Jumping on the Data Analytics Bandwagon - cdn.ymaws.com · • Recognize the differences between...

23

Jumping on the Data Analytics Bandwagon TACCBO 2018 Annual Meeting and Conference

Transcript of Jumping on the Data Analytics Bandwagon - cdn.ymaws.com · • Recognize the differences between...

Jumping on the Data Analytics Bandwagon

TACCBO 2018 Annual Meeting and Conference

2

Presenting Today

Elisa Gilbertson, CPAManager, Weaver Analytics

More than 10 years of experience Practice emphasis in data analytics, auditing and consulting for a

variety of industries including nonprofit organizations and higher education.

Reema Parappilly, CISAPartner, IT Advisory Services

More than 13 years of experience Practice emphasis in IT audits, data analytics, Sarbanes-Oxley

Compliance, and System and Organization Controls (SOC) reporting.

Objectives

• Recognize the differences between data and information

• Understand the process of analysis used to turn data into information

• Provide examples of analytics that may be useful for you

First, Some Perspective:The Data Analytics Bandwagon

What is Data Analysis?

The process of drawing inferences fromlarge sets of data to help identify trends,preferences, hidden patterns, and more.

Data vs Information

Data:• Raw, unorganized facts

that need processing

• No interpretation or analysis

• Inefficient and ineffective for communicating

• Cannot be wrong (but isn’t always right)

Information:• Data that is

processed, organized, structured, and/or presented in a given context to make it useful

• Meaningful to the user

• Can be wrong

Data: Journal Entries (as part of a

general ledger detail)

Vendor Lists (with no comparative figures)

Employee Master Files

Student AR Subledger Detail

Information: Subset of Journal Entries posted

on a holiday

Period-by-period comparison of Vendor purchases

Period-by-period comparison of Employee gross pay

Student AR Aging

7

Data vs Information

Garbage In – Garbage Out

• Computers operate by logical processes– Will process unintended or nonsensical inputs– Result in undesired and nonsensical outputs

• Fields not used as intended– Non-unique or non-required Purchase Order numbers– Transaction Dates vs Posting Dates

• Processes not occurring as intended– Attendance not taken in every class– Manual adjustments used instead of subledger entry

Data Analytics Matrix

Data to Information: Phases of Analysis

11

Phases of AnalysisIdentify a

problem or question

Create a hypothesis

Gather the data

Develop and run a

model

Prepare the final product

Adjust as needed

Data to Information

1. Identify a problem or question– Be as specific as reasonable– Make a problem “hierarchy” if needed

– Example: Why was there such a large return of Federal Student Financial Aid (SFA) funds during the Spring-18 semester?

2. Create a hypothesis– Be as specific as possible– Utilize knowledge of others to provide direction

– Example: There was an increase in SFA recipient withdrawals during SP-18.

Data to Information

3. Gather the data– Start broad, but stay on target– Check completeness and accuracy– Verify data validity

– Example: Obtain multiple semester’s worth of student enrollment data (including withdrawal and financial aid information)**

4. Create a “draft” model & run analysis– Identify analysis parameters – Review results against hypothesis – do they agree?

– Example: SP-18 student withdrawals went DOWN

Data to Information

5. Make adjustments and repeat (as necessary) – Hypothesis – was the original disproved?– Data – did it contain garbage?– Analysis – did it return useless information?

– Example: New hypothesis that SP-18 withdrawals occurred EARLIER, resulting in greater R2T4 returns.

6. Prepare product for presentation – Present analysis in clear, succinct manner

– Example: Comparative bar chart showing R2T4 days

Data Analysis Examples

Analysis Tools

• Microsoft Excel• Microsoft Access• ACL• IDEA

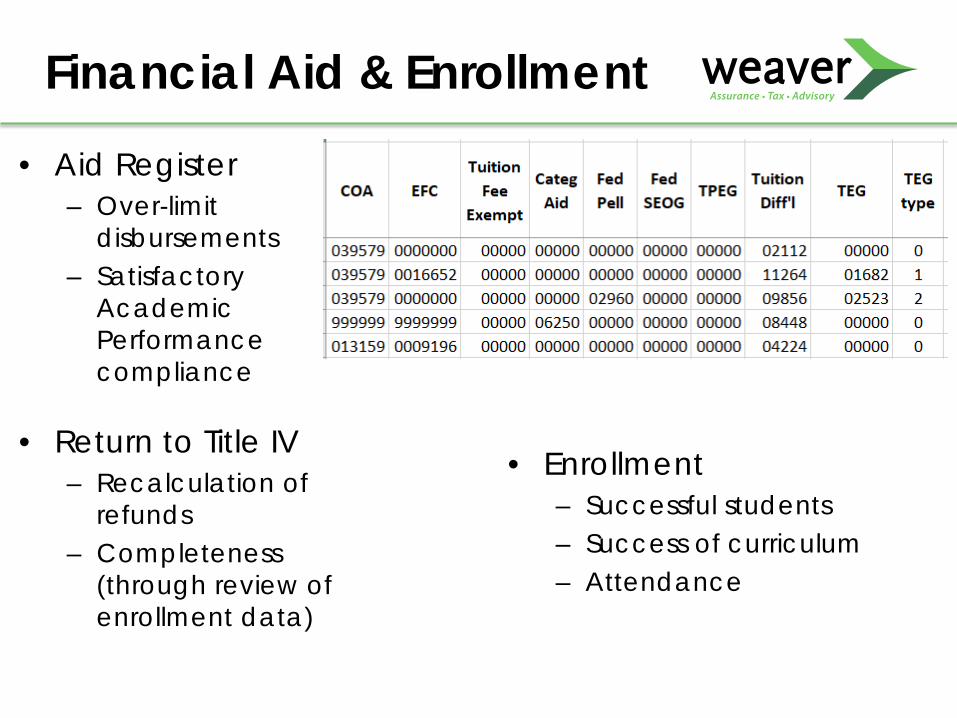

• Aid Register– Over-limit

disbursements– Satisfactory

Academic Performance compliance

• Return to Title IV– Recalculation of

refunds– Completeness

(through review of enrollment data)

• Enrollment– Successful students– Success of curriculum– Attendance

Financial Aid & Enrollment

• Check Register– Check number gaps– Check number dups– Duplicate payments– Unapproved vendors– Employee payments– Threshold avoidance

• Vendor Master File– Lacking proper fields– Vendor duplicates– Employee matches– Address irregularities

Accounts Payable

VendorID VendorName CheckAmount #Of Checks VendorAddr1 VendorCity VendorState1 Company A 7,896.29 3 PO BOX 8 Anywhere TX2 Company A 74,199.82 16 PO BOX 1 Anywhere TX

56 Company B 756.00 4 PO BOX 3 Anywhere TX77 Company B 186.00 1 PO BOX 3 Anywhere TX

9879 Company C 57.00 1 1100 Main Here TX23 Company C 675.00 2 PO BOX 3 Here TX

345 Company D 5,372.00 3 PO BOX 141 Here TX456 Company D 11,743.00 1 PO BOX 149 Here TX234 Company E 1,500.00 1 PO BOX 32 Here TX

8421 Company E 52,185.14 9 101 15 Here TX215 Company F 574.80 2 PO BOX 30 Anywhere TX

8753 Company F 30,314.65 19 PO BOX 26 Elsewhere WA

Check Register GapsGap_Start_Check

Gap_End_Check

Number_Items _Missing

178140 178142 1178142 178144 1178260 178262 1178386 178388 1178422 178424 1178466 178468 1178472 178474 1178506 178523 16

1782523 178661 137

Multiple Vendor Records for 1 Vendor

• Invoice Register– Duplicate payments– Duplicate billing– Threshold avoidance

Accounts Payable

– Split-transactions– Invoice number irregularities– Comparative analysis

Potential duplicate billings – same amounts, same dates, different invoice numbers

• Payroll Register– Payments after termination– Employees not in master file– Comparative analysis– Overtime appropriateness– Vacation/Benefit analysis

Payroll

• Employee Master File– Lacking proper fields– Employee duplicates– Address irregularities

Employees with duplicate addresses

• P-Card Charges– Duplicate payments– Out-of-policy purchases– Credits/returns

P-Cards

– Split-transactions– Off-time purchases– MCC analysis– Benford Analysis

Data analysis can be a daunting and stressful process;

however, with good data and focused analysis,the process can

add value to your operations.

23

Let’s Connect

@weavercpas

facebook.com/weavercpas

linkedin.com/company/weavercpas

youtube.com/weavercpas

Insights blog – weaver.com

Questions?

Elisa Gilbertson, CPAManager, Weaver Analytics

Reema Parappilly, CISAPartner, IT Advisory Services