KBC Group - Invest Bulgaria...

25

Christof De Mil Member of the Management Board and Executive Director of CIBANK JSC Brussels, March 20, 2013 KBC Group

Transcript of KBC Group - Invest Bulgaria...

Christof De Mil

Member of the Management Board

and Executive Director of CIBANK JSC

Brussels, March 20, 2013

KBC Group

Overview of KBC Group

• Strong bank-insurance group present with leading market positions in core geographies

(Belgium and CEE)

• A leading financial institution in both Belgium and the Czech Republic

• Business focus on Retail, SME & Midcap clients

• Unique selling proposition: in-depth knowledge of local markets and profound relationships with clients

• Integrated bancassurance business model, leading to high cross-selling rates

• Strong value creator with good underlying results through the cycle

• Integrated model creates cost synergies by avoiding overlap of supporting entities and generates added

value for our clients through a complementary and optimized product and service offering

• Refocus of KBC Group well-advanced (during 4Q12)

• Capital operations: capital increase of 1.25bn EUR and the sale of treasury shares (350m EUR)

• Repayment of 3.5bn EUR Belgian YES (+15% penalty) in 2012

• Sales of Absolut Bank and NLB have been announced, BZWBK merged with Kredyt Bank

• Updated strategy ‘KBC 2013 and beyond’ being implemented as of 1st January 2013

2

3

Business profile

Breakdown of allocated capital by business unit at 31 December 2012

• KBC is a leading player (retail and SME bancassurance, private banking,

commercial and local investment banking) in Belgium and our 4 core countries

in CEE

Well defined core markets provide access to ‘new growth’ in Europe

1. Excluding Centea and Fidea

2. Including 55% of the joint venture with CMSS

3. Source: KBC data, February 2013

BE CZ SK HU BG

% of Assets

2012e

2013e

2014e SPAIN

FRANCE

BELGIUM

NETHERLANDS

GERMANY

CZECH REP SLOVAKIA

HUNGARY

BULGARIA

UK

IRELAND

ITALY

GREECE Macroeconomic outlook Based on GDP, CPI and unemployment trends

Inspired by Financial Times

KBC Group’s core markets

In Belgium and CEE-4

PORTUGAL

Real

GD

P g

row

th o

utl

oo

k

for

co

re m

ark

ets

3

Mark

et

sh

are

, a

s o

f en

d 2

012

BE¹ CZ SK HU BG

Loans and deposits

Investment funds

Life insurance

Non-life insurance

4

Overview of key financial data at end 2012

5

6

Key non-financial figures, KBC Group

Customers (estimate) 31/12/2012

Belgium, Czech Rep., Slovakia, Hungary,

Bulgaria 9 million

Bank branches 31/12/2012

Belgium, Czech Rep., Slovakia, Hungary,

Bulgaria 1 632

Number of staff (in FTEs) 31/12/2012

Total (excluding companies to be

divested) 37 083

7

Market position

In the table below, estimates are provided regarding KBC’s position on its home markets in Belgium and Central & Eastern Europe.

Market share estimate of the KBC Group, 31-12-2012 Belgium

Czech

Rep. Slovakia Hungary Bulgaria

Traditional banking products (credits and deposits) 20% 20% 10% 9% 2%

Investment funds 35% 30% 8% 20% -

Life insurance 17% 8% 5% 3% 13%

Non-Life insurance 9% 6% 3% 4% 11%

Bulgarian Economy

Fiscally sound

9

Government debt, % GDP, 2012 Q3

Bulgarian government debt, % GDP

Source: EUROSTAT

Source: EU Commission Economic forecasts Winter 2013

• Bulgaria has the 2nd lowest public debt as % of GDP in EU

(after Estonia). The forecast is that the country will maintain this

position in the next couple of years.

• According to the winter 2013 EU Commission forecast for 2012

Bulgaria is the country with the 3rd lowest budget deficit in EU

(after Estonia and Sweden; Germany has surplus).

• Recent political instability caused by the resignation of the

government raised fears that it will cause also economic instability.

However, the markets reacted calmly and the large debt

emission issued by the government the same day it filed its

resignation was all sold out at very low interest rate (1% interest

rate, 6 month treasury bills). Currently, a broadly well-accepted

interim government is managing the country until elections are

held in May 2013.

• Low budget deficit and low indebtedness ensure stable basis

for future economic development.

Budget deficit, % GDP

Source: actuals: EUROSTAT; forecasts: EU Commission Winter 2013

KBC Group in Bulgaria

Why KBC entered the Bulgarian market 2007

11

• The country at that time had experienced strong economic growth which

was expected to continue at an above EU level average.

• Especially the banking and the insurance sectors offered penetration

potential, both in the retail and SME market segments.

• At the same time, the country was on its way to EU entry and already made

use of a fixed exchange rate to the Euro which provides stability.

• Bulgaria has an ample supply of skilled labor and both the tax environment

and the labor costs are attractive

12

Together with DZI it is able to propose its

customers an integrated bank-insurance

model which still leaves room for additional

leverage and market penetration.

Bulgaria is one KBC’s core markets

CIBANK over the years has become an

stable market player and a true household

brand.

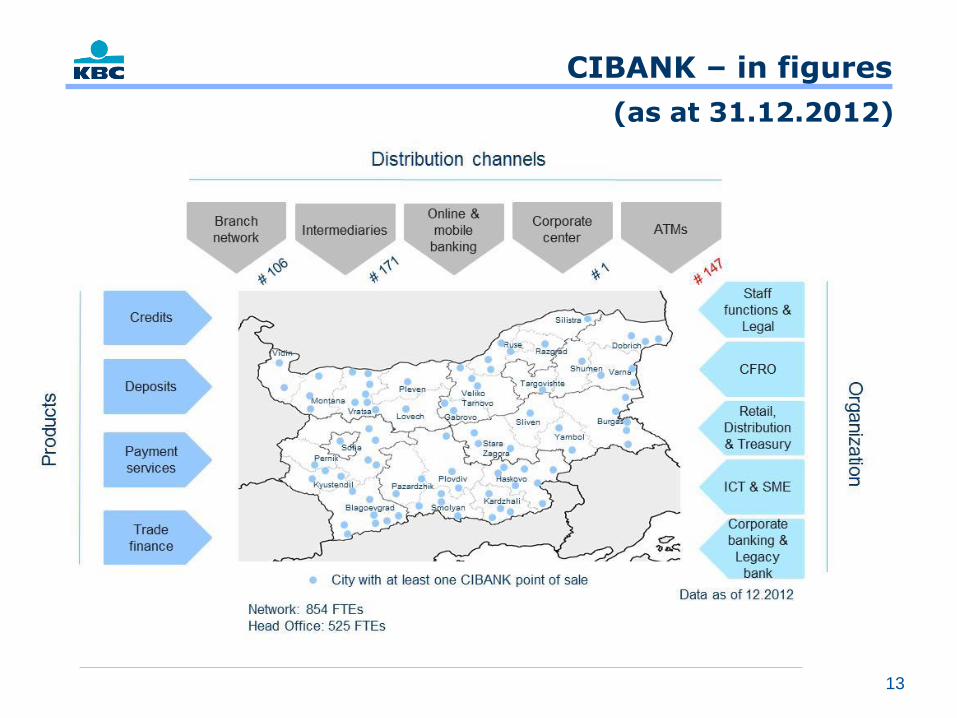

CIBANK – in figures

13

(as at 31.12.2012)

CIBANK – in figures

14

(as at 31.12.2012)

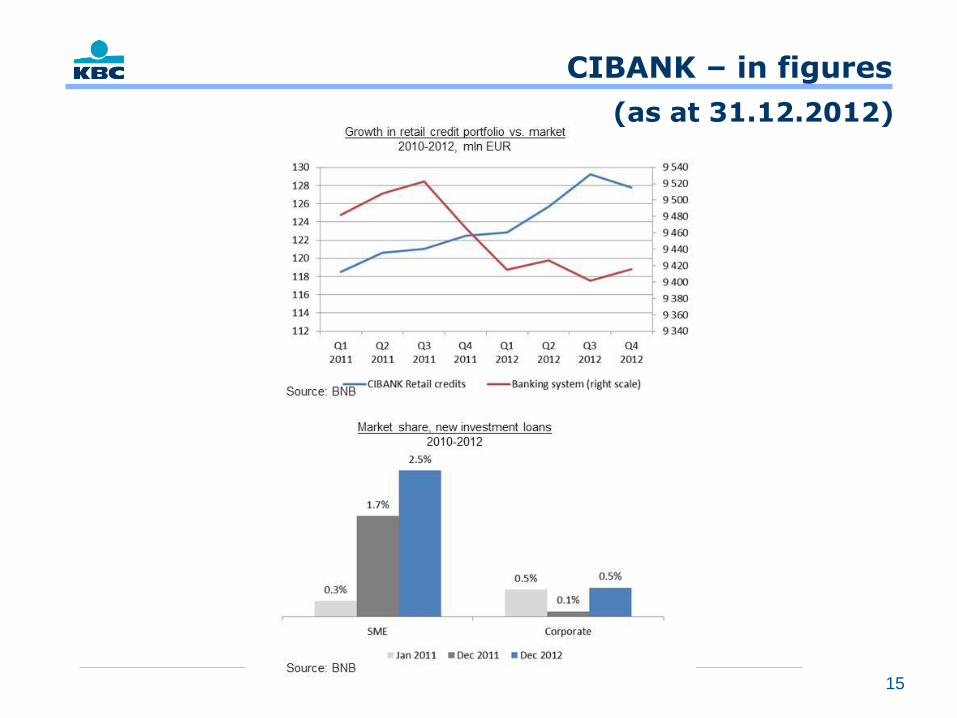

Source: BNB

CIBANK – in figures

15

(as at 31.12.2012)

The bank of the European subsidies

Europrojects funding (6+1facilities)

Standard loans

• Bridge & Investment financing

• VAT credit lines

• Bank guarantees

• Guidance for participation in

EU projects

• Partnership with leading

consulting firms

• Over 1000 loans

EIB global loans:

- 25MEUR – 100% allocated

- 30 MEUR – 70% allocated

- 105 MEUR under negotiation

EBRD- Energy Efficiency for retail - 5 MEUR (80% allocated)

Bulgarian Development Bank - 1 facility (100% allocated)

State Fund Agriculture – 2 facilities (no limit)

JEREMIE - 71 MEUR limit; 125 loans =19.3MEUR

National Guarantee Fund:

• 2 facilities – 127 credits for 10MEUR

• 1 facility for projects under the EC Rural Programme -

51.4 MEUR guarantee limit

• 1 for the Fisheries sector - 2 MEUR limit (2 credits incl.)

• 1 new to be contracted in April 2013- 4 MEUR guaranteed amount

Bulgarian Agency for Export Insurance – 51credits, 10MEUR

Bulgarian Development Bank - 93 micro credits

Municipal Guarantee Fund Sofia

RSI-EIF- for R&D projects – in pipeline

Risk sharing (6+2 facilities)

• Investment, working capital

• Attractive conditions

• DZI Insurance

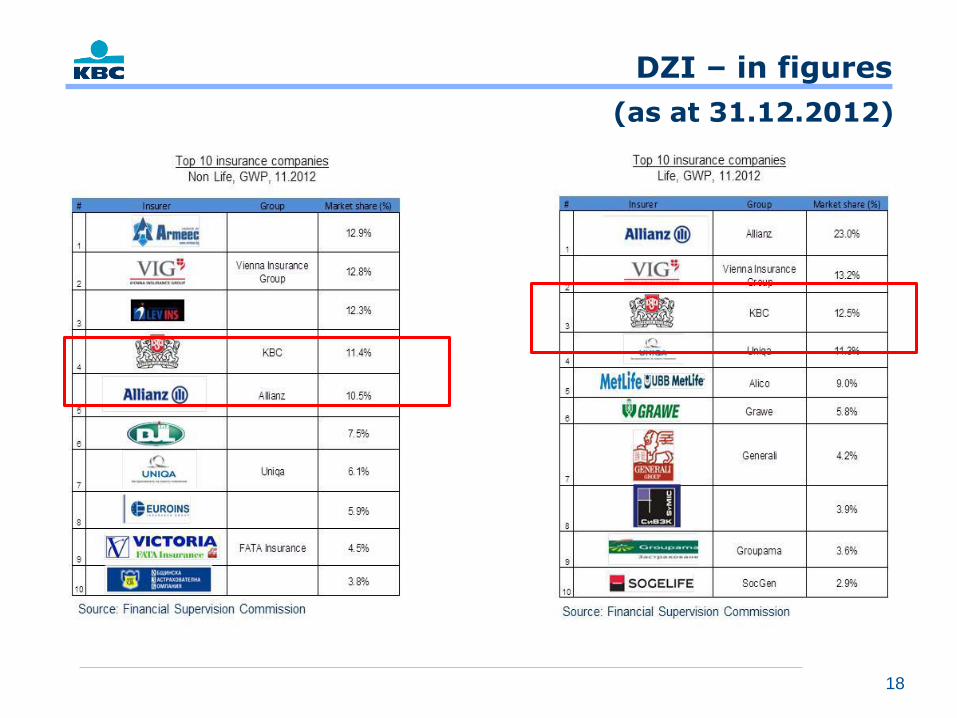

DZI – in figures

17

DZI – in figures

18

(as at 31.12.2012)

Profitability of Bulgarian banking market is at average levels due to high capital requirement; good bank capitalization provides strong basis for future growth

19

Profitability vs. market size

ROE (%) and Loans outstanding, 2011

• With return on equity (ROE) for 2011 of 4.6% Bulgarian banking market is slightly above the EU average of 4.2%. However, the

country has one of the highest capital adequacy requirement in EU and many banks keep addition buffers on top of the

required.

• As part of Basel III the expectation is that minimal capital requirement will be raised (currently 6% core Tier 1).

• Bulgaria will not be impacted by Basel III since the country already has very high capital requirement (10% core Tier 1).

This combined with the additional buffers kept by the local banks will provide strong basis for growth. In addition, some country

specific restrictions are expected to be removed/reduced – e. g. non-interest baring minimum reserve requirements for

deposits in the central bank, the capital deductions, ex ante deposit insurance scheme which does not take into account the

individual bank’s risk, etc.

Capital adequacy per country

31.12.2012

Source: ECB Source: CBD, ECB

Low penetration of credit in mortgage, consumer and SME lending

20

Low penetration of mortgage lending.

Banking penetration – mortgage lending

Loans outstanding as % of GDP, 2011

Banking penetration – consumer lending

Loans outstanding as % of GDP, 2011 Banking penetration – companies lending

Loans outstanding as % of GDP, 2011

Low penetration of consumer lending. • High penetration of company lending.

The main reasons for this is the

underdeveloped stock exchange and

lack of alternative to banking lending

for company financing.

• Data on size of credit indicates that

the majority of lending currently

goes to large corporate entities not

to SMEs.

Source: European Banking Federation Source: European Banking Federation Source: European Banking Federation

Bulgarian insurance market in EU context

21

Bulgarian insurance market size

GWP, bn EUR, 2011

• Size of Bulgarian insurance market still limited compared to Group peers and to EU average.

• Other EU-markets in Life are driven by Single Premium. Bulgarian Life insurance market is most

underdeveloped,

Bulgarian insurance market penetration

GWP as % GDP, 2011

Source: Insurance Europe, January 2013 report Source: Insurance Europe, January 2013 report

The future market potential in Insurance market

22

Motor Insurance Penetration

GWP as % of GDP, 2011

Property Insurance Penetration

GWP as % of GDP, 2011

Source: Insurance Europe, January 2013 report

Life Insurance Penetration

GWP as % of GDP, 2011

• Motor insurance penetration almost at par

with EU average.

• Property has significant convergence

potential which will go hand in hand with

real estate market.

• Market surveys show that only 10% of

the buildings in the country are insured

(yet many buildings are old village

houses).

• Life insurance is long way from EU

averages. Life insurance is 20% of

Non life market, while in Europe it is

140%.

• Increasing income levels coupled with

forecasted period of low interest rates

on bank deposits are expected to give

boost to this market.

• The prolonged period of economic

stability will eventually erase bad

memories of hyperinflation from the

late 1990s and encourage people to

put savings in long term products.

The Outlook: Issues and opportunities

23

Issues:

• Political Stability (recent resignation of government and upcoming elections)

• Structural reforms needed to

• Create jobs

• Increase consumer confidence

• Attract again FDI

• Stimulate growth of the Economy

Opportunities:

• Skilled labor and low labor cost

• Interest rates dropping (favourable for lending)

• Liquidity and capital available in banking system to provide loans (supported by local

subsidies/financial facilities (government support programs, NFG, ….) and supranational

financial facilities (EIB/EIF/EBRD))

• Favorable tax environment both personal and COR tax

• Prudent fiscal policy

• Stable banking system and currency board

Domestic demand and investments will be the engines for growth

24

GDP growth contribution per components

2012-2015

• Private consumption and investments will

be the main drivers of economic growth in

the next 4 years.

• Government spending is expected to

remain limited.

Source: BNB

25