Katie Sam UW-Stout Senior CREDIT AND DEBT MANAGEMENT AMONG COLLEGE STUDENTS: PRACTICES AND...

27

Katie Sam UW- Stout Senior CREDIT AND DEBT MANAGEMENT AMONG COLLEGE STUDENTS: PRACTICES AND IMPLICATIONS

-

Upload

clifton-harvey -

Category

Documents

-

view

217 -

download

0

Transcript of Katie Sam UW-Stout Senior CREDIT AND DEBT MANAGEMENT AMONG COLLEGE STUDENTS: PRACTICES AND...

Katie Sam

UW-StoutSenior

CREDIT AND DEBT MANAGEMENT

AMONG COLLEGE STUDENTS:

PRACTICES AND IMPLICATIONS

Credit – Ability of a customer to obtain goods and services before payment

Debt – State of owing money

If you use credit, you accumulate debt

CREDIT AND DEBT

FINANCIAL MARKET IS GROWING IN BOTH SIZE & COMPLEXITY

Easier for Average American to: Invest in the MarketManage Own Stock/Mutual Fund InvestmentsSet Up Various Savings Tools

More Young Adults Have Access to Credit to:Pay for EducationMake Ends MeetMake Major Life Purchases

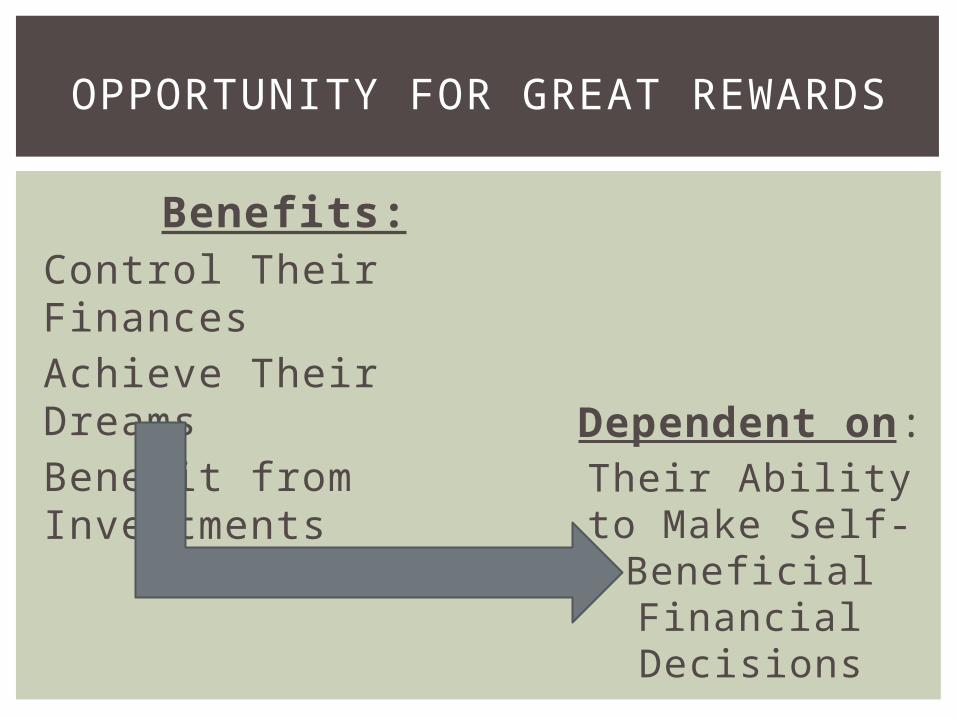

OPPORTUNITY FOR GREAT REWARDS

Benefits:Control Their FinancesAchieve Their DreamsBenefit from Investments

OPPORTUNITY FOR GREAT REWARDS

Dependent on:Their Ability to

Make Self-Beneficial Financial Decisions

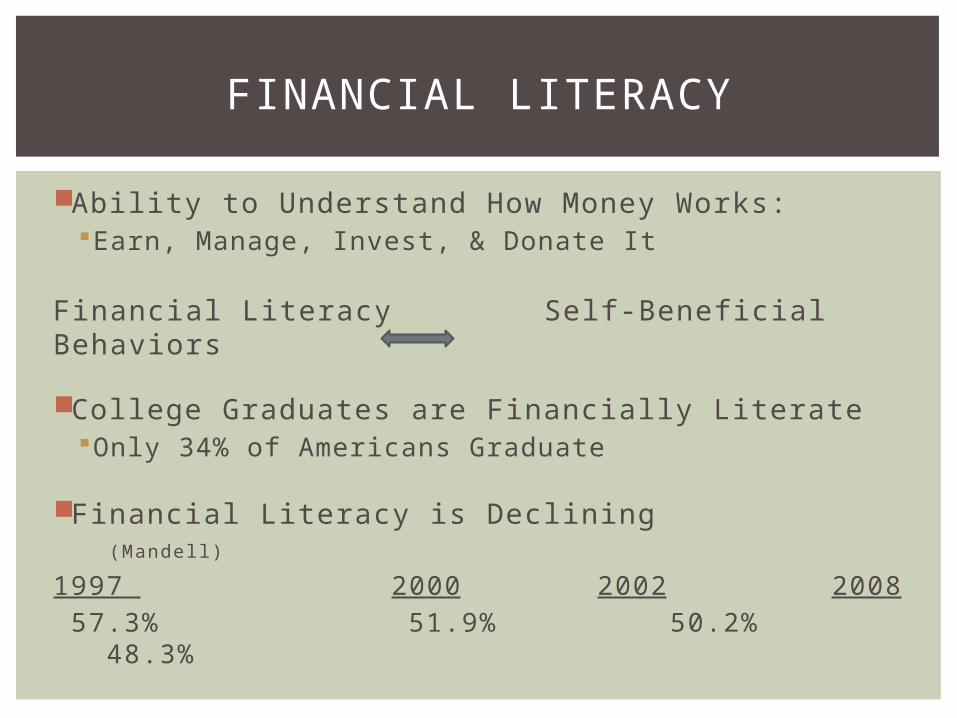

Ability to Understand How Money Works:Earn, Manage, Invest, & Donate It

Financial Literacy Self-Beneficial Behaviors

College Graduates are Financially LiterateOnly 34% of Americans Graduate

Financial Literacy is Declining (Mandell)

1997 2000 2002 2008 57.3% 51.9% 50.2% 48.3%

FINANCIAL LITERACY

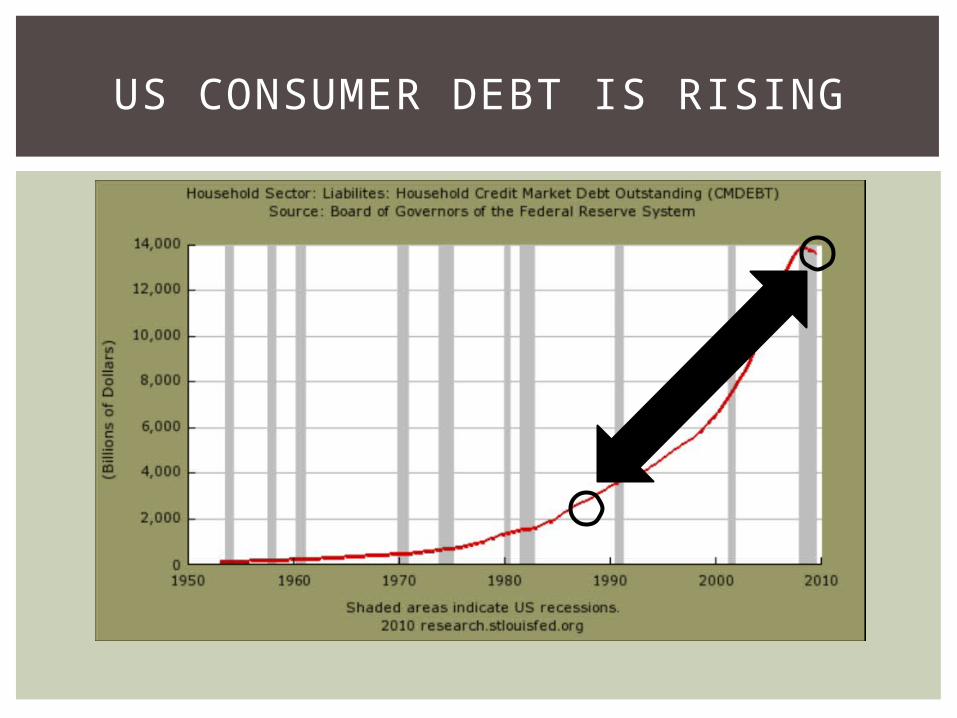

US CONSUMER DEBT TRENDS

US CONSUMER DEBT IS RISING

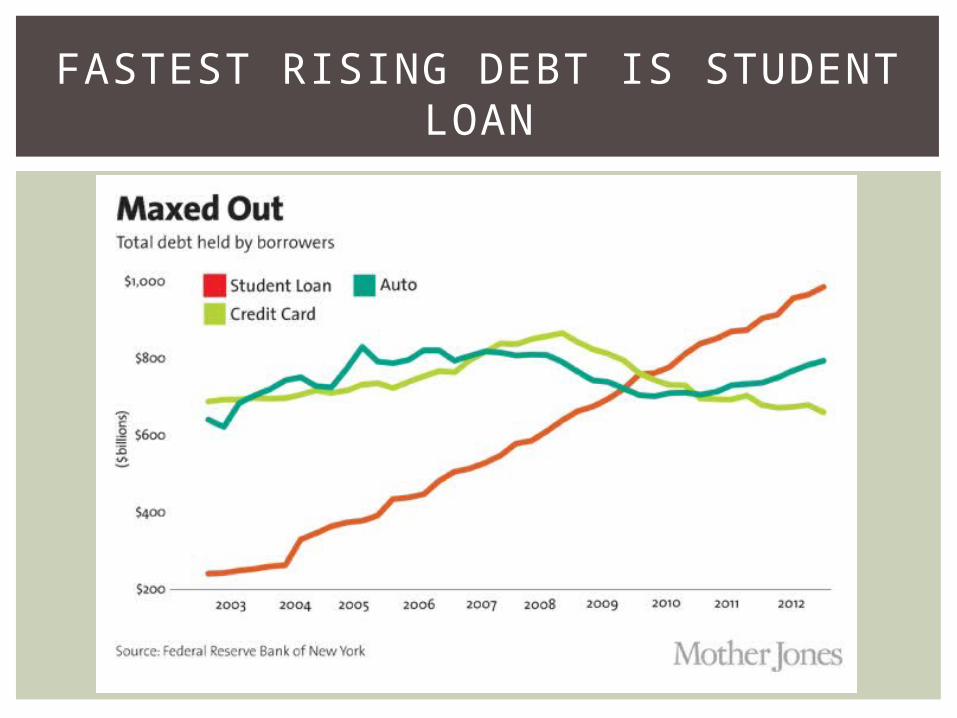

FASTEST RISING DEBT IS STUDENT LOAN

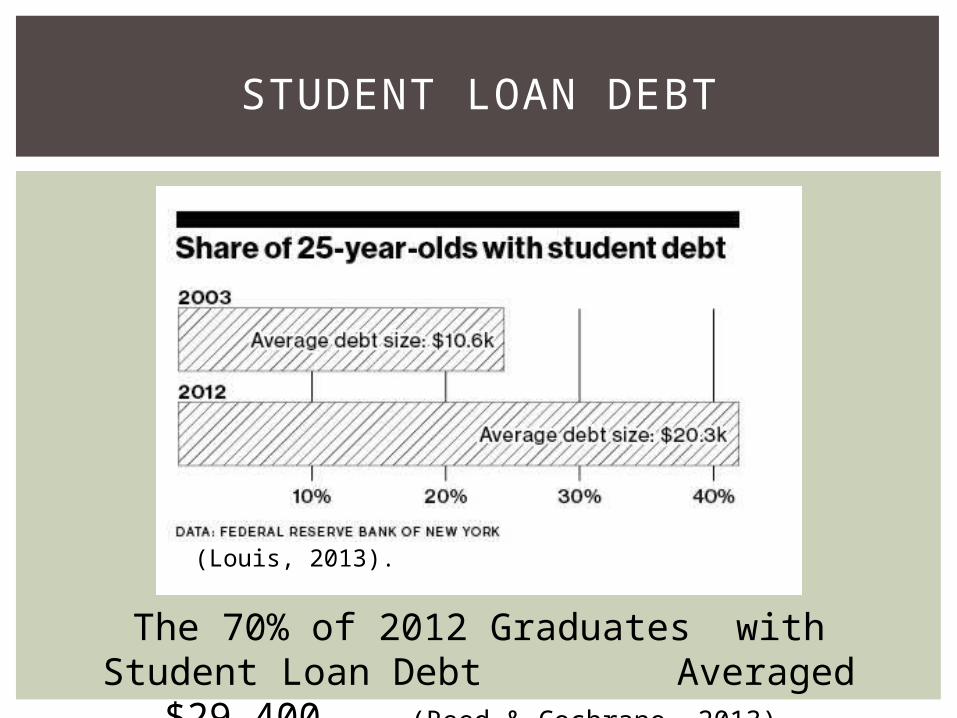

STUDENT LOAN DEBT

The 70% of 2012 Graduates with Student Loan Debt Averaged $29,400 (Reed

& Cochrane, 2013).

(Louis, 2013).

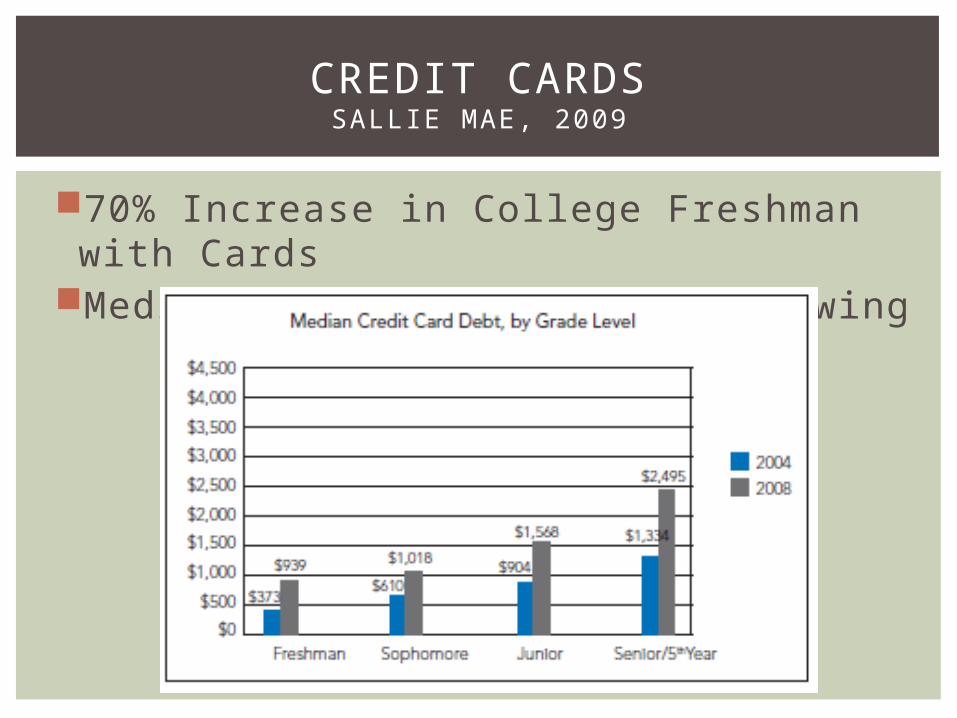

70% Increase in College Freshman with Cards

Median Debt at Every Grade Growing

CREDIT CARDSSALLIE MAE, 2009

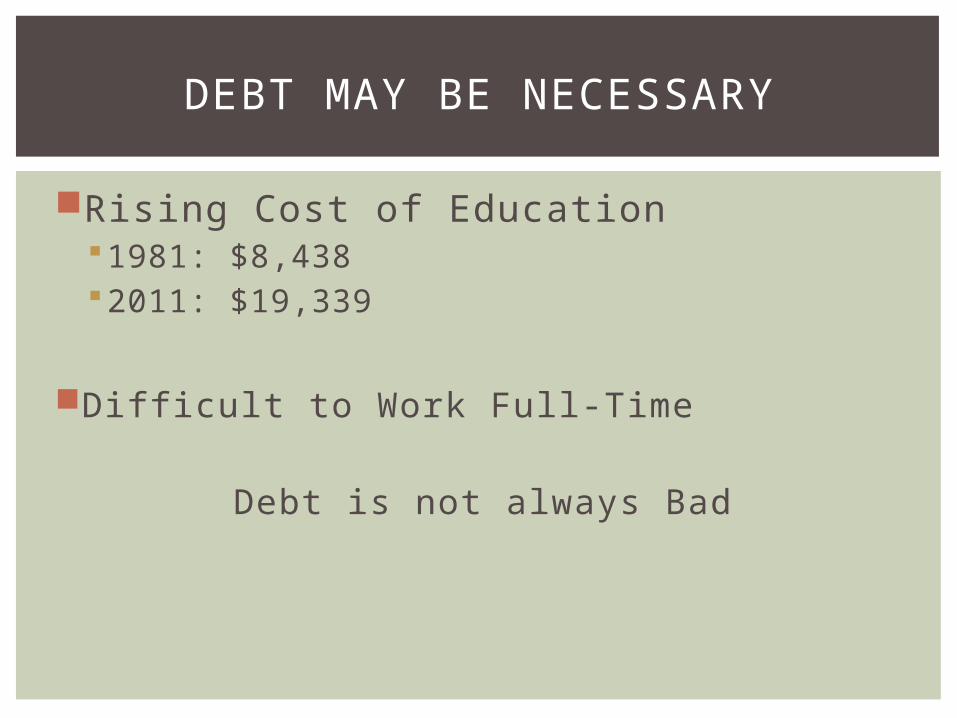

Rising Cost of Education1981: $8,4382011: $19,339

Diffi cult to Work Full-Time

Debt is not always Bad

DEBT MAY BE NECESSARY

Use Credit to Live Beyond Your Means40% Respondents Charged Item Knowing They Didn’t have the Money to Pay (Sallie Mae, 2009)

Accumulating Debts Aren’t Paid OffFailure to Recognize Costs Associated

with Borrowing Money

BAD DEBT PRACTICES

What Students Know What They Don’t Know

Credit Limit Late Fee Payments

Current Balance Overbalance Fees

Interest Rates

STUDENTS AT UW-STOUT

No Cards

1 Card

2+ Cards

$0

Under $5,000

Under $10,000

Over $20,000

0% 20% 40% 60% 80% 100%

Freshman

Senior

SENIORS HOLD MORE DEBT/CARDSTo

tal

Deb

t#

C

ard

s

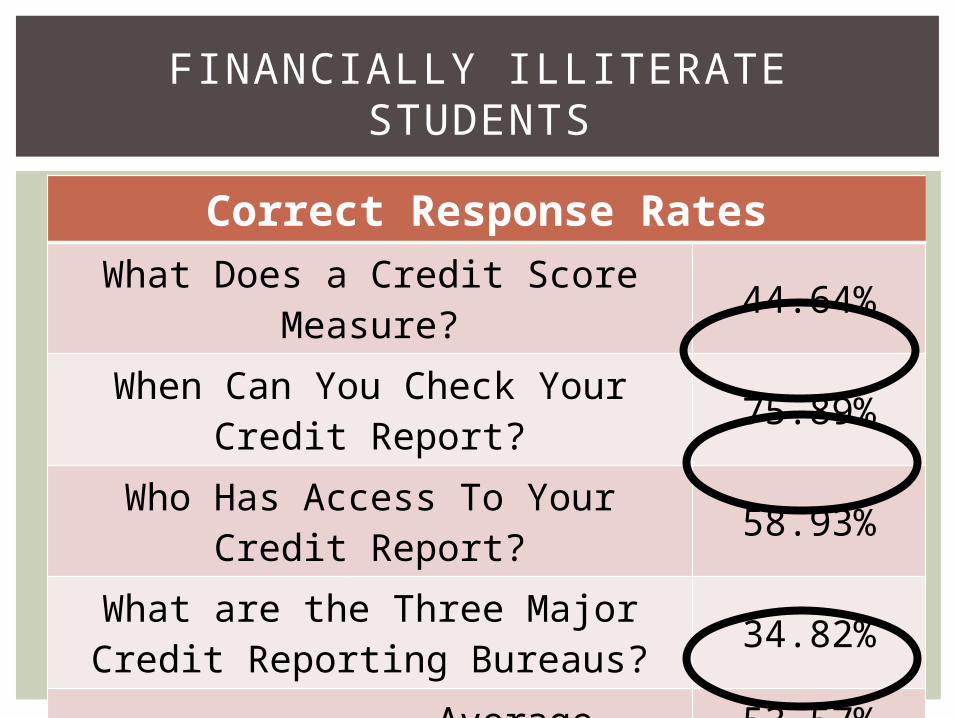

Correct Response RatesWhat Does a Credit Score

Measure? 44.64%

When Can You Check Your Credit Report? 75.89%

Who Has Access To Your Credit Report? 58.93%

What are the Three Major Credit Reporting Bureaus? 34.82%

Average 53.57%

FINANCIALLY ILLITERATE STUDENTS

Pinto & Mansfield, 2006

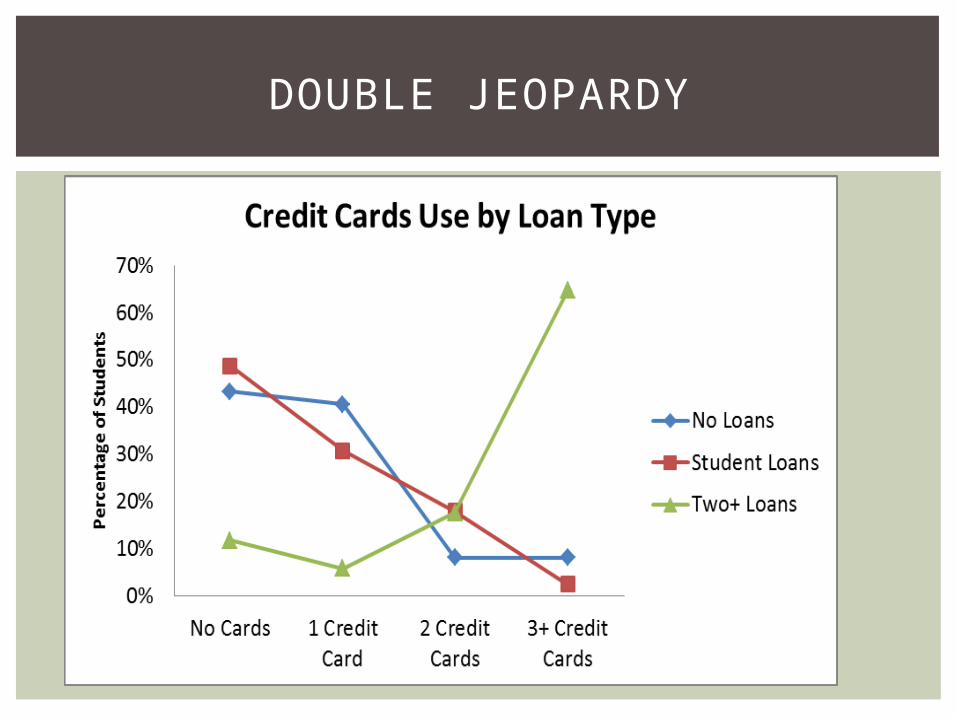

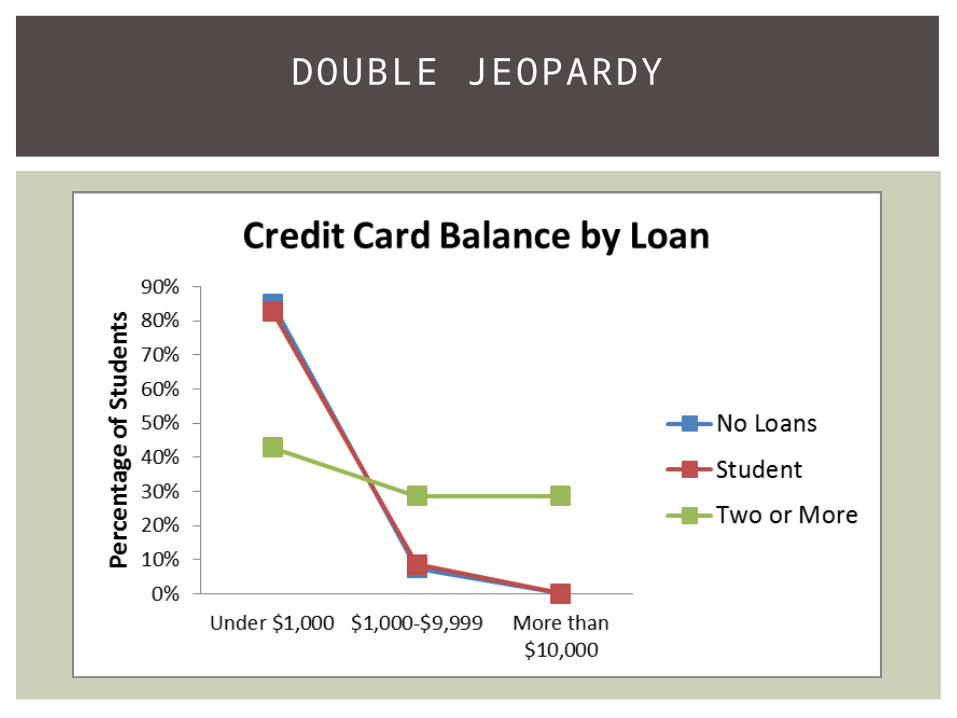

DOUBLE JEOPARDY:

HIGHER OUTSTANDING

CREDIT BALANCES ARE ASSOCIATED

WITH HIGH STUDENT LOAN

DEBT

DOUBLE JEOPARDY

DOUBLE JEOPARDY

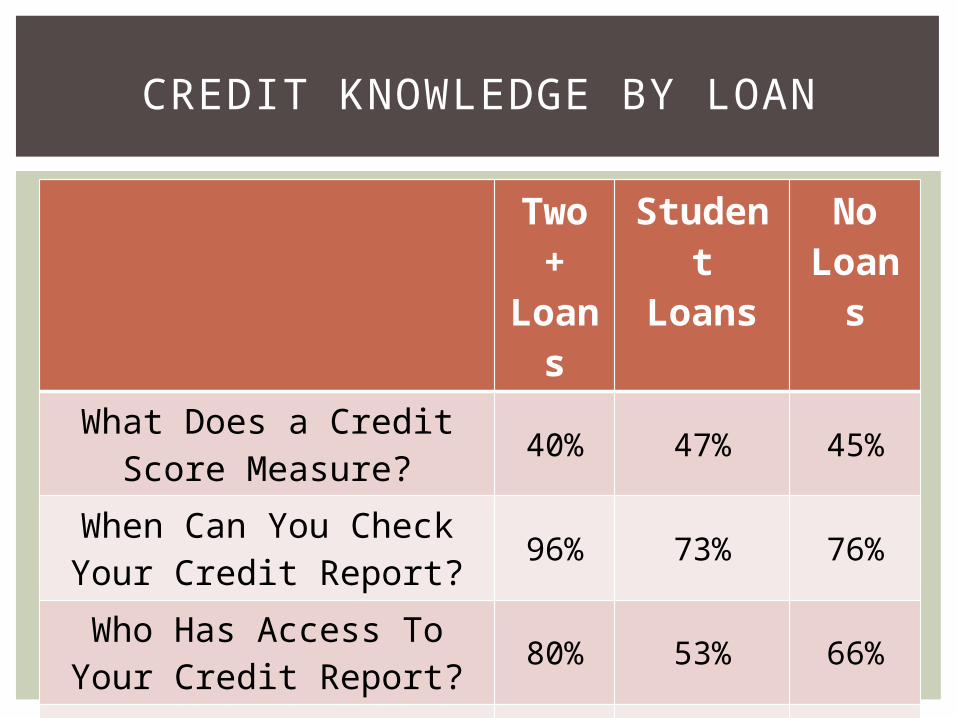

Two +

Loans

Student Loans

No Loan

s

What Does a Credit Score Measure?

40% 47% 45%

When Can You Check Your Credit Report?

96% 73% 76%

Who Has Access To Your Credit Report?

80% 53% 66%

What are the Three Major Credit Reporting

Bureaus?67% 19% 55%

Average 71% 48% 60.5%

CREDIT KNOWLEDGE BY LOAN

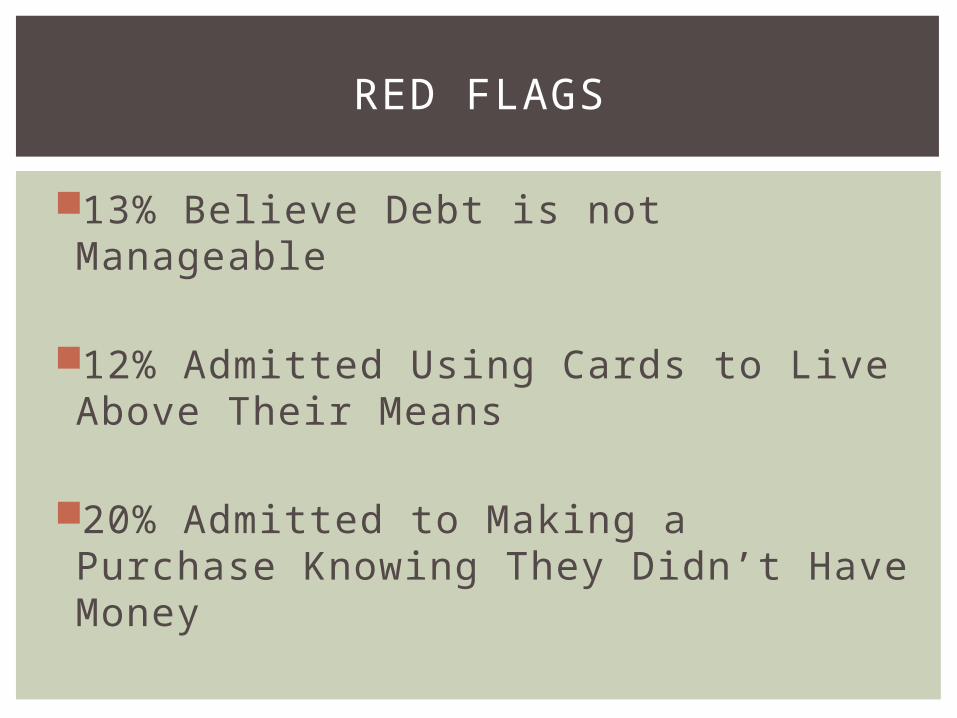

13% Believe Debt is not Manageable

12% Admitted Using Cards to Live Above Their Means

20% Admitted to Making a Purchase Knowing They Didn’t Have Money

RED FLAGS

LONG TERM IMPLICATIONS

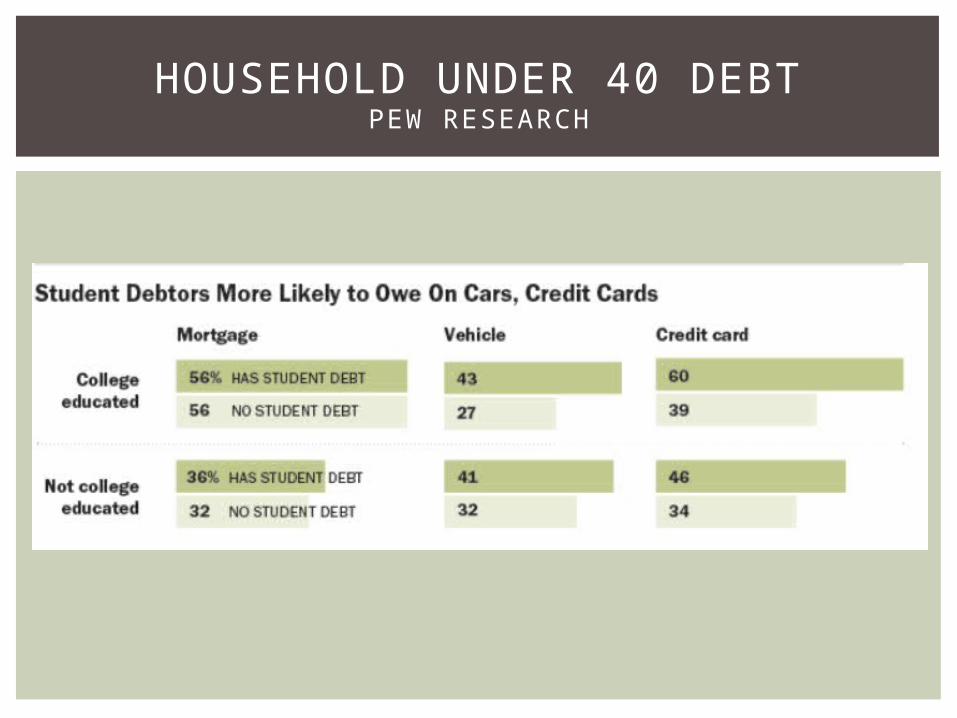

HOUSEHOLD UNDER 40 DEBTPEW RESEARCH

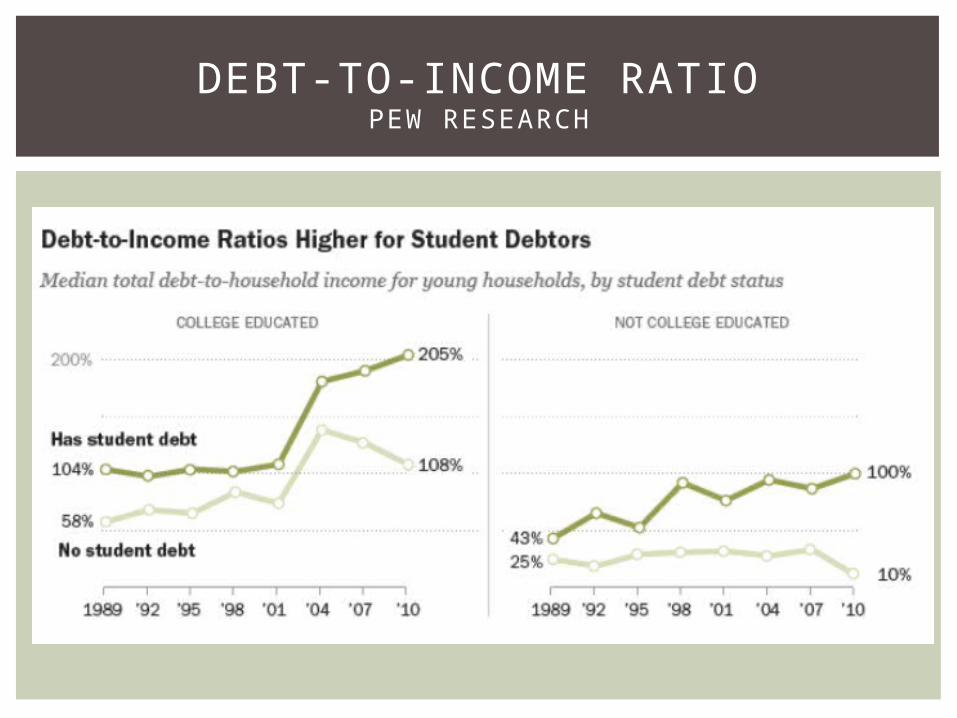

DEBT-TO-INCOME RATIOPEW RESEARCH

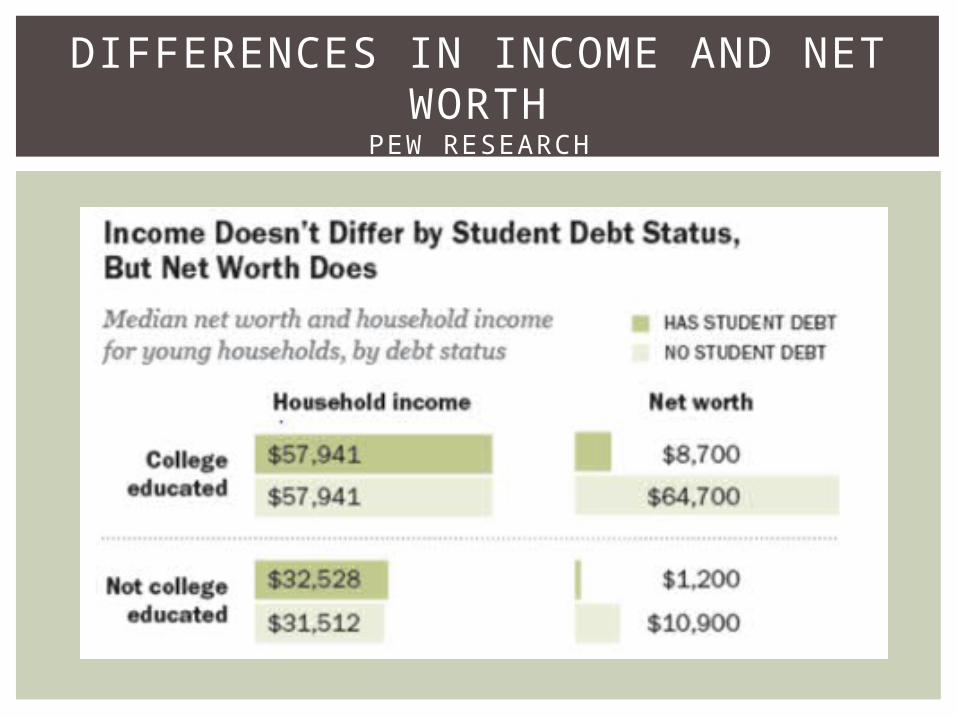

DIFFERENCES IN INCOME AND NET WORTH

PEW RESEARCH

Accumulate More Debt

Harder to:Pay off Debt QuicklySave Early for Major Purchases & RetirementAccumulate Assets

Impede Ability/Desire to take out Small Business Loans

LONG TERM CONSEQUENCES

THANK YOU