Journal of Ekonomi Teknik2

of 18

-

Upload

din-aswan-ritonga -

Category

Documents

-

view

217 -

download

0

Transcript of Journal of Ekonomi Teknik2

-

8/13/2019 Journal of Ekonomi Teknik2

1/18

Journal of Derivatives Accounting, Vol. 1, No. 1 (2004) 2946c JDA

STOCK OPTIONS AND MANAGERIAL INCENTIVES TO INVEST

TOM NOHELUniversity of Michigan, USA

STEVEN TODD

Department of Finance, School of Business Administration,Loyola University, Chicago, 820 N. Michigan Avenue

Chicago, IL 60611, [email protected]

We examine the effect of stock options on managerial incentives to invest. Our chief innovationis a model wherein rm value and executive decisions are endogenous. Numerical solutions toour model show that managerial incentives to invest are multi-dimensional and highly sensitiveto option strike prices, the managers wealth, degree of diversication, risk aversion, and careerconcerns. We show that under- and over-investment problems can be large and economicallysignicant, with hurdle rates ranging from more than 20 percentage points below to morethan 35 percentage points above shareholders required rate of return. Finally, rm value isnot a strictly increasing function of a managers incentive compensation or conventional payperformance sensitivity metrics. Stronger managerial incentives to invest can benet or harma rm.

Keywords : Executive stock options; incentives; investment; risk aversion; career concerns.

1. Introduction

Researchers looking to examine the incentiveeffects of executive stock options are confrontedwith two immediate challenges. First, standardBlackScholes risk-neutral valuation techniquesare inaccurate because executive stock optionsare not traded, and they are frequently heldby managers with undiversied wealth (includ-ing human capital) facing short-sale and liquidityconstraints. Second, option values are inextrica-bly linked to executive actions and rm value. If options did not affect managerial behavior, andif managerial behavior did not affect rm value,then why would rms choose to grant options?The fact that options are a large and growingportion of US executive pay (Murphy, 1999), that

rms routinely re-price stock options (Brenneret al ., 2000), that largely as a result of stockoption pay, US executives, on average, hold aclaim on more than 3% of their rms shares(Conyon and Murphy, 2000) all these factssuggest that the agency problems between man-agers and shareholders are large and that thebenets of stock option compensation are poten-tially great.

This paper examines the effect of stockoptions on managerial incentives to invest. Weextend the literature by studying this effectwithin a model that links executive actions andrm value. This is important. Managers havedirect control over their rms nancing andinvestment decisions. And stock options are amechanism to alter managerial behavior so that

Corresponding author.29

-

8/13/2019 Journal of Ekonomi Teknik2

2/18

30 Tom Nohel and Steven Todd

shareholder and executive interests are aligned tomaximize rm value.

The value and incentive effects of exec-utive stock options depend on the parame-ters of the option contract, and the managerswealth, degree of diversication, and risk aver-

sion (Lambert et al ., 1991). We construct a modelof managerial investment that links rm valueto managerial behavior and managerial behav-ior to executive-specic risk and wealth param-eters. One advantage of our approach is thatwe are able to describe managerial incentivesto invest as hurdle rates, rather than partialderivatives of the managers utility function (Halland Murphy, 2000) or comparative statics froma BlackScholes option pricing model (Johnsonand Tian, 2000). These hurdle rates allow us toquantify the degree of under- or over-investmentin simple terms.

In our model, a risk-averse executive sets theinvestment strategy of his rm based on privateinformation he possesses about project payoffs.We assume the executive maximizes the expectedutility of his future wealth. His wealth includescash, and incentive compensation in the form of shares and options on his rms shares; it alsoincludes a measure of his human capital the

value of his expected future compensation, whichitself is a function of the managers perceivedability. We assume the value of the managershuman capital rises and falls with the value of the rm he manages. Since the manager is riskaverse, he overweighs the downside risk to thevalue of his human capital. When the manager isreluctant to put his human capital at risk we sayhe has career concerns. Career concerns createan agency problem between the executive andthe risk-neutral owners of the rm: the execu-tive ignores investors risk-return preferences andmaximizes his own utility (see Holmstrom andRicart i Costa, 1986; Milgrom and Roberts, 1992;Nohel and Todd, 2003). We analyze how the exec-utives investment choices change as the param-eters of his wealth and compensation vary.

Our analysis produces some interestingresults. First, we nd that executive incentivesto invest are highly sensitive to the distributionof managerial wealth and the magnitude of

executive career concerns. Using reasonable val-ues for these parameters, we show that under-and over-investment problems can be large andeconomically signicant, with hurdle rates rang-ing from more than 20 percentage points belowto more than 35 percentage points above share-

holders required rate of return.Second, we nd that incentive alignment ispossible, there are a variety of ways to achieveincentive alignment, and that depending oninvestment risks and executive-specic risk andwealth parameters, stock options can be a smallor large component of executive pay.

Third, contrary to Hall and Murphy (2000),we nd that managerial incentives to invest arehighly sensitive to stock option strike prices.Even when options constitute only 10% of anexecutives wealth, a 10% change in the optionstrike price can move the managers hurdlerate up or down by more than 9 percentagepoints. In our model, at-the-money options max-imize a managers incentive to take risk. How-ever, in many situations, premium options do abetter job of aligning executive and shareholderinterests, a point made in Johnson and Tian(2000). The relation between option strike pricesand managerial investment incentives has impor-

tant implications for the issue of stock optionre-pricing.

Fourth, we argue that if incentive alignmentwere the primary rationale for the use of stockoptions by corporations, we would expect to seefrequent option re-pricing both when stock pricesfall and when they rise. In contrast, Brenner et al .(2000) nd that nearly all re-pricing occurs aftera fall in stock prices. We would also expect cor-porations to monitor executive wealth, possiblyrestricting executive share holdings, which dis-courage risk-taking and counteract the desiredeffects of stock options.

Finally, we nd that the comparative staticsfrom risk-neutral option valuation models (e.g.BlackScholes) do not provide accurate guide-posts for the magnitude of managerial incentivesto invest. Our results indicate that a risk-aversemanager who cannot diversify the risk associ-ated with his stock option wealth may not pre-fer an increase in the value of his rms stock

-

8/13/2019 Journal of Ekonomi Teknik2

3/18

Stock Options and Managerial Incentives to Invest 31

or the variance of his rms stock returns. Man-agerial incentives to increase rm value do notnecessarily rise as the managers pay becomesmore sensitive to performance. Our results arerelevant to studies that examine the relationbetween executive compensation and corporate

investment decisions, such as Aggarwal andSamwick (1999) and Datta et al . (2001). Ourresults can also inform studies of ownershipstructure and rm performance, such as Demsetzand Villalonga (2001), Himmelberg et al . (1999),and Ljungqvist and Habib (2003).

The remainder of this paper is organizedas follows. We develop a model of managerialinvestment in Section 2 and solve the modelnumerically for a variety of parameterizations inSection 3. We discuss payperformance sensitiv-ity and rm value in Section 4 and conclude inSection 5.

2. A Model of ManagerialInvestment

In this section, we model the investment behav-ior of a risk-averse manager whose wealth con-sists of cash and incentive compensation in theform of shares, and call options on his rmsshares. We assume the manager maximizes theexpected utility of his future wealth, whichincludes not only cash and incentive compensa-tion, but also a measure of his human capital the expected value of his future compensationthat is based on his perceived ability. 1 The man-ager sets his rms investment strategy based onprivate information he possesses about projectpayoffs. One salient feature of our model is thatrm value is a function of managerial behaviorand managerial behavior is a function of execu-

tive wealth.

2.1. Set-up and information structure of the model

Consider a rm with I dollars in cash on itsbalance sheet at t = 0. The rms investment

opportunity set consists of two mutually exclu-sive projects. Each project requires an initialinvestment of I . One project is riskless and thusearns the risk-free rate, which we set equal to0 for ease of exposition. The other project isrisky and generates a payoff that is uniformly

distributed on the interval [ V L , V H ], with V H I V L . The low end of the distribution, V L , isknown and certain. The high end, V H , is uncer-tain but known to be uniformly distributed onthe interval, [ V H1 , V H2 ]. Assume the relation-ship among I, V L , V H1 , and V H2 is such that I =(V L + ( V H1 + V H2 )/ 2)/ 2.2

Our model has three types of partici-pants: investors, a manager, and an intermedi-ary. Investors put their capital at risk in therm. They select an intermediary to hire a man-ager and design the managers compensation.Think of this intermediary as either a compensa-tion consultant or the rms board of directors.For ease of exposition, we refer to the intermedi-ary as the board of directors, or simply the board.We assume that the board acts in the interest of shareholders and is otherwise passive. The man-ager makes the rms investment decisions.

The timing in our model is as follows: at t =0, investors know that the rm has I in cash on

its balance sheet. Furthermore, at t = 0, investorsare aware of the rms investment opportuni-ties (including the distribution of project pay-offs) and they elect a board of directors to hirea manager of unknown talent. The board xes acompensation budget for the manager and setsthe terms of his compensation. At t = 0+, theboard hires a manager and pays him. His payconsists of a cash salary, and incentive compen-sation in the form of shares and options on hisrms shares. At t = 1, the manager receives asignal that identies V H . Based on this signal, themanager chooses between the rms two invest-ment opportunities. The signal is never revealedand thus cannot be contracted on. At t = 2, theoutcome of the investment decision is realized,the managers shares and options vest, and the

1 The compensation a manager can expect to earn over his career depends on his reputation. In our model, reputationis not something that the manager can cultivate, say, by working harder.2 That is, ex-ante , both the riskless and the risky projects have zero NPV. This assumption is consistent with strong-formmarket efficiency. However, as long as V H1 I V L , most of our results hold.

-

8/13/2019 Journal of Ekonomi Teknik2

4/18

32 Tom Nohel and Steven Todd

rm is liquidated. 3 Below is a time line specifyingcritical events in our model: Investor select board and set comp. budget

Designer hires mgr.,reveals contract & inv. opps

Manager gets privatesignal and invests

Project payoffsdetermined, shares & options vest, andthe firm is liquidated

|-------------------------------|----------------------------------|----------------------------------|

t = 0 t = 0 + t = 1 t = 2

Investors and the managers differ in theirpreferences towards risk. We assume investorsare risk neutral and the manager is risk averse inwealth. This assumption is consistent with Hem-mer et al . (1996) who nd that executives exer-cise their stock options early. We further assumethe managers utility function exhibits constantrelative risk aversion as described below. 4

U (w) =

1

1 bw(1 b)

, b 0, b = 1 (1)Here, w is the level of the managers wealththat he derives from the following sources: cash(including salary and non-rm wealth), incen-tive compensation (shares and options on hisrms shares), and the change in the value of themanagers human capital. 5

Let K denote the value of the managers cashwealth. The managers incentive compensationincludes n shares and m options with an exercise

price of X . Here, n and m represent fractions of the shares outstanding in the managers rm. Werestrict K , n, and m to be non-negative and weassume shares and options vest at t = 2. 6

We assume that the managers performanceaffects his expected future income, i.e. the valueof his human capital. Since the manager is risk

averse, he overweighs the downside risk to thevalue of his human capital. These career con-cerns create an agency problem between themanager and the risk-neutral owners of the rmhe manages (see also: Holmstrom and Ricart iCosta, 1986; Milgrom and Roberts, 1992; Nohel

and Todd, 2003).7

Fee and Hadlock (2001) show that stockreturns are used as a performance metric by theexternal labor market for top-ranked executives,and Jagannathan and Wang (1996) show thatstock returns are linearly related to the returnon human capital. Consistent with these results,we assume the value of the managers humancapital is linear in rm value. 8 Specically, weassume the change in the value of the managershuman capital is proportional to the change inrm value from the time when the manager ishired ( t = 0+), to the time when the rm is liq-uidated ( t = 2). If is a non-negative constant,V is the rms liquidation value, and V 0+ is thevalue of the rm immediately after the manageris hired, then the change in the value of the man-agers human capital is (V V 0+ ). Note thatwith this specication, the expected change inthe value of the managers human capital is zero.Intuitively, we interpret the change in the value of

the managers human capital as the present valueof all future compensation gains (losses) that areattributable to the managers performance.

Investors are rational so the rms valuechanges as new information is released. Startingat an initial value of I (at time 0), the rmsvalue adjusts sequentially to reect information

3 The distribution of project outcomes and the information structure of our model are similar to Ross (1977). The binarynature of the investment choice is common in the literature. See, for example, John and John (1993), Lambert (1986),and Holmstrom and Ricart i Costa (1986).4 The conclusions of our paper are valid with any utility function that exhibits decreasing absolute risk aversion. Wechose the specication above since it is common in the literature; see Lambert et al . (1991) and Hall and Murphy (2000).5 In the interests of simplicity, we model the managers risky security holdings as cash equivalents. For a similar treatment,see Lambert et al . (1991) and Hall and Murphy (2000).6 In the interests of simplicity, we sidestep the more general problem of an executive who has a portfolio of options withvarying strike prices.7 We side-step the common assumption of managerial dis-utility of effort. The notion that a manager can positively affectoutput by working harder but prefers not to is inconsistent with the behavior of top-level executives. Kaplan (1984)points out that contemporary managers often work too hard rather than too little. It is hard to conceive of managersshirking, given continual monitoring by the nancial press and securities analysts. Allen (2001) suggests that insteadof modeling effort aversion, research in this area should focus on implicit contracts and reputation. He considers thenancial industry, but his remarks apply to any situation where, as he says, the principal does not have the expertisethat the agent does.8 This mirrors Graham (1999) who assumes that analysts wages increase linearly with their reputations.

-

8/13/2019 Journal of Ekonomi Teknik2

5/18

Stock Options and Managerial Incentives to Invest 33

about the hiring of the manager (time 0+), themanagers investment decision (time 1), and thenal project outcome (time 2). The price adjust-ment from time 0 to time 0+ reects investorsvaluation of the marginal benet/cost of hir-ing the manager, and is consistent with investor

reactions to awards of incentive pay, as docu-mented in Defusco et al . (1990) and Yermack(1997). Note that since the rms value is I just prior to the manager being hired, optionswith strike prices above (below) I are out-of-the-money (in-the-money). The stock price adjuststo V 0+ only after the hiring of the manager ismade public.

Due to the binary nature of the investmentchoice in our model, an investment strategy isdened as a cut-off point. Consider any V H , whereV H2 V H V H1 . [V H] denotes the strategywhere the manager invests in the risky projectwhenever he observes a signal V H V H ; oth-erwise, he invests in the riskless project. Thus,if the manager follows investment strategy [ V H],he chooses the risky project with probability(V H2 V H )/ (V H2 V H1 ), and he chooses the risk-less project with probability 1 (V H2 V H)/ (V H2 V H1 ) = ( V H V H1 )/ (V H2 V H1). By denition, theriskless project has zero NPV. In contrast, the

opportunity to take the risky project has NPVequal to [( V H2 + V H)/ 2 + V L]/ 2 I .9

Therefore, if the manager follows investmentstrategy [ V H], the value of the rm after the man-ager is hired, V 0+ , as a function of the managersinvestment strategy, [ V H], is given by

V 0+ (V H ) = I + (V H2 V H )(V H2 V H1 )

(V H2 + V H)/ 2 + V L

2 I (2)

Equation (2) ignores the cost of the managerscompensation.

Risk-neutral shareholders strictly prefer therisky project as long as it offers an expected

return that exceeds the risk-free rate of zero. Thisimplies that their preferred investment strategyis to set V H = 2I V L .

The risk-averse manager with career con-cerns ignores investors preferences on investmentstrategy and maximizes his own utility. Herein

lies the agency problem. Compensate the man-ager in cash and he is too conservative, becausea risky project entails human capital risk with-out sufficient reward in some states. Substitutingshares for cash makes matters worse. In fact, inour model, the change in the value of a managershuman capital is equivalent to the change in thevalue of a long forward contract on the managersrms shares. When compensation is linear inrm value, the combination of the managers riskaversion and career concerns compels the man-ager to follow an overly conservative investmentstrategy [ V H], where V H > 2I V L . The boardof directors is faced with the problem of ndingways to overcome the managers excessive conser-vatism by incorporating compensation elementswhose values are convex in rm value. 10

2.2. Solution to the model

The manager develops his investment strategy[V H ] by solving for the value of the signal thatmakes him indifferent between the two projects.Given wealth and compensation ( K,n,m,X ) anda signal V H , the manager can invest in the riskyproject and derive expected utility equal to

E [U (K,n,m,X,V H )]

= 11 b

1(V H V L)

Min( X,V H )

V L(nV + K + (V V 0+ )) (1

b) dV

+ V H

Min( X,V H )(nV + m(V X ) + K

+ (V V 0+ )) (1 b) dV (3)

9 Note, this differs from the ex-ante NPV because, here, it is known that the manager gets a signal about V H .10 One possible solution to this problem is for shareholders to insure the managers human capital with a bonusthat isequivalent to a short forward contract on the rms shares. However, such a scheme is not incentive compatible becauseit asks the manager to return money to his rm when the value of his human capital increases. Since the managersperformance is observable, the manager can simply quit his current rm and capture the increased value of his humancapital at another rm.

-

8/13/2019 Journal of Ekonomi Teknik2

6/18

34 Tom Nohel and Steven Todd

In this expression, (V V 0+ ) measures thechange in the value of the managers humancapital. 11 Alternatively, the manager can investin the riskless project and derive (expected) util-ity equal to

U (K,n,m,X,V H )=

11 b

[nI + m Max(0 , I X )

+ (I V 0+ ) + K ]1 b (4)

Here, the term (1 V 0+ ) measures the changein the value of the managers human capital.

The manager sets his investment rule [ V H],by solving for the value of V H that equates (3)and (4); this is the value of V H that solves (5):

11 b

1(V H V L)

Min( X,V H )

V L(nV + K + (V V 0+ )) (1

b) dV

+ V H

Min( X,V H )(nV + m(V X ) + K

+ (V V 0+ )) (1 b) dV

= 11 b

[nI + mMax(0 , I X )

+ (I V 0+ ) + K ]1 b (5)

Let V H denote the value of V H that solves (5). If the manager acts in his own interest, he followsinvestment strategy [ V H ].

3. Wealth, Incentive Compensation,and Managerial Investment

In this section, we report solutions to Eq. (5). Weare interested in comparing the incentive effectsof various divisions of wealth and incentive com-pensation ( K,n,m,X ). We follow Johnson and

Tian (2000) and Hall and Murphy (2000) andcompare schemes of equal cost from the perspec-tive of risk-neutral shareholders. 12 This approachis broadly consistent with Bebchuk et al . (2002)who argue that executives have power to inu-ence their own compensation. As an alterna-tive, an optimal contracting approach presumesshareholder value is maximized, with managersbeing guaranteed a reservation utility. Such anapproach is considered in Nohel and Todd (2003).

We set the managers coefficient of relativerisk aversion, b = 3, consistent with studiesby Friend and Blume (1975), Litzenberger andRonn (1986), Lambert et al . (1991) and Hall andMurphy (2000). The change in the value of themanagers human capital is given by (V V 0+ ).Since we are comparing compensation schemes of equal cost, and since the managers utility func-tion exhibits constant relative risk aversion, onlythe ratio of to wealth matters. We consider arange of ratios, /W , from 0% to 0.6%. With thisrange of ratios, career concerns run the gamutfrom slight to extreme. 13

We set X = I (rm value at time 0) ini-tially, consistent with the near uniform prac-tice of granting options at-the-money (Murphy,1999).14 We consider three risky projects, eachrequiring an initial investment of I = $100: a low-risk project with ( V L , V H1 , V H2 ) = (75 , 100, 150);

11 We set the integral limits equal to Min( X, V H ) rather than X . When the option strike price is greater than the valueof the managers signal, the options are worthless and the manager makes his investment decision based only on thevalue of his cash and shares.12 In determining the cost of a compensation plan, we assume that the board values shares and options under share-holders preferred investment strategy, V H = 2 I V L . Therefore, we compute n using the formula for rm value givenin (2), with V H set equal to 2 I V L . We determine m in an analogous way using the call option formula derived inAppendix A. For a similar treatment see Gavish and Kalay (1983).13 Other things being equal, we would expect younger (or more recently tenured) managers with less accumulated wealthto have higher career concerns (see Gibbons and Murphy, 1992). In our numerical solutions below, we consider a rangeof risky project cash ows. For the median CEO with effective shareholdings equal to 1.48% of his rms shares (Conyonand Murphy, 2000), the range of career concerns we consider covers a gain/loss in human capital equal to +37% to 34%of total share wealth. For a CEO with smaller (larger) effective shareholdings or other wealth, the potential gain/lossin human capital covered by this range of career concerns can be considerably larger (smaller).14 Again, note that until the manager is hired, the rm value is I . Thus, striking the managers options at-the-moneymeans setting X = I .

-

8/13/2019 Journal of Ekonomi Teknik2

7/18

Stock Options and Managerial Incentives to Invest 35

a medium risk project with ( V L , V H1 , V H2 ) =(50, 100, 200); and a high-risk project with(V L , V H1 , V H2 ) = (25 , 100, 250). As a percentageof invested capital, these projects have volatili-ties equal to 14.4%, 28.9%, and 43.3%, respec-tively, and net present values equal to 3.125%,

6.25%, and 9.375%, respectively. We believethese projects are representative of the projectsavailable to typical US rms. As Dimson andMarsh (2001) show, for the period 19551999,the geometric equity risk premium for US rms is6.2%. Moreover, Ibbotson and Sinqueeld (2001)report that over the period 19262000, stockreturns had an average standard deviation of 28%, with rms in the largest decile averaging19.1% and rms in the smallest decile averaging45.8%.

Tables 13 summarize managerial invest-ment strategies for various divisions of wealthand incentive compensation and for a range of

career concerns. To facilitate comparative analy-sis, we convert the managers investment strategy[V H ] into a hurdle rate. In all tables, sharehold-ers preferred hurdle rate is 0.0%. Table 1 reportsmanagerial hurdle rates for the low risk project;Tables 2 and 3 report managerial hurdle rates for

the medium and high risk projects, respectively.We set bold numeric values in the tables whereover-investment occurs.

We nd that managerial incentives to investare highly sensitive to the distribution of wealthand the magnitude of executive career concerns.For the medium-risk project (Table 2), if wex the managers wealth at 50% cash and 50%options, the range of hurdle rates is 25.00%(when the ratio of to wealth equals 0%) to+25 .00% (when the magnitude of career concernsequals 0.6%).

Paying the manager entirely in cash workswell when career concerns are zero, but leads

Table 1. Managerial investment strategy (hurdle rates) for thelow-risk project.

% Share of managerial wealth as Career concerns, /Wealth

Cash Shares Options 0% 0.2% 0.4% 0.6%

25 75 0 2.86 4.01 5.46 7.3725 50 25 6 .79 4 .93 2 .97 0 .6825 25 50 9 .27 6 .89 4 .15 0 .4625 0 75 12 .50 8 .16 2 .51 12.50

50 50 0 1.75 2.70 3.86 5.3150 40 10 6 .06 4 .23 2 .55 0 .8250 30 20 8 .19 6 .33 4 .59 2 .7850 20 30 9 .55 7 .59 5 .76 3 .8050 10 40 10 .73 8 .55 6 .57 4 .3950 0 50 12 .50 9 .42 7 .21 4 .70

75 25 0 0.81 1.61 2.55 3.7075 20 5 6 .71 4 .29 2 .53 0 .9375 15 10 8 .71 6 .30 4 .51 2 .87

75 10 15 9 .93 7 .49 5 .70 4 .0575 5 20 10 .94 8 .35 6 .55 4 .8875 0 25 12 .50 9 .04 7 .21 5 .51

100 0 0 0.00 0.67 1.46 2.39

Table 1 reports hurdle rates implied by the managers preferred investmentstrategy. Under shareholders preferred investment strategy, the managersets the hurdle rate at 0.00%. We assume the risky project cash owsare uniformly distributed on the interval (75, V H ) with V H uniformly dis-tributed on the interval (100, 150). We set the managers coefficient of relative risk aversion equal to 3.0; measures the magnitude of the man-agers career concerns. We set bold numeric values in the table whereover-investment occurs.

-

8/13/2019 Journal of Ekonomi Teknik2

8/18

36 Tom Nohel and Steven Todd

Table 2. Managerial investment strategy (hurdle rates) for themedium-risk project.

% Share of managerial wealth as Career concerns, /Wealth

Cash Shares Options 0% 0.2% 0.4% 0.6%

25 75 0 14.63 25.00 25.00 25.0025 50 25 4 .81 6.46 25.00 25.0025 25 50 13 .40 0.41 25.00 25.0025 0 75 25 .00 5 .03 25.00 25.00

50 50 0 8.00 14.41 25.00 25.0050 40 10 5 .79 1.50 11.90 25.0050 30 20 11 .63 4 .16 6.03 25.0050 20 30 15 .81 8 .05 2.41 25.0050 10 40 19 .59 11 .32 0 .33 25.0050 0 50 25 .00 14 .43 2 .72 25.00

75 25 0 3.39 7.54 14.29 25.0075 20 5 9 .13 2 .15 4.81 15.9775 15 10 14 .19 6 .82 0.11 10.0375 10 15 17 .60 9 .95 3 .05 6.4475 5 20 20 .51 12 .38 5 .46 3.8675 0 25 25 .00 14 .43 7 .46 1.82

100 0 0 0 2.91 7.08 14.32

Table 2 reports hurdle rates implied by the managers preferred investmentstrategy. Under shareholders preferred investment strategy, the managersets the hurdle rate at 0.00%. We assume the risky project cash owsare uniformly distributed on the interval (50, V H ) with V H uniformly dis-tributed on the interval (100, 200). We set the managers coefficient of relative risk aversion equal to 3.0; measures the magnitude of the man-agers career concerns. We set bold numeric values in the table whereover-investment occurs.

to an ever increasing under-investment prob-lem as the ratio of to wealth increases. Theunder-investment problem is exacerbated whenshares are substituted for cash. For example, inTable 2, if we x the magnitude of career con-cerns at 0.4%, the managers hurdle rate risesfrom 7.08% (when his wealth consists of 100%cash) to 14.29% (when his wealth consists of 75%cash and 25% shares).

Options, with their convex payoffs, can be

used to overcome the managers reluctance toinvest. For example, in Table 2, keeping the mag-nitude of career concerns xed at 0.4%, the man-ager lowers his hurdle rate to +0 .11% when hiswealth consists of 75% cash, 15% shares, and10% options. With this mix of wealth, the man-agers interests are nearly aligned with those of the shareholders.

With too much option wealth, the man-ager over-invests. In Table 2, too much optionwealth can be as little as 5% or 10% of wealth.

For example, if we x the magnitude of careerconcerns at 0.2%, the manager sets his hurdlerate at 6.82% when his wealth consists of 75%cash, 15% shares and 10% options. Tables 13show that problems of either over-investment orunder-investment can be large and economicallysignicant.

There are a variety of ways to achieveincentive alignment between managers andshareholders. Depending on investment risks and

executive-specic risk and wealth parameters,stock options can be a small or large compo-nent of executive pay. Kole (1997) and Murphy(1999) nd considerable variation in compensa-tion awards across industries. Tables 13 showthat incentive alignment is not inconsistent withthis result.

Two other features of Tables 13 are worthnoting. First, increasing the share of optionwealth generally leads to increased risk takingon the part of the manager. However, when

-

8/13/2019 Journal of Ekonomi Teknik2

9/18

Stock Options and Managerial Incentives to Invest 37

Table 3. Managerial investment strategy (hurdle rates) for thehigh-risk project.

% Share of managerial wealth as Career concerns, /Wealth

Cash Shares Options 0% 0.2% 0.4% 0.6%

25 75 0 37.50 37.50 37.50 37.5025 50 25 11.10 37.50 37.50 37.5025 25 50 10 .68 37.50 37.50 37.5025 0 75 37 .50 37.50 37.50 37.50

50 50 0 20.93 37.50 37.50 37.5050 40 10 0.59 25.28 37.50 37.5050 30 20 10 .52 11.93 37.50 37.5050 20 30 19 .11 2.20 37.50 37.5050 10 40 26 .95 6 .19 37.50 37.5050 0 50 37 .50 14 .09 37.50 37.50

75 25 0 7.96 20.94 37.50 37.5075 20 5 8 .93 6.35 37.50 37.5075 15 10 17 .53 1 .83 22.50 37.5075 10 15 23 .74 7 .71 14.06 37.5075 5 20 29 .20 12 .45 7.84 37.5075 0 25 37 .50 16 .54 2.73 37.50

100 0 0 0.00 7.17 21.48 37.50

Table 3 reports hurdle rates implied by the managers preferred invest-ment strategy. Under shareholders preferred investment strategy, themanager sets the hurdle rate at 0.00%. We assume the risky project cashows are uniformly distributed on the interval (25, V H ) with V H uniformlydistributed on the interval (100, 250). We set the managers coefficientof relative risk aversion equal to 3.0; measures the magnitude of themanagers career concerns. We set bold numeric values in the table whereover-investment occurs.

options comprise a large portion of compensa-tion, the reverse effect is possible (see, for exam-ple, Table 1, when the ratio of to wealth equals0.6% and cash wealth equals 25%). Second, x-ing the managers mix of wealth and increasinga projects risk leads to decreased risk taking onthe part of the manager, unless the magnitude of career concerns is small. An increase in projectrisk has two conicting effects on an optionsvalue to the manager: a positive effect from the

convexity of the options payoff (wealth effect),and a negative effect from the concavity of themanagers utility function (risk-aversion effect).In Tables 13, the wealth effect dominates whenthe ratio of to wealth is less than or equal to0.2% and the risk-aversion effect dominates whenthis ratio is greater than 0.2%.

Several studies (e.g. Guay, 1999; Rajgopaland Shevlin, 2002) nd that options are used toencourage risk taking, and more option pay isassociated with greater risk taking. These studies

implicitly assume the extra risk taking is bene-cial to shareholders. Our analysis indicates itis quite conceivable that rms overshoot andencourage excessive risk taking.

In summary, Tables 13 show that manage-rial incentives to take risk are multi-dimensional.Several factors have signicant inuence overmanagerial incentives to take risks. Moreover, theBlackScholes metrics that are so often used asguideposts to understand option-based incentives

do not apply once rm value is endogenous andmanagerial risk aversion is factored in.

3.1. Option strike prices and managerial investment

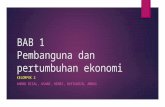

We next consider the effect of option strikeprices on managerial incentives to invest. Table 4xes the magnitude of career concerns at 0.2%and reports hurdle rates for the medium riskproject. We consider a range of strike pricesfrom $70 to $150, with $100 being at-the-money.

-

8/13/2019 Journal of Ekonomi Teknik2

10/18

-

8/13/2019 Journal of Ekonomi Teknik2

11/18

Stock Options and Managerial Incentives to Invest 39

5 0 7 0

9 0

1 1 0

1 3 0

1 5 0

0

40

20

15

10

5

0

5

10

15

20

25

H u r d

l e r a

t e ( % )

O p t i o n s t r i k e p r i c e

O p t i o n s

( % )

Fig. 1. Managerial investment as a function of mixof wealth and option strike prices: / Wealth = 0 .2%;cash = 50%; shares = (50 options)%.

(i.e. accepts fewer risky projects). However, whenX < I , the managers investment behaviorresponds dramatically to changes in the optionsexercise price. The intuition is as follows: as X increases from I , the options are still worthlessunder the risk-free project, and they are incre-mentally worth less under the risky project. Incontrast, as X falls below I , the options sud-denly have value under the risk-free project, thusinducing more conservative behavior.

The relation between managerial investmentand option strike prices bears directly on theissue of re-pricing options. Our analysis indi-cates that if incentive alignment were the pri-mary rationale for executive stock option awards,we would expect to see option re-pricing bothwhen stock prices fall and when they rise. 16

In fact, since a managers investment behaviorresponds so dramatically to a rise in an optionsintrinsic value, we would expect to see more fre-

quent option re-pricing when stock prices rise(and options resemble shares). Quite the reverse,Brenner et al . (2000) nd that more than 99% of all re-pricing events are associated with a reduc-tion in the option strike price, following a declinein stock prices.

Our analysis also indicates that the dis-tribution of a managers wealth has a largeimpact on his incentives to invest. Thus, if incen-tive alignment were the primary rationale forstock option awards, we would expect to seecompanies monitor executive wealth and possi-

bly place restrictions on share holdings, whichtend to encourage risk avoidance and counteractthe desired effects of stock options. We have noevidence of either practice, though some rmsmandate minimal shareholdings for executives(see Core and Larcker, 2001). In contrast, Ofekand Yermack (2000) nd evidence that executivesprefer to sell shares whenever possible.

4. Risk-Taking Incentives and FirmValue

In this section we examine risk-taking incentivesand rm value. Table 5 reports rm value underthe managers investment strategy for variousdivisions of wealth and incentive compensationand for a range of career concerns. We presentresults for the medium-risk project only, and wecompute rm value using Eq. (2). Equation (2)ignores the cost of the managers compensation,but this is not a problem because we are com-paring rm values derived from compensationschemes of equal cost.

Firm value is highly sensitive to the distri-bution of wealth and the magnitude of execu-tive career concerns. If we x the magnitudeof career concerns at 0.4%, rm value variesfrom $106.25 (when wealth consists of 50% cash,10% shares, and 40% options) to $100.00 (whenwealth consists of 25% cash and any mix of sharesand options). If we x the managers wealthat 50% cash and 50% shares, rm value varies

from $105.61 (when career concerns are nil) to$100.00 (when the magnitude of career concernsis 0.6%).

Contrary to the implications of risk-neutraloption valuation models, rm value is not anincreasing function of a managers option wealth

16 In drawing a parallel between the results of Table 5 and the re-pricing phenomenon, we are assuming that options arere-priced at constant cost. Hall and Murphy (2002) call this a BlackScholes re-pricing and cite General Dynamics asone of the rst companies to adopt such a practice in 1991. Brenner et al . (2000) nd that from an ex-ante standpoint,re-pricing produces a small benet to executives, generally less than 15% of the initial option award value. Callaghanet al . (2000) obtain similar estimates of the benet executives derive from option re-pricing events.

-

8/13/2019 Journal of Ekonomi Teknik2

12/18

40 Tom Nohel and Steven Todd

Table 5. Firm value, given the managers investment strategy.

% Share of managerial wealth as Career concerns, /Wealth

Cash Shares Options 0% 0.2% 0.4% 0.6%

25 75 0 104.11 100.00 100.00 100.0025 50 25 106.02 105.83 100.00 100.0025 25 50 104.45 106.25 100.00 100.0025 0 75 100.00 106.00 100.00 100.0050 50 0 105.61 104.17 100.00 100.0050 40 10 105.92 106.23 104.83 100.0050 30 20 104.90 106.08 105.89 100.0050 20 30 103.75 105.60 106.19 100.0050 10 40 102.41 104.97 106.25 100.0050 0 50 100.00 104.17 106.18 100.00

75 25 0 106.14 105.68 104.21 100.0075 20 5 105.42 106.20 106.02 103.7075 15 10 104.24 105.78 106.25 105.2475 10 15 103.15 105.26 106.16 105.8475 5 20 102.04 104.72 105.95 106.1075 0 25 100.00 104.17 105.69 106.22

100 0 0 106.25 106.17 105.75 104.20

Table 5 reports rm value [based on Eq. (2) in the text] under the man-agers preferred investment strategy. At time 0, rm value is $100.00.We assume the risky project cash ows are uniformly distributed on theinterval (50, V H ) with V H uniformly distributed on the interval (100,200). We set the managers coefficient of relative risk aversion equal to3.0; measures the magnitude of the managers career concerns.

or the delta of his portfolio. For example, with

the ratio of to wealth xed at 0.2%, rm valueis $105.68 when the managers wealth consists of 75% cash and 25% shares. Firm value rises to$106.20 when the managers wealth consists of 75% cash, 20% shares, and 5% options, but fallsto $104.17 when the managers wealth consistsof 75% cash and 25% options. Stronger manage-rial incentives to invest can benet or harm arm, depending on the rms investment oppor-tunities and executive specic risk and wealthparameters. 17

We illustrate sections of Table 5 in Figs. 24,where we x one component of wealth and showrm value as a function of career concerns andthe mix of other wealth. In Fig. 2, cash repre-sents 50% of managerial wealth. Here, we see thatwhen career concerns are low, substituting shares

100101102103104105

106107

0 10 20 30 40 50Shares (%)

F i r m

V a

l u e

( $ )

alpha / Wealth = 0% 0.20% 0.40% 0.60%

Fig. 2. Firm value as a function of career concernsand mix of wealth: cash = 50%; options = (50 shares)%.

for options results in an increase in rm value.In Fig. 3, shares represent 50% of managerialwealth. Here, we see that once options constituteabout 10% of wealth, increasing option wealth bysubstituting options for cash results in a decreasein rm value. In Fig. 4, options represent 25% of managerial wealth. Here, we see that when career

17 Managerial risk aversion is not driving this result. If we set the magnitude of career concerns equal to zero andthe managers coefficient of relative risk aversion, b, equal to zero (i.e. if the manager is risk neutral), this result stillholds. Firm value is not strictly increasing in managerial option wealth as long as rm value is endogenous. In contrast,risk-neutral valuation models treat rm value as exogenous and independent of managerial decisions.

-

8/13/2019 Journal of Ekonomi Teknik2

13/18

Stock Options and Managerial Incentives to Invest 41

100101102103104105106107

0 10 20 30 40 50

Options (%)

F i r m

V a

l u e

( $ )

alpha / Wealth = 0% 0.20% 0.40% 0.60%

Fig. 3. Firm value as a function of career concernsand mix of wealth: shares = 50%; cash = (50 options)%.

alpha / Wealth = 0% 0.20% 0.40% 0.60%

100101

102103104105106107

0 25 50 75Cash (%)

F i r m

V a

l u e

( $ )

Fig. 4. Firm value as a function of career concernsand mix of wealth: options = 25%; shares = (75 cash)%.

concerns are high, substituting cash for sharesresults in an increase in rm value.

In summary, Figs. 24 conrm that rmvalue is highly sensitive to the distribution of wealth and the magnitude of executive careerconcerns.

4.1. Payperformance sensitivity and rm value

It is possible to assess the extent to whichan executive participates in wealth creation byestimating payperformance sensitivity (PPS)measures. Jensen and Murphy (1990) exam-ine PPS and estimate that the average exec-utive experiences a wealth increase of $3.25for every $1000 increase in his rms value.Such a low PPS challenges the principalagent paradigm, which predicts, in the caseof risk-neutral managers, a one-for-one relation

between executive and shareholder gains. Lowpay sensitivities, however, may provide ade-quate incentives if managers are risk-averse(Haubrich, 1994), or if rms are highly lev-ered (John and John, 1993). Consistent withthe principalagent paradigm, payperformance

measures decrease, and salaries increase, as rmand CEO incomes become more volatile (Garen,1994). Stock options, used only modestly in thetime period that Jensen and Murphy study, bol-ster PPS measures (Hall and Liebman, 1998)and provide powerful incentive effects (Guay,1999).

Following Jensen and Murphy (1990), wedene PPS as the change in managerial compen-sation associated with a $1000 change in rmvalue, for all possible liquidation values of therm. We describe the computation method forthis measure in Appendix B. We also compute aPPS measure based on the BlackScholes optionpricing model, as described in Guay (1999). 18

The former measure allows for variation in exec-utive career concerns; the latter ignores careerconcerns.

Table 6 reports payperformance measuresfor various divisions of wealth and incentive com-pensation and for a range of career concerns. Col-

umn 1 uses the PPS measure described by Guay(1999); the remaining columns use the PPS mea-sure outlined in Appendix B. We see that xingthe managers career concerns, there is a positiverelation between option wealth and PPS. If wex the managers mix of wealth, PPS declines ascareer concerns increase.

Figures 5 and 6 illustrate the relationbetween rm value (again, without netting outthe cost of the managers compensation) andPPS. Both gures are based on the PPS measureoutlined in Appendix B. In Fig. 5, we x cashwealth at 75%; in Fig. 6 we x cash wealth at50%. The gures show that xing the managerscareer concerns, there is no simple monotonicrelation between PPS and rm value. In fact, ina simple regression of the rm value observationsfrom Table 5 on the PPS measures in Table 6,

18 We assume stock prices follow a lognormal process with expected return and volatility parameters equal to 6.25%and 28.9%, respectively (same as the medium-risk project). We assume options are granted at-the-money and expire in2 years, with the risk-free rate equal to 0%.

-

8/13/2019 Journal of Ekonomi Teknik2

14/18

42 Tom Nohel and Steven Todd

Table 6. Payperformance sensitivity under managers investmentstrategy.

% Share of managerial wealth as Career concerns, /Wealth

Cash Shares Options 0%** 0% 0.2% 0.4% 0.6%

25 75 0 $7.06 $7.06 $7.06 $7.06 $7.0625 50 25 17.54 12.40 9.78 4.71 4.7125 25 50 28.02 21.08 15.41 2.35 2.3525 0 75 38.50 33.13 23.21 0 0

50 50 0 4.71 4.71 4.71 4.71 4.7150 40 10 8.90 6.92 6.28 5.23 3.7650 30 20 13.09 10.06 8.86 6.97 2.8250 20 30 17.28 13.61 11.91 9.16 1.8850 10 40 21.47 17.51 15.32 11.66 0.9450 0 50 25.67 22.04 19.08 14.48 0

75 25 0 2.35 2.35 2.35 2.35 2.3575 20 5 4.45 3.60 3.30 2.98 2.4075 15 10 6.55 5.21 4.66 4.05 3.0875 10 15 8.64 6.98 6.18 5.33 3.9975 5 20 10.74 8.86 7.82 6.73 5.0475 0 25 12.83 11.04 9.54 8.24 6.20

100 0 0 0 0 0 0 0

Table 6 reports PPS measures (i.e. the change in the value of the man-agers compensation per $1000 change in shareholder wealth) under themanagers preferred investment strategy. We assume the risky project cashows are uniformly distributed on the interval (50, V H ) with V H uniformlydistributed on the interval (100, 200). We set the managers coefficient of relative risk aversion equal to 3.0; measures the magnitude of the man-agers career concerns. See Appendix B for a description of PPS.*These PPS measures are computed from the BlackScholes option pricingmodel, as described in Guay (1999).

alpha / Wealth = 0% 0.20% 0.40% 0.60%

100101102103104105106107

0 2 4 6 8 10 12PPS ($ change in manager's wealth per $1,000 change in shareholder wealth)

F i r m

V a

l u e

( $ )

Fig. 5. Firm value and PPS: cash = 75%.

alpha / Wealth = 0% 0.20% 0.40% 0.60%

PPS ($ change in manager's wealth per $1,000 change in shareholder wealth)

100

101

102

103

104

105106

107

0 5 10 15 20 25

F i r m

V a

l u e

( $ )

Fig. 6. Firm value and PPS: cash = 50%.

the coefficient on the PPS measure is not statis-tically signicant. 19

4.2. Robustness

The results we present in Tables 16 andFigs. 16 are qualitatively robust to changes inthe parameters of our model, including projectcash ows, -to-wealth ratios, risk-aversion coef-

cients and risk-free rates. The conclusions of our paper are valid with any managerial util-ity function that exhibits decreasing absoluterisk aversion. Our results do not depend on ourassumption that the managers human capitalis linear in rm value. Moreover, our resultsdo not depend on our assumption that man-agerial career concerns are responsible for the

19 We do not mean to suggest that the rows of Tables 5 and 6 represent a reasonable division of managerial wealth at across-section of rms.

-

8/13/2019 Journal of Ekonomi Teknik2

15/18

Stock Options and Managerial Incentives to Invest 43

agency problem between managers and share-holders. Similar results obtain as long as themanagers indirect utility function is concave inrm value.

5. Conclusions

This paper examines the effect of stockoptions on managerial incentives to invest.We develop a model in which rm value isendogenous: a manager affects rm value throughhis investment decisions, which depend on themanagers risk and wealth parameters. We thensolve the model numerically for a variety of parameterizations that are consistent with themarketplace.

We nd that managerial incentives to investare multi-dimensional and highly sensitive tooption strike prices, the managers wealth, degreeof diversication, risk aversion, and career con-cerns. Under- and over-investment problems canbe large and economically signicant, with hurdlerates ranging from more than 20 percentagepoints below to more than 35 percentage pointsabove shareholders required rate of return.

There is no simple monotonic relationbetween PPS and rm value. Firm value isnot a strictly increasing function of a man-

agers incentive compensation. Stronger manage-rial incentives to invest can benet or harm arm, depending on the rms investment oppor-tunities and executive specic risk and wealthparameters. Moreover, increasing the amount of incentive pay does not necessarily increase theincentive to take risks, and may even decreaseit. Our results should prove useful to researcherswho study managerial behavior, specically theimpact of managerial compensation and/or own-

ership structure on rm value.Acknowledgments

We are indebted to Lu Hong for many helpfuldiscussions and suggestions, as well as com-ments from seminar participants at the Univer-sity of Pittsburgh. Our research has benetedfrom comments by discussants and participantsat the following 2002 meetings: the Royal Eco-nomic Society (Warwick), the European Finan-cial Management Association (London), the

APFA/PACAP/FMA (Tokyo) and the Finan-cial Management Association European confer-ence (Copenhagen). A previous version of thispaper was titled Executive compensation, rep-utation and risk-taking incentives.

Appendix A: Valuing a Call OptionBased on the InvestmentStrategy, [ V H ]

Here we derive a formula for calculating thevalue of a call option, assuming the manager pur-sues the investment strategy [ V H ]. If the managertakes the riskless project, the nal stock price (att = 2) is known with certainty. A call option onthe entire rm with exercise price X , expiring att = 2, is worth Max(0 , I X ). When the manager

takes the risky project, the value of a call optionon the rm (ignoring compensation costs) is

Call Value = 1

V H V L V H

V LMax(0 , V X )dV

(A.1)

Thus, if the manager follows investment policy,[V H ], the call value at time 0 is

C 0 = 1

V H2 V H1 V H

V H1 Max(0 , I X )dV H

+ 1

V H2 V H1 V H2

V H

1V H V L

V H

V LMax(0 , V X )dV dV H (A.2)

The rst integral represents the calls payoff under the riskless project, while the second inte-gral represents the calls expected payoff underthe risky project. To simplify expression (A.2),we consider the cases X < V H and X > V Hseparately. If X < V H , then,

C 0 =V H V H1V H2 V H1

Max(0 , I X )

+ 1

V H2 V H1

V H2

V H

1V H V L

V H

X (V X )dV dV H

(A.3)

-

8/13/2019 Journal of Ekonomi Teknik2

16/18

44 Tom Nohel and Steven Todd

Alternatively, if X > V H , then,

C 0 =V H V H1V H2 V H1

Max(0 , I X )

+ 1

V H2 V H1

V H2

X

1V H V L

V H

X (V X )dV dV H

(A.4)

These can be integrated to give the following val-uation formulae for the call option at t = 0 . If X < V H ,

C 0 =V H V H1V H2 V H1

Max(0 , I X )

+ 1

2(V H2 V H1 )

(V H2 V L)2

2

(V H V L)2

2 2(X V L)(V H2 V H )

+ ( X V L)2 lnV H2 V LV H V L

(A.5)

If X > V H ,

C 0 =V H V H1V H2 V H1

Max(0 , I X )

+ 1

2(V H2 V H1 )(V H2 V L)2

2

(X V L)2

2 2(X V L)(V H2 X )

+ ( X V L)2 lnV H2 V LX V L

(A.6)

Appendix B: PayPerformanceSensitivity

Following Jensen and Murphy (1990), we denePPS as the change in compensation value associ-ated with a $1000 change in rm value for all pos-

sible liquidation values of the rm, given a xedcompensation package. The value of cash com-pensation is uncorrelated with changes in rmvalue, while the value of share and option com-pensation is positively correlated with changes inrm value. Thus, PPS is zero for cash compen-sation and positive for share- and option-basedcompensation. In our model, the rms value isV 0+ once the manager is hired. As rm valuemoves from V 0+ to V (its liquidation value), thevalue of the managers incentive compensation

changes by

(m Max[V X , 0] + n V + K ) (m C 0+ + n

V 0+ + K ) (B.1)

Rearranging terms, the change in the value of the managers compensation, as a function of the

change in rm value from t = 0+ to t = 2, i.e. asrm value changes from V 0+ to V , is

Pay

=

m (V 0+ X C 0+ ) + ( n + m )Value;when V > X

m C 0+ + n Value ,when V X

(B.2)

We dene PPS as the coefficient of Valuein (B.2), consistent with Jensen and Murphy(1990a,b). It is straightforward to show that PPSis dened as

PPS = n + [m Prob(risky)

Prob( V > X | risky)] (B.3)

Here, Prob(risky) is the probability thatthe manager pursues the risky project, andProb( V > X | risky) is the probability that

the risky project payoff exceeds the option strikeprice, given the risky project is selected.

References

Aggarwal, RK and AA Samwick (1999). Empire-builders and shirkers: investment, rm per-formance, and managerial incentives. Workingpaper. Dartmouth College, Hanover, NH.

Allen, F (2001). Presidential address: do nan-cial institutions matter? Journal of Finance ,

56, 11651176.Bebchuk, L, J Fried and D Walker (2002).Managerial power and rent extraction in thedesign of executive compensation. University of Chicago Law Review , 69, 751846.

Brenner, M, R Sundaram and D Yermack (2000).Altering the terms of executive stock options.Journal of Financial Economics , 57, 103128.

Callaghan, SR, PJ Saly and C Subramaniam(2000). The timing of option repricing. Work-ing paper. Texas Christian University, FortWorth, TX.

-

8/13/2019 Journal of Ekonomi Teknik2

17/18

Stock Options and Managerial Incentives to Invest 45

Conyon, MJ and K Murphy (2000). The princeand the pauper? CEO pay in the United Statesand United Kingdom. The Economic Journal ,100, F640F671.

Core, JE and DF Larcker (2001). Perfor-mance consequences of mandatory increasesin CEO stock ownership. Journal of Financial Economics , 64, 317340.

Datta, S, M Iskandar-Datta and K Raman(2001). Executive compensation and corporateacquisition decisions. Journal of Finance , 56,22992336.

DeFusco, R, R Johnson and T Zorn (1990). Theeffect of executive stock option plans on stock-holders and bondholders. Journal of Finance ,45, 617627.

Demsetz, H and B Villalonga (2001). Ownershipstructure and corporate performance. Journal

of Corporate Finance , 7, 209233.Dimson, E and P Marsh (2001). U.K. nan-

cial market returns, 19552000. Journal of Business , 74, 131.

Fee, CE and CJ Hadlock (2001). Raids, rewards,and reputations in the market for CEO talent.Review of Financial Studies , 16, 13151357.

Friend, I and M Blume (1975). The demandfor risky assets. American Economic Review ,December, 901922.

Garen, J (1994). Executive compensation and

principal-agent theory. Journal of Political Economy , 102, 11751199.Gavish, B and A Kalay (1983). On the asset sub-

stitution problem. Journal of Financial and Quantitative Analysis , 18, 2130.

Gibbons, R, K Murphy (1992). Optimal incen-tive contracts in the presence of career con-cerns. Journal of Political Economy , 100,468505.

Graham, J (1999). Herding among investmentnewsletters: theory and evidence. Journal of

Finance , 54, 237268.Guay, W (1999). The sensitivity of CEO wealthto equity risk: an analysis of the magni-tude and determinants. Journal of Financial Economics , 53, 4371.

Hall, B and J Leibman (1998). Are CEOs reallypaid like bureaucrats? Quarterly Journal of Economics , 113, 653691.

Hall, B and K Murphy (2000). Optimal exerciseprices for executive stock options. American Economic Review , 90, 209214.

Hall, B, and K Murphy (2002). Stock options forundiversied executives. Journal of Account-ing and Economics , 33, 342.

Haubrich, J (1994). Risk aversion, perfor-mance pay, and the principalagent prob-lem. Journal of Political Economy , 102,258276.

Hemmer, T, S Matsunaga and T Shevlin (1996).The inuence of risk diversication on theearly exercise of employee stock options byexecutive officers. Journal of Accounting and Economics , 21, 4568.

Himmelberg, CP, RG Hubbard and D Palia(1999). Understanding the determinants of managerial ownership and the link betweenownership and performance. Journal of Finan-cial Economics , 53, 353384.

Holmstrom, B and J Ricart i Costa (1986).

Managerial incentives and capital manage-ment. Quarterly Journal of Economics , 101,835860.

Ibbotson, R and R Sinqueeld (2001). Stocks,Bonds, Bills and Ination (SBBI) 2000 Year-book . Chicago: Ibbotson Associates.

Jagannathan, R and Z Wang (1996). Theconditional CAPM and the cross-section of expected returns. Journal of Finance , 51,353.

Jensen, M and K Murphy (1990). Performance

pay and top management incentives. Journal of Political Economy , 98, 225264.John, K and T John (1993). Top management

compensation and capital structure. Journal of Finance , 48, 949974.

Johnson, SA and YS Tian (2000). The valueand incentive effects of non-traditional exec-utive stock option plans. Journal of Financial Economics , 57, 334.

Kaplan, R (1984). The evolution of manage-ment accounting. The Accounting Review , 59,

390418.Kole, S (1997). The complexity of compensationcontracts. Journal of Financial Economics , 43,79104.

Lambert, R (1986). Executive effort and theselection of risky projects. Rand Journal of Economics , 17, 7788.

Lambert, R, D Larcker and R Verrechia(1991). Portfolio considerations in valuingexecutive compensation. Journal of Account-ing Research , 29, 129149.

-

8/13/2019 Journal of Ekonomi Teknik2

18/18

46 Tom Nohel and Steven Todd

Litzenberger, R and E Ronn (1986). A utility-based model of common stock price move-ments. Journal of Finance , March, 6792.

Ljungqvist, AP and MA Habib (2003). Firmvalue and managerial incentives: a stochas-tic frontier approach. Journal of Business ,forthcoming.

Milgrom, P and J Roberts (1992). Economics,Organization and Management . EnglewoodCliffs, NJ: Prentice Hall.

Murphy, KJ (1999). Executive compensation.In O Ashenfelter and D Card (eds.), Hand-book of Labor Economics , Vol. 3. Amsterdam:North-Holland.

Nohel, T and S Todd (2003). Compensation formanagers with career concerns: the role of

stock options in optimal contracts. Journal of Corporate Finance, forthcoming.

Ofek, E and D Yermack (2000). Taking stock:equity-based compensation and the evolutionof managerial ownership. Journal of Finance ,55, 13671384.

Rajgopal, S and T Shevlin (2002). Empirical evi-dence on the relation between stock optioncompensation and risk taking. Journal of Accounting and Economics , 33, 145171.

Ross, S (1977). The determination of nancialstructure: the incentive-signaling approach.Bell Journal of Economics , 8, 2340.

Yermack, D (1997). Good timing: CEO stockoption awards and company news announce-ments. Journal of Finance , 52, 449476.