June 2008 KeyBanc Conference - IIS Windows...

38

June 2008 KeyBanc Conference Brady Investor Presentation 1

Transcript of June 2008 KeyBanc Conference - IIS Windows...

June 2008 KeyBanc Conference

Brady Investor Presentation

1

Forward-Looking Statements

We believe that certain statements in this presentation are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All statements related to future, not past, events included in this presentation, including, without limitation, statements regarding our future financial position, business strategy, targets, projected sales, costs, earnings, capital expenditures, debt levels and cash flows, and plans and objectives of management for future operations are forward-looking statements. When used in this presentation, words such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “should,” “project” or “plan” or similar terminology are generally intended to identify forward-looking statements. These forward-looking statements by their nature address matters that are, to different degrees, uncertain and are subject to risks, assumptions and other factors, some of which are beyond our control, that could cause actual results to differ materially from those expressed or implied by such forward-looking statements. For us, uncertainties arise from future financial performance of major markets we serve, which include, without limitation, telecommunications, manufacturing, electrical, construction, laboratory, education, governmental, public utility, computer, transportation; difficulties in making and integrating acquisitions; risks associated with newly acquired businesses; our ability to retain significant contracts and customers; future competition; our ability to develop and successfully market new products; changes in the supply of, or price for, parts and components; increased price pressure from suppliers and customers; interruptions to sources of supply; environmental, health and safety compliance costs and liabilities; our ability to realize cost savings from operating initiatives; our ability to attract and retain key talent; difficulties associated with exports; risks associated with international operations; fluctuations in currency rates versus the US dollar; technology changes; potential write-offs of our substantial intangible assets; risks associated with obtaining governmental approvals and maintaining regulatory compliance for new and existing products; business interruptions due to implementing business systems; and numerous other matters of national, regional and global scale, including those of a political, economic, business, competitive and regulatory nature contained from time to time in our U.S. Securities and Exchange Commission filings, including, but not limited to, those factors listed in the "Risk Factors" section located in Item 1A of Part II of our Form 10-K for the period ended July 31, 2007. These uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements.

We refer to certain non-GAAP financial measures in this presentation. Reconciliations of these non-GAAP financial measures to the most directly comparable GAAP financial measures can be found within this presentation.

2

Brady’s Mission

We identify and protect premises, products and people

3

Products

• With state of the art clean rooms and the latest in die-cut technology, Brady provides custom-designed products that seal, insulate, protect, shield or otherwise enhance mechanical performance.

Die Cut Wire Identification

• Brady’s labels, sleeves, printers and software provide the total labeling and documentation solution for wire identification

• Brady’s safety & facility products help customers create and maintain safer work environments and comply with regulatory standards.

Facility and Safety

Identification

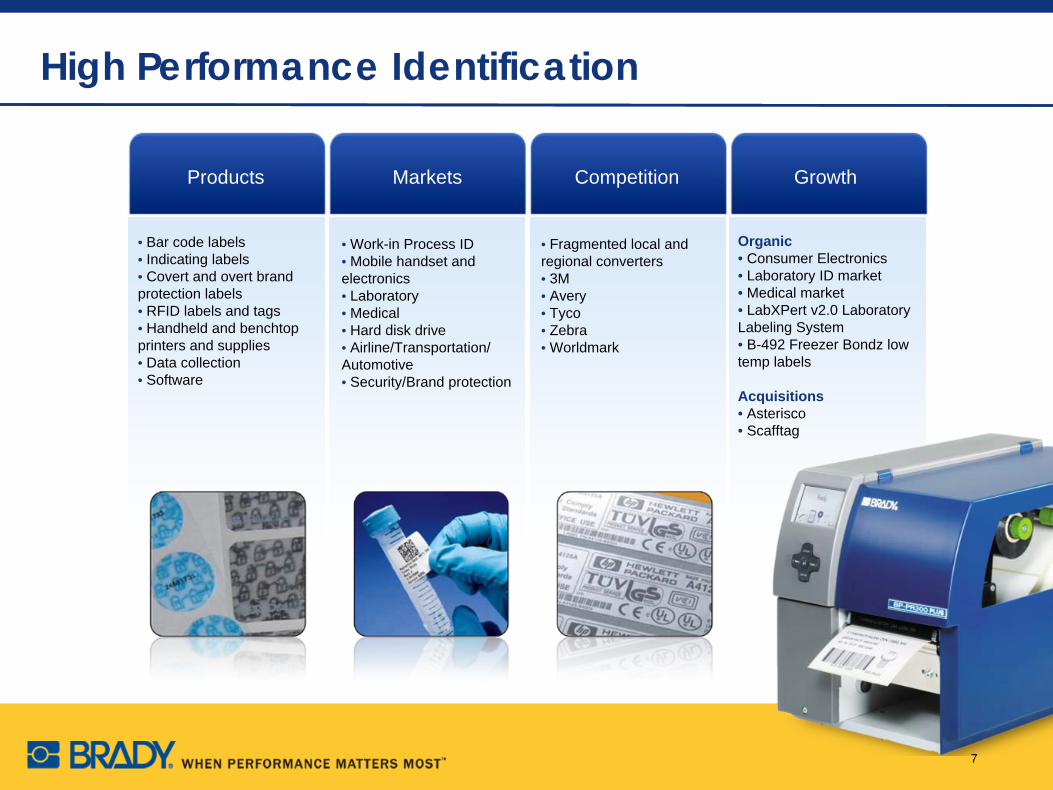

High Performance Identification

• Brady uses materials expertise and printing technology to create identification and brand protection solutions that can withstand even the harshest environments.

People Identification

• Brady helps identify people and enhance security by ensuring the right persons are in the right places at the right time.

4

Markets

• General Manufacturing• Maintenance• Safety• Process Industries• New Construction• Safety

Competition

• Fragmented competitor base• Local sign shops• No other global competitors• Regional players• Accuform• National Marker• Panduit

Growth

• Signs• Labels• Handheld Labelers and Supplies• Benchtop Printers and Supplies• Lockout/Tagout• Pipe and Value ID• Tags• Software• Data Collection

Products

Facility and Safety Identification

Organic• Upgraded Globalmark and Handimark printing systems• Lockout Pro 3.0• Commercial Grade Signs• 1st catalogue in Seton China• Commercial buildings

Acquisitions• Sorbent Products• Clement Communications• Accidental First Aid• Personnel Concepts• Transposafe

Markets

• Mobile handset• Hard disk drive• Medical• Automotive• Consumer electronics

Competition Growth

• Die-cut adhesives, gaskets & seals• EMI/RFI shields• Dampers• Back light & anti-splinter films• Antennae, meshes, felts & insulators• Thermal management solutions• Test strips, electrodes, drug delivery & would care• Application equipment

Products

Precision Die Cut Parts

Organic• Consumer electronics• Medical market• Speaker adhesive with small holes & thin frames adapted for auto assembly• X-Y CU wrapped gasket• 3D gasket• HDD damping label• Automotive thermalset adhesive

Acquisitions• Daewon• Tradex• QDPT

• Very fragmented by market segments & geography• Fabritech• Adampak• Zephyr• Marian Rubber

6

Markets

• Work-in Process ID• Mobile handset and electronics• Laboratory• Medical• Hard disk drive• Airline/Transportation/Automotive• Security/Brand protection

Competition

• Fragmented local and regional converters• 3M• Avery• Tyco• Zebra• Worldmark

Growth

• Bar code labels• Indicating labels• Covert and overt brand protection labels• RFID labels and tags• Handheld and benchtop printers and supplies• Data collection• Software

Products

High Performance Identification

Organic• Consumer Electronics• Laboratory ID market• Medical market• LabXPert v2.0 Laboratory Labeling System• B-492 Freezer Bondz low temp labels

Acquisitions• Asterisco• Scafftag

7

Markets

• Electrical• Voice/Data Communications• General Manufacturing• Mass Transit

Competition

•Concentrated Competitor Base•Tyco•Raychem/Critchley•Panduit•Newell Rubbermaid•Dymo - Purchased 11/05•HellermannTyton

Growth

• Wire and Cable Markers• Wrap Around• Sleeves• Terminal Block Markers• Patch Panel, Outlet & Faceplate Markers• Portable & Benchtop Labeling Systems• Software

Products

Wire Identification

Organic• IDXpert vZ•Brady PR 300 Plus Thermal Transfer Printer• NetDoc cable management system

Acquisitions• Modernotecnica• Caroll Australasia• Texit

8

Markets

• Employee ID• Visitor management• Access control• Customer facing

Competition

• Fragmented, regional competition• HID (Fargo)• Zebra• Datacard• Dymo• Evolis• Cardscan• Bristol ID Technologies• Laminex• All Safe• PC Nametag

Growth

• Name badges• Employee ID cards• Time expiring badges• Lanyards, badge holders & reels• Visitor management software• Printers/hardware

Products

People Identification

Organic• Premisys – new access control software/handware• OmniLife – new durable, secure and superior color ID card• Passage Point EDU visitor badging and management software for schools K-12

Acquisitions• CIPI• IdentiCard/IdentiCam• JAM• Stopware

9

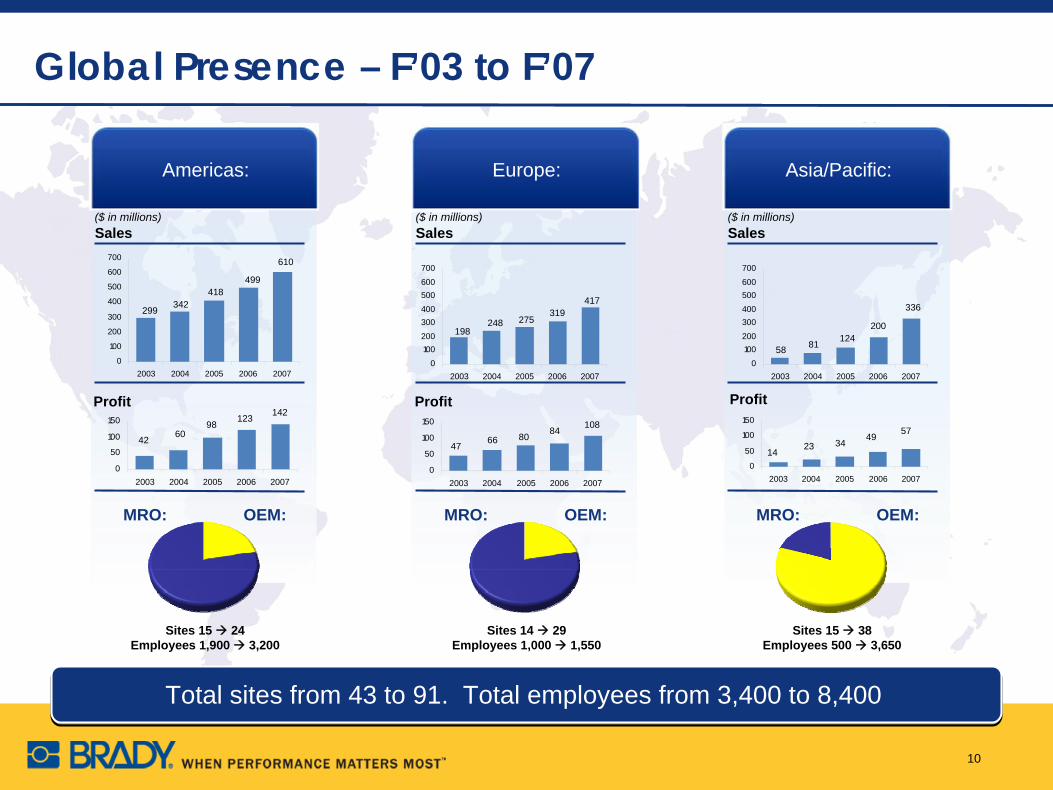

Global Presence – F’03 to F’07

Total sites from 43 to 91. Total employees from 3,400 to 8,400

Americas:

Sales($ in millions)

MRO: OEM:

Europe:

Sales($ in millions)

MRO: OEM:

Asia/Pacific:

Sales($ in millions)

MRO: OEM:

Sites 15 24Employees 1,900 3,200

Sites 14 29Employees 1,000 1,550

Sites 15 38Employees 500 3,650

10

0

100

200

300

400

500

600

700

2003 2004 2005 2006 2007

299 342418

499

610

0100200

300400500600

700

2003 2004 2005 2006 2007

198248 275

319417

0100200

300400500600

700

2003 2004 2005 2006 2007

58 81 124200

336

0

50

100

150

2003 2004 2005 2006 2007

Profit

1423 34

49 57

0

50

100

150

2003 2004 2005 2006 2007

Profit

47 66 80 84 108

0

50

100

150

2003 2004 2005 2006 2007

Profit

42 6098

123 142

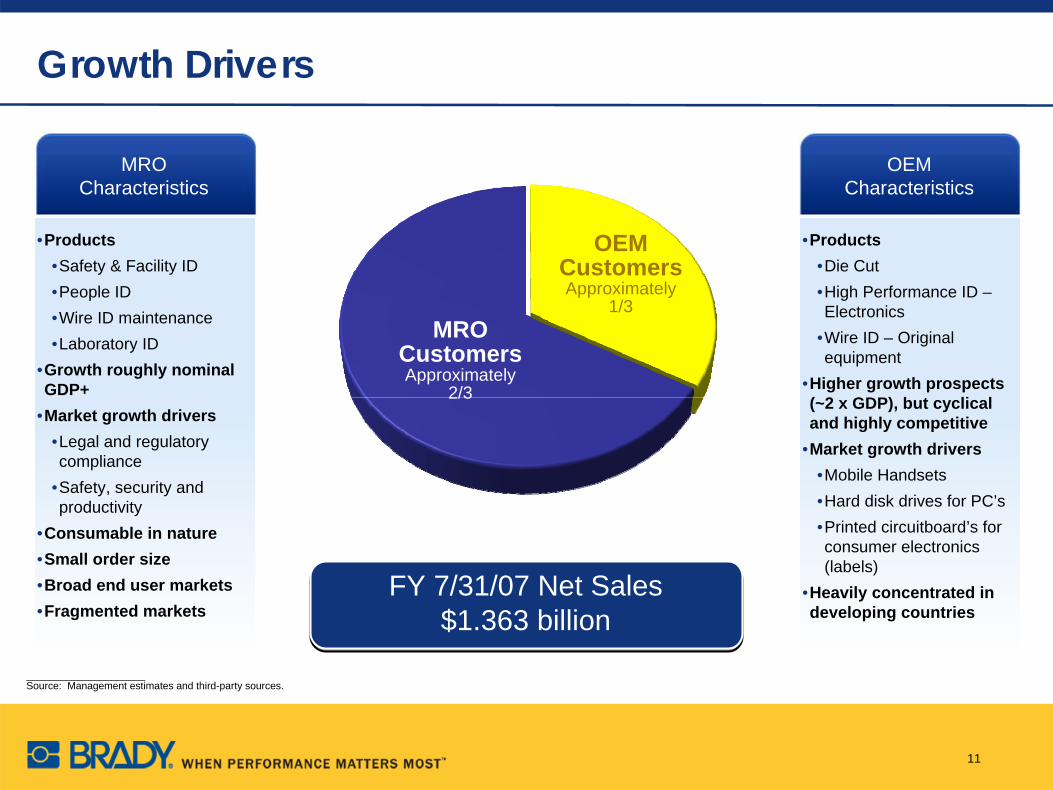

Growth Drivers

OEM Customers Approximately

1/3MRO

Customers Approximately

2/3

_____________________Source: Management estimates and third-party sources.

•Products•Safety & Facility ID•People ID•Wire ID maintenance•Laboratory ID

•Growth roughly nominal GDP+

•Market growth drivers•Legal and regulatory compliance

•Safety, security and productivity

•Consumable in nature•Small order size•Broad end user markets•Fragmented markets

MRO Characteristics

•Products•Die Cut•High Performance ID – Electronics

•Wire ID – Original equipment

•Higher growth prospects (~2 x GDP), but cyclical and highly competitive

•Market growth drivers•Mobile Handsets•Hard disk drives for PC’s•Printed circuitboard’s for consumer electronics (labels)

•Heavily concentrated in developing countries

OEMCharacteristics

FY 7/31/07 Net Sales $1.363 billion

11

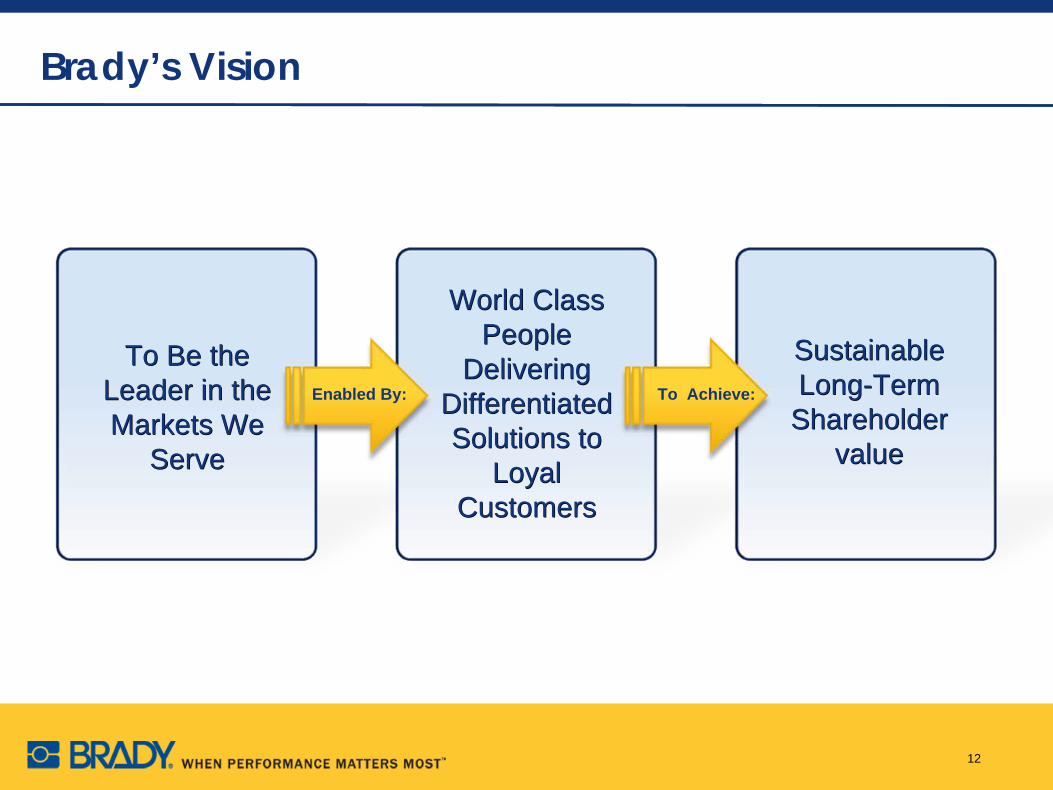

Brady’s Vision

Enabled By: To Achieve:

To Be the Leader in the Markets We

Serve

To Be the Leader in the Markets We

Serve

World Class People

Delivering Differentiated Solutions to

Loyal Customers

World Class People

Delivering Differentiated Solutions to

Loyal Customers

Sustainable Long-Term

Shareholder value

Sustainable Long-Term

Shareholder value

12

Driving Shareholder Value Creation$3

20 $366 $4

34

$463

$479 $5

51

$546

$517 $555 $6

71

$816

$1,4

89

$101

8

$136

3

1995 1997 1999 2001 2003 2005 2007

Revenue($ in millions)

Net Income($ in millions)

$27

$28 $32

$28 $4

0 $47

$28

$28

$21

$51

$82

$124

$104 $109

1995 1997 1999 2001 2003 2005 2007

13

7% CAGR7% CAGR

25% CAGR

25% CAGR

50% CAGR

50% CAGR

Green bars equal TTM for the period ended October 31st 2007

TTM TTM

Direct Marketing

‣Business to business only‣Continually reacquire‣Smaller average order value‣Often one-time needs

Distribution

‣Strong relationships in U.S.‣Europe more fragmented‣Regular purchasers‣Larger order values

Direct

‣Key regional accounts

Global Account Management

‣Dedicated strategic account managers for large global customers‣Consistent/seamless service

Channels

14

Shareholder Value Creation

15

Leadership Position in

Niche Markets

Leadership Position in

Niche Markets

How We Drive Shareholder Value

Differentiated Solutions &

Commitment to Innovation

Differentiated Solutions &

Commitment to Innovation

Geographic, Customer &

Channel Diversity

Geographic, Customer &

Channel Diversity

OperationalExcellenceOperationalExcellence

World Class PeopleWorld Class People

Disciplined Acquisition &

Integration Strategy

Disciplined Acquisition &

Integration Strategy

FOCUSDISCIPLINE

16

Leadership Position in Niche Markets

• We participate in many fragmented market segments populated with smaller or regional competitors

• A leadership position:• Helps us be a preferred supplier• Helps us sell at premium prices• Helps us to attract and maintain talent

Our Goal is to be #1 or #2 in the niche markets in which we participateOur Goal is to be #1 or #2 in the niche markets in which we participate

17

Materials Systems Software

Research and Development

Providing quality products through a long term commitment to innovation, technology and customer focus.

Brady’s technical team has a highly diverse set of skills focusing on differentiated solutions in materials, systems and software

Focus on innovation, not “me too”• Customer application expertise• Materials Expertise

Strong commitment to continue to build our capabilities

Research & Development($ in millions)

GlobalMark2

IDXpertV2

Variquest Visual Learning ToolsBrand Protection Label

LED Adhesives

Low Temp Label

HDD Damping Label

Label Archive

ExpressionsID Badge Design

Lockout PRO 3.0

PassagePoint EDU

18

$0

$10

$20

$30

$40

2004 2005 2006 2007 YTD2008

+21%+9%

+20%+18%

IP Series Printer System

+11%

Geographic, Customer & Channel Diversity

Multiple Channels

• Complete coverage of the market• Provides scalability• Greater opportunities for acquisitions• Expertise in multiple business models

Global Presence

• More than 500,000 customers• Broad penetration of Fortune 1000• Diverse end markets

Customer Diversity

Americas Asia Europe

We have geographic, channel, customer and end market diversity

19

World Class People

• We recruit people committed to excellence and invest in their potential

• We generally have local nationals run local businesses

• We provide training in our code of ethics to newly acquired companies and refresher training to existing employees

• We have a strong Internal Audit function which reports directly to the Audit Committee

LEADERSHIP MODEL

Inspire One Another

Continuously Learn More and Coach Others

Hold Ourselves and Others Accountable

Be Bold and Decisive

Expect High Performance of Ourselves and Others

Focus on the Customer

Practice the Values

The Brady culture: candid, collaborative and ethicalThe Brady culture: candid, collaborative and ethical

20

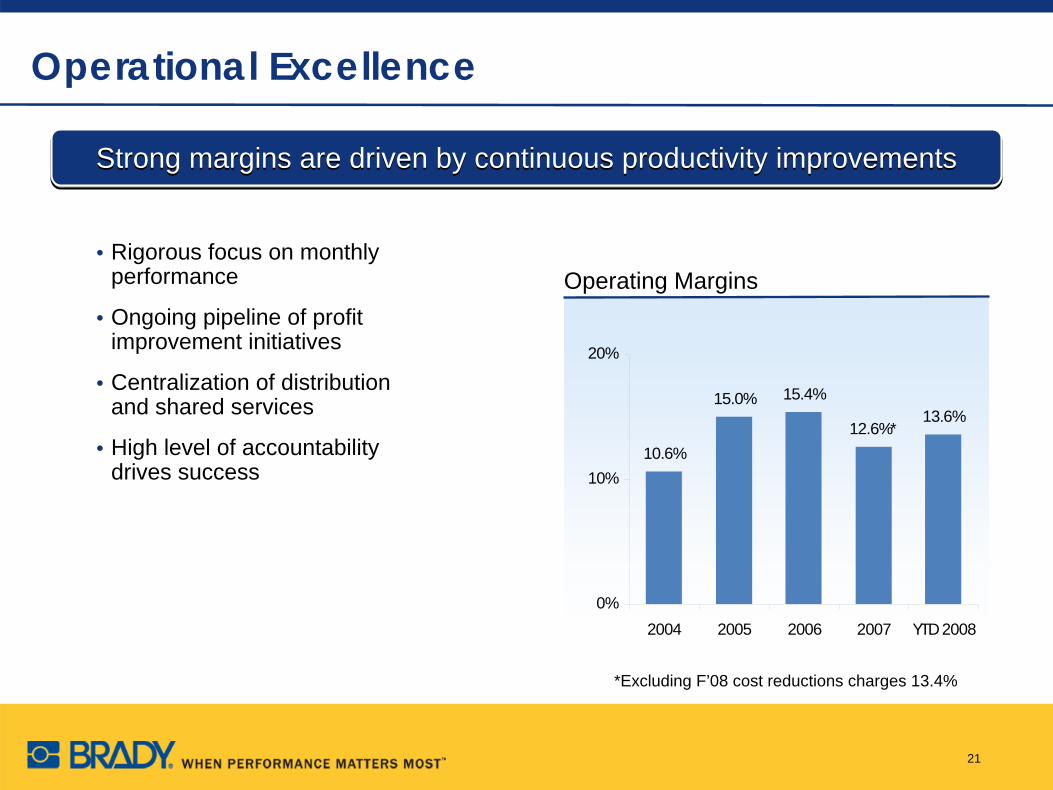

Operational Excellence

• Rigorous focus on monthly performance

• Ongoing pipeline of profit improvement initiatives

• Centralization of distribution and shared services

• High level of accountability drives success

10.6%

15.0% 15.4%

12.6%*13.6%

0%

10%

20%

2004 2005 2006 2007 YTD 2008

Strong margins are driven by continuous productivity improvementsStrong margins are driven by continuous productivity improvements

Operating Margins

21

*Excluding F’08 cost reductions charges 13.4%

Disciplined Acquisition & Integration Strategy

• Dedicated experienced team• “A List” of candidates driven by strategy • Top talent leads integration

• Quarterly review of integration results and opportunities

• A variant of EVA, SVE is a primary tool to gauge financial attractiveness

Approximately $850 million invested in acquisitions since F’04

Approximately $850 million invested in acquisitions since F’04

Since F’96 we have acquired and integrated 50 companies providing new geographies, technologies, market expansion and increased market share Since F’96 we have acquired and integrated 50 companies providing new geographies, technologies, market expansion and increased market share

Historical ROIC($ in millions)

22

0%

10%

20%

2003 2004 2005 2006 2007

13.0%14.5% 14.0%

10.1%

6.1%

Long-term, Sustainable Growth Strategy

23

Growth Strategy

Core Business 5%+

New SolutionsNew TechnologyNew Markets

Operational ExcellenceDifferentiated Solutions

Acquisitions 5%+

Productivity

Gross MarginsSG&AWorking Capital

Sales Growth 10%+

Net Income of 12% of sales

by F’2010

Increased Shareholder ValueIncreased Shareholder Value

24

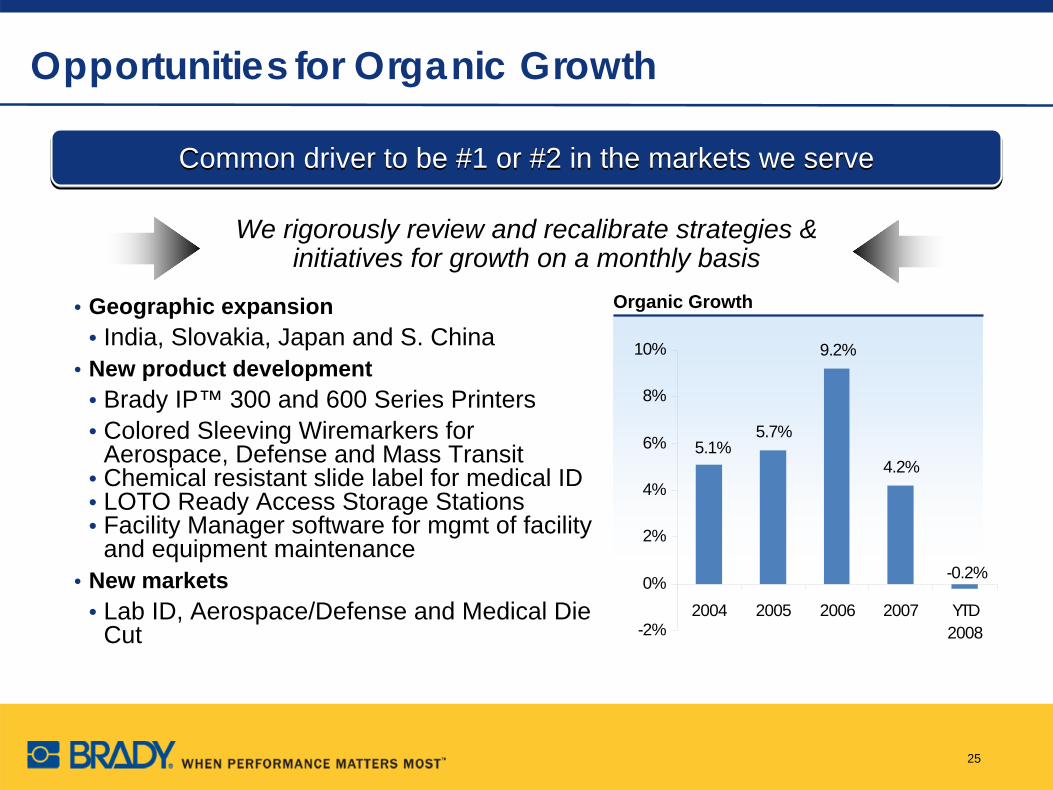

We rigorously review and recalibrate strategies & initiatives for growth on a monthly basis

Common driver to be #1 or #2 in the markets we serveCommon driver to be #1 or #2 in the markets we serve

Organic Growth

5.7%

9.2%

4.2%

-0.2%

5.1%

-2%

0%

2%

4%

6%

8%

10%

2004 2005 2006 2007 YTD2008

Opportunities for Organic Growth

• Geographic expansion• India, Slovakia, Japan and S. China

• New product development• Brady IP™ 300 and 600 Series Printers• Colored Sleeving Wiremarkers for

Aerospace, Defense and Mass Transit • Chemical resistant slide label for medical ID• LOTO Ready Access Storage Stations• Facility Manager software for mgmt of facility

and equipment maintenance• New markets

• Lab ID, Aerospace/Defense and Medical Die Cut

25

Opportunities for Acquisition Growth

• Geographic(Thailand, Modernotecnica)

• Market share(Daewon, Tradex, Emedco, Signs & Labels, Texit, Prinzing, Scafftag)

• Adjacencies(Personnel Concepts, CIPI, JAM, TruMed, Clement, Sorbent Products Co., Transposafe)

• Technology or capabilities(QDPT, Stopware, Asterisco)

• Going forward: nice pipeline of MRO opportunities

12.7%16.0%

25.5%

6.8%9.7%

0%

5%

10%

15%

20%

25%

30%

2004 2005 2006 2007 YTD2008

Acquisition Growth

Striving to be #1 or #2 in the markets we serveStriving to be #1 or #2 in the markets we serve

26

Hitting Our Profitability Target

Leverage from top line growth initiatives

Increasing Gross Margins• Facility rationalization• F’07 cost reduction activities• Better utilization of globalization

• SAP Productivity• High volume stock production (Mexico, Slovakia, China)

• China sourcing

Reducing SG&A• SAP Productivity• Telesales in Phillippines• Shared service in India

• Facility rationalization• F’07 cost reduction activities• Better utilization of globalization

27

Recognitions

•Forbes magazine’s Platinum 400 list of America’s Best Big Companies

•BusinessWeek’s Hottest 100 Growth Companies

•Business Ethics’ list of 100 best corporate citizens for 8th

consecutive year!

• Outstanding Corporate Growth Award from the Association for Corporate Growth (WI and National winner)

• Corporate Strategic Acquirer of the Year by M&A Advisor

• Wisconsin Manufacturer of the Year special award for corporate excellence

28

Financial Overview

29

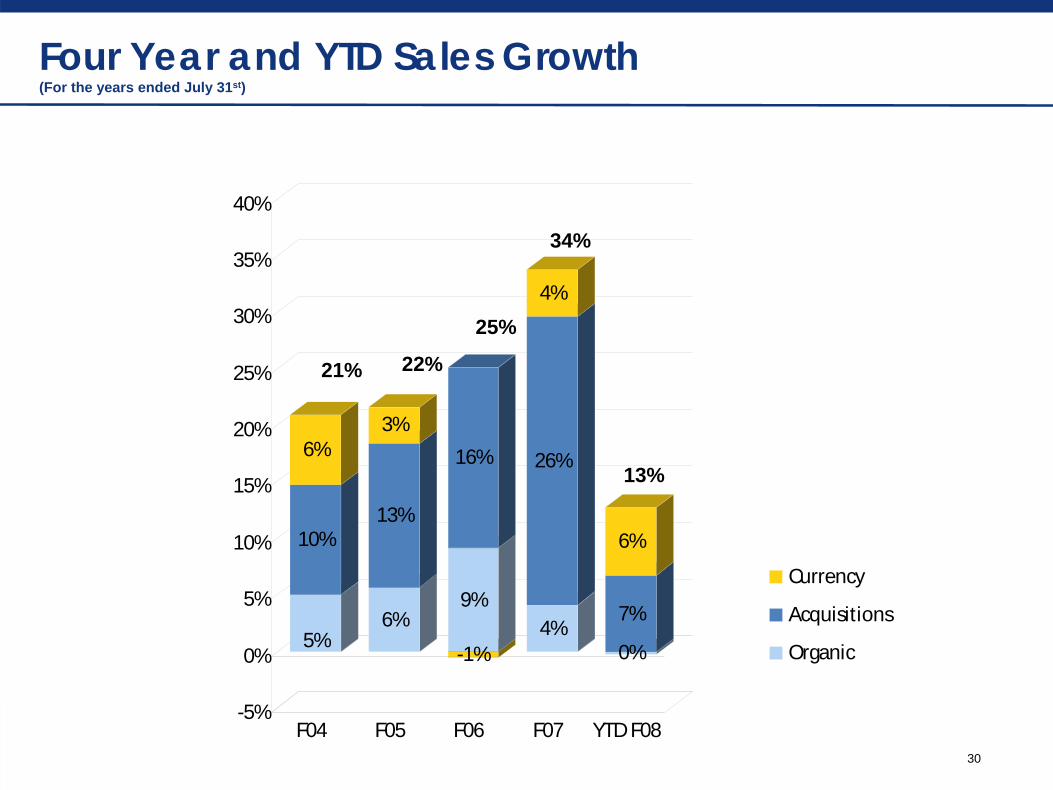

5%

10%

6%

6%

13%

3%

9%

16%

-1%4%

26%

4%

0%

7%

6%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

F04 F05 F06 F07 YTD F08

Currency

Acquisitions

Organic

Four Year and YTD Sales Growth (For the years ended July 31st)

13%

21% 22%

25%

34%

30

SG&A %

30%

32%

34%

36%

38%

F04 F05 F06 F07 YTD F08

Operating Income %

Gross Margin %

Four Year and YTD Profitability Metrics

46%

48%

50%

52%

54%

F04 F05 F06 F07 YTD F08

0%

3%

6%

9%

12%

15%

18%

Cost Red. Charges 0.6% 0.8%GAAP 10.6% 15.0% 15.4% 12.6% 13.6%

F04 F05 F06 F07 YTD F08

48.2%

51.5%

53.1%

32.8%

37.0%

35.0%

13.6%

10.6%

15.0%

51.6%

33.3%

15.4%49.0%

33.0%

12.6%

31

Working Capital and Cash Flow

$M Cash from Operating Activities

% Controllable Working Capital

10%12%14%16%18%20%

Q1 F07 Q2 F07 Q3 F07 Q4 F07 Q1 F08 Q2 F08 Q3 F08

19.1%18.8% 18.9%19.6% 19.0%

• Incentives for fiscal 2008 include and element for Working Capital management

• Positive trend continues in Q3• Comparison at constant currencies

• Cash from Operating Activities at $152.1, up 91% or $72M ytd vs. p/y Q3

• Record Q3 cash flow• Working capital focus in c/y paying off

$0$10$20$30$40$50$60

Q1 Q2 Q3 Q4

F07 F08

18.5%17.4%

Disciplined Capital Structure

Debt / EBITDA vs. Net Debt/PF EBITDAQ2 Ending Balances

We maintain a conservative balance sheet with flexibility for future growth

We maintain a conservative balance sheet with flexibility for future growth

33

*ST plus LT Debt less Cash and Cash Equivalents and ST Investments

$0

$100

$200

$300

$400

$500

$M's 500 302 259 262

Gross Debt Net Debt* Q3 TTM Q3 TTM PF

1.9x2.0x2.1x2.0x2.3x 2.2x

1.0x1.2x

1.3x1.4x1.6x 1.4x

.0x

.5x

1.0x

1.5x

2.0x

2.5x

Q2 F'07 Q3 F'07 F'07 Q1 F'08 Q2 F'08 Q3 F'08

Q4 Outlook and Fiscal 2008 priorities

Q4 Outlook and PrioritiesContinue to be cautious about economy and currencyContinued focus on cost structure, profitability and working capital managementOrganic growth

Continue investment and improvements in new product development

Acquisition growthSubstantively complete with integrationsExecute our current pipeline

Continue roll out of SAP

For More Information

Contact:

Barbara BolensDirector, Investor Relations414-438-6940

And see our Web site at www.investor.bradycorp.com

35

Summary of Cost Reduction Charges in F’07

Cost Reduction Charges Summary - $M's Q1 Q2 Q3 Q4 TotalIncome statement - Pre-tax 0.8 0.5 2.7 7.5 11.5Balance Sheet 0.0 1.6 6.6 0.5 8.7Total Charges 0.8 2.1 9.3 8.0 20.2

After-tax NI impact 0.6 0.4 1.9 5.4 8.3EPS Impact 0.01$ 0.01$ 0.03$ 0.10$ 0.15$

Examples of Q4 cost reduction activities include:Thailand reorganizationContinued reorganization of Signs and Labels business in UKItaly reorganizationBrady and Tradex Sweden reorganizationClosed Brandon US facility

Expected annual pre-tax savings from F’07 cost reduction activities in F’08 ~ $14M

36

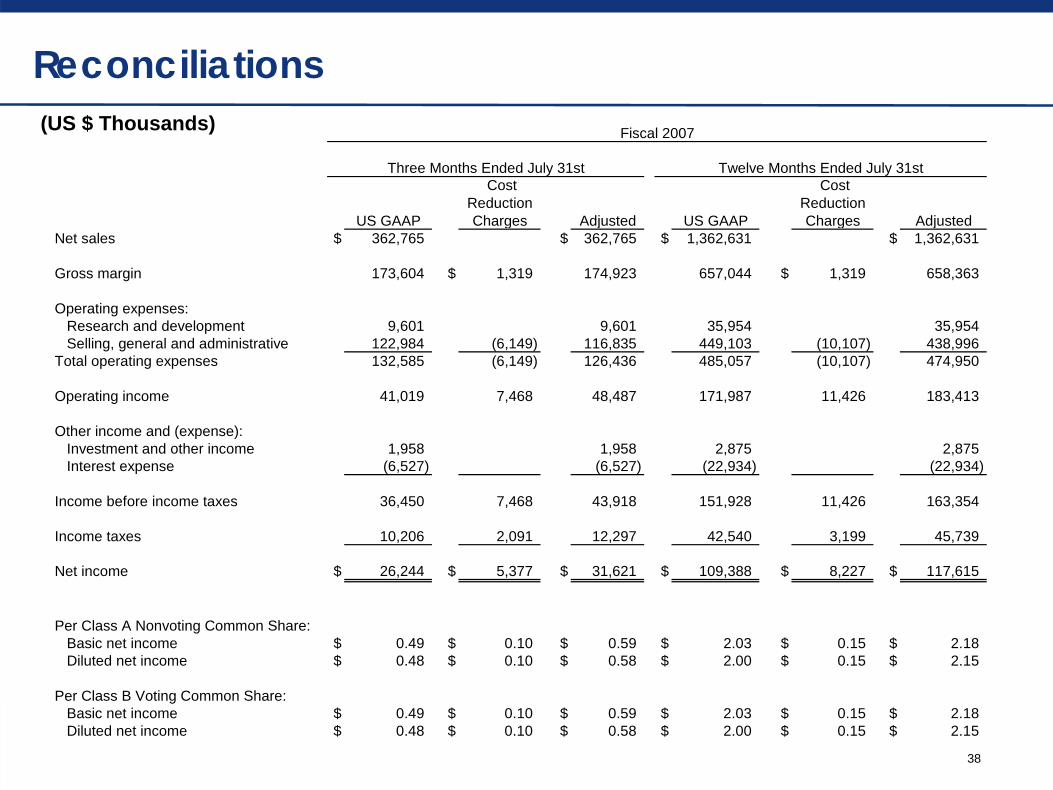

Reconciliations

(1) Brady is presenting EBITDA because it is used by many of our investors and lenders, and is presented as a convenience to them. EBITDA represents net income before interest expense, income taxes and depreciation and amortization. EBITDA is not a calculation based on generally accepted accounting principles (GAAP). The amounts included in the EBITDA calculation, however, are derived from amounts included in the Condensed Consolidated Statements of Income data. EBITDA should not be considered as an alternative to net income or operating income as an indicator of the company's operating performance, or as an alternative to operating cash flows as a measure of liquidity. However, the EBITDA measure presented may not always be comparable to similarly titled measures reported by other companies due to differences in the components of the calculation.

(US $ Thousands)

Q1 Q2 Q3 Q4 TotalEBITDA (1)

Net income 34,448$ 19,709$ 28,987$ 26,244 109,388$ Interest expense 4,735 5,244 6,428 6,527 22,934 Income taxes 13,396 7,665 11,273 10,206 42,540 Depreciation and amortization 12,927 13,169 14,307 13,453 53,856

EBITDA (non-GAAP measure) 65,506$ 45,787$ 60,995$ 56,430$ 228,718$

Q1 Q2 Q3 Q4 TotalEBITDA (1)

Net income 36,370$ 26,690$ 34,351$ 97,411$ Interest expense 6,720 6,747 6,961 20,428 Income taxes 15,366 11,276 12,188 38,830 Depreciation and amortization 14,168 15,501 16,013 45,682

EBITDA (non-GAAP measure) 72,624$ 60,214$ 69,513$ 202,351$

Fiscal 2008

Fiscal 2007

Reconciliations(US $ Thousands)

38

Fiscal 2007

US GAAP

Cost Reduction Charges Adjusted US GAAP

Cost Reduction Charges Adjusted

Net sales $ 362,765 $ 362,765 $ 1,362,631 $ 1,362,631

Gross margin 173,604 $ 1,319 174,923 657,044 $ 1,319 658,363

Operating expenses: Research and development 9,601 9,601 35,954 35,954 Selling, general and administrative 122,984 (6,149) 116,835 449,103 (10,107) 438,996 Total operating expenses 132,585 (6,149) 126,436 485,057 (10,107) 474,950

Operating income 41,019 7,468 48,487 171,987 11,426 183,413

Other income and (expense): Investment and other income 1,958 1,958 2,875 2,875 Interest expense (6,527) (6,527) (22,934) (22,934)

Income before income taxes 36,450 7,468 43,918 151,928 11,426 163,354

Income taxes 10,206 2,091 12,297 42,540 3,199 45,739

Net income $ 26,244 $ 5,377 $ 31,621 $ 109,388 $ 8,227 $ 117,615

Per Class A Nonvoting Common Share: Basic net income $ 0.49 $ 0.10 $ 0.59 $ 2.03 $ 0.15 $ 2.18 Diluted net income $ 0.48 $ 0.10 $ 0.58 $ 2.00 $ 0.15 $ 2.15

Per Class B Voting Common Share: Basic net income $ 0.49 $ 0.10 $ 0.59 $ 2.03 $ 0.15 $ 2.18 Diluted net income $ 0.48 $ 0.10 $ 0.58 $ 2.00 $ 0.15 $ 2.15

Three Months Ended July 31st Twelve Months Ended July 31st

![160602 Keybanc conference vF [Read-Only]](https://static.fdocuments.net/doc/165x107/6254baa30a36c136df5a2274/160602-keybanc-conference-vf-read-only.jpg)