Kazakh banks 22 Oct - Renaissance Capital

44

Kazakh banks Blessing in disguise Alexey Bulgakov +7 (495) 725 5229 [email protected] Alexey Moisseev +7 (495) 258-7946 [email protected] Fixed income research 22 October 2007 Banking Kazakhstan Gradual recovery. Grigory Marchenko, the president and CEO of Halyk Bank and the former governor of the National Bank of Kazakhstan, has said that the current liquidity squeeze could serve as a “blessing in disguise” for the whole Kazakh banking system. We concur with this view and believe that the banks, over the medium term, are likely to recover from the current shock, slowing growth rates to emerge as more domestically focused institutions. However, over the short term, we are likely to see some pricing volatility. Recent rating downgrades served as a late warning. Very little news about developments in the local banking system has come out of the country until recently therefore recent rating downgrades provided investors with a valuable external assessment of the situation. The refinancing situation of the individual banks (within the top six) appear to be manageable on a standalone basis: (1) most have already managed to refinance part of their short-term debt through syndicated or bilateral loans; (2) all banks report a balanced asset/ liabilities maturity profile and many state that they are preparing repayments of due loans from gradually matured assets. However, we believe the signs of funding redistribution within the system are worrying. Industry recapitalisation appears to be on the cards and will likely be assisted by state support (the announced creation of a state property fund) and support from current shareholders, actively fostered by the authorities. New large-scale issuance is unlikely. Whatever the outcome of the current situation (i.e. either a ‘hard’ or ‘soft landing’), it could be taken for granted that the country’s banks will receive external funding in the volumes necessary to cover their refinancing needs, but would see little new money. The purpose of this report is to present different views, as discussed by investors, exploring the subject. Figure 1: Real estate exposure of local banks – state should help Figure 2: Redistribution of local funding base is a concern 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 BTA KKB Alliance CCr Halyk ATF Temir Nurbank Caspian AstFin Loans to construction/ equity 18.0% 22.8% 21 .0% 18.7% 17.5% 24.4% 19.0% 19.2% 18.5% 10.8% 11 .0% 9.4% 11.2% 9.6% 7.0% 6.7% 8.7% 8.9% 15.6% 11 .2% 10.8% 0% 20% 40% 60% 80% 100% Dec. 06 June 07 Sept. 07 KKB Halyk BTA CCr Alliance ATF Other Source: MSCI, Bloomberg Source: FMSA, Kazkommertsbank, Renaissance Capital Important disclosures begin on page 42. This research material is released by Renaissance Securities (Cyprus) Limited. Regulated by the Cyprus Securities & Exchange Commission (License No: KEPEY 053/04).

Transcript of Kazakh banks 22 Oct - Renaissance Capital

Kazakh banks Blessing in disguise

Alexey Bulgakov +7 (495) 725 5229 [email protected] Alexey Moisseev +7 (495) 258-7946 [email protected]

Fixed income research 22 October 2007

Banking Kazakhstan

Gradual recovery. Grigory Marchenko, the president and CEO of Halyk Bank and the former governor of the National Bank of Kazakhstan, has said that the current liquidity squeeze could serve as a “blessing in disguise” for the whole Kazakh banking system. We concur with this view and believe that the banks, over the medium term, are likely to recover from the current shock, slowing growth rates to emerge as more domestically focused institutions. However, over the short term, we are likely to see some pricing volatility.

Recent rating downgrades served as a late warning. Very little news about developments in the local banking system has come out of the country until recently therefore recent rating downgrades provided investors with a valuable external assessment of the situation.

The refinancing situation of the individual banks (within the top six) appear to be manageable on a standalone basis: (1) most have already managed to refinance part of their short-term debt through syndicated or bilateral loans; (2) all banks report a balanced asset/ liabilities maturity profile and many state that they are preparing repayments of due loans from gradually matured assets. However, we believe the signs of funding redistribution within the system are worrying.

Industry recapitalisation appears to be on the cards and will likely be assisted by state support (the announced creation of a state property fund) and support from current shareholders, actively fostered by the authorities.

New large-scale issuance is unlikely. Whatever the outcome of the current situation (i.e. either a ‘hard’ or ‘soft landing’), it could be taken for granted that the country’s banks will receive external funding in the volumes necessary to cover their refinancing needs, but would see little new money.

The purpose of this report is to present different views, as discussed by investors, exploring the subject.

Figure 1: Real estate exposure of local banks – state should help Figure 2: Redistribution of local funding base is a concern

0.00.51.01.52.02.53.03.54.04.5

BTA

KKB

Allia

nce

CCr

Halyk AT

F

Temi

r

Nurba

nk

Casp

ian

AstF

in

Loan

s to

con

stru

ctio

n/ e

quity

18.0% 22.8% 21.0%

18.7%17.5% 24.4%

19.0% 19.2%18.5%

10.8% 11.0% 9.4%11.2% 9.6% 7.0%6.7% 8.7% 8.9%15.6% 11.2% 10.8%

0%

20%

40%

60%

80%

100%

Dec. 06 June 07 Sept. 07KKB Halyk BTA CCr Alliance ATF Other

Source: MSCI, Bloomberg Source: FMSA, Kazkommertsbank, Renaissance Capital

Important disclosures begin on page 42. This research material is released by Renaissance Securities (Cyprus) Limited. Regulated by the Cyprus Securities & Exchange Commission (License No: KEPEY 053/04).

22 October 2007 Kazakh banks Renaissance Capital

2

Investment summary 3

A. Macroeconomics 3 B. Refinancing and funding base 4 C. Asset quality and recapitalisation 5 Recommendations 7

Macro backdrop 8 Problem 1: Too much external debt 11

Local money markets 13 External funding – appears to be too much 13 Rebalancing of funding structure – what are the options? 15 Rating agencies 16 Equity view – a very important angle 18 Impact on M&A activity 18 ATF bank – a special situation 19

Problem 2: Short-term refinancing 20 Assessment of short-term refinancing requirements 20 Refinancing – still available, but in limited volumes 21 Redistribution of deposit base – Halyk benefits, small banks lose 22 Corporate deposits 25 Other factors that can potentially distort refinancing schedules 26 A. Covenants of syndicated loans 26 B. Bond buybacks 26 Liquidity and funding assessment of individual banks 26 A. Kazkommerzbank 27 B. TuranAlem and Temir 28 C. Alliance Bank 29 D. ATF 30 E. Halyk Bank 31 F. Centercredit 31 G. Caspian 32 H. Astana Finance 33 NBK as the lender of last resort 33

Problem 3: Asset quality 35 Potential remedies 38

Verbal interventions 38 Liquidity support 38 Rebalancing of funding base 38 Asset quality and potential recapitalisation of the sector 40 1. Creation of a state-controlled construction fund 40 2. Other forms of real estate refinancing 40 3. Increase of allocations of local pension funds 40 4. ‘Assets go home’ 40

Appendix I: Summary financial statements 41 Important disclosures 42

Contents

Renaissance Capital Kazakh banks 22 October 2007

3

Kazakhstan’s financial sector is significantly exposed to the increasing price and declining availability of credit. Banks are exposed to the recent trend of rising credit spreads on both the funding and asset sides of their balance sheets. Within emerging markets, the Kazakh banking sector is one of the more exposed on the liability side of the balance sheet, given sector-wide dependence on international credit for funding. This perception of market participants is captured in the current level of credit spreads.

Figure 3: Credit spreads widened by 250-300 bpts from mid-July levels

100

200

300

400

500

600

700

800

900

1000

06/2007 06/2007 06/2007 07/2007 07/2007 08/2007 08/2007 09/2007 09/2007 10/2007

pbs

Alliance 5Y ATF 5Y BTAS 5YBCC 5Y Halyk 5Y KKB 5Y

Source: Bloomberg

Figure 4: Moody’s ‘official’ and ‘market implied’ ratings show significant discrepancies Senior unsecured rating Market implied rating Difference, notches KKB Baa2 B3 7 Bank TuranAlem Baa3 Caa1 7 ATF Ba1 B2 4 Halyk Savings Bank Baa2 Ba3 4 Centercredit Ba1 Caa1 6 Alliance Ba2 Caa3 7 Temirbank Ba1 Ca 9

Source: Moody's, Renaissance Capital estimates

The situation in the Kazakh banking sector can be viewed from three different angles: (1) macroeconomic fundamentals; (2) short-term refinancing and redistribution of funding; (3) high probability of impairment of a substantial part of local assets and adverse impact on the capitalisation of the banking system.

A. Macroeconomics The country’s current account deficit is a major structural problem (resulting

from significant outflows of direct investment interest). In 1H07, Kazakhstan’s current account deficit was $2.0bn; other things being equal, we estimate that the full-year current account deficit is approximately $6bn.

We believe the NBK will aim to maintain nominal exchange rate stability in the short term, even at the cost of spending reserves. Basically, considering the current rate of reserve spending ($1.0-1.5bn per month), we think that the NBK will continue to intervene for 2-2.5 months unless access conditions of the local banks to international markets

Investment summary

22 October 2007 Kazakh banks Renaissance Capital

4

improve (hence intensified communication between the major banks and international investors).

The aforementioned presumes a high probability of attempts to allocate new supply (bonds and syndicated loans) from Kazakh banks by the year end.

If the need arises, we expect the Kazakh authorities to be prepared to revert to foreign financing, which, in our view, will be readily available. In the medium to long term, however, risks for the currency remain in place, and we expect the currency to start depreciating – eventually to much weaker levels in early 2008.

We think that there is a relatively high probability that the government might apply for standby financing from international monetary institutions or to issue a large sovereign bond. If the bid for external financing takes place, then similarly to issuance of a deeply discounted rights issue by a corporate in distress, it should be taken positively by the creditors, since it would assure currency stability and free more reserves to provide support to the banking system.

B. Refinancing and funding base As of the end of June, we estimate Kazakh banks’ short-term external

financial liabilities at $12bn, $4.3bn of which has been refinanced or redeemed. These numbers can be amplified by the redistribution of funding within the system (i.e. individual depositors gradually shifting money from private banks to Halyk or just taking money out of the system).

We believe the large Kazakh banks’ (within the top six) refinancing requirements can be viewed as manageable on a standalone basis: (1) most of them (with the notable exception of Alliance) have already managed to refinance part of the short-term indebtedness through syndicated or bilateral loans; (2) all banks report a balanced asset/ liabilities maturity profile so, in theory, can repay maturing loans from gradually matured assets; (3) owners of several banks and the banks themselves have large identifiable and, potentially, valuable assets outside of Kazakhstan and, in theory, can use them as collateral for/ sources of financing and recapitalisation.

Figure 5: Kazakh banks: Estimated short-term refinancing requirements, Oct 2007, $bn 30 June 2007, <1M 30 June, 1-12M Refinanced in 3Q07 To be refinanced

BTA + Temir 1.0 2.5 1.9 0.6 KKB 2.1 2.6 0.6 2.0 Alliance 0.9 2.2 0.2 2.0 CCr 0.1 1.2 0.6 0.7 Halyk 1.0 0.6 0.4 0.2 ATF 0.6 0.5 0.4 0.0 Caspian 0.2 0.2 0.2 0.1 less repos -4.1 0.0 0.0 0.0 Total 2.0 9.9 4.3 7.6

Source: Company data, Renaissance Capital estimates

Option number (2) from the above is negative from a systemic point of view, since the country needs currency inflow, and the bank borrowing abroad is one of the major sources.

Renaissance Capital Kazakh banks 22 October 2007

5

Potential payment acceleration events. We believe a number of bank rating revisions is possible from the rating agencies. All straight Kazakh banks’ eurobonds have very limited covenant protection; however, many syndicated loans, especially ones signed recently, might contain rating change triggers and other covenants (Alliance’s comments about a possible violation of its loan covenants has illustrated this point).

Figure 6: Alliance and the smaller banks are clear net losers (30 June – 31 Aug, absolute change)

-25.0%

-15.0%

-5.0%

5.0%

15.0%

25.0%

35.0%

KKB

BTA

Allia

nce

Halyk AT

F

CCr

Temi

r

Casp

ian

Nurb

ank

Eura

sian

Tses

na

Othe

r

Abs

olut

e ch

ange

in re

tail

depo

sits

Source: FMSA, Renaissance Capital estimates

In an emergency, the National Bank of Kazakhstan (NBK) appears capable of providing extraordinary liquidity to one or two large institutions if necessary (we estimate its disposable reserves as of the end of September totalled $13bn); however, it also has to defend the national currency.

Kazakh banks have to substitute a material amount of external funding with domestic funding, and we cannot see any obvious immediate sources for such a substitution as the size of the banking sector has clearly outgrown the development of other country’s financial institutions (such as pension funds and insurance companies).

Over the medium term, we believe the system could readjust its funding structure; however, due to the limited size of available local funding, it would only be at the price of a growth slowdown or even a fall in the aggregate asset base, as the alternatives of domestic funding are quite limited.

C. Asset quality and recapitalisation Most Kazakh banks have a relatively high exposure to real estate and

construction financing (KKB 2.8x equity, BTA 1.8x, ATF 2.4x, Centercredit 2.2x). The banks stopped providing new loans to the industry several months ago, and now there are visible signs of a deterioration in the asset quality.

A large amount of the liquidated collateral can create pressure on the secondary real estate market (additional pressure might come from

22 October 2007 Kazakh banks Renaissance Capital

6

currency depreciation and many residential mortgages are provided in dollars). If real estate prices decrease materially, the crystallised losses taken from the disposal of collateral might exert a very negative impact on banks’ capital.

The are several ways for recapitalisation of the system if the above scenario is realised: (1) equity contributions from current owners (see the liquidity section); (2) support from foreign shareholders (for banks like Caspian or ATF; (3) a bail-out from the state (the creation of a special ‘state property fund’ with money from the National Fund that would buy out distressed ’nationally important’ property on painful, but excessively so, conditions for the banks.

Figure 7: Loans to construction & real estate as a proportion of the loan portfolio and shareholders' equity

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

BTA

KKB

Allia

nce

Cente

rcred

it

Halyk AT

F

Temi

r

Nurba

nk

Casp

ian

Astan

a Fina

nceLo

ans

to c

onst

ruct

ion/

tota

l loa

ns

0.00.5

1.01.52.0

2.53.03.5

4.04.5

BTA

KKB

Allia

nce

Cente

rcred

it

Halyk AT

F

Temi

r

Nurba

nk

Casp

ian

Astan

a Fina

nce

Loan

s to

con

stru

ctio

n/ e

quity

Source: Company data, Renaissance Capital estimates Source: Company data, Renaissance Capital estimates

With regard to the last scenario, we do not think that external debt holders will be hurt intentionally, i.e. the restructuring terms, if the system goes through this exercise, are likely to be onerous. It seems to us that the reputation of the country and its institutions as trustworthy borrowers is a very important component of the current political/ economic regime.

We do not think that industry consolidation is very likely, since Kazakhstan’s banking system lacks a dominant well-capitalised institution, there are no sizable state-controlled banks and soon there may be a lack of capital in the system.

In the recapitalisation scenario, the best chance for a successful completion of the exercise, in our opinion, is to have large transparent institutions with an established presence on the international markets, which have identifiable valuable assets outside of the country.

From the pricing prospective, we think that the volatility in the sector is not over as we are likely to hear more negative news flow (i.e. KKB remains on Moody’s negative watch, and we believe more negative rating action may follow).

Any sign of debt markets becoming more accommodative to Kazakh debt should be taken positively, as this would help the NBK to keep

Renaissance Capital Kazakh banks 22 October 2007

7

reserves to protect the national currency. However, sector restructuring (i.e. reduction of foreign activities and shifting funding towards domestic sources) will likely take some time.

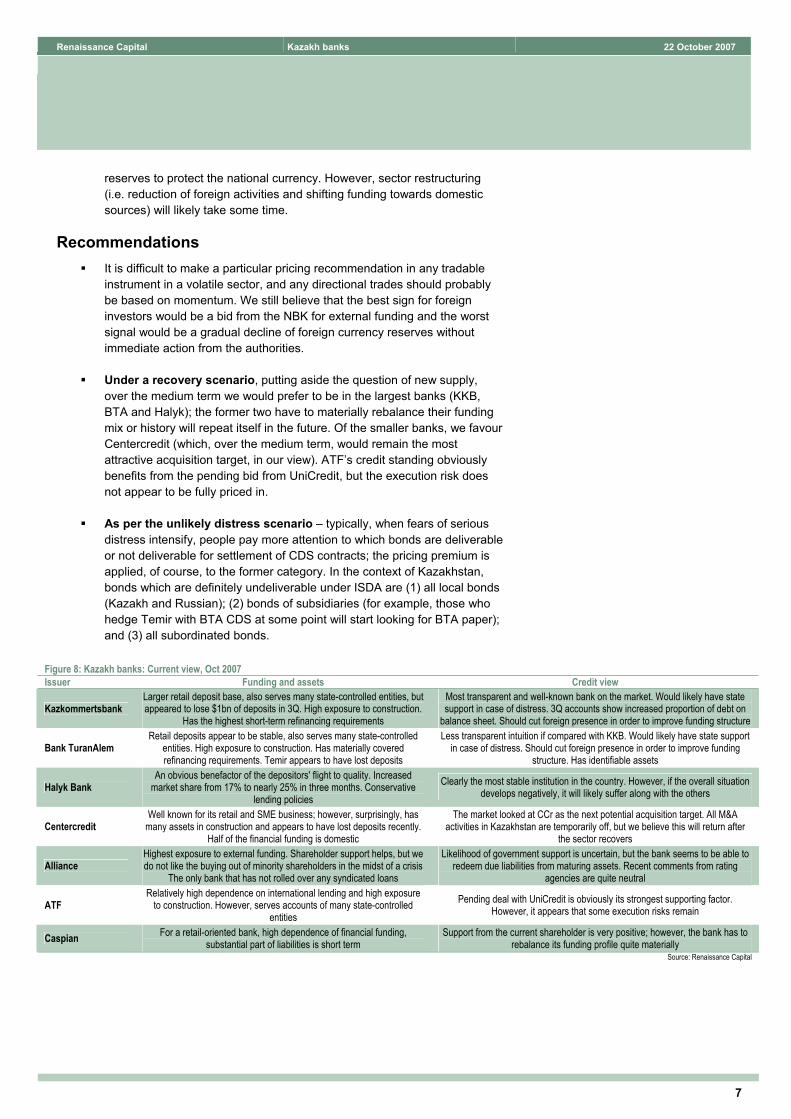

Recommendations It is difficult to make a particular pricing recommendation in any tradable

instrument in a volatile sector, and any directional trades should probably be based on momentum. We still believe that the best sign for foreign investors would be a bid from the NBK for external funding and the worst signal would be a gradual decline of foreign currency reserves without immediate action from the authorities.

Under a recovery scenario, putting aside the question of new supply, over the medium term we would prefer to be in the largest banks (KKB, BTA and Halyk); the former two have to materially rebalance their funding mix or history will repeat itself in the future. Of the smaller banks, we favour Centercredit (which, over the medium term, would remain the most attractive acquisition target, in our view). ATF’s credit standing obviously benefits from the pending bid from UniCredit, but the execution risk does not appear to be fully priced in.

As per the unlikely distress scenario – typically, when fears of serious distress intensify, people pay more attention to which bonds are deliverable or not deliverable for settlement of CDS contracts; the pricing premium is applied, of course, to the former category. In the context of Kazakhstan, bonds which are definitely undeliverable under ISDA are (1) all local bonds (Kazakh and Russian); (2) bonds of subsidiaries (for example, those who hedge Temir with BTA CDS at some point will start looking for BTA paper); and (3) all subordinated bonds.

Figure 8: Kazakh banks: Current view, Oct 2007 Issuer Funding and assets Credit view

Kazkommertsbank Larger retail deposit base, also serves many state-controlled entities, but appeared to lose $1bn of deposits in 3Q. High exposure to construction.

Has the highest short-term refinancing requirements

Most transparent and well-known bank on the market. Would likely have state support in case of distress. 3Q accounts show increased proportion of debt on

balance sheet. Should cut foreign presence in order to improve funding structure

Bank TuranAlem Retail deposits appear to be stable, also serves many state-controlled

entities. High exposure to construction. Has materially covered refinancing requirements. Temir appears to have lost deposits

Less transparent intuition if compared with KKB. Would likely have state support in case of distress. Should cut foreign presence in order to improve funding

structure. Has identifiable assets

Halyk Bank An obvious benefactor of the depositors' flight to quality. Increased

market share from 17% to nearly 25% in three months. Conservative lending policies

Clearly the most stable institution in the country. However, if the overall situation develops negatively, it will likely suffer along with the others

Centercredit Well known for its retail and SME business; however, surprisingly, has

many assets in construction and appears to have lost deposits recently. Half of the financial funding is domestic

The market looked at CCr as the next potential acquisition target. All M&A activities in Kazakhstan are temporarily off, but we believe this will return after

the sector recovers

Alliance Highest exposure to external funding. Shareholder support helps, but we do not like the buying out of minority shareholders in the midst of a crisis

The only bank that has not rolled over any syndicated loans

Likelihood of government support is uncertain, but the bank seems to be able to redeem due liabilities from maturing assets. Recent comments from rating

agencies are quite neutral

ATF Relatively high dependence on international lending and high exposure

to construction. However, serves accounts of many state-controlled entities

Pending deal with UniCredit is obviously its strongest supporting factor. However, it appears that some execution risks remain

Caspian For a retail-oriented bank, high dependence of financial funding, substantial part of liabilities is short term

Support from the current shareholder is very positive; however, the bank has to rebalance its funding profile quite materially

Source: Renaissance Capital

22 October 2007 Kazakh banks Renaissance Capital

8

Small open economies are vulnerable to exogenous shocks. The global liquidity squeeze came as a specific exogenous shock for Kazakhstan, amplifying its own structural problems.

In July and August, Kazakhstan was hit by the global financial turmoil, and has experienced significant capital outflows – a major event given that the country crucially depends on capital flows in order to finance its (widening) current account deficit. Capital outflows were combined with tenge weakening to KZT126/USD, and up to KZT135/USD on the cash market. In August, the NBK lost $1.6bn of its reserves, followed by a $1.6bn decline in September and $0.6bn in the first half of October. This is partially explained by NBK’s interventions to support the tenge.

Figure 9: Change in reserves, capital and financial, and current account in Kazakhstan

-4,000

-2,000

0

2,000

4,000

6,000

8,000

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07

$mnChange in gross foreign reserv es, eop Capital and financial account Current account

Source: National Bank of Kazakhstan

The country’s current account deficit is a significant structural problem (resulting from significant outflows of direct investment interest in the projects, developed in the framework of production-sharing agreements (over a third of the total oil export value), and the limited ability of the domestic industry to cater for domestic demand, particularly for higher quality goods, as well as for investment needs. The 2Q current account deficit was 7.8% of GDP on a quarterly basis, and we see very little – if any – room for that to decline going forward.

We think that a slowdown in banking asset growth would not significantly impact import growth (45-50% YoY currently), and the only way to remedy the current account situation is to renegotiate all PSA agreements, significantly increasing Kazakhstan’s share – which, in our view, is not doable in the short term. It should be noted that FDI net inflow has essentially stopped – down to $265mn in 2Q from $1.8bn in 1Q, and suspension of the Kashagan licence will likely make matters worse. For a long time, banks were the only channel to finance the current account deficit, through the inflow of capital – particularly in the form of loans, mostly in the short-term segment. This window is now closed. Other things being equal, we estimate that Kazakhstan’s full-year current account deficit will be approximately $6bn.

Macro backdrop

The country is experiencing significant capital outflows

Current account deficit is the major structural problem

Renaissance Capital Kazakh banks 22 October 2007

9

Over August- September, NBK has been spending reserves to support the currency. This policy is not sustainable. However, NBK has supported the currency in order to (1) allay the population’s fears and (2) protect the local banking system from additional pressure. The NBK has also said that it fears that if devaluation occurs, the dollarisation of the economy will rise again, and will be increasingly difficult to reduce.

Figure 10: Kazakhstan’s current account components

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07

$mn

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%% of GDP

Other Income Net current transfers Imports, goodsImports, serv ices Direct inv estment interest Inv estment income on credits netEx ports, serv ices Ex ports, goods Current account, % of GDP

Source: National Bank of Kazakhstan

We believe the NBK will aim to maintain nominal exchange rate stability in the short term, even at the cost of spending reserves. Basically, considering the current rate of reserve spending ($1.0-1.5bn per month), we think that the NBK will continue to intervene for 2-2.5 months unless access conditions of the local banks to international markets improve (hence the intensified communication between major banks with international investors).

Figure 11: Local currency exhibited material volatility over the past months

117.00

118.00

119.00

120.00

121.00

122.00

123.00

124.00

125.00

126.00

127.00

26/06/2007 10/07/2007 24/07/2007 07/08/2007 21/08/2007 04/09/2007 18/09/2007 02/10/2007

KZT/USD

Source: Bloomberg

NBK spending reserves to support the currency

We think that, all things being equal, this policy can be sustained only over the short term…

22 October 2007 Kazakh banks Renaissance Capital

10

Afterwards, if the need arises, we expect the Kazakh authorities to revert to foreign financing, including from international financial organisations, which, in our view, will be readily available. In the medium to long term, however, risks for the currency remain in place, and we expect the currency to start depreciating – eventually to much weaker levels in early 2008.

We see devaluation next year to KZT135-140/USD as essentially inevitable, but well within expectations of local investors, so the shock to the economy should not be unexpected. Currency devaluation will put additional pressure on the domestic banking system (higher servicing costs of foreign debt, additional requirements for customers, borrowing in dollars, approximately 50% of all loans to individuals).

. . . and the NBK would have to get external funding if capital outflows are sustained

Renaissance Capital Kazakh banks 22 October 2007

11

The growth of Kazakhstan’s banking system over recent years has surprised many observers. A large proportion of asset growth was financed by external financial debt and it appears that the market (with the notable exception of Kazakh banks themselves) agrees that the key problem the system currently faces is the very high proportion of foreign funding. Following reassessment of credit risk on the international capital markets, the country’s banks started to experience difficulties rolling over outstanding debt obligations and raising new funds.

The gross outstanding external debt of Kazakhstan’s financial system as of end-June 2007 was reported at $42.4bn.

Figure 12: Funding structure of Kazakh banks, 30 June 2007

$2.9bn, 3.2%

$21.1bn, 23.1%

$30.3bn, 33.2%

$9.6bn, 10.5% $4.1bn, 4.5%

$11.2bn, 12.3%

$12.1bn, 13.3%

Money markets (NBK) Domestic bonds Corporate deposits Retail depositsEx ternal debt - short term Ex ternal debt - long term Capital

Source: FMSA, Renaissance Capital estimates

Approximately $20bn of the outstanding external long-term debt is represented by outstanding eurobonds, the rest is in longer-dated portions of syndicated and bilateral loans.

We estimate Kazakh banks’ short-term external financial liabilities to be approximately $12bn (see our assessment of short-term refinancing requirements provided in the following sections of this report). These are mostly short-dated portions of syndicated and bilateral loans (see our liquidity assessment in the sections below).

Corporate deposits ($21bn) are another large component of the bank’s funding1. The total probably contains a large proportion of speculative money (Kazakhstan does not have zero-rate double-taxation agreements with any foreign jurisdiction, so back-to-back deposits have been a popular scheme to provide funding for offshore entities for acquisitions of local assets). Some comments provided in the media (e.g. Financial Times) estimate the mid-summer amount of ‘hot money’ in the Kazakh banking system at approximately $7bn. The NBK estimates that, as of the end of June 2007, foreigners directly owned $3.7bn of Ministry of Finance and NBK notes (or 35% of the outstanding volume); in addition, there were $1.5bn of foreign deposits in individual commercial banks. Also,

1 Official statistics, published monthly by NBK, puts the total of corporate deposits outstanding as of end June 2007 at $40.7bn. This amount includes all outstanding eurobonds

Problem 1: Too much external debt

Too much external debt – the major problem of the banking sector

Corporate deposits – essentially a mixture of cash of resource companies, ‘hot money’ and local buy side

22 October 2007 Kazakh banks Renaissance Capital

12

approximately $2bn of total corporate deposits are accounts of local insurance companies and pension funds. The balance represents deposits and current accounts from companies belonging to resource-oriented sectors and infrastructure (approximately 40% or $8bn of the reported corporate deposits) and consumer-oriented sectors of the economy ($6bn).

Local bonds represent a relatively minor funding component of Kazakh banks due to the relatively small size of the local buy-side base (the total size of the local pension funds’ assets and investment portfolios of insurance companies is approximately $11bn, while the National Fund can invest only in foreign currency instruments) and transactional difficulties for foreign investors, willing to take direct access to the market. We estimate that out of $4bn of local banking bonds outstanding, approximately $3-3.5bn are kept with the local pension funds and insurance companies. It should be noted that all local banking bonds are relatively long term, only 3% of the outstanding notional amount matures in 2007-2008.

Figure 14: Notional amount of local bonds, issued by Kazakh banks, Oct 2007

0

200

400

600

800

1,000

1,200

1,400

1,600

KKB BTA Alliance Halyk ATF CCr Temir Nurbank Tsesna

$mn

Source: KASE, Renaissance Capital estimates

Figure 13: Breakdown of corporate deposits of major Kazakh banks, 30 June 2006, $bn KKB BTA incl.

Temir Alliance Halyk *ATF Centercredit Total, 6 largest banks

Individuals 2.6 2.2 1.0 2.1 0.5 1.2 9.6 Oil, gas and chemical 1.8 0.9 0.0 0.5 0.7 0.2 4.0 Mining and metallurgy 0.1 0.5 0.1 0.2 0.1 0.1 1.1 Transport and communication 0.5 0.4 0.0 0.3 0.4 0.1 1.6 Other 2.9 2.2 1.0 1.9 1.3 1.2 10.5 Total deposits 7.8 6.1 2.2 5.0 3.0 2.7 26.8 Corporate deposits 5.2 3.9 1.1 2.9 2.4 1.5 17.2 Deposits from ‘natural resources’, % of corporate deposits 45% 43% 9% 35% 47% 23% 39% Deposits from ‘natural resources’, % of total deposits 30% 28% 5% 20% 38% 13% 25% Deposits from individuals, % of total deposits 33% 36% 48% 42% 18% 44% 36% * 31 Dec 2006

Source: Company data, Renaissance Capital estimates

Local bonds are a relatively minor funding component; new issuance is limited by the relatively small size of the local buy-side

Renaissance Capital Kazakh banks 22 October 2007

13

Local money markets The NBK currently employs several instruments for provision of additional liquidity to the system.

Repo transactions with banks, with 28-day durations using government securities as underlying assets. Out of $7.0bn of government securities outstanding, approximately $2.5bn are held by pension funds and insurance companies and around $2.0-2.5bn are still probably held by speculative accounts, so the amount of liquidity available to the system through this instrument is $2.0-2.5bn.

Banks can receive liquidity in the form of currency swaps for the currency proportion of the reserves, held at the NBK (KZT500bn out of KZT800bn total reserves) of up to 50% (many Kazakh banks have traditionally funded their reserve requirements with the NBK through taking loans in low-yielding currencies, such as yen). The NBK can supply up to $2.0bn liquidity to the market through this instrument.

The NBK currently provides approximately KZT300bn of liquidity to the system via both of these instruments; this is more than early September (KZT250mn), but lower than during the peak of the currency crisis at the end of August (KZT360-400bn).

External funding – appears to be too much The absolute size of external liabilities of the Kazakh banking segment has doubled over the past 15 months. Kazakh officials and bank representatives, while publicly commenting on the change in pricing of external bonds issued by Kazakh banks, are often quoted as saying they unduly suffer because of the spill-over effects of global liquidity tightening. These comments seem to miss the fact that, the first implications of a very large new supply overhang were first seen in 1H07, when spreads of long-term bonds issued by Kazakh financial institutions widened by 50-100 bpts after huge amounts of primary bond placements and signings of new syndicated loans in 4Q06-1Q07.

Figure 15: New supply overhang was the first factor that affected Kazakh bond spreads

200250300350400450500550600650700750

16 O

ct 20

06

01 N

ov 20

06

20 N

ov 20

06

06 D

ec 20

06

22 D

ec 20

06

19 Ja

n 200

7

07 F

eb 20

07

27 F

eb 20

07

15 M

ar 20

07

02 A

pr 20

07

19 A

pr 20

07

11 M

ay 20

07

29 M

ay 20

07

14 Ju

n 200

7

02 Ju

l 200

7

18 Ju

l 200

7

03 A

ug 20

07

21 A

ug 20

07

07 S

ep 20

07

25 S

ep 20

07

11 O

ct 20

07

Z-sp

read

to U

ST, b

ps

BTAS'15 KKB'13

Spread tighteing, exceptionally good

sentiment

Spread widening after huge offerings of primary issues

M&A talk intesifies, ATF

annonuncement

Liquidity squeeze

Source: Bloomberg, Renaissance Capital estimates

The NBK currently provides KZT300mn of liquidity to the system

External liabilities of Kazakh banking segment doubled over the past 15 months

New supply overhang was the first factor that affected Kazakh banking bonds

22 October 2007 Kazakh banks Renaissance Capital

14

Overall, in Oct 2006-Mar 2007, Kazakh banks attracted slightly less that $15bn of new external funding, this was approximately equally split between new bonds (all of which were long term) and syndicated loans (a material proportion of which was short and medium term). According to our observations, trading and investment allocations of all types of international investors, who traded in Kazakh issues, reached their limits very quickly, and secondary bond quotes reacted very negatively to any attempt to place external tradeable issues (we can recollect at least three attempts from BTA to make a eurobond placement in spring-summer 2007, all of which led to immediate selling of the outstanding bonds and were unsuccessful). The increased new supply of structurally subordinated bonds (like a large new issue of Temir, a subsidiary of BTA, which offered bonds at 180 bpts spread over BTA itself, or a large subordinated placement of KKB) also affected the secondary pricing quite negatively.

Figure 16: Total debt issuance – outstanding debt doubled within 15 months Figure 17: Net debt issuance – very large placements late 2006 – early 2007

8.7 10.1 12.018.5 21.0

11.713.6

21.4

19.921.4

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2Q06 3Q06 4Q06 1Q07 2Q07

LoansBonds

1.3 1.4 1.9

6.5

2.51.7 1.9

7.7

-1.5

1.5

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2Q06 3Q06 4Q06 1Q07 2Q07

LoansBonds

Source: FMSA, Bloomberg, Renaissance Capital Source: FMSA, Bloomberg, Renaissance Capital

It terms of proportion, however, external funding remained a relatively stable component of the system’s funding base, staying around 45% for the past three years. However, banks’ individual exposures to external funding vary greatly.

Figure 18: External funding as a percentage of total liabilities, excl. shareholders equity, 30 June 2007

67.4%

25.0%

53.7%

64.6%

45.5%

31.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Alliance Centercredit *BTA **KKB ***ATF Halyk

* including Temir ** as of 31 Mar 200 *** as of YE06

Source: Company data, Renaissance Capital estimates

Renaissance Capital Kazakh banks 22 October 2007

15

The highest proportions are observed in banks which are very active internationally (BTA and KKB, which report 38% and 35% of consolidated assets located abroad, respectively) and banks which consciously pursued an external wholesale funding strategy of Kazakh local retail operations (i.e. Alliance).

Rebalancing of funding structure – what are the options? Basically, Kazakh banks have to substitute a material amount of external funding with domestic funding, and we cannot see obvious immediate sources for such a substitution as the size of the banking sector has clearly surpassed the development of other financial institutions.

The current size of domestic buy-side accounts (insurance companies and pension funds) is $11bn (or 12% of the current size of the banking system). Approximately half of their funds are already invested in banking instruments (bonds and deposits), so the increase in allocations of the domestic buy-side – a measure, currently being promoted by BTA and KKB – is unlikely to help in the medium term.

Retail deposits over the past 12 months grew at $300-350mn per month. However, how this will be sustained in the short term is unclear –recent sector statistics suggest a material slowdown in deposit growth. During a recent conference call, KKB suggested that customers take cash to buy real estate; they also might take cash to repay bank loans if rollovers were not easily available.

Short-term dynamics of corporate deposits is unclear – on the one hand, there is no reason to assume that transactional balances of the country’s resource companies (40% of corporate deposits) will be reduced; however; a material proportion of the ’hot money component’ creates uncertainty. Foreign speculative money, invested in Kazakh government securities, is positioned with a view of currency appreciation (which we do not support) and we might see further contraction here.

We think it is probable that the system will be able to readjust its funding structure towards more balance over the medium term; however, it would only be at the price of a slowdown in growth or even a decline in the aggregated asset base, as the alternatives of domestic funding are quite limited.

Figure 19: Local sources of funding appear to be limited

Sources of funding Estimated volume of inflows, 12 months, $bn Comment

Retail deposits 2.0-3.5bn

Retail deposits have been growing by approximately $300mn per month over the past two years. May slowdown as banks reduce lending programmes, people will pay back from savings. Also, we see evidence of a redistribution of the deposit base

Increase of allocations of local pension funds plus new money

0.5-1.5bn

The measure is lobbied by BTA and KKB; total assets of local pension system are $9.0bn. Note: pension

funds are already keeping 50% of their assets in local corporate bonds and bank deposits. Seem to be

opposed by Halyk’s Marchenko

Corporate deposits 0.0-2.0bn Difficult to estimate; over the past two years have been

growing by approximately $500mn per month, but probably two-thirds of this was speculative capital

Source: Renaissance Capital

The banking system seems to have surpassed other domestic financial institutions

Material changes in the funding structure are feasible, but in the medium term

22 October 2007 Kazakh banks Renaissance Capital

16

Rating agencies All three major international rating agencies have traditionally assessed the Kazakh banking system and individual banks in the context of benefiting from being located in a country whose economy is strongly exposed to international commodity prices (which remains obviously a very positive factor), and benefits from the presence of high quality regulatory supervision and a visibly high-quality asset base. High exposure to external funding has been traditionally mentioned as a potential credit-constraining factor (and, actually, was the major reason for Moody’s changing outlook of the country’s largest banks to stable from positive in May 2006); however, until recently, all comments have been moderately worded.

In early October, several rating agencies looked at the implications of the global liquidity squeeze on the Kazakh banking system, resulting in a wave of negatively worded statements, not previously seen with regard to the country’s banks for quite a while. The rating actions caused subsequent critical comments from a number of highly ranked Kazakh politicians, including President Nazarbayev.

In the first week of October, S&P downgraded Kazakhstan’s sovereign credit rating by one notch, together with the ratings of some state-controlled institutions (such as the Development Bank of Kazakhstan). The major reason for the statement was to reflect the adverse situation in the local banking system. The wording of the rating statement was quite negative; in particular, the agency talked about "tighter liquidity conditions” in the banking system and "potentially compromising asset quality", and the initial market reaction to the statement was very negative.

S&P also changed its rating outlook of Bank TuranAlem (rated at BB flat) from Positive to Stable, basically saying that it is probably inappropriate to expect a medium-term rating upside for any financial institution (with the exception of special situations such as ATF, which remains on watch Positive) in a time when the whole banking system of the country is experiencing severe liquidity pressure. The rating action statement presumes that the agency is going to review all individual banks’ ratings after it assess the systemic risks (the review of the sovereign rating is scheduled to conclude within a week, quite a short timeframe in our view). Although no other negative rating action in respect of individual banks followed, it would be reasonable to assume that they are still likely to follow, given that the reason for a sovereign downgrade was problems of individual banks.

Following S&P’s announcement about a then-possible downgrade of Kazakhstan’s sovereign rating, Moody’s put Kazakommertsbank (senior debt currently rated at Baa2, previously the rating had a negative outlook) on negative review, saying, that it will assess the bank’s short-term liquidity position and the “significant possibility of a material deterioration of the bank's loan portfolio quality due to the rapid growth in lending and the high concentration of construction and real estate exposure". Moody’s does not say how large the rating cut might be or when the review will conclude. It should be noted that compared with other rating agencies, Moody’s assigns material weight to the implied opinion of the credit markets about quality of the particular issuer (as manifested by observed credit spreads),

Several negative rating actions in October caused critical political comments

Moody’s review of KKB – probably the most aggressive rating action so far

Renaissance Capital Kazakh banks 22 October 2007

17

so we would not be surprised to see ratings of major Kazakh banks aligned with ratings of S&P and Fitch.

Figure 20: Moody’s ‘official’ and ‘market implied’ ratings show great discrepancy Senior unsecured rating Market implied rating Difference, notches KKB Baa2 B3 7 Bank TuranAlem Baa3 Caa1 7 ATF Ba1 B2 4 Halyk Savings Bank Baa2 Ba3 4 Centercredit Ba1 Caa1 6 Alliance Ba2 Caa3 7 Temirbank Ba1 Ca 9

Source: Moody's, Renaissance Capital estimates

Fitch revised its outlook of Kazakhstan’s sovereign rating and ratings of Kazkommrzbank, Bank TuranAlem and Halyk (all rated BB+) from Positive to Stable, providing arguments very similar to S&P about BTA (see above). Interestingly, Fitch also said that its credit ratings for all six of the largest Kazakh banks (KKB, BTA, Halyk, ATF, Alliance and Centercredit) are based on the strong probability of sovereign support, and therefore those will be downgraded only with Kazakhstan’s sovereign rating or if individual banks show signs of deteriorating asset quality. We believe the agency means that the state is likely to help the country’s largest banks if liquidity problems arise but does not specify in what form and over which timeframe it expects this support to be manifested. It may also mean that Fitch remains so far the most moderate of all three agencies and we are unlikely to see it make any sudden moves (or provide early warning).

Figure 21: Summary of rating agencies' opinions, Oct 2007 Moody's S&P Fitch Before Oct 2007

Rates senior debt of large Kazakh banks two to three

notches above Moody's and Fitch. However, comments over

the past year suggest the increased attention towards

concentration of funding of all large banks (downgrade of KKB,

BTA and Temir ratings in summer etc). Assigns high

likelihood of state support to KKB, BTA, Halyk and ATF

Quite vague reports, which list all observable factors, putting

stress on the asset side (desirable decrease of loan

concentration) and maintenance of capitalisation; seem not to

treat concentration of funding as material risk. Assigns high

likelihood of state support to KKB, BTA and Halyk

Quite vague reports about individual banks, mentions refinancing risks of some of

them but never classifies as a key factor. Assigns high

likelihood of state support to KKB, BTA and Halyk

Oct 2007 Put KKB on negative review, talks about liquidity and

potential asset impairment because of excessive exposure

to the real estate and construction sectors. So far no

rating action on other banks and no official comments about

Kazakhstan's sovereign rating. Difference between senior debt ratings and CDS/bond implied

ratings of individual banks is four to nine notches

Cut Kazakhstan's sovereign rating over concerns about the

developing situation in the banking system (mentions tight

liquidity and potential imparement of assets). Apart

from reducing rating outlook of BTA to 'stable' has not yet

announced any negative action about private banks

Reduced outlook of sovereign ratings and KKB, Halyk and BTA

to ‘stable’. In subsequent comments said that it is not going to take any action on individual banks because it

assumes a high probability of state support to all banks.

Describes the liquidity position of all banks as “manageble”. Says will review individual ratings only if it sees quality problems on the

asset side Source: Rating agencies, Renaissance Capital estimates

Negative implications of potential rating downgrades of individual banks are threefold:

Fitch will probably refrain from sudden moves for now

22 October 2007 Kazakh banks Renaissance Capital

18

Informational effect. Any negative (or positive) statement from rating agencies about any large bank will be taken as a confirmation from an independent third party about negative (or positive) developments in the sector. The rating agencies are also aware of the flipside after high-profile political statements about “victimisation” of Kazakh banks.

Technical effect. A material downgrade of a high-rated bank (such as KKB or BTA) might cause a supply overhang from the current holders whose mandate specifies a high credit rating as a necessary investment criterion.

Negative liquidity effect. A number of Kazakh banks’ syndicated loans might have minimum rating requirements. Bond documentation and financial reports of individual banks do not provide details about covenant arrangements for syndicated loans.

Equity view – a very important angle While analysing the current situation in the Kazakh banking system from a credit perspective, it should be noted that, as in any emerging market economy, both equity and debt sides of the same events complement each other. Three Kazakh banks have equity, tradable on international stock exchanges and the rest have been constantly engaged in negotiations with potential industrial partners. We believe that for many institutions fulfilment of equity holders’ expectations is often the priority.

The major driver behind the (until recently) very high equity valuations of Kazakh banks was the expectation of sustainable high growth rates. During our July visit to Almaty, the county’s major banks see nothing wrong in that, forecasting 2008 “moderate” growth rates of 25% pa. Some of them point at the high proportion of loans extended to projects outside of Kazakhstan (KKB and BTA have 20-25% of their loan book outside of the country), but the major argument went along the lines of “as long as we see good demand for financing from our customers we see no reason to worry”.

Impact on M&A activity

When we visited Almaty mid-July, the assumption of the large banks was that toughening regulatory measures will lead to the consolidation of independent smaller players, as the cost of running the business notably increased. Apparently, all of the independent smaller banks were for sale – Eurasian, Tsesna, Caspian (by

Figure 22: Summary of credit ratings of Kazakh banks, 9 Oct 2007 Moody's S&P Fitch Rating Outlook Date last

changed Rating Outlook Date last changed Rating Outlook Date last

changed Development Bank of Kzh Baa1 SO May 06 BBB- SO Oct-07 BBB SO Oct 07 KKB Baa2 NW Oct 07 BB+ SO Feb-06 BB+ SO Oct 07 Bank TuranAlem Baa3 SO Jun 07 BB SO Oct-07 BB+ SO Oct 07 ATF Ba1 PW Jul 07 B+ PW Jun-07 BB- PW Jun 07 Halyk Savings Bank Baa2 SO May 07 BB+ SO Jul-06 BB+ PO Dec 06 Centercredit Ba1 SO May 07 - - - BB- SO Dec 05 Alliance Ba2 SO May 07 B+ SO Oct-07 BB- SO Dec 05 Nurbank B1 SO May 07 B SO Jul-05 - - - Caspian Ba3 SO May 07 - - - B+ SO Sep 05 Astana Finance Ba1 SO Jan 06 - - - BB+ SO Jan 06 Temirbank Ba1 SO Jun 07 B+ SO Nov-06 BB- SO Dec 06 Tsesna Bank B1 SO Nov 04 B- SO Aug-06 B- SO Sep 06

Source: Rating agencies

Assumption of high growth rates – the main contributor to the recent equity valuations in the sector

Renaissance Capital Kazakh banks 22 October 2007

19

definition, the controlling shareholder is a private equity house, Barings Vostok) and Temir (BTA later publicly announced its decision to sell the bank, saying that it is planning to complete the disposal by YE07, later putting the sale on hold).

Figure 23: Equity valuations decreased materially over the past several months

5.00

7.50

10.00

12.50

15.00

17.50

20.00

22.50

25.00

27.50

02/11

/2006

02/12

/2006

02/01

/2007

02/02

/2007

02/03

/2007

02/04

/2007

02/05

/2007

02/06

/2007

02/07

/2007

02/08

/2007

02/09

/2007

02/10

/2007

$

KKB LI Equity HSBK LI Equity ALLB LI Equity

Source: Bloomberg, Reuters, Renaissance Capital estimates

The current M&A landscape has definitely changed, with equity valuations of the largest tradable bank (once again with the exception of Halyk) down by some 30-50%. For example, VTB representatives said in September that the bank had abandoned its talks about the potential acquisition of an unnamed Kazakhstan-based mid-sized bank. In mid-June, we think that all Kazakh mid-sized banks had been engaged in active talks with potential foreign buyers. However, it seems very likely that in the current environment all negotiations are temporarily off. BTA’s decision to put the disposal of Temir Bank on hold also illustrates this.

ATF bank – a special situation

At the end of June, Italian banking conglomerate, UniCredit, announced that it had reached a deal with the common equity holders of Bank ATF to purchase 100% of the bank at approximately $2.3bn. The deal is scheduled to conclude by the end of 2007, subject to regulatory approval. While waiting for the deal to close, ATF enjoys quite healthy liquidity support from the parent-to-be and, along with Halyk, sees considerable inflow of private and corporate deposits. UniCredit’s CEO publicly stated mid-October that his bank intends to complete the transaction.

However, we think it is obviously facing some execution risks here. It will be reasonable to assume that, seeing a material correction in sector asset prices, UniCredit might be willing to renegotiate the pre-agreed price. Also, the lasting dispute between common and preferred equity holders about the conversion ratio does not help as the conflict might increase the timeframe for completion of the deal thus increasing execution risk.

All M&A deals seem to be temporarily off

22 October 2007 Kazakh banks Renaissance Capital

20

The ability of Kazakh banks to refinance their financial liabilities in an orderly manner in the difficult conditions on the international capital markets is viewed by many investors as the major short-term problem currently faced by the Kazakh banking system. It should be noted that, due to the sustained negative dynamics of the current account, re-opening access of the local banks to foreign funding is a task of paramount political importance. Improved conditions of access would help to improve the country’s balance of payments and prevent NBK from bidding for external liquidity.

Assessment of short-term refinancing requirements It is important to note that official external debt statistics, published by the NBK, classifies short-term external liabilities as only liabilities with ‘original contractual maturities shorter than one year’; these liabilities as of 30 June 2007 totalled $7.35bn. This presentation does not take into account the redemption of instruments with longer contractual durations and therefore materially underestimates the size of real short-term servicing requirements.

It should be noted that the observed redemption schedule of outstanding eurobonds issued by Kazakh banks (i.e. the debt category, where debt redemption statistics can be received from multiple publicly available sources) is very light; the covenant packages of all outstanding bonds also does not contain any rating triggers or other restrictive financial covenants, which theoretically could accelerate the repayment. Therefore, an attempt to construct a short maturity profile schedule for individual banks essentially boils down to the review of the outstanding syndicated loans, the breakdown of which is often provided in published IFRS financials.

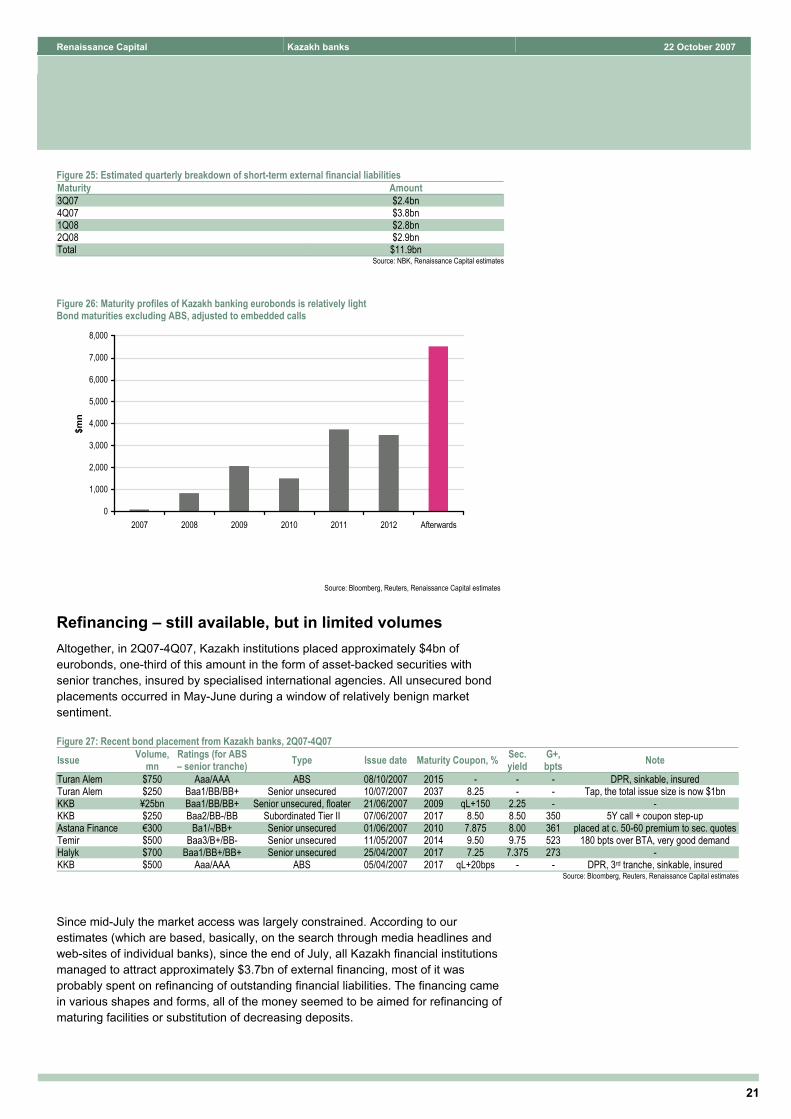

In the table below, we provide a summary of the short-term maturities of financial obligations (excluding deposits) of Kazakhstan’s largest banks. The disclosure was taken from the latest available IFRS accounts or calculated using local accounts with certain adjustments. The material part of the financial liabilities with a duration shorter than one month represent repo transactions (with the NBK and other counterparties), whose rollover should not represent any practical difficulties, so we estimate the total short-term external liabilities of Kazakh banks as of 30 June at $11.9bn.

Figure 24: Kazakh banks - estimated short-term refinancing requirements, Oct 2007, $bn 30 June 2007, <1M 30 June, 1-12M Refinanced in 3Q07 To be refinanced

BTA + Temir 1.0 2.5 1.9 0.6 KKB 2.1 2.6 0.6 2.0 Alliance 0.9 2.2 0.2 2.0 CCr 0.1 1.2 0.6 0.7 Halyk 1.0 0.6 0.4 0.2 ATF 0.6 0.5 0.4 0.0 Caspian 0.2 0.2 0.2 0.1 less repos -4.1 0.0 0.0 0.0 Total 2.0 9.9 4.3 7.6

Source: Company data, Renaissance Capital estimates

This assessment approximately equals the estimate of the NBK, which, during its October conference call, put the short-term redemption schedule of the country’s banks at $3bn per quarter.

Problem 2: Short-term refinancing

Redemption schedule of Kazakh banking eurobonds is relatively light

The NBK estimates short-term refinancing requirements of the system at $3bn per quarter for the next nine months

Renaissance Capital Kazakh banks 22 October 2007

21

Figure 25: Estimated quarterly breakdown of short-term external financial liabilities Maturity Amount 3Q07 $2.4bn 4Q07 $3.8bn 1Q08 $2.8bn 2Q08 $2.9bn Total $11.9bn

Source: NBK, Renaissance Capital estimates

Figure 26: Maturity profiles of Kazakh banking eurobonds is relatively light Bond maturities excluding ABS, adjusted to embedded calls

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2007 2008 2009 2010 2011 2012 Afterwards

$mn

Source: Bloomberg, Reuters, Renaissance Capital estimates

Refinancing – still available, but in limited volumes Altogether, in 2Q07-4Q07, Kazakh institutions placed approximately $4bn of eurobonds, one-third of this amount in the form of asset-backed securities with senior tranches, insured by specialised international agencies. All unsecured bond placements occurred in May-June during a window of relatively benign market sentiment.

Since mid-July the market access was largely constrained. According to our estimates (which are based, basically, on the search through media headlines and web-sites of individual banks), since the end of July, all Kazakh financial institutions managed to attract approximately $3.7bn of external financing, most of it was probably spent on refinancing of outstanding financial liabilities. The financing came in various shapes and forms, all of the money seemed to be aimed for refinancing of maturing facilities or substitution of decreasing deposits.

Figure 27: Recent bond placement from Kazakh banks, 2Q07-4Q07

Issue Volume, mn

Ratings (for ABS – senior tranche) Type Issue date Maturity Coupon, % Sec.

yield G+, bpts Note

Turan Alem $750 Aaa/AAA ABS 08/10/2007 2015 - - - DPR, sinkable, insured Turan Alem $250 Baa1/BB/BB+ Senior unsecured 10/07/2007 2037 8.25 - - Tap, the total issue size is now $1bn KKB ¥25bn Baa1/BB/BB+ Senior unsecured, floater 21/06/2007 2009 qL+150 2.25 - - KKB $250 Baa2/BB-/BB Subordinated Tier II 07/06/2007 2017 8.50 8.50 350 5Y call + coupon step-up Astana Finance €300 Ba1/-/BB+ Senior unsecured 01/06/2007 2010 7.875 8.00 361 placed at c. 50-60 premium to sec. quotes Temir $500 Baa3/B+/BB- Senior unsecured 11/05/2007 2014 9.50 9.75 523 180 bpts over BTA, very good demand Halyk $700 Baa1/BB+/BB+ Senior unsecured 25/04/2007 2017 7.25 7.375 273 - KKB $500 Aaa/AAA ABS 05/04/2007 2017 qL+20bps - - DPR, 3rd tranche, sinkable, insured

Source: Bloomberg, Reuters, Renaissance Capital estimates

22 October 2007 Kazakh banks Renaissance Capital

22

Bonds. The last straight issue placed on the market was a relatively small $250mn BTA tap of its longest senior unsecured bond maturing 2037. The placement, albeit small, severely affected secondary quotes. By early October, BTA concluded placement of its $750mn DPR securitisation programme, where two senior tranches were secured by specialised international insurance agencies. The bank commented that the placement “was not aimed to refinance its financial liabilities” (probably a mere courtesy remark); the cost of placement was not disclosed. It also should be noted that by early August KKB cancelled the solicited exchange of $500mn of bonds maturing in 2009 into longer-dated issue due to unfavourable market conditions.

Shareholders’ support. Three banks – Alliance, ATF and Caspian – announced liquidity support from their current or prospective shareholders. Alliance’s support came in the form of a $220mn deposit from its controlling shareholder, Seimar Group (we discuss this transaction in more detail below), and Caspian announced a $150mn standby liquidity facility from one of its controlling shareholders, private equity fund Barings Vostok. ATF Bank received two smaller loans from Unicredit, one senior short-term (money market) and one subordinated $220mn and said that it could also agree to an increase of the money market line of up to $450mn. It is unclear however to what extent the availability of money market funds is linked to the successful conclusion of the ATF acquisition by UniCredit.

Several banks announced full or partial rollovers of existing syndicated loan facilities. The most notable examples include KKB (rollover of $400mn in August with an increase of the principal to $660mn), Centercredit (a rollover and increase of a $300mn facility matured in August by $150mn to $450mn) and ATF (a $210mn three- and five-year syndicated line).

Redemption of matured liabilities through available funds/ maturing assets. In theory, all Kazakh banks report balanced short-term asset/ liabilities maturity profiles and should be able to repay liabilities falling due from gradually maturing assets. In September, BTA said it fully redeemed a $600mn loan facility from Deutsche/ HSBC, using available funds. Alliance uses the ‘balanced asset/ liabilities profile’ argument, while explaining how it is going to refinance its syndicated loans falling due.

Redistribution of deposit base – Halyk benefits, small banks lose Several circumstances distinguish Kazakhstan as a place to conduct retail banking. The country occupies territory slightly less than four times the size of Texas, but has a population of only 15mn people, of which 8-9mn are economically active – of these only 3-4mn can be classified as ‘commercially attractive’. Large income dispersion and the relative poverty of a large proportion of retail customers means that, en masse, retail deposits are a source of funding of secondary importance (hence the uniform strategy to pursue only ‘high income retail customers’ until recently adopted by several banks). Many retail clients keep low cash balances; for example, the current average size of a retail deposit in Halyk – the largest deposit taking bank in the country (which however has a high proportion of pensioners and public servants as depositors) – is approximately $300.

Refinancing seem to be available, but in limited volumes

Shareholder support is very important in times of crisis

Retail deposits were until recently only the secondary source of funding

Renaissance Capital Kazakh banks 22 October 2007

23

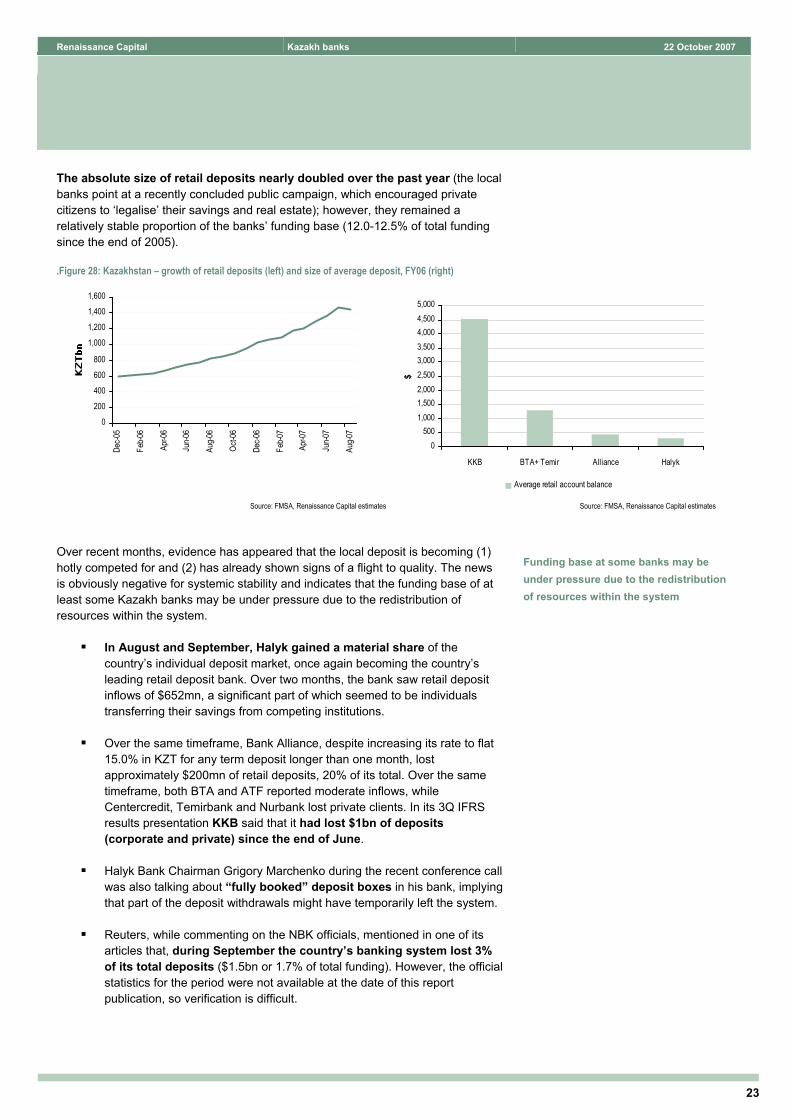

The absolute size of retail deposits nearly doubled over the past year (the local banks point at a recently concluded public campaign, which encouraged private citizens to ‘legalise’ their savings and real estate); however, they remained a relatively stable proportion of the banks’ funding base (12.0-12.5% of total funding since the end of 2005).

.Figure 28: Kazakhstan – growth of retail deposits (left) and size of average deposit, FY06 (right)

0

200

400

600

800

1,000

1,200

1,400

1,600

Dec-0

5

Feb-0

6

Apr-0

6

Jun-0

6

Aug-0

6

Oct-0

6

Dec-0

6

Feb-0

7

Apr-0

7

Jun-0

7

Aug-0

7

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

KKB BTA+ Temir Alliance Halyk

$

Average retail account balance

Source: FMSA, Renaissance Capital estimates Source: FMSA, Renaissance Capital estimates

Over recent months, evidence has appeared that the local deposit is becoming (1) hotly competed for and (2) has already shown signs of a flight to quality. The news is obviously negative for systemic stability and indicates that the funding base of at least some Kazakh banks may be under pressure due to the redistribution of resources within the system.

In August and September, Halyk gained a material share of the country’s individual deposit market, once again becoming the country’s leading retail deposit bank. Over two months, the bank saw retail deposit inflows of $652mn, a significant part of which seemed to be individuals transferring their savings from competing institutions.

Over the same timeframe, Bank Alliance, despite increasing its rate to flat 15.0% in KZT for any term deposit longer than one month, lost approximately $200mn of retail deposits, 20% of its total. Over the same timeframe, both BTA and ATF reported moderate inflows, while Centercredit, Temirbank and Nurbank lost private clients. In its 3Q IFRS results presentation KKB said that it had lost $1bn of deposits (corporate and private) since the end of June.

Halyk Bank Chairman Grigory Marchenko during the recent conference call was also talking about “fully booked” deposit boxes in his bank, implying that part of the deposit withdrawals might have temporarily left the system.

Reuters, while commenting on the NBK officials, mentioned in one of its articles that, during September the country’s banking system lost 3% of its total deposits ($1.5bn or 1.7% of total funding). However, the official statistics for the period were not available at the date of this report publication, so verification is difficult.

Funding base at some banks may be under pressure due to the redistribution of resources within the system

22 October 2007 Kazakh banks Renaissance Capital

24

Figure 29: Halyk is a clear beneficiary of retail depositors’ flight to quality (market shares at indicated dates)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

KKB

BTA

Allia

nce

Halyk AT

F

CCr

Temi

r

Casp

ian

Nurb

ank

Eura

sian

Tses

na

Othe

r

Mar

ket s

hare

30.06.2007 31.08.2007

Source: FMSA, Renaissance Capital estimates

Along with the intensive, but not necessarily accurate coverage of the events on the international capital markets by local media, the major factor that is seen by the local banks as the major contributors to the apparent depositors’ run is the recent volatility on the local currency market. By the end of August, reportedly due to a change in customs legislation, the local currency exchange offices started to experience a shortage of dollars. High street KZT/USD cash exchange rates jumped to 140, and making simple conclusions, many private citizens reduced balances on their bank accounts. The NBK quickly intervened and the local currency exchange rate returned to pre-run levels; however, so far it seems that the retail depositors have not returned quickly.

Figure 30: And Alliance, Temir and Nurbank are clear net losers (30 June – 31 Aug, absolute change)

-25.0%

-15.0%

-5.0%

5.0%

15.0%

25.0%

35.0%

KKB

BTA

Allia

nce

Halyk AT

F

CCr

Temi

r

Casp

ian

Nurb

ank

Eura

sian

Tses

na

Othe

r

Abs

olut

e ch

ange

in re

tail

depo

sits

Source: FMSA, Renaissance Capital estimates

It also should be noted that the national deposits insurance fund is technically a very small entity, with annual funds inflow of approximately $70mn and with the size of total assets as of July 2007 of KZT5bn ($40mn) – the amount, not large

Late August currency volatility is seen by the local banks as the major contributor to the depositors’ run

Some of the safeguarding institution are simply too small to be effective

Renaissance Capital Kazakh banks 22 October 2007

25

enough to cover in full private deposits of any bank within the top 20. Back in February the fund fell short of the recently failed Valut-Tranzit Bank (then 12th largest, rated at B1 by Moody's half a year before the licence was revoked) – a fact, actively discussed then by the media. For comparison, the Russian deposit insurance fund currently holds approximately $2.1bn, which is enough to cover individual deposits of any private bank with quite a good margin (perhaps the significant factor here is the presence of a dominant state-controlled retail institution such as Sberbank).

All of the above, coupled with the intention of all major country’s banks to increase the proportion of retail deposits in the funding base, creates material pre-requisites of a deposit war.

Corporate deposits

As mentioned above, corporate deposits form one of the major components of Kazakh banks’ funding, totalling approximately $21bn or 23% of the system’s funding base. Those can be roughly broken down as transactional balances and term deposits from cash rich natural resources and infrastructure companies (approximately 40% of the total), speculative ‘hot money’ (difficult to asses: say, 25% of the total) with the rest being accounts of social institutions and consumer-oriented companies. The first category, obviously, represents the most coveted type of corporate client for any local bank; in fact, accounts of major state-controlled corporates are relatively evenly distributed between the country’s largest banks.

Figure 31: Change in corporate deposits (adjusted for new debt issuance), July-Aug 2007

-200-150

-100-50

050

100

150200

250300

350400

KKB

BTA

Allia

nce

Halyk AT

F

CCr

Temi

r

Casp

ian

Nurba

nk

Euras

ian

Tses

na

Othe

rAbs

olut

e ch

ange

in

corp

orat

e de

posi

ts, $

mn

Source: FMSA, Renaissance Capital estimates

In early September, Grigory Marchenko, when commenting about the early consequences of the deposit run, was quoted as saying that during the late August deposit run, Halyk received “several hundred million dollars worth” of large, state-controlled corporate accounts. It is difficult to assess for the outsider whether such transfers really took place, and the aggregated monthly data, provided by the regulator, do not provide any conclusive evidence. It would be reasonable to assume that the government, especially taking into account its relatively aggressive and supportive public statements, would discourage account transfers of all state-controlled corporates for the time being. Subsequently Marchenko refrained from making any statements on the subject. The previous chart provides inconclusive

Statistical data are inconclusive

Apart from private deposits, Halyk also receives inflows of corporate accounts

22 October 2007 Kazakh banks Renaissance Capital

26

data; however, the increase of corporate balances with ‘other’ banks (i.e. probably local subsidiaries of international banks) can be attributed to the consequences of the August capital flight.

Other factors that can potentially distort refinancing schedules A. Covenants of syndicated loans

In the short term, we might see material rating downgrades from rating agencies, as evidenced by recent statements from S&P and Moody’s. All straight Kazakh bank’s eurobonds have very limited covenant protection (with the likely exception of DPR securitisation programmes) – something that would probably change for the new primary placements from the sector. However, many syndicated loans, especially signed recently, might contain rating change triggers or other types of covenants that might accelerate payments and distort published liquidity schedules.

Thus, in early October, Bank Alliance said that it is close to a breach of covenants of one of its smaller syndicated loans, which stipulated the minimum acceptable proportion of deposits to loans (the bank was the major victim of a flight to quality of retail depositors in August-September). The bank later specified that the amounts involved are relatively immaterial ($45mn), nevertheless, as is the case with all ‘unknown unknowns’, the potential threat of similar statements Alliance or other banks probably should not be underestimated.

B. Bond buybacks

In our opinion, one should take statements about ‘market buybacks’ from Kazakh banks with a pinch of salt. All external bonds are long term and the major point of concern currently seems to be orderly redemption of short-term debt obligations. As long as external investors are in doubt, whether the system has enough liquidity or not, it might not make sense from the point of view of improvement of investor sentiment to use the valuable money to redeem the long-term debt. In addition, potential downgrades and redistribution of deposits might lead to a violation of covenants for syndicated loans (as we heard from Alliance) and subsequent acceleration of payments, i.e. the banks might suddenly discover that they need more available cash than planned. Through buybacks, banks can probably achieve some reduction of funding costs, although they would obviously reduce the asset base. However, if any particular bank felt comfortable to do so, market repurchases of bonds would obviously be positive for the secondary pricing.

Liquidity and funding assessment of individual banks We think that the large Kazakh banks’ (within the top six) refinancing requirements can be viewed as manageable on a standalone basis: (1) most of them have already managed to refinance part of the short-term indebtedness through syndicated or bilateral loans; (2) all banks report a balanced asset/ liabilities maturity profile so, in theory, can repay maturing loans from gradually matured assets; (3) owners of several banks and the banks themselves have large identifiable and, potentially, valuable assets outside of Kazakhstan and, in theory, can use them as collateral for/ sources of financing and recapitalisation.

Covenants of syndicated loans – ‘unknown knowns’

Bond buybacks would not make sense in the environment of deficit financing

Renaissance Capital Kazakh banks 22 October 2007

27

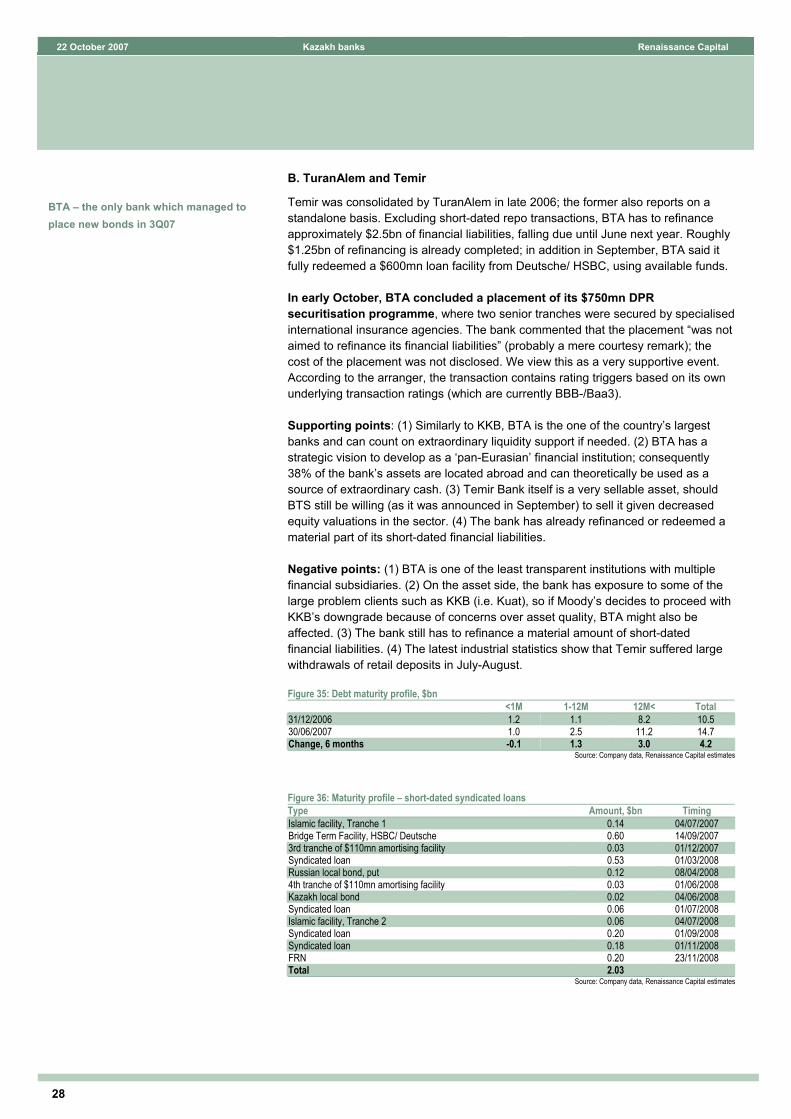

A. Kazkommerzbank

The largest Kazakh bank has probably the highest short-term refinancing requirements. Excluding short-dated repo transactions, it has to refinance approximately $2.6bn of financial liabilities, falling due until June next year. Since June $600mn of refinancing has been completed; in early August, KKB cancelled the solicited exchange of $500mn of bonds maturing in 2009 into longer-dated issue due to unfavourable market conditions. The closest large redemption is in December, when the bank has to repay or rollover a $700mn syndicated loan facility. As a potential redemption source the bank’s representatives mentioned the possibility of using cash from maturing assets.

Supporting points: (1) KKB is the country’s largest bank and obviously can count on extraordinary liquidity support if needed. (2) 33% of the bank’s assets are located abroad and might be used as a source of extraordinary cash. (3) The bank’s shares are actively tradable on the international stock exchanges and are very liquid, so there is always the potential of additional equity funding. (4) The bank can also count on other forms of support from local authorities, as evidenced by the recent statements of highly ranked Kazakh officials (share purchases on the open market etc.).

Negative points: (1) So far, KKB is the only Kazakh bank on a negative rating review (Moody’s). (2) The bank has the highest refinancing requirements in the whole sector. (3) KKB probably cannot issue more new insured DPRs, like BTA did, since it already has an established DPR programme. (4) 3Q IFRS accounts show that the bank lost $1bn of deposits (retail and wholesale) in the quarter (local accounts suggested only $120mn in July-August).

Figure 32: Debt maturity profile, $bn <1M 1-12M 12M< Total

31/12/2006 2.7 1.6 6.0 10.2 30/06/2007 2.1 2.6 9.6 14.4 Change, 6 months -0.6 1.0 3.6 4.1

Source: Company data, Renaissance Capital estimates