Key Financials (NOKm) 2019 2020 2021E 2022E 2023E

17

Important information: All information regarding limitation of liability and potential conflicts of interest can be found at the end of the report Redeye, Mäster Samuelsgatan 42, 10tr, Box 7141, 103 87 Stockholm. Tel. +46 8-545 013 30, E-post: [email protected] Key Financials (NO 2019 2020 2021E 2022E 2023E Revenues 2 2 4 65 446 Revenue growth 21% 139% 1378% 588% EBITDA -96 -60 -71 -51 35 EBIT -96 -62 -73 -52 34 EBIT Margin (%) -6328% -3370% -1672% -80% 8% Net Income -96 -62 -74 -47 34 EV/Revenue 434,3 368,0 184,0 13,2 1,8 EV/EBITDA neg neg neg neg 23,7 EV/EBIT neg neg neg neg 23,9 Research Update Equity Research 2 November 2021 KEY STATS Ticker ZWIPE Market Merkur Mkt Share Price (NOK) 27 Market Cap (NOKm) 1000 Net Debt (NOKm) -180 Free Float (%) 75% Avg. daily volume ('000) 25 BEAR BASE BULL 6 32 46 The Four Pillars of Value Redeye raises the valuation of Zwipe driven by increased confidence in mass market adoption turning into higher sales estimates. We think Zwipe is well positioned with a strong financial position. Larger commercial orders will be a catalyst for the share price. Increasing the pie Zwipe continue to show their strong deal making capabilities by reaching new agreements every month. Between today and our last longer update on the 17 th of July they have announced that they are under evaluation with a Global Tier 1 Smartcard Manufacturer, they received two commercial orders from Beautiful Cards Corporation and Inkript, and they also announced pilots with MEPS, Reltime, Credit Lebanaise and a Global Tier-1 Bank. And that was just part of the announcements, we will leave a brief comment on all in this update. Stable financial situation Having secured funding from Erik Selin, Zwipe should be fully funded through commercial launches. We updated our forecast after the Q2 report as we saw a delay in the take-off and the cash injection creates a cushion. We increase the financial rating from a 1 to a 2 considering this. Raised confidence in the long-term story While the disruptions caused by the lack of electronic components hurts in the near term, we think the sky is about to become clearer. We think there is a very high probability that Zwipe Pay One will receive the necessary certifications and that leaves us with the pilots. Zwipe announced three pilots in the third quarter and one after the period and we expect more to come and are also eager to find out the results from the current ones. This should lead to investors getting more confident in the long-term story of a biometric card in everybody’s pocket with Zwipe gaining a large share of the market. Due to increased sales estimates in the long term we raise our base case valuation from NOK 27 to NOK 32. Zwipe Sector: Biometrics REDEYE RATING 4 3 2 ZWIPE VERSUS OMXSPI 0 5 10 15 20 25 30 35 40 27-okt 25-jan 25-apr 24-jul 22-okt OMXSPI Zwipe Financials People Business FAIR VALUE RANGE

Transcript of Key Financials (NOKm) 2019 2020 2021E 2022E 2023E

Important information: All information regarding limitation of liability and potential conflicts of interest can be found at the end of the report Redeye, Mäster Samuelsgatan 42, 10tr, Box 7141, 103 87 Stockholm. Tel. +46 8-545 013 30, E-post: [email protected]

Key Financials (NOKm) 2019 2020 2021E 2022E 2023E

Revenues 2 2 4 65 446

Revenue growth 21% 139% 1378% 588%

EBITDA -96 -60 -71 -51 35

EBIT -96 -62 -73 -52 34

EBIT Margin (%) -6328% -3370% -1672% -80% 8%

Net Income -96 -62 -74 -47 34

EV/Revenue 434,3 368,0 184,0 13,2 1,8

EV/EBITDA neg neg neg neg 23,7

EV/EBIT neg neg neg neg 23,9

Research Update

Equity Research 2 November 2021

KEY STATS

Ticker ZWIPE Market Merkur Mkt

Share Price (NOK) 27 Market Cap (NOKm) 1000 Net Debt (NOKm) -180 Free Float (%) 75%

Avg. daily volume ('000) 25

BEAR BASE BULL

6

32

46

The Four Pillars of Value Redeye raises the valuation of Zwipe driven by increased confidence in

mass market adoption turning into higher sales estimates. We think

Zwipe is well positioned with a strong financial position. Larger

commercial orders will be a catalyst for the share price.

Increasing the pie

Zwipe continue to show their strong deal making capabilities by reaching new

agreements every month. Between today and our last longer update on the 17th

of July they have announced that they are under evaluation with a Global Tier 1

Smartcard Manufacturer, they received two commercial orders from Beautiful

Cards Corporation and Inkript, and they also announced pilots with MEPS,

Reltime, Credit Lebanaise and a Global Tier-1 Bank. And that was just part of the

announcements, we will leave a brief comment on all in this update.

Stable financial situation

Having secured funding from Erik Selin, Zwipe should be fully funded through

commercial launches. We updated our forecast after the Q2 report as we saw a

delay in the take-off and the cash injection creates a cushion. We increase the

financial rating from a 1 to a 2 considering this.

Raised confidence in the long-term story

While the disruptions caused by the lack of electronic components hurts in the

near term, we think the sky is about to become clearer. We think there is a very

high probability that Zwipe Pay One will receive the necessary certifications and

that leaves us with the pilots. Zwipe announced three pilots in the third quarter

and one after the period and we expect more to come and are also eager to find

out the results from the current ones. This should lead to investors getting more

confident in the long-term story of a biometric card in everybody’s pocket with

Zwipe gaining a large share of the market. Due to increased sales estimates in

the long term we raise our base case valuation from NOK 27 to NOK 32.

Zwipe Sector: Biometrics

REDEYE RATING

4

32

ZWIPE VERSUS OMXSPI

0

5

10

15

20

25

30

35

40

27-okt 25-jan 25-apr 24-jul 22-okt

OMXSPI Zwipe

Financials

People

Business

FAIR VALUE RANGE

REDEYE Equity Research Zwipe 02 11 2021

2

The Four Pillars of Value Let's start with an update to our investment thesis of Zwipe. In our latest longer update in July, we focused on four

pillars:

• Mass-market adoption

• Probability for mass-market adoption versus a niche market

• Size of the market

• Market share

• Technology leadership

• Go-to-market execution

• Competition

• Time to end of life

• For how many years do we think the market for biometric cards to exist

• Margins

• Operating margins at scale

We have summarized our estimates in the model below:

Source: Redeye Research

We will get back to these pillars in our longer updates for investors to grasp how we view and monitor the situation

and make it easy for investors to benchmark these factors against our view. Let's dig deeper!

Market

As we have discussed in previous updates the market for payment cards is around 4 billion units per year and

growing. The growth mainly stems from cash losing ground to payment cards as well as mobile payments.

McKinsey recently released their global payments report in which they state that the pandemic accelerated the

declines in cash usage and adoption of electronic and e-commerce transaction methods which they think will

continue. “Cash payments declined by 16 percent globally in 2020, performing in line with the projections we made last

fall for most large countries (Brazil 26 percent decline, United States 24 percent decline, United Kingdom 8 percent

decline).” In Australia, the adoption of digital wallet usage surged 90 percent from March 2020 to March 2021 at

which 40% of all contactless volume came from digital wallets. The increase in e-commerce volumes is a threat to

biometric payments as the technology is not needed when authenticating a payment online.

REDEYE Equity Research Zwipe 02 11 2021

3

Source: https://unctad.org/press-material/global-e-commerce-jumps-267-trillion-covid-19-boosts-online-retail-sales

Payment Cards and Mobile issued a report earlier in 2021 where they described their estimates for payment

methods online vs offline in the years to come. What is interesting to note is that they believe the adoption of cards

and mobile wallets in offline transactions will continue to grow.

Source: https://www.paymentscardsandmobile.com/global-payments-report-trends-in-global-payments/

Analysis from UBS and Goode Intelligence during 2021 shows that they think biometric payment cards could reach

15-20% penetration by 2026. We have used the lower range of those assumptions and have set a 75% probability on

a mass market as we think the odds are favorable for this to happen. This is more optimistic than our earlier view.

Hence we raise our sales estimates from 2024 onwards. The main reasons for our optimistic view are that

REDEYE Equity Research Zwipe 02 11 2021

4

consumer surveys show that they prefer biometric cards to alternatives, they are willing to pay extra for it which

improves the business case for banks. Humans are creatures of habit, and payment cards are the leading payment

option in most regions. The most significant risk in our view comes from mobile payment solutions, where a longer

delay for biometric payment cards could lead to mobile payments securing a stronger position (i.e. humans change

their habits). In a few countries, such as China, that payment method dominates completely but, in most markets,

both cards and mobile continue to grow by increasing their respective share of the wallet at the expense of cash.

The benefit for mobile is that biometrics or face recognition is already part of the authentication. We however note

that mobile is still a small share of total payments. In a recent interview Jean-Marie Dragon, Head of Electronic

Banking and Innovative Payments at BNP Paribas describes how the bank is betting on both biometric payment

cards and mobile payments and that mobile is growing fast but only makes up around 5% of transactions today

(https://california18.com/biometric-card-we-are-moving-from-experimentation-to-generalization-bnp-

paribas/936502021/). Dragon also confirms our view of strong habits with cards “On the French market, customers

are still very attached to the card. We can clearly see the success of contactless and the habit that has been taken. If

the card is to disappear, it will take several more years.” In the latest issue of the Nilson Report they are estimating

payment cards to continue to increase at a strong rate where cards in circulation is projected to increase from

around 25.2 billion in 2021 to 31.44 billion in 2026 (Nilson Report – Cards Projected Worldwide). According to the

ECB the number of payment cards issued in the Euro area increased by 6.5% in 2020.

Another risk apart from mobile is that the hygiene factor that has been top of mind during the pandemic will

become less of a concern in the future, causing consumers to become less interested in biometric payment cards

than shown in recent surveys. If biometric payment cards instead become a smaller niche market, we think it will be

hard for actors such as Zwipe to earn a living, thereby turning into our bear case of NOK 6.

As a summary we estimate that there will be 4.3 billion payment cards issued in 2021 growing to 5.6 billion in 2026

with a 15% penetration of biometric cards at the end of the period turning into around 840 billion biometric smart

cards (our earlier view was 10% or around 550 million cards).

How do we track our assumptions and what could cause us to change our view? Pilots are signs in the right

direction, but the industry participants need to convert it to large orders. We are therefore closely following any

developments from the ongoing pilots from BNP Paribas, Rocker and Zwipe. Positive results could cause us to

increase the probability from 75% of mass market take off, while negative results could cause us to bring down our

estimates.

Market share

As we have written in our earlier updates, we think Zwipe stands out with its clear focus on the biometric payment

market, where they are practically running circles around their larger competitors. The sales organization continues

to deliver while the technology is among the best in class. The competitors in the emerging market is both card

manufacturers and other technology providers. It’s difficult to find the latest data of market shares for the

manufacturing of payment cards today and the most updated data we can find is from 2018.

Estimated biometric payment cards market

2021 2022 2023 2024 2025 2026

Total EMV payment cards shipped (bn. units) 4,3 4,5 4,8 5,1 5,4 5,6

BSC share of total cards 0% 0% 2% 5% 10% 15%

Biometric smart cards (mil. units) 0,9 11 102 254 536 837

Source: Redeye Research, The Nilson Report, Other industry sources

REDEYE Equity Research Zwipe 02 11 2021

5

Source: Statista 2021

If we calculate with that the market shares have continued as is and that the market shares are the same for

magnetic strips and EMV chip cards then the market shares in percent is in the following range:

Source: The Nilson Report, Redeye Research

There are numerous smaller players in the “Others” category which Zwipe is partnering up with and they have

around 22 of the 50 largest manufacturers as announced partners and are in dialogue with more than 40. While the

largest players still focus mainly on their cash cows which are the EMV chip cards and magnetic strips Zwipe are

taking a strong position in the emerging market. Other technology providers such as IDEX, NXP, Infineon and

Fingerprint Cards are also aiming to take a piece of the pie (see our latest update from July for more details on

each). We think the market will become more competitive over time if the market becomes large. A 15% market

penetration in 2026 leads to roughly 840 million biometric payment cards. We estimate Zwipe's market share to

land at around 11% or roughly 90 million cards and then leveling off to around 9% in the longer term. We handicap

REDEYE Equity Research Zwipe 02 11 2021

6

these figures with our view of a 75% probability for market take-off. Zwipe targets NOK 1 billion in annualized

revenue in the medium term, which we assume to be around 2024. With our estimates we land at around NOK 700

million in 2024.

Source: Redeye Research

Time to end of life

We think Zwipe will capture most of its value within the next 15 years. We are hesitant to estimate a longer lifetime

for biometric payment cards considering the ever-increasing pace of technological innovation and digitalization.

Eventually payment cards will likely become obsolete and be replaced by mobile and other technologies but as we

have seen with cash, it may take a long time (see the following table which describes the decline of cash use

between 2010 and 2020). We are only factoring in Zwipe’s opportunity within payment cards while there is certainly

an option that they could find opportunities in other verticals in the future which we don’t give them credit for in our

analysis.

Source: McKinsey Global Payments Report 2020

Margins

Base case volumes (mil.) & market share (%)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

500

1000

1500

2000

2500

3000

2022 2023 2024 2025 2026 2027 2028 2029 2030

Ma

rke

t sh

are

Zw

ipe

Mill

ion

ca

rds

Total Zwipe volumes Biometric smart cards Zwipe market share of biometric cards

REDEYE Equity Research Zwipe 02 11 2021

7

First, we think the average selling price (ASP) will trend from around USD 5 in 2023 to USD 3 in 2026 and further to

roughly 2 in 2030. Our view is that the gross margins will start at a high level , around 35%, and trend down to around

20% during the same time, driven by higher competition and lower ASP. Zwipe has guided for gross margins around

40% in the medium term as they believe the ASP will stay higher for longer. We think Zwipe will keep the operating

expenses tight, meaning healthy EBIT margins of around 10-15% (Zwipe has guided for EBITDA margins of 20% in

the medium term when reaching NOK 1 bn and growing with sales). In the terminal value calculation for the year

2035, we use an EBIT margin of 7% driven down by higher competition.

To sum it up

Our assumptions of a 75% probability of mass-market adoption, a market share of roughly 10% in the mid-to-long

term, 15 years to end of life, an EBIT margin of around 10-15% between 2024 to 2030, and then leveling off at 7%

and using a WACC of 13% we reach an updated base case value of NOK 32 per share. Our updated view is mainly

driven by us being more optimistic about mass-market adoption while we keep our estimates on margins and

market share largely intact. We don't put any value into potential new segments such as wearables in this valuation.

In our bull case valuation, we increase the probability for mass-market adoption to 100% and reach a valuation of

NOK 46 which is line with our earlier bull case valuation.

Market development in the quarter There has been news from banks. Both BNP Paribas and Credit Agricole have released biometric cards as a

premium offering for EUR 24 per year. That is in line with our expectations that biometric cards will start as a

premium product before turning into a mass market. It's a bit of a chicken and egg problem where volume is

needed to get prices down, which is why Zwipe has a global strategy. A small share of the whole market still means

significant volumes.

Mastercard recently mentioned that they will stop issuing payment cards with magnetic strips in 2024 and stop

supporting them in 2033. This is interesting from many perspectives:

1. It shows how slow technology jumps within payments are. Zwipe's CEO has mentioned this for a long

time. Many investors may be too focused on the threat for possible new generations of biometric cards.

2. The step from EMV chips to biometric cards is closer than from magnetic strips from a user perspective

(still tap and pay) and an industry perspective (no need to replace existing payment terminals).

These developments support our 75% probability for mass-market take-off as outlined earlier.

Assumptions for Zwipe payment card sales

2021 2022 2023 2024 2025 2026 2027

Zwipe's share of total market (%) 8% 13% 13% 13% 12% 11% 10%

Zwipe cards (mil) 0,07 1,1 9,9 23,9 47,3 68,6 87,5

ASP (USD) 7,5 7,2 5,3 4,5 3,7 3,2 3,1

Zwipe payment card sales (NOKm) 4 65 446 908 1480 1845 2325

Source: Redeye Research

Earnings estimates (NOKm)

2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Total sales (NOKm) 4 65 446 908 1480 1845 2325 2414 2225 2238

whereof payment cards 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Gross margin 50% 35% 28% 24% 21% 21% 20% 19% 19% 19%

OPEX -75 -75 -90 -100 -110 -125 -150 -160 -170 -180

Operating profit/loss -73 -52 34 117 204 262 316 310 256 248

Tax 0% 0% 0% 0% 0% 20% 20% 20% 20% 20%

EPS (NOK) -1,98 -1,42 0,91 3,16 5,50 7,08 8,53 8,37 6,91 6,71

Source: Redeye Research

REDEYE Equity Research Zwipe 02 11 2021

8

Commercial progress Zwipe continues to show its strong deal-making capabilities by reaching new agreements continuously. Between

today and our last longer update on 17 July, they received two commercial orders from Beautiful Cards Corporation

(BCC) and Inkript (3 September). The order from BCC is substantial, with USD 1.9m or around 190 to 380 thousand

cards depending on the price point, which was not disclosed (we estimate it to be between 5-10 USD per card as it’s

only technology deliveries and not the whole card). The order will deliver in 2022 with an option of 2023 if the

market takes off slower than expected. BCC produces 20 million EMV payment cards today, so it's still a minor

share at less than one percent of the yearly production.

The order from Inkript, a digital security provider in the Middle East and Africa region, is small at USD 318 000,

where they are aiming for pilots from late 2021 and commercial rollouts from 2022. Inkript is a large player in the

region, supplying around 100 million smart cards per year. We think the order size is somewhere in the range of 15-

30 thousand cards with the same price points as discussed above. We believe there will be a mix of large and small

orders in the future, considering Zwipe's broad strategy and that the market is not at scale yet. Inkript placed a

minor order in 2020 to evaluate Zwipe Pay ONE. On 16 August, Zwipe announced a pilot with key decision-makers in

the same region through MEPS.

Pilot with Global Tier 1-Bank

Zwipe announced a pilot with MEPS, a Global Tier-1 Bank (which we commented on earlier) and Reltime. After the

quarter Zwipe also announced a pilot with Credit Libanais.

The news about Zwipe entering a pilot with one of the largest banks in Europe was a testament to its potential with

its product. They will partner with the bank to pilot a few hundred cardholders in three European countries in Q1

2022, with a potential commercial launch in the middle of 2022. The largest European banks measured in the

number of customers are Banco Santander with 148 million, BBVA with 80.7 million, Credit Agricole with 52 million,

HSBC with 40 million, and ING Group with 39 million. It's unlikely to be Credit Agricole as they recently mentioned

that they are launching commercially after having already completed the pilot stage. Still, the range is between 39 to

148 million.

We still have no news of which bank it is, but that will become clear in Q1 2022 at the latest as we think the bank will

announce the pilot by then.

Partnership with Global Tier 1-Smartcard Manufacturer

There are three Tier-1 card manufacturers: Idemia, Thales, and G+D, where Zwipe already partners with Idemia on

the technology side. This leaves Thales and G+D as potential customers in the recent press release. Our research

shows that Thales sells around 900 million payment cards yearly while G+D sells over 500 million. We don't want to

speculate too much around the identity, but we know that Thales was a former partner who decided to go separate

ways, while G+D is a current partner with Zwipe on wearables.

While the ASP will likely be lower with this potential partnership (as it will likely not include all components as is

expected to be custom with the smaller card manufacturers), it offers a significant opportunity for Zwipe to reach a

significant scale. It will probably take until around year-end before we get to know the current evaluation results,

which will include considerable testing and verification. Still, we see this as yet another confirmation that Zwipe has

a highly competitive product. It took us by surprise as we thought the Tier -1 players were too big for Zwipe.

We still don't know who the partner is but expect news on this shortly. Zwipe's CEO mentioned during the quarterly

webcast that he hopes for news during the fourth quarter. We believe it may be a significant positive trigger for the

stock, while there is undoubtedly downside potential if the parties decide to go separate ways.

REDEYE Equity Research Zwipe 02 11 2021

9

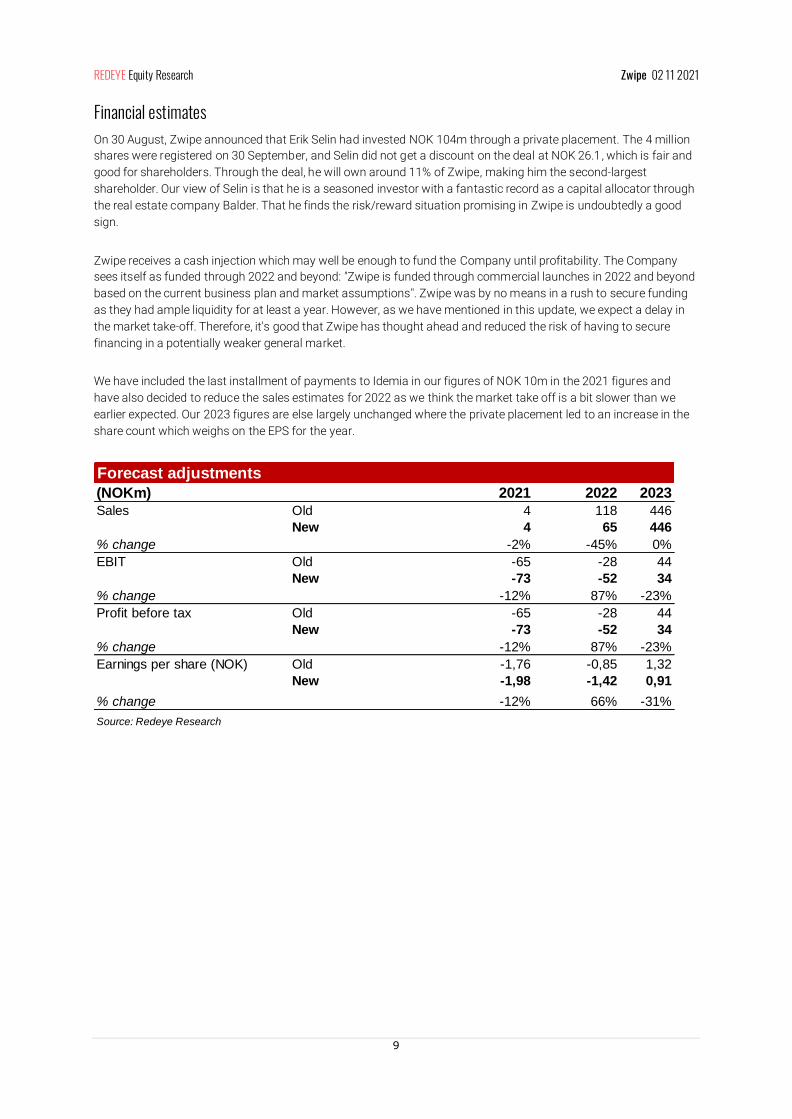

Financial estimates On 30 August, Zwipe announced that Erik Selin had invested NOK 104m through a private placement. The 4 million

shares were registered on 30 September, and Selin did not get a discount on the deal at NOK 26.1, which is fair and

good for shareholders. Through the deal, he will own around 11% of Zwipe, making him the second-largest

shareholder. Our view of Selin is that he is a seasoned investor with a fantastic record as a capital allocator through

the real estate company Balder. That he finds the risk/reward situation promising in Zwipe is undoubtedly a good

sign.

Zwipe receives a cash injection which may well be enough to fund the Company until profitability. The Company

sees itself as funded through 2022 and beyond: "Zwipe is funded through commercial launches in 2022 and beyond

based on the current business plan and market assumptions". Zwipe was by no means in a rush to secure funding

as they had ample liquidity for at least a year. However, as we have mentioned in this update, we expect a delay in

the market take-off. Therefore, it's good that Zwipe has thought ahead and reduced the risk of having to secure

financing in a potentially weaker general market.

We have included the last installment of payments to Idemia in our figures of NOK 10m in the 2021 figures and

have also decided to reduce the sales estimates for 2022 as we think the market take off is a bit slower than we

earlier expected. Our 2023 figures are else largely unchanged where the private placement led to an increase in the

share count which weighs on the EPS for the year.

Forecast adjustments

(NOKm) 2021 2022 2023

Sales Old 4 118 446

New 4 65 446

% change -2% -45% 0%

EBIT Old -65 -28 44

New -73 -52 34

% change -12% 87% -23%

Profit before tax Old -65 -28 44

New -73 -52 34

% change -12% 87% -23%

Earnings per share (NOK) Old -1,76 -0,85 1,32

New -1,98 -1,42 0,91

% change -12% 66% -31%

Source: Redeye Research

REDEYE Equity Research Zwipe 02 11 2021

10

Investment Case Opportunistic with Great Value Proposition

In 2019 Zwipe partnered with the world's second largest card manufacturer, Idemia – a clear indication of its

competitiveness. This improves the ability to manufacture biometric smart cards (" BSCs") cost-efficiently, in turn,

imperative to the success of BSCs. Zwipe has consistently built on its position by partnering up with many actors in

the payments ecosystem while larger actors (such as the larger card manufacturers) have moved slowly. Zwipe has

nothing to protect while large card manufacturers have their cash cows in the existing EMV payment cards and are

ripe for disruption.

Strong IP and a market moving in the right direction

Through the partnership with Idemia, Zwipe targets a reduction of card costs by over 50%, implying potential cost

leadership. We view Idemia and Zwipe's IP as strong cards up Zwipe's sleeve. Zwipe has been granted wide patent

protection for how terminals identify a biometric card, a prerequisite for processing biometric contactless

payments. In an emerging market, technology in and of itself is not sufficient. We see continuous signs for a market

take-off. We believe, however, the cheaper card stemming from the Idemia/Zwipe solution can facilitate

commercial volumes from 2022. Contactless BSCs combine state-of-the-art security and the highest convenience,

i.e. there is no need for a cap (using PIN codes), meaning faster retail checkout. This should render more

transactions and revenue for the issuing banks. Thus, BSCs are simply too good not to happen.

Roadblocks on the way

One of the challenges for Zwipe and the market as a whole is further delay in take-off. There are other solutions

than cards, such as mobile phones with strong authentication solutions through biometrics or face recognition. A

larger share of the younger population is using their mobile phones as the primary way to pay. Another challenge is

around the actual user-friendliness of biometric cards. With the current technology, it takes up to a second to finish

a transaction which is not much. However, the authentication using a biometric card may not always be smooth.

There is risk for the shoppers having to re-authenticate several times before finishing a transaction, thereby

increasing friction. This leads to our view of a 75% probability for mass-market adoption.

Commercial orders to drive the stock

Commercial orders can drive the stock towards our base case of NOK 32. Our bear case is based on failed market

traction and a fire sale of the IP at NOK 6 per share. In our bull case, we see a significant upside to NOK 46 based on

higher BSC penetration. The wide fair value range illustrates the uncertainty of Zwipe's market.

REDEYE Equity Research Zwipe 02 11 2021

11

Valuation

Bear Case 6 NOK Base Case 32 NOK Bull Case 46 NOK In our bear case we see the market scaling at a very slow pace - too slow for Zwipe to cover its costs. In this scenario, we believe larger players like NXP can survive as they have more economic muscles behind them and can wait for the market to really take-off. Zwipe does not have strong institutional ownership and another rights issue could prove hard, especially if the stock market in general is experiencing a significant downturn. Also, it is yet uncertain how the large change in the organization and new collaboration with Idemia will pan out. We, therefore, assume that Zwipe will not be able to continue in its current shape and instead tries to monetize its strong IP portfolio, especially its wait time extension patent, and possibly also in post-placement, outside Europe. As Zwipe has spent around NOK 300m this far, we believe a reasonable value of the IP is half of these investments. This corresponds to NOK ~150m that Zwipe could possibly receive in a fire sale of its strong IP portfolio. Moreover, we assume there is value of at least NOK 50m in e.g. the expertise and knowhow, meaning a bear case of NOK 6 per share.

Our valuation scenarios are based on years 2021-2035 and the payment cards. All scenarios use a required rate of return of 12% and a terminal growth of -10%. We expect the market share for biometric payment cards will reach 15% of total cards in 2026 equaling around 840 million cards growing to 2.2 billion in 2030. We handicap this by setting our probability for mass market adoption to 75%. As for Zwipe's market share, we expect it to begin at 13%, average 10% during the period and drop to 9% by 2030. All in all, this implies volumes for Zwipe reaching ~150 million in 2030, following a ~50% CAGR between 2022 and 2030. We expect the ASP to start at about USD 7 (including sensors), dropping to ASP 2, averaging USD 2 over the whole period, since the higher volumes are delivered in the end of the period, when ASP is lower. Our ASP and volume assumptions above means a sales CAGR of ~40% and payment BSC sales reaching about NOK 1.2 bn in 2030. We expect the gross margin to start at slightly above 30% (incl lower margins for sensors) and then we assume it will come down to ~20% due to competitive dynamics. We assume the average gross margin over the whole period will be 21%. We expect OPEX to grow by CAGR 7%, averaging about 8% of sales from 2026. The following leads to EBIT margins of on average 12% over the period. We assume a long-term EBIT margin of 7%.

The differing parameter in our optimistic scenario, compared to base case, is that we increase the probability for mass market adoption from 75% to 100% and adjust Zwipe's volumes accordingly. With a BSC market penetration of 30% of all payment cards sold globally, instead of 15% as in the base case, we derive a fair value of NOK 46. The discrepancy from our base case shows the innate potential for Zwipe if biometric cards can gain a larger market share. We assume similar cost levels as in base case. Consequently, we assume average EBIT margins of 12%. Our long-term EBIT margin is 7%

REDEYE Equity Research Zwipe 02 11 2021

12

Catalysts Pilots

The most important catalyst during the next 12 months, in our view, is card pilots, from existing and new

partnerships.

IMPACT Downside Upside Time Frame

Significance Likelihood Significance Likelihood Minor Unlikely Major Highly likely Mid

Increased hygiene focus

The Coronavirus has highlighted the critical hygiene aspects of contactless biometric cards as people are becoming

reluctant to touch the terminals. We see a chance that this could prove to be a game-changer for Zwipe in the long

term.

IMPACT Downside Upside Time Frame

Significance Likelihood Significance Likelihood Minor Possible Major Possible Long

Large commercial order for Zwipe Pay ONE

Pilots are one thing, but commercial orders from the Idemia collaboration will prove a substantial value in Zwipe's

offering. The first commercial orders have arrived, which have led to a valuation at our base case, and we are

awaiting news for further substantial orders.

IMPACT Downside Upside Time Frame

Significance Likelihood Significance Likelihood Major Unlikely Major Possible Mid term

Proven breakthrough in production costs

The costs are expected to come down with scale in production. The goal is to get the total card costs down to USD

5 per card, which we think will likely happen in the next couple of years driven by high volumes.

IMPACT Downside Upside Time Frame

Significance Likelihood Significance Likelihood Major Unlikely Major Possible Long

REDEYE Equity Research Zwipe 02 11 2021

13

Summary Redeye Rating The rating consists of three valuation keys, each constituting an overall assessment of several factors that are

rated on a scale of 0 to 1 points. The maximum score for a valuation key is 5 points.

Rating changes in the report People upgraded from 3 to 4. Financials upgraded from 1 to 2.

People: 4

We arrive at an average people rating (4/5) where the most positive aspect is the skill set and experience in the management team

and board, following recent additions. A large part of the management team has now been in place for a period of 3+ years and

they have shown their capabilities in attracting several key employees with long experiences in the sector. While the CEO has

increased his ownership considerably we would like to see an even higher ownership stake. Regarding capital allocation skills it's

too early to judge as partnerships have not turned into sales at this stage and more time is needed to know if the capital ha s been

employed in the best possible way. We think the company could be even more upfront on communicating near-term challenges.

Business: 3

Biometric payment cards have been considered around the corner for several years, yet the market does not exist today. However,

we expect it to quickly emerge as soon as costs come down to adequate levels, given the strong advantages of biometric

payment cards. Considering the 4 billion payment cards that are shipped each year, even a moderate penetration implies

significant growth opportunities. Zwipe's business model is scalable when volumes ramp. The expertise of Zwipe is also valida ted

by partnerships with large players like e.g., Idemia, which compensates for its tiny size (pre-revenue etc.). The payment industry is

slow moving, which creates a barrier to entry, but it is hard to identify how sustainable the competitive advantages are at this early

point in time. However, competition is positive in this stage, as it will help starting the market.

Financials: 2

Following raising NOK 104m in a recent directed share issue, Zwipe has a strong financial position. We therefore raise our

financial rating from a 1 to a 2 in this update. Zwipe is, however, still essentially pre-revenue and therefore unprofitable, which

weighs on the financials rating, but the scalable business model means Zwipe can quickly scale when sales ramp up and

consequently reach break-even.

REDEYE Equity Research Zwipe 02 11 2021

14

2020 2021 E 2022E 2023E D C F Valuation Metrics S um F C F (N O Km)IN C O ME S T AT E ME N T Initial Period (2021–2023) -30

Revenues 2 4 65 446 Momentum Period (2024–2030) 700

Cost of Revenues 5 2 42 323 Stable Period (2031–) 339

Gross Profit -3 2 23 124 Firm Value 1010

Operating Expenses 57 73 74 89 Net Debt -180

EBITDA -60 -71 -51 35 Equity Value 1190

Depreciation & Amortization 2 3 1 0 Fair Value per Share 32,17

EBIT -62 -73 -52 34

Net Financial Items 0 0 5 0 2020 2021 E 2022E 2023EEBT -62 -74 -47 34 C APIT AL S T RU C T U REIncome Tax Expenses 0 0 0 0 Equity Ratio 0,9 1,0 1,0 1,0

Non-Controlling Interest 0 0 0 0 Debt to equity ###### 0,0 0,0 0,0

Net Income -62 -74 -47 34 Net Debt ###### -191 -145 -179

Capital Employed 124 200 153 187

BALAN C E S HE E T Working Capital Turnover -0,2 4,6 ###### ######

As s e tsCurrent assets G RO W T HCash & Equivalents 125 191 145 179 Revenue Growth 21% 139% 1378% 588%

Inventories 0 1 0 0 Basic EPS Growth ###### ###### -36% -173%

Accounts Receivable 1 1 0 0 Adjusted Basic EPS Growth ###### 5% -36% -173%

Other Current Assets 0 0 0 0

Total Current Assets 127 193 145 179 PRO F IT ABIL IT YROE -61% -46% -27% 20%

Non-current assets ROCE -50% -37% -34% 18%

Property, Plant & Equipment, Net 3 2 1 1 ROIC 805% -501% -694% 457%

Goodwill 0 0 0 0 EBITDA Margin (%) -3260% -1607% -79% 8%

Intangible Assets 7 7 7 7 EBIT Margin (%) -3370% -1672% -80% 8%

Right-of-Use Assets 0 0 0 0 Net Income Margin (%) -3379% -1675% -73% 8%

Shares in Associates 0 0 0 0

Other Long-Term Assets 0 0 0 0

Total Non-Current Assets 10 9 8 8 VALU AT IO NBasic EPS 0,0 -2,0 -1,3 0,9

Total Assets 137 202 153 187 Adjusted Basic EPS -1,9 -2,0 -1,3 0,9

P/E neg neg neg 29,1

L iabilities EV/Revenue 368,0 184,0 13,2 1,8

Current liabilities EV/EBITDA neg neg neg 23,7

Short-Term Debt 0 0 0 0 EV/EBIT neg neg neg 23,9

Short-Term Lease Liabilities 0 0 0 0 P/BAccounts Payable 3 1 0 0

Other Current Liabilities 11 1 0 0

Total Current Liabilities 14 1 0 0 S HARE HO LD E R S T RU C T U RE C APIT AL %VO T E S %Vasastaden Holding AB 16,9% 16,9%

Non-current liabilities Erik Selin 10,8% 10,8%

Long-Term Debt - 0 0 0 Lars Windfeldt 4,6% 4,6%

Long-Term Lease Liabilities 0 0 0 0 Avanza Pension 3,7% 3,7%

Other Long-Term Liabilities 1 0 0 0 Jörgen Lantto 2,6% 2,6%

Total Non-current Liabilities 1 0 0 0

S HARE IN F O RM AT IO NNon-Controlling Interest 0 0 0 0 Reuters code ZWIPE:SS

Shareholder's Equity 123 200 153 187 List Merkur Mkt, First North

Total Liabilities & Equity 137 202 153 187 Share price 27

Total shares, million 37

C AS H F LO WNOPAT -62 -73 -52 34

Change in Working Capital 59 -13 1 0 M AN AG E ME N T & BO ARDOperating Cash Flow -60 -38 -46 35 CEO André Løvestam

CFO Lars Kristian Solheim

Capital Expenditures 0 0 0 0 Chairman Jörgen Lantto

Investment in Intangible Assets -2 -1 0 0

Investing Cash Flow -2 -1 0 0

AN ALY S T S Redeye ABFinancing Cash Flow 226 105 0 0 Niklas Sävås Mäster Samuelsgatan 42, 10trFree Cash Flow -62 -39 -46 35 111 57 Stockholm

REDEYE Equity Research Zwipe 02 11 2021

15

Redeye Rating and Background Definitions Company Quality

Company Quality is based on a set of quality checks across three categories; PEOPLE, BUSINESS, FINANCE. These

are the building blocks that enable a company to deliver sustained operational outperformance and attractive long-

term earnings growth.

Each category is grouped into multiple sub-categories assessed by five checks. These are based on widely

accepted and tested investment criteria and used by demonstrably successful investors and investment firms.

Each sub-category may also include a complementary check that provides additional information to assist with

investment decision-making.

If a check is successful, it is assigned a score of one point; the total successful checks are added to give a score for

each sub-category. The overall score for a category is the average of all sub-category scores, based on a scale that

ranges from 0 to 5 rounded up to the nearest whole number. The overall score for each category is then used to

generate the size of the bar in the Company Quality graphic.

People

At the end of the day, people drive profits. Not numbers. Understanding the motivations of people behind a business

is a significant part of understanding the long-term drive of the Company. It all comes down to doing business with

people you trust, or at least avoiding dealing with people of questionable character.

The People rating is based on quantitative scores in seven categories:

• Passion, Execution, Capital Allocation, Communication, Compensation, Ownership, and Board.

Business

If you don't understand the competitive environment and don't have a clear sense of how the business will engage

customers, create value and consistently deliver that value at a profit, you won 't succeed as an investor. Knowing

the business model inside out will provide you some level of certainty and reduce the risk when you buy a stock.

The Business rating is based on quantitative scores grouped into five sub-categories:

• Business Scalability, Market Structure, Value Proposition, Economic Moat, and Operational Risks.

Financials

Investing is part art, part science. Financial ratios make up most of the science. Ratios are used to evaluate the

financial soundness of a business. Also, these ratios are key factors that will impact a company's financial

performance and valuation. However, you only need a few to determine whether a company is financially strong or

weak.

The Financial rating is based on quantitative scores that are grouped into five separate categories:

• Earnings Power, Profit Margin, Growth Rate, Financial Health, and Earnings Quality.

REDEYE Equity Research Zwipe 02 11 2021

16

Redeye Equity Research team

Management Björn Fahlén

Tomas Otterbeck

Technology Team Hjalmar Ahlberg

Henrik Alveskog

Mattias Ehrenborg

Douglas Forsling

Forbes Goldman

Jesper Henriksson

Viktor Lindström

viktor.lindströ[email protected]

Fredrik Nilsson

Mark Siöstedt

Jacob Svensson

Niklas Sävås

Danesh Zare

Editorial

Joel Karlsson

Mark Siöstedt

Life Science Team Gergana Almquist

Frank H Andersen

Oscar Bergman

Christian Binder

Filip Einarsson

Mats Hyttinge

Erik Nordström

Richard Ramanius

Kevin Sule

Fredrik Thor

Johan Unnerus

REDEYE Equity Research Zwipe 02 11 2021

17

Disclaimer Important information Redeye AB ("Redeye" or "the Company") is a specialist financial advisory boutique that focuses on small and mid -cap growth companies in the Nordic region. We focus on the technology and life science sectors. We provide services within Corporate Broking, Corporate Finance, equity research and investor relations. Our strengths are our award-winning research department, experienced advisers, a unique investor network, and the powerful distribution channel redeye.se. Redeye was founded in 1999 and since 2007 has been subject to the supervision of the Swedish Financial Supervisory Authority. Redeye is licensed to; receive and transmit orders in financial instruments, provide investment advice to clients regarding f inancial instruments, prepare and disseminate financial analyses/recommendations for trading in financial instruments, execute orders in financial instruments on behalf of clients, place financial instruments without position taking, provide corporate advice and services within mergers and acquisition, provide services in conjunction with the provision of guarantees regarding financial instruments and to operate as a Certified Advisory business (ancillary authorization). Limitation of liability This document was prepared for information purposes for general distribution and is not intended to be advisory. The information contained in t his analysis is based on sources deemed reliable by Redeye. However, Redeye cannot guarantee the accuracy of the information. The forward-looking information in the analysis is based on subjective assessments about the future, which constitutes a factor of uncertainty. R edeye cannot guarantee that forecasts and forward-looking statements will materialize. Investors shall conduct all investment decisions independently. This analysis is intended to be one of a number of tools that can be used in making an investment decision. All investors are therefore encour aged to supplement this information with additional relevant data and to consult a financial advisor prior to an investment decision. Accordingly, Redeye accepts no liability for any loss or damage resulting from the use of this analysis. Potential conflict of interest Redeye's research department is regulated by operational and administrative rules established to avoid conflicts of interest and to ensure the objectivity and independence of its analysts. The following applies: • For companies that are the subject of Redeye's research analysis, the applicable rules include those established by the Swedish Financial

Supervisory Authority pertaining to investment recommendations and the handling of conflicts of interest. Furthermore, Redeye employees are not allowed to trade in financial instruments of the Company in question, from the date Redeye publishes its analysis plus one trading day after this date.

• An analyst may not engage in corporate finance transactions without the express approval of management and may not receive an y remuneration directly linked to such transactions.

• Redeye may carry out an analysis upon commission or in exchange for payment from the Company that is the subject of the analysis, or from an underwriting institution in conjunction with a merger and acquisition (M&A) deal, new share issue or a public listing . Readers of these reports should assume that Redeye may have received or will receive remuneration from the company/companies cited in th e report for the performance of financial advisory services. Such remuneration is of a predetermined amount and is not dependent on the content of the analysis.

Redeye's research coverage Redeye's research analyses consist of case-based analyses, which imply that the frequency of the analytical reports may vary over time. Unless otherwise expressly stated in the report, the analysis is updated when considered necessary by the research department, for example in the event of significant changes in market conditions or events related to the issuer/the financial instrument. Recommendation structure Redeye does not issue any investment recommendations for fundamental analysis. However, Redeye has developed a proprietary analysis and rating model, Redeye Rating, in which each Company is analyzed and evaluated. This analysis aims to provide an independent assessment of the Company in question, its opportunities, risks, etc. The purpose is to provide an objective and professional set of data for owners an d investors to use in their decision-making. Redeye Rating (2021-11-01)

Duplication and distribution This document may not be duplicated, reproduced or copied for purposes other than personal use. The document may not be distributed to physical or legal entities that are citizens of or domiciled in any country in which such distribution is prohibited according to appl icable laws or other regulations. Copyright Redeye AB.

Rating People Business Financials

5p 33 15 4 3p - 4p 137 123 43 0p - 2p 5 37 128 Company N 175 175 175

CONFLICT OF INTERESTS

Niklas Sävås owns shares in the company : No Redeye performs/have performed services for the Company and receives/have

received compensation from the Company in connection with this.