Ka Shui International | 822.HK China Puti Grow with ultrabooks

16

Page 1 of 16 26 March 2013 Susanna Chui [email protected] (852) 2235 7131 Trading data 52-Week Range (HK$) 3 Mth Avg Daily Vol (m) No of Shares (m) Market Cap (HK$m) Major Shareholders (%) Auditors Result Due 0.56/1.96 3.26 890.63 1,718.91 Lee Yuen Fat (68%) Directors (6%) RSM Nelson Wheeler 1H13: Aug Company description Established in 1980, Ka Shui is a leading manufacturer engaging in magnesium (for notebook cases), zinc (for household products and consumables), and aluminium (for household products and auto parts) alloy die casting components, and plastic (for smart device protective cases) injection moulding components. The company is currently the 4th magnesium alloy notebook case manufacturer in the Greater China, following Foxconn Technology (2354.TT), Juteng (3336.HK) and Catcher (2474.TT). Price chart - 0.50 1.00 1.50 2.00 2.50 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 HK$ Grow with ultrabooks Rating Buy Initiation Target Price HKD 2.42 Current price HKD 1.93 Upside +21% A leading magnesium alloy notebook case manufacturer Ka Shui is a leading die casting manufacturer, with a fast growing notebook casing manufacturing business. The company is currently the 4 th magnesium alloy notebook case manufacturer in the Greater China, following Foxconn Technology (2354.TT), Juteng (3336.HK) and Catcher (2474.TT). And its plastic injection business is worthy of attention. It supplies plastic smartphones and tablets protective cases for Otter, which is no. 1 selling case for smartphones in US. We believe these two segments will be the twin growth engine. Grow with ultrabooks 2013 is a better year for PC, with 12% of combined desktop, notebook and tablet unit sales growth, catalyzed by Windows 8. Especially ultrabooks will be one of the winners. It is because we notice ultrabook are moving into the mainstream PC price band of USD500-799. We expect ultrabook shipment will grow at 374%, representing 25% of the total notebooks in 2013. As magnesium casing is one of the best solutions for ultrabooks, Ka Shui’s magnesium alloy business can deliver strong growth on this wave. Play on smartphone and tablet adoption We see 2013 as another strong year for smartphones, with shipment growth rate of 40%. It is because adoption will go on, supported by continuous lower priced models and migration to 4G. As for tablets, tablet penetration rates will also accelerate and drive shipment to grow at 49% in 2013, as tablet prices come down with Apple’s iPad Mini. Therefore, we expect plastic smartphones and tablets protective cases will continue the growth momentum to the plastic injection moulding business. We initiate coverage on Ka Shui with BUY The company is trading at 10.1x FY13E PER, which is 20.1% lower than the average 12.6x of the peers (Foxconn Tech and Catcher are trading at 10.5x and 9.5x, lower than three-year-average 15.0x.and 12.7x, because of iPhone peaking and Apple’s supply chain competition). We believe the valuation discount will be narrowed given its best exposure to Lenovo (992.HK)’s market share gain and customer base expansion and customer base expansion. We initiate coverage with target price of HK$2.42, based on 12.6x FY13E PER. HKD million FY11A FY12A FY13E FY14E FY15E Revenue 1,192 1,569 2,064 2,585 3,054 Net Profit 63 126 170 216 253 Consensus NP 168 217 246 EPS (RMB) 0.07 0.14 0.19 0.24 0.28 P/E (x) 27.2 13.6 10.1 8.0 6.8 Dividend yield (%) 2.6 5.1 7.0 8.8 10.3 Sources: Bloomberg, CIRL estimates Ka Shui International | 822.HK China Puti

Transcript of Ka Shui International | 822.HK China Puti Grow with ultrabooks

Page 1 of 16

26 March 2013

Susanna Chui

(852) 2235 7131

Trading data

52-Week Range (HK$)

3 Mth Avg Daily Vol (m)

No of Shares (m)

Market Cap (HK$m)

Major Shareholders (%)

Auditors

Result Due

0.56/1.96

3.26

890.63

1,718.91

Lee Yuen Fat (68%)

Directors (6%)

RSM Nelson Wheeler

1H13: Aug Company description

Established in 1980, Ka Shui is a leading

manufacturer engaging in magnesium (for

notebook cases), zinc (for household products

and consumables), and aluminium (for household

products and auto parts) alloy die casting

components, and plastic (for smart device

protective cases) injection moulding components.

The company is currently the 4th magnesium

alloy notebook case manufacturer in the Greater

China, following Foxconn Technology (2354.TT),

Juteng (3336.HK) and Catcher (2474.TT).

Price chart

-

0.50

1.00

1.50

2.00

2.50

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

HK$

Grow with ultrabooks

Rating Buy Initiation

Target Price HKD 2.42

Current price

HKD 1.93 Upside +21%

A leading magnesium alloy notebook case manufacturer

Ka Shui is a leading die casting manufacturer, with a fast growing

notebook casing manufacturing business. The company is currently the

4th magnesium alloy notebook case manufacturer in the Greater China,

following Foxconn Technology (2354.TT), Juteng (3336.HK) and Catcher

(2474.TT). And its plastic injection business is worthy of attention. It

supplies plastic smartphones and tablets protective cases for Otter, which

is no. 1 selling case for smartphones in US. We believe these two

segments will be the twin growth engine.

Grow with ultrabooks

2013 is a better year for PC, with 12% of combined desktop, notebook

and tablet unit sales growth, catalyzed by Windows 8. Especially

ultrabooks will be one of the winners. It is because we notice ultrabook are

moving into the mainstream PC price band of USD500-799. We expect

ultrabook shipment will grow at 374%, representing 25% of the total

notebooks in 2013. As magnesium casing is one of the best solutions for

ultrabooks, Ka Shui’s magnesium alloy business can deliver strong

growth on this wave.

Play on smartphone and tablet adoption

We see 2013 as another strong year for smartphones, with shipment

growth rate of 40%. It is because adoption will go on, supported by

continuous lower priced models and migration to 4G. As for tablets, tablet

penetration rates will also accelerate and drive shipment to grow at 49% in

2013, as tablet prices come down with Apple’s iPad Mini. Therefore, we

expect plastic smartphones and tablets protective cases will continue the

growth momentum to the plastic injection moulding business.

We initiate coverage on Ka Shui with BUY

The company is trading at 10.1x FY13E PER, which is 20.1% lower than

the average 12.6x of the peers (Foxconn Tech and Catcher are trading at

10.5x and 9.5x, lower than three-year-average 15.0x.and 12.7x, because

of iPhone peaking and Apple’s supply chain competition). We believe the

valuation discount will be narrowed given its best exposure to Lenovo

(992.HK)’s market share gain and customer base expansion and

customer base expansion. We initiate coverage with target price of

HK$2.42, based on 12.6x FY13E PER.

HKD million FY11A FY12A FY13E FY14E FY15E

Revenue 1,192 1,569 2,064 2,585 3,054

Net Profit 63 126 170 216 253

Consensus NP 168 217 246

EPS (RMB) 0.07 0.14 0.19 0.24 0.28

P/E (x) 27.2 13.6 10.1 8.0 6.8

Dividend yield (%) 2.6 5.1 7.0 8.8 10.3

Sources: Bloomberg, CIRL estimates

Ka Shui International | 822.HK

China Puti

Page 2 of 16

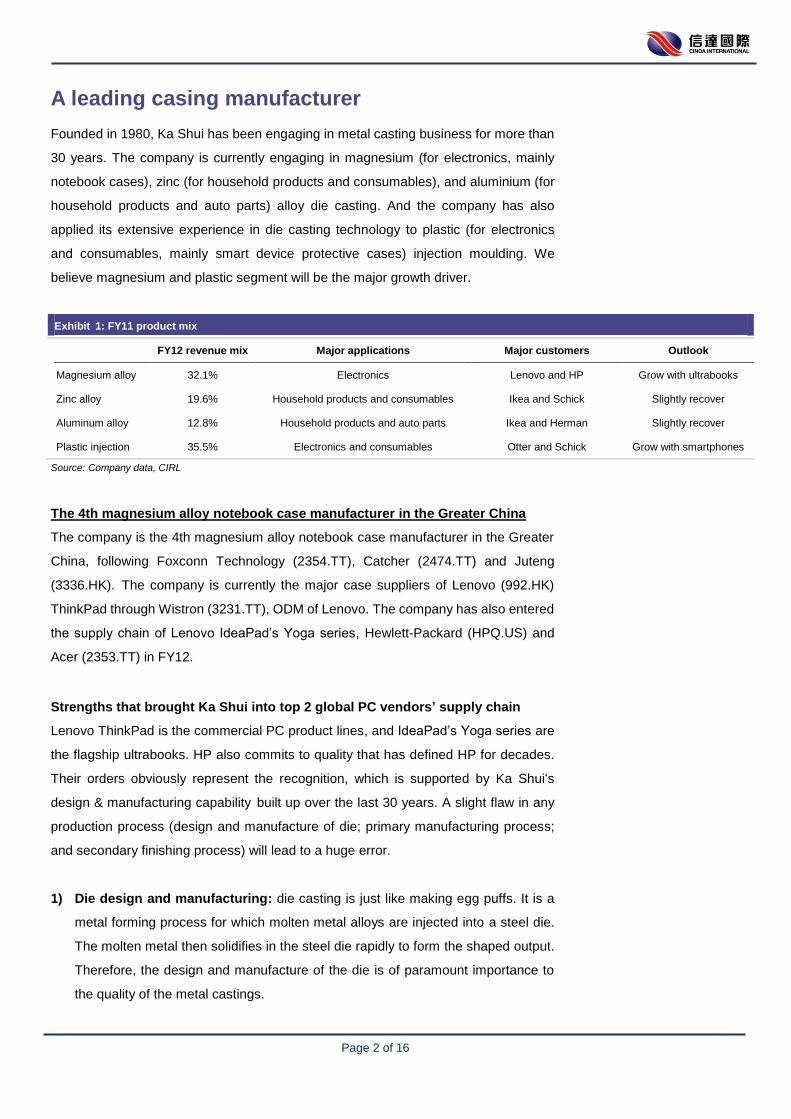

A leading casing manufacturer

Founded in 1980, Ka Shui has been engaging in metal casting business for more than

30 years. The company is currently engaging in magnesium (for electronics, mainly

notebook cases), zinc (for household products and consumables), and aluminium (for

household products and auto parts) alloy die casting. And the company has also

applied its extensive experience in die casting technology to plastic (for electronics

and consumables, mainly smart device protective cases) injection moulding. We

believe magnesium and plastic segment will be the major growth driver.

Exhibit 1: FY11 product mix

FY12 revenue mix Major applications Major customers Outlook

Magnesium alloy 32.1% Electronics Lenovo and HP Grow with ultrabooks

Zinc alloy 19.6% Household products and consumables Ikea and Schick Slightly recover

Aluminum alloy 12.8% Household products and auto parts Ikea and Herman Slightly recover

Plastic injection 35.5% Electronics and consumables Otter and Schick Grow with smartphones

Source: Company data, CIRL

The 4th magnesium alloy notebook case manufacturer in the Greater China

The company is the 4th magnesium alloy notebook case manufacturer in the Greater

China, following Foxconn Technology (2354.TT), Catcher (2474.TT) and Juteng

(3336.HK). The company is currently the major case suppliers of Lenovo (992.HK)

ThinkPad through Wistron (3231.TT), ODM of Lenovo. The company has also entered

the supply chain of Lenovo IdeaPad’s Yoga series, Hewlett-Packard (HPQ.US) and

Acer (2353.TT) in FY12.

Strengths that brought Ka Shui into top 2 global PC vendors’ supply chain

Lenovo ThinkPad is the commercial PC product lines, and IdeaPad’s Yoga series are

the flagship ultrabooks. HP also commits to quality that has defined HP for decades.

Their orders obviously represent the recognition, which is supported by Ka Shui‘s

design & manufacturing capability built up over the last 30 years. A slight flaw in any

production process (design and manufacture of die; primary manufacturing process;

and secondary finishing process) will lead to a huge error.

1) Die design and manufacturing: die casting is just like making egg puffs. It is a

metal forming process for which molten metal alloys are injected into a steel die.

The molten metal then solidifies in the steel die rapidly to form the shaped output.

Therefore, the design and manufacture of the die is of paramount importance to

the quality of the metal castings.

Page 3 of 16

2) Primary manufacturing process: the temperature, composition and flow of the

molten metal are kept under stringent control to avoid defects such as surface air

pockets and internal pores. And unsmoothness will increase difficulty in coloring

magnesium alloy, especially in light color. Yoga’s orange and silver color

represents Ka Shui’s strength in primary manufacturing process and also surface

treatment.

Exhibit 2: Lenovo IdeaPad’s Yoga in orange and silver color

Source: Company data, CIRL

3) Secondary manufacturing process: The die castings produced are subjected to

further processing, using CNC (computer controlled machine) machines—drilling,

scribing, lapping, etching, etc—to fine-tune shapes and make details on the piece

of metal. This requires a lot of experience to decide the best suitable tools to meet

the specifications as required by the customers.

Therefore, metal casing requires extensive experience. Ka Shui is founded in 1980,

engaging in metal casting business for more than 30 years. The experience and the

knowledge gained is obviously Ka Shui’s core competence. That is why it entered the

supply chain of Lenovo in FY05, and HP also started to allocate the order to the

company.

Page 4 of 16

Exhibit 3: Ka Shui’s metal die casting production process

Source: Company data, CIRL

Gaining order from the leaders

Foxconn Technology and Catcher, having three times more capacities than Ka Shui,

are clearly the leaders in the magnesium casing space. Ka Shui’s capacity is close to

Juteng and far more than other Chinese peers such as Dongguan Eonte (300328.CH).

Currently, the leaders focus more on aluminum unibody and allocate most of their

capacity to Apple (AAPL.US). Therefore, the second tier manufacturers such as

Juteng and Ka Shui are gaining order of non-apple camp such as HP, Lenovo, Dell

(DELL.US), Acer and Asus (2357.TT). We expect Ka Shui’s magnesium alloy

business can deliver strong growth on ultrabook wave and market share gain.

Exhibit 4: Major competitors, their customers and their capacities

Major metal casing customer Estimated capacity for magnesium case

Foxconn Tech Apple 2,000 kpcs

Catcher Apple 2,000 kpcs

Juteng Dell and Samsung 600 kpcs

Ka Shui Lenovo and HP 500 kpcs

Source: Company data, CIRL

Post processing

Surface finishing treatment

Post machining (i.e. CNC machining)

Primary manufacturing process

Injection of molten metal into a steel die

Solidification of molten metal

Melting of metal alloy ingots

Die design and manufacturing

Secondary manufacturing process

Page 5 of 16

Call option on potential handset metal casing business

Ka Shui is developing new applications based on its core die casting technology. The

company is exploring opportunities in handset metal casing. The company has

approached several smartphone vendors, and set up a JV with Shenzhen

Dongweifeng Electronic Technology and Shenzhen On Xun Electronic for developing

the new business. We believe handset metal casing business can be potentially a new

explosive growth driver for the company.

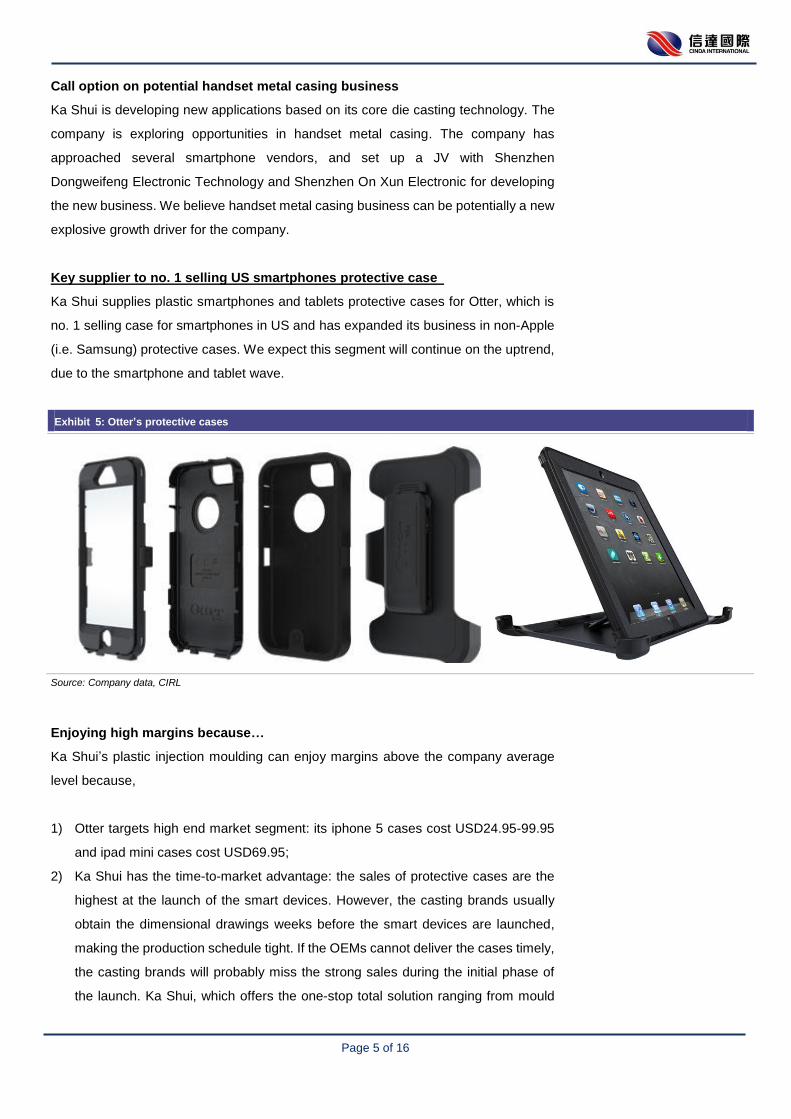

Key supplier to no. 1 selling US smartphones protective case

Ka Shui supplies plastic smartphones and tablets protective cases for Otter, which is

no. 1 selling case for smartphones in US and has expanded its business in non-Apple

(i.e. Samsung) protective cases. We expect this segment will continue on the uptrend,

due to the smartphone and tablet wave.

Exhibit 5: Otter’s protective cases

Source: Company data, CIRL

Enjoying high margins because…

Ka Shui’s plastic injection moulding can enjoy margins above the company average

level because,

1) Otter targets high end market segment: its iphone 5 cases cost USD24.95-99.95

and ipad mini cases cost USD69.95;

2) Ka Shui has the time-to-market advantage: the sales of protective cases are the

highest at the launch of the smart devices. However, the casting brands usually

obtain the dimensional drawings weeks before the smart devices are launched,

making the production schedule tight. If the OEMs cannot deliver the cases timely,

the casting brands will probably miss the strong sales during the initial phase of

the launch. Ka Shui, which offers the one-stop total solution ranging from mould

Page 6 of 16

design & manufacturing to plastic injection, has the time-to-market advantage

over other competitors; and

3) Ka Shui has a track record in secrecy: To prevent competitors’ preemption and

plagiarization, secrecy is the key consideration for the casting brands to choose

suppliers. Ka Shui, with a track record in keeping the dimensional drawings

confidential and protecting the intellectual property, thus cannot be easily

replaced by other new comers.

Stable zinc and aluminum alloy business

Zinc alloy business’ major applications are household products and consumables,

with IKEA and Schick as its major clients. As for aluminum alloy business, household

products and auto parts are the major application. Major customers include IKEA and

Herman (HAR.US, a global leader in automotive infotainment with known customers

such as BMW and Audi). The revenue of these two segments has decreased 12.1%

and 20.5% yoy respectively in FY12, amid the global economic slowdown. However,

according to IKEA’s guidance, the management has expected the situation will be

improved following a gradual market recovery.

Exhibit 6: Zinc and aluminum alloy business

Source: IKEA,Schick, Harman, CIRL

Page 7 of 16

Grow with ultrabooks

2013 is a better year for PC, catalyzed by Microsoft’s Windows 8 (first touch-capable

OS unified across mobile and PC). New Windows OS always stimulates PC shipment

growth in the following year as users await new product and postpone purchases.

Thus Windows 8 will be a positive catalyst for PC in 2013. We expect combined

desktop, notebook and tablet unit sales growth is 12% in 2013.

Exhibit 7: PC Shipment (mn units)

Source: IDC, IHS iSuppli, CIRL

There is no big demand problem, but the market is playing musical chairs. Tablet

substitution for notebooks (especially low-end consumer market) will likely accelerate,

with Apple stepping down the price curve with iPad Mini, cheaper Android tablets, and

Windows 8 also supporting the tablet form factor. We expect the shipment of tablets

will go head to head with notebooks in 2013.

Yet ultrabooks taking off

Struggling to compete with tablets, PC manufacturers are aggressively pushing

ultrabooks with thinner form factors, extended battery life, better performance and

even touch panels. And at current price points of USD600 and up, ultrabooks are not

only taking over the high/mid-range of PC price band of > USD800 (25% of notebook

units), but moving into the mainstream PC price band of USD500-799 (47% of

notebook units). We believe ultrabook shipment will grow at 374%, representing 25%

of the total notebooks in 2013.

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

-

100

200

300

400

500

600

700

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

E

20

14

E

20

15

Desktop Notebook (ex ultrabook)

Ultrabook Tablets

yoy

Win XP

Win Vista

Win 7

Win 8

Page 8 of 16

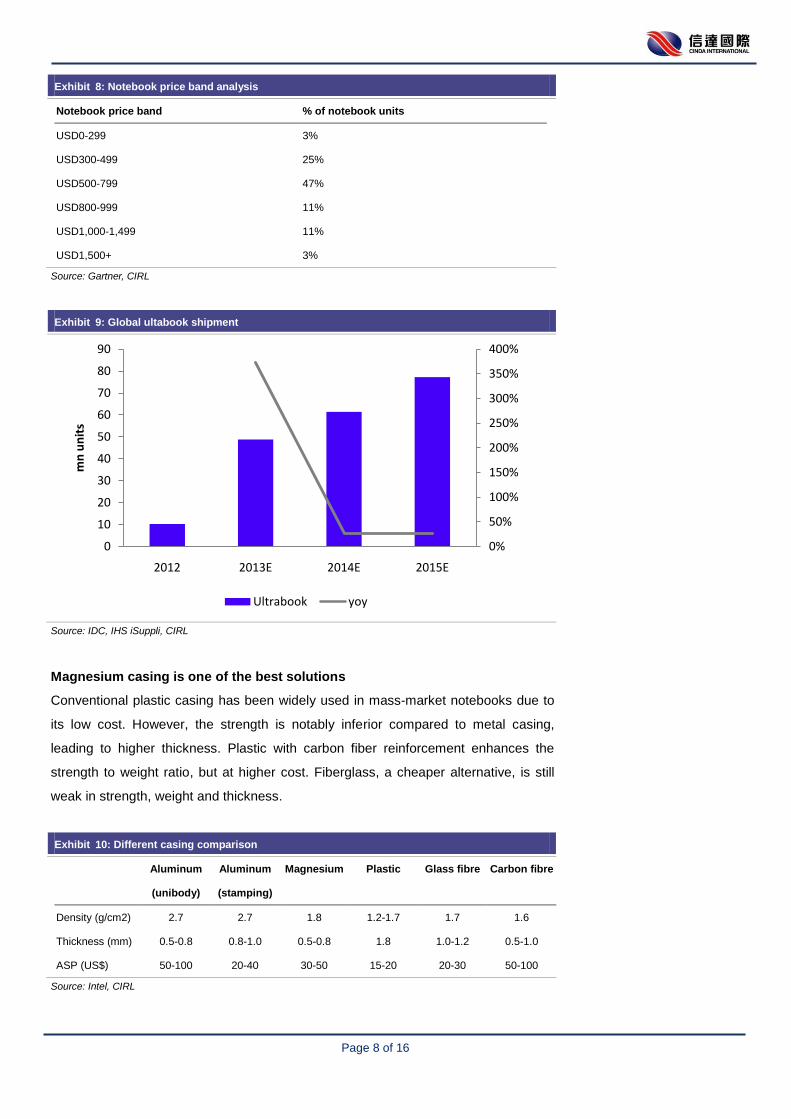

Exhibit 8: Notebook price band analysis

Notebook price band % of notebook units

USD0-299 3%

USD300-499 25%

USD500-799 47%

USD800-999 11%

USD1,000-1,499 11%

USD1,500+ 3%

Source: Gartner, CIRL

Exhibit 9: Global ultabook shipment

Source: IDC, IHS iSuppli, CIRL

Magnesium casing is one of the best solutions

Conventional plastic casing has been widely used in mass-market notebooks due to

its low cost. However, the strength is notably inferior compared to metal casing,

leading to higher thickness. Plastic with carbon fiber reinforcement enhances the

strength to weight ratio, but at higher cost. Fiberglass, a cheaper alternative, is still

weak in strength, weight and thickness.

Exhibit 10: Different casing comparison

Aluminum

(unibody)

Aluminum

(stamping)

Magnesium Plastic Glass fibre Carbon fibre

Density (g/cm2) 2.7 2.7 1.8 1.2-1.7 1.7 1.6

Thickness (mm) 0.5-0.8 0.8-1.0 0.5-0.8 1.8 1.0-1.2 0.5-1.0

ASP (US$) 50-100 20-40 30-50 15-20 20-30 50-100

Source: Intel, CIRL

0%

50%

100%

150%

200%

250%

300%

350%

400%

0

10

20

30

40

50

60

70

80

90

2012 2013E 2014E 2015E

mn

un

its

Ultrabook yoy

Page 9 of 16

Instead metal casing has several key advantages such as lightweight, better heat

dissipation, and better structural support. It was mostly found in high-end products

such as commercial notebooks in earlier times. Apple is the first brand that widely

uses metal across consumer products such as iPod, Macs, iPad and iPhone 5. To

mimic Apple’s success, other brands started to increase the metal content in their

products such as notebooks, tablets and smartphones. We believe the trend of thinner

and lighter portable PC (Intel (INTC.US) has shown how an ultrabook that is 15mm

thick at its thickest point in its 2012 annual conference), will definitely lead to growing

demand for metal casing.

Exhibit 11: Ultrabooks getting thinner and lighter

Source: Intel, CIRL

Among different metal casing, aluminum unibody are extremely thin and lightweight,

but at high cost. They are processed by CNC machines, which cost over million each

and only produce single digit units of unibody frame per hour. Aluminum stamping is a

cheaper solution, but in inferior thickness level.

Instead magnesium casing is competitive in the cost-performance aspect, given its

advantage of weight and thickness, and cost advantage versus aluminum unibody.

The casing will be formed by metal liquid through the injection moulding, and then be

processed by CNC machines for fine tuning. Magnesium casing thus reduces reliance

on CNC machines, and increases output with cheaper costs versus aluminum

unibody.

As magnesium casing is one of the best solutions for ultrabooks, Ka Shui’s

magnesium alloy business can deliver strong growth on the increasing magnesium

casing adoption in ultrabooks. We expect Ka Shui’s revenue from magnesium alloy

die casting will deliver 75.5% growth in FY13E.

Page 10 of 16

Play on smartphone and tablet adoption

The global smartphone shipments rose from 482mn units in 2011 to 698mn units in

2012, up 45%. We see 2013 as another strong growth year for smartphones, with

shipment growth rate of 40%, Developed markets’ penetration rates are high (47% in

North America and 40% in Western Europe), supporting replacement sales. On the

other hand, the new adoption will be driven by the demand from emerging markets

with low penetration rates of 7%-15%. Penetration moves higher, triggered by a

combination of lower priced models and migration to 4G.

Exhibit 12: Global mobile phone shipments

Source: IDC, CIRL

Exhibit 13: 2012 smartphones penetration

Source: IDC, CIRL

0

50

100

150

200

250

300

350

1Q

20

09

2Q

20

09

3Q

20

09

4Q

20

09

1Q

20

10

2Q

20

10

3Q

20

10

4Q

20

10

1Q

20

11

2Q

20

11

3Q

20

11

4Q

20

11

1Q

20

12

2Q

20

12

3Q

20

12

4Q

20

12

mn

un

its

Non-smartphone Smartphone

47%

40%

50%

15% 13%10%

7%

17%

0%

10%

20%

30%

40%

50%

60%

North America

Western Europe

Japan APAC (ex Japan)

Latin America

Eastern Europe

Middle East & Africa

Global

Page 11 of 16

As for tablets, the global shipments rose from 71mn units in 2011 to 117mn units in

2012, up 65%. We believe that the tablet market is still in the early stages of growth.

So far tablet growth has been mostly limited to customers in developed countries, who

can afford to pay >US$500 for an iPad. The tablet penetration rates in North Amercia

and Western Europe are even still 15% and 8%, while those in other developing

countries are almost 0%. But as tablet prices come down with Apple’s iPad Mini, we

believe tablet penetration rates will accelerate and drive shipment to grow at 49% in

2013.

And we appreciate Otter’s product line expansion to non-Apple (i.e. Samsung)

protective cases. However, we are conservative to the execution and expect Ka Shui’s

revenue from plastic injection moulding will deliver 18.0% growth in FY13E.

Exhibit 14: 2012 tablet penetration

Source: IDC, CIRL

Exhibit 15: Global smartphone and tablet shipement

Source: IDC, CIRL

15%

8%

3%

1% 1%0% 0%

2%0%

2%

4%

6%

8%

10%

12%

14%

16%

North Amercia

Western Europe

Japan Eastern Europe

Latin America

APAC (ex Japan)

Middle East & Africa

Global

0%

50%

100%

150%

200%

250%

300%

-

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013E 2014E 2015E

mn

un

its

Tablets Smartphone

Tablets growth yoy Smartphone growth yoy

Page 12 of 16

Product mix shift positive to margins

Riding on the booming ultrabook market, magnesium segment will outgrow other

segment. Following the increase in proportion of magnesium segment from 32.1% in

FY12 to 51.0% in FY15E, the overall GPM will be pulled up because,

1) the GPM of magnesium segment will be stable or even on the uptrend, on the

back of its new customer, such as HP, offering higher margins.

2) the GPM of magnesium segment s 25.8%, above 22.4% of company average in

FY12, on the back of the stricter requirements compared with other products such

as household products and consumables.

Exhibit 16: Ka Shui’s product mix

Source: Company data, CIRL

Exhibit 17: Ka Shui’s margins trend

FY12 GPM FY13E outlook

Zinc alloy 15.0% Slightly improve following a gradual market recovery.

Magnesium alloy 25.8% Stable or even on uptrend: the company has entered the supply chain of HP offering higher margins

Aluminum alloy 18.7% Slightly improve following a gradual market recovery.

Plastic injection 25.9% Stable or even on uptrend: adding non-Apple protective cases to Otter’s current product line can make

the company utilize the capacity evenly over the year.

Source: Company data, CIRL

29%20% 15% 13% 11%

24%32% 43% 48% 51%

21%13%

10% 8% 7%

25%35% 32% 31% 31%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY11A FY12A FY13E FY14E FY15E

Zinc alloy die casting components Magnesium alloy die casting

Aluminium alloy die casting Plastic injection moulding

Page 13 of 16

Financial analysis and valuation

Ka Shui reported a strong FY12 results with increase of 31.7% yoy in revenue and

100.4% in net profit, driven by magnesium alloy die casting and plastic injection

moulding businesses. GPM has improved by 3.1pts to 22.5%, because the

fast-growing magnesium alloy die casting and plastic injection moulding businesses

has enjoyed higher margin, rising with economies of scale.

We forecast revenue to grow by 31.6%/25.2%/18.1% for FY13E/FY14E/FY15E

mainly driven by 1) the growth of ultrabooks, smartphones and tablets; and 2) rising

magnesium casing adoption in smart devices; and 3) obtaining new customers, such

as HP and Acer.

GPM keeps uptrend at above 23% because 1) the GPM of fast-growing magnesium

segment will be stable or even on the uptrend, on the back of its new customer, such

as HP, offering higher margins; and 2) the GPM of magnesium segment s 25.8%,

above 22.4% of company average in FY12, on the back of the stricter requirements.

SG&A expense will increase to 12.8% in FY13E-FY15E, on the back of developing

new business. We expect that net profit will rise 35.4%/26.6%/17.4% to HKD170.4,m/

HKD215.7mn/ HKD253.4mn in FY13E/FY14E/FY15E.

Payout will maintain a ~70.0% of net profit in FY13E-FY15E representing 7.0% of

FY13E dividend yield, the highest compared with the peers. The company has

maintained a stable cash dividend payout of 70.0-75.0% since FY09.

We initiate coverage on Ka Shui with BUY. The company is trading at 9.4x FY13E

PER, which is 20.1% lower than the average 12.6x of the peers (Foxconn Tech and

Catcher are trading at 10.5x and 9.5x, lower than three-year-average 15.0x.and 12.7x,

because of iPhone peaking and fears of competition in Apple’s supply chain). Though

Juteng and Tongda (698.HK) are trading at 7.9x and 6.6x FY13E PER, we attribute

the lower valuation to their exposure to the plastic casing business. We believe the

valuation discount will be narrowed given its best exposure to Lenovo’s market share

gain and customer base expansion. We initiate coverage on the stock with target price

of HK$2.42, based on 12.6x FY13E PER.

Page 14 of 16

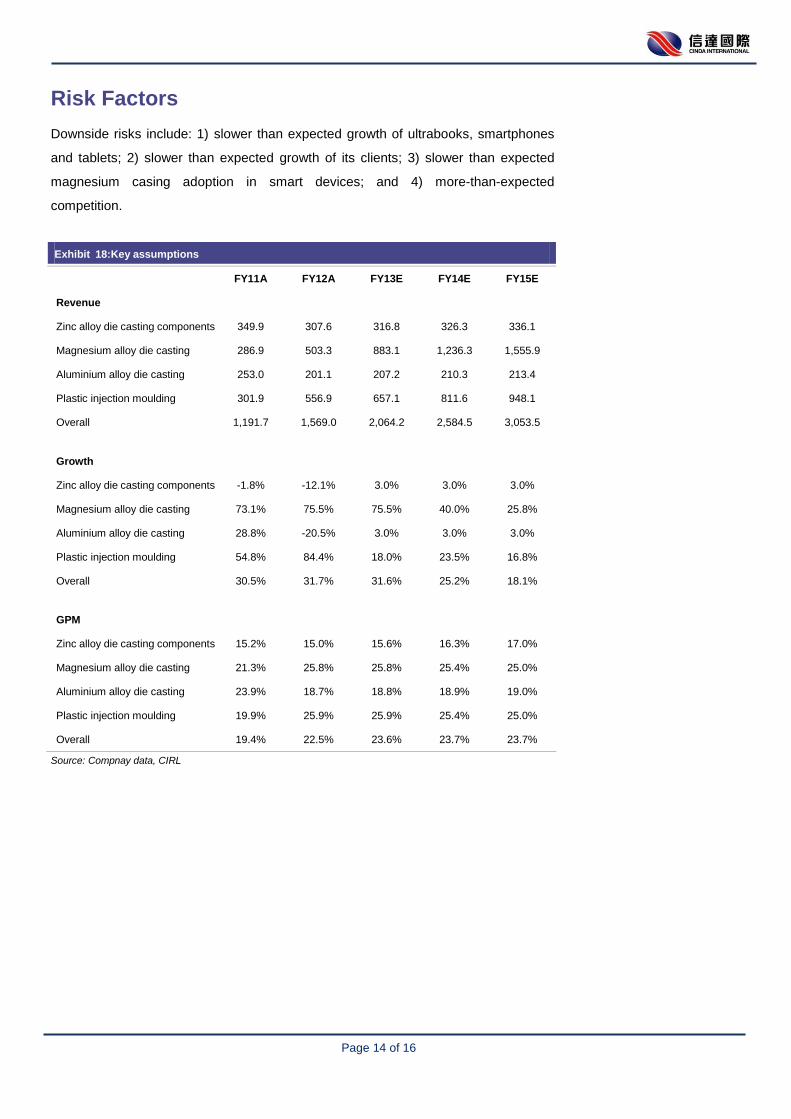

Risk Factors

Downside risks include: 1) slower than expected growth of ultrabooks, smartphones

and tablets; 2) slower than expected growth of its clients; 3) slower than expected

magnesium casing adoption in smart devices; and 4) more-than-expected

competition.

Exhibit 18:Key assumptions

FY11A FY12A FY13E FY14E FY15E

Revenue

Zinc alloy die casting components 349.9 307.6 316.8 326.3 336.1

Magnesium alloy die casting 286.9 503.3 883.1 1,236.3 1,555.9

Aluminium alloy die casting 253.0 201.1 207.2 210.3 213.4

Plastic injection moulding 301.9 556.9 657.1 811.6 948.1

Overall 1,191.7 1,569.0 2,064.2 2,584.5 3,053.5

Growth

Zinc alloy die casting components -1.8% -12.1% 3.0% 3.0% 3.0%

Magnesium alloy die casting 73.1% 75.5% 75.5% 40.0% 25.8%

Aluminium alloy die casting 28.8% -20.5% 3.0% 3.0% 3.0%

Plastic injection moulding 54.8% 84.4% 18.0% 23.5% 16.8%

Overall 30.5% 31.7% 31.6% 25.2% 18.1%

GPM

Zinc alloy die casting components 15.2% 15.0% 15.6% 16.3% 17.0%

Magnesium alloy die casting 21.3% 25.8% 25.8% 25.4% 25.0%

Aluminium alloy die casting 23.9% 18.7% 18.8% 18.9% 19.0%

Plastic injection moulding 19.9% 25.9% 25.9% 25.4% 25.0%

Overall 19.4% 22.5% 23.6% 23.7% 23.7%

Source: Compnay data, CIRL

Page 15 of 16

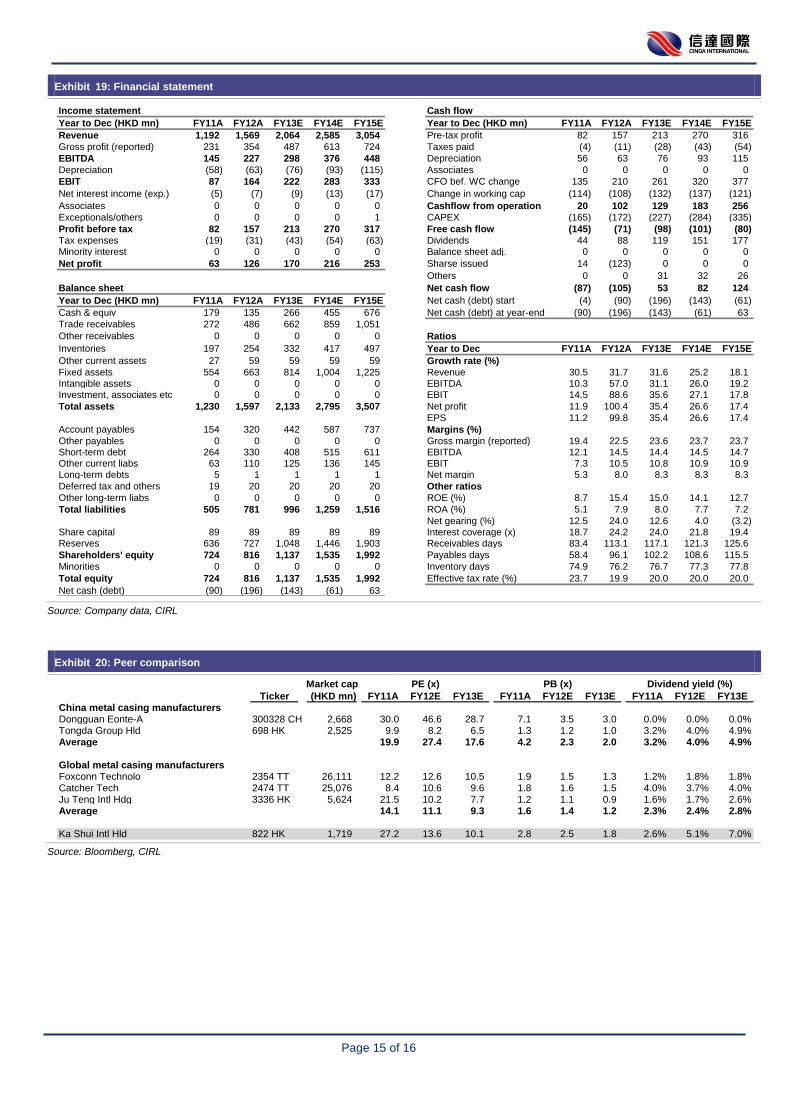

Exhibit 19: Financial statement

Source: Company data, CIRL

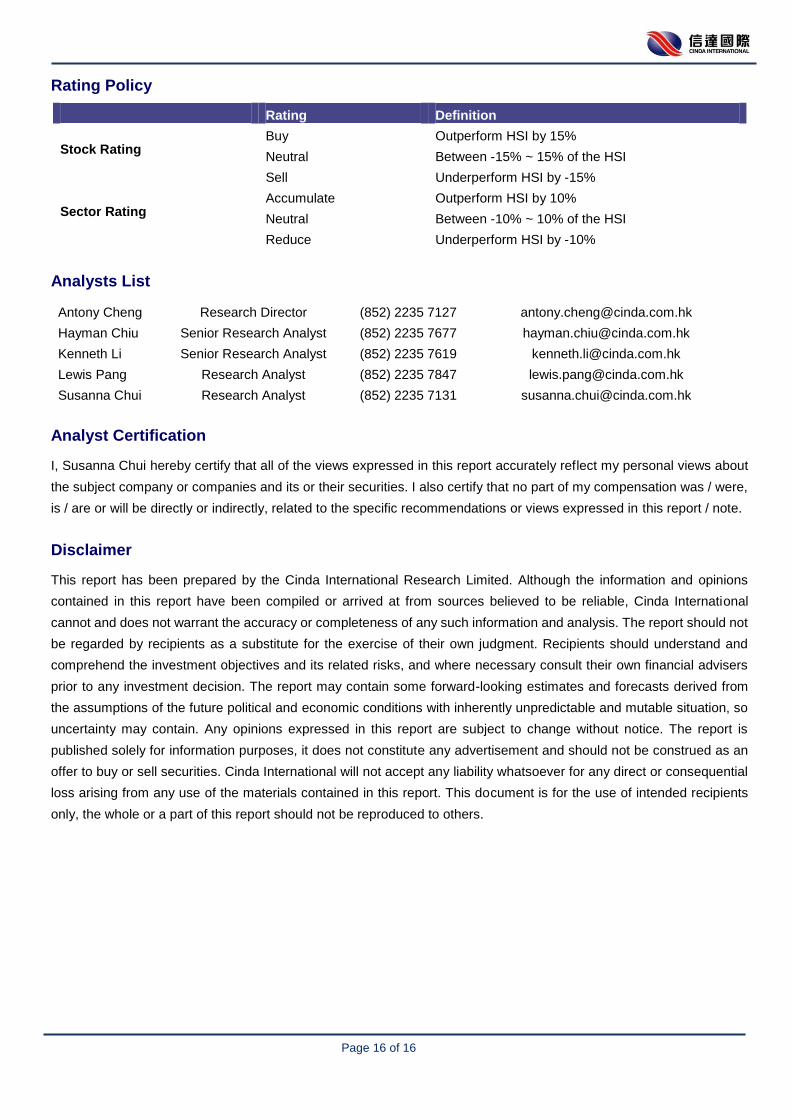

Exhibit 20: Peer comparison

Source: Bloomberg, CIRL

Income statement Cash flow

Year to Dec (HKD mn) FY11A FY12A FY13E FY14E FY15E Year to Dec (HKD mn) FY11A FY12A FY13E FY14E FY15E

Revenue 1,192 1,569 2,064 2,585 3,054 Pre-tax profit 82 157 213 270 316

Gross profit (reported) 231 354 487 613 724 Taxes paid (4) (11) (28) (43) (54)

EBITDA 145 227 298 376 448 Depreciation 56 63 76 93 115

Depreciation (58) (63) (76) (93) (115) Associates 0 0 0 0 0

EBIT 87 164 222 283 333 CFO bef. WC change 135 210 261 320 377

Net interest income (exp.) (5) (7) (9) (13) (17) Change in working cap (114) (108) (132) (137) (121)

Associates 0 0 0 0 0 Cashflow from operation 20 102 129 183 256

Exceptionals/others 0 0 0 0 1 CAPEX (165) (172) (227) (284) (335)

Profit before tax 82 157 213 270 317 Free cash flow (145) (71) (98) (101) (80)

Tax expenses (19) (31) (43) (54) (63) Dividends 44 88 119 151 177Minority interest 0 0 0 0 0 Balance sheet adj. 0 0 0 0 0

Net profit 63 126 170 216 253 Sharse issued 14 (123) 0 0 0

Others 0 0 31 32 26

Balance sheet Net cash flow (87) (105) 53 82 124

Year to Dec (HKD mn) FY11A FY12A FY13E FY14E FY15E Net cash (debt) start (4) (90) (196) (143) (61)

Cash & equiv 179 135 266 455 676 Net cash (debt) at year-end (90) (196) (143) (61) 63

Trade receivables 272 486 662 859 1,051

Other receivables 0 0 0 0 0 Ratios

Inventories 197 254 332 417 497 Year to Dec FY11A FY12A FY13E FY14E FY15E

Other current assets 27 59 59 59 59 Growth rate (%)

Fixed assets 554 663 814 1,004 1,225 Revenue 30.5 31.7 31.6 25.2 18.1Intangible assets 0 0 0 0 0 EBITDA 10.3 57.0 31.1 26.0 19.2Investment, associates etc 0 0 0 0 0 EBIT 14.5 88.6 35.6 27.1 17.8

Total assets 1,230 1,597 2,133 2,795 3,507 Net profit 11.9 100.4 35.4 26.6 17.4

EPS 11.2 99.8 35.4 26.6 17.4

Account payables 154 320 442 587 737 Margins (%)

Other payables 0 0 0 0 0 Gross margin (reported) 19.4 22.5 23.6 23.7 23.7Short-term debt 264 330 408 515 611 EBITDA 12.1 14.5 14.4 14.5 14.7Other current liabs 63 110 125 136 145 EBIT 7.3 10.5 10.8 10.9 10.9Long-term debts 5 1 1 1 1 Net margin 5.3 8.0 8.3 8.3 8.3

Deferred tax and others 19 20 20 20 20 Other ratios

Other long-term liabs 0 0 0 0 0 ROE (%) 8.7 15.4 15.0 14.1 12.7

Total liabilities 505 781 996 1,259 1,516 ROA (%) 5.1 7.9 8.0 7.7 7.2

Net gearing (%) 12.5 24.0 12.6 4.0 (3.2)Share capital 89 89 89 89 89 Interest coverage (x) 18.7 24.2 24.0 21.8 19.4Reserves 636 727 1,048 1,446 1,903 Receivables days 83.4 113.1 117.1 121.3 125.6

Shareholders' equity 724 816 1,137 1,535 1,992 Payables days 58.4 96.1 102.2 108.6 115.5

Minorities 0 0 0 0 0 Inventory days 74.9 76.2 76.7 77.3 77.8

Total equity 724 816 1,137 1,535 1,992 Effective tax rate (%) 23.7 19.9 20.0 20.0 20.0

Net cash (debt) (90) (196) (143) (61) 63

Market cap PE (x) PB (x) Dividend yield (%)

Ticker (HKD mn) FY11A FY12E FY13E FY11A FY12E FY13E FY11A FY12E FY13EChina metal casing manufacturersDongguan Eonte-A 300328 CH 2,668 30.0 46.6 28.7 7.1 3.5 3.0 0.0% 0.0% 0.0%Tongda Group Hld 698 HK 2,525 9.9 8.2 6.5 1.3 1.2 1.0 3.2% 4.0% 4.9%Average 19.9 27.4 17.6 N/A 4.2 2.3 2.0 3.2% 4.0% 4.9%

Global metal casing manufacturersFoxconn Technolo 2354 TT 26,111 12.2 12.6 10.5 1.9 1.5 1.3 1.2% 1.8% 1.8%Catcher Tech 2474 TT 25,076 8.4 10.6 9.6 1.8 1.6 1.5 4.0% 3.7% 4.0%Ju Teng Intl Hdg 3336 HK 5,624 21.5 10.2 7.7 1.2 1.1 0.9 1.6% 1.7% 2.6%Average 14.1 11.1 9.3 N/A 1.6 1.4 1.2 2.3% 2.4% 2.8%

Ka Shui Intl Hld 822 HK 1,719 27.2 13.6 10.1 2.8 2.5 1.8 2.6% 5.1% 7.0%

Page 16 of 16

Rating Policy

Rating Definition

Stock Rating Buy Outperform HSI by 15%

Neutral Between -15% ~ 15% of the HSI

Sell Underperform HSI by -15%

Sector Rating Accumulate Outperform HSI by 10%

Neutral Between -10% ~ 10% of the HSI

Reduce Underperform HSI by -10%

Analysts List

Antony Cheng Research Director (852) 2235 7127 [email protected]

Hayman Chiu Senior Research Analyst (852) 2235 7677 [email protected]

Kenneth Li Senior Research Analyst (852) 2235 7619 [email protected]

Lewis Pang Research Analyst (852) 2235 7847 [email protected]

Susanna Chui Research Analyst (852) 2235 7131 [email protected]

Analyst Certification

I, Susanna Chui hereby certify that all of the views expressed in this report accurately reflect my personal views about

the subject company or companies and its or their securities. I also certify that no part of my compensation was / were,

is / are or will be directly or indirectly, related to the specific recommendations or views expressed in this report / note.

Disclaimer

This report has been prepared by the Cinda International Research Limited. Although the information and opinions

contained in this report have been compiled or arrived at from sources believed to be reliable, Cinda International

cannot and does not warrant the accuracy or completeness of any such information and analysis. The report should not

be regarded by recipients as a substitute for the exercise of their own judgment. Recipients should understand and

comprehend the investment objectives and its related risks, and where necessary consult their own financial advisers

prior to any investment decision. The report may contain some forward-looking estimates and forecasts derived from

the assumptions of the future political and economic conditions with inherently unpredictable and mutable situation, so

uncertainty may contain. Any opinions expressed in this report are subject to change without notice. The report is

published solely for information purposes, it does not constitute any advertisement and should not be construed as an

offer to buy or sell securities. Cinda International will not accept any liability whatsoever for any direct or consequential

loss arising from any use of the materials contained in this report. This document is for the use of intended recipients

only, the whole or a part of this report should not be reproduced to others.