Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best...

of 12

-

Upload

joseph-kundu -

Category

Documents

-

view

220 -

download

0

Transcript of Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best...

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

1/12

Whitepaper

Logistics

in

2020:

The

future

is

closer

than

you

think

March2013

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

2/12

KewillWhitepaper:Logisticsin2020

Today,2020seemsarelatively longway in the future.Although itsadate that features inour longerterm

plans, it isntcloseenough formostofus toenvisagepreciselywhatwellbedoing,or translatingstrategic

aims andhighlevel objectives into tactical activities. It isnowover five years from the startof the global

economic downturn, a period in which the world has experienced a series of interdependent regional

economic crises. Following a long periodof debtpowered prosperity and growth in the 1990s and 2000s,

establishedwesterneconomieshaveenduredanextendedhangoveraftertheaffluentearlyyearsofthenew

millennium.

Diminishinghouseholdincomesandconsumerspendingpowerarereflectedinthecutsbusinesseshavebeen

forced tomake in order to reduce costs and remain profitable (or in some casesminimize losses). Some

companieshavechosen to take their logistics inhouse,particularly in thehitech/electronicssectors,whilst

othershavemovedtooutsourcinglogisticsforgreaterflexibilityandcostcontrol.

Andduetoglobalizationtheeffectsofthedownturnhavebeenfeltalmosteverywhere.Whilstmanyregions

havenowexitedrecession,others(inparticularintheEurozone)continuetofeelitsdirecteffectswhilsteven

those thatarewellon theway to recovery still continue to feel thepinch through reduceddemand from

EuropeandNorthAmerica.Evenmanyofthehighgrowthemergingmarketshavetendedtoseegrowthlevel

offclosertosingledigitfigures.

The worldwide impact of the prolonged downturn means that the global logistics industry has been

particularly hardhit.Subduedconsumerdemandandretailsaleshave translated to lowerproduction levels

andconsequently lowershippingvolumes,drivingpermanentchangestothe landscapeanddynamicsofthe

logisticsindustry.

The

industry

is

shaping

up

for

some

radical

changes

and

in

this

paper

we

set

out

how

the

logistics

industry

may

look

in

2020

using

the

data

points

and

trends

that

we

have

today.

This

paper

is

intended

to

help

youshapeyourthinkingandplanningforthefuture.

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

3/12

KewillWhitepaper:Logisticsin2020

LSPsareseekingoutwaysofprotectingtheir

margins,byleveragingeconomiesofscale

throughpartnershipsandnetworksand

takingabiggershareofsupplychainprofits

throughexpandingthereachoftheir

operationsandofferingvalueaddedservices.

Despiteahandfulof keyeconomies continuing to falter, the signsof recoveryarenowevidentwithin the

logistics industryandbeyond.Transportationratesandmarginsmayremainvolatile,reflectingtheongoing

fluctuationsinlocalretailperformance,particularlyforairfreight,butvolumesarestabilizingandroadandrail

freight inparticularareshowingan increasing trend.Sea freightvolumesoverallcontinue tobeaffectedby

overcapacity,withslowsteamingandfewerroutesstillcommon. Mergerandacquisitionactivity levelsare

buoyantandnewpartnershipsbetweenregionalandinternationalLSPsareregularlybeingannounced.

Yet there are a number of challenges ahead. In particular, key operating costs are set to keep increasing.

Spirallingfuelcostsareawelldocumented issueforthe logistics industry,particularlyforthoseoperating in

theEurozonewheregovernmenttaxesexacerbatetheimpactoftheregularperbarreloilpriceincreases. And

labor costs are increasing theworld over; standards of living and averagewages are rising significantly in

emerging markets whilst in more established western

economies, several years of lower birth rates are

beginning to create more competition to attract

employees. LSPs are therefore seeking out ways of

protectingtheirmargins,byleveragingeconomiesofscale

through partnerships and networks and taking a bigger

shareofsupplychainprofitsthroughexpandingthereach

oftheiroperationsandofferingvalueaddedservices.

Time tomarket (speed) and agility to react to changing demand aswell as customer service are key and

potential differentiators. Themodes of transport and sourcing destinations are changing as the customer

criteriachange,withmorenearshoreandsameshoringandmoreroadandrail(versus longseavoyagesor

highcostairfreight)as somesupplynetworkscontractintermsofgeographicdistances.

InWesternmarkets,consumerdemandcontinuestobefocusedaroundhightechgoodssuchassmartphones

and tablet computers,with their reachwidening to ever younger consumersand further into thebusiness

world.Multichannelretailhasfirmlytakenholdwithtechsavvyconsumersincreasinglyshoppingaroundfor

bothvariety

and

price,

shopping

online

and

via

mobiles

as

well

as

continuing

to

visit

physical

stores.

These

consumersexpectfast,oftenfreedelivery,whichputsincreasingpressureonthesupplychainlogistics.

Developingcountries,suchasChinaand India,notonly remainat the forefrontofproduction forhightech

goodsbutarealsoexperiencingagrowingmiddleclassdomesticmarketfortheseandotherproducts.Thereis

strong demand, particularly for branded goods thatwere previously out of the reach of themajority of

householdbudgets.Multichannelhasexpandedatasimilarrapidrateastheseeconomies,withsocialchange

inbuyingpatternsbeingdrivenby technology, fast changing fashion/newproducts,varietyandavailability,

workingpatterns,trafficcongestionandtheabilitytocomparepriceandconvenience.Manyconsumersstill

liketotouchandfeelthegoods first,butthenpricesearchandbuyonlinefromatrustedbrandorretailer.

Inthis

whitepaper

we

take

alook

into

the

future,

at

the

key

issues

affecting

road,

air,

sea

and

rail

freight

and

warehousingby2020,and importantly,how the technology thatunderpins the logistics industry is likely to

havechanged.

Lookingaheadto2020

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

4/12

KewillWhitepaper:Logisticsin2020

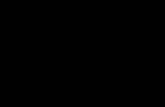

Manufacturer

(goodsentersupply

chain

at

point

of

production)

LocalLSP

(goods

processed,collected

&

loadedinto

shippingcontainer)

International

Customs

(requirements

for

port

of

origin

&

port(s)of

desination)

Global

Freight

Forwarder

(international

transport

by

land,

air&sea)

Local

Customs

(compliance

checkpriorto

releaseof

goods)

LocalLSP

(collectsgoodsfrom

(air)port

&

processedforonward

distribution)

Retailer

(goods

arrive

at

DC)

Technology is, by its verynature, constantly evolving. By the beginning of the 21st century, businesses in

almost every sectorwere already reliant on increasingly sophisticated telecommunications and IT. By the

beginningoftheseconddecade,manywesternmarketscouldboastamobilephoneinuseforeverymember

ofthepopulation,anddoingbusinesswithoutsmartphonesandhandhelddeviceswouldbeunthinkable.

Herearesomeofthekeytechnologydevelopmentsthelogisticsindustrywillbeaffectedbyin2020:

GenerationZ/thepost90sgenerationhaveenteredthemarket,asbothconsumersandemployees.

Having grown up using email, social networking and communications technology such asmobile

/smartphones,MP3players, laptops/tablets andgames consoles, theyhavenever knownaworld

without them.Adeptatswitchingbetweenmultipleplatforms, formatsanddevices, theyexpect to

utilizethetechnologytheyarefamiliarwithintheworkenvironment,acceleratingtheprevalenceof

BringYourOwnDevice (BYOD) in industriesheavily relianton the timely transferofdata, suchas

logistics. They are uncompromising in their expectations from the retail supply chain. Shopping

aroundonline,globally,forthebestpriceandchoice,theyexpectsamedayorrapiddeliveryeither

freeorlowcost,withdefinedtimeslots,anddemandchoicesonwheretheregoodswillbedelivered.

Cloudtechnology

will

be

widely

adopted,

and

enabling

the

sharing

and

re

use

of

data

more

comprehensivelythaneverbefore.Asthenaturalprogressiontoasharedphysicalandfinancialflow,

a shared flow of information and documentation will increasingly exist, improving visibility and

efficiencythroughoutthesupplychain.Inlogisticsthisbringsmajorbenefits,e.g.thestreamliningof

internationalcustomsdeclarationsandimprovedaccuracyoffollowonactivityscheduling.

2020:SharingDataintheGlobalSupplyChain

The diagram above illustrates the example of goodspassing through the supply chainfrompoint ofproduction in,for

exampleChina,

via

alocal

LSP

and

fulfilling

local

and

international

customs

requirements

before

being

transported

via

a

globalfreightforwarder to Europe. Here they again clear customs before beingprocessed by a local LSP andfinally

deliveredtothecustomeramajorretailer. Ideally,ateachstagethenextpartner inthesupplychainmakesuseofthe

previouspartnersdata,enrichingit,augmentingitandsharingitonwards.

Technology

in

2020

Data

Shared,

Augmented

&

Passed

Onwards

Through

Entire

Supply

Chain

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

5/12

KewillWhitepaper:Logisticsin2020

DataasaService(DaaS)hasstartedtobecomeareality.LSPshavebeguntoexchangedataasthey

previouslydidwithotherassets suchas staff, realestate/publicwarehouse, trucks,etc, improving

efficiencyandreducingcosts.This ispartlydrivenbyadesiretoimprovethequantityandqualityof

datashared

and

partly

by

necessity

as

road

carriers

in

particular

partner

and

sub

contract

one

anotherwithgreaterfrequency.

o DatahubssuchasINTTRAandTRAXXONforseaandairhavebecomemorewidespread.

Smartphoneshavebecomea commodity inusebyeveryone from children to theelderlyandare

usedextensivelyforbusinessandpleasure.Email isnowlargelyathingofthepast themajorityof

messages are sent via instantmessaging and socialmedia and contain less than 156 characters.

Marketing/service providershaveadaptedtheirofferingsaccordingly,andthelargerLSPshaveissued

andregularlyupdatesmartphoneappsfortheirsupplychainpartners.

Touch screens areeverywhereatbothhomeandwork andgiveanewdimension to theuser

experience.Businesses

with

more

complex

operations,

such

as

multiple

languages

and

currencies,

sometimesstruggle tokeepupwithacompletechange to touchscreen.On theplusside, training

requirementsandsupportcallshavereduced,duetotheintuitivenessoftouchscreenonthewhole.

RoadfreightrepresentsamajorpartofmostLSPsstrategies.Regardlessoftheimportanceofothermodalities

to global logistics, it is almost impossible for the supply chain to keep moving, either domestically or

internationally, withoutusingtheroadnetwork.

Yet LSPs are facing a number of key challenges in keeping the supply chainmoving via our increasingly

congestedroads:

Fuelpriceshavekeptonrisingandrising.Bynow,thepriceperbarrelofoilwillbeonaverageabout

$150,withmuch higher peaks possible (source: International Energy Agency OilMarketOutlook

2011).Energy

savings

are

amajor

focus

for

LSPs

worldwide,

with

activities

that

maximise

haulage

efficiency, such as groupage/consolidation andparticipation in logistics networks,more important

thaneverbefore.

o LSPscontinuetoexperimentwithgreenfuelsandvehicleinnovations,suchaslongerlength

trailersandbetteraerodynamics,withtheoverallaimofmakingvehiclesmorefuelefficient

anddrivingdown fuelconsumption.Solarpanelsontheroofsoftruckcabsandcontainers

arebynowarelativelycommonsight.

o Manyregionsarebynowbeginningtoseeroadfreightshifttorailover longcrosscountry

routestominimisefuelcostswiththeaddedbenefitofreducingCO2emissions.

Green logistics; traffic congestion has certainly not been resigned tohistory. Themileage tax or

ecotaxhas

been

implemented

in

many

regions

(starting

with

France

in

2013).

Trucks

incur

asurcharge

basedonaveragefueleconomies,withbetterthanaverageincurringalowersurcharge/tax.

Road

freight

in

2020

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

6/12

KewillWhitepaper:Logisticsin2020

o CarriersarenowmeasuredontheirCO2emissionsandcanusethistodifferentiate,nextto

price, quality and speed,with listed companies (both shippers and LSPs) evermindful of

compliancewithincreasingcorporatesocialresponsibilityreportingrequirements.

o

Roadmay

increasingly

be

used

for

the

last

mile,

while

sea

and

rail

are

used

for

long

distance

haulage.The2011publicationofaWhitepaper from theEuropeanCommission concluded

30% of road freight transport over 300 km should shift to othermodes such as rail or

waterbornetransportby2030,andmorethan50%by2050(EuropeanCommission,2011).

o LogisticsDirectors are feeling pressure from the Board to stay aheadof innovations that

make vehiclesmore costeffective, and to continue exploring alternative fuels/modalities.

Laborshortages;theshortageofdriversandwarehouseworkerswillpresentaveryrealchallengeto

thelogisticsindustry.Theinternationalspreadoftheoriginofdriverswillgrow,increasingcomplexity

intermsofhealthandsafetycompliance.Ofgreatestconcernistheforecastincreaseinshareofcost

oflaborforroadtransport,whichissettorisebyupto50%by2025,accordingtovariousstudies.

Reducedinventories;retailersandmanufacturersareincreasingly lookingtoreducetheirinventories,

minimisingtheirowncostsbycarrying lessstock.LSPsareunderpressuretoserviceDCsandstores

withsmaller,more frequentdeliveries.This isdriving them to fill loadsacrossbusinesssectorsand

theyareincreasingly seekingtoenterintocollaborativeagreementswithcustomersandcompetitors

to maintain margins. Achieving flexibility and agility efficiently has become even more critical.

Parcel shipping; the rapid growth of Internet, shop and collect and catalogue shopping is placing

pressureon logisticsserviceproviderstonotonlymanagefull loadandpalletdeliveries,buttoalso

manageparcelshippingonbehalfoftheircustomers.

Trafficcongestion;increasingtrafficcongestionresultsintrucksbeingstuckintrafficsjamsandlosing

valuabletransporttime.Inthefuture,wemayseeincreasinguseoflivetrafficconditionstooptimize

routesorrerouteshipments,andvehicleswillbeconnectedtothe internetasstandardandableto

accessupdates.

4PL;movement towards 4thparty logisticsproviders thatdonotown any assetsbutmanage the

movementofgoodsthroughthesupplychainonbehalfoftheircustomers(singleormultimodal).

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

7/12

KewillWhitepaper:Logisticsin2020

Globalizationhasmeantthatairandseafreightplayamajorroleingettingconsumergoodsfromfruitand

vegetablestocomputergamesontheshelvesinstores(onlineandvirtual).Yetbothmodalitiesarehardhit

bythesuddenchangesinvolumescreatedbylowerorhigherthanexpectedlevelsofconsumerdemandthat

becamecommonfollowingthedownturn.

The

key

issues

on

the

agenda

for

air

and

sea

freight

carriers

are

summarized

below:

Chinaisnowthelargesttradenation,havingovertakentheU.S.astheworldslargesttradingnation

by2016,(accordingtoa2012forecastHSBCHoldingsPlc).Chineseportsandhubandspokenetworks

areofprimaryimportancetoglobalfreightforwarders,andshippingschedulesaredevelopedaround

them.Chinahassignificantlyharmonizeditscustomsrules,whichpreviouslyvariedbyport.Countries

includingChinaare investingheavily in infrastructure tomoveproducts from inlandmanufacturing

sitestotheports.

Improvedsupplychain linkswithemergingeconomies inLatinAmerica,theMiddleEastandAfrica

areontheagendaasChina leverages itsallianceswiththoseregionsand increases importsfrom its

tradingpartners

to

support

its

own

infrastructure

projects.

LSPs

have

begun

to

gear

up

for

increases

in future shipment volumes going the otherway. Rising costs are forcing Chinese companies to

outsourcesomelowskilledandlabourintensiveproductiontolowercostcountries.

NearshoreandonshoringisonceagainbecomingmorepopularinsomeWesterncountries.Thisis

largely for speed to market, agility to react to consumer demands and because the economic

downturncombinedwiththerapiddevelopmentofChinaismakingitcostjustifiable(ifnotcheaper).

Increasing fuel costswill continue to affectmargins; In2004Air FranceKLM spentover 2billion

Euroson fuel.By2010 thiswasalready tripled toover6billionEuros.Carriershavebecomeeven

more sophisticated at measuring profitability of routes and customers, with unprofitable routes

unceremoniouslydroppedandevensharperincreasesinratescommonwherecapacityislimited.

Megacontainers;by2014,several18,000TEUvesselsweredue tobeoperational, forcingamove

towardsahubandspokenetworkduetothelimitednumberofportsthatcanreceivethesevessels

andtheneedtorunasclosetofullcapacityaspossible inordertodelivereconomicrunningcosts.

Thisisleadingtoshippinglineslimitingthenumberofportstheyservice.

o Utilizationandagilityarekeyfactors;speedisincreasinglyimportant operatorscannotwait

forafullloadwithoutmissingcustomersdeliveryduedates.Moreriverandcanalbargesare

underproductiontoservicethehubandspokenetworks,alongwithmoreraillinks.

o Withovercapacityinshippingan issuepriortothe18,000TEUvesselsenteringthemarket

andprerecessionordersforcontainershipshavingpreviouslybeensurplustorequirements,

by2020theremaywellbeahighlycompetitivemarket,resultinginaweakeninginrates.

Air&seafreightin2020

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

8/12

KewillWhitepaper:Logisticsin2020

Inlandwaterways/shortsea;produces80%lessCO2comparedtoroadand30%lessthanrail.AsCO2

reporting legislation comes into place inmore countries there will likely be increasing focus on

environmentalimpact.Andpotentiallyfurthertaxationonpollution,drivingLSPstoadoptgreener

transportmodes.

TrackandTrace;isincreasinglyimportantforsupplychainvisibility,andperformancemeasurement,

asservicelevelsbecomestricterandmoredirectlylinkedtoremuneration.

Withroadcongestion,highfuelpricesandfewerportsbeingservicedbymegacontainerships,the(relatively)

fuelefficientoptionofrailfreightissettoplayamoreimportantroleingloballogisticsgoingforward.

Thekeydriversaroundtheexpansioninrailfreightaresummarizedbelow:

Risingfuelcosts;withroadtransporthardesthitbytheongoing increases,railfreight,whichwhilst

lessflexibleissignificantlymorefuelefficient,isplayingamoreimportantpartinlogisticsstrategies.

Increased Government funding; Governments in established and emerging markets have major

investmentsunderwayandplannedinrail.December2012sawtheopeningofa1,428milerail line

linking Beijing to Guangzhou in only 8 hours, the precursor to a planned 248bn investment to

completea10,000milenetworkby2020,with fourmain linesrunningeast towestand four from

northtosouth.

Speed is imperative;roadnetworksare increasingly unreliable,withcongestioncommonanda lack

ofdirectroutesinsomeareas.

Longdistance;Tocounterthis,LSPsare lookingtorailfreighttocoverlongdistancescrosscountry,

forexampletakinggoodsfromChinatoEurope,asinfrastructuresinformerSovietcountriesreapthe

benefitsof

major

investment.

Panalpina

recently

boosted

its

fast

growing

less

than

container

load

AsiaEuropenetworkwith the launchof three services fromChina and Singapore toHungary, the

CzechRepublicandAustria.Thisoffersshippersa lowercost thanairfreightandfasterservicethan

seacargo.

Green Logistics; more stringent regulation and reporting requirements on both emissions and

measures taken to reduce environmental impact arepushing retailers,manufacturers and LSPs to

utilizerailfreightforlargerportionsofjourneysduetobetterfueleconomy.

Hubandspoke logisticsnetworks; theevolvingnatureofglobal trade,withnewports inemerging

marketsgrowingrapidlyincommercialimportance,alongwiththenowprevalenceofmegacontainer

shipsand

larger

cargo

planes

has

prompted

arise

in

hub

and

spoke

networks

for

global

shipments.

Rail is playing an increasingly important role in getting goods frommajor hub ports to their final

destination.There is increasingfocusonrailterminals,oftenmultimodal,toenableaservicefeeder

Railfreightin2020

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

9/12

KewillWhitepaper:Logisticsin2020

concept.Thechallenge for theexpansionof rail inEurope is theneed forpriorityof freightonrail

wheregovernmentshave focusedon thevotewinnerofprioritizingpassenger transport,with rail

freightnormallymovingonthesametracksintimewindowsduringnight.

At the heart of the logistics industry is warehousing. Often dismissed as the lowtech, lowinnovation

workhorseofthesupplychain,warehousingisinfacttheareamostpivotalinenablingthelogisticsindustry

tokeepupwiththefastpaceofchange.

ThekeyissuesontheagendaaroundwarehousingforLSPsaresummarizedbelow:

Optimizing the flowofgoods throughout thewhole supply chain remainsa critical concern,with

LSPscontinuingtofavormaintainingstorageandvalueaddedlogistics(VAL)facilitiesthatarelocated

closetothemainregionalseaportsandrailterminals.Automatedhighbayrackingsystemstoutilize

space and improve efficiency will become more and more common.

Goodswillbynowberoutinelybroughtclosertotheirfinaldestination; insteadofoneenormous

regionaldistribution

centre,

there

are

multiple

local

DCs,

served

by

more

frequent

deliveries.

Supply

chain network planning will become increasingly important, as will days coverage planning of

inventory to ensure the right stock is held at each location tomaximize availability and optimize

replenishmentcycleswhileminimizingcashtiedup.

Processadjustmentsare increasingly influencedbyecommerceandtheneedforflexibilitytofulfil

customerdemand forchoice in termsofproductanddelivery timescaleand location. A relatively

simplestandardprocessforawarehouseusedtobePalletsorContainersin,Parcelsout,Returnsin.

o With valueadded logistics increasingly common, goodsmaymove from one area of the

warehousetotheother,via labelling/packaging, andmaynevertouchtheretailerthatsold

them

where

orders

are

fulfilled

via

direct

despatch.

o Intheearlydaysofmultichannel,ecommerceinventorywassometimeskeptseparatefrom

normaldistribution inventory.To leverageefficiency itwillbe increasingly importantwhen

optimizinglogisticsthatallunallocatedinventoryispooledandvisiblefororderfulfilment.

Crossdocking;increasinguseofcrossdockingtoreduceinventoryholdingcostsatdifferentlocations

andtoreducetrucksrunningwithpartialloads.

Warehousingin2020

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

10/12

KewillWhitepaper:Logisticsin2020

KeyareaswhereITwillsupportlogisticscompaniesinachievingsuccessin2020:

Datasharing; now more than ever before, information is power. The electronic exchange of

information (including documentation) and financial data with supply chain partners, including

regulatorybodies,willbebecomingmandatoryinmanyregionsby2020.

Strategicsupplychainplanning;forsimulatingnetworkdesignandsourcingdecisions.

Any device, anywhere; BYOD and the effective utilization of platformneutral apps (for example

delivery tracking by courier) require increasing levels of collaboration between IT systems, both

internalandexternal,andabiggerpictureapproachtopolicies.

Betterplanningonmultimodaltransportation;tomeetbothgreenandefficiencytargetsandhandle

hubandspoke networks. Estimated breakdowns of potential routes will be required, by CO2

emissionsandcostaswellasspeed,asLSPsincreasinglyneedtosubstituteroutesandpartsofroutes

withalternativemodesoftransportforcost,environmentalimpactoraccess.

Betterutilizationofresource;viagranularcostallocationanddetailedefficiencyanalysisbyroute,

modality,carrierandtypeofgoods.

CO2 reporting compliance; impossible to achieve without effective allocation, tracking and

measurementofcostsandresourcesdowntoindividualshipmentlevel.

Reacttotrafficconditions; linkingofTradeManagementSystemsandTransportationManagement

Systemstolivetrafficconditionswithprocessflowsandautomationthatcaninfluencerouteplanning

insufficienttimetodivert.

Trackandtracevisibility;vision isendtoendvisibilityof thesupplychain from factory to theend

customerorconsumer.

Inventorymanagement;

first

by

minimizing

the

inventory

required

in

each

location

to

meet

customer

demand and secondly by optimizing every last cubic centimetre of warehouse space, with agile

systems thatenable rapidputaway, selectionandprocessing,aswellas integration towarehouse

equipmentsuchasforklifts,highbayrackingsystems,etc.

Mobility;systemsmustbequickandeasytorollout,withflexiblesetupandconfiguration, tocope

withnewcustomers,newroutes,newregions,partnershipsandalliances,mergersandacquisitions.

Standards and interoperability; increasingly connected supply chains to enable the sharing of

informationwith customers and subcontractors systems aswell as connections to industryHubs

suchasINTTRAandTRAXXON,andtrafficinformationsites.

Streamliningof

cross

border

and

compliance

processes;

multi

country

customs,

AES

submissions,

hazardousgoodschecking,deniedpartyscreeningandotherregulatorycompliance.

Role

of

IT

in

2020

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

11/12

KewillWhitepaper:Logisticsin2020

Summary

Theperiodto2020willseethebalanceofglobaltradecontinuetoshiftawayfromthetraditionallydominant

West towards the East. Emergingmarkets such as China, India and Russia are beingmatched byMiddle

Easternand

North

African

nations

that

are

frenetically

expanding

and

improving

theirinfrastructurestokeeppacewithdemandforbothimportsandexports.

Throughdirect investment from theirowngovernmentsand increased trading

cooperation with one another, emerging markets are overcoming major

challengesincludingclimate,terrain,longdistancesbetweendenselypopulated

areasand theavailability (or lack)of local labor tobuildnew roads, railways,

ports and airports. These infrastructure developments demonstrate the drive

and commitment of emerging markets to taking centre stage in the global

marketplaceofthefuture.

Thisexpansioninthenumberofcountriesthataremajorplayersinglobaltrade

suggestsamore

pivotal

future

role

for

the

logistics

industry,

with

infrastructure

development increasingly designed with the supply chain in mind. Logistics

companies are increasingly driving supply chain strategies, as developed countries rely on them to fulfil

consumerdemandanddevelopingcountriesseek theirassistance inestablishing robustexportand internal

distributionflows.

Going forward, LSPswill actively seek to offset increases in operating costs by taking advantage of their

expandedroleinglobaltradetotakeabiggershareofsupplychainprofits,byworkingmorecloselywiththeir

customersandwiththeirsupplychainpartners.Asbusinessmodelsevolve,theboundariesbetweenretailer,

supplierandLSPwillbecomeincreasingly blurred.

Workinginpartnershipwiththeircustomers,LSPswillcontinuetoexpandtheirrangeofoutsourcedservices

from

taking

complete

responsibility

for

their

customers

logistics

right

down

to

offeringamenuofservicesatamuchmoregranularlevel.Theywilldifferentiate

through a much broader offering, including valueadded services (e.g. light

assembly, kitting, packaging, labelling, repacking, quality checking, localmarket

customization) and delivering superior customer service. Together with their

supply chain partners, they will continue to leverage economies of scale by

working in partnership on some routes despite competing on others. Theywill

participate innetworks,whichwillexpandtocovermoremodalities,andbeyond

closeregionalboundaries.

Environmental issueswillrise inprominence forLSPs,ascountriesacross theworldstart to implementand

enforcelongtalkedaboutmeasurestoreducetheenvironmentalimpactoffossilfuelsviatransportation, and

enforce compliance through regulationand in some cases taxation.Environmental reportingwillbecomea

statutoryrequirement,drivingthelogisticsindustrytoimprovevisibilityofdatadowntoshipmentlevel.

Asever,thegreatestcertaintyfor2020andbeyondisthatitwillinvolveagreatdealofchange.Someofthis

change is foreseeable theshift inglobaltrade fromWest toEast.Some lessso,suchas the impactofcivil

unrestandpoliticalinstabilitywhichthreatenstodisrupteventhebestlaidplans.LSPsneedtostayaheadof

thecurveandbereadytoadapttheirstrategies,structuresandoperationstofutureprooftheirbusinesses.

Technologywill remain an essential enabler for LSPswhen deployed flexibly,with the global big

pictureinmind.

Technology will also be a driver of change and open up new business models and streamline

processes.

Technology

can

also

be

an

inhibitor,

where

investment

fails

to

keep

pace

with

industry

and

technologicaldevelopments.Thosethatdonthavegoodbusinesscriticalsystemsinplacetodaymay

loseoutorstruggletocatchup.

2020isntadateinthedistantfutureitsjust

aroundthecorner

-

8/12/2019 Kewill White Paper - Logistics in 2020 - The Future is Closer Than You Think. Fulfillment Best Practice to Deliver on Customer Promises and Drive Down Returns

12/12

KewillWhitepaper:Logisticsin2020

AboutKewill

Kewills Transport Management, Warehouse Management, Customs Compliance and Freight Forwarding

softwaredeliversendtoendgloballogistics,enablingLSPsandenterprisestomanagethemovementofgoods

andinformation

domestically

and

across

the

globe.

Our logistics solution suite empowers LSPs to: lower logistics and shipping costs, gain better control and

visibility&maximizecompliance.

For more information about Kewill, our solutions and our logistics expertise, visit our website at

www.kewill.com andourblogatwww.kewill.com/logistics_blog

Established in 1972, Kewill has over 7,000 customers around the world including Crane Worldwide, DHL,

Hankyu Hanshin, ITG Global Logistics,KLine Logistics,MOL Logistics,Raben Group, VAT Logistics,UPSand

TNT.

KewillLtd2013.Allrightsreserved.KewillandtheKewilllogoaretrademarksorregisteredtrademarksofKewillLtd.