Karl Schmedders - Home - HKUST Business School Materials.pdf · EMAIL:...

185

Karl Schmedders MANAGERIAL ECONOMICS & DECISION SCIENCES Visiting Professor of Managerial Economics & Decision Sciences PhD, 1996, Operations Research, Stanford University MS, 1992, Operations Research, Stanford University Vordiplom, 1990, Business Engineering, Universitat Karlsruhe, Highest Honors, Ranked first in a class of 350 EMAIL: [email protected] OFFICE: Jacobs Center Room 528 Karl Schmedders is Associate Professor in the Department of Managerial Economics and Decision Sciences. He holds a PhD in Operations Research from Stanford University. Professor Schmedders’ research interests include computational economics, general equilibrium theory, asset pricing and portfolio selection. His work has been published in Econometrica, The Review of Economic Studies, The Journal of Finance, and many other academic journals. He teaches courses in decision science both in the MBA and the EMBA program at Kellogg. Professor Schmedders has been named to the Faculty Honor Roll in every quarter he has taught at Kellogg. He has received numerous teaching awards, including the 2002 Lawrence G. Lavengood Outstanding Professor of the Year. Professor Schmedders is the only Kellogg faculty member to receive the ‘Ehrenmedaille’ (Honorary Medal) of Kellogg’s partner school WHU. Research Interests Mathematical economics, in particular general equilibrium models involving time and uncertainty Asset pricing Mathematical programming

Transcript of Karl Schmedders - Home - HKUST Business School Materials.pdf · EMAIL:...

Karl Schmedders

MANAGERIAL ECONOMICS & DECISION SCIENCES

Visiting Professor of Managerial Economics & Decision

Sciences

PhD, 1996, Operations Research, Stanford University

MS, 1992, Operations Research, Stanford University

Vordiplom, 1990, Business Engineering,

Universitat Karlsruhe, Highest Honors, Ranked first in a

class of 350

EMAIL: [email protected]

OFFICE: Jacobs Center Room 528

Karl Schmedders is Associate Professor in the Department of Managerial Economics and

Decision Sciences. He holds a PhD in Operations Research from Stanford University.

Professor Schmedders’ research interests include computational economics, general equilibrium

theory, asset pricing and portfolio selection. His work has been published in Econometrica, The

Review of Economic Studies, The Journal of Finance, and many other academic journals. He

teaches courses in decision science both in the MBA and the EMBA program at Kellogg.

Professor Schmedders has been named to the Faculty Honor Roll in every quarter he has taught

at Kellogg. He has received numerous teaching awards, including the 2002 Lawrence G.

Lavengood Outstanding Professor of the Year. Professor Schmedders is the only Kellogg

faculty member to receive the ‘Ehrenmedaille’ (Honorary Medal) of Kellogg’s partner school

WHU.

Research Interests

Mathematical economics, in particular general equilibrium models involving time and

uncertainty

Asset pricing

Mathematical programming

KH19, Course Description

1

Managerial Statistics

Course Description In this course we will cover the following topics:

Confidence Intervals Hypothesis Tests Regression Analysis

Our objective is to quickly cover the first two topics. While they are important by themselves many people describe them as rather “dry” course material. However, they will be of great help to us when we cover the main subject of the course, regression analysis. Regressions are extremely useful and can deliver eye-opening insights in many managerial situations. You will solve some entertaining case studies which show the power of regression analysis. We will cover the material in this case packet as well as the following chapters of the textbook:

Sections 13.1 and 13.2 of chapter 13; Section 14.1 of chapter 14; Chapter 15; Chapter 16; Chapter 19; Chapter 21; Chapter 23.

Time permitting, we will also cover parts of chapter 25. There will be several team assignments. After the conclusion of the course, there will be an in-class final exam on the first day of the following module, that is, on April 1, 2016. The final grades in this course will be determined as follows.

Team assignments: 40% Class participation: 10% Final Exam: 50%

KH19, Course Description

2

In case you would like to prepare for our course, you should start reading the relevant sections of Chapters 13 and 14 in our textbook. Before you do that, please also consider the following suggestions. 1) Review the material on the normal distribution from your probability course. In

particular, you should review the use of the functions NORMDIST, NORMSDIST, NORMINV and NORMSINV in Excel.

2) We will use the software KStat that was developed at Kellogg. Ideally you should install KStat on your laptop before our first class.

I realize that all of you are very busy and you may not have the time to prepare at length for our course. Please note, however, that the better you prepare the faster we can cover the early parts of the course material and the more time we have for the fun part, the coverage of regression analysis. Of course, I am happy to help you with your preparation. Please do not hesitate to contact me with any questions or concerns. My email address is [email protected].

September 29, 1998

When Scientific Predictions Are So Good They're Bad By WILLIAM K. STEVENS

NOAH had it easy. He got his prediction straight from the horse's mouth and was left in no doubt about what to do.

But when the Red River of the North was rising to record levels in the spring of 1997, the citizens and officials of Grand Forks, N.D., were not so privileged. They had to rely on scientists' predictions about how high the water would rise. And in this case, Federal experts say, the flood forecast may have been issued and used in a way that made things worse.

The problem, the experts said, was that more precision was assigned to the forecast than was warranted. Officials and citizens tended to take as gospel an oft-repeated National Weather Service prediction that the river would crest at a record 49 feet. Actually, there was a wider range of probabilities; the river ultimately crested at 54 feet, forcing 50,000 people to abandon their homes fast. The 49-foot forecast had lulled the town into a false sense of security, said Dr. Roger A. Pielke Jr. of the National Center for Atmospheric Research in Boulder, Colo., a consultant on a subsequent inquiry by the weather service.

In fixating on the single number of 49 feet, the people involved in the Grand Forks disaster made a common error in the use of predictions and forecasts, experts who have studied the case say. It was, they say, a case of what Alfred North Whitehead, the mathematician and philosopher, once termed ''misplaced concreteness.'' And whether the problem is climate change, earthquakes, droughts or floods, they say the tendency to overlook uncertainties, margins of error and ranges of probability can lead to damaging misjudgments.

The problem was the topic of a workshop this month at Estes Park, Colo. In part, participants said, the problem arises becausedecision makers sometimes want to avoid making hard choices in uncertain situations. They would rather place responsibility on the predictors.

Scientifically based predictions, typically using computerized mathematical models, have become pervasive in modern society. But only recently has much attention been paid to the proper use -- and misuse -- of predictions. The Estes Park workshop, of which Dr. Pielke was an organizer, was an attempt to come to grips with the question. The workshop was sponsored by the Geological Society of America and the National Center for Atmospheric Research.

People have predicted and prophesied for millenniums, of course, through means ranging from the visions of shamans and the warnings of biblical prophets to the examination of animal entrails. With the arrival of modern science, people teased out fundamental laws of physical and chemical behavior and used them to make better and better predictions.

But once science moves beyond the relatively deterministic processes of physics and chemistry, prediction gets more complicated and chancier. The earth's atmosphere, for instance, often frustrates efforts to predict the weather and long-term climatic changes because scientists have not nailed down all of its physical workings and because a substantial measure of chaotic unpredictability is inherent in the climate system. The result is a considerable range of uncertainty, much more so than is popularly associated with science. So while computer modeling has often made reasonable predictions possible, they are always uncertain; results are by definition a model of reality, not reality itself.

The accuracy of predictions varies widely. Some, like earthquake forecasts, have proved so disappointing that experts have turned instead to forecasting longer-term earthquake potential in a general sense and issuing last-second warnings to distant communities once a quake has begun.

In some cases, the success of a prediction is near impossible to judge. For instance, it will take thousands of years to know whether the environmental effects of buried radioactive waste will be as predicted.

On the other hand, daily weather forecasts are checked almost instantly and are used to improve the next day's forecast. But weather forecasting is also a success, the assembled experts agreed, because people know its shortcomings and take them into consideration. Weather forecasts ''are wrong a lot of the time, but people expect that and they use them accordingly,'' said

Page 1 of 3When Scientific Predictions Are So Good They're Bad - The New York Times

7/15/2009http://www.nytimes.com/1998/09/29/science/when-scientific-predictions-are-so-good-they...

Robert Ravenscroft, a Nebraska rancher who attended the workshop as a ''user'' of predictions.

A prediction is to be distrusted, workshop participants said, when it is made by the group that will use it as a basis for policy making -- especially when the prediction is made after the policy decision has been taken. In one example offered at the workshop, modeling studies purported to show no harmful environmental effects from a gold mine that a company had decided to dig.

Another type of prediction miscue emerged last March in connection with asteroids, the workshop participants were told by Dr. Clark R. Chapman, a planetary scientist at the Southwest Research Institute in Boulder. An astronomer erroneously calculated that there was a chance of one-tenth of 1 percent that a mile-wide asteroid would strike Earth in 30 years. The prediction created an international stir but was withdrawn a day later after further evidence turned up.

This ''uncharacteristically bad'' prediction, said Dr. Chapman, would not have been issued had it been subjected to normal review by the forecaster's scientific peers. But, he said, there was no peer-review apparatus set up to make sure that ''off-the-wall predictions don't get out.'' (Such a committee has since been established by NASA.)

Most sins committed in the name of prediction, however, appear to stem from the uncertainty inherent in almost all forecasts. ''People don't understand error bars,'' said one scientist, referring to margins of error. Global climate change and the Red River flood offer two cases in point.

Computer models of the climate system are the major instruments used by scientists to project changes in climate that might result from increasing atmospheric concentrations of heat-trapping gases, like carbon dioxide, emitted by the burning of fossilfuels.

Basing its forecast on the models, a panel of scientists set up by the United Nations has projected that the average surface temperature of the globe will rise by 2 to 6 degrees Fahrenheit, with a best estimate of 3.5 degrees, in the next century, and more after that. This compares with a rise of 5 to 9 degrees since the depths of the last ice age. The temperature has increased by about 1 degree over the last century.

But the magnitude and nature of any climate changes produced by any given amount of carbon dioxide are uncertain. Moreover, it is unclear how much of the gas will be emitted over the next few years, said Dr. Jerry D. Mahlman, a workshop participant who directs the National Oceanic and Atmospheric Administration's Geophysical Fluid Dynamics Laboratory at Princeton, N.J. The laboratory is one of the world's major climate modeling centers, and the oldest.

This uncertainty opens the way for two equal and opposite sins of misinterpretation. ''The uncertainty is used as a reason for governments not to act,'' in the words of Dr. Ronald D. Brunner, a political scientist at the University of Colorado at Boulder. On the other hand, people often put too much reliance on the precise numbers.

In the debate over climate change, the tendency is to state all the uncertainties and caveats associated with the climate model projections -- and then forget about them, said Dr. Steve Rayner, a specialist in global climate change in the District of Columbia office of the Pacific Northwest National Laboratory. This creates a ''fallacy of misplaced confidence,'' he said, explaining that the specific numbers in the model forecasts ''take on a validity not allowed by the caveats.'' This tendency to focus unwisely on specific numbers was termed ''fallacious quantification'' by Dr. Naomi Oreskes, a historian at the University of California at San Diego.

Where uncertainty rules, many at the workshop said, it might be better to stay away from specific numbers altogether and issue a more generalized forecast. In climate change, this might mean using the models as a general indication of the direction in which the climate is going (whether it is warming, for instance) and of the approximate magnitude of the change, while taking the numbers with a grain of salt.

None of which means that the models are not a helpful guide to public policy, said Dr. Mahlman and other experts. For example, the models say that a warming atmosphere, like today's, will produce heavier rains and snows, and some evidence suggests that this is already happening in the United States, possibly contributing to damaging floods. Local planners might be well advised to consider this, Dr. Mahlman said.

One problem in Grand Forks was that lack of experience with such a damaging flood aggravated the uncertainty of the flood forecast. Because the river had never before been observed at the 54-foot level, the models on which the prediction was based were ''flying blind,'' said Dr. Pielke; there was no historical basis on which to produce a reliable forecast.

But this was apparently lost on local officials and the public, who focused on the specific forecast of a 49-foot crest. This number was repeated so often, according to the report of an inquiry by the National Weather Service, that it ''contributed to an

Page 2 of 3When Scientific Predictions Are So Good They're Bad - The New York Times

7/15/2009http://www.nytimes.com/1998/09/29/science/when-scientific-predictions-are-so-good-they...

impression of certainty.'' Actually, the report said, the 49-foot figure ''created a sense of complacency,'' because it was only a fraction of a foot higher than the record flood of 1979, which the city had survived.

''They came down with this number and people fixated on it,'' Tom Mulhern, the Grand Forks communications officer, said in an interview. The dikes protecting the city had been built up with sandbags to contain a 52-foot crest, and everyone figured the town was safe, he said.

It is difficult to know what might have happened had the uncertainty of the forecast been better communicated. But it is possible, said Mr. Mulhern, that the dikes might have been sufficiently enlarged and people might have taken more steps to preserve their possessions. As it was, he said, ''some people didn't leave till the water was coming down the street.''

Photo: Petty Officer Tim Harris patroled an area of Grand Forks, N.D., in April 1997, where the Red River flooded the houses up to the second story. Residents, relying on the precision of forecasts, were forced to flee quickly. (Reuters)(pg. F6)

Copyright 2009 The New York Times Company Home Privacy Policy Search Corrections XML Help Contact Us Back to Top

Page 3 of 3When Scientific Predictions Are So Good They're Bad - The New York Times

7/15/2009http://www.nytimes.com/1998/09/29/science/when-scientific-predictions-are-so-good-they...

1 – Sampling

Managerial Statistics

KH 19

Course material adapted from Chapters 13.1, 13.2, and 14.1 of our textbookStatistics for Business, 2e © 2013 Pearson Education, Inc.

2

Learning Objectives

Describe why sampling is important

Understand the implications of sampling variation

Explain the flaw of averages

Define the concept of a sampling distribution

Determine the mean and standard deviation for the sampling distribution of the sample mean

Describe the Central Limit Theorem and its importance

Determine the mean and standard deviation for the sampling distribution of the sample proportion

3

Descriptive statistics

Collecting, presenting, and describing data

Inferential statistics

Drawing conclusions and/or making decisions concerning a population based only on sample data

Tools of Business Statistics

4

A Population is the set of all items or individuals of interest Examples: All likely voters in the next election

All parts produced todayAll sales receipts for March

A Sample is a subset of the population Examples: 1000 voters selected at random for interview

A few parts selected for destructive testingRandom receipts selected for audit

Populations and Samples

5

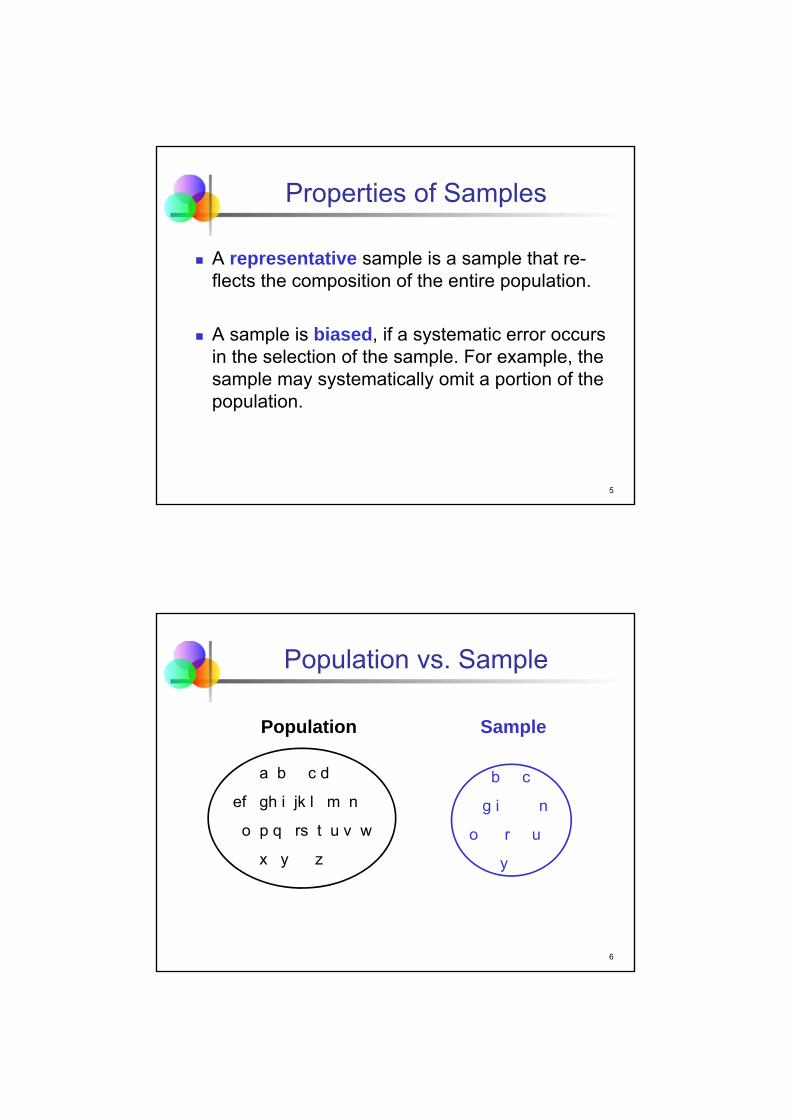

Properties of Samples

A representative sample is a sample that re-flects the composition of the entire population.

A sample is biased, if a systematic error occurs in the selection of the sample. For example, the sample may systematically omit a portion of the population.

6

Population vs. Sample

a b c d

ef gh i jk l m n

o p q rs t u v w

x y z

Population Sample

b c

g i n

o r u

y

7

Why Sample?

Less time consuming than a census

Less costly to administer than a census

It is possible to obtain statistical results of a sufficiently high precision based on samples

8

Two Surprising Properties

Surprise 1: The best way to obtain a repre-sentative sample is to pick members of the population at random.

Surprise 2: Larger populations do not require larger samples.

9

Randomization

A randomly selected sample is representative of the whole population (avoids bias).

Randomization ensures that on average a sample mimics the population.

Randomization enables us to infer character-istics of the population from a sample.

10

Comparison of Two Random Samples

Two large samples (each with 8,000 data points) drawn at random from a population of 3.5 million customers of a bank

11

(In)Famous Biased Sample

The Literary Digest predicted a landslide defeat for Franklin D. Roosevelt in the 1936 presiden-tial election. They selected their sample from, among others, a list of telephone numbers. The size of their sample was about 2.4 million!

Telephones were a luxury during and soon after the Great Depression. Roosevelt’s supporters tended to be poor and were grossly underrepre-sented in the sample.

12

Simple Random Sample (SRS)

A Simple Random Sample (SRS) is a sample of n data points chosen by a method that has an equal chance of picking any sample of size n from the population.

An SRS is the standard to which all other sampling methods are compared.

An SRS is the foundation for virtually all of the theory of statistics.

13

Making statements about a population by examining sample results

Sample statistics Population parameters

(known) Inference (unknown, but can

be estimated from

sample evidence)

Sample Population

Inferential Statistics

14

Tools of Inferential Statistics

Estimation Example: Estimate the population

mean age using the sample mean age.

Hypothesis Testing Example: Use sample evidence to

test the claim that the population mean age is 40.5 years.

Drawing conclusions and/or making decisions concerning a population based on sample results.

15

Estimating Parameters

Parameter: a characteristic of the population (e.g., mean µ)

Statistic: an observed characteristic of a sample (e.g., sample average )

Estimate: using a statistic to approximate a parameter

xy ,

16

Notation for Statistics and Parameters

17

Sampling Variation

Sampling Variation is the variability in the value of a statistic from sample to sample.

Two samples from the same population will rarely (if ever) yield the same estimate.

Sampling variation is the price we pay for working with a sample rather than the population.

18

The Flaw of Averages

19

The Flaw of Averages

Our culture encodes a strong bias either to neglect or ignore variation. We tend to focus instead on measures of central tendency, and as a result we make some terrible mistakes, often with considerable practical import.

Stephen Jay Gould, 1941 – 2002,

evolutionary biologist, historian of science

(continued)

20

Point Estimates

A sample statistics is a point estimate. It pro-vides a single number (e.g. the sample mean) for an unknown population parameter (e.g. the population mean).

A point estimate delivers no information on the possible sampling variation.

A key step in any careful statistical analysis is to quantify the effect of sampling variation.

21

Definitions

An estimator of a population parameter is a random variable that depends on sample

information . . .

whose value provides an approximation to this unknown parameter.

A specific value of that random variable is called an estimate.

22

Sampling Distributions

The sampling distribution is the proba-bility distribution that describes how a statistic, such as the mean, varies from sample to sample.

23

Testing of GPS Chips

A manufacturer of GPS chips selects samples for highly accelerated life testing (HALT).

HALT scores range from 1 (failure on first test) to 16 (chip endured all 15 tests without failure).

Even when the production process is functioning normally, there is variation among HALT scores.

24

Testing 400 Chips

Distribution of individual HALT scores

25

Distribution of Daily Average Scores

Distribution of average HALT scores

(54 samples, each with sample size n=20)

26

Benefits of Averaging

Averaging reduces variation: The sample-to-sample variance among average HALT scores is smaller than the variance among individual HALT scores.

The distribution of average HALT scores appears more “bell shaped” than the distribution of individual HALT scores.

27

Sampling Distributions

Sampling Distributions

Sampling Distribution of Sample Mean

Sampling Distribution of Sample Proportion

28

Expected Value of Sample Mean

Let x1, x2, . . . , xn represent a random sample from a population.

The sample mean value of these observations is defined as

The random variable “sample mean” is denoted by and its specific value in the sample by .

n

iixn

x1

1

X x

29

Standard Error of the Mean

Different samples from the same population will yield different sample means.

A measure of the variability in the mean from sample to sample is given by the Standard Error of the Mean:

The standard error of the mean decreases as the sample size increases.

n

σ)XSE(

30

Standard Error of the Mean

The standard error is proportional to σ. As population data become more variable, sample averages become more variable.

The standard error is inversely proportional to the square root of the sample size n. The larger the sample size, the smaller the sampling variation of the averages.

(continued)

31

If the Population is Normal

If a population is normally distributed with mean μ and standard deviation σ, then the sampling distribution of the sample mean is also normally distributed with

and

X

μ)XE( n

σ)XSE(

32

Normal Population Distribution

Normal Sampling Distribution (has the same mean)

Sampling Distribution Properties

( is unbiased )X x

x

μ)XE(

μ

)XE(

33

Sampling Distribution Properties

As n increases,

decreasesLarger sample size

Smaller sample size

x

(continued)

)XSE(

μ

34

If the Population is not Normal

We can apply the Central Limit Theorem:

Even if the population is not normal,

… sample means from the population will beapproximately normal as long as the sample size is large enough.

Properties of the sampling distribution:

andμ)XE( n

σ)XSE(

35

n↑

Central Limit Theorem

As the sample size gets large enough …

the sampling distribution becomes almost normal regardless of shape of population.

x

36

Population Distribution

Sampling Distribution (becomes normal as n increases)

Central Tendency

Variation

x

x

Larger sample size

Smaller sample size

If the Population is not Normal(continued)

Sampling distribution properties:

μ)XE(

n

σ)XSE(

μ)XE(

μ

37

How Large is Large Enough?

For most distributions, a sample size of n > 30will give a sampling distribution that is nearly normal.

For normal population distributions, the sampling distribution of the mean is always normally distributed regardless of the sample size.

38

More Formal Condition

Sample Size Condition for an application of the central limit theorem:

A normal model provides an accurate approxi-mation to the sampling distribution of if the sample size n is larger than 10 times the squared skewness and larger than 10 times the absolute value of the kurtosis,

and .

X

2310Kn 410Kn

39

Average HALT Scores

Design of the chip-making process indicates that the HALT score of a chip has a mean µ = 7 with a standard deviation σ = 4.

Sampling distribution of average HALT scores

(n = 20)

2

22

8902047 .

n

σ,μ~NX

40

Average HALT Scores

The sampling distribution of average HALT scores is (approximately) a normal distribution with mean 7 and standard deviation 0.89.

(continued)

41

Sampling Distributions ofSample Proportions

Sampling Distributions

Sampling Distribution of Sample Mean

Sampling Distribution of Sample Proportion

42

Population Proportions p

p = the proportion of the population having some characteristic

Sample proportion ( ) provides an estimate of p:

0 ≤ ≤ 1

p has a binomial distribution, but can be approximated by a normal distribution when n is large enough

size sampleinterest of sticcharacteri with thesample in the items#ˆ p

p

p

43

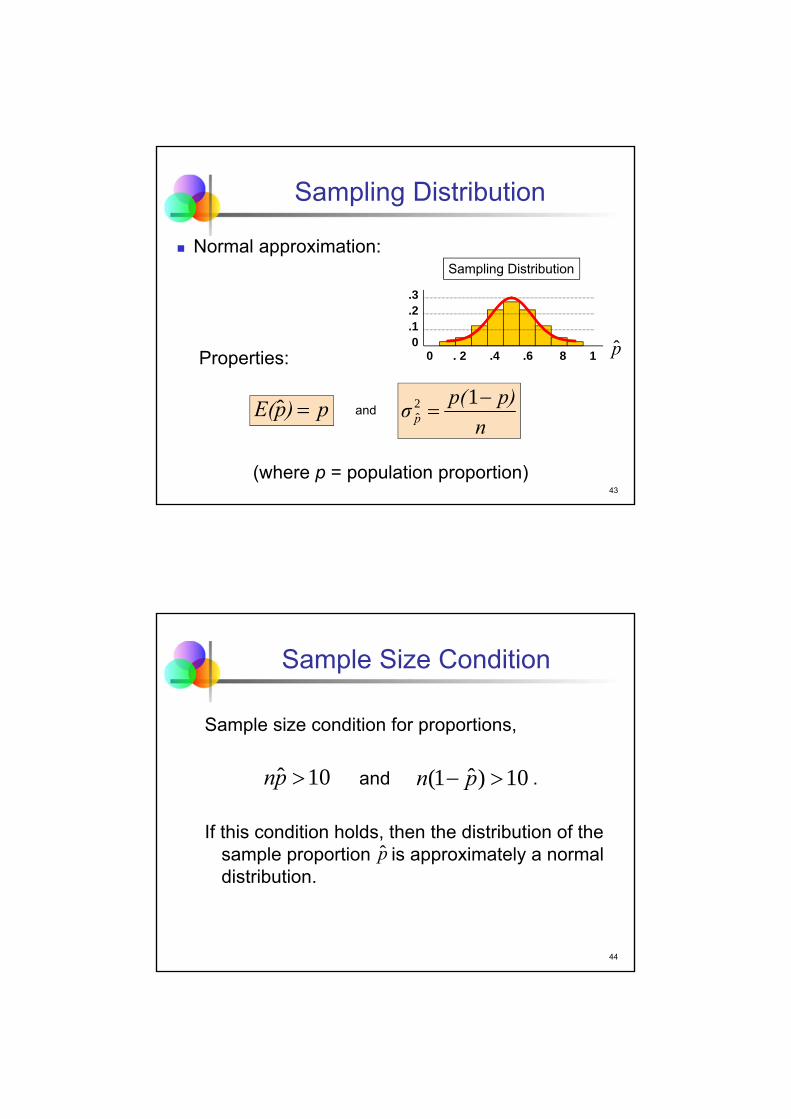

Sampling Distribution

Normal approximation:

Properties:

and

(where p = population proportion)

Sampling Distribution

.3

.2

.10

0 . 2 .4 .6 8 1

p)pE( ˆn

p)p(σ p

12ˆ

p

44

Sample Size Condition

Sample size condition for proportions,

and .

If this condition holds, then the distribution of the sample proportion is approximately a normal distribution.

10ˆ pn 10)ˆ1( pn

p

45

Take Aways

Understand the notion of sampling variation.

Appreciate the dangers of the flaw of averages.

Grasp the concept of a sampling distribution.

Have an idea of the central limit theorem.

Know the sampling distributions of a sample mean and of a sample proportion.

46

Pitfalls

Do not confuse a sample statistic for the population parameter.

Do not fall for the flaw of averages.

2 – Confidence Intervals

Managerial Statistics

KH 19

Course material adapted from Chapter 15 of our textbookStatistics for Business, 2e © 2013 Pearson Education, Inc.

2

Learning Objectives

Distinguish between a point estimate and a confidence interval estimate

Construct and interpret a confidence interval of a population proportion

Construct and interpret a confidence interval of a population mean

3

Point and Interval Estimates

A point estimate is a single number.

A Confidence Interval provides additional information about variability.

Point Estimate

Lower

Confidence

Limit

Upper

Confidence

Limit

Width of confidence interval

4

We can estimate a population parameter …

Point Estimates

with a sample statistic(a point estimate)

mean

proportion p

xμ

p

5

Confidence Interval Estimate

An interval gives a range of values: Takes into consideration variation in sample

statistics from sample to sample

Based on observation from a single sample

Provides more information about a population characteristic than does a point estimate

Relies on the sampling distribution of the statistic.

Stated in terms of level of confidence Can never be 100% confident

6

Estimation Process

(mean, μ, is unknown)

Population

Random Sample

Mean = 50

Sample

I am 95% confident that μ is between 40 and 60.

x

7

General Formula

The general formula for all confidence intervals is:

The value of the reliability factor depends on the desired level of confidence.

Point Estimate (Reliability Factor)(Standard Error)

8

Confidence Intervals

Population Mean

ConfidenceIntervals

PopulationProportion

9

Confidence Interval for the Proportion

Recall that the Central Limit Theorem implies a normal model for the sampling distribution of .

E( ) = p and SE( ) =

SE( ) is called the Standard Error of the Proportion.

npp /)1(

p

p p

p

10

Interpretation

The sample statistic in 95% of samples lies within 1.96 standard errors of the population parameter.

11

Interpretation

Probability that sample proportion deviates by less than 1.96 standard errors of the proportion from the true (but unknown) population propor-tion p is 95%.

P( –1.96 SE( ) ≤ p – ≤ +1.96 SE( ) ) = 0.95.

(continued)

p

p pp

12

95% Confidence Interval for p

For 95% of samples, the interval formed by reaching 1.96 standard errors to the left and right of will contain p.

Problem: We do not know the value of the standard error of the proportion, SE( ), since it depends on the true (but unknown) parameter p.

We estimate this standard error using in place of p,

p

p

p

n

)p(p)pse(

ˆ1ˆˆ

13

Confidence Interval for p

The 100(1 – α)% confidence interval for p is

where z/2 is the standard normal value for the level of

confidence desired (“reliability factor”)

is the sample proportion

n is the sample size

n

)p(pzpp

n

)p(pzp α/α/

ˆ1ˆˆˆ1ˆˆ 22

p

14

Finding the Reliability Factor, z/2

Consider a 95% confidence interval:

z = -1.96 z = 1.96

.951

.0252

α .025

2

α

Point EstimateLower Confidence Limit

UpperConfidence Limit

z units:

p units: Point Estimate

0

15

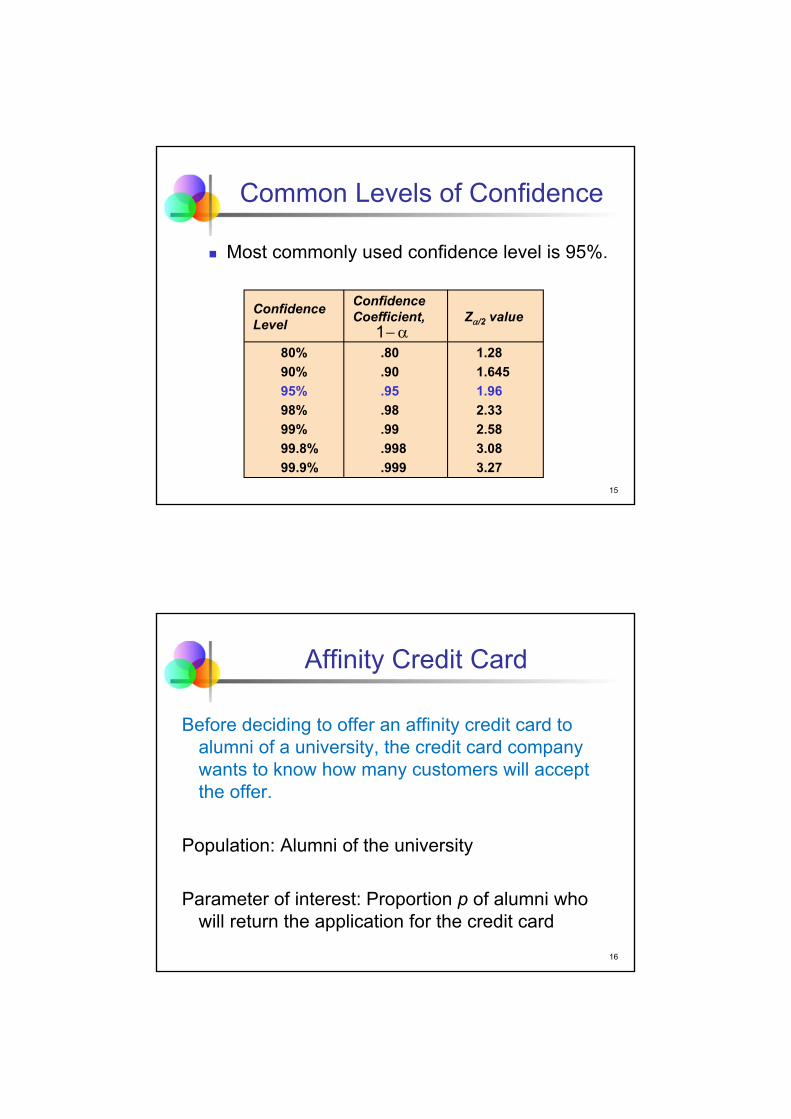

Common Levels of Confidence

Most commonly used confidence level is 95%.

Confidence Level

Confidence Coefficient, Z/2 value

1.28

1.645

1.96

2.33

2.58

3.08

3.27

.80

.90

.95

.98

.99

.998

.999

80%

90%

95%

98%

99%

99.8%

99.9%

1

16

Affinity Credit Card

Before deciding to offer an affinity credit card to alumni of a university, the credit card company wants to know how many customers will accept the offer.

Population: Alumni of the university

Parameter of interest: Proportion p of alumni who will return the application for the credit card

17

SRS of Alumni

Question: What should we conclude about the proportion p in the population of 100,000 alumni who will accept the offer if the card is launched on a wider scale?

Method: Construct a confidence interval based on the results of a simple random sample.

18

SRS of Alumni

The credit card issuer sent preapproved applica-tions to a sample of 1000 alumni. Of these, 140 accepted the offer and received the card.

Summary Statistics:

(continued)

19

Checklist for Application of Normal

SRS condition. The sample is a simple random sample from the relevant population.

Sample size condition (for proportion). Bothand are larger than 10.

pnˆ)ˆ1( pn

20

Credit Card: Confidence Interval

The estimated standard error is

The 95% confidence interval is

0.14 ± 1.96 × 0.01097 ≈ [0.1185, 0.1615]

0109701000

1401140ˆ .).(.

)pse(

21

Credit Card: Conclusion

With 95% confidence, the population proportion that will accept the offer is between 11.85% and 16.15%.

If the bank decides to launch the credit card, might 20% of the alumni accept the offer? It’s not impossible but rather unlikely given the information in our sample; 20% is outside the 95% confidence interval for the unknown proportion p.

22

Margin of Error

The confidence interval,

can also be written as

where ME is called the Margin of Error,

n

)p(pzpp

n

)p(pzp α/α/

ˆ1ˆˆˆ1ˆˆ 22

MEp ˆ

n

)p(pzα/

ˆ1ˆME 2

23

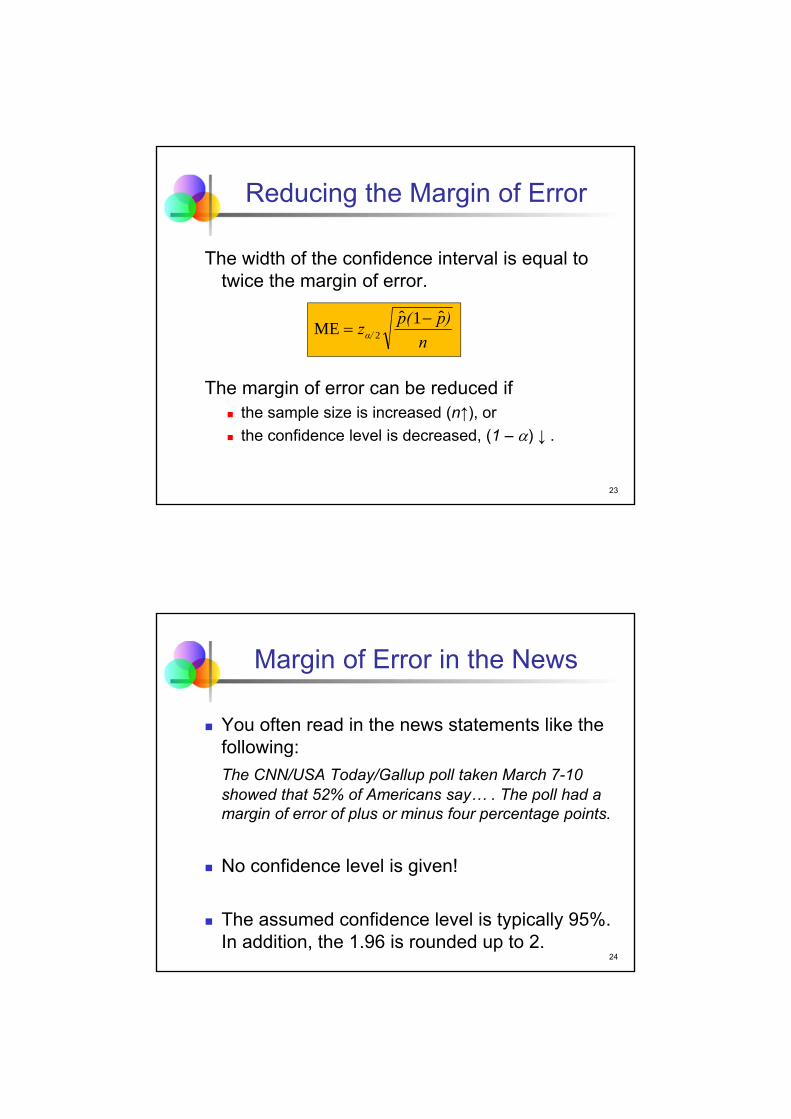

Reducing the Margin of Error

The width of the confidence interval is equal to twice the margin of error.

The margin of error can be reduced if the sample size is increased (n↑), or

the confidence level is decreased, (1 – ) ↓ .

n

)p(pzα/

ˆ1ˆME 2

24

Margin of Error in the News

You often read in the news statements like the following:

The CNN/USA Today/Gallup poll taken March 7-10 showed that 52% of Americans say… . The poll had a margin of error of plus or minus four percentage points.

No confidence level is given!

The assumed confidence level is typically 95%. In addition, the 1.96 is rounded up to 2.

25

Margin of Error in the News

For an interpretation of this statement we use the confidence interval formula

where ME = 0.04 ≥ .

We can have (slightly more than) 95% confidence that the true proportion of Americans saying … is between 48% and 56%.

(continued)

MEp ˆ

n

)p(p ˆ1ˆ2

26

Confidence Intervals

Population Mean

ConfidenceIntervals

PopulationProportion

27

Sampling Distribution of the Mean

Recall that the Central Limit Theorem implies a normal model for the sampling distribution of .

E( ) = μ and

SE( ) is called the Standard Error of the Mean.

X

X

X

n

σ)XSE(

28

Interpretation

Probability that sample mean deviates by less than 1.96 standard errors of the mean from the true (but unknown) population mean μ is 95%.

P( –1.96 SE( ) ≤ μ – ≤ +1.96 SE( )) = 0.95.

Once again, the sample statistic lies within about two standard errors of the corresponding population parameter in 95% of samples.

X X

X

X

29

Since the population standard deviation σ is unknown, we estimate it using the sample standard deviation, s.

This step introduces extra uncertainty, since sis variable from sample to sample.

As an adjustment, we use the t-distributioninstead of the normal distribution.

Confidence Interval for μ

11

2

n-

)x(xs

n

ii

30

Student’s t-Distribution

Consider an SRS of n observations with mean and standard deviation s

from a normally distributed population with mean μ.

Then the variable

follows the Student’s t-distribution with (n - 1) degrees of freedom.

nS/

μXTn

1

x

31

Student’s t-Distribution

The t-distribution is a family of distributions.

The t-value depends on the degrees of freedom (df). Number of observations that are free to vary after

sample mean has been calculated

df = n – 1

32

Student’s t-Distribution

t0

t (df = 5)

t (df = 13)t-distributions are bell-shaped and symmetric, but have ‘fatter’ tails than the normal

Standard Normal(t with df = ∞)

Note: t Z as n increases(continued)

33

t distribution values

With comparison to the Z value

Confidence t t t ZLevel (df = 10) (df = 20) (df = 30) ____

.80 1.372 1.325 1.310 1.282

.90 1.812 1.725 1.697 1.645

.95 2.228 2.086 2.042 1.960

.99 3.169 2.845 2.750 2.576

Note: t Z as n increases

34

Assumptions Population is normally distributed.

If population is not normal, use “large” sample.

Use Student’s t-Distribution

100(1-α)% Confidence Interval for μ:

where t α/2,n-1 is the reliability factor from the t-distribution with n-1 degrees of freedom and an area of α/2 in each tail.

Confidence Interval for μ

n

stxμ

n

stx ,n-α/,n-α/ 1212

35

Affinity Credit Card

Before deciding to offer an affinity credit card to alumni of a university, the credit card company wants to know how large a balance those alumni will carry who accept the offer.

Population: (Future) credit card balances of (future) customers among the alumni of the university

Parameter of interest: Mean μ of (future) balances carried by alumni on their affinity credit card

36

SRS of Alumni

The 140 alumni who accepted the offer and received the affinity credit card have been carrying an aver-age monthly balance of = $1990.50 with a standard deviation of s = $2,833.33.

x

37

SRS of Alumni

Question: What should we conclude about the average future credit card balance μ on the new affinity credit card for this particular university?

Method: Construct confidence interval.

(continued)

38

Checklist for Application of Normal

SRS condition. The sample is a simple random sample from the relevant population.

Sample size condition (for mean). The sample size is larger than 10 times the squared skew-ness and 10 times the absolute value of the kurtosis.

39

Credit Card: Confidence Interval

The estimated standard error is

se ( ) = 2,833.33 / = 239.46.

The t-value for a 95% confidence interval with 139 degrees of freedom is

T.INV.2T(0.05,139) = 1.97718.

The 95% confidence interval is

1,990.50 ± 1.97718 × 239.46

= [1517.04, 2463.96].

X 140

40

Credit Card: Conclusion

We are 95% confident that the true but unknown µ lies between $1,517.04 and $2,463.96.

If the bank decides to launch the credit card, might the average balance be $1,250? It’s not impossible but based on the sample results it’s rather unlikely.

41

Confidence Interval and Confidence Level

If P(a ≤ p ≤ b) = 1 - then the interval from a to bis called a 100(1 - )% confidence interval of p.

The quantity (1 - ) is called the confidence levelof the interval ( between 0 and 1).

In repeated samples of the population, the true value of the parameter p would be contained in 100(1 - )% of intervals calculated this way.

42

p)pE( ˆ

Intervals and Level of Confidence

Confidence Intervals

Intervals extend from

to

100(1-)%of intervals constructed contain p;

100()% do not.

Sampling distribution of the proportion

p

2α/ 2α/α1

)ˆ(ˆ 2 psezp α/

)ˆ(ˆ 2 psezp α/

pp

43

Confidence Level, (1-)

Suppose confidence level = 95%

Also written (1 - ) = 0.95

A relative frequency interpretation: From repeated samples, 95% of all the

confidence intervals that can be constructed will contain the unknown true parameter.

44

Common Confusions:Wrong Interpretations

95% of all customers keep a balance of $1,517 to $2,464. The CI gives a range for the population mean µ, not

the balance of individual customers.

The mean balance of 95% of samples of 140 accounts will fall between $1,517 and $2,464. The CI provides a range for µ, not the means of other

samples.

45

Common Confusions:Wrong Interpretations

The mean balance is between $1,517 and $2,464. The average balance in the population may not fall

within the CI. The confidence level of the interval is 95%. It may not contain µ.

(continued)

46

Correct Interpretation

We are 95% confident that the mean monthly credit card balance for the population of customers who accept an application lies between $1,517 and $2,464.

The phrase “95% confident” is our way of saying that we are using a procedure that produces an interval containing the unknown mean in 95% of samples.

47

Transforming Confidence Intervals

Obtaining Ranges for Related Quantities

If [L,U] is a 100(1 – α)% confidence interval for µ, then [c×L,c×U] is a 100 (1 – α)% confidence interval for c×µ and [c+L,c+U] is a 100(1 – α)% confidence interval for c+µ.

48

Application: Property Taxes

Motivation

A mayor is considering a tax on business that is proportional to the amount spent to lease property in her city. How much revenue would a 1% tax generate?

49

Property Taxes

Method

Need a confidence interval for µ (average cost of a lease) to obtain a confidence interval for the amount raised by the tax. Check conditions (SRS and sample size) before proceeding.

50

Property Taxes

Mechanics

(continued)

Univariate statisticsTotal Lease Cost

mean 478,603.48standard deviation 535,342.56standard error of the mean 35,849.19

minimum 20,409.00median 290,559.00maximum 2,820,213.00range 2,799,804.00

skewness 1.953kurtosis 4.138

number of observations 223

t-statistic for computing95%-confidence intervals 1.9707

51

Property Taxes

Mechanics

95% confidence interval for average lease cost

478603 ± 1.9707 × 35849

= [407955, 549252]

95% confidence interval for average tax revenue per business

0.01 × [407955, 549252]

= [4079.55, 5492.52]

(continued)

52

Conclusion

Message

We are 95% confident that the average cost of a lease is between $407,955 and $549,252. The 95% confidence interval for tax raised per business is therefore [$4079, $5493]. Since the number of businesses leased in the city is 4,500, we are 95% confident that the amount raised will be between $18,358,000 and $24,716,000.

53

Best Practices

Be sure that the data are an SRS from the population.

Stick to 95% confidence intervals.

Round the endpoints of intervals when presenting the results.

Use full precision for intermediate calculations.

54

Pitfalls

Do not claim that a 95% confidence interval holds µ.

Do not use a confidence interval to describe other samples.

Do not manipulate the sampling to obtain a particular confidence interval.

3 – Hypothesis Tests

Managerial Statistics

KH 19

Course material adapted from Chapter 16 of our textbookStatistics for Business, 2e © 2013 Pearson Education, Inc.

2

Learning Objectives

Formulate null and alternative hypotheses for applications involving

a single population proportion

a single population mean

Execute the four steps of a hypothesis test

Know how to use and interpret p-values

Know what Type I and Type II errors are

3

Motivating Example

An office manager is evaluating software to filter SPAM e-mails (cost $15,000). To make it profitable, the software must reduce SPAM to less than 20%. Should the manager buy the software?

The manager wants to test the software.

4

Motivating Example

To demonstrate how well the software works, the software vendor applied its filtering system to email arriving at the office. After passing through the filter, a sample of 100 messages contained only 11% spam (and no valid messages were removed).

(continued)

5

Motivating Example

Question: Okay, 11% is better than 20%. But does that mean the manager should buy this software?

Method: Use a Hypothesis Test to answer this question.

Idea: Use the sample result, , to decide whether the software will be profitable, p < 0.2.

(continued)

110ˆ .p

6

What is a Hypothesis?

A hypothesis is a claim about the value of an unknown parameter:

population proportion

population mean

Example: The proportion of spam will be below 20%, that is, p < 0.2.

Example: The average monthly rent for all rent-al properties exceeds $500, that is, μ > 500.

7

The Null Hypothesis, H0

The Null Hypothesis, H0, states the claim to be tested; specifies a default course of action; preserves the status quo. Example: The proportion of spam that slips past the

filter is at least 20% (H0: p ≥ 0.2).

H0 is always about a population parameter, not about a sample statistic.

H0 : p ≥ 0.20 H0 : ≥ 0.20p

8

The Null Hypothesis, H0

We begin with the assumption that the null hypothesis is true.

Similar idea to the notion of innocent untilproven guilty

Always contains “=” , “≤”, or “” sign

May or may not be rejected

(continued)

9

The Alternative Hypothesis, Ha

The Alternative Hypothesis, Ha (H1), is the opposite of the null hypothesis. Example: The proportion of spam that slips past

the filter is less than 20% (Ha: p < 0.2).

Ha never contains the “=” , “≤”, or “” sign.

Ha may or may not be supported.

Ha is generally the hypothesis that the decision maker is trying to support.

10

Spam Filter: Hypotheses

Step 1 of a hypothesis test:

Define the hypotheses H0 and Ha.

H0: p ≥ p0 = 0.20

Ha: p < p0 = 0.20

11

Two Possible Options

We may decide to reject H0 (accept Ha).

Alternatively, we may decide not to reject H0 (we do not accept Ha).

There is no third option.

12

Sampling Distribution of p

p = 0.2If H0 is true

If it is unlikely that we would get a sample proportion of this value ...

... then we reject the null hypothesis that p ≥ 0.2.

Reason for Rejecting H0

0.11

... if in fact this were the population proportion…

X

13

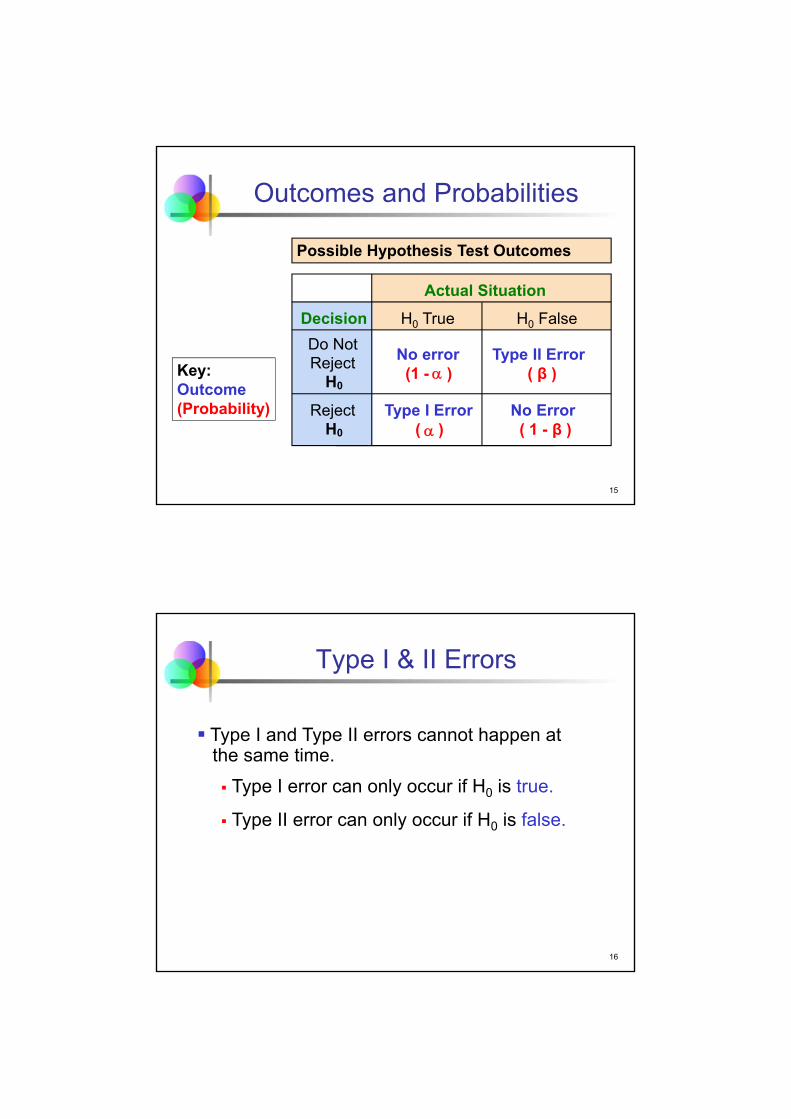

Errors in Decision-Making

Type I Error

Reject a true null hypothesis Example: Buy software that will not reduce spam to

below 20% of incoming emails.

Considered a serious type of error

Threshold probability of Type I Error is Called level of significance or simply -

level of the test

Set in advance by decision maker

14

Errors in Making Decisions

Type II Error

Fail to reject a false null hypothesis Example: Do not buy software that would have reduced

spam to below 20% of incoming emails.

The probability of Type II Error is β. 1-β is also called the power of a test.

(continued)

15

Outcomes and Probabilities

Actual Situation

Decision

Do NotReject

H0

No error(1 - )

Type II Error( β )

RejectH0

Type I Error( )

Possible Hypothesis Test Outcomes

H0 FalseH0 True

Key:Outcome(Probability) No Error

( 1 - β )

16

Type I & II Errors

Type I and Type II errors cannot happen atthe same time.

Type I error can only occur if H0 is true.

Type II error can only occur if H0 is false.

17

Evaluation of Hypotheses

Sample proportion < 0.2. Is this

relationship sufficient to reject the null

hypothesis?

No! The claim is about the population

proportion p. Maybe we just have a lucky

(unlucky?) sample. That is, the test result

may be due to sampling error.

110ˆ .p

18

Evaluation of Hypotheses

Hypothesis tests rely on the sampling distribution of the statistic that estimates the parameter specified in the null and the alternative.

Key question: What is the chance of getting a sample that differs from H0 by as much as (or even more than) this one if H0 is true?

(continued)

19

Spam Filter

A sample of size n = 100 delivered a sample proportion of .

Question: Assuming H0: p ≥ 0.20 is true, how likely is this deviation of 0.09 (or more)?

Assuming H0 is true, the sampling distribution of is approximately normal with mean p = 0.20 and SE( ) = 0.04 (note that the hypothe-sized “boundary” value p0 = 0.20 is used to calculate SE).

110ˆ .p

pp

20

Spam Filter

What is the chance of finding a sample proportion of or even smaller?

(continued)

110ˆ .p

21

Test Statistic

Step 2 of a hypothesis test:

Calculate the test statistic.

252

1002001200200110

1ˆ

00

0

.

)/.(.

..

)/np(p

ppz

22

Meaning of Test Statistic

The test statistic measures the difference between the sample outcome and the boundary value of the null hypothesis in multiples of the standard error.

Spam filter example: The sample proportion lies 2.25 standard errors of the proportion below the boundary value in the null hypothesis.

Since the sample distribution is assumed to be normal, the test statistic for proportions is also called z-statistic.

23

From Test Statistic to Probability

Since the sampling distribution of the sample proportion is (approximately) normal, we can calculate the probability of a sample outcome of at least 2.25 standard errors below the mean.

This probability is the famous p-value.

24

p-value

Step 3 of a hypothesis test:

Calculate the p-value.

p = NORM.S.DIST(-2.25,1) ≈ 0.012

p = NORM.DIST(0.11,0.2,0.04,1) ≈ 0.012

25

Calculating the p-value

)ˆ(ˆ 0

pSE

ppz

0-2.25

Under the null hypothesis (H0: p ≥ 0.2), our sample proportion is at least 2.25 standard errors below the population proportion. The probability of such a sample outcome is 1.2% (p-value).

p-value =

NORMSDIST(-2.25) = 0.012

26

Type I Error and p-value

Question: Suppose we decide to reject H0. What is the probability of a Type I error?

Answer: The p-value is the (maximal) chance of a Type I error if H0 is rejected based on the observed test statistic.

27

Level of Significance

Common practice is to reject H0 only if the p-value is less than a preset threshold.

This threshold that sets the maximum tolerance for a Type I error is called level of significance or α-level.

Statistically significant difference from the null hypothesis: Data contradicts H0 and leads us to reject H0 since p-value < α.

28

Decision

Step 4 of a hypothesis test:

Compare p-value to α and make a decision.

p-value = 0.012 < 0.05 = α

We reject H0 and accept the alternative hypothesis Ha. The spam software reduces the proportion of spam e-mails to less than 20%. The office manager should buy the software.

29

Summary

30

Take Aways I

The Four Steps of a Hypothesis Test:

1. Define H0 and Ha.

2. Calculate the test statistic.

3. Calculate the p-value.

4. Compare the p-value to the significance

level α. Make a decision. Accept Ha if p-

value < α.

31

Take Aways II

Hypothesis Testing: The Idea

We always try to prove the alternative hypo-thesis, Ha.

We then assume that its opposite (the null hypothesis) is true.

H0 and Ha must be totally exhaustive & mutually exclusive.

We can never possibly prove H0!

32

Take Aways III

We ask the question: how likely is to obtain our evidence, given that the null hypothesis is (supposedly) true?

This probability is called the p-value.

Not likely (small p) we have statistically “proven” the alternative hypothesis, so we reject the null.

Likely (not small p) we cannot reject the null.

33

Application: Burger King Ads

Motivation

The Burger King ad featuring Coq Roq won critical acclaim (and resulted in much controversy as well as several lawsuits). In a sample of 2,500 homes, MediaCheck found that only 6% saw the ad. An ad must be viewed by 5% or more of households to be effective. Based on these sample results, should the local sponsor run this ad?

34

Burger King Ads

Method

Perform a hypothesis test.

Set up the null and alternative hypotheses.H0: p ≤ 0.05Ha: p > 0.05

Use α = 0.05. Note that p is the population proportion who watches this ad. (Both SRS and sample size conditions are met.)

35

Burger King Ads

Mechanics

Perform the necessary calculations for an evaluation of the null hypothesis.

NORM.S.DIST(2.294,1) = 0.9891

p-value = 1 – 0.9891 = 0.0109 < 0.05 = α

Reject H0.

(continued)

294.2500,2/)05.01(05.0

05.006.0

z

36

Conclusion

Message

The hypothesis test shows a statistically significant result. We can conclude that more than 5% of households watch this ad. The Burger King Coq Roq ad is cost effective and should be run.

37

Hypothesis Test of a Mean

Hypothesis tests of the mean are similar to tests of proportions.

H0 and Ha are claims about the unknown population mean μ. For example,

H0: µ ≤ µ0 and Ha: µ > µ0 .

The test statistic uses the random variable , the sample mean.

Unlike in the test of proportions, the standard error is not specified since σ is unknown.

X

38

Hypothesis Test of a Mean

Just as in the calculation of a CI we estimate the unknown population standard deviation σwith the known sample standard deviation s.

The resulting test statistic is

(continued)

n

σ)XSE(

n

s)Xse(

ns

xt

/0

39

Hypothesis Test of a Mean

In a hypothesis test of a mean the test statistic is called a t-statistic since the appropriate sampling distribution is the t-distribution.

Specifically, the distribution of the t-statistic in a hypothesis test of a mean is the t-distribution with n-1 degrees of freedom.

We use this distribution to calculate the p-value.

(continued)

40

Denver Rental Properties

A firm is considering expanding into the Denver area. In order to cover costs, the firm needs rents in this area to average more than $500 per month. Are Denver rents high enough to justify the expansion?

41

Univariate Statistics

The firm obtained rents for a sample of size n = 45; the average rent was $647.33 with a sample std. dev. s = $298.77.

Univariate statisticsRent ($/Month)

mean 647.3333333standard deviation 298.7656424standard error of the mean 44.53735239

minimum 140median 610maximum 1600range 1460

skewness 0.617kurtosis 0.992

number of observations 45

t-statistic for computing95%-confidence intervals 2.0154

42

Hypotheses H0 and Ha

Let µ = mean monthly rent for all rental properties in the Denver area.

Step 1: Set up the hypotheses.

H0: µ ≤ µ0 = 500

Ha: µ > µ0 = 500

43

Test Statistic

Step 2: Compute the test statistic.

The average rent in the sample is 3.308 standard errors of the mean above the boundary value in the null hypothesis.

308.344.5374

50033.647/

0

ns

xt

44

p-value

Step 3: Calculate the p-value.

T.DIST.RT(3.308,44) = 0.0009394

The p-value is 0.09394% and thus below 0.1%.

45

Make a Decision

Step 4: Compare the p-value to α and make a decision.

p-value = 0.0009394 < 0.05 = α

We reject H0 and accept Ha. We conclude that the average rent in the Denver area exceeds the break-even value.

46

Summary: Tests of a Mean

47

Checklist

SRS condition: the sample is a simple random sample from the relevant population.

Sample size condition. Unless the population is normally distributed, a normal model can be used to approximate the sampling distribution of if the sample size n is larger than 10 times both the squared skewness and the absolute value of the kurtosis.

48

Application: Returns on IBM Stock

Motivation

Does stock in IBM return more, on average, than T-Bills? From 1980 through 2005, T-Bills returned 0.5% each month.

49

Returns on IBM Stock

Method

Let µ = mean of all future monthly returns for IBM stock. Set up the hypotheses as follows (Step 1):

H0: µ ≤ 0.005

Ha: µ > 0.005

The sample consists of monthly returns on IBM for 312 months (January 1980 – December 2005).

50

Returns on IBM Stock

The sample yields

= 0.01063

s = 0.08053

(continued)

x

Univariate statisticsIBM Return

mean 0.01063365standard deviation 0.08053206standard error of the mean 0.00455923

minimum -0.2619median 0.0065maximum 0.3538range 0.6157

skewness 0.303kurtosis 1.624

number of observations 312

t-statistic for computing95%-confidence intervals 1.9676

51

Returns on IBM Stock

MechanicsStep 2: Calculation of test statistic.

Step 3: Calculation of p-value.

T.DIST(1.236,311,1) ≈ 0.1088

Step 4: Compare p-value to α = 0.05.

p-value = 0.1088 > 0.05 = α. Do NOT reject H0.

(continued)

23610045590

0050010600 ..

..

ns/

μxt

52

Conclusion

Message

According to monthly IBM returns from 1980 through 2005, the IBM stock does not generate statistically significantly higher earnings than comparable investments in US Treasury Bills.

53

Failure to Reject H0

Our failure to reject H0 and to prove Ha does not mean the null is true. We did not prove the null hypothesis.

Our sample evidence is just too weak to prove Ha at a 5% or even 10% significance level. If we had rejected H0, then the chance of making a Type I error (p-value of about 11%) would have been too high for the given level of significance.

If the α-level had been 15% then we could have proven Ha.

54

Significance vs. Importance

Statistical significance does not mean that you have made a practically important or meaning-ful discovery.

The size of the sample affects the p-value of a test. With enough data, a trivial difference from H0 leads to a statistically significant outcome. Such a trivial difference may be practically un-important.

55

Confidence Interval vs. Test

Confidence intervals make positive statements about the population. A confidence interval provides a range of parameter

values that are compatible with the observed data.

Hypothesis tests provide negative statements. A test provides a precise analysis of specific

hypothesized values for a parameter.

A test attempts to reject a specific hypothesis for a parameter.

56

Two-tailed Hypothesis Test

Hypotheses in a Two-tailed Hypothesis Test are of the following form:

mean: H0: µ = 0.005 Ha: µ ≠ 0.005

proportion: H0: p = 0.2 Ha: p ≠ 0.2

The calculation of the test statistic is identical to the calculation in a One-tailed Hypothesis Test.

57

Two-Tailed Hypothesis Test

By convention, the p-value in a two-tailed test is defined as two times the p-value of the corresponding one-tailed test.

As a consequence, the two-tailed p-value does not have the intuitive interpretation along the lines

“The probability of the sample result assuming the null is true”.

This convention leads to a paradox.

(continued)

58

One-tailed Test on IBM Returns

Step 1: H0: µ ≤ 0.005 Ha: µ > 0.005

Step 2: Calculation of test statistic.

Step 3: Calculation of p-value.

T.DIST(1.236,311,1) ≈ 0.1088

Step 4: Compare p-value to α = 0.15.

p-value = 0. 1088 < 0.15 = α.

Reject H0.

236.10.004559

005.00106.0/

0

ns

xt

59

Two-tailed Test on IBM Returns

Step 1: H0: µ = 0.005 Ha: µ ≠ 0.005

Step 2: Calculation of test statistic.

Step 3: Calculation of p-value.

T.DIST(1.236,311,2) ≈ 0.2175

Step 4: Compare p-value to α = 0.15.

p-value = 0. 2175 > 0.15 = α.

Do NOT reject H0.

236.10.004559

005.00106.0/

0

ns

xt

60

Paradox

According to the one-tailed hypothesis test we can prove that µ > 0.005. But according to the two-tailed test we cannot prove that µ ≠ 0.005.

That’s the paradox!

The reason for the convention leading to the paradox is to obtain a sensible relation between two-tailed hypothesis tests and confidence intervals.

61

Two-tailed Tests and Confidence Interval

The hypothesis Ha: µ ≠ 0.005 can be proved at the significance level α if and only if the (1- α)*100% confidence interval does not include 0.005.

62

Summary

Discussed hypothesis testing methodology

Introduced four-step process of hypothesis testing

Defined p-value

Performed z-test for the proportion

Performed t-test for the mean

Discussed two-tailed hypothesis test

63

Best Practices

Be sure that the data are an SRS from the population.

Pick the hypotheses before looking at the data.

Pick the α-level before you compute the test statistic and the p-value.

Think about whether α = 0.05 is appropriate for each test.

Report a p-value to summarize the outcome of a test.

64

Pitfalls

Do not confuse statistical significance with substantive importance.

Do not think that the p-value is the probability that the null hypothesis is true.

Avoid cluttering a test summary with jargon.

4 – Simple Linear Regression

Managerial Statistics

KH 19

Course material adapted from Chapter 19 of our textbookStatistics for Business, 2e © 2013 Pearson Education, Inc.

2

Learning Objectives

Calculate and interpret the simple linear regression equation for a set of data

Describe the meaning of the coefficients of the regression equation in the context of business applications

Examine and interpret the scatterplot and the residual plot as they relate to a regression

Understand the meaning (and limitation) of the R-squared statistic

3

Diamond Prices

Motivation: What is the relationship between the price and weight of diamonds?

Method: Using a sample of 320 emerald-cut diamonds of various weights, regression analysis produces an equation that relates price to weight.

Mechanics: Let y denote the response (“dependent”) variable (price) and let x denote the explanatory (“independent”) variable (weight).

4

Scatterplot of Price vs. Weight

$0.00

$200.00

$400.00

$600.00

$800.00

$1'000.00

$1'200.00

$1'400.00

$1'600.00

$1'800.00

$2'000.00

0.3 0.35 0.4 0.45 0.5 0.55

Pri

ce (

$)

Weight (carats)

Scatterplot

5

Linear Equation

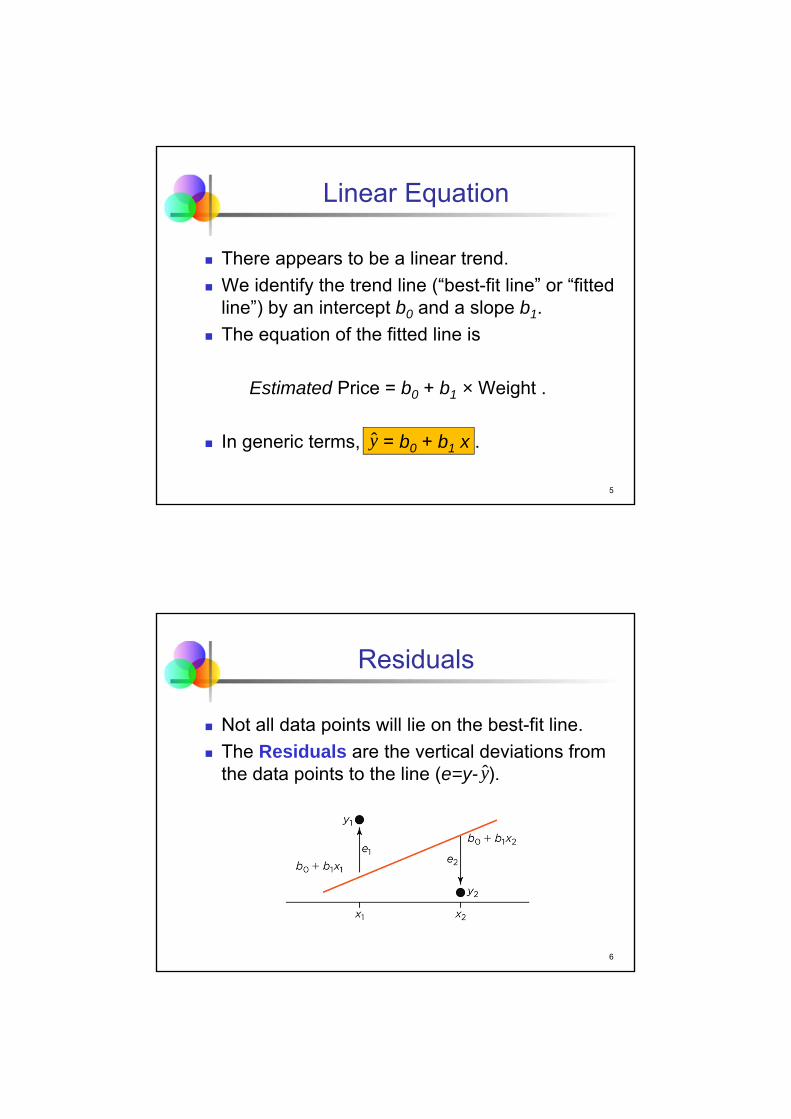

There appears to be a linear trend.

We identify the trend line (“best-fit line” or “fitted line”) by an intercept b0 and a slope b1.

The equation of the fitted line is

Estimated Price = b0 + b1 × Weight .

In generic terms, = b0 + b1 x . y

6

Residuals

Not all data points will lie on the best-fit line.

The Residuals are the vertical deviations from the data points to the line (e=y- ).y

7

Method of Least Squares

The Method of Least Squares determines the best-fit line by minimizing the sum of squared residuals.

The method uses differential calculus to obtain the values of the coefficients b0 and b1 that minimize the sum of squared residuals, also called the sum of squared errors, SSE.

8

Minimizing SSE

Let the index i indicate the ith data point, (xi,yi).

210

2

2

min

ˆmin

min SSEmin

)]xb(b[y

)y(y

e

ii

ii

i

9

Least Square Regression

The method of least squares generates the following coefficient values:

X

Yn

ii

n

iii

s

sr

)x(x

)y)(yx(xb

1

2

11

xbyb 10

10

Diamonds: Fitted Line

The least squares regression equation relating diamond prices to weight is

Estimated Price =

43.5 + 2670 Weight

Regression: Price ($)constant Weight (carats)

coefficient 43.48910163 2669.745803std error of coef 71.90155144 172.4731816t-ratio 0.6048 15.4792p-value 54.5715% 0.0000%beta-weight 0.6555

standard error of regression 170.2149256R-squared 42.97%adjusted R-squared 42.79%

number of observations 320residual degrees of freedom 318

t-statistic for computing95%-confidence intervals 1.9675

11

Using the Fitted Line

The average price of a diamond that weighs 0.4 carat is

Estimated Price = 43.49 + 2669.75 × 0.4

≈ 1111.39,

that is, the estimated price is (about) $1,111.

A diamond that weighs 0.5 carat costs (about) $267 more, on average.

12

Illustration

13

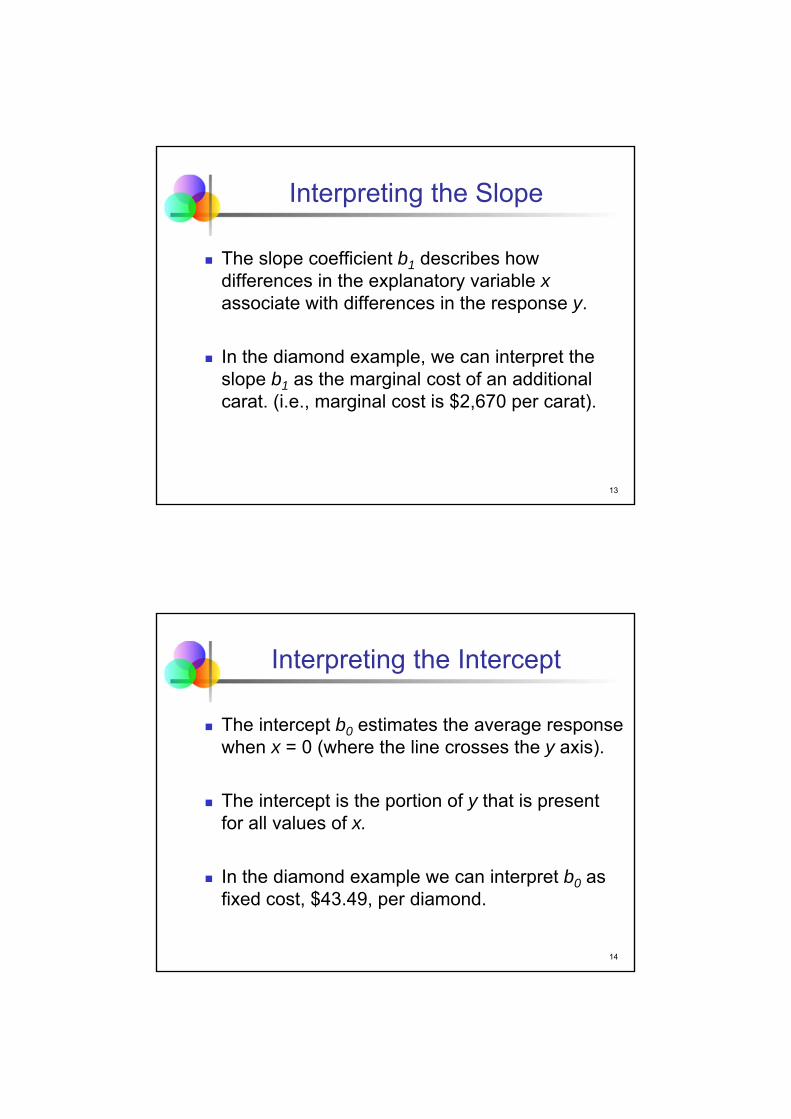

Interpreting the Slope

The slope coefficient b1 describes how differences in the explanatory variable xassociate with differences in the response y.

In the diamond example, we can interpret the slope b1 as the marginal cost of an additional carat. (i.e., marginal cost is $2,670 per carat).

14

Interpreting the Intercept

The intercept b0 estimates the average response when x = 0 (where the line crosses the y axis).

The intercept is the portion of y that is present for all values of x.

In the diamond example we can interpret b0 as fixed cost, $43.49, per diamond.

15

Interpreting the Intercept

In many applications, the intercept coefficient does not have a useful interpretation.

Unless the range of x values includes zero, the value for b0 is the result of an extrapolation.

(continued)

16

Residual Plot

A Residual Plot shows the variation that remains in the data after accounting for the linear relationship defined by the fitted line. Put differently, the plot shows the variation of the data points around the fitted line.

The residuals should be plotted against the predicted values of y (or against x) to check for patterns.

17

Residual Plot

If the least squares line captures the association between x and y, then a plot of residuals should stretch out horizontally with consistent vertical scatter. No particular pattern should be visible.

Our task is to visually check for the absence of a pattern.

(continued)

18

Residuals vs. Predicted Values

-600

-400

-200

0

200

400

600

800 900 1000 1100 1200 1300 1400 1500

resi

du

als

predicted values of Price ($)

Residual Plot

19

Variation of Residuals

The standard deviation of the residuals measures how much the residuals vary around the fitted line.

This standard deviation is called the Standard Error of Regression or the Root Mean Squared Error (RMSE).

22

222

21

n

eee)SSE/(ns n

e

20

Diamonds

For the diamond example, se=170.21.

The standard error of regression is $170.21.

Regression: Price ($)constant Weight (carats)

coefficient 43.48910163 2669.745803std error of coef 71.90155144 172.4731816t-ratio 0.6048 15.4792p-value 54.5715% 0.0000%beta-weight 0.6555

standard error of regression 170.2149256R-squared 42.97%adjusted R-squared 42.79%

number of observations 320residual degrees of freedom 318

t-statistic for computing95%-confidence intervals 1.9675

21

Measures of Variation

xi

y

X

SST = (yi - y)2

SSE = (yi - yi )2

SSR = (yi - y)2 _

_

y

y

__y

Yyi

22

Measures of Variation

SST = total sum of squares

Variation of the yi values around their mean,

SSR = regression sum of squares

Explained variation attributable to the linear relationship between x and y

SSE = error sum of squares (sum of squared errors)

Variation attributable to factors other than the linear relationship between x and y

y

(continued)

23

Measures of Variation

Total variation is made up of two parts:

SSE SSR SST Total Sum of Squares

Regression Sum of Squares

Error Sum of Squares

2i )y(ySST 2

ii )y(ySSE ˆ 2i )yy(SSR ˆ

where:

= Average value of the dependent variable

yi = Observed values of the dependent variable

i = Predicted value of y for the given xi valuey

y

(continued)

24

The Coefficient of Determination is the portion of the total variation in the dependent variable that is explained by variation in the independent variable.

The coefficient of determination is also called R-squared and is denoted by r2 or R2.

Coefficient of Determination, R2

10 2 Rnote:

squares of sum total squares of sum regression

SSTSSR2 R

25

r2 = 1

Examples of R-squared Values

Y

X

Y

X

r2 = 1

r2 = 1

Perfect linear relationship between X and Y:

100% of the variation in Y is explained by variation in X.

26

Examples of R-squared Values

Y

X

Y

X

0 < r2 < 1

Weaker linear relationships between X and Y:

Some but not all of the variation in Y is explained by variation in X.

(continued)

27

Examples of R-squared Values

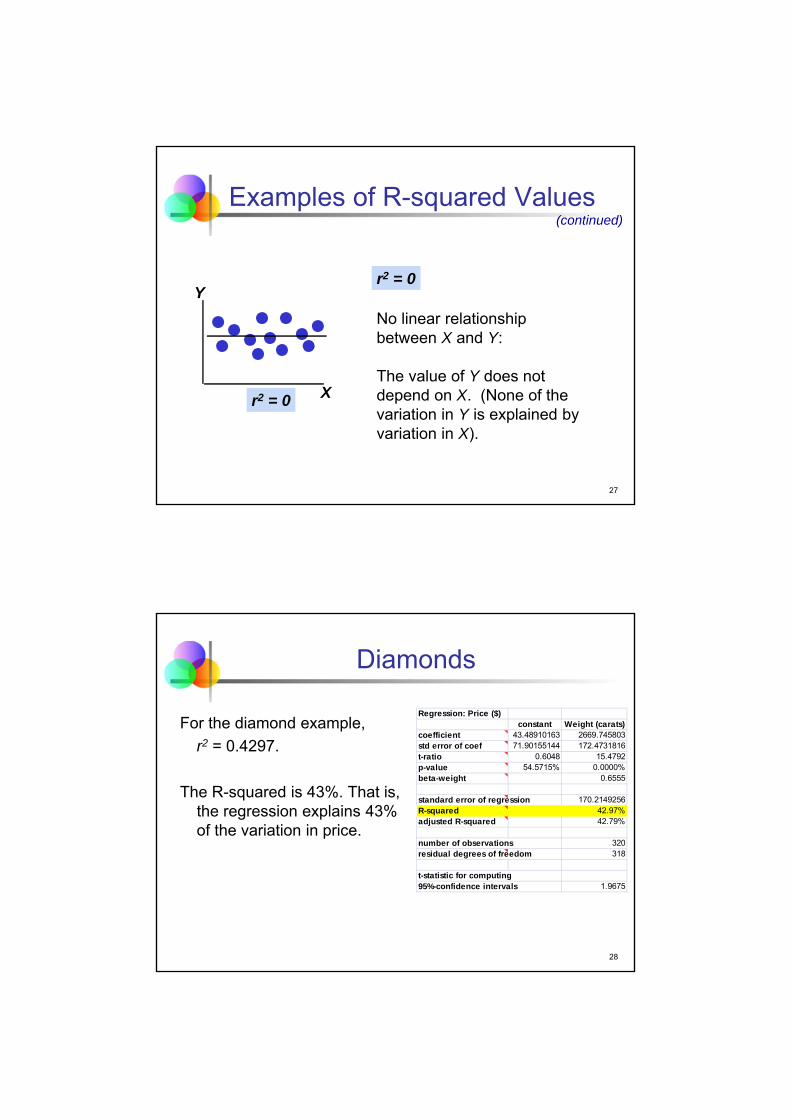

r2 = 0

No linear relationship between X and Y:

The value of Y does not depend on X. (None of the variation in Y is explained by variation in X).

Y

Xr2 = 0

(continued)

28

Diamonds

For the diamond example,

r2 = 0.4297.

The R-squared is 43%. That is, the regression explains 43% of the variation in price.

Regression: Price ($)constant Weight (carats)

coefficient 43.48910163 2669.745803std error of coef 71.90155144 172.4731816t-ratio 0.6048 15.4792p-value 54.5715% 0.0000%beta-weight 0.6555

standard error of regression 170.2149256R-squared 42.97%adjusted R-squared 42.79%

number of observations 320residual degrees of freedom 318

t-statistic for computing95%-confidence intervals 1.9675

29

Checklist for Simple Regression

Linear: Examine the scatterplot to see if pattern resembles a straight line.

Random residual variation: Examine the residual plot to make sure no pattern exists.

(No obvious lurking variable: Think about whether other explanatory variables may better explain the linear association

between x and y.)

30

Application: Lease Costs

Motivation

How can a dealer anticipate the effect of age on the value of a used car? The dealer estimates that $4,000 is enough to cover the depreciation per year.

31

Lease Costs

Method

Use regression analysis to find the equation that relates y (resale value in dollars) to x (age of the car in years). The car dealer has data on the prices and age of 218 used BMWs in the Philadelphia area.

32

Lease Costs

Mechanics

(Think about lurking variables)

Check scatterplot

Run regression

Check residual plot

(continued)

33

Lease Costs: Scatterplot

$10'000.00

$15'000.00

$20'000.00

$25'000.00

$30'000.00

$35'000.00

$40'000.00

$45'000.00

$50'000.00

0 1 2 3 4 5 6

Pri

ce

Age

Regression Equation: Price = 39851.7199 - 2905.5284 Age

Scatterplot

34

Lease Costs: Regression

MechanicsRegression: Price

constant Agecoefficient 39851.7199 -2905.5284std error of coef 758.460867 219.3264t-ratio 52.5429 -13.2475p-value 0.0000% 0.0000%beta-weight -0.6695

standard error of regression 3366.63713R-squared 44.83%adjusted R-squared 44.57%

number of observations 218residual degrees of freedom 216

t-statistic for computing95%-confidence intervals 1.9710

35

Lease Costs: Residual Plot

-10000

-5000

0

5000

10000

15000

20000 25000 30000 35000 40000 45000

resi

du

als

predicted values of Price

Residual Plot

36

Lease Costs: Regression

Mechanics

The linear regression equation is

Estimated Price = 39,851.72 – 2,905.53 Age

The R-squared is 0.4483, the standard error of regression is se = $3366.64.

37

Conclusion

Message

The results indicate that used BMWs decline in resale value by $2,900 per year. The current lease price of $4,000 per year appears profitable. However, the fitted line leaves more than half of the variation unexplained.

Leases longer than 5 years would require extrapolation.

38

Best Practices

Always look at the scatterplot.

Know the substantive context of the model.

Describe the intercept and slope using units of the data.

Limit predictions to the range of observed conditions.

39

Pitfalls

Do not assume that changing x causes changes in y.

Do not forget lurking variables.

Do not trust summaries like R-squared without looking at plots.

Do not call a regression with a high R-squared “good” or a regression with a low R-squared “bad”.

5 – Simple Regression Model

Managerial Statistics

KH 19

Course material adapted from Chapter 21 of our textbookStatistics for Business, 2e © 2013 Pearson Education, Inc.

2

Learning Objectives

Understand the framework of the simple linear regression model

Calculate and interpret confidence intervals for the regression coefficients

Perform hypothesis tests on the regression coefficients

Understand the difference between confidence and prediction intervals for the predicted value

3

Berkshire Hathaway

Motivation: How can we test the CAPM (Capital Asset Pricing Model) for Berkshire Hathaway stock?

Method: Formulate the simple regression with percentage excess return in Berkshire Hathaway stock as y and the percentage excess return in value of the whole stock market (“value-weighted stock market index) as x.

4

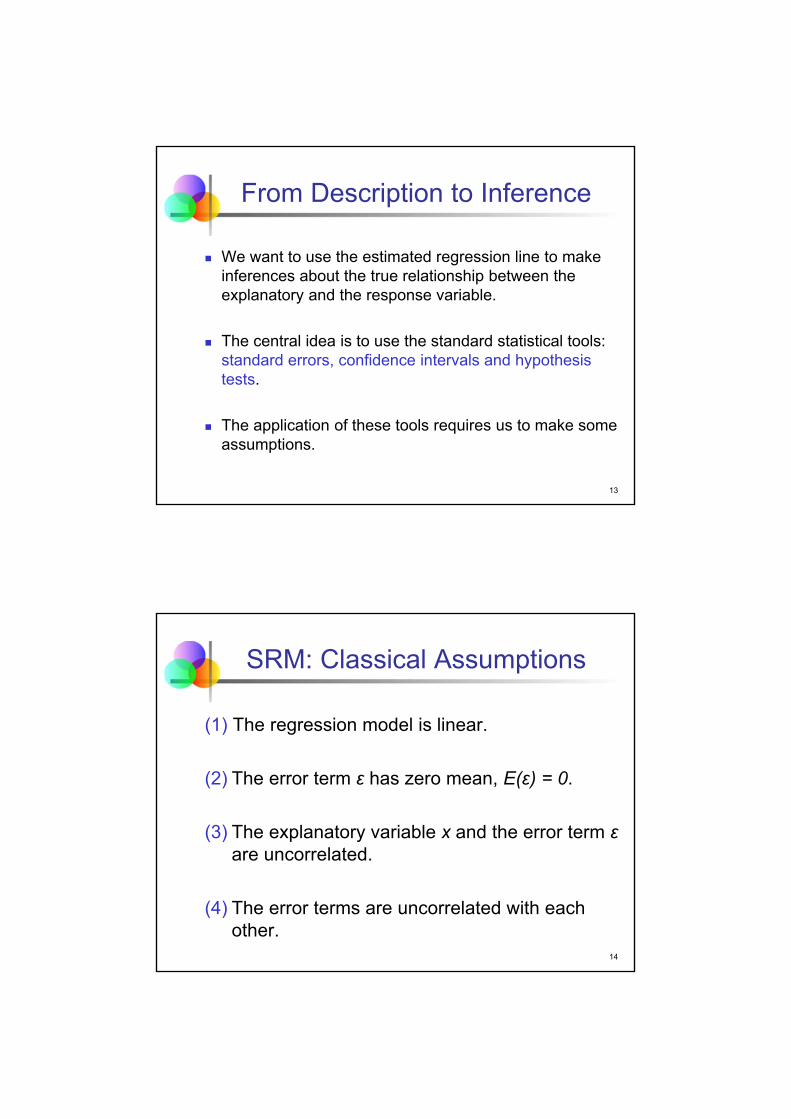

From Description to Inference

We do not only want to describe the historical relationship between x and y that is evident in the data. In addition, we now want to make inferences about the underlying population.

We have to think of our data as a sample from a population.

5

From Description to Inference

Naturally, the question arises, what conclusions can we derive from the sample about the population?

The central idea is to use inference related to regression: standard errors, confidence intervals and hypothesis tests.

(continued)

6

Model of the Population

The Simple Linear Regression Model (SRM) is a model for the association in the population between an explanatory variable x and a response variable y.

The SRM equation describes how the (conditional) mean of y depends on x.

The SRM assumes that these means lie on a straight line with intercept β0 and slope β1:

xxXYExy 10)(

7

Model of the Population

The response variable y is a random variable. The actual values vary around the mean. The deviations of responses around their (conditional) mean are called errors,

Errors ε can be positive or negative. They have zero mean, that is, the average deviation from the line is zero.

(continued)

xyy

8

εxββy 10linear component

Simple Linear Regression Model

The population regression model:

population Y intercept

population slopecoefficient

random error term

dependent variable

independent variable

random errorcomponent

9

(continued)

random error for this xi value

Y

X

observed value of y for xi

average value of y for xi

iii εxββy 10

xi

slope = β1

intercept = β0

εi

Simple Linear Regression Model

10

Data Generating Process

The “true regression line” is a characteristic of the population, not the observed data.

The true line’s parameters β0 and β1 are (and will remain) unknown!

The SRM is a model and offers a simplified view of the population.

The observed data points are a simple random sample from the population.

The fitted line provides an estimate of the population regression line.

11

ii xbby 10ˆ