Kalyan's ...... [email protected] The Directive Principles laid down in the Constitution aim at...

182

www.OnlineIAS.com [email protected] www.OnlineIAS.com Indian Economy: www.OnlineIAS.com PLANNING IN INDIA WHAT IS PLANNING? Planning is a process which Involves taking stock of resources, formulation of objectives and priorities, fixation of specific targets, mobilization of resources. establishment of implementation machinery wherever necessary, achieving objectives, and evaluating the performance of planning. Concepts: Planning is distinguished on the basis of time: like short term planning, medium term planning and long-term planning. Physical Planning: Plans are outlined In terms of various physical output targets. Financial Planning: It is planning In terms of allocating the financial resources amongst the various investment avenues. Indicative planning involves influencing investment decisions through fiscal and monetary policies. Fixed Plan: In a fixed five year plan, we have a fixed five year perspective with the first annual plan forming the base for the entire plan period. Rolling Plan: In a five year rolling plan, every year there will be a five year perspective while introducing an annual plan. Kalyan's www.OnlineIAS.com Kalyan's www.OnlineIAS.com 1

Transcript of Kalyan's ...... [email protected] The Directive Principles laid down in the Constitution aim at...

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Indian Economy:

www.OnlineIAS.com

PLANNING IN INDIA

WHAT IS PLANNING?

Planning is a process which Involves taking stock of resources, formulation of

objectives and priorities, fixation of specific targets, mobilization of resources.

establishment of implementation machinery wherever necessary, achieving

objectives, and evaluating the performance of planning.

Concepts:

Planning is distinguished on the basis of time: like short term planning, medium

term planning and long-term planning.

Physical Planning:

Plans are outlined In terms of various physical output targets.

Financial Planning:

It is planning In terms of allocating the financial resources amongst the various

investment avenues. Indicative planning involves influencing investment

decisions through fiscal and monetary policies.

Fixed Plan:

In a fixed five year plan, we have a fixed five year perspective with the first annual

plan forming the base for the entire plan period.

Rolling Plan:

In a five year rolling plan, every year there will be a five year perspective while

introducing an annual plan.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 1

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Centralised Planning:

Refers to planning from above Here the plan perspective encompasses the

economy as a whole.

Decentralised Planning: Refers to planning from below.

How did planning as a system emerge?

Planning as an economic institution emerged due to the extreme inadequacies of

free enterprise policy with respect to optimal allocation of resources and

maximising social benefit.

Evolution of Indian Planning:

During the Great Depression (1930s) the whole world was caught in a phase of

declining income, output and employment, wilt) the exception of the USSR It

was this success exhibited by the planned economy of Soviet Union, that brought

planning concept to the forefront. India was greatly influenced by this planning

wave. The evolution of Indian planning is briefly outlined below:

1934 : Planned Economy for India, the first systematic work contemplating a

planned economy for India, was written by Visvesvraya.

1938 : Indian National Congress established the National Planning Committee.

However, its work was interrupted by the world war-II and the Quit India

Movement.

1943 : Bombay Plan was presented by a few Bombay industrialists which

emphasised on industrial development with high priority for basic industries like

steel and cement. -

1944 : The British Indian Government set up the Department of Planning and

Economic Development, headed by A.D. Dalal. Its aim was to restore economic

normalcy and also economic development.

1946 : The Planning Advisory Board was constituted to collect relevant matter

for planning In India, by the Interim Government.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 2

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

The Directive Principles laid down in the Constitution aim at creating a society

in which all have equal opportunity, right to work and where disparities In income

and wealth have been reduced to the minimum. To translate these ideas into

reality economic planning is a necessity. India suffered from low per capita

income, large population, inefficient production and inequality distribution. To

overcome these problems and to get maximum benefit of scarce resources,

planning was taken up.

Objectives of planning:

The objectives of planning differ from country to country. The major objectives

of planning In India have been

1. Achieving full employment

2. Maximising national per capita income

3. Rapid Industrialisation

4. Self sufficiency in food

5. Reduction of inequalities

1950 : The Planning Commission was established through a Cabinet resolution.

It is not a Constitutional body like the Finance Commission.

1952 : National Development council (NDC) was constituted on the advice of the

Planning Corn- mission through an executive order to serve as the highest

reviewing and advisory body On planning;

FORMATIVE PHASE: Draft Plans: Bombay Plan: A plan was formulated by a

few big industrialists who aimed at doubling per capita income in a period of

fifteen years. The Plan laid emphasis on strengthening the basic industries.

People’s Plan (M.N.Roy): The laid emphasis on agriculture and the consumer

goods industry.

Gandhlan Plan (SM. Agarwal) : The Plan Stressed decentralised economic

system. Agriculture and the allied activities were outlined for development

Mentioned only Draft

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 3

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Note: The above mentioned plans were only Draft plans and never implemented

Basic Features of Indian planning:

1. Comprehensive democratic planning

2. Mixed Economy: Coexistence of both the public sector and private sector. But

greater role of the public sector is a dominant feature

3. Balanced Growth Strategy Both the .agricultural and Industrial infrastructure

are to be strengthened.

4. Minimizing foreign assistance, both in terms of aid and transfer of technology

FIRST FIVE YEAR FLAN (1st April, 1951 - 31st March, 1956)

OBJECTIVES:

1. Rehabilitation of Indian economy affected by partition and Second World War,

2. Solving the food crisis,

3. Easing the raw material position particularly in jute and cotton,

4. Checking the inflationary tendencies,

5. Building economic overheads like roads, railways, irrigation and hydro-electric

works,

6. Building administrative organizations needed for carrying out the programmes

of development in India, and

7. Initiating balanced all round development.

OUTLAY:

Public Sector: Rs 1,960 Crores.

PRIORITIES:

Agriculture and allied sectors with 31% of outlay got the first priority,

Transport and communications with 27% outlay and Social Services with 23%

outlay got the second and third priorities respectively.

Industry, with a meagre 4% of the outlay, was neglected.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 4

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

PERFORMANCE:

Target

(% growth per

annum)

Achievement

National Income

Per Capita Income

Industrial Production

Agricultural Production

2.1

0.9

7.0

-

3.4

1.2

7.3

4.1

The first Five Year Plan was a grand success as the achievement exceeded the

targets.

- Production of food grains increased by and cotton by 45%.

- Irrigation facilities were provided to 16 million acres of land; over 6 million

acres were benefitted through major irrigation works and 10 million acres through

minor and medium irrigation.

- Shortages in the economy were eliminated.

- The pace level fell by 30% and food prices also declined.

• The Locomotive factory at Chittaranjan Fertilizer factory at Sindri, and I.T.I.

(Indian Telephone Industry) at Bangalore were established.

• Community Development Programme was launched on October 2nd 1952 to

bring about allround development of rural areas with special emphasis on

agriculture.

- Co-op greater attention to agriculture and neglected large scale industries.

Scant attention has been paid to social objectives.

SECOND FIVE YEAR PLAN (1st April, 1956 to 31st March, 1961)

Circumstances under which the plan was launched:

The Five Year Plan was launched In context at the success of the First Five Year

Plan

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 5

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

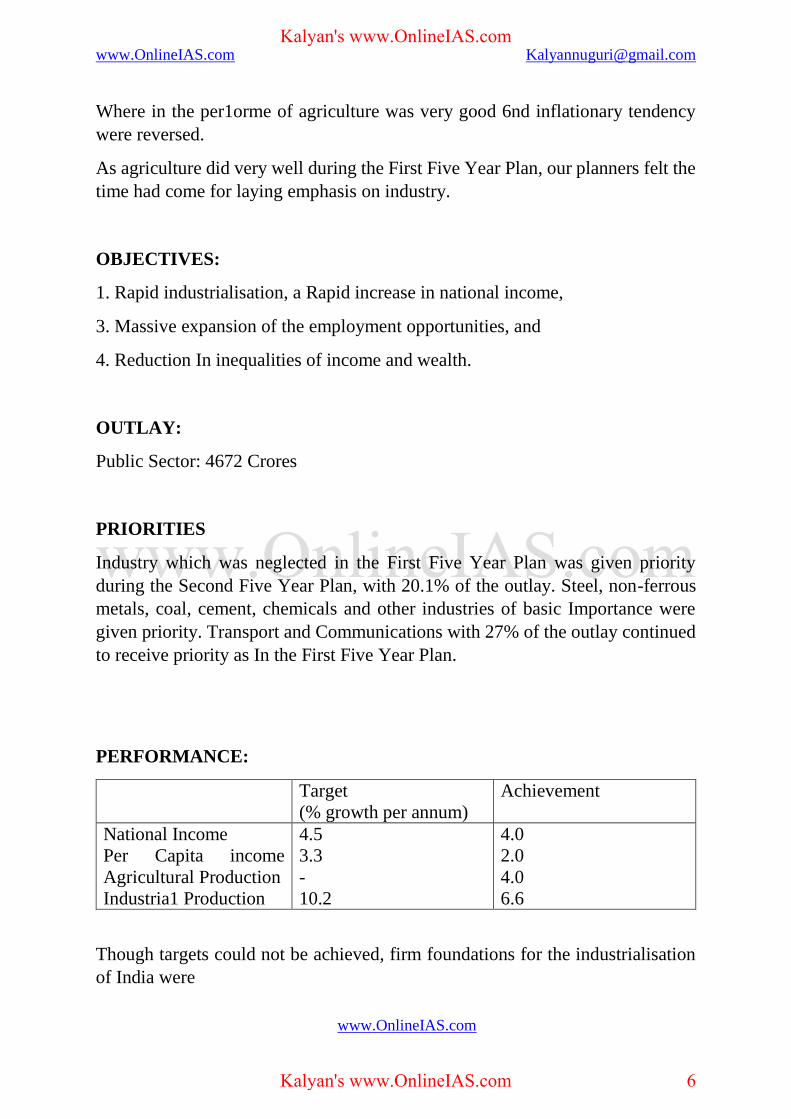

Where in the per1orme of agriculture was very good 6nd inflationary tendency

were reversed.

As agriculture did very well during the First Five Year Plan, our planners felt the

time had come for laying emphasis on industry.

OBJECTIVES:

1. Rapid industrialisation, a Rapid increase in national income,

3. Massive expansion of the employment opportunities, and

4. Reduction In inequalities of income and wealth.

OUTLAY:

Public Sector: 4672 Crores

PRIORITIES

Industry which was neglected in the First Five Year Plan was given priority

during the Second Five Year Plan, with 20.1% of the outlay. Steel, non-ferrous

metals, coal, cement, chemicals and other industries of basic Importance were

given priority. Transport and Communications with 27% of the outlay continued

to receive priority as In the First Five Year Plan.

PERFORMANCE:

Target

(% growth per annum)

Achievement

National Income

Per Capita income

Agricultural Production

Industria1 Production

4.5

3.3

-

10.2

4.0

2.0

4.0

6.6

Though targets could not be achieved, firm foundations for the industrialisation

of India were

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 6

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

laid with launching of the steel plants at Bhilai (M.P), Rourkela (Orissa), and

Durgapur (West Bengal), heavy engineering plant at Ranchi (Bihar) Lignite

Corporation at Neyveli (Tamil Nadu), and Integral Coach Factory at Perumbur

(Tamil Nadu).

Except in sugar and tea, targets could not be achieved in the production of food

grains, jute, and cotton and oil seeds. Unfavorable monsoons in 1957-58 and

1959-60, in addition to the slow progress in the programme of multiplication of

improved seeds, use of fertilizers and irrigation contributed to this fall in

agricultural production:

Prices of food grains increased all over the country. Prices of imported

machinery also went up. And this was further aggravated by the Suez Crisis as it

affected international supplies to India for a short period. As a result, prices Went

up further.

Foreign exchange balance dwindled from Rs. 700 Crores in 1955-56 to Rs. 100

Crores at the end of the Plan.

CRITICISM:

The Plan gave too much priority to heavy industries neglecting production of food

and consumer goods. This led to balance of payments problem and inflationary

pressures.

THIRD FIVE YEAR PLAN (1st April 1961 to 31st March 1966)

OBJECTIVES:

1. Self-sufficiency in food grains, and increase in agricultural production to meet

the requirements of industry and exports,

2. Expansion of basic industries like steel, chemical industries, fuel and power,

and establishment of machine building capacity

3. Substantial expansion in employment opportunities,

4. Increase in National income of over 5.6 per cent per annum, and

5. Creation of equality of opportunities, and reduction in disparities in income

and wealth.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 7

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

OUTLAY :

Public Sector :Rs. 8,577 Crores.

PRIORITIES:

Agriculture, Industry, Transport and Communication were given priority.

PERFORMANCE :

Performance of the Third Five Year Plan was very poor. Achievement was much

below the targets.

The performance in agriculture in particular was very bad. Prices of food and

other essential commodities rose. Causes for the poor performance of this plan

were: 1962 Chinese aggression, 1965 Indo- Pak war, and failure of monsoons,

particularly in 65-66. Except in 1964-65 in all other years of the plan monsoons

failed in some region or the other.

THREE ANNUAL PLANS

1st April 1966 to 31st March 1967

1st April 1967 to 31st March 1968

1st April 1968 to 31st March 1969

As the planning process got seriously affected because of wars and drought

during the 3rd Five Year Plan, Five Year Planning was given up till economic

Target

(Per annum)

Achievement

National income

Per Capita Income

Agricultural production

Industrial Production

5.6

3.2

6.0

10.7

2.2

0.2

-1.4

9.0

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 8

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

normalcy was restored. Instead, Annual Plans were launched for three years. This

period is also known as Plan Holiday.

During 1966-67, the economy did not do well because of drought. Performance

of both agriculture and industry was bad. Only 76 million tons of food was

produced, which was substantially lower than 89 rnillion tonnes of 1964-65 To

meet the shortage, 8.7 million tonne of food were imported.

The economy started recovering during 1967-68 and continued during 1968-69.

Food production

during 67-68 was good partly because of new agricultural strategy based on High

Yielding Seeds and partly because of good monsoons. This increased production

was maintained during 1968. 69. Prices of food grains started falling because of

improved supply position. Thu, economic stability was restored.

FOURTH FIVE YEAR PLAN (1st April, 1969 to 31st March, 1974)

OBJECTIVES:

1. Growth with stability in terms of prices,

2. Achievement of 5.5% Annual growth of national income,

3. Achievement of self-reliance by doing away with PL-48O, imports of food

grains and reducing foreign aid by about half by the end of 4th plan,

4. Achieving social justice and equality through greater creation of diffusion of

ownership of means of production1 and employment

5. Correcting imbalance in development among different States and regions in

the country.

OUTLAY:

Public Sector :. Rs. 15, 779 Crores

PRIORITIES:

Agriculture and allied sectors were given the highest priority by allocating 23.3%

of the outlay. The allocation to industry was only 18.2%. Trans. port and

Communications with 19.5% outlay was given relatively lesser percentage

compared to the earlier plans. Family Planning was given considerable

Importance with Rs. 278 Crores of allocation.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 9

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

PERFORMANCE:

The Fourth plan was also not a success as the achievements fell short of the targets

substantially.

Though high yielding seeds brought considerable Improvement in wheat

production, their success was marginal in the case of rice, jute, cotton, and pulses

continued to be problem areas.

Performance of the industrial sector was bad because of low output in steel,

metals and metal products, non-electrical machinery, textile, sugar etc. This was

mainly because of power shortage.

Summing up:

The Fourth Plan turned out to be a Plan with shortfalls all along:

10.8% Food

10% Oil seeds

15% Sugar

18% Cotton and Jute

16.7% Cement

8.2% Irrigation

17.3% Power

All these shortages indicate a poor performance Absence of general price

stability. Developments in Bangladesh and consequent Indo-Pak war in 1971 and

Target

(Per annum)

Achievement

National income

Per Capita Income

Agricultural production

Industrial Production

5.7

-

5.0

8.1

3.3

0.6

2.9

4.7

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 10

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

drought in 1972 virtually robbed the Fourth Plan of the boost that it was to give

to the economy

FIFTH FIVE YEAR PLAN (1st Apr11, 1974 - 31st March, 1979)

This Fifth Five Year plan was terminated one year

aheadofthescheduleOn3lstMarch,1978as the Janatha Party Government wanted

to introduce Rolling Plan in place of Five Year Plans.

The Fifth Year Plan under went many changes because of changes in the

leadership of the Planning Commission. An approach to the Fifth Plan was

prepared by the Planning Commission when Mr. C. Subrahmanyam was the

Planning Minister. Later Mr. D.P. Dhar replaced him as Planning Minister. He

got prepared an another approach to the Fifth Plan. This approach document was

further revised and a new draft Fifth Five Year Plan was prepared. Later Mr. D.P.

Dhar passed away. Mr. P.N. Haksar became Deputy Chairman of the Planning

Commission. As a result, the Fifth Five Year plan was again revised.

OBJECTIVES :

1. Removal of poverty, and

2. Attainment of self-reliance were the two major objectives of the Fifth Five

Year Plan which called for higher growth, better distribution of income, and

radical increase in domestic rate of saving.

3. 5.5% growth of GDP.

4. An adequate public procurement and distribution system for assured supply of

essential consumption goods, at least to the poorer sections at reasonably stable

prices.

5. A National Programme for Minimum Needs covering elementary education,

drinking water, medical care in rural areas, nutrition, house sites for the landless

labourers, rural roads, rural electrification and slum improvement

6. Vigorous export promotion and imports substitution. And

7. Expansion of productive employment opportunities.

OUTLAY:

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 11

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

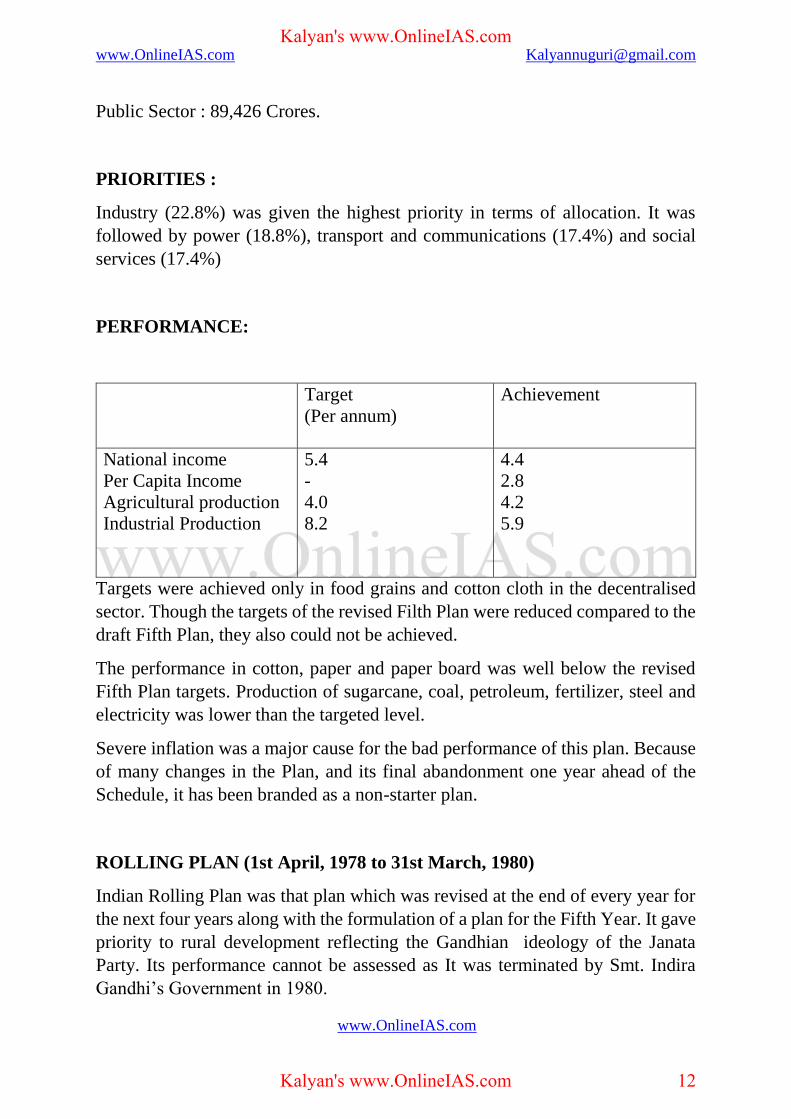

Public Sector : 89,426 Crores.

PRIORITIES :

Industry (22.8%) was given the highest priority in terms of allocation. It was

followed by power (18.8%), transport and communications (17.4%) and social

services (17.4%)

PERFORMANCE:

Targets were achieved only in food grains and cotton cloth in the decentralised

sector. Though the targets of the revised Filth Plan were reduced compared to the

draft Fifth Plan, they also could not be achieved.

The performance in cotton, paper and paper board was well below the revised

Fifth Plan targets. Production of sugarcane, coal, petroleum, fertilizer, steel and

electricity was lower than the targeted level.

Severe inflation was a major cause for the bad performance of this plan. Because

of many changes in the Plan, and its final abandonment one year ahead of the

Schedule, it has been branded as a non-starter plan.

ROLLING PLAN (1st April, 1978 to 31st March, 1980)

Indian Rolling Plan was that plan which was revised at the end of every year for

the next four years along with the formulation of a plan for the Fifth Year. It gave

priority to rural development reflecting the Gandhian ideology of the Janata

Party. Its performance cannot be assessed as It was terminated by Smt. Indira

Gandhi’s Government in 1980.

Target

(Per annum)

Achievement

National income

Per Capita Income

Agricultural production

Industrial Production

5.4

-

4.0

8.2

4.4

2.8

4.2

5.9

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 12

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

SIXTH FIVE YEAR PLAN (1st April, 1980 to 31st March, 1985)

OBJECTIVES :

1. Speedy development of indigenous sources of energy with proper emphasis on

conservation and efficiency r energy use.

2.Strengthening the process of modernisation for the achievement of economic

and technological self-reliance.

3. Protection and improvement of ecological and environmental assets.

4. Controlling the population growth through voluntary acceptance of small

family norm.

5. progressive reduction in the incidence of poverty and unemployment

6. improving the quality of life of people in general with special reference to the

socially and economically handicapped population through a Minimum Needs

Programme.

7. progressive reduction in regional inequalities, and

8. Significant step-up in the growth of the economy.

OUTLAY:

Public Sector (Proposed) 97,500 Crores Actual : 1,1000O Crores

Regarding the moblisation of resources, 94.3% of the total investment came from

domestic resources.

PRIORITIES :

1. Energy was given the highest priority with 27.9% allocation of the public sector

outlay.

2. Agriculture and allied sectors with 23.9% of the public sector outlay got second

priority.

STRATEGY:

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 13

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Strategy of the Plan involves simultaneously strengthening the Infrastructure for

the agriculture and industry, and providing employment opportunities

particularly in the rural areas through special programmes .

PERFORMANCE:

ACHIEVEMENTS :

The growth rate target of 5.2% has been achived

Agriculture :

Foodgrains production target has also been achieved.

The performance in irrigation is impressible though targets could not be achieved.

Infrastructure :

Crude Oil production target has been exceeded with 29.43 million tonnes of

production in 1984-85.

The performance in power production is also impressive though it tell short of

targets both n addition of installed capacity and generation.

The Government of India claimed that the percentage of the people below poverty

line has been brought down from 48.8% in 1960 to 37% by the end of the Plan,

which meant a decrease in the number of people below poverty line from 335

million to 273 million. Price rise was not high.

Target

(Per annum)

Achievement

National income

Per Capita Income

Agricultural production

Industrial Production

5.2

3.5

3.8

6.9

5.2

2.7

4.3

3.7

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 14

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

SHORTCOMINGS :

Agriculture:

Shortages in oil seeds and sugarcane have cropped up.

Infrastructure:

Performance of railways and coal was not upto the mark. Power production

targets were not achieved.

Industry:

Production of fertilizers, steel, power equipment, etc., were short of expectations.

Export performance also fell short of the targets.

GENERAL COMMENTS :

The positive performance in the oil sector and foodgrains production has greatly

contributed to the success of 6th Plan. The achievement of 5.2% growth target is

not significant, if the fact of the poor performance to the base year (1979-80) is

taken into account.

SEVENTH FIVE YEAR PLAN (1st April, 1985 to 31st March 1990)

OBJECTIVES :

1. Improved efficiency

2. Growth rate of 5% in G.D.P.

3. Social justice, and

4.Self-reliance

OUTLAY :

Public Sector : 180,000 crores

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 15

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Professed Priorities :

1. Food

2. Work, and

3. Productivity

Priorities In terms of allocation :

Energy was given the highest priority with 30.5% of the public sector outlay.

Agriculture got the second priority with 22% of the public sector outlay. Social

service got the third priority with 17.2 percent of the public sector outlay.

PERFORMANCE OF THE 7th FIVE YEAR PLAN

The 7th Five Year Plan was a success as it exceeded the targeted growth of 5.0%

by achieving 5.5% growth rate. The economy for the first time exhibited

resilience as it withstood the shock of severe drought in the 3rd year of the Plan.

The Growth rate was achieved in spite of drought, because of accelerated growth

in industrial sector.

Agriculture: Record level of Food Production of 172 million tonnes was

achieved during this Plan. Oil Seeds production has gone upto 15 million tonnes.

Industry: 8.5% average growth rate in spite of drought is- significant except in

the last year.

Infrastructure: Coal, Power, Railways and Ports have also done well.

Exports: Performance of exports was exceedingly good.

Negative features of 7th Five Year Plan.

Balance of payments position was bad.

Deficit of Rs.29,000 crores was more than double the target of Rs.14,000 crores.

Financing of the Plan through inflationary methods of borrowing and deficit

financing was also bad.

Pulses production continued to be an area of concern.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 16

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Industrial sickness particularly in small sector.

Power shortage continued to persist.

The growth rate of the employment generation was stagnant. Crude Oil

production was also almost stagnant.

EIGHTH PLAN (1992-97)

Objectives :

The Eighth Five Year Plan (1992-97) , launched on 1st April 1992, aimed at 5.6%

growth rate.

i. Generation of adequate employment to achieve near full employment level by

the turn of the century;

ii. Containment of population growth through people’s active cooperation and an

effective scheme of incentives and disincentives.

iii. Universalisation of elementary education and complete eradication of

illiteracy among the people In the age group of 15 to 35 years;

iv. provision of safe drinking water and primary health facilities, including

immunisation, accessible to all villages and the entire population, and complete

elimination of scavenging;

v. Growth and diversification of agriculture to achieve self sufficiency in food

and generation of surplus for exports.

vi. Strengthening the infrastructure (energy, transport, communication, irrigation)

in order to support the growth process on sustainable basis.

PRIORITY AREAS:

The priority of the 8th Plan was Human Development. To ensure this, generation

of employment opportunities, population control universal elementary education

& eradication of illiteracy, provision of health care facilities including safe

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 17

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

drinking water and elimination of scavenging were given major emphasis by the

Government.

As Human Development is not possible without economic growth, strengthening

of infrastructural facilities like energy, transport and communications were given

priority. Growth and diversification of agriculture would be given the emphasis

to not only achieve sell sufficiency in food but also generate surplus for exports.

For better implementation of the. Plan, it aimed at involving Panchayati Raj

bodies, Nagar Pahkas, NGOs, etc. in the formulation and implementation of the

Plan.

PLAN OUTLAY:

The total investment of the Plan was fixed at Rs. 7.98,000 crores. 55% of this

amount was shared by the private sector and the remaining 45% of the investment

provided by the Public Sector. The outlay of Public Sector was fixed at Rs.

4,34,100 crores.

Out of this the Central Plan would be Rs. 2,47,865Crores while the plan of the

states and Union Territories would be Rs. i86 235 crores. The budgetary support

to the Plan f9nding would b Rs. 1.88,475 crores.

The Planning Process:

Planning and market mechanism should be so dovetailised that one is

complementary to the other. Market mechanism must serve as an efficiency

promoting devise’. whale planning will be the larger guiding force, keeping the

long term social goals in the perspective

Performance of the Eighth Plan:

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 18

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

NINTH FIVE YEAR PLAN

On January 9, 1999. the Union Cabinet of the BJP led coalition Government off

acted certain changes in the Draft of the 9th Five Year Plan approved by the

United Front Government1 as the growth rates in GDP in the first two years of

9th Five Year Plan were only 5% in 1997-98 and 5.8% in 1998-99, against the

average 9th Plan target of 7%, and also due to the inadequate availability of funds.

Revised Targets of the 9th Five Year Plan

REVISED ORGINAL

1) Growth Rate 6.5% 7%

2)Agriculture and allied Sectors 3.9% 4.5%

3)Industry (Manufacturing only) 8.2% 9.7%

Objectives:

The objectives of the Ninth Five Year Plan are:

i. accelerating agriculture and rural development with a view to generating

adequate productive employment and eradication of poverty.

ii. achieving 6.5% growth rate of the economy with stable prices.

iiii. ensuring food and nutritional security for all, particularly the vulnerable

sections of society.

iv. providing the basic minimum services of safe drinking water, primary health

care facilities, universal primary education, shelter, and connectivity to all in a

time bound manner.

v. containing the growth rate of population.

vi. Ensuring environmental sustainability of the development process through

social mobilisation and Participation of people at all levels.

Target

(Per annum)

Achievement

National income

Agricultural production

Industrial Production

5.6%

3.1%

7.5%

6.54%

4.72%

7.29%

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 19

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

vii. empowerment of women and socially disadvantage groups such as scheduled

Castes, Scheduled Tribes and Other Backward Classes and Minorities as agents

of socio-economic changes and development,

viii. promoting and developing people’s participatory institutions like Panchayati

Raj cooperatives and self-help groups, and

ix. strengthening efforts to build set-reliance

Priorities:

Among the objectives of Ninth Five Year Plan, priority is given to agriculture and

rural development which have immense employment potential, accelerated

economic growth rate, and containing population growth.

Outlay:

The Planning Commission estimated a total plan outlay of Rs.20,00,000 crores

which is a 20 percent step up in real terms over the projected Eighth Plan

allocations.

The State Plans are to account for 45 percent of the Public Sector outlay of

Rs.8,59,000 crores.

Suggestions for mobilisation of resources:

The Planning Commission called for

Augmentation of non-tax revenues through revision of user charges for

power and irrigation and royalties on minerals.

introduction of expenditure based Presumptive income Tax,

tapping unaccounted money, rationalizing and widening the base of tax

structure, and

Increasing savings in all sectors: domestic, corporate and even

government savings also.

The planning commission suggested that subsidies should not exceed R.72,800

Crores in the ninth plan period. This can be done only by linking administered

prices with the increase in their costs.

The Prime Minister said that to achieve an economic growth of 6.5 percent the

country has to take some difficult decisions like containing fiscal deficit,

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 20

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

rationalization of User changes for power and irrigation disinvestment of public

sector enterprises and focused subsidies.

Elaborating on the broad theme approach to the Ninth Plan, the Prime Minister

said that no significant dent could be made on poverty and unemployment without

rapid and sustained growth. Equitable growth, he said, requires a special focus on

agriculture and rural non-farm activities as a dynamic rural sector was both an

enabling condition for industrialization and an end in itself He mentioned poor

state of infrastructure as the most pressing constraint for growth.

Performance of the Ninth Plan:

Target Achievement

GDP Growth Rate 6.5% 5.52%

Agriculture 3.9% 2.44%

Industry 8.2% 4.29%

Services 8.5% 7.82%

TENTH FIVE YEAR PLAN 2002-07

Highlights:

Objectives and Targets:

• achieving an 8% economic growth rate during 2002-2007,

- generating 50 million new jobs in the next five years,

- reducing poverty levels from the present 26 per cent to 21 per cent of the

population by 2007,

- reducing the decadal population growth rate between 2001 & 2011 to 16.2%

from 21.3% registered during 1991-2001,

- increasing literacy levels up to 75 per cent of the population, taking appropriate

measures to enroll all children in schools by 2003, so that they complete five

years of primary education by 2007,

• providing clean drinking water facility to all the villages in the country,

- cleaning all the major polluted rivers,

- increasing the forest cover to 25 per cent,

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 21

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Mobilisation of Resources :

- Rs. 15,92,300 crores of Public Sector resources of the Centre, States and UT’s

• raising FDI inflows to the extent of $7.5 billion per annum during 2002-2007,

• gathering Rs. 78,000 crores through disinvestment In PSUs,

- increasing Investment rate up to 28.4% of the G.D.P.,

• increasing Tax-GOP ratio to 10.3 per cent,

• widening the tax base and increasing the collections,

- introducing an integrated central and state VAT,

- cutting subsidies and administrative overhead costs to prune expenditure,

• establishing major airports in partnership with the private sector, and

• dismantling barriers to inter-state trade, are the highlights of the 10th Five Year

Plan for the period 2002-2007 approved by the Planning Commission under the

Chairmanship of Prime Minister Atal Bihari Vajpayee in New Delhi, on October

5, 2002.

Details :

The Planning Commission, stressed the need to achieve an eight per cent

economic growth rate over the next five years and advocated stringent measures

like accelerating tax reforms, moving towards an integrated central and state

Value Added Tax (VAT) for goods and services, striving for fiscal prudence at

both the center and state levels, improving the capital output ratio, and removing

bottlenecks in energy, transport and water infrastructure to reach the targets set

by the draft 10th Five Year Plan.

The plan proposed to carry forward key reforms. particularly in agriculture, td

generate 50 million jobs in the next five years besides raising FDI flow to $7.5

billion annually and gather Rs. 78,000 crore through disinvestment

It noted that the key to achieving the growth target would be to shift capital to

those areas where the returns are high So that additional demand Is created

through employment which Will increase the purchasing power of the People.

The eight per cent growth rate would require an Investment of 28.4 per cent of

the GDP which would be met from domestic savings of 26.8 per cent of GDP and

external Savings of 1.6 per cent. The public sector outlay has been pegged at

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 22

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Rs.15,92,300 crore which includes Rs. 9,21,291 crore as central outlay and Rs.

6,71 ,009 crore as states’ plan outlay.

Acknowledging the role of good governance in enhancing efficiency, the plan

underlined the need to strengthen Panchayati Raj institutions and urban local

bodies to increase people’s participation in development process.

It also emphasised undertaking revenue and judicial reforms, right sizing the

government, improving transparency and accountability, using it for good e-

governance, enactment of right to information act and involvement of civil

society as partners in development.

Agriculture:

The tenth plan identified an eight point key reform agenda in agriculture. The key

reforms proposed include elimination of inter-state barriers to trade, amendment

to Essential Commodities Act and Agricultural Marketing Act, liberalizing agri-

exports, encouraging contract farming and consolidating various acts dealing

with food sector into a comprehensive food law. The agenda also proposes futures

trading in all commodities and removal of restrictions on financing of stocking

and trading.

Industry:

A six point agenda on industrial reforms was envisaged to improve efficiency,

neurial energy and promote rapid and sustainable growth. They include enacting

labour reforms, proposed repeal of Sick Industrial Companies Act (SICA),

strengthening bankruptcy and fore closure Laws to facilitate transfer of assets,

early enactrnent of Electricity Bill, Coal Nationalization Bill and Communication

Convergence Bill.

The plan also seeks to abolish restrictions an encourage decontrol of private road

transport., passenger services and private sector participation in road

maintenance. It proposed to expedite the formulation of civil aviation policy and

development of major airports with active private participation.

Balanced Regional Development:

The plan aims at promoting balanced and equitable regional development and for

the first time it has devoted a separate chapter to state-wise breaks up of targets

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 23

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

in order to provide the requisite focus. Proposing a plan strategy for states, the

document envisages resource mapping at the block level. Special focus has been

laid on the North Eastern States. 100 most backward districts would be given

special assistance by way of Rashtriya Sam Vikas Yojana.

Approval by the Cabinet and NDC :

The plan was approved by the Union Cabinet on October 29, 2002, and by the

National Development Council (NDC) on December 21, 2002. Macro-

Parameters for the Tenth Plan

(2002-07)

IX Plan X Plan

1. Domestic Savings Rate (% of

GDPmp)

2. Current Account Deficit (% of

GDPmP)

3. Investment Rate (% of the GDPmp)

(1+2)

4. ICOR

5. GOP Growth Rate (% per annum)

(3/4)

6. Export Growth Rate (% per annum)

7. import Growth (% per annum)

23.31

0.90

24.23

4 53

5.35

6.91

9.80

26.84

1.57

28.41

3.58

7.93

12.38

17.13

Note: GDPmp implies Gross Domestic Product at market Prices

Source Planning Commission, Tenth Five Year Plan (2002-2007)

Sectoral Allocations of public Sector Resources for the Ninth And Tenth Plan

Ninth

Plan

Tenth

Plan

%

Amount % Amount % Increase

(1) (2) (3) (4)

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 24

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

1. Agriculture & Allied Activities

2. Rural Development

3. Special Area Programmes

4. Irrigation & Flood Control

5. Energy

6. Industry and Minerals

7. Transport

8. Communications

9. Science, Technology &

Environment

10. General Economic Services

11. Social Services

12. General Services

Total

37,239

88,965

5,408

69,830

2,19,243

44,695

1,43,249

92,836

15,667

13,734

1,94,529

15,646

9,41,041

3.9

9.5

0.5

7.4

23.2

4.7

15.2

9.9

1.7

1.5

20.7

1.7

100.0

58,933

1,21,928

20,879

1,03,315

4,03,927

58,939

2,25,977

98,968

30,424

38,630

3,47,391

16,328

15,25,639

3.9

8.0

1.3

6.8

26.5

3.9

14.8

6.5

2.0

2.5

22.8

1.0

100.0

58.3

37.1

286.1

48.0

84.2

31.9

57.8

6.6

94.2

181.3

78.6

4.4

62.1

Source: Planning Commission . Tenth Five Plan(2002-07)

Final Performance of 10th Plan

Target Achievement

GDP Growth (%)

Agriculture (%)

Industry

Services

Domestic Savings Rate %of GOP at Market

Prices

Investment Rate % of GDP at Market Prices

8

4

8.9

9.3

26.84

28.41

7.76

2.30

9.17

9.30

30.9

32.4

ELEVENTH FIVE YEAR PLAN (2007-2012)

Highlights:

On December 19, 2007, the National Development Council approved the 11,’

Five Year Plan that aims at sustaining

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 25

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

- 8.1per cent overall growth in G.D.P, Contributed by 4 per cent agricultural

growth, 10 to 11 per cent industrial growth, and 9 to 11 per cent growth in

services.

Attaching highest priority to education; rural development, agriculture, irrigation

and health, the Plan earmarks more than half of the budgetary support toward

these areas. The total outlay for the plan is Rs.36,44,718 crore, of which

budgetary support would be Rs.10,96,860 crore. Education Outlay Increased to

19 per cent : The Plan outlay for the education sector has been raised from 7.68

per cent of the Centre’s Gross Budgetary Support (GBS) in the 10 Plan to 19 per

cent In the 11th Plan. Education is best hope for achieving inclusiveness and for

spreading development to backward regions and marginalized groups.

Apart from strengthening the Sarva Shiksha Abhiyan (SSA) programme,

government plans to establish 6,000 model schools in all blocks, 30 new central

universities, and 370 new colleges in educationally backward districts in the 11’

Plan period

Also, to give a push to professional education In the country, the government

plans to setup 8 HITs and 7IIMs by 2011-12.

Additionally, with a view to provide vocational training to more than 1 crore

students, the government also plans to set up 1,600 new Industrial Training

Institutes (IITs) and polytechnics, 10000 new vocational schools and 50.000 new

skill development centers.

Monitor able Targets of the 11th Five Year Plan:

The Commission also listed the socioeconomic targets that will require

monitoring throughout the Plan period to ensure that the growth process is

beneficial to the masses. Some of the important targets are :

• doubling per capita income by 2016-17,

- creating 7 crore new jobs.

• reducing educated unemployment rate to below 5 per cent,

- reducing dropout rate of school children to 20 per cent from 52 per cent,

- Increasing literacy rate to 80 per cent.

- reducing infant mortality rate to 28 per 1000 births and maternal mortality rate

to 1 per 1,000 births,

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 26

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

- providing clean drinking water to all by 2009,

- improving sex ratio t 935 by 2011-12 and 950 by 2016.17,

• Access to electricity to all by 2009,

• Tele-connectivity to every village by November 2007,

• Broadband connectivity to all villages by 2011-12,

- Road to all villages with 1,000 populations by 2009,

- Increasing forest cover and tree cover by 5 percent,

- achieving WHO standard air quality in major cities by 2011-12,

- treating all urban waste water by 2011-12 to clear rivers.

Thrust Areas of the Eleventh Plan

Sectors Thrust Areas

Education

Health, Nutrition, Drinking

Water, and Sanitation

Agriculture and Irrigation

Rural Development, Land

Resources and Panchayati Raj

Quality Upgradation in Primary

Education, Expansion of

Secondary Education, major

emphasis on Upgradation of

Higher Education including

Technical Education, ICT

throughout education system.

Major Upgradation of rural

health infrastructure, Medical

education,

Nutritional Support to children

and pregnant and lactating

women through ICDS, health

insurance based urban health

facilities, Health care for elderly,

achieving sustainability,

improvement in service levels

and moving towards universal

access to safe and clean drinking

water.

Ensuring Food Security,

Supporting State-specific

agriculture strategy and

programmes, Better seed

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 27

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Social Justice and Empowerment

Physical Infrastructure

Energy

Scientific Departments

production, Focused agricultural

research, Extension,

Development of modem

markets.

Universalization and

improvement in pro me delivery

of NREGP, Integrated

Watershed management

including management of

underground water level.

Special attention to the needs of

SCs, STs and minorities and

other excluded groups through

pre and post-metric scholarship,

Hostels for boys/girls, Income

and employment generation

opportunities, Multi-sectoral

development programmes for

minorities in minority

concentration districts.

Emphasis on the public—private

partnership in investment,

policies to ensure time bound

creation of world-class

infrastructure, especially in

remote and inaccessible rural

areas and NE, Hinterland

connectivity through improved

rail and road Infrastructure.

Electrification of all villages and

extending free household

connections to all 2.3 crore BPL

households through RGGVY,

Nuclear power development.

Development of satellite launch

capabilities; GSLV-Mk-lll,

Development of new energy

systems, viz, advance heavy

water reactor and

nanotechnology.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 28

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Details: Sectoral Growth in Recent Plans

Sector Eighth Plan Ninth Plan

(1997-01)

Tenth Plan

(2002-06)

Eleventh Plan

Projections

(2007-11)

1.Agriculture 4.72 2.44 2.30 4.0

2.Industry 7.29 4.29 9.17 10-11

3.Services 7.28 7.87 9.30 9-11

4.Total 6.54 5.52 7.74 9.0

Sectoral Allocation- Tenth plan and Eleventh plan

Tenth plan Eleventh

Plan

Sectors Allocation % to total Projected

Allocation

% to

total

1.Education

2.Rural Development Land resource

and Panchayati Raj

3.Physical Infrastructure

4.Health Family Welfare and Ayush

5.Agriculture and Irrigation

6.Social Justice

7.Scientific Departments

8.Energy

Total Priority Sector (1 to 6)

9.Others

Total

62461

87041

89021.

45771

50639

36381

29823

47266

448403

365375

813778

7.68

10.70

10.94

5.62

6.22

4.47

3.66

5.81

510

44.90

100.00

274228

190330

128160

123900

121556

90273

66580

57409

1052436

369275

1421711

19.29

13.39

9.01

8.1

8.55

6.35

4.68

4.04

- 74.03

25.97

100

Sectoral allocation for public Sector’s resources- Tenth Plan(2002-07)

Realisations And Eleventh Plan

(Rs. Crore at 2006-07

prices)

Centre, States And UT’s total Outlay

Tenth Plan Eleventh plan

projection

% Increase

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 29

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

1. Agriculture and Allied

Activities

2. Rural Development

3. Special Area Programmes

4. irrigation & Flood Control

5, Energy

6. Industry & Minerals

7. Transport

8. Communications

9. Science, Technology &

Environment

10. General Economic

Services

11 Social Services

12.General Services

Total

60702

137710

16423

112415

363635

64655

263934

82945

28673

30349

436529

20489

1618460

136381

301069

26329

210326

854123

153600

572443

95380

87933

62523

1102327

42283

3644718

124:7

118.6

60.3

87.1

134.9

137.6

116.9

15

206.7

106.0

152.5

106.4

125.2

Note: Based on the sectoral outlay reported by the states. Totals may tally due to

rounding errors.

Macro economic Parameters

Tenth plan Eleventh

plan

1. Invisible Rate (% of GDPmp)

2. Domestic Savings Rate (% of GDPmp)

3. Current Account Deficit (% of GDPmp)

4. ICOR

5. GDP Growth Rate (% per annum)

32.4

30.9

1.5

4.3

7.5

36.7

34.8

1.9

4.1

9.0

Note: GDPmp=GDP at market prices.

Public sector allocations for Eleventh Plan

(Rs crore at 2006-07 prices)

Centre

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 30

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Sources of funding Allocation

1. Budgetary Support

2. IEBR (Internal and Extra Budgetary Resources)

3. Total Centre(1+2)

1 096860

1059711

2156571

States and UTs

Sources of funding Allocation

4, State Own Resources

5. Central assistance to State/UT Plan

8. Total States & UTs (4+5)

1163296

324851

1488147

Total public Sector Outlay

7.Grand total (3+6) 3644718

Source: Planning Commission

PLANNING COMMISSION’S INDIA VISION 2020’ DOCUMENT

On January 23, 2003, Planning Commission released ‘India : Vision 2020’

document.

Highlights:

• achieving 100 per cent literacy,

• eradicating unemployment and poverty,

• quadrupling per capita income,

• attaining 9 per cent GDP growth rate per annum by year 2020,

• checking contagious diseases completely,

100 per cent school enrolment in the age group of 6 to 14, and keeping urban air

pollution under control by strict enforcement of motor vehicle emission standards

and widespread use of ethanol- blended motor fuels are the highlights of the

document.

The document is a futuristic report prepared by a committee headed by SP. Gupta,

Member, Planning Commission.

TWELFTH FIVE YEAR PLAN (2012-17) TARGETS 8 CENT GROWTH

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 31

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

The Twelfth Five Year Plan (2012-17) which focuses on ‘Faster. More inclusive

and Sustainable Growth has set a target of 8.2 per cent during the plan period.

The total outlay of the Twelfth Plan is estimated at Rs. 00,50,123 crores of which

the centres share is Rs. 43,33,739 crores end states share is Rs. 37,18,385 crores.

The Plan Identified 25 rnonitorable targets which are to be achieved by the end

of plan period i.e 2012-17.

Economic Growth:

1. GDP Growth Rate of 8.2 per cent,

2. Agriculture Growth Rate Of 4.0 per cent,

3. Manufacturing Growth Rate of 10,0 per cent,

4. Growth rate of very state In the Twelfth Plan preferably higher than that

achieved In the ‘Eleventh Plan,

Poverty and Employment:

5. reducing headcount ratio of consumption poverty by 10 percentage points over

the preceding estimates by the end of Twelfth Five Year Plan,

6. generating 50 million new work opportunities In the non-farm sector and

providing skill certification to equivalent numbers,

Education :

7.increasing mean years of schooling to seven years,

8. enhancing access to higher education by creating two million additional seats

lot each age group aligned to the skill needs of the economy,

9.Eliminating and social gap In school enrolment (that Is. between girls and boys,

and between SC., ST Muslims and the rest of the populations

Health:

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 32

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

10.. reducing Infant Mortality Rate (IMR) to 25 and Maternal Mortality Rate

(MMR) to 1 per 1,000 live births, and improving Child Sex Ratio (0-6 years) to

950.

11. reducing Total Fertility Rate 2.1.

12. reducing under-nutrition among children aged 0-3 years to half of the National

Family Health Survey -3 (NFHS-3) levels,

Infrastructure, Including Rural infrastructure

13. Increasing investment in Infrastructure, as a percentage of GDP to 9 per cent.

14. increasing the Gross Irrigated Area tram 90 million hectares to 103 million

hectares,

15. Providing electricity to all villages and reducing Aggregate Technical and

Commercial (AT8C) losses to 20 per cent,

16. Connecting all, villages with all-weather roads

17. Upgrading national and state highways to the minimum two-lane standard,

18. Completing Eastern and Western dedicated Freight Corridors,

19. Increasing rural tale-density to 70 per cent,

20. Ensuring 50 per cent of rural population has access to 40 liter per capita per

day piped drinking water supply, and 50 pr cent gram Panchayats achieve Nirrnal

Gram Status

Environment and Sustainability:

21. Increasing green cover (as measured by satellite Imagery) by I million hectare

every year during the Twelfth Five Year Plan,

22. Adding 30,000 MW of renewable energy capacity

23. Reducing emissions in line with the target of

20 per cent to 25 per cent reduction over 2005 levels by 2020, Service Delivery

24. Providing access to banking services to 90 per cent Indian households, and

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 33

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

25. Shifting. Major subsidies and welfare related beneficiary payments to a direct

cash transfer mode by the end of the Twelfth Plan, Using the Aadhar platform

with linked bank accounts

Allocation of center’s Gross Budgetary Support (GBS) by Major Sectors-

Eleventh plan Realization and Twelfth plan Projection

(Rs Crore in Current Prices)

Eleventh

plan

Twelfth Plan %

increase

over

Major Sectors Allocation % Share Projected

Allocation

% Share Eleventh

plan

1 Agriculture and

Water Resources

2 Rural Development

& Panchayati Raj

3 Scientific

Departments

4 Transport and Energy

5 Education

6 Health and Child

Development

7 Urban Development

8 Others

Total Plan Allocation

1,16554

3,97524

58,690

2,04,076

1,77,538

1,12,646

63.465

4,58,849

1589,342

7.33

25.01

3.69

12.84

11.17

7.09

3,99

28.87

100.00

2,84.030

6,73,034

1,42,167

4,48,736

4,53,728

4,08,521

1,64,078

9,94,333

35,68,626

7,96

18.86

3.98

12.57

12.71

11.45

4.60

27.86

100.00

143.69

69.31

142.23

119.89

155.57

262.66

158.53

116.70

124.53

National Institution for Transforming India Aayog

National Institution for Transforming India Aayog (Hindi: Policy Commission)

is a Government of India policy think-tank established by Prime

Minister Narendra Modi after his having dissolved the Planning Commission.

Pronounced nithi, meaning "policy" in Hindi, the acronym stands for National

Institution for Transforming India. "Aayog'" is the Hindi word for "commission".

The stated aim of NITI Aayog's creation is to foster involvement and participation

in the economic policy-making process by state governments of India, a "bottom-

up" approach in contrast to the Planning Commission's tradition of "top-down"

decision-making. The Prime Minister heads the Aayog as its chairperson. Thus,

while the Planning Commission had no representation for state and Union

Territories, the NITI Aayog has.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 34

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

The Union Government of India announced formation of NITI Aayog on 1

January 2015, and the first meeting of NITI Aayog was held on 8 February

2015. "NITI Blogs", which provide public access to articles, field reports and

work in progress as well as the published opinions of NITI officials, are available

to the public on the Aayog website.

There are a couple of things to be considered here. NITI Aayog would therefore

mean:

• A group of people with authority entrusted by the government to

formulate/regulate policies concerning transforming India.

• It is a commission to help government in social and economic issues.

• Also it's an Institute of think tank with experts in it.

India's Finance Minister Arun Jaitley made the following observation on the

necessity of creating NITI Ayog: “The 65-year-old Planning Commission had

become a redundant organization. It was relevant in a command economy

structure, but not any longer. India is a diversified country and its states are in

various phases of economic development along with their own strengths and

weaknesses. In this context, a ‘one size fits all’ approach to economic planning is

obsolete. It cannot make India competitive in today’s global economy”

Renaming of Planning Commission

May 29, 2014 -> According to the first IEO (Independent Evaluation Office )

assessment report which was submitted to Prime Minister Modi on May 29,

Planning Commission to be replaced by "control commission"

15th -17th Aug. 2014 –> Govt. of India officials viewed Planning

Commission to be replaced with a diluted version of the National

Development and Reform Commission (NDRC) of China "

1st January 2015 –> Cabinet resolution to replace Planning Commission by

NITI Aayog (National Institution for Transforming India) "

February 8, 2015: The first meeting of NITI Aayog was chaired by Narendra

Modi.

Origin and formation

1950 : Planning commission was established

May 29, 2014 : The first IEO(Independent Evaluation Office ) assessment

report was submitted to Prime Minister Modi on May 29, three days after he

was sworn in. According to Ajay Chibber, who heads the IEO, views in the

report are based on the views of stakeholders and some Planning Commission

members themselves. Planning Commission to be replaced by "control

commission"

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 35

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

August 13, 2014 : Cabinet of Modi govt. scrapped the Planning Commission

Aug. 15 2014 : Modi mentioned to replace Planning Commission by National

Development and Reform Commission (NDRC) on the line of China

Members

The NITI Aayog comprises the following:

1. Prime Minister of India as the Chairperson

2. Governing Council comprising the Chief Ministers of all the States and

Union territories with Legislatures and lieutenant governors of other

Union Territories.

3. Regional Councils will be formed to address specific issues and

contingencies impacting more than one state or a region. These will be

formed for a specified tenure. The Regional Councils will be convened by

the Prime Minister and will comprise of the Chief Ministers of States and

Lt. Governors of Union Territories in the region. These will be chaired by

the Chairperson of the NITI Aayog or his nominee

4. Experts, specialists and practitioners with relevant domain knowledge as

special invitees nominated by the Prime Minister

5. Full-time organizational framework (in addition to Prime Minister as the

Chairperson) comprising

1. Vice-Chairperson: Arvind Panagariya

2. Members: Three (3) Full-time: economist Bibek Debroy, former

DRDO chief V.K. Saraswat and Agriculture Expert Professor

Ramesh Chand

3. Part-time members: Maximum of two from leading universities

research organizations and other relevant institutions in an ex-

officio capacity. Part-time members will be on a rotational basis

4. Ex Officio members: Maximum of four members of the Union

Council of Ministers to be nominated by the Prime Minister

5. Chief Executive Officer: To be appointed by the Prime Minister for

a fixed tenure, in the rank of Secretary to the Government of India.

Sindhushree Khullar appointed as the Chief Executive Officer.

6. Secretariat as deemed necessary

Present Members

The various members of NITI Aayog are:

1. Chairperson: Prime Minister Narendra Modi

2. 1stCEO: Sindhushree Khullar IAS,present CEO:Amitabkanth

3. Vice Chairperson: Arvind Panagariya

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 36

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

4. Ex-Officio Members: Rajnath Singh, Arun Jaitley, Suresh

Prabhu and Radha Mohan Singh

5. Special Invitees: Nitin Gadkari, Prakash javadekar and Thawar Chand

Gehlot

6. Full-time Members: Bibek Debroy, V. K. Saraswat and Ramesh chand

7. Governing Council: All Chief Ministers and Lieutenant Governors of

States and Union Territories

Difference between NITI Aayog and Planning Commission

Financial clout

NITI Aayog – To be an advisory body, or a think-tank. The powers to allocate

fund vested in the finance ministry.

Planning Commission – Enjoyed the powers to allocate funds to ministries and

state governments

Full-time members

NITI Aayog – Two full-time members.

Planning Commission – had eight full-time members

States' role

NITI Aayog – Includes the Chief Ministers of all States and the Lieutenant

Governors of all Union territories in its Governing Council, devolving more

power to the States of the Union.

Planning Commission – States' role was limited to the National Development

Council and annual interaction during Plan meetings

Member secretary

NITI Aayog – To be known as the CEO and to be appointed by the prime minister

Planning Commission – Secretaries or member secretaries were appointed

through the usual process

Part-time members

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 37

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

NITI Aayog – To have a number of part-time members, depending on the need

from time to time

Planning Commission – Full Planning Commission had no provision for part-

time members

Constitution

Niti Aayog – Governing Council has state chief ministers and lieutenant

governors.

Planning Commission- The commission reported to National Development

Council that had state chief ministers and lieutenant governors.

Organization

Niti Aayog – New posts of CEO, of secretary rank, and Vice-Chairperson. Will

also have two full-time members and part-time members as per need. Four cabinet

ministers will serve as ex-officio members.

Planning Commission – Had deputy chairperson, a member secretary and full-

time members.

Participation

Niti Aayog- Consulting states while making policy and deciding on funds

allocation. Final policy would be a result of that.

Planning Commission- Policy was formed by the commission and states were

then consulted about allocation of funds.

Allocation

Niti Aayog- No power to allocate funds

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 38

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Planning Commission- Had power to decide allocation of government funds for

various programs at national and state levels.

Nature

Niti Aayog- NITI is a think-tank and does not have the power to impose policies.

Planning Commission- Imposed policies on states and tied allocation of funds

with projects it approved.

Aims and Objectives of NITI Ayog

NITI Aayog will seek to provide a critical directional and strategic input into the

development process.

The centre-to-state one-way flow of policy, that was the hallmark of the Planning

Commission era, is now sought to be replaced by a genuine and continuing

partnership of states.

NITI Aayog will emerge as a "think-tank" that will provide Governments at the

central and state levels with relevant strategic and technical advice across the

spectrum of key elements of policy.

The NITI Aayog will also seek to put an end to slow and tardy implementation

of policy, by fostering better Inter-Ministry coordination and better Centre-State

coordination. It will help evolve a shared vision of national development

priorities, and foster cooperative federalism, recognizing that strong states make

a strong nation.

The NITI Aayog will develop mechanisms to formulate credible plans to the

village level and aggregate these progressively at higher levels of government. It

will ensure special attention to the sections of society that may be at risk of not

benefitting adequately from economic progress.

The NITI Aayog will create a knowledge, innovation and entrepreneurial support

system through a collaborative community of national and international experts,

practitioners and partners. It will offer a platform for resolution of inter-sectoral

and inter-departmental issues in order to accelerate the implementation of the

development agenda.

In addition, the NITI Aayog will monitor and evaluate the implementation of

programmes, and focus on technology upgradation and capacity building.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 39

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Through the above, the NITI Aayog will aim to accomplish the following

objectives and opportunities:

An administration paradigm in which the Government is an "enabler" rather

than a "provider of first and last resort."

Progress from "food security" to focus on a mix of agricultural production, as

well as actual returns that farmers get from their produce.

Ensure that India is an active player in the debates and deliberations on the

global commons.

Ensure that the economically vibrant middle-class remains engaged, and its

potential is fully realized.

Leverage India's pool of entrepreneurial, scientific and intellectual human

capital.

Incorporate the significant geo-economic and geo-political strength of the

Non-Resident Indian Community.

Use urbanization as an opportunity to create a wholesome and secure habitat

through the use of modern technology.

Use technology to reduce opacity and potential for misadventures in

governance.

The NITI Aayog aims to enable India to better face complex challenges, through

the following:

Leveraging of India's demographic dividend, and realization of the potential

of youth, men and women, through education, skill development, elimination

of gender bias, and employment

Elimination of poverty, and the chance for every Indian to live a life of dignity

and self-respect

Redressal of inequalities based on gender bias, caste and economic disparities

Integrate villages institutionally into the development process

Policy support to more than 50 million small businesses, which are a major

source of employment creation

Safeguarding of our environmental and ecological assets.

Major Highlights

1. The new National Institution for Transforming India (NITI) will act more like

a think tank or forum and execute programs by taking the States along with them.

This is in sharp contrast with the defunct Planning Commission which imposed

five-year-plans and allocated resources while running roughshod over the

requests of the various States.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 40

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

2. NITI will include leaders of India's 29 states and seven union territories. But

its full-time staff – a deputy chairman, Chief Executive Officer and experts – will

answer directly to the Prime Minister of India, who will be chairman.

3. The opposition Congress IS mocked the launch as a cosmetic relabelling

exercise – the new body's acronym-based name means 'Policy Commission' in

Hindi, suggesting a less bold departure than the English version does. Several

believe that is consistent with the negativism that has become the hallmark of the

Congress.

4. Despite being blamed by critics for the slow growth that long plagued India,

the Commission survived the market reforms of the early 1990s, riling Mr Modi

with its interventions when he was Chief minister of industry and investor

friendly Gujarat.

5. Mr Modi, elected by a landslide last year on a promise to revive flagging

growth and create jobs, had vowed to do away with the Planning Commission

that was set up in 1950 by Congressman and Prime Minister Jawaharlal Nehru.

6. But his plans been derided by the Congress party, which wants to defend the

Nehru legacy and describes Mr Modi's vision of "cooperative federalism" as

cover for a veiled power grab.

7. India's first Prime Minister Jawaharlal Nehru, a socialist who admired Joseph

Stalin's drive to industrialize the Soviet Union, set up and chaired the Commission

to map out a development path for India's agrarian economy.

8. In 2012, the Planning Commission was pilloried for spending some Rs. 35 lakh

to renovate two office toilets, and then it was lampooned for suggesting that

citizens who spent Rs. 27 or more a day were not poor.

9. The commission had remained powerful over the decades because it had

emerged as a sort of parallel cabinet with the Prime Minister as its head.

10. The Commission's power in allocating central funds to states and sanctioning

capital spending of the central government was deeply resented by states and

various government departments.

11. The NITI Aayog will also seek to put an end to slow and tardy implementation

of policy, by fostering better Inter-Ministry coordination and better Centre-State

coordination. It will help evolve a shared vision of national development

priorities, and foster cooperative federalism, recognizing that strong states make

a strong Nation.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 41

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

Criticisms of NITI Aayog

The government's move to replace the Planning Commission with a new

institution called 'NITI Aayog’ was criticized by opposition parties of India. The

Congress sought to know whether the reform introduced by the BJP-led

government was premised on any meaningful programme or if the move was

simply born out of political opposition to the party that ran the Planning

Commission for over 60 years. "The real issue is do you (the government) have

a substantive meaningful Programme to reform the Planning Commission?"

Congress spokesperson Abhishek Manu Singhvi said. "If you (the BJP

government) simply want to abolish it (the commission), because it is something

which (Jawaharlal) Nehru created for this country and you don't like Nehru or

simply because it was run by the Congress for 60 years and you don't like the

Congress, that is pitiable," he said.

The Communist Party of India-Marxist said a mere change in the name would not

yield the desired results. "Mere changing this nomenclature, and this sort of

gimmickry is not going to serve the purpose. Let us wait and see what the

government is eventually planning," CPI-M leader Sitaram Yechury said.

The Planning Commission used to plan policy. I don't know what is the

government trying to do by merely changing the nomenclature from Planning

Commission to Niti Ayog," said Congress spokesman Manish Tewari.

However, Commerce and Industry Minister Nirmala Sitharaman of BJP accused

the critics of being “ignorant of facts”.

“With the new set of changes, the state governments no longer need to have a

begging attitude and instead take independent steps for development,” said

Sitharaman. With this the NDA government is fulfilling one more of its key

promises of robust federalism.

"The idea to create an institution where states' leaders will be part and parcel of

the collective thinking with the Centre and other stakeholders in formulating a

vision for the development of the country is right on as compared with the

previous structure, where a handful of people formulated the vision and then

presented it to the National Development Council (NDC). This was not entirely

absorbed and adopted by the latter," said former Planning Commission member

Arun Maira.

Kalyan's www.OnlineIAS.com

Kalyan's www.OnlineIAS.com 42

www.OnlineIAS.com [email protected]

www.OnlineIAS.com

In fact, a recent survey of expert opinions in the magazine "Business World"

shows that either a very clear distinction of roles of NDC, Governing Council and

Inter State Council or a merger of one or two with a vibrant and functional ISC

can serve the two key goals of such forums: policy development and conflict

resolution.

Economic growth and Development

Economic growth is the increase in the inflation-adjusted market value of the

goods and services produced by an economy over time. It is conventionally

measured as the percent rate of increase in real gross domestic product, or real

GDP. Of more importance is the growth of the ratio of GDP to population

(GDP per capita, which is also called per capita income). An increase in growth

caused by more efficient use of inputs (such as physical capital, population, or

territory) is referred to as intensive growth. GDP growth caused only by increases