Jordan: Appraisal of Industrial...

75

FILE COPY ReportNo. 1018a-JO Jordan: Appraisal of Industrial Development Bank IncludingIts Small Scale Industry and Handicraft Program June 3, 1976 Industrial Credit and DevelopmentFinance Companies Europe, Middle East and North Africa Regional Office FOR OFFICIAL USE ONLY Document of the World Bank Thisdocumenthas a restricted distribution and maybe used by recipients only in the performance of their official duties. Its contentsmaynot otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Jordan: Appraisal of Industrial...

FILE COPYReport No. 1018a-JO

Jordan:Appraisal of Industrial DevelopmentBank Including Its Small Scale Industry and Handicraft Program

June 3, 1976

Industrial Credit and Development Finance CompaniesEurope, Middle East and North Africa Regional Office

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS(The JD has been pegged to the SDR

since February 1975 with JD = SDR 2.57895.)

Currency = dinar (JD) = 1,000 filsJD1 = US$3.03JD1,000 = US$3,030JD1,O00,000 = US$3,030,300

GLOSSARY OF ABBREVIATIONS

IDB - Industrial Development Bank of JordanIERR - Internal Economic Rate of ReturnIFRR - Internal Financial Rate of ReturnKfW - Kreditanstalt fur WiederaufbauSSI&HP - Small Scale Industry and Handicraft Program

INDUSTRIAL DEVELOPMENT BANK of JORDAN

FISCAL YEAR

January 1 - December 31

PM OFFICAL u ONLYAPPRAISAL OF

INDUSTRIAL DEVELOPMENT BANK OF JORDAN

INCLUDING ITS SMALL SCALE INDUSTRY AND HANDICRAFT PROGRAM

Table of ContentsPage No.

SUMARY ........................... i-ii

I. INTRODUCTION 1......................................... I

II. THE ENVIRr_p.ENT .........

Economic Environment 1The Industrial Sector 3The Tourism Sector 6The Financial Community 7

III. IDB's STRUCTURE ....................... ..*. ........... 10

Establishment and Legal Basis 10Ownership and Control 10Board and Committees. ....................... 11Management and Staff 1lObjectives and Powers .... 12Policies and Procedures . . .. . ........0.. .*... 13

IV. IDB's OPERATIONS .... - . ....... . ...... o............ 16

Characteristics ........................................ 16The Small Scale Industry and Handicraft Program ..... 17Economic Impact .. .............. *.00........0....... 21

V. IDB's FINANCIAL SITUATION .O ..... 000*0.00 22

Resource Position .. ..... 6......i.... .. 22Quality of Portfolio ............................ 000 23Financial Performance and Position ............. 0.... 24Audit *. . . * -. ... ... e* * 25

VI. PROSPECTS ....... **....**.....25

The Environment os* * *o* oo* eo* *** e.* *. ****....*... 25Operations . .. .... .* .......... ... ...... 27Resource Requirements ............ g.....*....o... 28Financial Prospects 28

VII. THE.CREDIT - ITS OBJECTIVES, JUSTIFICATION AND FEATURES. 29

VIII. RECOMMENDATION . ....... ......... o............. .... 31

This report was prepared by Messrs. Henry B. Thomas and Takashi Miyawaki withthe assistance of Mr. J. Chanmugam on the basis of their two-week mission toJordan in November 1975.

This document has a restricted distibuton a may be usd by recipicnts only in the perfonuaceof their official duties. Its contents may not otberwise be discosed without Wori Bank authoiration.

Table of Contents (continued)

BASIC DATA

ANNEXES

1. Industrial Production Index2. Distribution of Establishments in the Industrial Sector by

Principal Cities3. Distribution of Establishments in the Industrial Sector by

Size of Employment4. Domestic Exports5. Visitor Arrivals by Region 1966-19756. Specialized Credit Institutions7. Interest Rates8. Expected Real Financial Charges on Subloans9. List of Shareholders10. Board of Directors11. Organization Chart12. Investment Policy13. Summary of Operations: 1965-7514. Classification of Approved Loans: 1965-7515. A. Resources and Resource Position

B. Notes on Resources16. Loan Portfolio17. A. Income Statements: 1971-75

B. Balance Sheets: 1971-75C. Indicators: 1972-75

18. Projections: 1976-80A. Major Assumptions Underlying the ProjectionsB. Projected OperationsC. Projected Income StatementsD. Projected Cash Flow StatementsE. Projected Balance SheetsF. Projected Indicators

19. Strategy Statement: 1976-8020. Estimated Schedule of Disbursements

MAP

APPRAISAL OF

INDUSTRIAL DEVELOPMENT BANK OF JORDAN

INCLUDING ITS SMALL SCALE INDUSTRY AND HANDICRAFT PROGRAM

SUMMARY

i. The Industrial Development Bank of Jordan (IDB) was established in1965 with the objective of providing term financing for industry and tourism.It is the only such institution in Jordan and plays a significant role inboth sectors. While IDB has been in contact with the Bank Group over severalyears, the proposed IDA credit of $4.0 million would be the first Bank Grouplending to IDB.

ii. The economic development of Jordan has been seriously affected bythe political situation in the region since the 1967 war. The return of in-ternal stability in 1971 permitted the Government to devote more attention toeconomic issues and a Three-Year Plan (1973-75) was published in 1972. Itplaced heavy emphasis on the development of productive sectors, including in-dustry. This Plan has been followed by a Five-Year Plan (1976-80) with thesame emphasis. The Government has actively encouraged the private sectorwith generous incentives and liberal currency regulations.

iii. Most of IDB's activities have been in the industrial sector. Thissector consists of a few large enterprises which, being of national import-ance, enjoy strong Government support and in many cases Government participa-tion in ownership, several hundred medium scale enterprises mainly owned byprivate interests, and several thousand small scale enterprises. IDB's lend-ing, until recently, has been directed at the medium scale subsector. Earlyin 1975 it initiated an experimental program to provide financial and tech-nical assistance to the small scale subsector, the first such program inJordan. By the end of 1975 IDB had made 43 loans to this subsector, averag-ing $4,100 equivalent each. It intends to expand this program in the comingyears.

iv. The tourism sector has received about 15% of IDB's lending. Ithas been especially sensitive to developments in the region but now showssigns of a strong revival.

v. In the absence of a formally organized capital market the mainsources of financing for industrial investment are the promoters themselves,IDB and the commercial banks. During the Three-Year Plan period projectsfinanced by IDB, which are a representative sample of all projects in themedium scale industrial and tourism sectors, received half of their fundingfrom the entrepreneurs' own resources, with IDB providing over 30% of whichmost was to finance imported capital equipment. The contribution of the com-mercial banks during this period was only 14%, and mostly on short-term. TheCentral Bank, which exercises the usual regulatory powers over the commercialbanks, has recently taken several measures to improve the mobilization of

- ii -

local financial resources, to absorb part of the excess liquidity of the bank-ing system and to redirect credit to the productive sectors. These measuresinclude a restructuring of interest rates and the selective use of creditceilings and reserve requirements.

vi. IDB itself is a sound institution with experienced and capable man-agement and staff. Its procedures, especially its appraisal work, are good.It is widely respected within Jordan as a well-run institution. During theThree-Year Plan period it assisted projects accounting for about 75% of pri-vate investment in medium scale industry and perhaps 90% of investment inhotels and related tourism oriented enterprises.

vii. IDB has prepared a strategy statement outlining the objectives ithopes to achieve during the Five-Year Plan period. These include three newinitiatives: establishment of an industrial estate, promotion of new proj-ects and establishment of a management training center. It also intends toexpand its experimental small scale industry and handicraft program (SSI&HP)as well as its normal lending. IDB and the Government have indicated thatthey would like Bank Group assistance and advice as IDB becomes active inthese new areas.

viii. The proposed project has three components. The first is the provi-sion of $3,675,000 million to fill the forecast gap in IDB's foreign exchangeresources directed towards its normal lending activities during the two-yearperiod July 1976 to June 1978. This would represent about 25% of IDB's for-eign exchange needs during this period. This portion of the credit will belent by the Government to IDB on normal Bank terms. The second component isthe provision of $300,000 to help finance IDB's SSI&HP over the same two-yearperiod. An important objective here is to ensure the Bank Group's close asso-ciation with that program to maximize what it can learn from IDB's experienceand to lay the basis for possible future Bank Group assistance to this sub-sector, both in Jordan and elsewhere. This portion will be provided bythe Government to IDB as a grant. The third component will provide up to$25,000 to finance an interdisciplinary study of the small scale industrysubsector. The objective of the study is to gain knowledge of the subsectorwhich IDB's exposure is not likely to provide so that a more complete picturewill emerge of the needs, prospects and constraints of the subsector. TheGovernment will pay for the cost of the study out of this portion of theproposed credit. In addition to financial assistance the project will alsoinclude Bank Group technical assistance to IDB in such areas as improving itsappraisal and supervision work as well as the new fields it plans to enter.

ix. Agreement having been reached on the principal issues, the projectis suitable for an IDA credit of $4.0 million on the usual terms, to be uti-lized as outlined above.

I. INTRODUCTION

1.01 The Industrial Development Bank of Jordan (IDB) was established in

1965 with the objective of providing term financing for industry and tourismin Jordan. It has developed into an efficient development financing institu-

tion with a good record of performance. It recently has undertaken an experi-

mental lending program aimed at snall scale industry and handicraft projects

and intends in the next few years to undertake other new activities. Though

IDB has been in contact with the Bank Group from time to time since its estab-

lishment, the credit proposed in this report would be the first Bank Group

lending to IDB.

1.02 An IDA credit of $4.0 million to the Government of Jordan is pro-

posed. Of this, $3,675,000 will be lent to IDB by the Government on normal

Bank terms for on-lending by IDB to its usual industrial and tourism clients.

This amount will provide about 25% of IDB's foreign exchange resource needs

during the two-year period beginning July 1976; the rest of its foreign

exchange needs is expected to be filled by other foreign loans. A second

portion of $300,000 will be provided by the Government to IDB as a grant for

use by IDB in its small scale industry and handicraft program (SSI&HP). A

third portion of up to $25,000 will be used to finance an interdisciplinary

study of the small scale industry and handicraft subsector. While the Bank

Group can expect to provide IDB with technical assistance relating to its

usual activities as an adjunct to the $3,675,000 portion of the credit, the

main objective in providing funds for the SSI&HP and the study is to ensure

the Bank Group's close association with this subsector to maximize what it

can learn from IDB's experience and to lay the basis for possible future Bank

Group assistance to this subsector, both in Jordan and elsewhere.

II. THE ENVIRONMENT

Economic Environment

2.01 The most recent report on the economy of Jordan entitled "SpecialEconomic Report, Jordan, Review of the Five-Year Plan (1976-80)" (Report No.

1144-JO, dated May 24, 1976) has been distributed to the Executive Directors.

The report embodies the conclusions of an economic mission which visitedJordan in January/February 1976 to review the new Five-Year Development Plan

(1976-80).

2.02 Since the 1967 war the economic development of Jordan has been

seriously affected by the political situation in the region. The occupationof the West Bank with 30% of Jordan's 2.6 million population deprived the

country of most of its agricultural and tourism resources and increased itsdependence on external transfers. The East Bank mostly consists of arid land

with only 5% of the total land area being cultivable. Other natural resources

are also limited with the exception of abundant phosphate deposits. Reflect-

ing the narrowness of Jordan's productive base, services (mainly public serv-ices and commerce) account for about two-thirds of domestic production. In1975 Jordan's (East Bank) GNP per capita was estimated at $590.

-2-

2.03 The return of internal stability in 1971 permitted the Governmentto devote more attention to medium- and long-term economic issues. In 1972the Government published a Three-Year Plan covering the 1973-75 period. Themain targets of the Plan were to achieve an 8% p.a. growth of GDP at 1972prices, to reduce the 8% unemployment rate and the serious underemployment inthe East Bank, to phase out the economy's heavy dependence on foreign budgetsupport by reducing the budget and trade deficits through increased domesticrevenues and foreign exchange earnings and to foster a more equitable distri-bution of economic gains between the various income groups and geographicalregions. To achieve these targets, the Plan envisaged a thorough restructur-ing of the economy by reducing its heavy reliance on services of which defensewas a major part, and by developing agriculture, manufacturing and mining boththrough institutional and infrastructure support to private initiative andthrough public investment in productive enterprises.

2.04 Development performance during the Plan period was a mixed success.The real annual growth rate of GDP over the three-year period was of the orderof 3% per year as a result of poor weather conditions and slow growth in com-merce and services following the October 1973 war. However, mining and manu-facturing grew at an annual rate of 10%. Rock phosphate accounted for much ofthis increase following a doubling of production coupled with a five-fold in-crease in the world price between July 1972 ($11.4/ton FOB Jordan Rock) andJanuary 1975 ($56/ton). The real annual growth rate of the manufacturingsector taken alone was a little over 8% and capacity utilization improved dur-ing the three-year period to reach 95% in 1975. With a 6% p.a. growth rate,the construction sector also achieved a better than average performance, duemainly to increased remittances from Jordanians working abroad which fueleddemand for investment in housing and for related industrial inputs.

2.05 Although the Three-Year Plan aimed at reducing reliance on externalsources to fill the country's chronic resource gap, the trade balance deficitactually increased from JD 81 million in 1973 to JD 115 million in 1974 andan estimated JD 147 million in 1975 as a result of sharp increases in theprices of Jordan's imports such as food and capital goods, only partiallycompensated for by the five-fold increase in phosphate prices. Fortunatelythis trade deficit was covered by significant increases in unrequited trans-fers (from JD 65 million in 1973 to JD 151 million in 1975) and in workers'remittances (from JD 15 million in 1973 to JD 53 million in 1975). However,the availability and adequacy of these resources in the coming years is un-certain, at a time when the need for external resources to carry out the in-vestment program contained in the country's new Five-Year Plan will be veryhigh. Jordan will thus continue to need substantial external financial as-sistance.

2.06 Jordan experienced considerable price stability for many years untilthe early 1970's. Prior to 1967 the overall price level experienced an aver-age annual increase of only 2%; from 1967 to 1971 the increase was 4.6% p.a.However, the Amman cost of living index indicates that the general price levelincreased by 8.1% in 1972, 10.4% in 1973 and a record 20.0% in 1974, slightlybelow the international inflation rate estimated at 21.7% for that year. The

-3-

increase in the index was about 12% in 1975. Depending on supply conditions,particularly in agriculture, and on aggregate demand levels, which will belargely influenced by the rate of implementation of Plan targets, inflationin Jordan is expected to continue at its current level of 12% per annum dur-ing the first two years of the Five-Year Plan period, and should drop duringthe latter years of the Plan and subsequently decline to about the interna-tional rate of inflation, which according to Bank projections should fall from10.8% in 1975 to 7.0% in 1980 through 1985. To some extent, the higher ratesexpected in the initial years of the Five-Year Plan result from a bunching ofplanned investment expenditures during that period. However, there may occursubstantial slippages in the actual timing of investments which would lowerpressures on domestic resources, resulting in a lower rate of inflation.

2.07 It appears that unemployment is no longer a problem in Jordan.Emigration to the Gulf States and expanded employment opportunities in Jordanhave created a labor shortage, in particular in the skilled and foremanclasses, which might prove one of the most serious constraints in the imple-mentation of the Five-Year Plan. This shortage has led to increases in wageswhich now appear to reflect correctly the opportunity cost of labor. Jordan'shigh literacy rate (65% in 1974) and pool of entrepreneurial skills suggestthat the country enjoys some comparative advantages over its neighbors for itsindustrial development.

The Industrial Sector

2.08 Preliminary results from the 1975 industrial census 1/ indicate thatthere were 7,478 industrial enterprises (both mining and manufacturing) on theEast Bank of Jordan in 1974, employing some 26,700 workers. Fixed assets atthe end of 1974 were estimated at JD 69.0 million. The value added by thissector in 1975 was estimated at JD 45 million and represented about 15.6% ofGDP at factor cost. By contrast, this sector contributed only JD 20 millionor 11% to GDP in 1972. Using as weights 1970 prices, the industrial produc-tion index for about 15 major commodities also shows the steady growth of thissector, except during the 1967 war and the 1970 domestic disturbances (seeAnnex 1). The index increased by 9.9% in 1973, by 6.1% in 1974, and by 7.2%in 1975.

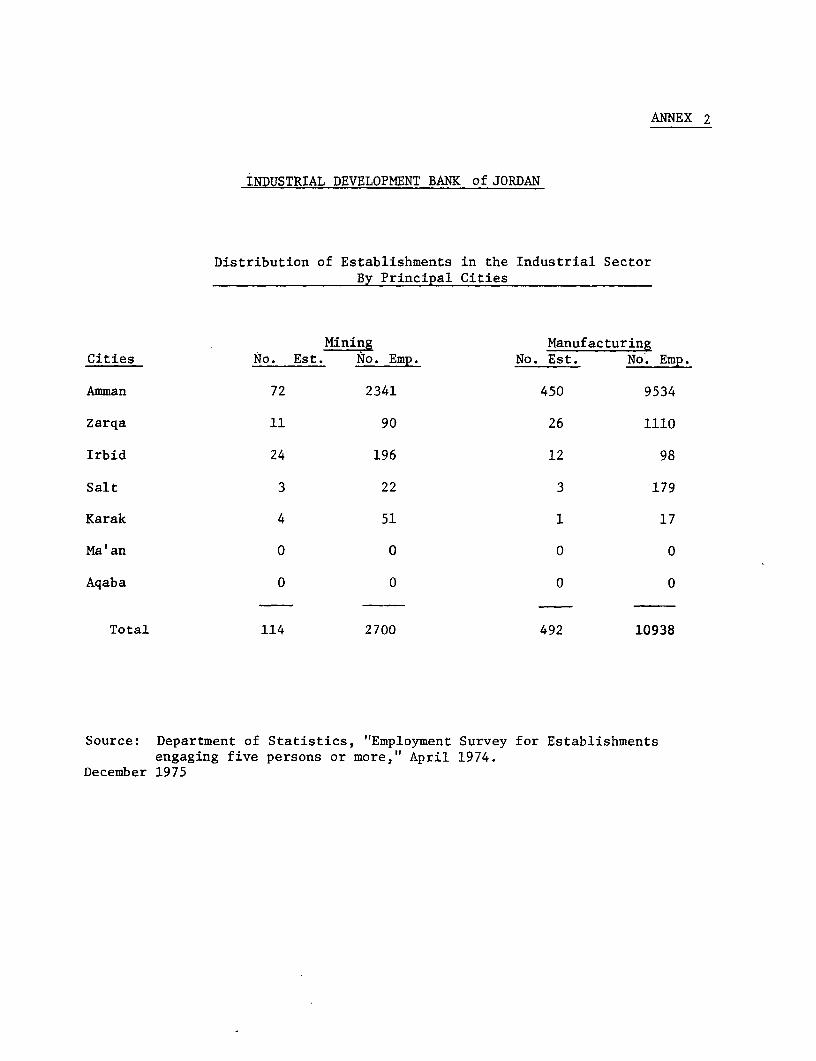

2.09 Existing industrial activities are heavily concentrated in the Amman-Zerka area. Of 606 firms covered in the 1974 employment survey 2/, as manyas 559 were located in this area (see Annex 2). However strains are beginningto appear due to such a concentration, particularly with regard to the supply

1/ This census, the results of which are still being tabulated, covered thevery smallest enterprises (1-4 employees) through the largest (over 200employees).

2/ This survey did not cover the very smallest enterprises (1-4 employees).

- 4 -

of power and water. The Three-Year Plan called for a better geographical dis-tribution of industry, but progress in this direction was and will continueto be slow because of the absence of both infrastructure and markets in thesmaller population centers.

2.10 Industrial activity in Jordan can be conveniently separated intolarge scale enterprises which, being of national importance, enjoy strongGovernment support and in many cases Government participation in ownership,medium scale enterprises which, while encouraged by Government, are almostcompletely privately owned, and small scale enterprises which until recentlywere more or less neglected by Government. The 1974 employment survey indic-ated that among the 606 establishments covered, the 36 largest (employing 50or more workers) accounted for 57% of total industrial employment (see Annex3). Of even greater significance is the dominant role of the eight largestfirms, each of which is the only one of its kind in Jordan and which togetheremploy 38% of the total. In a 1971 survey they were estimated to account forover half of the fixed assets held by the sector and almost half of the in-dustrial sector's contribution to GDP. These firms are the phosphate mine,the cigarette factory, the tannery, the pharmaceuticals company, the oil re-finery, the cement mill, the rolling mill and the wet batteries factory.

2.11 Medium scale industry is mostly composed of enterprises producingconsumer goods for export or import substitution. Major industries in thissub-sector are food processing (mostly flour milling, oil pressing and olivepackaging), clothing, textiles and footwear, and the fabrication of metalproducts (hand tools, structural metal products and metal furniture). Thissubsector has played a growing role in the past few years. While its exportsare small compared to those of the large scale enterprises (see Annex 4),they are increasing significantly. IDB estimates that about one-third of itsrecent projects, which are by and large all medium scale enterprises, are ex-port oriented. One result of the comparatively tight labor market is thatJordanian industry is tending to become relatively sophisticated and capitalintensive, enabling it to become technologically advanced in relation tocompeting industry in neighboring countries. The resulting higher qualityof its products has enhanced their acceptability in these markets. Ceramics,tiles, marble products, aluminum window and door frames, plastic products,and paints are some examples of products which are being successfully sold inthese markets. Using the projects financed by IDB as a sample, profits madeby medium scale industries are rather attractive: in 1975 the ratio ofprofit before interest to capital employed ranged from 16% (paints) to 58%(tiles) and as high as 77% in cosmestics and detergents.

2.12 The 1975 industrial census attempts to cover for the first time thesmall scale industry subsector (firms employing less than five workers) aswell as the medium and large scale subsectors. Of the 7,478 firms covered,fully 6,887 were in this category. They employed about 10,800 workers versusthe almost 16,000 employed by the larger firms. Clearly this is a substantialsubsector, and one which until recently has almost totally lacked institutionalsupport. This subsector is a mixture of very small scale industries, handi-crafts and household or "cottage" industries; almost without exception they

- 5 -

all originated from some form of household industrial activity, the most suc-cessful ones emerging into small factories with some division of labor andan emerging need for planning and technical assistance. Stone cutting andcarpentry are typical examples of small scale industry in Amman, tailoringand traditional embroidery are examples of Jordan's cottage industries whilepottery and wood carving are among the most popular handicrafts. There arealso some "mode-rn small industries" such as ready-made clothing produced bysmall factories for delivery to large stores.

2.13 Incentives. Under the Encouragement of Investment Law projectsthat are approved by a committee chaired by the Minister of Industry andTrade are granted exemptions from income and social services tax for sixyears (nine if they are outside the Amman-Zerka area), from custom duties andother charges on imported fixed assets during the period of project implemen-tation, and from building and land taxes for five years (seven if outsideAmman-Zerka). Projects outside the Amman-Zerka area may be granted, free ofcharge, tracts of government land. Foreign capital invested in an approvedproject, whether in conjunction with local capital or not, is given the sametreatment as local capital. In addition, the Law contains provisions facil-itating the transfer outside the country of profits and interest earned onforeign investment, the investment itself, and salaries earned by expatriatestaff. To qualify for these benefits, however, a project must have fixedassets excluding land of at least JD 5,000 (JD 15,000 in the case of tourismprojects).

2.14 The provisions of the Law are quite generous and in general welldirected, although their selectivity might be improved as industrial activitygrows. Most investment projects qualifying under this Law are submitted forapproval. During 1972-75, the committee approved 105 projects involving cap-ital investments totalling JD 21 million. Besides the exemptions allowed inthe Law, if a suitable case is presented custom duties on imported raw mat-erials and components may be waived or reduced, and protective duties on im-ports of competing products raised or imposed. Amendment of the present Lawis under consideration to further enhance its incentives.

2.15 Licensing. Under the Licensing and Control of Industry Instruc-tions of 1973, no new industrial establishment may be set up and no existingindustrial establishment may be modernized or expanded without having ob-tained a license from the Ministry of Industry and Trade. (Projects in thetourism sector must obtain a similar license from the Ministry of Tourism andAntiquities.) For a project costing less than JD 5,000, a license is rou-tinely issued without specific requirements. For a project which costs morethan JD 5,000, the Ministry asks for a study of the project to check its eco-nomic and technical feasibility.

2.16 In the last few years, licenses have been issued rather liberally.This reflects a change in policy towards industrial development. Until abouttwo years ago the Government sought to limit the number of establishments ineach field to what it felt the limited domestic market could sustain. How-ever, because of this limited market, many enterprises successfully turned to

-6-

foreign markets. Encouraged by this trend, the Government has adopted a newpolicy allowing "industrial duplication", i.e., the establishment of severalenterprises in the same line of production. The underlying reasoning is thatmore competition will encourage industrial enterprises to break into foreignmarkets and bring about more growth. This liberal approach has enhanced theopen atmosphere of Jordan's business climate without apparently leading toexcess capacity.

2.17 Industrial establishments are also required to obtain a license toimport machinery, equipment, spare parts, or raw materials. Reflecting theliberal project licensing, import licenses are also issued quite liberally,though the mechanism itself is intended to control allocation of foreign ex-change. Commercial banks, on the strength of this license, are authorizedby the Central Bank within certain limits to issue a foreign exchange permit.Thus an industrialist, once his project has been licensed, and because of thepresent availability of foreign exchange, is able to obtain foreign exchange

quite easily.

2.18 Tariff Protection. Industry enjDys varying degrees of tariff pro-tection from competing imports originating from outside the Arab countries.Tariffs on typical industrial products are in the 10-30% ad valorem range,although a few selected manufactured imports such as confectionery, shoes,furniture and tomato sauce carry tariffs of more than 50%. However, importsfrom the Arab Common Market (Egypt, Syria, Iraq and Jordan) as well as im-ports resulting from bilateral trade agreements with the countries of the

Council of Arab Economic Unity do provide a considerable measure of competi-tion for Jordan's industrial firms.

The Tourism Sector

2.19 An inevitable result of the 1967 war and the disturbances in Jordanin the following years was a precipitious drop in tourist traffic. As a re-sult of the occupation of the West Bank, Jordan was also deprived of her bestknown attractions and of 80% of her hotel capacity. Recently, though, a re-covery of the tourism sector has been felt. In 1975 the number of visitorsreached an estimated 767,000, surpassing the 1966 peak of 619,000 visitors bya substantial margin (see Annex 5). Jordan is a gateway not only for Moslempilgrims en route to Mecca but also for an increasing number of visitors tothe West Bank from Western countries. Some of these visitors take advantageof their stopover in Jordan to visit historical sites on the East Bank. Forexample, there were about 41,000 foreign visitors to the archaeological siteof Petra in 1975.

2.20 In general, the development of tourist facilities on the East Bankhas lagged behind the growth of foreign visitor demand, especially for accom-modation of international standard. As a result of the recent shortage ofhotel rooms, occupancy rates and financial returns for hotels are relative-ly high. In response to this situation, a number of hotels are either underconstruction or in the planning stage. In addition other tourist facilitiessuch as shops, restaurants and transportation facilities are also being ex-panded.

-7-

2.21 Gross foreign exchange earnings from tourism have grown from JD 4.6

million in 1968 to JD 32.2 million in 1975, representing over 28% of total

1975 exports of goods and services. Net foreign exchange earnings from tour-

ism, after deducting imported goods and services, are estimated to be about

70% of gross receipts. Direct employment in tourism facilities is presently

estimated at 4,000.

The Financial Community

2.22 The financial community in Jordan consists of the Central Bank,

eleven commercial banks, six specialized credit institutions and several in-

surance companies. The Post Office began a Savings Fund in September 1974.

There is no organized capital market.

2.23 The Central Bank. The Central Bank, established in 1964,. has the

usual regulatory power over the commercial banks. It can establish interest

rates and regulate credit as well as establish reserve requirements, liquid-

ity requirements and the capital/deposit ratio (currently 10%). It makes a

market in Government Treasury Bills (first issued in 1969) and Bonds (1971).

It offers rediscount facilities to banks and specialized credit institutions

at 5% p.a.

2.24 The Commercial Banks. There are eleven commercial banks operating

in Jordan. Four are incorporated in Jordan, three in other Arab countries

and four in other countries (a fifth is expected to open in 1976). These

banks had 73 branches in Jordan at the end of 1975, 43 of which were in Amman.

Credit facilities extended by the commercial banks have been growing steadily,

more or less in line with growing deposits and total assets. Outstanding

credit at the end of 1975 totalled JD 121.4 million, a 45% increase over the

year before. However, this represented only 57% of the banks' total assets.

The vast majority of these credits are bill discounting and short-term loans

and advances, including overdraft facilities. While the banks are not yet

prepared to lend substantial amounts on long-term, due mainly to their con-

servative approach and to the still unsettled conditions in the area, they

do roll over their short-term advances quite freely, particularly for their

established clients.

2.25 Bank lending to industry accounted for only 12% of total bank lend-

ing at the end of 1975. General commence and trade received the bulk of bank

credit (42%) with construction and the purchase of land and buildings being

the second largest category (22%). The banks rarely if ever lend to small

scale industry, the main reason being the lack of sufficient security. They

do hold a substantial amount of Treasury Bills and Government Bonds (11% of

total assets) and maintain large deposits with the Central Bank (15% of total

assets, or 21% of deposits versus the 12% reserve requirement). In view of

this liquidity, the banks rarely use the Central Bank's rediscount facility.

On the whole the structure of commercial bank assets reflects a traditional

outlook which will have to give way to more dynamic banking policies if these

banks are to play a more active role in Jordan's industrialization.

2.26 Until recently the Jordanian commercial banks have been ill-equip-ped to engage in sophisticated international banking activities, due in partto restrictions on foreign account operations. In a recent move that must beinterpreted in the context of the virtual immobilisation of the Lebanese bank-ing system over the past few months, the Central Bank has authorized the com-mercial banks to exclude their non-resident deposits in foreign currencies,including deposits by Jordanians residing abroad, from the 12% legal reserverequirement, and to place these funds with their correspondents abroad in-stead of placing them with the Central Bank. This move should enable commer-cial banks to offer more competitive interest rates and to play a more activerole on the Arab and international capital market.

2.27 The Specialized Credit Institutions. The six specialized credit in-stitutions, including IDB, are each incorporated under a special law and ex-tend medium- and long-term credit for specific purposes in different sectors.None compete with IDB. They are briefly described in Annex 6.

2.28 Other Financial Institutions. There are some 25 insurance com-panies and agencies or branches operating in Jordan, of which seven areJordanian. Premium income is small (JD 2.7 million in 1973) and is investedin real estate, government securities and, to a small extent, in equities oflarge corporations. The amounts deposited with the Post Office Savings Fundare still quite small and this too is not a source of industrial finance.On the other hand, a pension fund recently established by the Government hasthe potential to become a source of funds for long-term investment.

2.29 Though there is no organized capital market, there are about tenprivate brokers who handle transactions in shares. The volume is small(there are no statistics available), if only because the number of companieswith public ownership is small. Despite the narrowness of the market theGovernment is actively encouraging equity participation by the private sec-tor in several major industrial ventures (e.g. refinery, cement). The onlydebt instruments available for trade are Government Bonds which are mainlyhandled by the banks. The new Five-Year Plan foresees the issuance of deben-tures by large corporations. Following a request from the Government, IFChas been providing some technical assistance to the Government for the estab-lishment of a securities market in Jordan. IFC advice has been particularlysought for the drafting of a new Capital Market Bill.

2.30 Interest Rates. As noted in paragraph 2.06, Jordan experienced alow level of inflation up to the early 1970's. This was still reflected inthe interest rate structure as of September 1975, given in Annex 7, whichhad essentially remained unchanged for many years. Whereas until the early1970's the structure was positive in real terms, in 1975 it had become nega-tive and had fallen out of line with trends in the international capitalmarket. To reverse this trend and encourage the channeling of private savingsinto the banking system, the Central Bank on January 1, 1976, raised the mini-mum interest rates payable by commercial banks on savings and time deposits.These rates now range from 5 to 5-1/2%, as opposed to the 2-1/2 to 3-1/2%

- 9 -

minimum rates prevailing earlier. As a result of this increase in the costof funds to the commercial banks, the minimum lending rate charged to primeborrowers has been increased from 6.5 to 7.5%.

2.31 The recent increase in the long-term lending rate of IDB from 8 to9% has to be seen in the light of this general overhaul of the interest ratestructure in Jordan. Although the increase in IDB's lending rate to 9% wouldnot bring it up to the inflation rates expected for the next three or fouryears (see Annex 8), this increase does reflect the effort by the Governmentto rationalize the interest rate structure. Since there are clear signs thatthe inflation rate is slowly moving downward, the increase represents themaximum that can be expected from the Government at this time. The Govern-ment is indeed rightly concerned about the expectation effects of too largean upward adjustment in interest rates which would have the tendency to signala continuation of high inflation rates to consumers and investors. Also theGovernment intends to maintain an incentive to investors in the form of an at-tractive long-term interest rate at a time when investment activity in Jordanis gaining momentum.

2.32 Other recent steps taken by the Central Bank to reduce excessivemonetary and credit expansion of the commercial banking system while direct-ing more financial resources to the industrial sector include the following:

(i) reducing from 80% to 75% the credit-deposit ratio for thecommercial banks; the ratio is expected to be further re-duced to 70% in July 1976;

(ii) limiting the expansion of credit by the commercial banksin the first six months of 1976 to not more than 10% abovethe level extended in the previous six months. Creditextended to joint-stock industrial companies is exemptedfrom this ceiling; and

(iii) imposing an additional 3% reserve requirement on commercialbank over-drafts for all purposes, except on loans to joint-stock industrial companies. This last measure became effec-tive on March 1, 1976.

2.33 Mobilization of Local Currency Resources. During the Three-YearPlan projects financed by IDB, which are a representative sample of all proj-ects in the medium scale industrial and tourism sectors, received half oftheir funding from the entrepreneurs' own resources. IDB provided over 30%,of which most was to finance imported capital equipment. The contribution ofthe commercial banks, the only other potential source of long-term funds inJordan during this period, was small (14%), and then mostly on short-term.Thus, the main source for long-term local currency funds was the promotersthemselves. While this pattern of financing may well continue in the future,the authorities are aware of the need to better mobilize local currency re-sources for productive investment in all sectors, not only those presently

- 10 -

served by IDB. Recent Government actions, summarized in paragraphs 2.30-2.32above, toward a restructuring of interest rates and reserve requirementsshould be seen as evidence of a serious commitment by the Government to im-prove the mobilization of local financial resources.

III. IDB's STRUCTURE

Establishment and Legal Basis

3.01 IDB was established in 1965 in accordance with a special Law whichprovides IDB with certain privileges and powers not available to companiesestablished under the Companies Law. The most important of these are thatpreference shares issued to the private sector carry a minimum 6% tax freedividend guaranteed by the Government, IDB is exempt from all taxes, thenominal value of the preference shares is guaranteed by the Government incase of liquidation and, at IDB's option, its loans can be collected by theGovernment under the terms of the Law for the Collection of Government Funds.IDB has never had to call on the Government to meet the preference sharedividend nor has it turned any loan over to the Government for collection.

3.02 The IDB Law provides that IDB has a prior charge over a borrower'sassets. This provision created some difficulty in arranging the financingplan for one project which involved IFC (Jordan Ceramic Industries Company)and resulted in IDB's not lending to the company but instead making a standbyequity investment commitment. IDB's management considers this an isolatedincident not warranting a change in the provision. The Law is satisfactoryand provides IDB with sufficient flexibility to carry out its objectives.

Ownership and Control

3.03 IDB's authorized share capital is JD 3 million divided into or-dinary and preference shares with par values of JD 1. Ordinary shares canbe owned only by the Government; preference shares, only by the Jordanianprivate sector or by foreign investors. With the exception of dividend andliquidation rights and the voting procedures for the Board of Directors, thetwo classes of shares are equal. Besides the minimum 6% dividend guaranteedto preference shareholders, these shareholders have the right to receivedividends of up to 10% before the ordinary shares attract any dividends.

3.04 Initially one million ordinary shares and two million preferenceshares were authorized. In 1971, however, the Government bought 110,000shares previously held by a private bank. These shares were converted to or-dinary shares and the number of authorized ordinary shares was increased to1.11 million with a similar decline in the number of authorized preferenceshares.

3.05 The Government has subscribed to and fully paid for all the author-ized ordinary shares. Some 840 individuals and institutions, including somenon-Jordanians, have subscribed to 1.13 million of the preference shares (see

- 11 -

Annex 9). The initial payment schedule for these shares called for periodicinstallments through December 1967. The 1967 war disrupted this timetable,however, with the result that investors from the West Bank were unable tomake their final payments. These payments are being made from the dividendsdeclared on these shares; only some JD 1,000 remains to be paid.

3.06 The preference shares are widely held with no one investor holdingmore than 5% of the total. The major shareholders are commercial banks oper-ating in Jordan. There is, however, no dominant group of private shareholdersexercising effective control over IDB's activities. The Government, of course,is in a position to effectively control IDB but has refrained from doing so.In any case, the IDB Law prohibits IDB from adopting policies which conflictwith those of the Government. IDB has established an effective working rela-tionship with the various Government departments while maintaining its auto-nomy in decision-making.

Board and Committees

3.07 The IDB Law specifies that the Board of Directors shall have fromnine to 15 members, as well as specifying who each member is to represent.Of the basic nine-man membership, three represent the Government and six theprivate sector; this reflects the division of the authorized (though not ofthe issued) capital between ordinary and preference shares. The remainingsix seats are reserved for representatives of private shareholders holding 10%or more of the authorized capital; as there are no such shareholders, theseseats are not filled. The present Board membership is given in Annex 10.

3.08 The three Government representatives are appointed by the Ministerof Trade and Industry, the President of the National Planning Council and theGovernor of the Central bank. The Chamber of Industries appoints one director.Two directors represent commercial banks, rotating each year. Three directorsare elected by the preference shareholders, excluding the commercial banks.Directors serve for three years, excepting those representing the commercialbanks. The General Manager attends meetings as a non-voting participant.

3.09 By tradition the Chairman is one of the Directors representing thepreference shareholders. The IDB Law requires that the Board meet at leastonce a month; in fact it meets some 14 times a year. Attendance at meetingsis excellent. Two-thirds of the members are required for a quorum and deci-sions are taken by a simple majority of those present. The Board determinesgeneral policy and approves all loans over JD 10,000 and all equity invest-ments. It has delegated approval of loans up to JD 10,000 to a Loan Commit-tee consisting of the General Manager, his Deputy, and the Division Heads.The Board does not concern itself with internal, day-to-day matters, leavingthese to management.

Management and Staff

3.10 IDB has operated in the past with a very small staff. From itsfounding in 1965 up to 1971 the number of staff remained fairly constant atabout 18, including eight professionals. Since 1972, however, there has been

- 12 -

a drive to recruit new staff members, especially professionals, in order tokeep pace with IDB's expanding business. By the end of 1975 the total staffhad expanded to 35, including 21 professionals. Members of the professionalstaff have attended a number of training courses, including those offered byEDI, and have spent time working in other mature DFCs. As a result they, andespecially the senior staff, are quite familiar with current development bank-ing procedures.

3.11 As can be seen from the organization chart (Annex 11), IDB is or-ganized along traditional lines. There are separate investment, technicaland follow-up divisions as well as the usual support divisions. Very recentlycreated is a separate division to handle IDB's SSI&HP. During 1976 IDB in-tends to recruit five more professionals for the existing divisions in anti-cipation of further growth in its business. It also intends to establishanother new division during 1976, the Research and Project IdentificationDivision, and to recruit at least two new staff members for it. This divi-sion will handle IDB's promotional work which is expected to be undertakenduring the Five-Year Plan period.

3.12 Mr. Ziyad Annab has been the General Manager since joining IDB inJune 1966 following a distinguished career with the Government. He is an ex-perienced, capable and articulate individual who has provided strong and ef-fective leadership. He is ably assisted by Mr. Rajab As-Saad, Deputy GeneralManager, who joined IDB in October 1965. The four Division Heads have beenwith IDB for between eight and ten years each. They are all well qualifiedfor their positions. Mlorale among the staff is excellent, in part becauseworking conditions and remuneration are well above average by Jordanian stand-ards but mainly because of the open and participatory style of management.

Objectives and Powers

3.13 The IDB Law provides a broad mandate for IDB. It is to financeprivate industrial, tourism and mining projects registered in Jordan throughloans, equity participations, underwriting and guarantees. It is also toassist in developing a stock market and in encouraging the private ownershipof shares and bonds, to provide technical assistance, to promote new projectsand to help small industries. It is prohibited from financing agriculturalprojects, public utilities or government or municipality projects.

3.14 To date it has concentrated its efforts on making loans to indus-trial and tourism projects, and on providing these clients with technical as-sistance. It has taken some equity participations but the scope for thisactivity in Jordan is small as most companies are organized as partnerships.The promotion of new projects, and the investment in their share capital, wasexpected to be the main activity of the Industrial Development Corporation, agovernment-owned entity that was established in mid-1973. As this companynever became active and has since been dissolved, IDB is expected to becomeactive in this area in the future.

- 13 -

3.15 In view of the large number of relatively small loans that IDB has

made in the past, it can be inferred that IDB has provided some assistance to

small industries. However, it has not directly assisted the very small entre-

preneurs until very recently. This new activity is described in paragraphs

4.07-4.25.

Policies and Procedures

3.16 Policy Statement. IDB's Board adopted an Investment Policy state-ment in 1965. It appears as Annex 12, as amended to the present. This state-

ment contains most of the provisions relating to investment policy normallyfound in such statements. What is not covered in the statement is covered in

the IDB Law. For example, the Law prohibits a Director from attending Boardmeetings at which matters in which he has a special interest (including finan-

cial assistance to projects in which he holds more than 5% of the share cap-ital) are to be discussed.

3.17 Following discussions with the appraisal mission, IDB's management

intends to suggest to its Board certain modifications in the statement. Thesewould include a change in paragraph 3 to increase the amount of IDB's paid-in

capital that could be invested in equity participations from the present 25%to perhaps 100%, an alteration in paragraph 5 to define the base for singleexposures as paid-in capital and reserves and to increase the percentage of

this base that may be lent or otherwise invested in a project from 10% to per-haps 20%, and a clarification in paragraph 6 to indicate that in the case of

expansion projects IDB's total exposure would not exceed 50% of the total in-vestment in the existing as well as the expansion project.

3.18 With regard to IDB's reserve policy, the IDB Law requires that 25%

of IDB's profit be allocated each year to a statutory reserve. In addition,IDB has followed the policy of allocating 10% of profits to the provision forlosses. It has steadily increased the tax-free dividend paid on preference

shares from the guaranteed minimum of 6% to 8% in 1975 and intends to con-tinue increasing this dividend to 10% (after which ordinary shares would be-

gin to attract a dividend too). This policy is designed to enhance the at-tractiveness of IDB's preference shares relative to alternative investments(for example, Government development bonds which yield 8% tax-free) so that

IDB will be able to increase its share capital when this becomes necessary.In the few transactions that take place IDB's preference shares now trade atpar, though they were trading at below par a few years ago.

3.19 Foreign Exchange Risk. The foreign exchange risk on loans made by

IDB from foreign lines of credit has been borne by the Government (all of

IDB's loans are denominated in local currency). The Government has confirmed

that it will continue to bear this risk since this is seen by the Governmentas a further incentive to industrial investment. At present, with foreignexchange apparently readily available from the Central Bank for any projectthat is licensed (see paragraph 2.17), an increase in IDB's lending rate for

foreign exchange loans would make such loans uncompetitive with local cur-

rency loans; under the existing regulations the proceeds of these loans canbe easily converted into foreign exchange.

- 14 -

3.20 Project Appraisal. The Ministry of Trade and Industry and theMinistry of Tourism and Antiquities routinely send IDB a copy of each licensewhen it is issued for an industrial or a tourism project. IDB in turn con-tacts each licensee to offer him technical assistance in carrying out hisproject and to indicate that it is prepared to consider providing financialassistance. About 70% of the licensees reply. This is the main source ofIDB's present business, and allows IDB to become involved at an early stagein the formulation of most projects it finances.

3.21 Prospective clients meet initially with the Head of the InvestmentDivision who determines whether the proposed project is suitable for IDB. Ifso, a team consisting of either a financial analyst or an economist and anengineer meet with the entrepreneur to discuss the project and IDB's require-ments in detail. The team will help the client prepare his project if neces-sary. Project preparation can often stretch over several years while theclient searches for suitable land, locates partners, obtains building permits,etc. Once the project has been prepared and appraised, a report is preparedcovering the financial, economic and technical aspects of the project. Thisreport is considered by the Loan Committee and, if found satisfactory (andthe loan amount is over JD 10,000), sent to the Board for its consideration.

3.22 IDB's appraisal work and its reports have undergone considerable im-provement and broadening in recent years. Earlier reports, for example, didnot separate fixed assets into sub-categories such as land, buildings and ma-chinery, or forecast financial results; they now do. Recently IDB has begunto calculate the internal financial rate of return (IFRR) for most projectsand is preparing to calculate the internal economic rate of return (IERR). Onbalance, IDB's appraisal work now is quite good. Further improvement can bemade, however. While the appraisal reports cover the factual aspects of proj-ects quite completely, they often lack sufficient analysis of these facts.The assumptions underlying the conclusions in the reports are often not stated.IDB's management is aware of the deficiencies and is continually working toimprove appraisal work. It anticipates that an association with the BankGroup will be helpful in this regard.

3.23 IDB has undertaken to calculate the IERR as well as the IFRR on allprojects it submits to the Bank for financing under the proposed line of cred-it that are above the free limit. As there appear to be few systematic dis-tortions or subsidies within the Jordanian economy (other than tariff protec-tion in some cases), it seems likely that the IERR will often not be signif-icantly lower than the IFRR. In such cases IDB will not be required to makeboth calculations but instead will provide a statement explaining why theIERR would not be lower than the IFRR.

3.24 Project Supervision. The Follow-Up Division was established as aseparate division in 1971. It is still in the process of developing andrefining its procedures, though a fairly definite pattern has already evolved.It is clear that IDB recognizes the importance of closely following the pro-gress of its clients, not only to anticipate problems but also so that its

- 15 -

appraisal techniques benefit from past experience, and continued emphasis onthis aspect of its operation can be expected.

3.25 Supervision during the disbursement of IDB's loans is quite intense.Site inspections are frequently made. When IDB's loan is about half disburseda progress report is prepared discussing, among other things, any delays theproject is experiencing. When disbursements are completed a completion reportis prepared which compares actual costs and timing with those forecast in theappraisal report.

3.26 Once a project has started operations IDB requests quarterly reportsfrom its clients. However, IDB usually only receives annual reports, and thenonly from the, larger firms. IDB faces two general difficulties in obtainingbetter compliance with its reporting requirements. Its clients are often sus-picious of IDB's motives in requesting financial and operating details. IDB ismaking progress in gaining its clients' confidence in this area by demonstrat-ing the benefits its clients can gain by a continued close association with it.Secondly, the smaller firms usually do not have well enough developed account-ing procedures to enable them to produce the required reports. When reportsare not received, IDB attempts to obtain the data through visits to the firms.

3.27 A report is usually prepared once a year on each firm in operation.This report compares actual results with those forecast and focuses on prob-lem areas. Clients that are experiencing little difficulty are visited oncea year; those with problems, more often. As the vast majority of IDB's proj-ects are located in or near Amman, IDB is able in fact to adhere quite closelyto this visitation schedule. As a result of these fairly frequent visits andbecause of IDB's widespread contacts within the relatively small industrialcommunity, IDB is able to follow quite closely the progress of most of itsclients.

3.28 Procurement. Most projects are too small to justify internationalcompetitive bidding. IDB does require that its clients provide quotes fromat least two suppliers in all cases. The reasonableness of these quotes arereviewed by IDB. In some cases visits to the suppliers in Europe or else-where are made. In other cases the services of consulting engineers are used.IDB's procurement procedures are satisfactory.

3.29 Disbursements. Disbursements for machinery and equipment are madeon the basis of invoices and, in the case of imported goods, bills of lading.Disbursements for construction are made on the basis of documents indicatingthe progress made, which are checked by site visits. Disbursements practicesand procedures are satisfactory.

3.30 Internal Reports. IDB has instituted a comprehensive system of re-gular internal reports. Each month reports are prepared and circulated with-in the institution covering applications approved during the month and cur-rently under study, disbursements made during the month and expected to bemade during the next three months, repayments due and received, arrears,

- 16 -

IDB's financial position (trial balance sheet, rebouiae statement and proj-ected cash flow), etc. These reports, combined with IDB's small size andopen atmosphere, allow management and senior staff to keep up to date on allof IDB's activities.

IV. IDB's OPERATIONS

Characteristics

4.01 A summary of IDB's operations since its establishment is containedin Annex 13. While it has approved several equity investments, most of itsactivity has been confined to the granting of loans. The year to year trendin loan approvals reflects the changing political situation in the MiddleEast. After a promising first full year of operation in 1966 (approvals to-talled JD 933,600), business dropped drastically in 1967 (approvals were onlyJD 472,800) and by 1969 had only recovered to about 80% of the 1966 level.The internal disturbances in 1970 and 1971 led to another slump in business.Since 1972, however, loan approvals have continually reached new yearly highs,reflecting the political stability within Jordan and the consequent improvedinvestment climate.

4.02 Loans. Annex 14 classifies approved loans according to severalcriteria. Of the 285 loans approved through the end of 1975, 45 were fortourism projects (with only a few exceptions, hotels). The amount approvedfor these projects represents about 15% of total approvals. The largestsingle industrial category, food, beverage and tobacco, had received a totalof 23% of IDB's loan financing, with the chemical, rubber and plastic pro-ducts category following with 19%. The remaining loan approvals are spreadover a number of other categories, indicating that IDB has not unduly concen-trated its efforts on any one industrial branch but has tried to reach allmedium scale industrial activities being pursued in Jordan.

4.03 Over half of the number of loans approved (though accounting foronly about 10% of the amount approved) have been for amounts of less thanJD 20,000 (about $61,000 equivalent). This is a reflection of the small sizeof the enterprises IDB caters to. The average size of IDB's loans, whilesteadily increasing each year, is still quite small; during 1975 it was JD59,400 (about $180,000 equivalent) while the average size of all loans ap-proved since 1965 was JD 36,200 (about $110,000 equivalent). This again re-flects the size of the enterprises in the medium scale industrial sector.Not reflected in these figures is IDB's SSI&HP.

4.04 In recent years most of IDB's loans have had a repayment period ofbetween five and seven years plus a grace period of about a year and a half.Most of the projects IDB has supported have been expansion projects, thoughnew enterprises have been lent more money. IDB began granting loans for rawmaterials (working capital loans) following the 1967 war in an effort to as-sist firms to recover from the effects of the war; it ceased making such

- 17 -

loans in 1973. During the last three years over half of IDB's loans weremade to new clients, some 30% to repeat clients, with the remainder to enter-prises where some of the partners were new clients and others, repeat clients.The enterprises assisted by IDB have been heavily concentrated in the Amman-Zerka region, reflecting the general pattern in Jordan.

4.05 Equity Investments. Since its establishment IDB has approvedequity investments in six companies. One investment, JD 150,000 in theJordan Ceramics Industries Company approved in 1973, was a standby commitmentto cover cost overruns. It was not needed and was cancelled during 1975. Anadditional JD 150,000 investment in this company for an expansion project wasapproved late in 1975. An investment of JD 10,000 in the Jordan Paper Com-pany was written off; subsequently the company was reorganized as the JordanPaper and Cardboard Factory Company and IDB has invested in its capital. Dur-ing 1974 IDB received dividends totalling JD 16,700 from three companies, re-presenting a return of almost 14% on its equity investment portfolio.

4.06 Managed Funds. IDB manages on behalf of the National PlanningCouncil a portfolio of small loans made before IDB was established from theproceeds of a Kuwait loan to the Government. IDB's activities are limited tocollecting amounts that are due, receiving for its efforts 1/4 of 1% of whatit collects.

The Small Scale Industry and Handicraft Program

4.07 The Three-Year Plan called for the establishment of a special fundto assist the very small entrepreneur. This fund never materialized and inits absence IDB established in March 1975 an experimental program to begin totry to provide financial and other assistance to entrepreneurs in the smallscale industry and handicraft field. IDB defines these as enterprises thatemploy up to five people and that use manual production methods or simple ma-chines; small service establishments and traditional handicrafts are also in-cluded. No studies have been made of this subsector in the past. The re-sults of the 1975 industrial census will assist IDB and others in learningmore about these entrepreneurs (see paragraph 2.12). Until IDB's entry intothis field there was no institutional support for this subsector. Commercialbanks by and large have not lent to these entrepreneurs.

4.08 The establishment of this program was announced in local newspaperadvertisements and over the radio. Letters describing the program were sentto all municipalities, Chambers of Commerce and Industry, trade schools andother interested parties. Staff members from IDB visited different parts ofthe country to discuss the program. As a result of this publicity 129 loanapplications were received by the end of 1975. A number of these had to berejected as falling outside the scope of the program. Of the remainder, 52loans were approved totalling JD 72,200. Nine were later cancelled, leaving anet total of 43 loans amounting to JD 57,700 or an average of JD 1,340 (about$4,100 equivalent) per loan. IDB estimates that these 43 projects will pro-vide 71 new job opportunities at an average cost of about $2,800 equivalentper job.

- 18 -

4.09 All of these loans were for existing projects. Over half arelocated in the Amman-Zerka area with the remainder scattered among othertowns. Almost half have been for carpentry shops with garments being thenext largest category. Other endeavors assisted include stone cutting, tilemanufacturing, cement blocks and printing. IDB estimates that only six ofthe 43 enterprises will have assets exceeding JD 5,000 after the execution oftheir projects; none exceeded this level before IDB became involved (the aver-age size was JD 1,550 or $4,700 equivalent).

4.10 IDB has established some general criteria for this program, thoughat this initial stage flexibility is being stressed. The maximum size ofloans granted under this program is JD 2,000. There is no minimum size; thesmallest loan granted so far was for JD 360. The interest rate charged onthese loans is 7% p.a. The term of the loans can be up to ten years; theaverage term is four to five. The proceeds of the loan can be used only tofinance machinery and tools. In general, IDB will lend up to 80% of the costof such machinery and tools, but no more than 75% of the total cost of theproject. However, in some cases it has financed the total cost of expansionprojects. As security IDB will take a mortgage on real estate if any isavailable; otherwise it will mortgage the machinery and accept personalguarantees.

4.11 The 7% interest rate is seen by both the Government and IDB as anecessary encouragement for these entrepreneurs to approach IDB for funds toimprove their operations. It is not possible to assess the suitability ofthis relatively low rate before more is known about the cost of operatingthis program, the risks involved and the appropriate form and level of sub-sidy. These entrepreneurs, because they generally have assets of less thanJD 5,000, do not qualify for the incentives under the Encouragement of In-vestment Law, and IDB and the Government point out that the lower interestrate can therefore be seen as a form of compensation for this exclusion. Itis not clear why that Law establishes a minimum asset size for qualification.It is also unknown whether the incentives available under the Law for largerenterprises would be of significant benefit to these entrepreneurs or whetherother incentives should be made available. Answers to these questions mayemerge as IDB gains more experience with this subsector.

4.12 IDB is experimenting with a very simplified appraisal procedure forthese loans. Basically it seeks to establish what assets the enterprise cur-rently has and what additional machinery is needed. As few of these clientskeep records, financial statements are usually not available. IDB attemptsto make simple financial projections on the basis of discussions with theclient.

4.13 IDB is trying to determine what technical assistance these clientsneed and how IDB can best provide it. IDB does help these entrepreneurs toselect appropriate machinery and to ensure that the price is competitive. Ittries to visit each of them to see if there are difficulties in obtaininglabor or raw materials. It has determined that financing raw materials isoften a problem for these clients. While suppliers' credit is sometimes

- 19 -

available, the only other sources of credit are family or friends or throughadvance payments from customers. Commercial bank financing is rarely avail-able as the clients are unknown and the amounts involved small. IDB has sofar not provided raw material financing but has the matter under review.

4.14 IDB has established a separate division to handle this program. Atthe end of 1975 only one staff member was involved full time but IDB intendsto recruit an engineer/technician to assist him. IDB is keeping the fundingof this program separate from its regular activities. KfW has agreed thatthe interest differential fund established with its first loan will be usedto help finance the program. Similarly, the Kuwait Fund has agreed that theinterest differential fund to be established with its second loan will alsobe used for this purpose. The amounts to become available from these twosources are expected to be relatively small (about $100,000 equivalent peryear over the next few years). In addition, the Government has made onesmall grant for the program and has indicated its intention to provide addi-tional yearly grants of JD 100,000 ($303,000 equivalent). The Central Bankrecently announced its intention also to provide yearly grants of JD 100,000.Finally, if the above funds are inadequate, TDB can borrow funds from theCentral Bank at a preferential rate of 4% against the promissory notes of itssmall scale clients. These funds are currently included in IDB's own balancesheet (grants as liabilities, offset by the small scale industry loans as as-sets). However, they will be accounted for independently of IDB's balancesheet as a managed fund in the future.

4.15 It is IDB's intention that the cost of operating this programshould also be covered from these same sources, as it will not be self-sup-porting. However, it has not yet determined what this cost is and has there-fore not separated it from its regular operating budget. It will do so as itgains more experience with the program.

4.16 While all principal repayments and interest payments have so farbeen made on time, it should be recognized that the risk of unrecoverableloans is probably higher under this program than with IDB's normal lending asappraisals cannot be done with the same thoroughness and supervision of indi-vidual loans cannot be as intensive as for larger loans. Because the fundingfor this program is presently on a grant basis, though, each loan is effec-tively fully reserved against and any bad debts will not affect IDB's credit-worthiness. This is an appropriate approach until more experience has beengained with the debt service performance of these small scale entrepreneursand, on this basis, adequate levels for bad debt provisions can be estimated. 1/

4.17 IDB has not yet decided on the best way to institutionalize thiseffort. It may prove to be more appropriate to establish this progran as anaffiliate or a subsidiary of IDB instead of as an internal division. Pos-sibly a separate institution altogether may be preferable. TDB has still todetermine what role, if any, cooperative societies have to play in this ef-fort, or whether special industrial estates would be useful.

1/ Grant funds are also needed to cover the operating costs not coveredby interest incone.

- 20 -

4.18 IDB anticipates that it will need at least a year and a half totwo years of experience with this program before the needs, prospects andconstraints are clear. By the end of 1976 it expects to have made some 200loans and to be in a better position to see how best to proceed. In themeantime there is ample support for this pioneering effort within Governmentand elsewhere as it is recognized that it is needed to raise the skills, pro-ductivity and income levels of this group of entrepreneurs.

4.19 The Bank Group can become associated with IDB's initiative by pro-viding some of the resources to be lent to small scale entrepreneurs; thiswould ensure that the Bank Group becomes intimately involved with the programand gains, with IDB, the maximum possible knowledge of this subsector. Thisshould provide a basis for future Bank Group assistance to this subsector,both in Jordan and elsewhere.

4.20 It is proposed that $300,000 of the proposed credit be earmarkedfor this program, to be committed over the two-year period July 1976 to June1978. This amount represents one-half of the amount to be made available bythe Government during this period and should be sufficient to provide theBank Group with an opportunity to influence the direction of the program. Itrepresents, however, only about 20% of the total amount to be made availableto the program from all sources. These funds would be made available by theGovernment to the program as a grant in recognition of the higher cost andrisk associated with these loans than with IDB's normal lending activity (seeparagraph 4.16). Once experience has been gained with the debt service per-formance of these clients, consideration can be given to different methods offunding the program.

4.21 In view of the large number of small loans that will be made fromthis portion of the proposed credit, prior approval of each loan would be im-practical. Instead the program as a whole will be closely monitored. Dis-bursements will be made periodically on a reimbursement basis and will cover20% of IDB's total disbursements, in line with the proportion of funds beingprovided by IDA. The IDA funds will be available only to cover part of thecost of machinery and tools, not to cover part of the administrative cost ofthe program which can be covered by the other available funds. Disbursementswill be made against a certificate of expenditure provided by IDB. Support-ing documentation such as purchase invoices will not be submitted for reviewby the Association, but will be retained by IDB and be available for inspec-tion by the Association during the course of supervision missions.

4.22 So far most of the machinery and tools for this program have beenimported by local agents specifically for the projects involved against im-port licences obtained by the entrepreneurs. As the program expands, however,these agents are likely to begin to stock the more standard items in anticipa-tion of demand. The foreign exchange component will, in any event, remainhigh, certainly well above the 20% to be financed from the proposed credit.

4.23 To place the Bank Group in a position to study the program and atthe same time to help and advise IDB as appropriate, Bank Group supervisionof this program will be especially intensive. This will take the form of

- 21 -

more extensive reporting than normal as well as frequent visits to Jordan.A sample of appraisal reports (every tenth one) will be translated and for-warded to Washington. Quarterly summary reports covering such areas as ap-plications received, approved and rejected, amounts disbursed, repayment ex-perience, problems detected, technical assistance provided, operating costs,etc. will be prepared and sent to Washington.

4.24 The Government, IDB and the Chambers of Commerce have expressed aninterest in having an interdisciplinary study of these entrepreneurs carriedout to cover such topics as their existing markets and how market outletsmight be improved, their impact on urban development, their need for servicessuch as water and power, and appropriate tax and other incentives. Such astudy would provide direction as to how IDB's program should evolve over theyears to best meet the needs of this subsector.

4.25 IDB and the Faculty of Economics and Commerce at the University ofJordan have prepared a proposal for this study. It will be based on a struc-tured questionnaire and interviews with a random sample drawn from the almost7,000 small scale enterprises. Students at the Faculty will carry out thefield investigation under the supervision of faculty members and IDB. Thesample will be selected with the assistance of the Government's Department ofStatistics which carried cut the 1975 industrial census. The approach beingtaken is pragmatic and the results will be operationally oriented. As thisstudy will also be of benefit to the Bank Group by increasing the availableknowledge of this subsector, it is proposed that up to $25,000 of the pro-posed credit be earmarked to cover the cost of this study, both the local cur-rency and foreign exchange component. IDB's and the University's preliminaryestimate is that this study should cost about $20,000.

Economic Impact

4.26 The Government estimates that some JD 45 million was invested inthe manufacturing and mining sectors during the Three-Year Plan period, sub-stantially exceeding the JD 26 million called for in the Plan. Part of thisexcess, of course, reflects the sharp increase in the price of imported cap-ital goods. More striking was the investment by the private sector in mediumand small industrial enterprises, estimated at about JD 31 million or two-thirds of the total. This was well above the Plan target of JD 14 million.

4.27 IDB's role in achieving this higher than expected industrial invest-ment was large. It is estimated that during the three years of the Plan IDBassisted projects accounting for some 75% of private investment in mediumscale industry. Though its tourism activities are quite small compared toits industrial investment, IDB still plays an important role in this sector.It is estimated that IDB was associated with perhaps 90% of the investment inhotels and related tourism oriented enterprises during the Plan period. Asdiscussed in paragraph 2.33 IDB provided on average about 30% of the fundsrequired by the projects it assisted in the industrial and tourism sectors.

- 22 -

4.28 About a third of the industrial enterprises IDB assisted duringthe Plan period intend to export at least a part of their production. As al-ready noted, medium scale industry in Jordan is able to compete in neighbor-ing countries to a surprising degree. While IDB has not yet begun to calcu-late the IERR of its projects, it has calculated the IFRR on some. Theserates of return have in general been more than satisfactory (see paragraph2.11). As noted in paragraph 3.23, these calculations can be considered areasonable approximation for the IERR. On this basis IDB's projects generallyappear well justified.

4.29 Employment created by projects assisted by IDB was fairly substan-tial in relation to the size of employment in the industrial sector (seeAnnex 3). As an example, in 1974 the 28 industrial projects IDB assisted ac-counted for the creation of 691 new jobs and the nine tourism projects forthe creation of 194. The average cost per job created was JD 8,800 ($26,700equivalent) for new projects and JD 7,300 ($22,100 equivalent) for expansionprojects, which is not excessive given the relative sophistication of theJordanian industrial sector.

4.30 The economic impact of IDB's SSI&HP is difficult to measure at thisearly stage. One can anticipate, however, that it will be of significance inreducing the level of underemployment in urban and other areas and in raisingthe productivity and hence the earning oportunities of this group of entrepre-neurs. This experimental program, designed specifically to reach the longneglected informal sector and to reduce economic dualism, is also expected togenerate intangible benefits in that experience gained from it can be drawnupon for a possible expansion of the program in Jordan as well as for similarefforts in other countries.

V. IDB's FINANCIAL SITUATION

Resource Position