sanction when auditor’s opinion and reports do

not conform with the law Disciplinary proceedings through ICAI have been lengthy

Reforms Establish a monitoring and enforcement arrangement in

line with recent international developments and the recommendations of Naresh Chandra Committee

World Bank ROSC on Accounting and Auditing to be published shortly provides an assessment of the strengths/weaknesses of the institutional framework for supporting high quality accounting and auditing practices

23

8. Strengthen Sanctions and Enforcement

The Companies Act provides sanctions for oppression by majority or mismanagementCourt delays are the norm We would recommend that: Enforcement powers of regulators can offset backlog

and delay of court procedures More effective cooperation between SEBI, SE and

DCA/CLB. Monetary sanctions should be strengthened to act as a

deterrent For fines to be appealed they should have to be paid An efficient delisting mechanism should be introduced

24

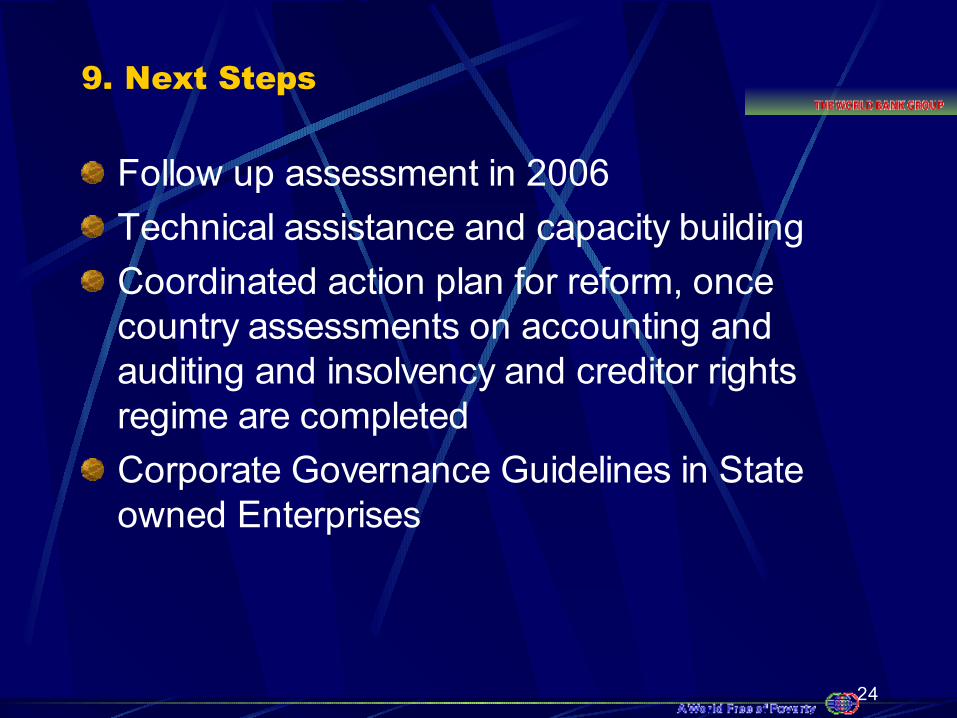

9. Next Steps

Follow up assessment in 2006Technical assistance and capacity buildingCoordinated action plan for reform, once country assessments on accounting and auditing and insolvency and creditor rights regime are completedCorporate Governance Guidelines in State owned Enterprises

25

Contact information

Mierta CapaulCorporate Governance Policy Practice

Corporate Governance DepartmentPrivate Sector Development

The World Bank GroupTel: (202) 473 0155Fax (202) 522 1604

Email: [email protected]://www.worldbank.org/ifa/rosc_cg.html