KAL Capital - Aerospace & Defense - KAL Capital Markets, LLC

8

Quarter in Review Q3 2020 Introduction KAL Capital - Aerospace & Defense Quarter In Review © KAL Capital, 2020 Dear Friends, Hope you are well. As the general economy and other aspects of everyday life slowly start to begin to ease towards normalcy (depending on where you are); the M&A market has orientated itself to a post-Covid reality and has entered into a full-blown “V-Shaped Recovery.” While that dynamic is very end-market and situation specific, we have seen private equity and their lending partners revitalized and back into (remote) deal making mode. As amazing as that buy-side dynamic may seem to outside observers, the supply of transactions has increased significantly and is close to approximating 2019 levels. While some of the M&A activity is opportunistic, we have observed a far greater proportion of the selling coming from family or owner-operated businesses that are seizing the opportunity to transact ahead of any potential changes in capital gains tax treatment. Both with our clientele and anecdotally, we have heard multiple examples of private sellers accelerating their time horizons to prevent potential tax leakage. For our practice, we are pleased to announce the close of Geodetics to Aevex Aerospace, a portfolio company of Madison Dearborn Partners. The sale of Geodetics checked many boxes for potential buyers including proprietary defense electronic products, national security and clandestine, military customers as well as playing into specific micro trends around operating in GPS-denied environments. We expect Q4 2020 to be our busiest to date as we have multiple transactions that we are excited to share. In this Quarterly Industry review, we will continue to assess the ongoing carnage in commercial aerospace. While recent deliveries and orders do not point to near-term recovery, we are hopeful that the upcoming quarter will finally mark a return to service for the B737MAX and a continuation of the gradual improvement in load factors and passenger miles. Even in this part of the market, there are multiple high-quality commercial aerospace businesses in the market that are seeing strong demand for a wide-range of buyers. Additionally, with the election forefront on everyone’s minds, we attempt to remind everyone that changes in defense spending tend to be more gradual (regardless of Administration) than partisan voices account for. As always, please feel free to reach out to either of us with any questions. Sincerely, Trevor Bohn Ryan Murphy Partner Partner

Transcript of KAL Capital - Aerospace & Defense - KAL Capital Markets, LLC

Quarter in Review Q3 2020Introduction

KAL Capital - Aerospace & DefenseQuarter In Review

© KAL Capital, 2020

Dear Friends,

Hope you are well. As the general economy and other aspects of everyday life slowly start tobegin to ease towards normalcy (depending on where you are); the M&A market hasorientated itself to a post-Covid reality and has entered into a full-blown “V-ShapedRecovery.” While that dynamic is very end-market and situation specific, we have seenprivate equity and their lending partners revitalized and back into (remote) deal makingmode.

As amazing as that buy-side dynamic may seem to outside observers, the supply oftransactions has increased significantly and is close to approximating 2019 levels. Whilesome of the M&A activity is opportunistic, we have observed a far greater proportion of theselling coming from family or owner-operated businesses that are seizing the opportunity totransact ahead of any potential changes in capital gains tax treatment. Both with ourclientele and anecdotally, we have heard multiple examples of private sellers acceleratingtheir time horizons to prevent potential tax leakage.

For our practice, we are pleased to announce the close of Geodetics to Aevex Aerospace, aportfolio company of Madison Dearborn Partners. The sale of Geodetics checked manyboxes for potential buyers including proprietary defense electronic products, nationalsecurity and clandestine, military customers as well as playing into specific micro trendsaround operating in GPS-denied environments. We expect Q4 2020 to be our busiest todate as we have multiple transactions that we are excited to share.

In this Quarterly Industry review, we will continue to assess the ongoing carnage incommercial aerospace. While recent deliveries and orders do not point to near-termrecovery, we are hopeful that the upcoming quarter will finally mark a return to service forthe B737MAX and a continuation of the gradual improvement in load factors and passengermiles. Even in this part of the market, there are multiple high-quality commercial aerospacebusinesses in the market that are seeing strong demand for a wide-range of buyers.Additionally, with the election forefront on everyone’s minds, we attempt to remindeveryone that changes in defense spending tend to be more gradual (regardless ofAdministration) than partisan voices account for.

As always, please feel free to reach out to either of us with any questions.

Sincerely,

Trevor Bohn Ryan MurphyPartner Partner

Table of Contents

I. KAL Capital OverviewI. KAL Capital Overview

III. Public Market & M&A SnapshotIII. Public Market & M&A Snapshot

IV. Commercial OEM FocusIV. Commercial OEM Focus

II. KAL Completes Sale of GeodeticsII. KAL Completes Sale of Geodetics

IV. Election: Trump vs. BidenIV. Election: Trump vs. Biden

A&D Sector

Knowledge

Transactions

Relationships

Clients

First

Team

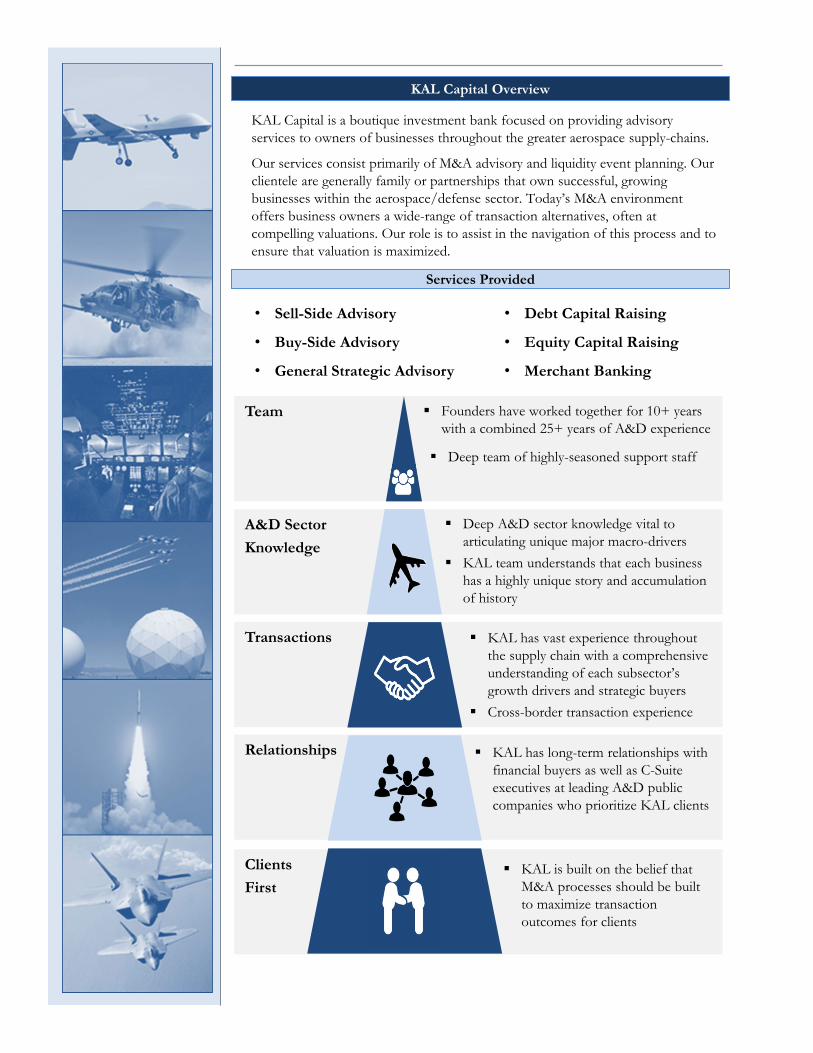

KAL Capital Overview

KAL Capital is a boutique investment bank focused on providing advisory services to owners of businesses throughout the greater aerospace supply-chains.

Our services consist primarily of M&A advisory and liquidity event planning. Our clientele are generally family or partnerships that own successful, growing businesses within the aerospace/defense sector. Today’s M&A environment offers business owners a wide-range of transaction alternatives, often at compelling valuations. Our role is to assist in the navigation of this process and to ensure that valuation is maximized.

KAL is built on the belief that M&A processes should be built to maximize transaction outcomes for clients

KAL has vast experience throughout the supply chain with a comprehensive understanding of each subsector’s growth drivers and strategic buyers

Cross-border transaction experience

KAL has long-term relationships with financial buyers as well as C-Suite executives at leading A&D public companies who prioritize KAL clients

Deep A&D sector knowledge vital to articulating unique major macro-drivers

KAL team understands that each business has a highly unique story and accumulation of history

Founders have worked together for 10+ years with a combined 25+ years of A&D experience

Deep team of highly-seasoned support staff

Services Provided

• Sell-Side Advisory

• Buy-Side Advisory

• General Strategic Advisory

• Debt Capital Raising

• Equity Capital Raising

• Merchant Banking

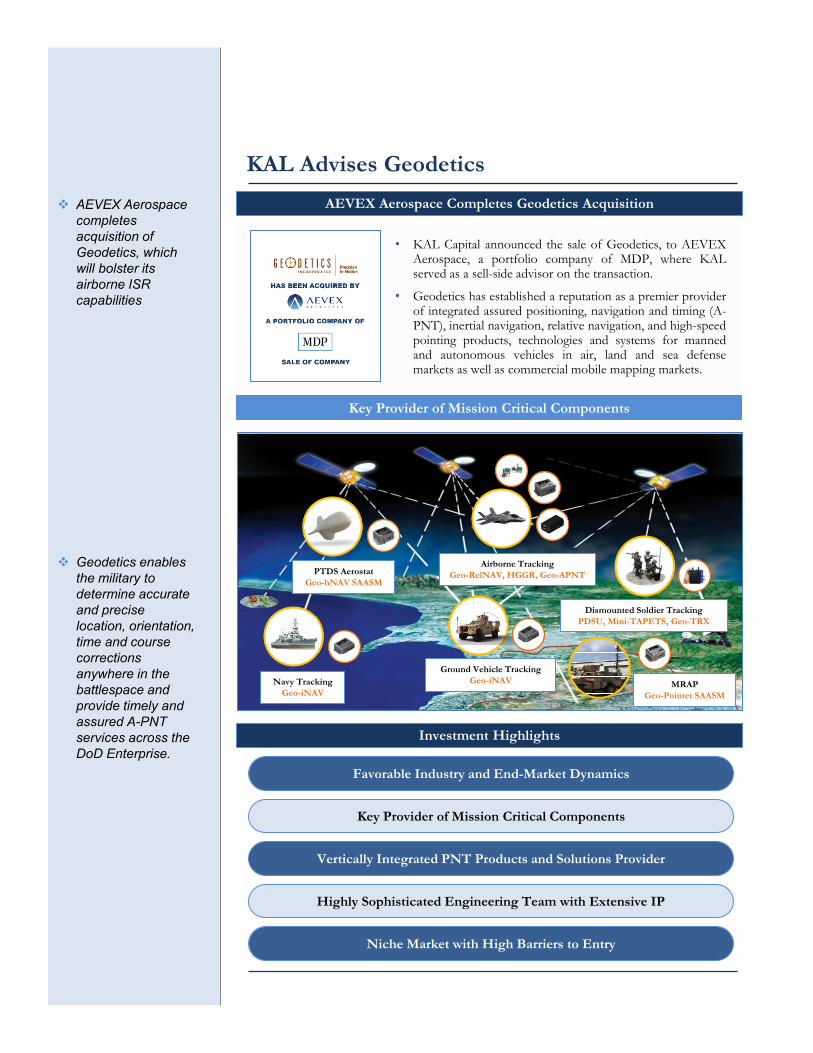

KAL Advises Geodetics

AEVEX Aerospace Completes Geodetics Acquisition

Geodetics enables the military to determine accurate and precise location, orientation, time and course corrections anywhere in the battlespace and provide timely and assured A-PNT services across the DoD Enterprise.

Key Provider of Mission Critical Components

Investment Highlights

Favorable Industry and End-Market Dynamics

Key Provider of Mission Critical Components

Vertically Integrated PNT Products and Solutions Provider

Highly Sophisticated Engineering Team with Extensive IP

Niche Market with High Barriers to Entry

• KAL Capital announced the sale of Geodetics, to AEVEXAerospace, a portfolio company of MDP, where KALserved as a sell-side advisor on the transaction.

• Geodetics has established a reputation as a premier providerof integrated assured positioning, navigation and timing (A-PNT), inertial navigation, relative navigation, and high-speedpointing products, technologies and systems for mannedand autonomous vehicles in air, land and sea defensemarkets as well as commercial mobile mapping markets.

Dismounted Soldier TrackingPDSU, Mini-TAPETS, Geo-TRX

Ground Vehicle Tracking Geo-iNAVNavy Tracking

Geo-iNAV

Airborne TrackingGeo-RelNAV, HGGR, Geo-APNT

MRAPGeo-Pointer SAASM

PTDS AerostatGeo-hNAV SAASM

AEVEX Aerospace completes acquisition of Geodetics, which will bolster its airborne ISR capabilities

Q3 Aerospace and Defense M&A Activity The M&A rotation from commercial assets to defense, space, & gov’t services assets continued in Q3

Public Market and M&A Snapshot

• M&A activity saw an encouraging uptick in Q3 as the industry attempts to recover fromthe strain that COVID-19 has placed on the economy, global air travel, and A&D supplychain. As such, the M&A trend towards defense companies has continued as buyers seekassets that are more insulated from the virus. KAL believes defense assets will continue toremain favorable as investors seek more stability.

Commercial aerospace stocks declined in Q3 due to covid-19 while defense stocks remained steady

Aerospace & Defense M&A Deal Activity YTD

Q3 Aerospace and Defense Public Market Activity

Q3 Share Price Performance

Company Q3 YTD

1.2% -12.1%

-9.8% -49.3%

-15.7% -42.0%

-7.4% -21.5%

5.0% -8.3%

0.1% -16.5%

-4.8% -9.6%

5.0% -1.6%

19.9% -25.5%

2.6% -8.3%

-6.6% -38.9%

-21.0% -74.1%

9.7% -19.1%

-27.7% -74.2%

• Commercial aerospace valuationspulled back in Q3 as the lack oftravel demand weighed heavily onthe supply chain.

• Boeing declined over the quarter asthe company reported lowerdelivery numbers, backlog ordersshrunk, and the 737 MAXremained grounded. Europe’s chiefaviation safety regulator saidBoeing’s 737 MAX could receiveregulatory approval to resumeflying in November and enterservice by the end of the year.Spirit, which generates more than75% of revenue from Boeing,followed suit and declined over thequarter.

• In contrast, defense companiesperformed relatively well over theperiod. Lockheed Martin andTextron gained nicely over thequarter after winning numerouscontracts.

6227 32

40

42 47

102

6980

020406080

100120

Q1 Q2 Q3

Commercial Defense, Space, & Gov't Services

Boeing will consolidate the B787 Dreamline production in South Carolina

Commercial OEM Focus

• Boeing and Airbus have slashed production rates and have announced additional lay offswill be necessary moving forward as demand remains suppressed due to the on-goingpandemic.

• Boeing announced it will consolidate the B787 Dreamliner production in South Carolinaas demand drops. In addition, Boeing has announced additional layoffs may be coming ontop of the 16,000 positions it previously announced it would eliminate.

• Airbus has cut production on several programs and is looking to hold underlying jetoutput at 40% below pre-pandemic plans for two years. They have committed to cutting15,000 jobs as production is expected to drop by 40% over the next two years.

Aviation has Proven Resilient Over and Over Again

Airbus is looking to hold underlying jet output at 40% below pre-pandemic plans for two years

Boeing and Airbus Slash Production and Announce Additional Layoffs

Boeing is confident the aviation industry will prove resilient and recover towards long-term growth within 3 years

OEMNet

Orders Deliveries Backlog

2020 YTD

Q3 2020 YoY%

2020 YTD YoY%

Q3 2020 YoY%

300 145 -20.3% 341 -40.3% 7,441 4.3%

-983 28 -55.6% 98 -67.5% 4,325 -21.4%

• Boeing’s latest commercial market outlook 2020-2039 paints an optimistic long-termprojection pointing to the industry’s ability to recover from demand shocks such as 9/11,SARS, and the global financial crisis. Top Boeing officials believe it will likely take aboutthree years for air travel to return to 2019 levels and a few years beyond that to return tolong-term growth trends.

0

2

4

6

8

10

12

1980 1990 2000 2010 2020

Actual RPK TrendSource: IATA

Rev

enue

Pas

seng

er K

ilom

eter

s ($

mm

)

9/11 and SARS

Global Financial CrisisCOVID-19 Pandemic

Scenario (RPKs)

Election Outcome is Unlikely to Drastically Impact The Defense Budget

Election: Trump vs. Biden

The biggest difference between Trump and Biden may be how they allocate the budget

The defense budget is likely to remain flat regardless of who is president

Peace Dividend

US Defense Budget Cycle Over Time

267 251 256 255 258 259 279 291 319246

438471 484

536602

673 665696 691

655585 596 571 587

619654

689 719 741 748 756 763

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

Clinton Obama Trump TBDBush

Sequestration

Downcycle1993-1998 = 0.9%

Upcycle1999-2010= 8.7%

Downcycle2011-2015= -(4.7)%

Upcycle2016-2021P= 4.8%

TBD

• Amid pandemic-related expenses and historic deficits, the budget is widely expected to stayrelatively flat regardless of who is president. Under Donald Trump, the Pentagon’s five-year defense plan indicates it will request flat defense spending after 2021. If Joe Bidenwins the election, budget cuts may be in order but would not constitute the deep cuts thata Sanders or Warren administration might have entailed. The biggest difference betweenTrump’s and Biden’s future defense budgets, many have speculated, won’t be the bottomline of total spending but how those dollars will be allocated.

• While Biden has statedhe doesn’t foreseedefense cuts if elected,he may face pressurefrom the left to make

them. To affordably deter Russia and China,Biden said he would shift investments from“legacy systems that won’t be relevant” to“smart investments in technologies andinnovations — including in cyber, space,unmanned systems and AI.”

- Joe Biden

• During Trump’s 4-year term as President,he championed recordnational defense toplines of $700 billion in

2018, $716 billion in 2019 and $733 billionfor 2020, and he created the new SpaceForce. Trump has emphasized rebuilding thecountry’s depleted military and vowed tobring US troops home from the Middle East.

– Donald Trump

Source: Defense News and Breaking Defense

This presentation has been prepared by KAL Capital Markets LLC (“KAL Capital”) for the exclusive use of the party to whom KAL Capital delivers thispresentation (together with its subsidiaries and affiliates, the “Recipient”) using publicly available information. KAL Capital has not independently verified theinformation contained herein, nor does Salem make any representation or warranty, either express or implied, as to the accuracy, completeness or reliability of theinformation contained in this presentation, or any other information (whether communicated in written or oral form) transmitted to or made available to theRecipient. Any estimates or projections as to events that may occur in the future (including projections of revenue, expense, net income and stock performance) arebased on publicly available information as of the date of this presentation. There is no guarantee that any of these estimates or projections will be achieved. Actualresults will vary from the projections and such variations may be material. Nothing contained herein is, or shall be relied upon as, a promise or representation as tothe past or future. KAL Capital expressly disclaims any and all liability relating to or resulting from the use of this presentation.

This presentation has been prepared solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or relatedfinancial instruments. The Recipient should not construe the contents of this presentation as legal, tax, accounting or investment advice or a recommendation. TheRecipient is urged to consult its own counsel, tax and financial advisors as to legal and related matters concerning any information described herein. Thispresentation does not purport to be all-inclusive or to contain all of the information that the Recipient may require. No investment, divestment or other financialdecisions or actions should be based solely on the information in this presentation. The Recipient should not rely on any information contained herein.

This presentation has been prepared on a confidential basis solely for the use and benefit of the Recipient. The Recipient agrees that the information containedherein and in all related and ancillary documents is not to be used for any other purpose, that such information is of a confidential nature and that Recipient willtreat it in a confidential manner. Distribution of this presentation to any person other than the Recipient and those persons retained to advise the Recipient whoagree to maintain the confidentiality of this material and be bound by the limitations outlined herein, is unauthorized without the prior consent of KAL Capital. Thismaterial must not be copied, reproduced, distributed or passed to others at any time without the prior written consent of KAL Capital.

Trevor BohnPartner

(949) [email protected]

Ryan MurphyPartner

(949) 404-4204 [email protected]

100 West BroadwaySuite 205

Long Beach, CA 90802www.kalcap.comP: (949) 404-4201