Karnataka Power Sector Reforms -Issues in...

24

Karnataka Power Sector Reforms -Issues in Restructuring- (Finance & Accounts areas) August 23, 2010 Bengaluru Resource persons: H.L Mukunda DCA, KPTCL & Vasuki, Director, Dhiya consulting Pvt. Ltd.

Transcript of Karnataka Power Sector Reforms -Issues in...

Karnataka Power Sector Reforms

-Issues in Restructuring- (Finance & Accounts areas)

August 23, 2010

Bengaluru

Resource persons: H.L Mukunda DCA, KPTCL & Vasuki, Director, Dhiya consulting Pvt. Ltd.

Contents

• Understanding the industry structure

• Financial restructuring

• Balance sheet cleaning up

• Cash management issues

• Subsidy administration

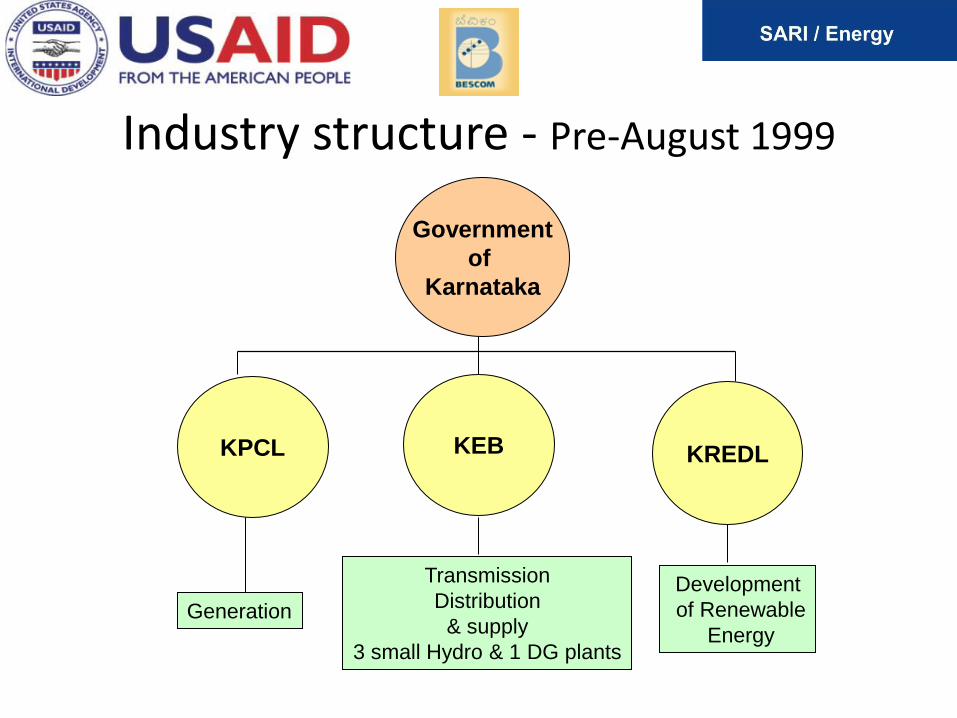

Industry structure - Pre-August 1999

Government

of

Karnataka

KPCL KEB KREDL

Generation

Transmission

Distribution

& supply

3 small Hydro & 1 DG plants

Development

of Renewable

Energy

Reform working groups formation Formation of Working Groups for Restructuring

– Karnataka Electricity Board constituted eight Working Groups in May 99

– Chief Financial Adviser was nominated as Director (Reforms)

– Exclusive Reforms Directorate established

• Working groups :

1. Financial Restructuring Group

2. Corporatization Group

3. Asset Listing, Identification and Valuation Group

4. Technical Up gradation and Investment Planning Group

5. Human Resource Development Group

6. Communication Group

7. Tariff Rationalization Group.

8. Distribution configuration Group

ToR for FRP Group • Take steps that are necessary to transform the existing accounting

procedure and practices to suit the corporate accounting practices

• Review the existing book-keeping methods, financial statements, audit

procedures and suggest corrective measures

• Examine KEB’s financial statements, Balance Sheet and propose a

restructuring action plan

• Make financial projections (including resource mobilization for investment

programme with reference to borrowing caps as well as debt management

limits as worked out by the Budget and Resources Section) keeping in view

the restructured scenario.

• Study the existing administrative hierarchy in the accounts cadre and

suggest correctives, if necessary

Sub groups under FRWG • Fixed Assets

• Capital Work in Progress

• Stocks and Assets not in use

• Cash and Bank Balances

• Receivables against supply of power

• Loans and Advances to Staff

• Sundry Receivables and Security Deposit from Consumers

• Power Purchase and related Contingent Liabilities

• Advances to Suppliers and Liability for supply of Materials

• Staff Related liabilities including study of unfunded liabilities

• Debt Servicing Obligations of existing as well as future loans

ToR for sub groups • Matching of Accounts Balances with Subsidiary Registers in respect of each

item in the Books of Accounts

• Appointment of Actuary and actuarial valuation of unfunded liabilities

• Identification of Contingent Liabilities in general and Power Purchase in

particular

• Examine major receivables from consumers and propose action plan for

clearance

• Ways and Means of funding unfunded liabilities

• Analysis of Existing Debt Profile and propose Debt Restructuring

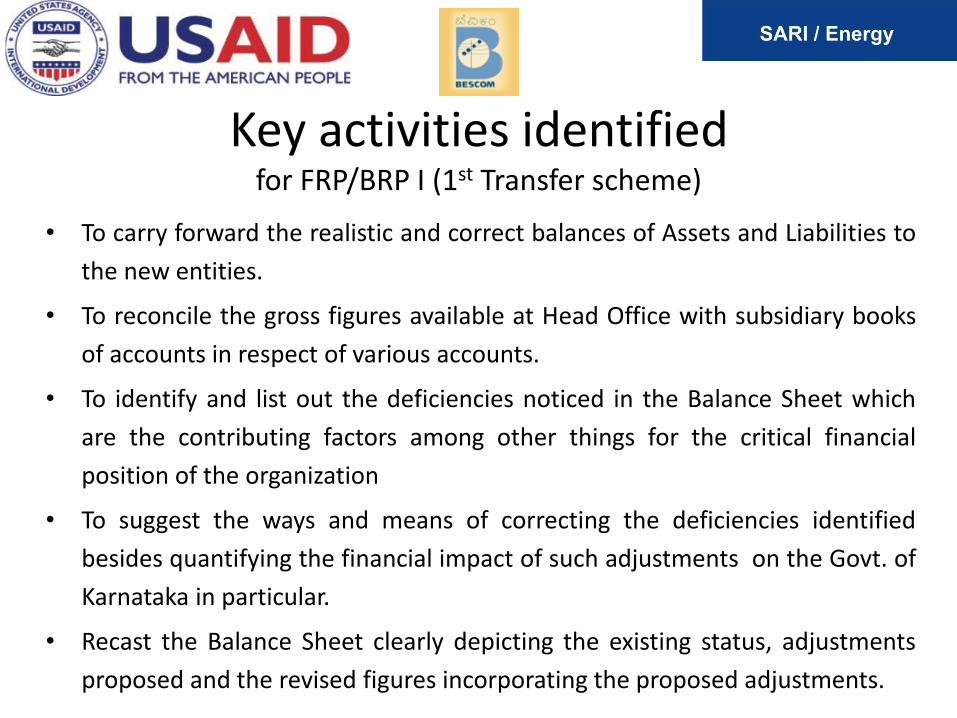

Key activities identified for FRP/BRP I (1st Transfer scheme)

• Make necessary changes required in Accounts to suit Corporate environment

• Diagnostic Study of existing Balance Sheet of KEB and evolving solution /

measures to overcome deficiencies

• Preparation of Closing Balance Sheet of KEB

• Segregation of Balance Sheet into KPTCL and VVNL Balance Sheets

• Develop Financial Projections for next five years and device alternate options

• Finding various funding options for new entities

• Take steps for maintenance of Transmission and Distribution Accounts

separately

Key activities identified for FRP/BRP I (1st Transfer scheme)

• To carry forward the realistic and correct balances of Assets and Liabilities to

the new entities.

• To reconcile the gross figures available at Head Office with subsidiary books

of accounts in respect of various accounts.

• To identify and list out the deficiencies noticed in the Balance Sheet which

are the contributing factors among other things for the critical financial

position of the organization

• To suggest the ways and means of correcting the deficiencies identified

besides quantifying the financial impact of such adjustments on the Govt. of

Karnataka in particular.

• Recast the Balance Sheet clearly depicting the existing status, adjustments

proposed and the revised figures incorporating the proposed adjustments.

Summary of recommendations • Write-back of power purchase liability of Rs.48.23 Crs.

• Recognition of contingent liability relating to power purchase Rs.581.05 Crs.

• Write-off of Rs.8.82 Crs. Assets not in use and write-back of Rs.5.93 Crs. stock

of materials.

• Assessment of Unfunded staff related liability by the Actuary Rs.2142 Crs.

• Write-back of Rs.7.60 Crs. and write-off of Rs.6.50 Crs. under Receivables for

sale of power.

• Suggested action plan for bringing down level of receivables through

securitization, cross-debt adjustment etc.

• Suggested action plan for clearance of huge arrears relating power purchase

through measures like cash payments, issue of Trade Bonds, cross-debt

adjustment, waiver of interest, etc.

Government Approval • The GoK approved the Balance Sheet Restructuring Plan – I (BRP-I) along

with the Financial Restructuring Plan, which was a significant step in the

direction of cleansing up the balance sheet of the erstwhile KEB

• The burden of cleaning of KEB Balance sheet on Government was Rs.819.28

crs

• Besides, as an one time measure, the outstanding dues of urban local

bodies were defrayed through a securitization programme

• A mechanism was also introduced to recover the local body dues on a

monthly basis

Key points

• Bridge consultants who later reviewed the Balance sheet cleansing

proposal fully agreed with the recommendations

• Almost all the recommendations of FR Group was accepted by GoK

• World Bank team placed on record the good wok done by FR Group

Reconstitution of Working group • In May 2001 working groups were constituted and 1o Groups

were formed:-

• Financial Restructuring

• Distribution configuration

• Revenue Improvement

• HRD and Change management

• Corporate Planning

• Commercialization

• Tariff Rationalization

• Technical Interface and Demand Supply Planning

• Social Assessment and Communication

• Asset Listing and Identification

ToR for FR Group • Disaggregation of the Karnataka Power Transmission Company Limited (“KPTCL”)

(post-corporatisation T&D Company) balance sheet in to Transmission and

Distribution Company’s (four Discoms) Balance sheet and proposing balance sheet

clean up process for each of the new entities

• Preparation of financial transfer scheme for transfer of assets, liabilities, and

personnel from KPTCL to distribution companies

• Assist the consultants in audit of accounts receivables and allocation to each

distribution company

• Developing mechanisms for improving the financial and accounting system in the

context of corporatisation and unbundling

• Make financial projections keeping in view the restructured scenario

FRP and BRP II Recommendations

• FRP Working group and the FDP consultants made the following

recommendations to GoK for BRP II adjustments before notifying the

opening balance sheets of new discoms:-

• Write off KPTCL’s receivables up to Rs 866 Crs. and retaining the same in

Government books as receivables

• Tripartite adjustment of Rs. 878 Crs. between GoK, KPTCL and KPCL to clear

off KPCL long term debt to GoK, GoK’s subsidy dues to KPTCL and KPTCL’s

power purchase dues to KPCL

• Government to take over servicing of long term debt of Rs 1050 Crs.

• Funding of terminal benefits as per “Pay as you go” concept

• Total support of Rs. 12140 Crs for power sector for next 10 years

Government approval • Government of Karnataka accepted all the recommendations and approved

the FRP and BRP II

• The principles observed for FRP and BP were in line with the Detailed Policy

Statement announced by the Government of Karnataka (GoK) during

January 2001, wherein it was mentioned that:

“Efforts will be made to ensure that as far as possible the newly formed

utilities are not burdened with historic liabilities. It is the intention of the

Government of Karnataka that the utilities particularly distribution

companies, start their operations with a clean balance sheet”.

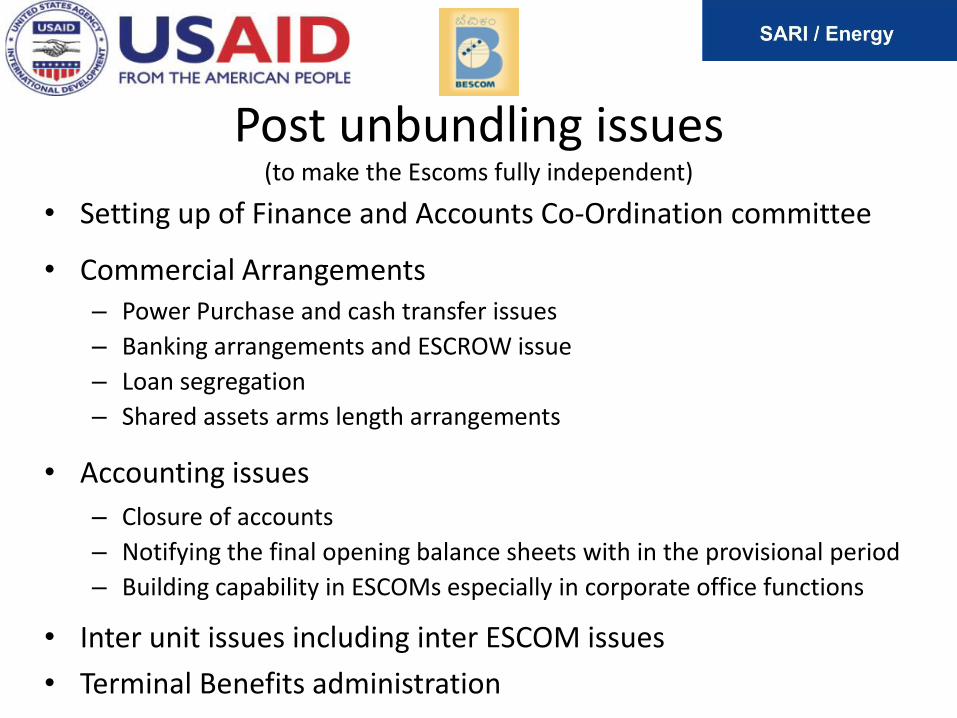

Post unbundling issues (to make the Escoms fully independent)

• Setting up of Finance and Accounts Co-Ordination committee

• Commercial Arrangements – Power Purchase and cash transfer issues

– Banking arrangements and ESCROW issue

– Loan segregation

– Shared assets arms length arrangements

• Accounting issues

– Closure of accounts

– Notifying the final opening balance sheets with in the provisional period

– Building capability in ESCOMs especially in corporate office functions

• Inter unit issues including inter ESCOM issues

• Terminal Benefits administration

BRP III Pre-BRP III -

KPTCL BRP III

Post BRP III -

KPTCL

Assets

Fixed Assets

- Gross Block 5,426 - 5,426

- Less: Accumulated Depreciation 2,121 - 2,121

- Net Block 3,304 - 3,304

- Capital work in progress 691 - 691

Total fixed assets 3,995 - 3,995

Investments 46 - 46

Current Assets

- Interest accrued on investments and deposits 2 - 2

- Inventories, stores and work in progress 232 - 232

- Sundry debtors 1,381 (709) 672

- Receivables from trading of power - - -

- Cash balances 36 - 36

- Bank balances 251 - 251

- Loans and advances 422 - 422

- Subsidy receivable from GoK 814 - 814

- Other assets 535 - 535

- Miscellaneous exp not written off 27 - 27

- IUA (57) 57 -

Total Current Assets 3,642 (652) 2,989

Less

Total Current liabilities

- Liability for supply of power 1,633 - 1,633

- Liability for supplies / works 405 - 405

- Staff related liabilities and provisions 437 - 437

Unpaid Salary and Other liabilities 34 - 34

Borrowing for working Capital - - -

Security deposits from Contractors in Cash 50 - 50

Security deposit other than Cash 71 - 71

- Other liabilities and provisions 327 - 327

Total Current liabilities 2,956 - 2,956

Net Current Assets 686 (652) 33

Total Assets 4,727 (652) 4,075

Rs. In crs.

BRP III Liabilities

Networth 1,571 (300) 1,271

Service line and security deposits

- Security deposit from consumer 1,246 - 1,246

- Service line deposit from consumers 336 (288) 48

Sub-total 1,581 (288) 1,294

Total Loans (a+b+c) 1,575 (65) 1,510

Total liabilities 4,727 (652) 4,075

Long term debt to equity ratio 1.00 1.19

Long term debt to equity ratio (security deposit as ST debt) 0.50 0.59

Total debt to equity ratio 2.01 2.21

Fixed asset coverage ratio 2.54 2.65

Rs. In crs.

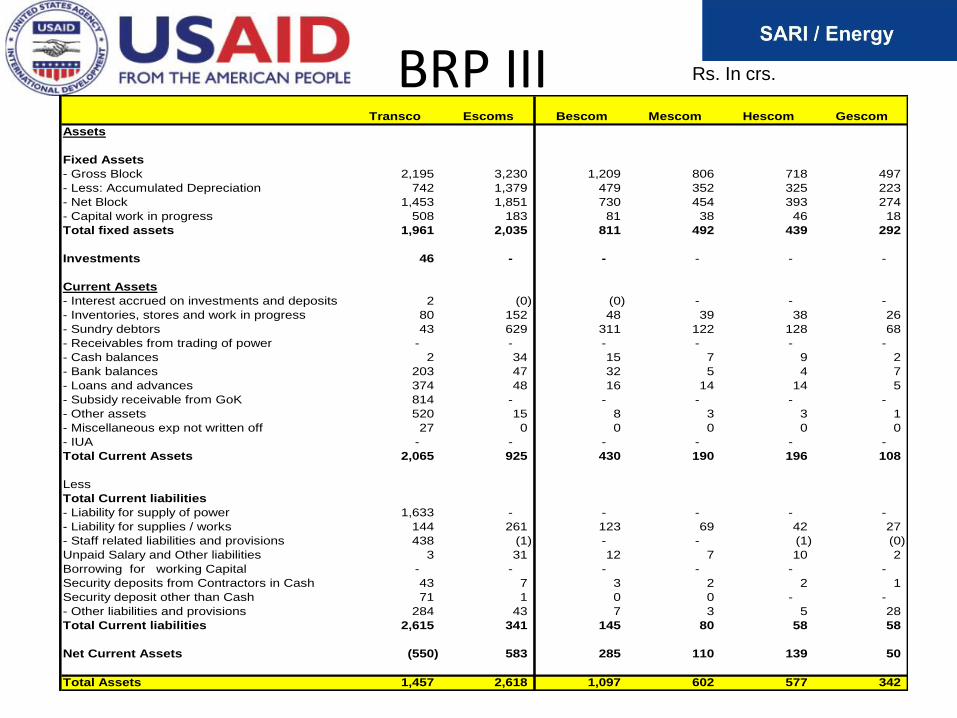

BRP III Transco Escoms Bescom Mescom Hescom Gescom

Assets

Fixed Assets

- Gross Block 2,195 3,230 1,209 806 718 497

- Less: Accumulated Depreciation 742 1,379 479 352 325 223

- Net Block 1,453 1,851 730 454 393 274

- Capital work in progress 508 183 81 38 46 18

Total fixed assets 1,961 2,035 811 492 439 292

Investments 46 - - - - -

Current Assets

- Interest accrued on investments and deposits 2 (0) (0) - - -

- Inventories, stores and work in progress 80 152 48 39 38 26

- Sundry debtors 43 629 311 122 128 68

- Receivables from trading of power - - - - - -

- Cash balances 2 34 15 7 9 2

- Bank balances 203 47 32 5 4 7

- Loans and advances 374 48 16 14 14 5

- Subsidy receivable from GoK 814 - - - - -

- Other assets 520 15 8 3 3 1

- Miscellaneous exp not written off 27 0 0 0 0 0

- IUA - - - - - -

Total Current Assets 2,065 925 430 190 196 108

Less

Total Current liabilities

- Liability for supply of power 1,633 - - - - -

- Liability for supplies / works 144 261 123 69 42 27

- Staff related liabilities and provisions 438 (1) - - (1) (0)

Unpaid Salary and Other liabilities 3 31 12 7 10 2

Borrowing for working Capital - - - - - -

Security deposits from Contractors in Cash 43 7 3 2 2 1

Security deposit other than Cash 71 1 0 0 - -

- Other liabilities and provisions 284 43 7 3 5 28

Total Current liabilities 2,615 341 145 80 58 58

Net Current Assets (550) 583 285 110 139 50

Total Assets 1,457 2,618 1,097 602 577 342

Rs. In crs.

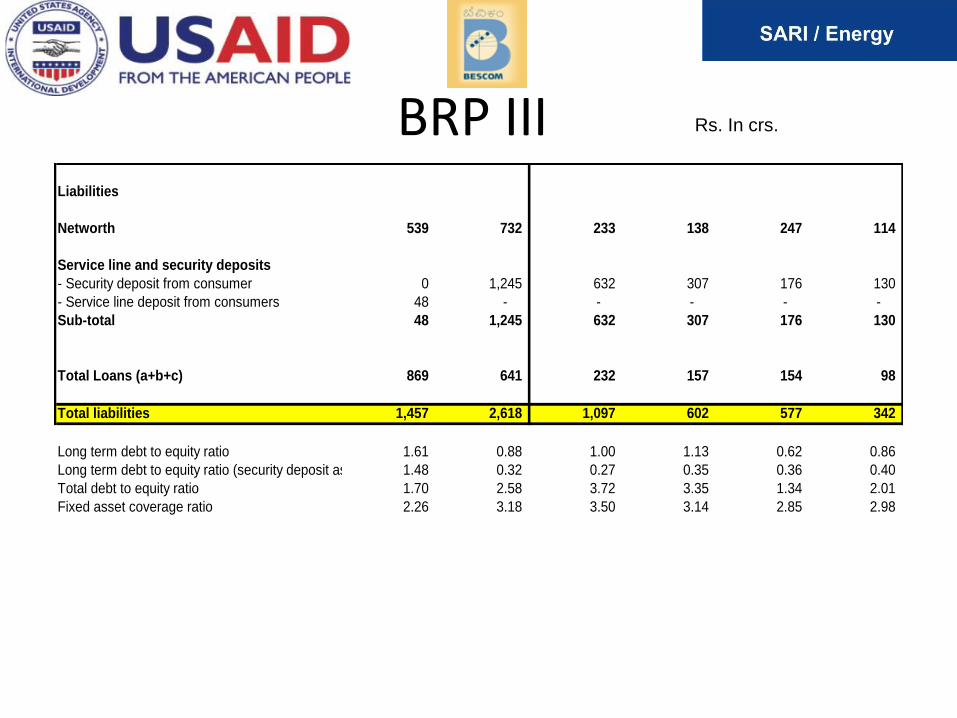

BRP III Liabilities

Networth 539 732 233 138 247 114

Service line and security deposits

- Security deposit from consumer 0 1,245 632 307 176 130

- Service line deposit from consumers 48 - - - - -

Sub-total 48 1,245 632 307 176 130

Total Loans (a+b+c) 869 641 232 157 154 98

Total liabilities 1,457 2,618 1,097 602 577 342

Long term debt to equity ratio 1.61 0.88 1.00 1.13 0.62 0.86

Long term debt to equity ratio (security deposit as ST debt) 1.48 0.32 0.27 0.35 0.36 0.40

Total debt to equity ratio 1.70 2.58 3.72 3.35 1.34 2.01

Fixed asset coverage ratio 2.26 3.18 3.50 3.14 2.85 2.98

Rs. In crs.

Implementation issues Management of existing Loans

• Loan allocation criteria

– End use – Transmission, Distribution, General capex, Corporate loans – Security offered – Escrow, Mortgage, Guarantee – Loan term

• There was objection from the lenders for transfer of disaggregated loans to

the books of ESCOMs

• KPTCL entered into a back to back arrangement with ESCOMs

• Depending on the Loan repayment schedule for each loan, KPTCL serviced

the loan and ESCOMs contributed their portion till all the loans were repaid

in 2009

• Further drawls for the already sanctioned loan came to KPTCL books initially

and was later transferred to ESCOMs by KPTCL

• Only fresh loans were drawn by ESCOMs

Implementation issues Cash management

• Unbundling happened w.e.f. 1st June 2002

• From 1st June 2002 to 30th Sept. 2002, KPTCL managed all cash management

issues of discoms

– All existing Bank accounts continued – Both operative and non-operative

– Separate cash book for each discom was opened by KPTCL

– Treated as receivable and payable in KPTCL books. Net balance was set off

against the BST

• From 1st October 2002, discoms took over the management of cash on their

own

– New disbursement bank accounts opened at Headquarters

– Collecting bank and disbursement bank accounts at field level changed to the

name of discom

– Fund transfer from HO and remittance to HO ( as per erstwhile practice)

continued at discom level also

Implementation issues Subsidy management

• Initially (till June 2005) the subsidy for the sector as a whole was received by

KPTCL

• Subsidy receivable comprised of :-

– Cash releases

– Electricity tax collected and retained

– Tripartite adjustments

– Other adjustments

• This was allocated by KPTCL on the basis “Gap” approved by KERC in the ERC

order

• Amount payable to each ESCOM by KPTCL was set off against the BST and

other receivables like loan repayment, interest on loans etc., from ESCOMs

• Post June 2005 subsidy is being received by ESCOMs directly from

Government of Karnataka

Thank you

![THE KARNATAKA DEVADASIS (PROHIBITION OF …dpal.kar.nic.in/pdf_files/10 of 1962 (E).pdf · 1962: KAR. ACT 10] Land Reforms 1 THE KARNATAKA LAND REFORMS ACT, 1961 . ARRANGEMENT OF](https://static.fdocuments.net/doc/165x107/5ac31bbc7f8b9af91c8ba2dd/the-karnataka-devadasis-prohibition-of-dpalkarnicinpdffiles10-of-1962.jpg)

![ARRANGEMENT OF SECTIONS - Kardpal.kar.nic.in/10 of 1962 (E).pdf1962: KAR. ACT 10] Land Reforms 1 THE KARNATAKA LAND REFORMS ACT, 1961 ARRANGEMENT OF SECTIONS Statement of Objects and](https://static.fdocuments.net/doc/165x107/5ab2910c7f8b9aea528d6838/arrangement-of-sections-of-1962-epdf1962-kar-act-10-land-reforms-1-the-karnataka.jpg)