JMC PROJECTS (INDIA) LIMITED - Cloud Object Storages3.amazonaws.com/zanran_storage/ · JMC PROJECTS...

430

Letter of Offer for Equity Shareholders of the Company only JMC PROJECTS (INDIA) LIMITED (The Company was originally incorporated as Civen Construction Private Limited on June 5, 1986 under the Companies Act, 1956 with its registered office at Ahmedabad. Subsequently on December 10, 1987, the name was changed to Joshi & Modi Constructions Private Limited. The name was further changed to JMC Projects (India) Private Limited on January 21, 1994 and was subsequently converted into a Public Limited Company in the name of JMC Projects (India) Limited on February 4, 1994) Registered & Corporate Office: A-104, Shapath-4, Opposite Karnavati Club, S.G.Road, Ahmedabad – 380 051, India. Tel: +91-79-3001 1500; Fax: +91-79-3001 1600/1700 Company Secretary & Compliance Officer: Mr. Ashish Shah; E-mail: [email protected]; Website: www.jmcprojects.com (The Registered Office of the Company was shifted from People’s Plaza Near Memnagar Fire Station, Navrangpura, Ahmedabad- 380 009 to 4, Kuldip Society, Near Ishvar Bhuvan, Navrangpura, Ahmedabad – 380 009 w.e.f. May 9, 1988 and subsequently to Level-11, JMC House, Ambawadi, Ahmedabad - 380 006 w.e.f. April 5, 2002 and to the present registered office w.e.f. November 7, 2005) LETTER OF OFFER ISSUE OF 36,28,058 EQUITY SHARES OF Rs. 10/- EACH AT A PREMIUM OF Rs. 100/- PER EQUITY SHARE AGGREGATING TO Rs. 3,990.86 LAKHS TO THE EQUITY SHAREHOLDERS ON RIGHTS BASIS IN THE RATIO OF 1 (ONE) EQUITY SHARE FOR EVERY 5 (FIVE) EQUITY SHARES HELD ON THE BOOK CLOSURE DATE i.e. JULY 31, 2009 (“ISSUE”). THE ISSUE PRICE IS 11 TIMES THE FACE VALUE OF THE EQUITY SHARE. GENERAL RISKS Investment in equity and equity related securities involve a degree of risk and investors should not invest any funds in this Issue unless they can afford to take the risk of losing their investment. Investors are advised to read the Risk Factors carefully before taking an investment decision in this Issue. For taking an investment decision, investors must rely on their own examination of the Issuer and the Issue including the risks involved. The securities have not been recommended or approved by Securities and Exchange Board of India (“SEBI”) nor does SEBI guarantee the accuracy or adequacy of this document. Investors are advised to refer to “Risk Factors” on page viii of this Letter of Offer before making an investment in this Issue. ISSUER’S ABSOLUTE RESPONSIBILITY The Issuer, having made all reasonable inquiries, accepts responsibility for, and confirms that this Letter of Offer contains all information with regard to the Issuer and the Issue, which is material in the context of this Issue, that the information contained in this Letter of Offer is true and correct in all material respects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this document as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. LISTING The existing Equity Shares of the Company are listed on the Bombay Stock Exchange Limited (“BSE”) and the National Stock Exchange of India Limited (“NSE”). The Company has made an application for in-principle approval for listing to BSE and NSE. The Company has received the “in-principle” approval from BSE and NSE for listing the Equity Shares arising from this Issue vide letters dated April 28, 2009 and May 06, 2009 respectively. For the purposes of the Issue, the Designated Stock Exchange will be BSE. LEAD MANAGER TO THE ISSUE REGISTRAR TO THE ISSUE Collins Stewart Inga Private Limited A-404, Neelam Centre, Hind Cycle Road, Worli, Mumbai – 400 030. Tel: +91-22-2498 2937/19/54 Fax :+91-22-2498 2956 Email: [email protected] Contact Person: Mr. Ashwani Tandon / Ms. Deepa Mutha Website: www.csinga.com SEBI Registration No.: INM000010924 Link Intime India Private Limited (formerly known as Intime Spectrum Registry Limited) C-13, Pannalal Silk Mills Compound,LBS Road, Bhandup West, Mumbai – 400 078. Tel: +91-22- 2596 0320 Fax: +91-22-2596 0329 E-mail: [email protected] Contact Person: Mr. Praveen Kasare Website: www.linkintime.co.in SEBI Registration No.: INR000004058 ISSUE PROGRAMME ISSUE OPENS ON LAST DATE FOR RECEIVING REQUESTS FOR SPLIT FORMS ISSUE CLOSES ON Monday, September 07, 2009 Tuesday, September 15, 2009 Wednesday, September 23, 2009

Transcript of JMC PROJECTS (INDIA) LIMITED - Cloud Object Storages3.amazonaws.com/zanran_storage/ · JMC PROJECTS...

Letter of Offer for Equity Shareholders of the Company only

JMC PROJECTS (INDIA) LIMITED(The Company was originally incorporated as Civen Construction Private Limited on June 5, 1986 under the Companies Act, 1956 with its registered office at Ahmedabad. Subsequently on December 10, 1987, the name was changed to Joshi & Modi Constructions Private Limited. The name was further changed to JMC Projects (India) Private Limited on January 21, 1994 and was subsequently converted into a Public Limited Company in the name of JMC Projects (India) Limited on February 4, 1994)

Registered & Corporate Office: A-104, Shapath-4, Opposite Karnavati Club, S.G.Road, Ahmedabad – 380 051, India.

Tel: +91-79-3001 1500; Fax: +91-79-3001 1600/1700 Company Secretary & Compliance Officer: Mr. Ashish Shah; E-mail: [email protected]; Website: www.jmcprojects.com

(The Registered Office of the Company was shifted from People’s Plaza Near Memnagar Fire Station, Navrangpura, Ahmedabad- 380 009 to 4, Kuldip Society, Near Ishvar Bhuvan, Navrangpura, Ahmedabad – 380 009 w.e.f. May 9, 1988 and subsequently to Level-11, JMC House, Ambawadi, Ahmedabad - 380 006 w.e.f. April 5, 2002 and to the present registered office w.e.f. November 7, 2005)

LETTER OF OFFERISSUE OF 36,28,058 EQUITY SHARES OF Rs. 10/- EACH AT A PREMIUM OF Rs. 100/- PER EQUITY SHARE AGGREGATING TO Rs. 3,990.86 LAKHS TO THE EQUITY SHAREHOLDERS ON RIGHTS BASIS IN THE RATIO OF 1 (ONE) EQUITY SHARE FOR EVERY 5 (FIVE) EQUITY SHARES HELD ON THE BOOK CLOSURE DATE i.e. JULY 31, 2009 (“ISSUE”). THE ISSUE PRICE IS 11 TIMES THE FACE VALUE OF THE EQUITY SHARE.

GENERAL RISKSInvestment in equity and equity related securities involve a degree of risk and investors should not invest any funds in this Issue unless they can afford to take the risk of losing their investment. Investors are advised to read the Risk Factors carefully before taking an investment decision in this Issue. For taking an investment decision, investors must rely on their own examination of the Issuer and the Issue including the risks involved. The securities have not been recommended or approved by Securities and Exchange Board of India (“SEBI”) nor does SEBI guarantee the accuracy or adequacy of this document. Investors are advised to refer to “Risk Factors” on page viii of this Letter of Offer before making an investment in this Issue.

ISSUER’S ABSOLUTE RESPONSIBILITYThe Issuer, having made all reasonable inquiries, accepts responsibility for, and confirms that this Letter of Offer contains all information with regard to the Issuer and the Issue, which is material in the context of this Issue, that the information contained in this Letter of Offer is true and correct in all material respects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this document as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect.

LISTINGThe existing Equity Shares of the Company are listed on the Bombay Stock Exchange Limited (“BSE”) and the National Stock Exchange of India Limited (“NSE”). The Company has made an application for in-principle approval for listing to BSE and NSE. The Company has received the “in-principle” approval from BSE and NSE for listing the Equity Shares arising from this Issue vide letters dated April 28, 2009 and May 06, 2009 respectively. For the purposes of the Issue, the Designated Stock Exchange will be BSE.

LEAD MANAGER TO THE ISSUE REGISTRAR TO THE ISSUE

Collins Stewart Inga Private LimitedA-404, Neelam Centre, Hind Cycle Road,Worli, Mumbai – 400 030.Tel: +91-22-2498 2937/19/54Fax :+91-22-2498 2956Email: [email protected] Person: Mr. Ashwani Tandon / Ms. Deepa Mutha Website: www.csinga.comSEBI Registration No.: INM000010924

Link Intime India Private Limited(formerly known as Intime Spectrum Registry Limited)C-13, Pannalal Silk Mills Compound,LBS Road,Bhandup West, Mumbai – 400 078.Tel: +91-22- 2596 0320Fax: +91-22-2596 0329E-mail: [email protected] Person: Mr. Praveen KasareWebsite: www.linkintime.co.inSEBI Registration No.: INR000004058

ISSUE PROGRAMME

ISSUE OPENS ON LAST DATE FOR RECEIVING REQUESTS FOR SPLIT FORMS

ISSUE CLOSES ON

Monday, September 07, 2009 Tuesday, September 15, 2009 Wednesday, September 23, 2009

TABLE OF CONTENTS

GLOSSARY OF TERMS AND ABBREVIATIONS iiPRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA viFORWARD LOOKING STATEMENTS viiRISK FACTORS viiiTHE ISSUE 1SUMMARY FINANCIAL INFORMATION 2GENERAL INFORMATION 9CAPITAL STRUCTURE 13OBJECTS OF THE ISSUE 31BASIS FOR ISSUE PRICE 38STATEMENT OF TAX BENEFITS 40INDUSTRY OVERVIEW 47BUSINESS OVERVIEW 58HISTORY AND CORPORATE STRUCTURE 60MANAGEMENT 68PROMOTERS 95FINANCIAL STATEMENTS 100MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

220

UNAUDITED WORKING RESULTS 230OUTSTANDING LITIGATIONS AND DEFAULTS 231GOVERNMENT APPROVALS 337STATUTORY AND OTHER INFORMATION 343TERMS OF THE ISSUE 356MAIN PROVISIONS OF ARTICLES OF ASSOCIATION 384MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION 405DECLARATION 407

ii

GLOSSARY OF TERMS AND ABBREVIATIONS Company 1JMC / Issuer JMC Projects (India) Limited Issue related Act The Companies Act, 1956 and amendments thereto Articles Articles of Association of the Company Banker to the Issue IDBI Bank Limited Board Board of Directors of JMC Projects (India) Limited Committee of Directors

Committee of the Board of Directors of JMC Projects (India) Limited authorized to take decisions on matters related to / incidental to this Issue

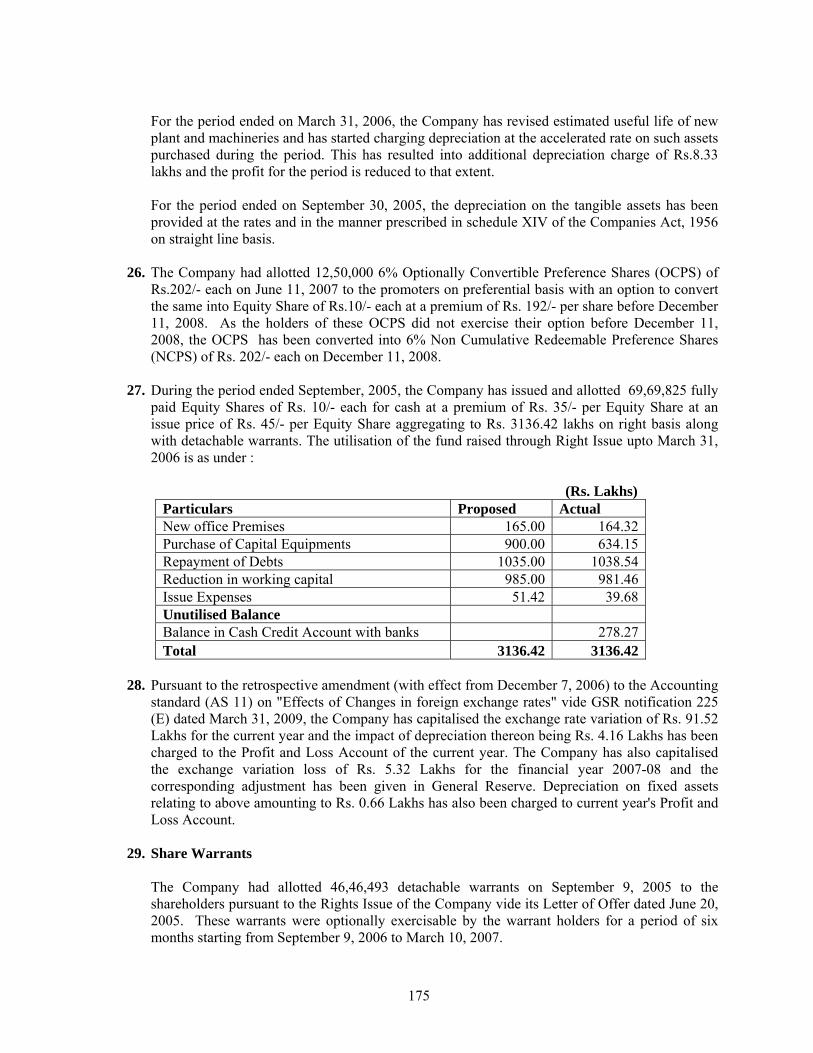

Depositories NSDL and CDSL Designated Stock Exchange Bombay Stock Exchange Limited (BSE) DP Depository Participant Director(s) Directors on the Board of the Company Equity Share(s) Equity Shares of the Company of Rs.10/- each Equity Shareholders

Equity shareholders whose names appear as beneficial owners as per the list furnished by the depositories in respect of the shares held in the electronic form and / or on the Register of Members of the Company in respect of the shares held in Physical Form on the Book Closure Date i.e. July 31, 2009 and to whom this Offer is being made.

Financial Year/Fiscal Year/FY

Any period of 12 months ended March 31 of that particular year, unlesss otherwise stated

Issue or Rights Issue or Offer

Issue by the Company of 36,28,058 Equity Shares of Rs. 10/- each for cash at Rs. 110/- per Equity Share (including a premium of Rs. 100/- per Equity Share) aggregating to Rs. 3,990.86 lakhs on Rights basis to the existing Equity Shareholders of the Company in the ratio of 1 (One) Equity Share for every 5 (Five) Equity Shares held on the Book Closure Date i.e. July 31, 2009.

Issue price Rs. 110/- per Equity Share Issue Opening Date Monday, September 07, 2009 Issue Closing Date Wednesday, September 23, 2009 Lead Manager to the Issue Collins Stewart Inga Private Limited Letter of Offer / LOO/ Offer Document

This Letter of Offer circulated to the Equity Shareholders of the Company

Memorandum Memorandum of Association of the Company Book Closure Date July 31, 2009 Registrar to the Issue Link Intime India Private Limited Rights Entitlement

The number of Equity Shares that an Equity Shareholder is entitled to under this Letter of Offer in proportion to his / her / its existing shareholding in the Company as on the Book Closure Date

Security certificates Equity Share certificates

iii

SPA Share Purchase Agreement dated October 14, 2004 executed between the ‘Purchaser’ being ‘Kalpataru Power Transmission Limited, Kalpataru Energy Venture (Private) Limited and the ‘Sellers’ being Late Mr. I. K. Modi, Mr. Hemant Modi, Mr. Suhas Joshi, Mrs. Sonal Modi, Mrs. Suverna Modi, Mrs. Madhuri Joshi, Late Mrs. Malti Joshi, Ms. Ami Modi, Ms. Anar Modi, Minar Investments and Finance Private Limited and the Company

Stock Exchanges BSE and NSE where the Equity Shares of the Company are presently listed Takeover Code Securities & Exchange Board of India (Substantial Acquisition of Shares and

Takeovers) Regulation, 1997 and amendments thereto Company/Industry related APDRP Accelerated Power Development and Reform Programme BOT Build Operate and Transfer BOOT Build Own Operate and Transfer BOLT Build Own Lease and Transfer CAR Contractors All Risk EPC Engineering, Procurement and Commissioning MORTH Ministry of Road Transport and Highways NH National Highway NHAI National Highway Authority of India NHDP National Highway Development Programme Abbreviations AGM Annual General Meeting

AS Accounting Standards issued by the Institute of Chartered Accountants of India

ASBA Applications Supported by Blocked Amount Asst. Assistant Anr. Another BSE Bombay Stock Exchange Limited BUTP Bombay Urban Transport Project CDSL Central Depository Services (India) Limited CAF Composite Application Form CEO Chief Executive Officer DD Demand Draft GM General Meeting EBIDTA Earnings before Interest, Depreciation, Tax and Appropriation EGM Extra-ordinary General Meeting EIO Eastern India Operation EPS Earnings Per Share

iv

EOU Export Oriented Unit FCNR Foreign Currency Non-Resident account FDI Foreign Direct Investment FEMA

Foreign Exchange Management Act, 1999 read with rules and regulations there under and amendments thereto

FIFO First In First Out FII(s) Foreign Institutional Investors registered with SEBI under applicable laws FIPB Foreign Investment Promotion Board FY

Financial year being a period commencing on April 1st and ending on March 31st of the following year

GDP Gross Domestic Product GIR Number General Index Registry Number GoI Government of India HUF Hindu Undivided Family IT/ITES Information Technology/Information Technology Enabled Services IT Act The Income Tax Act, 1961 and amendments thereto JV Joint Venture Kms Kilometers KPTL Kalpataru Power Transmission Limited KV Kilo Volt Kwh Kilowatt-hour LC Letter of Credit LIC Life Insurance Corporation of India Ltd. Limited MD Managing Director MoU Memorandum of Understanding MT Metric Ton MUTP Mumbai Urban Transport Project MW Mega Watt NA Not Applicable NAV Net Asset Value NCPS Non-Cumulative Redeemable Preference Shares NOC No Objection Certificate NR Non-resident NRI(s) Non-resident Indian(s) NRE Account Non Resident External account NRO Account Non Resident Ordinary account NSDL National Securities Depository Limited

v

NSE The National Stock Exchange of India Limited OCB(s) Overseas Corporate Body(ies) OCC Overdraft and cash credit OCPS Optionally Convertible Preference Shares Ors. Others PAC Persons Acting in Concert P/E or P/E ratio Price-Earnings Ratio p.a. Per annum PAN Permanent Account Number PAT Profit After Tax PBDIT Profit Before Depreciation Interest and Tax PBT Profit Before Tax PGCIL Power Grid Corporation of India Limited PSU Public Sector Undertaking PWD Public Works Department R&D Research & Development RONW Return on Networth SCSB Self Certified Syndicate Bank SEB State Electricity Board SEBI Securities and Exchange Board of India SEBI Guidelines/ SEBI (DIP)

SEBI (Disclosure & Investor Protection) Guidelines, 2000 as amended from time to time

SEBI (SAST) Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 1997 and subsequent amendments thereto

SIO Southern India Operations SPV Special Purpose Vehicle sq. ft. Square feet SSI Small Scale Industry TDS Tax Deducted at Source TPH Ton per hour UTI Unit Trust of India Vol Volume w.e.f. With effect from WIO Western India Operations WPI Wholesale Price Index

vi

PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA

In this Letter of Offer, unless the context otherwise requires, all references to one gender also refers to another gender and the word "Lakh" or "Lac" means "one hundred thousand" and the word "million" means "ten lac" and the word "Crore" means "ten million" and the word “One hundred crore” means “Billion”. In this Letter of Offer, any discrepancies in any table between total and the sum of the amounts listed are due to rounding-off. Unless stated otherwise, the financial information used in this Letter of Offer is derived from the Company’s consolidated and unconsolidated restated financial information as of March 31, 2009 (12 months), March 31, 2008 (12 months), March 31, 2007 (12 months), March 31, 2006 (6 months), September 30, 2005 (18 months) prepared in accordance with Indian GAAP, the Companies Act, 1956 and applicable SEBI DIP Guidelines. Throughout this Letter of Offer, all figures have been expressed in Lakhs unless otherwise stated. All references to “India” contained in this Letter of Offer are to the Republic of India. For additional definitions used in this Letter of Offer, see the section “Glossary of Terms and Abbreviations” on page ii of this Letter of Offer. Industry data used throughout this Letter of Offer has been obtained from industry publications and other authenticated published data. Industry publications generally state that the information contained in those publications has been obtained from sources believed to be reliable but that their accuracy and completeness are not guaranteed and their reliability cannot be assured. Although the Company believes that the industry data used in this Letter of Offer is reliable, it has not been independently verified. Similarly, internal Company reports, while believed by the Company to be reliable, have not been verified by any independent sources. CURRENCY OF PRESENTATION In this Letter of Offer, all references to “Rupees” and “Rs.” are to the legal currency of India.

vii

FORWARD LOOKING STATEMENTS This Letter of Offer contains certain “forward-looking statements”. These forward looking statements can generally be identified by words or phrases such as “aim”, “anticipate”, “believe”, “expect”, “estimate”, “intend”, “objective”, “plan”, “project”, “shall”, “will”, “will continue”, “will pursue” or other words or phrases of similar import. Similarly, statements that describe the objectives, plans or goals also are forward-looking statements. All forward looking statements are subject to risks, uncertainties and assumptions about the Company that could cause actual results to differ materially from those contemplated by the relevant forward looking statement. Important factors that could cause actual results to differ materially from the expectations include, among others:

• General economic and business conditions in India; • The ability to successfully implement the strategy, growth and expansion plans and technological

changes; • Changes in the value of Rupee and other currency changes; • Changes in the Indian and international interest rates; • Allocations of funds by the Government; • Changes in laws and regulations that apply to the customers of the Company; • Increasing competition in and the conditions of the customers of the Company and • Changes in political conditions in India.

For further discussion of factors that could cause actual results to differ, please see the section titled “Risk Factors” beginning on page no. viii of this Letter of Offer. By their nature, certain market risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated. Neither the Company, the Directors, any member of the Lead Manager team nor any of their respective affiliates have any obligation to update or otherwise revise any statements reflecting circumstances arising after the date hereof or to reflect the occurrence of underlying events, even if the underlying assumptions do not come to fruition. In accordance with SEBI requirements, the Company and the Lead Manager will ensure that investors in India are informed of material developments until such time as the grant of listing and trading permission by the Stock Exchanges.

viii

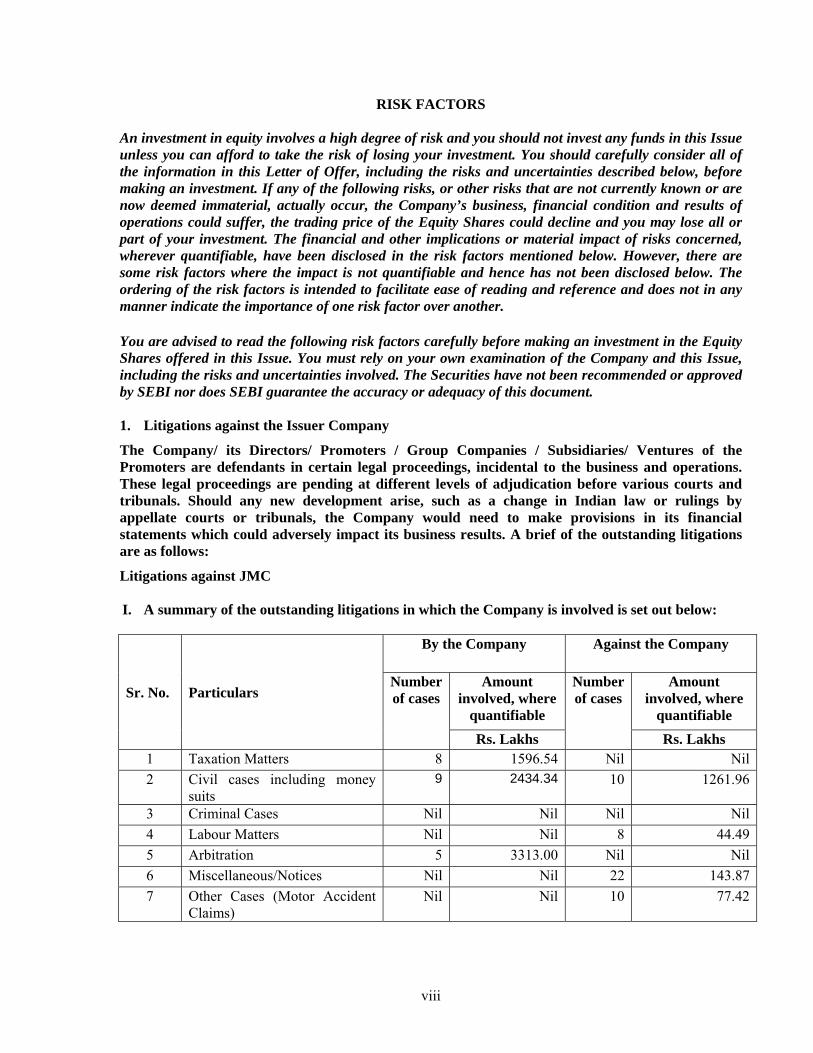

RISK FACTORS An investment in equity involves a high degree of risk and you should not invest any funds in this Issue unless you can afford to take the risk of losing your investment. You should carefully consider all of the information in this Letter of Offer, including the risks and uncertainties described below, before making an investment. If any of the following risks, or other risks that are not currently known or are now deemed immaterial, actually occur, the Company’s business, financial condition and results of operations could suffer, the trading price of the Equity Shares could decline and you may lose all or part of your investment. The financial and other implications or material impact of risks concerned, wherever quantifiable, have been disclosed in the risk factors mentioned below. However, there are some risk factors where the impact is not quantifiable and hence has not been disclosed below. The ordering of the risk factors is intended to facilitate ease of reading and reference and does not in any manner indicate the importance of one risk factor over another. You are advised to read the following risk factors carefully before making an investment in the Equity Shares offered in this Issue. You must rely on your own examination of the Company and this Issue, including the risks and uncertainties involved. The Securities have not been recommended or approved by SEBI nor does SEBI guarantee the accuracy or adequacy of this document. 1. Litigations against the Issuer Company

The Company/ its Directors/ Promoters / Group Companies / Subsidiaries/ Ventures of the Promoters are defendants in certain legal proceedings, incidental to the business and operations. These legal proceedings are pending at different levels of adjudication before various courts and tribunals. Should any new development arise, such as a change in Indian law or rulings by appellate courts or tribunals, the Company would need to make provisions in its financial statements which could adversely impact its business results. A brief of the outstanding litigations are as follows:

Litigations against JMC I. A summary of the outstanding litigations in which the Company is involved is set out below:

Sr. No. Particulars

By the Company Against the Company

Number of cases

Amount involved, where

quantifiable

Number of cases

Amount involved, where

quantifiable Rs. Lakhs Rs. Lakhs

1 Taxation Matters 8 1596.54 Nil Nil2 Civil cases including money

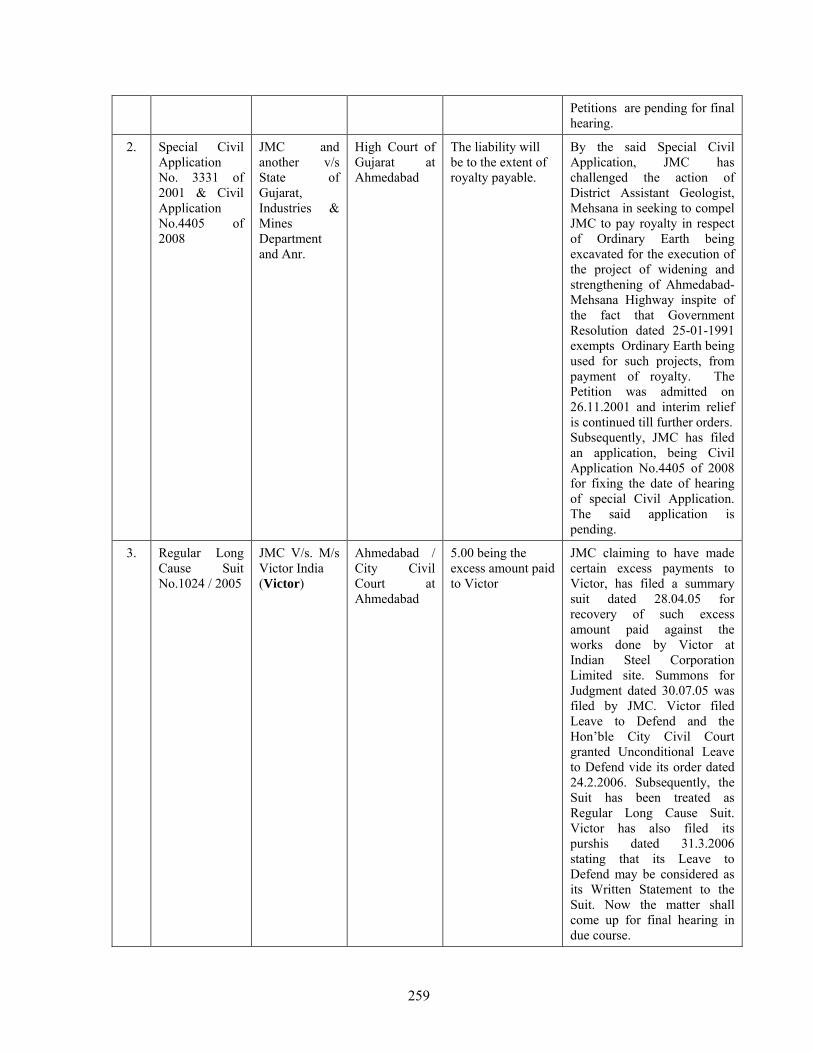

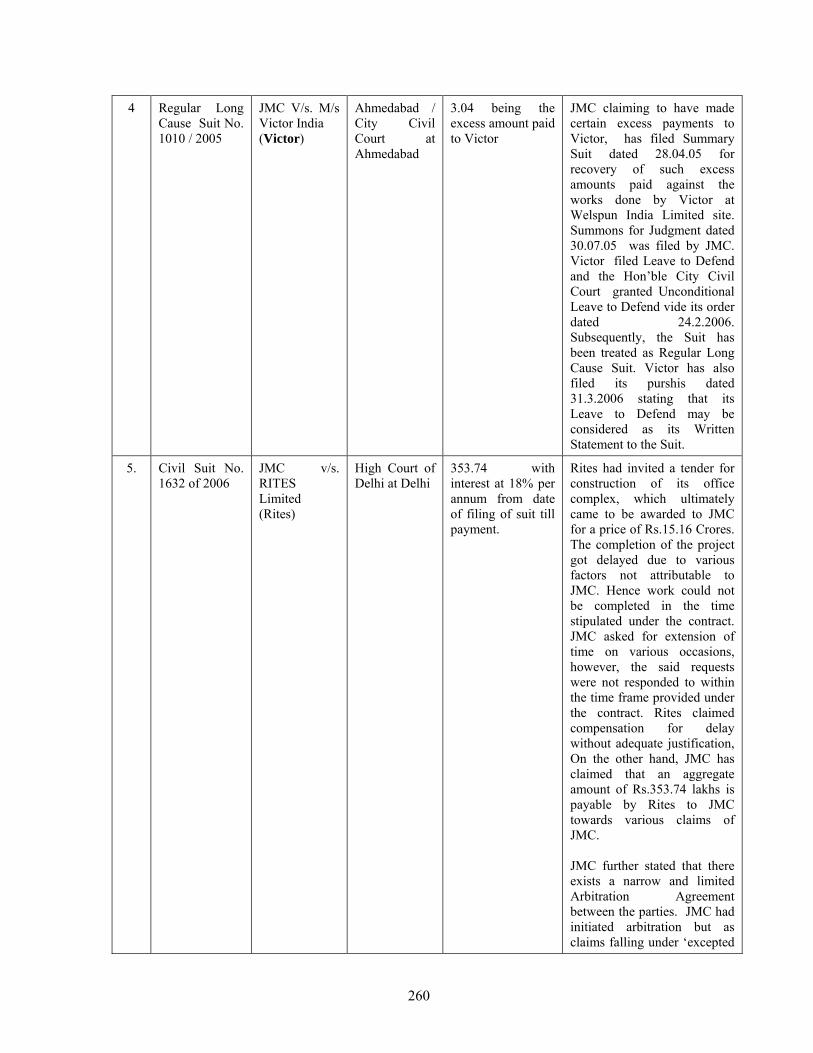

suits 9 2434.34 10 1261.96

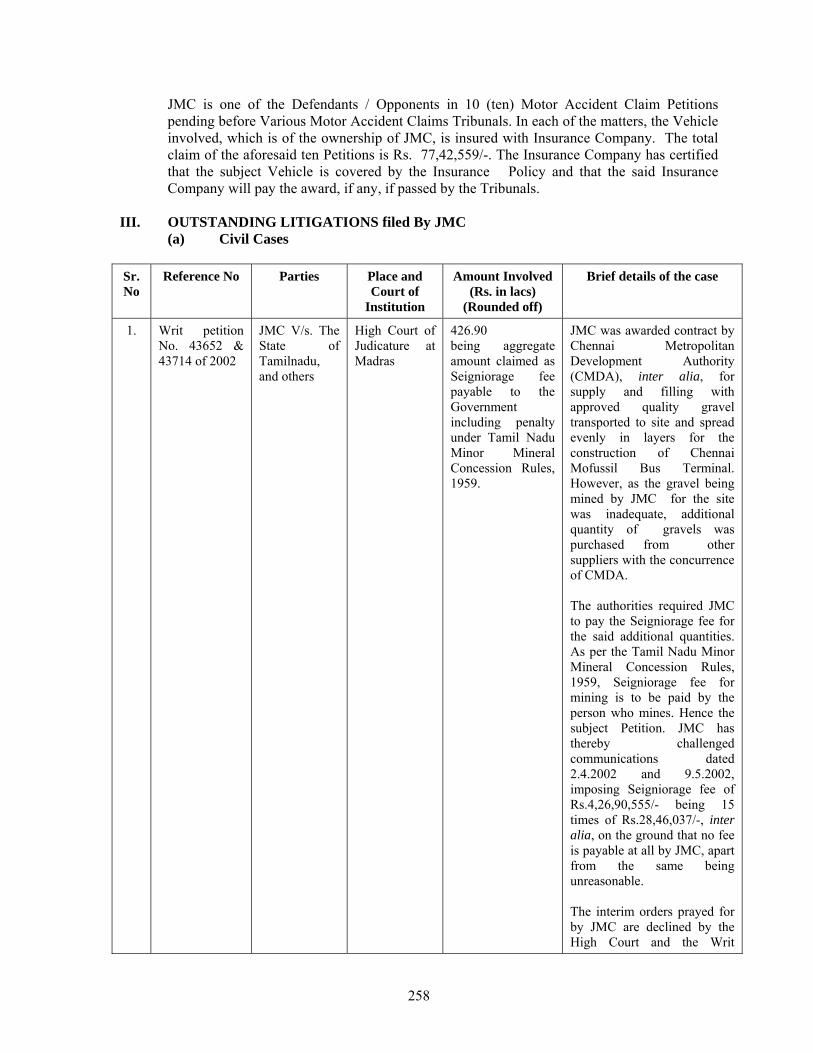

3 Criminal Cases Nil Nil Nil Nil4 Labour Matters Nil Nil 8 44.495 Arbitration 5 3313.00 Nil Nil6 Miscellaneous/Notices Nil Nil 22 143.877 Other Cases (Motor Accident

Claims) Nil Nil 10 77.42

ix

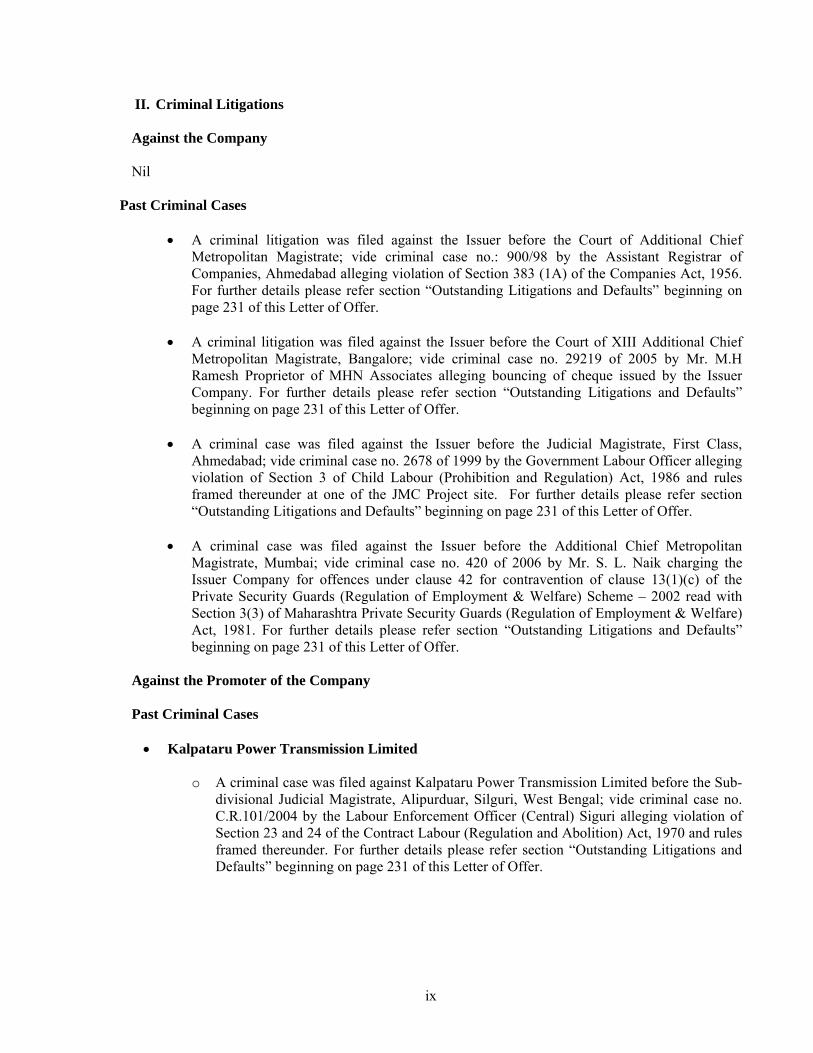

II. Criminal Litigations

Against the Company Nil

Past Criminal Cases

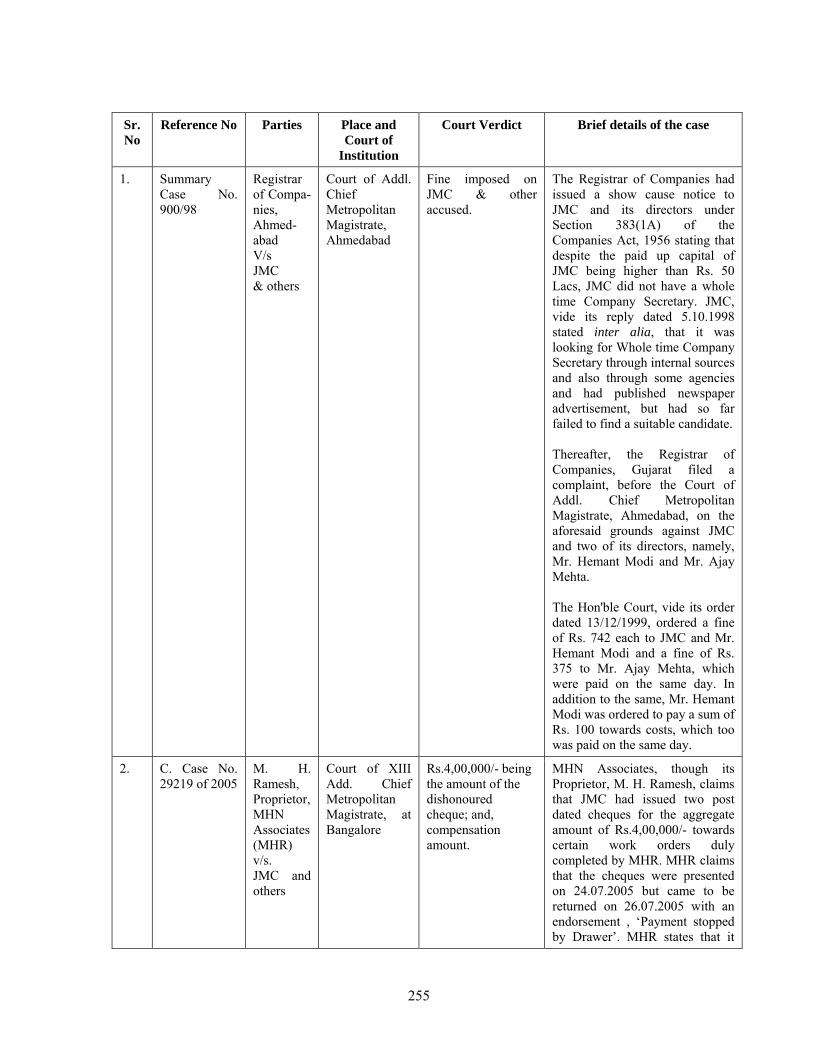

• A criminal litigation was filed against the Issuer before the Court of Additional Chief Metropolitan Magistrate; vide criminal case no.: 900/98 by the Assistant Registrar of Companies, Ahmedabad alleging violation of Section 383 (1A) of the Companies Act, 1956. For further details please refer section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer.

• A criminal litigation was filed against the Issuer before the Court of XIII Additional Chief

Metropolitan Magistrate, Bangalore; vide criminal case no. 29219 of 2005 by Mr. M.H Ramesh Proprietor of MHN Associates alleging bouncing of cheque issued by the Issuer Company. For further details please refer section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer.

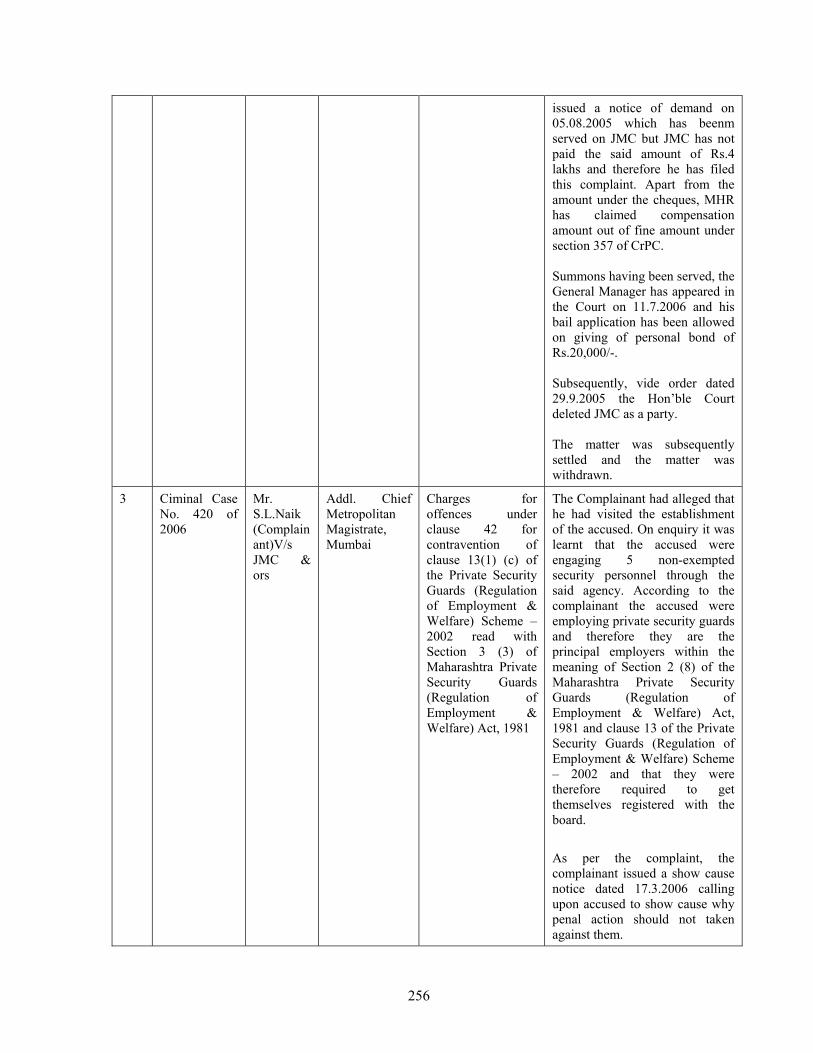

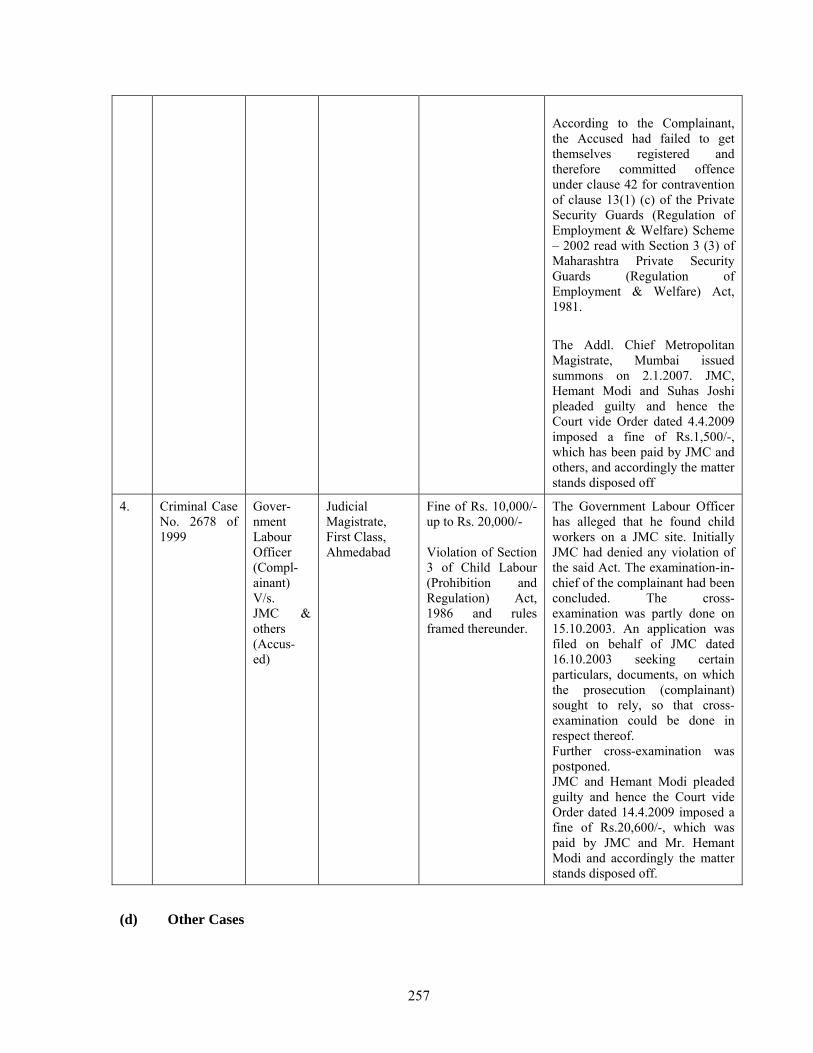

• A criminal case was filed against the Issuer before the Judicial Magistrate, First Class,

Ahmedabad; vide criminal case no. 2678 of 1999 by the Government Labour Officer alleging violation of Section 3 of Child Labour (Prohibition and Regulation) Act, 1986 and rules framed thereunder at one of the JMC Project site. For further details please refer section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer.

• A criminal case was filed against the Issuer before the Additional Chief Metropolitan

Magistrate, Mumbai; vide criminal case no. 420 of 2006 by Mr. S. L. Naik charging the Issuer Company for offences under clause 42 for contravention of clause 13(1)(c) of the Private Security Guards (Regulation of Employment & Welfare) Scheme – 2002 read with Section 3(3) of Maharashtra Private Security Guards (Regulation of Employment & Welfare) Act, 1981. For further details please refer section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer.

Against the Promoter of the Company

Past Criminal Cases

• Kalpataru Power Transmission Limited

o A criminal case was filed against Kalpataru Power Transmission Limited before the Sub-divisional Judicial Magistrate, Alipurduar, Silguri, West Bengal; vide criminal case no. C.R.101/2004 by the Labour Enforcement Officer (Central) Siguri alleging violation of Section 23 and 24 of the Contract Labour (Regulation and Abolition) Act, 1970 and rules framed thereunder. For further details please refer section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer.

x

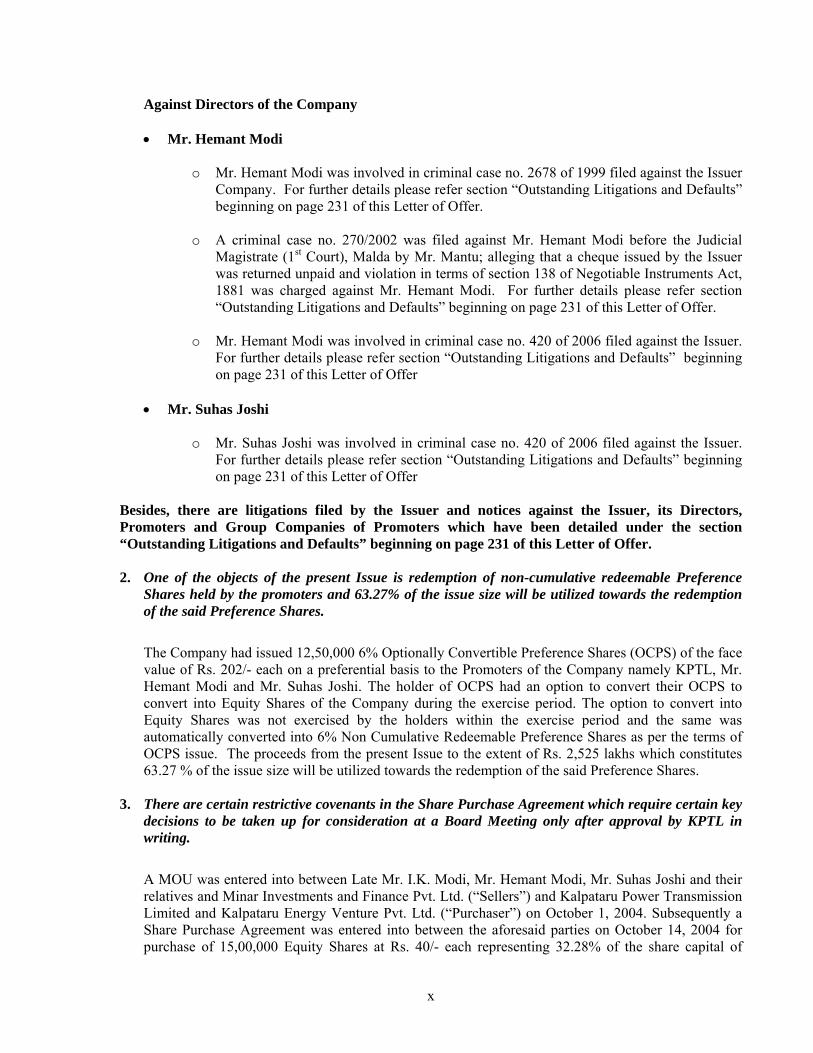

Against Directors of the Company

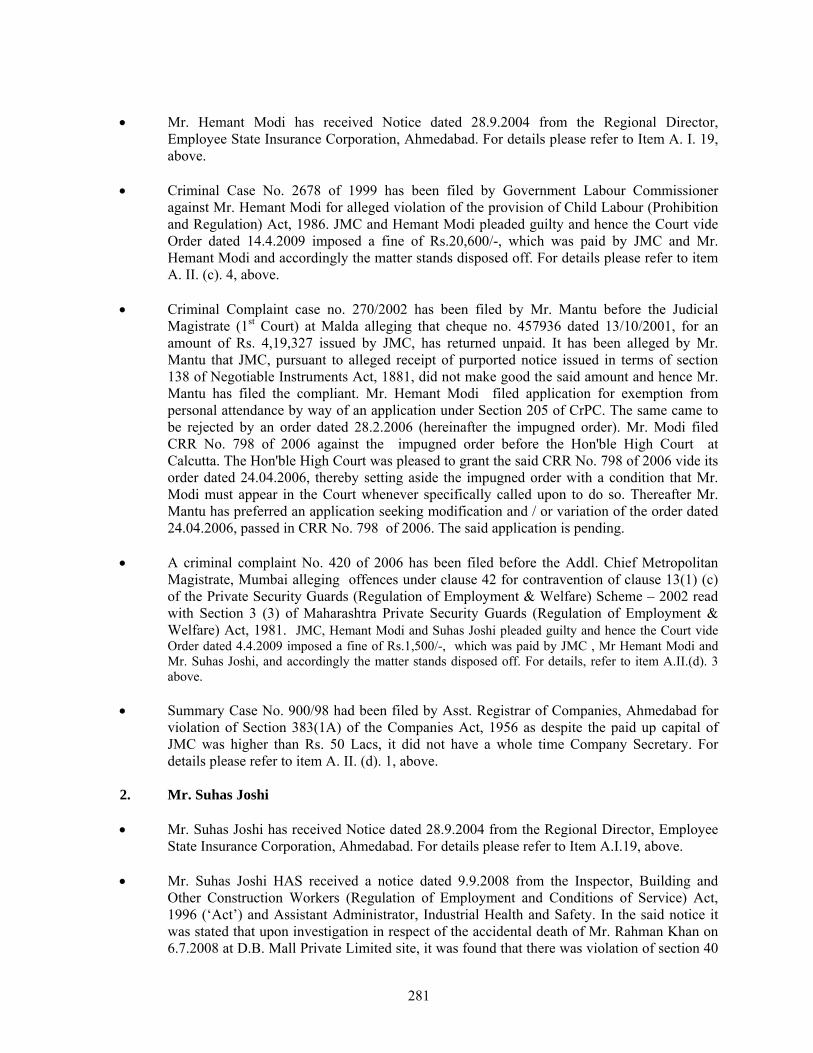

• Mr. Hemant Modi

o Mr. Hemant Modi was involved in criminal case no. 2678 of 1999 filed against the Issuer Company. For further details please refer section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer.

o A criminal case no. 270/2002 was filed against Mr. Hemant Modi before the Judicial

Magistrate (1st Court), Malda by Mr. Mantu; alleging that a cheque issued by the Issuer was returned unpaid and violation in terms of section 138 of Negotiable Instruments Act, 1881 was charged against Mr. Hemant Modi. For further details please refer section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer.

o Mr. Hemant Modi was involved in criminal case no. 420 of 2006 filed against the Issuer.

For further details please refer section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer

• Mr. Suhas Joshi

o Mr. Suhas Joshi was involved in criminal case no. 420 of 2006 filed against the Issuer. For further details please refer section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer

Besides, there are litigations filed by the Issuer and notices against the Issuer, its Directors, Promoters and Group Companies of Promoters which have been detailed under the section “Outstanding Litigations and Defaults” beginning on page 231 of this Letter of Offer. 2. One of the objects of the present Issue is redemption of non-cumulative redeemable Preference

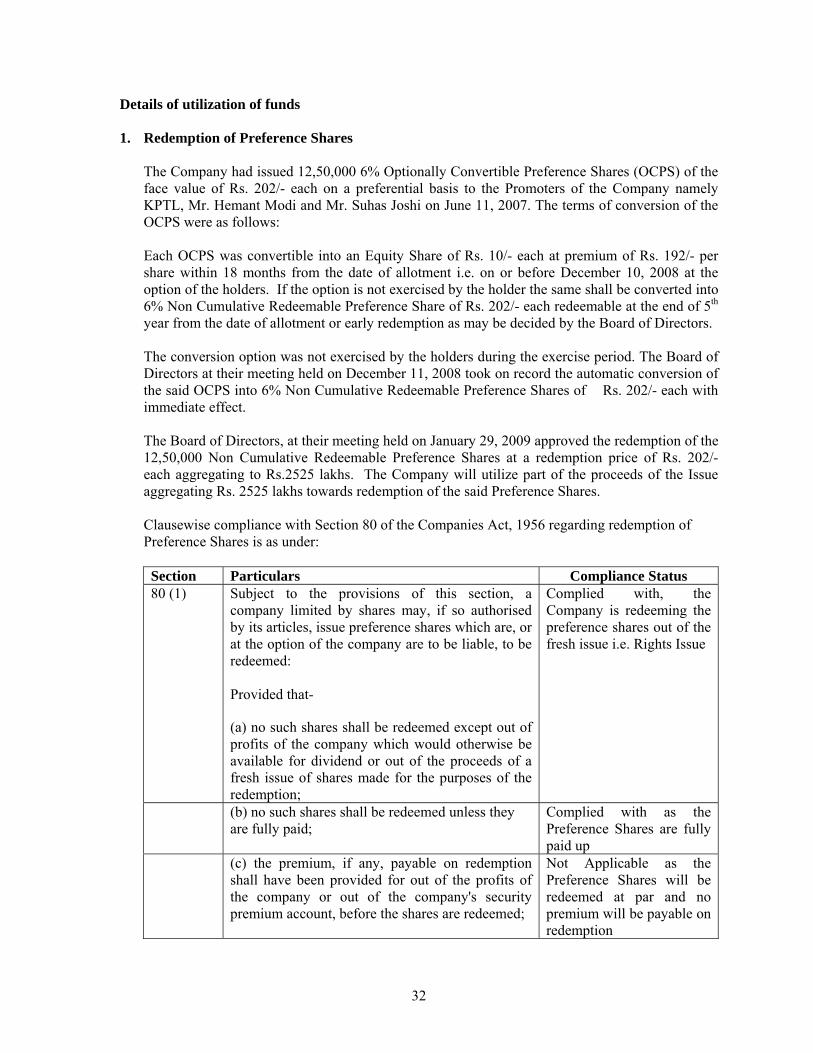

Shares held by the promoters and 63.27% of the issue size will be utilized towards the redemption of the said Preference Shares.

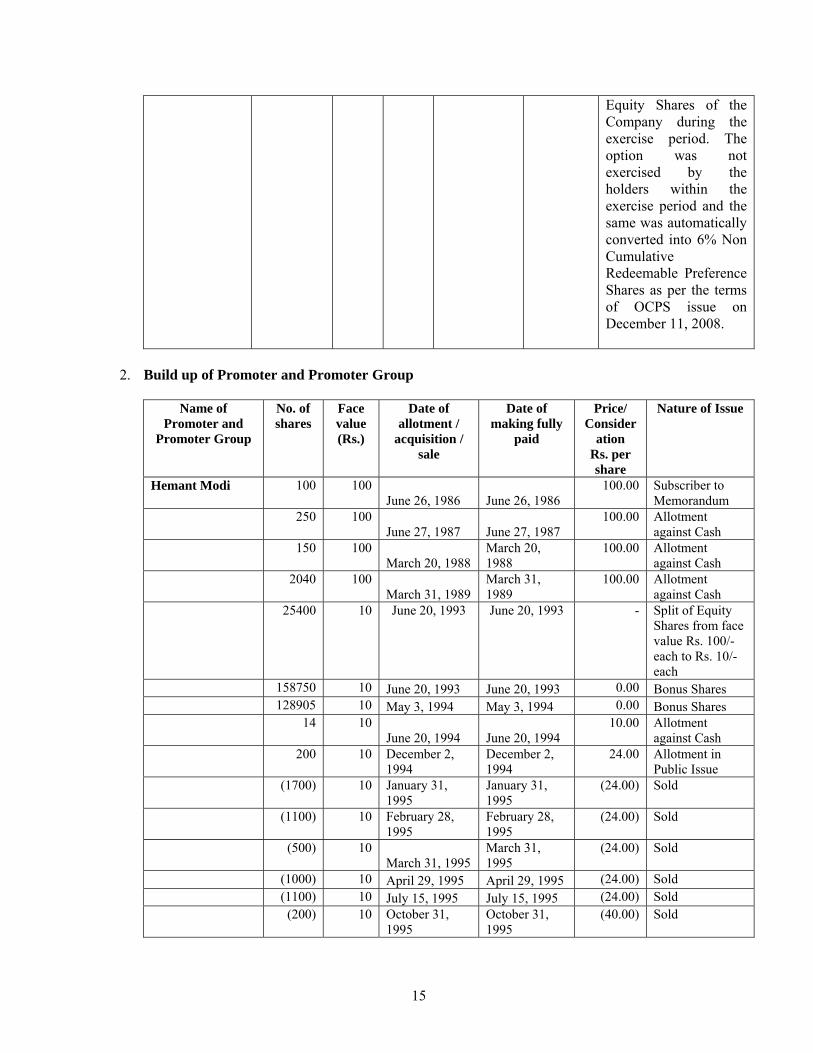

The Company had issued 12,50,000 6% Optionally Convertible Preference Shares (OCPS) of the face value of Rs. 202/- each on a preferential basis to the Promoters of the Company namely KPTL, Mr. Hemant Modi and Mr. Suhas Joshi. The holder of OCPS had an option to convert their OCPS to convert into Equity Shares of the Company during the exercise period. The option to convert into Equity Shares was not exercised by the holders within the exercise period and the same was automatically converted into 6% Non Cumulative Redeemable Preference Shares as per the terms of OCPS issue. The proceeds from the present Issue to the extent of Rs. 2,525 lakhs which constitutes 63.27 % of the issue size will be utilized towards the redemption of the said Preference Shares.

3. There are certain restrictive covenants in the Share Purchase Agreement which require certain key

decisions to be taken up for consideration at a Board Meeting only after approval by KPTL in writing.

A MOU was entered into between Late Mr. I.K. Modi, Mr. Hemant Modi, Mr. Suhas Joshi and their relatives and Minar Investments and Finance Pvt. Ltd. (“Sellers”) and Kalpataru Power Transmission Limited and Kalpataru Energy Venture Pvt. Ltd. (“Purchaser”) on October 1, 2004. Subsequently a Share Purchase Agreement was entered into between the aforesaid parties on October 14, 2004 for purchase of 15,00,000 Equity Shares at Rs. 40/- each representing 32.28% of the share capital of

xi

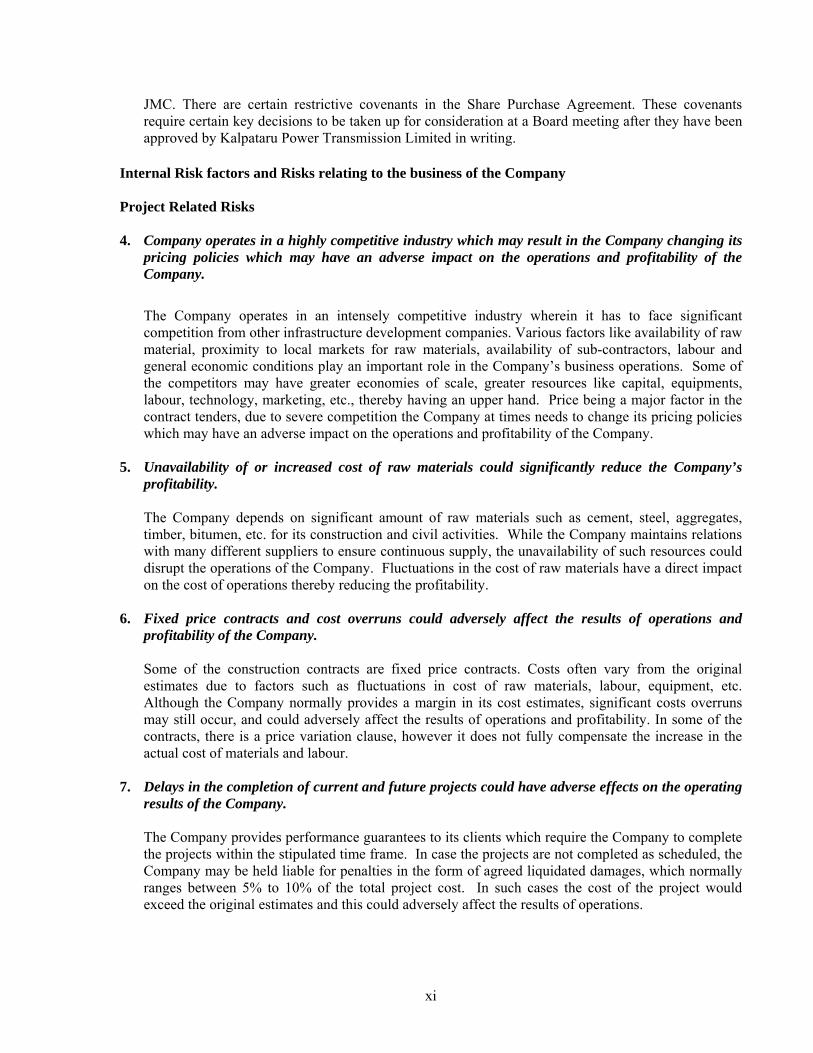

JMC. There are certain restrictive covenants in the Share Purchase Agreement. These covenants require certain key decisions to be taken up for consideration at a Board meeting after they have been approved by Kalpataru Power Transmission Limited in writing.

Internal Risk factors and Risks relating to the business of the Company Project Related Risks 4. Company operates in a highly competitive industry which may result in the Company changing its

pricing policies which may have an adverse impact on the operations and profitability of the Company.

The Company operates in an intensely competitive industry wherein it has to face significant competition from other infrastructure development companies. Various factors like availability of raw material, proximity to local markets for raw materials, availability of sub-contractors, labour and general economic conditions play an important role in the Company’s business operations. Some of the competitors may have greater economies of scale, greater resources like capital, equipments, labour, technology, marketing, etc., thereby having an upper hand. Price being a major factor in the contract tenders, due to severe competition the Company at times needs to change its pricing policies which may have an adverse impact on the operations and profitability of the Company.

5. Unavailability of or increased cost of raw materials could significantly reduce the Company’s profitability. The Company depends on significant amount of raw materials such as cement, steel, aggregates, timber, bitumen, etc. for its construction and civil activities. While the Company maintains relations with many different suppliers to ensure continuous supply, the unavailability of such resources could disrupt the operations of the Company. Fluctuations in the cost of raw materials have a direct impact on the cost of operations thereby reducing the profitability.

6. Fixed price contracts and cost overruns could adversely affect the results of operations and profitability of the Company. Some of the construction contracts are fixed price contracts. Costs often vary from the original estimates due to factors such as fluctuations in cost of raw materials, labour, equipment, etc. Although the Company normally provides a margin in its cost estimates, significant costs overruns may still occur, and could adversely affect the results of operations and profitability. In some of the contracts, there is a price variation clause, however it does not fully compensate the increase in the actual cost of materials and labour.

7. Delays in the completion of current and future projects could have adverse effects on the operating results of the Company. The Company provides performance guarantees to its clients which require the Company to complete the projects within the stipulated time frame. In case the projects are not completed as scheduled, the Company may be held liable for penalties in the form of agreed liquidated damages, which normally ranges between 5% to 10% of the total project cost. In such cases the cost of the project would exceed the original estimates and this could adversely affect the results of operations.

xii

8. Failure of joint venture partner to perform its obligations could impose additional financial and performance obligation on the Company. The Company enters into joint ventures with other construction companies for certain projects. The success of the joint ventures depends significantly on the performance and fulfillment of obligations by the joint venture partners. If the partners fail to perform their obligations, the Company may be required to make additional investments and provide additional services to ensure necessary performance as per the terms and conditions of the contract. These additional obligations could have an impact on the profits of the Company.

9. The Company utilizes independent construction contractors in some of its projects, who are not under its control which may in turn lead to delay in projects and result in impacting the operations and profitability of the Company. Small portions of work in some of the projects are sub-contracted to independent construction contractors. The Company does not have absolute control on these sub-contractors. Any lapses or non performance of obligation by these contractors could delay the projects and the Company may be required to incur additional costs and time to complete the projects which could result in reduced profits or in some cases, significant losses.

10. Breakdown of machinery and equipments may adversely affect the operations of the Company. The Company owns a large fleet of equipments which are used at various project sites. Breakdown of any of the major machinery may cause a delay in the execution of the project which could affect the results of operations.

11. Projects included in the order book may be delayed or modified, which could adversely affect the

cash flow and income from operations.

The order book presented may not necessarily indicate future income. The projects mentioned in the order book may undergo unanticipated variations in scope of work or schedule of implementation, etc. which could adversely affect the budgeted cash flow and results of operations.

12. The Company operates in a capital intensive industry. Inability to obtain adequate financing to

meet the Company’s liquidity and capital resource requirements may have an adverse effect on the Company’s results of operations. The Company has a mix of financial resources comprising of advance from customers, payables and borrowings from external sources. The Company’s inability to obtain such financing or delays in obtaining advances could affect the cash flow and results of operations. There can be no assurance that finance from external sources will be available at the times or in the amounts necessary to meet the Company’s requirements. The Company’s attempts to complete future financings may not be successful or favourable and failure to obtain financing on terms favourable to the Company could have an adverse effect on the business and results of operations of the Company.

13. The Company is dependent upon the experience and skills of senior management team and skilled

employees. Inability to retain them may have an adverse effect on the operations and profitability of the Company.

The senior management of the Company has vast experience in the construction business and is difficult to replace. Competition for experienced senior management and skilled employees is intense

xiii

and the Company may not be able to retain the services of its key managerial personnel or attract and retain such key managerial personnel in the future. For some of the projects the Company contracts with subcontractors and third parties for the provision of labour. It cannot be assured that skilled labour will continue to be available at reasonable rates and in the areas the projects are executed. As a result, the Company may be required to mobilize additional resources at a greater cost to ensure quality performance and delivery of contracted services.

14. The Company relies on various sub-contractors or certain third parties for their labour

requirement, any strained relations with these agencies will severely affect the operations of the Company

The Company operates in an industry which is highly labour intensive and continuous labour is critical to its business. The Company relies on external agency and certain sub-contractors to meet its labour requirements. Till date the Company shares a cordial relation with these external agencies and sub-contractors. However, it cannot be assured that the same will continue in future. Any strained relations with these agencies will severely affect the operations of the Company as it may not be able to meet any shortages arising due to this. There can also be no assurance that the external agencies and contractors will always be able to meet the Company’s labour requirement.

15. The significant portion of the Company’s order book consists of contracts from private clients

which may not progress as expected considering the current economic scenario. Any delay in the execution of the contracts could have an adverse effect on the financial performance of the Company.

The Company has been executing few major projects which are from private clients. In view of slowdown in the over all economy, there can be uncertainty about such projects being completed as per the schedule due to liquidity crunch and sluggish demand in reality sector. Heavy dependence on private clients may affect the results of operations and cash flow position of the Company.

16. The business may be affected by uninsured losses or losses exceeding the insurance limits to

the extent of the risk not covered or claims not honoured fully by the Insurance Company(s) . The Company has taken contractor’s all risk insurance policy in respect of projects, workmen’s compensation policies and for a variety of risks, including, among others, for risks relating to fire, burglary and certain other losses and damages and employee related risks. While the insurance coverage maintained would be reasonably adequate to cover all normal risks associated with the operation of the business, there can be no assurance that any claim under the insurance policies taken by us will be honoured fully, in part or on time. To the extent losses suffered by the Company or the damages not covered by insurance or which exceeds the insurance coverage, the results of operation or cash flows may be affected.

17. Monitoring the use of Issue proceeds will not be done by any independent body and the

deployment of funds would be at the sole discretion of the Company

The aggregate fund requirements have not been appraised by any bank or financial institution. The deployment of funds in various projects will be entirely at the discretion of the Company and as such no independent body will monitor the utilization of the Issue proceeds.

xiv

18. The Company has entered into various related party transactions which may potentially involve a conflict of interest which may adversely affect the operations of the Company.

The Company has entered into various transactions with related parties, including the promoters/relatives of the promoters/entities promoted by the promoters. Such transactions are made on an arm’s length basis and on no less favourable terms than if such transactions were carried out with unaffiliated third parties. These transactions in the present and future may potentially involve a conflict of interest which may adversely affect the operations of the Company.

19. The funding requirements and the deployment of the Net Proceeds of the Issue are based on

management estimates and have not been independently appraised.These management estimates may have to be revised which may result in reschedulement of expenditure programme.

The funding requirements and the deployment of the Net Proceeds of the Issue are based on management estimates and have not been appraised by any bank or financial institution. In view of the highly competitive nature of the industry in which the Company operates, the management estimates may have to be revised from time to time which may result in rescheduling of the expenditure programme.

20. Inability to obtain or maintain approvals or licenses required for its operations may adversely

affect the operations of the Company.

The Company requires certain approvals, licenses, registrations and permissions for operating its business, some of which may have expired and for which the Company has either made or is in the process of making an application for obtaining the approval or its renewal. The Company has applied for renewal of 5 Licenses which are still pending. For more information see the section titled Government Approvals beginning on page 337 of this Letter of Offer. There can be no assurance that the Company will be able to obtain the relevant licenses/approvals required within the statutory time limit and that the relevant authorities will issue any such permits, licenses or approvals in time or at all. Failure by the Company to renew, maintain or obtain the required permits, licenses or permits may adversely affect on the business of the Company.

21. The Company currently enjoys certain tax benefits, and any adverse change in the tax policies

applicable to it may affect the profitability of the Company.

Presently, the Company enjoys certain benefits under Section 80IA of the Income Tax Act, 1961. As a result of these incentives, some of the infrastructure projects are subject to relatively low tax liabilities. There is no assurance that the projects will continue to enjoy the tax benefits under Section 80IA in future. When these incentives expire or terminate, the tax expense will materially increase, thereby reducing the profitability.

22. The Company may not be selected for any of the projects for which it has submitted a bid

which may adversily affect overall performance of the Company. There are certain proposed projects for which the Company has submitted bids or are qualified to submit bids, individually and or jointly with other Companies. Preparing and submitting bids involve significant costs which are one time costs. There is no assurance that the Company’s bid would be accepted and that there might be a delay in the selection process and may not be finalized within the expected time frame.

xv

23. Changes in technology may render the current technologies obsolete or require the Company

to make substantial capital investments which may affect the profitability of the Company.

The technology requirements in the Industry in which the Company operates are subject to continuing change and development. Some of the existing technologies may become obsolete, performing less efficiently compared to the latest technologies and processes in future. The cost of upgrading or implementing new technologies, upgrading the existing equipment or replacing the old equipment could be significant and could adversely affect the results of operation of the Company.

Risks Internal to the Company 24. Certain entities in the Promoter Group are engaged in business activities similar to the

Company, which could result in a conflict of interest and may adversely affect the operations and the financial performance of the Company.

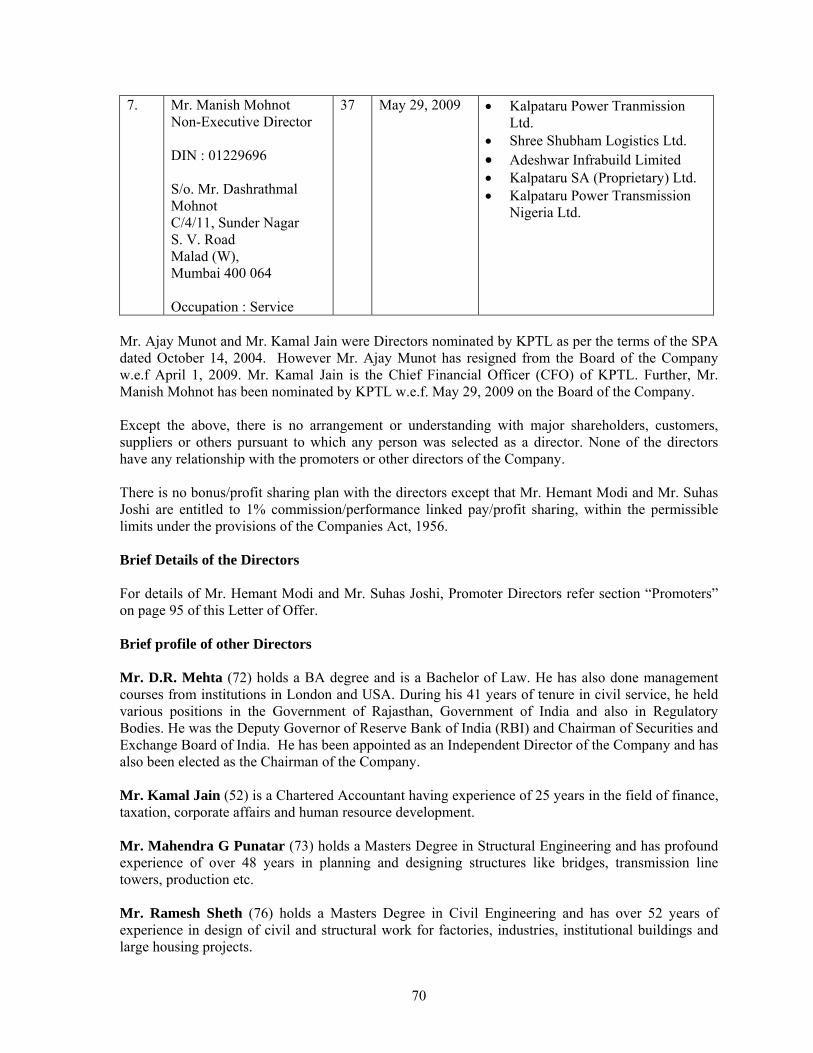

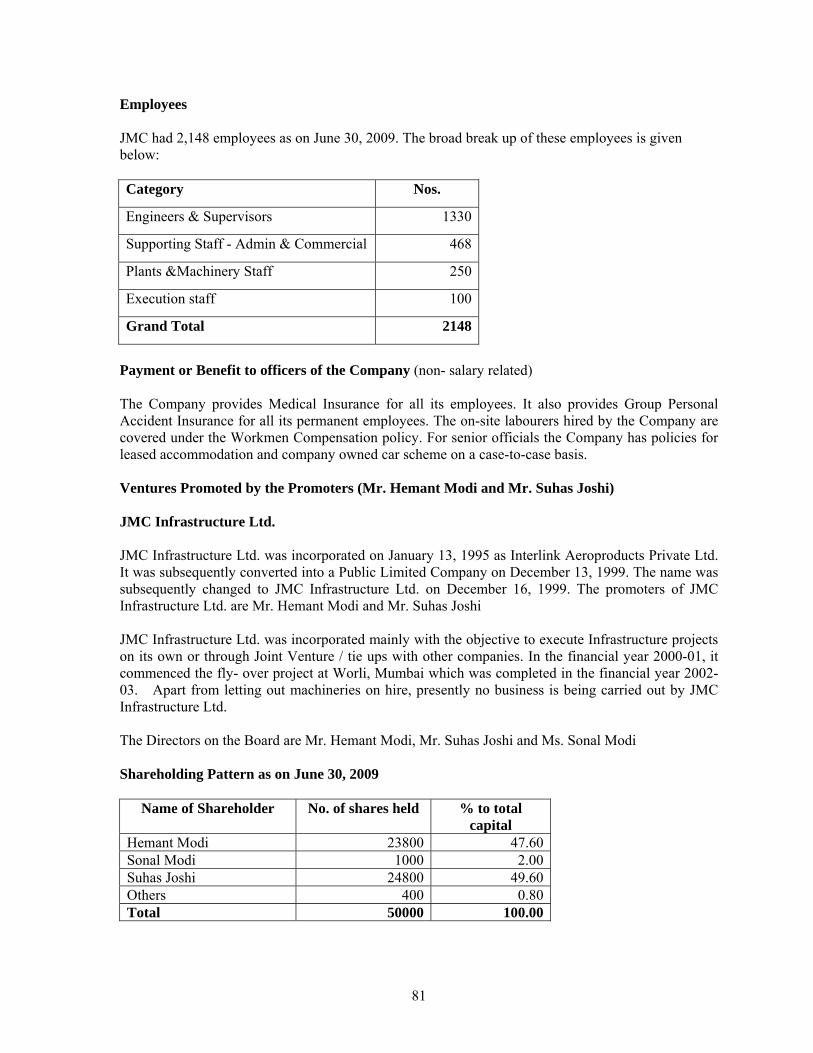

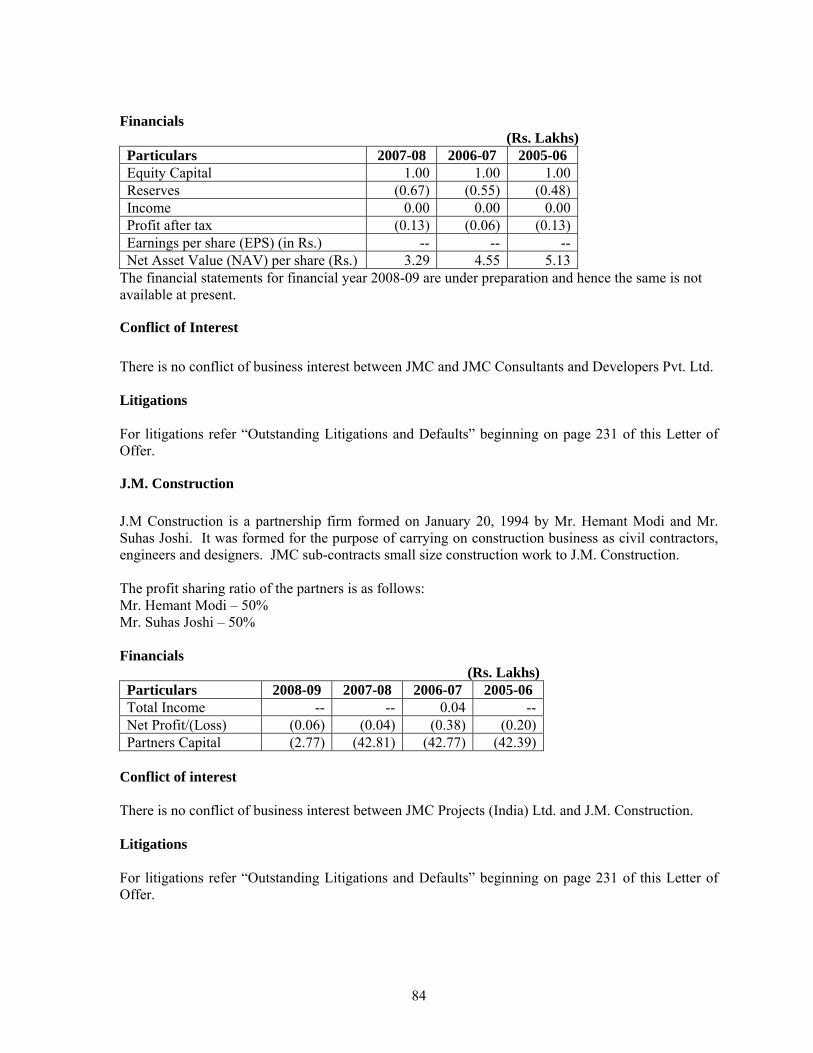

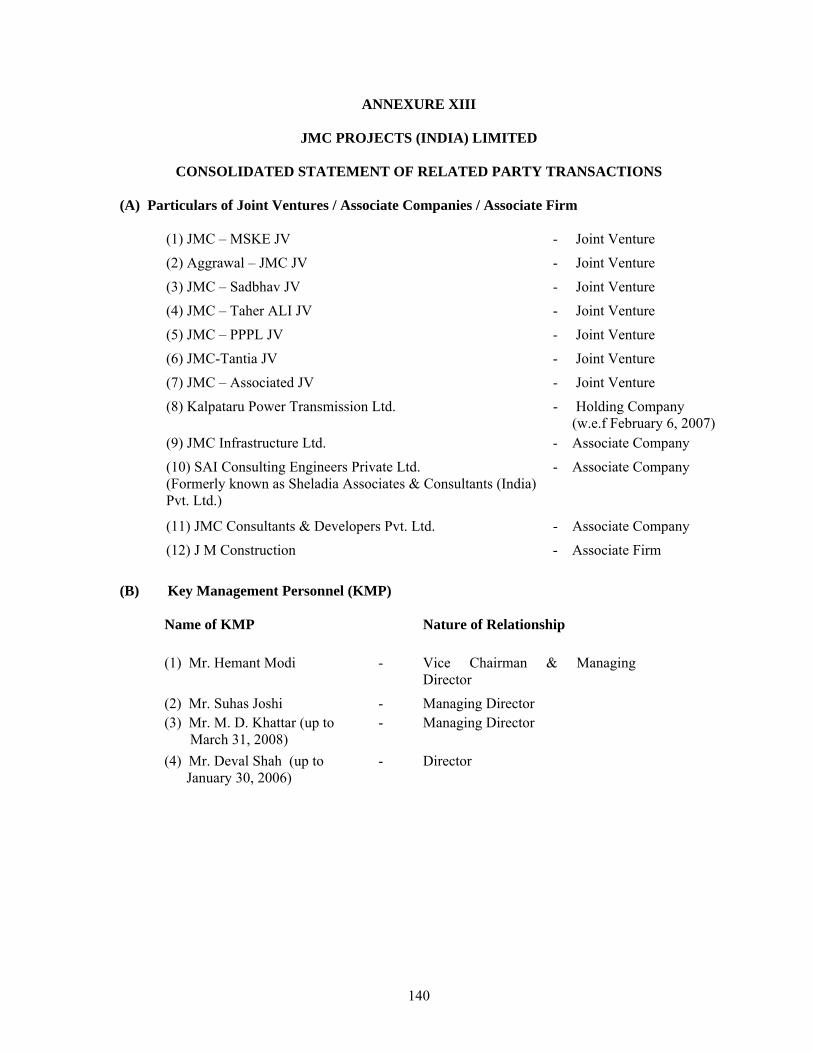

Mr. Hemant Modi and Mr. Suhas Joshi, Promoters of the Company, (individually or jointly) together with their relatives have interest in the following ventures which are authorized by its main objects clause to carry on a similar line of activities. At present there are no conflicting interest however in future there may be a conflict of business interests among these ventures and the Company. Their interest in the companies is given below:

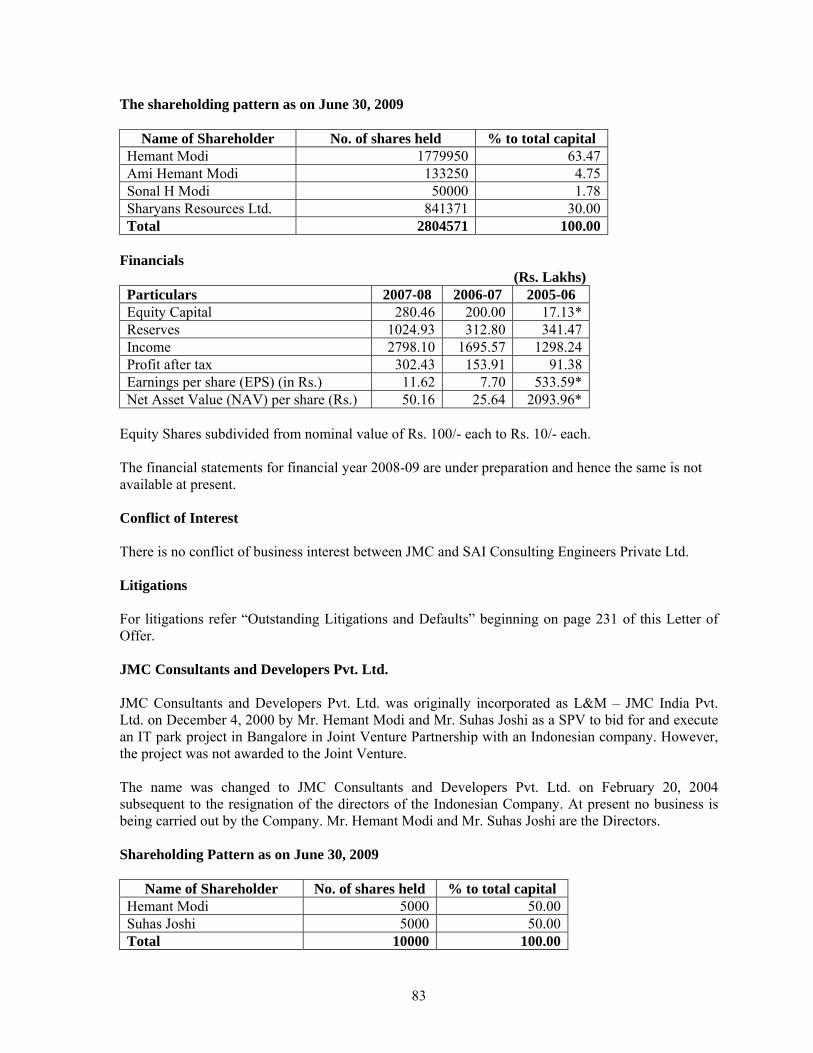

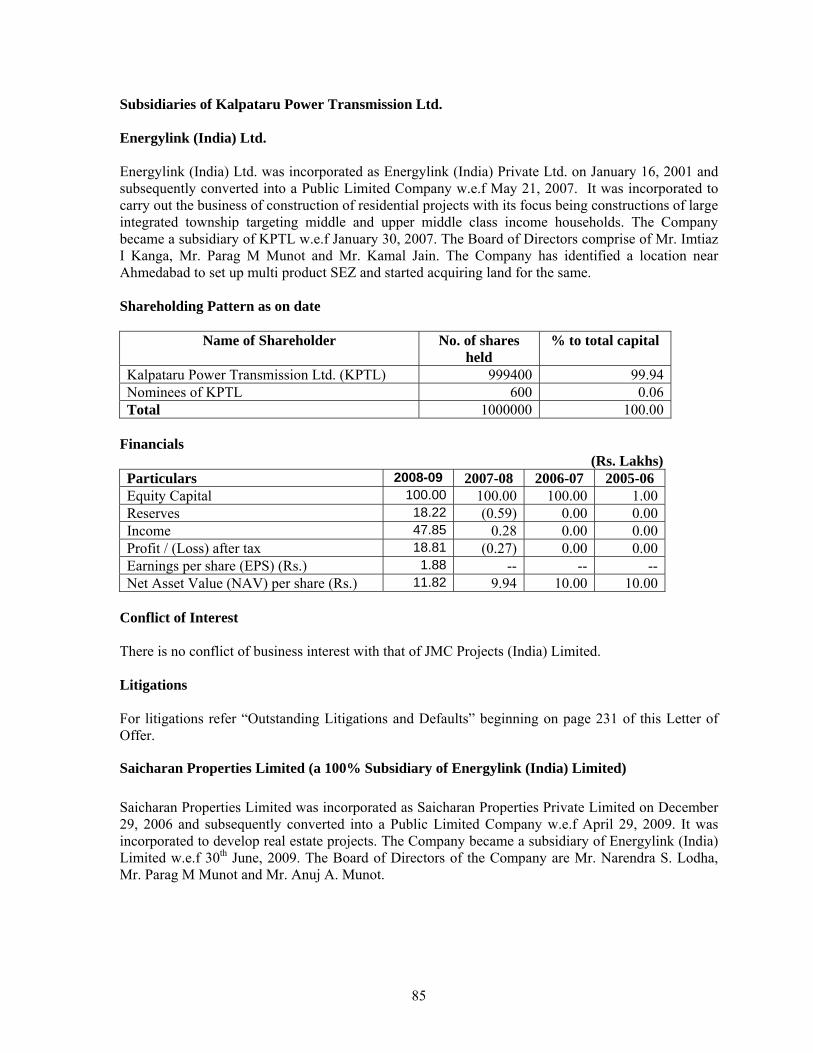

Name of the venture Nature of interest JMC Infrastructure Limited Shareholding (99.20%) SAI Consulting Engineers Private Limited Shareholding (70.00%) JMC Consultants and Developers Private Limited

Shareholding (100.00%)

JM Construction (Partnership Firm) Profit sharing (100.00%)

Apart from JMC Infrastructure Ltd., the Company does not have business transactions with any of the above mentioned ventures.

25. The Promoters and Directors of the Company have interest in the Company other than

reimbursement of expenses incurred or normal remuneration or benefits.

The Promoters and Directors are interested in the Company to the extent of their shareholding in the Company. They are also interested to the extent of any dividend payable to them. KPTL is interested to the extent of rent received for office premises and guest house that has been leased to the Company, interest on inter corporate deposits and income from sale of goods and providing erection & commissioning services to the Company.

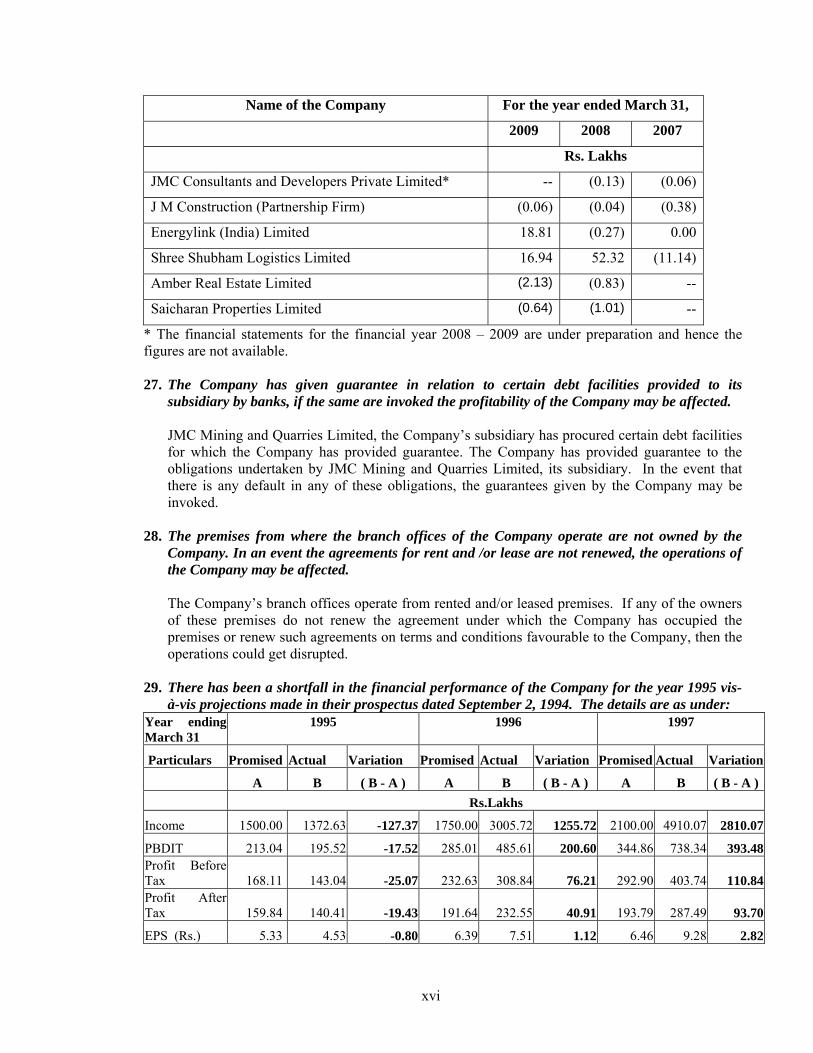

26. Some of the Group Companies and subsidiaries of the Promoter have incurred losses in the

last three fiscal years.

Some of the Group Companies and subsidiaries of the Promoter have incurred losses in the last three fiscal years, as set forth in the table below:

xvi

Name of the Company For the year ended March 31,

2009 2008 2007

Rs. Lakhs

JMC Consultants and Developers Private Limited* -- (0.13) (0.06)

J M Construction (Partnership Firm) (0.06) (0.04) (0.38)

Energylink (India) Limited 18.81 (0.27) 0.00

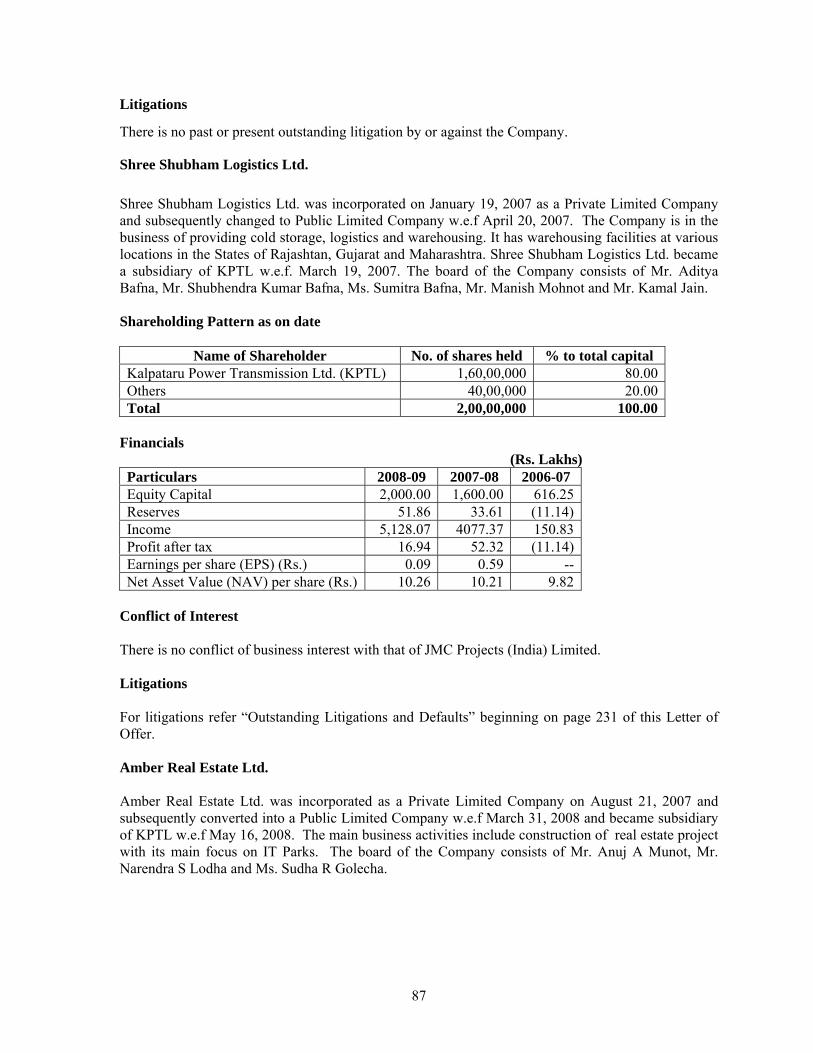

Shree Shubham Logistics Limited 16.94 52.32 (11.14)

Amber Real Estate Limited (2.13) (0.83) --

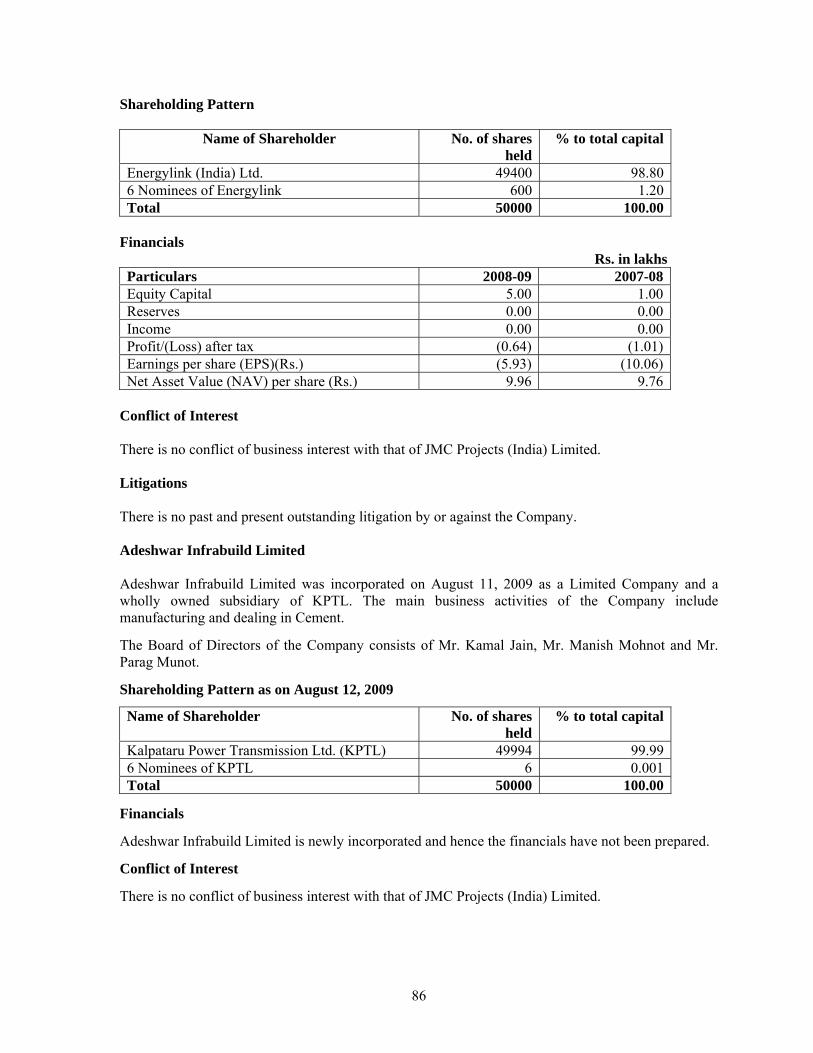

Saicharan Properties Limited (0.64) (1.01) --

* The financial statements for the financial year 2008 – 2009 are under preparation and hence the figures are not available. 27. The Company has given guarantee in relation to certain debt facilities provided to its

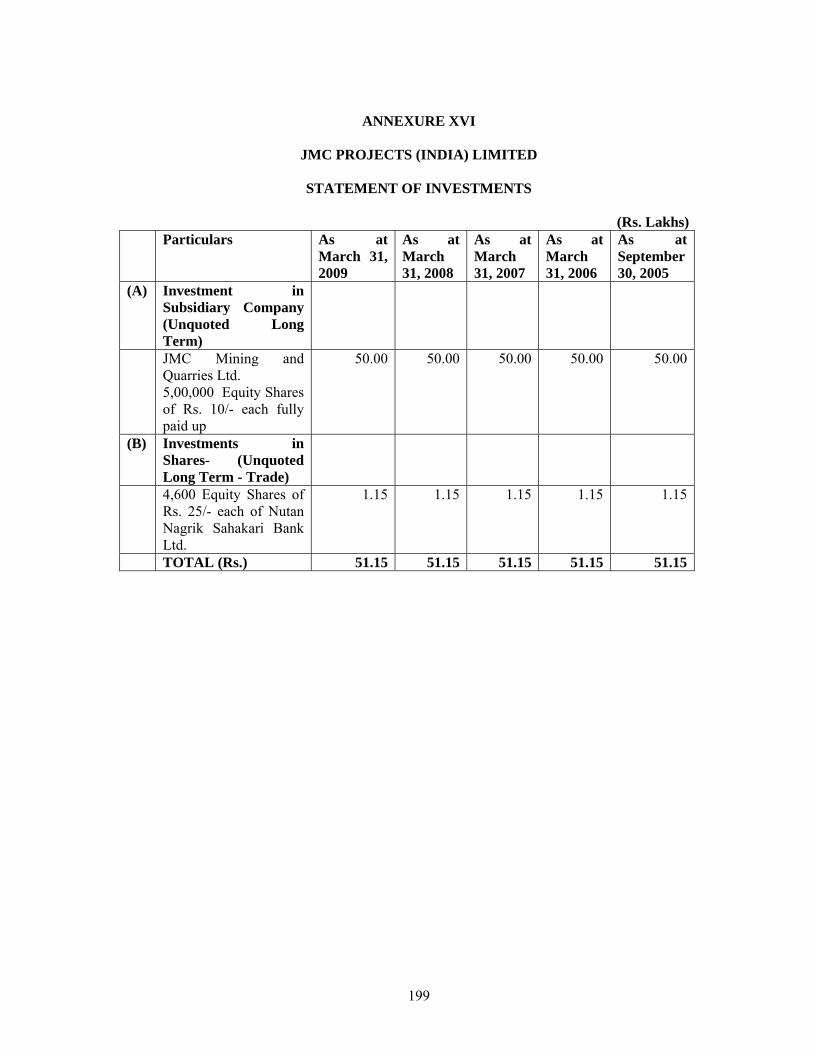

subsidiary by banks, if the same are invoked the profitability of the Company may be affected.

JMC Mining and Quarries Limited, the Company’s subsidiary has procured certain debt facilities for which the Company has provided guarantee. The Company has provided guarantee to the obligations undertaken by JMC Mining and Quarries Limited, its subsidiary. In the event that there is any default in any of these obligations, the guarantees given by the Company may be invoked.

28. The premises from where the branch offices of the Company operate are not owned by the

Company. In an event the agreements for rent and /or lease are not renewed, the operations of the Company may be affected.

The Company’s branch offices operate from rented and/or leased premises. If any of the owners of these premises do not renew the agreement under which the Company has occupied the premises or renew such agreements on terms and conditions favourable to the Company, then the operations could get disrupted.

29. There has been a shortfall in the financial performance of the Company for the year 1995 vis-

à-vis projections made in their prospectus dated September 2, 1994. The details are as under: Year ending March 31

1995 1996

1997

Particulars Promised Actual Variation Promised Actual Variation Promised Actual Variation

A B ( B - A ) A B ( B - A ) A B ( B - A ) Rs.Lakhs

Income 1500.00 1372.63 -127.37 1750.00 3005.72 1255.72 2100.00 4910.07 2810.07

PBDIT 213.04 195.52 -17.52 285.01 485.61 200.60 344.86 738.34 393.48Profit Before Tax 168.11 143.04 -25.07 232.63 308.84 76.21 292.90 403.74 110.84Profit After Tax 159.84 140.41 -19.43 191.64 232.55 40.91 193.79 287.49 93.70

EPS (Rs.) 5.33 4.53 -0.80 6.39 7.51 1.12 6.46 9.28 2.82

xvii

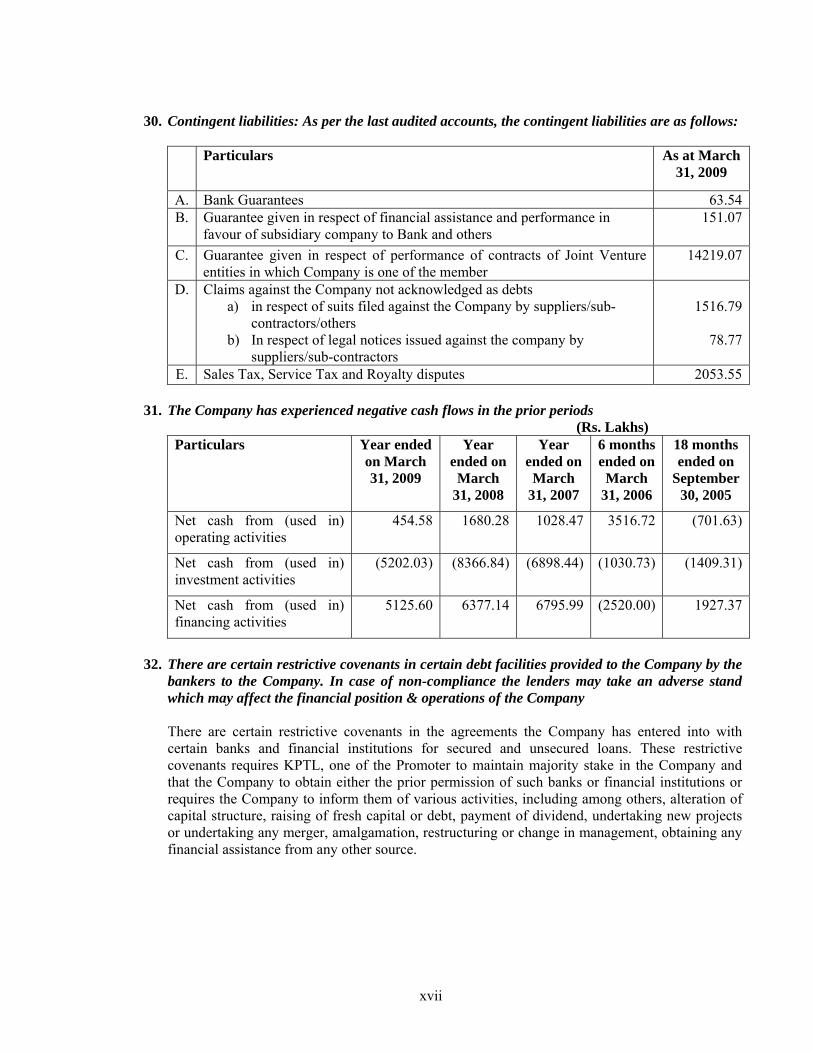

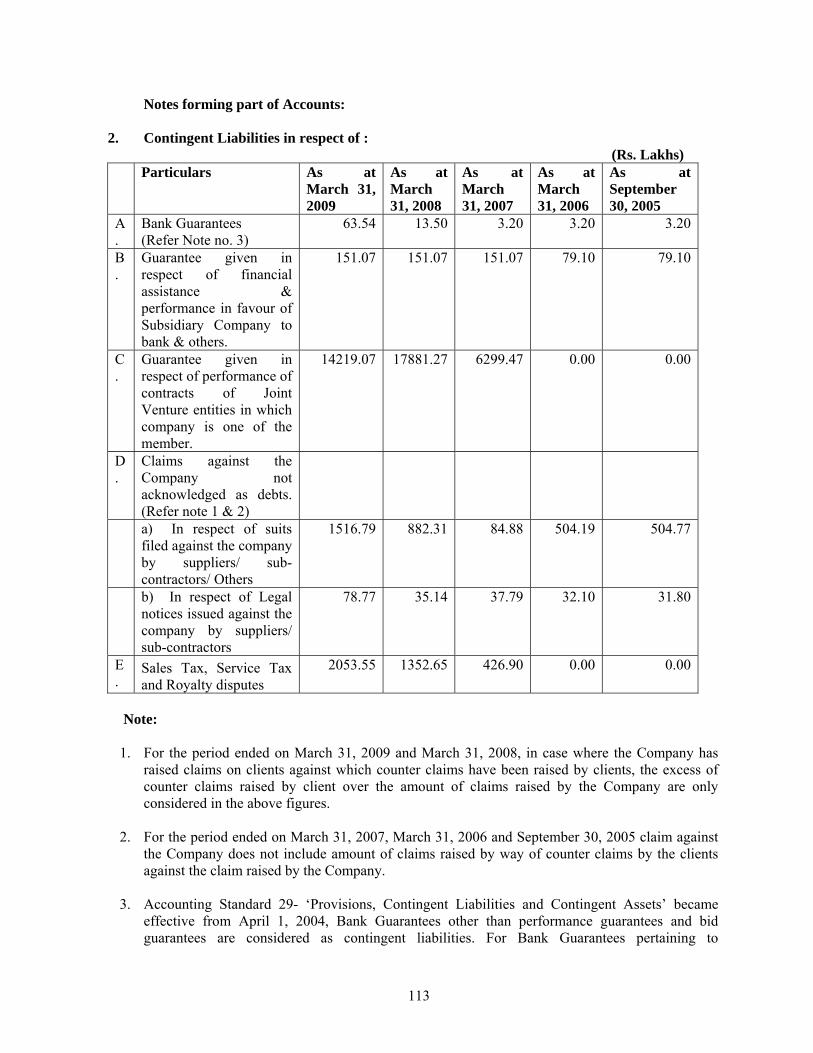

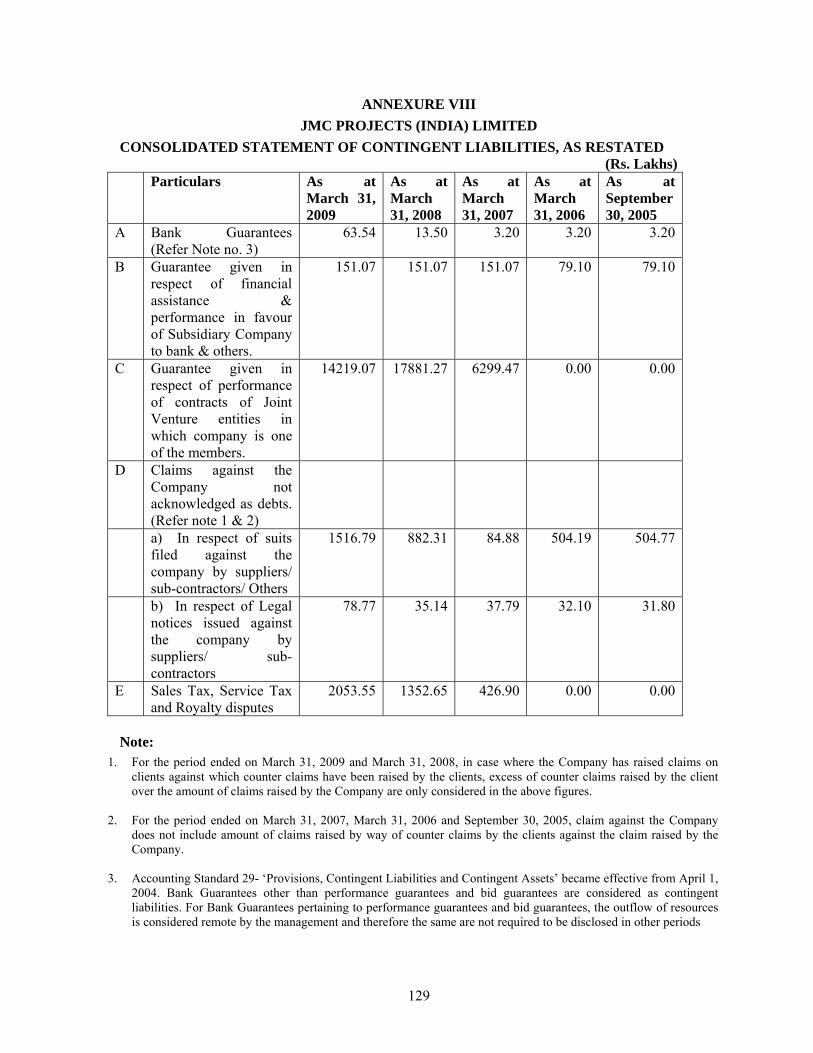

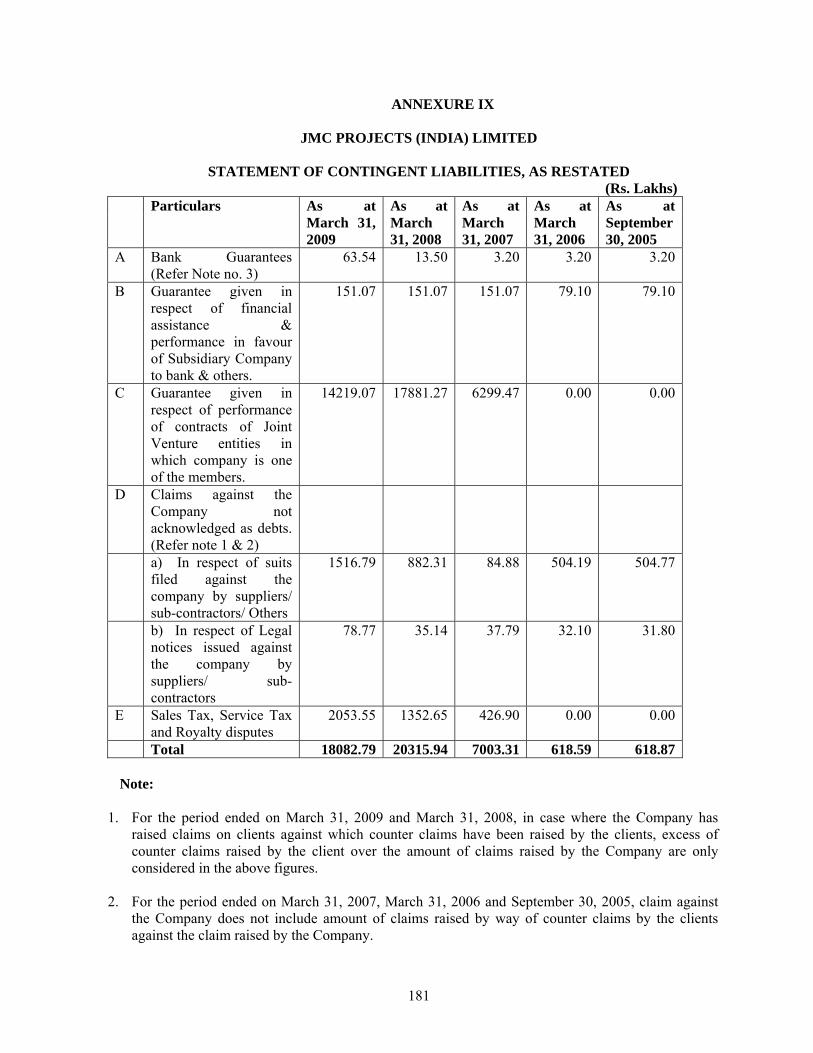

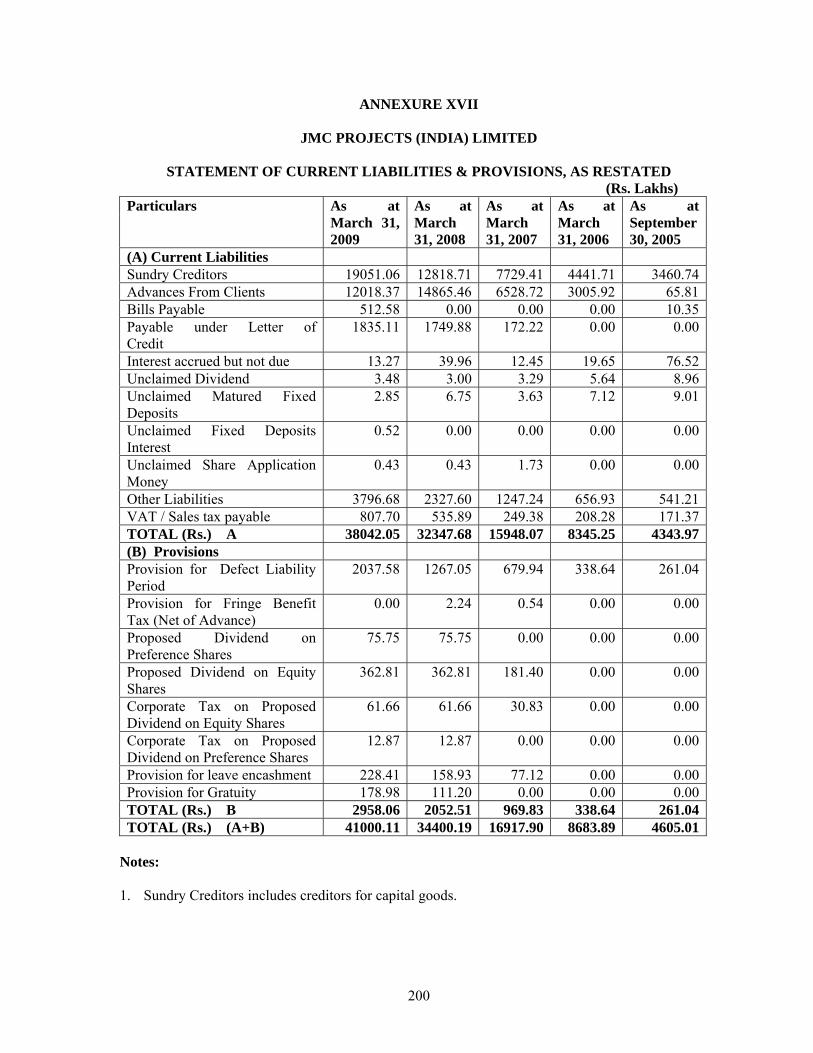

30. Contingent liabilities: As per the last audited accounts, the contingent liabilities are as follows:

Particulars As at March

31, 2009

A. Bank Guarantees 63.54B. Guarantee given in respect of financial assistance and performance in

favour of subsidiary company to Bank and others 151.07

C. Guarantee given in respect of performance of contracts of Joint Venture entities in which Company is one of the member

14219.07

D. Claims against the Company not acknowledged as debts a) in respect of suits filed against the Company by suppliers/sub-

contractors/others b) In respect of legal notices issued against the company by

suppliers/sub-contractors

1516.79

78.77

E. Sales Tax, Service Tax and Royalty disputes 2053.55

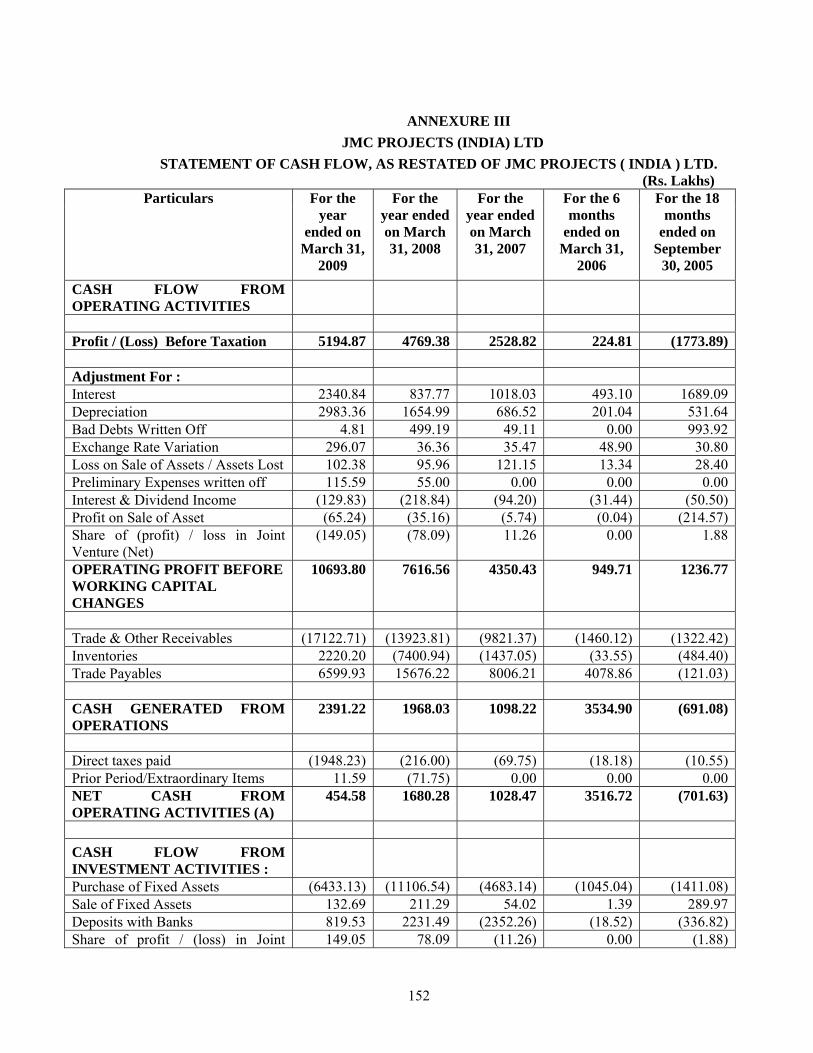

31. The Company has experienced negative cash flows in the prior periods (Rs. Lakhs)

Particulars Year ended on March 31, 2009

Year ended on March

31, 2008

Year ended on March

31, 2007

6 months ended on March

31, 2006

18 months ended on

September 30, 2005

Net cash from (used in) operating activities

454.58 1680.28 1028.47 3516.72 (701.63)

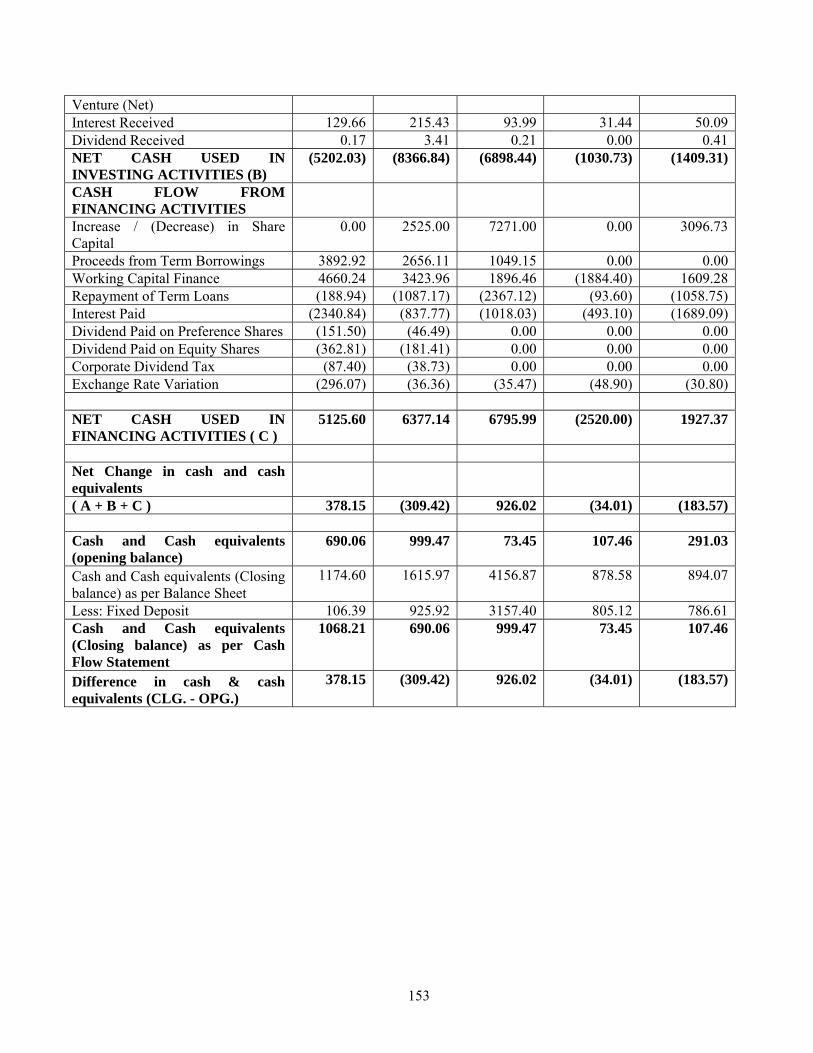

Net cash from (used in) investment activities

(5202.03) (8366.84) (6898.44) (1030.73) (1409.31)

Net cash from (used in) financing activities

5125.60 6377.14 6795.99 (2520.00) 1927.37

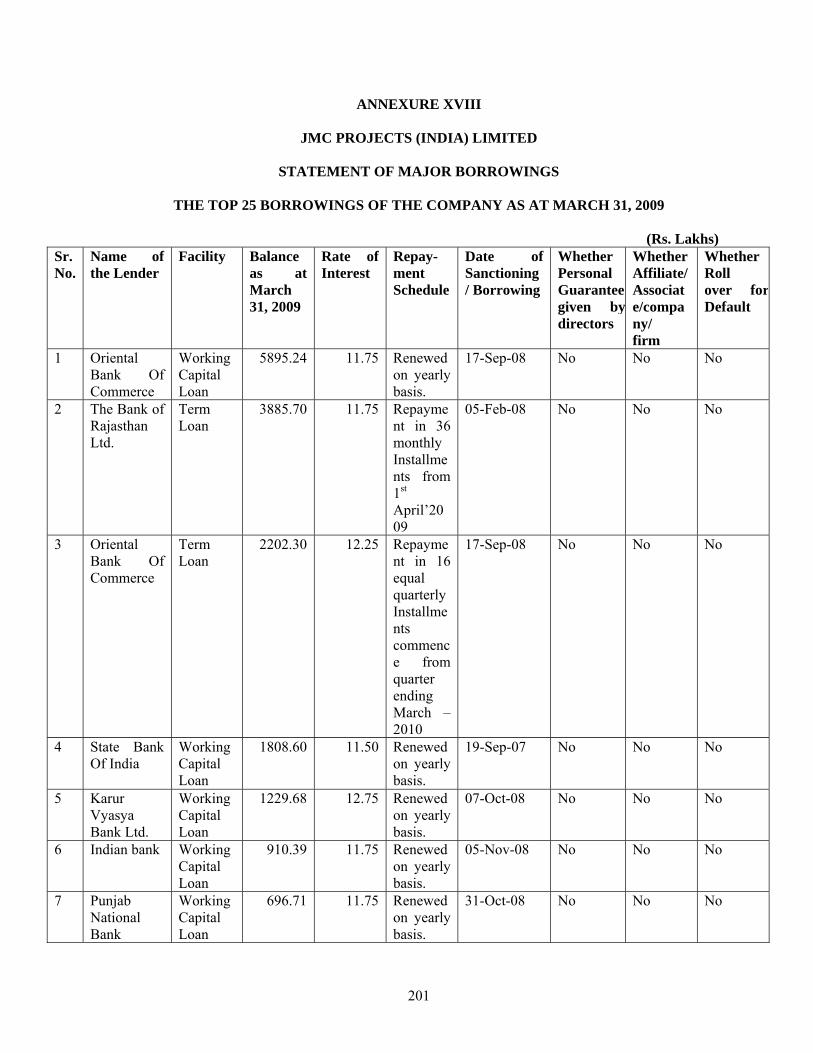

32. There are certain restrictive covenants in certain debt facilities provided to the Company by the

bankers to the Company. In case of non-compliance the lenders may take an adverse stand which may affect the financial position & operations of the Company

There are certain restrictive covenants in the agreements the Company has entered into with certain banks and financial institutions for secured and unsecured loans. These restrictive covenants requires KPTL, one of the Promoter to maintain majority stake in the Company and that the Company to obtain either the prior permission of such banks or financial institutions or requires the Company to inform them of various activities, including among others, alteration of capital structure, raising of fresh capital or debt, payment of dividend, undertaking new projects or undertaking any merger, amalgamation, restructuring or change in management, obtaining any financial assistance from any other source.

xviii

33. The past history of dividend declaration/payment does not assure that the Company will pay dividend to its shareholders in the near future.

The Company has declared dividends in the last two fiscal years. However, there can be no assurance that dividend will be paid in the future. The declaration and payment of dividends, if any in the future will be recommended by the Board of Directors of the Company, at their discretion and will depend on a number of factors, including legal requirements, its earnings, cash generated from operations, capital requirements and overall financial condition.

External Risk Factors The following factors which are beyond the control of the Company could have a negative impact on its performance.

34. The Company’s operations are sensitive to weather conditions. Severe weather conditions may

have an adverse effect on the results of operations of the Company

The business activities of the Company could be materially and adversely affected by severe weather conditions. Severe weather conditions may require the Company to evacuate personnel or curtail services and may result in damage to the equipment or facilities, resulting in the suspension of operations and may further prevent delivery of materials to the project sites in accordance with the contract schedules and thereby slow down the activities. This could have an adverse effect on the results of operations of the Company.

35. Natural calamities and other factors could have a negative impact on the Indian economy and

adversely affect the business.

India has experienced natural calamities like earthquakes, tsunami, floods and drought in the past few years. Our country has also witnessed political, economic, social development, acts of violence or war. All the above factors could have a negative impact on the Indian economy and may cause suspension, delays or damage to the current projects and operations, which may adversely affect the business and results of operations of the Company. Such events could also create a perception that investments in Indian companies involve a higher degree of risk, which could have an adverse effect on the market for securities of Indian companies.

36. Change in Government policies and fluctuating interest rates could have an adverse impact on

the results of operations of the Company.

Interest rates, rates of economic growth, fiscal and monetary policies of governments, inflation, deflation, tax rates and policy and other matters could significantly influence the results of operations of the business. Increasing volatility in financial markets may cause these factors to change with a greater degree of frequency and magnitude. Increase in interest rates may increase the Company’s financing costs. The taxation system within the country still remains complex. Any change in the regulatory environment may have an impact on the business of the Company.

37. A global recession and adverse market conditions could have an adverse impact on the

business of the Company.

The developed economies of the world viz. US, Europe, Japan and other are on the verge of a major recession which is affecting the economic condition and markets of not only these economies but also the economies of the emerging markets like Brazil, Russia, India and China.

xix

General business and consumer sentiment has been adversely affected due to the global slowdown and there can be no assurance that the developed economies will see good economic growth in the near future.

38. Unfavourable changes in the Exchange rates could have an adverse effect on the profitability

of the Company.

The Company has been importing raw materials & capital goods depending on the project requirements. This involves risk of exchange rate variations. In cases where the Company does not take forward cover to protect against major unfavorable variations in the exchange rate, high volatility in exchange rate may have some adverse impact on cost estimates and thereby financial performance of the Company.

39. After the present Issue, the Equity Shares of the Company may experience price and volume

fluctuation or an active trading market for the Equity Shares may not develop.

The price of the Equity Shares may fluctuate after this Issue as a result of several factors, including among other things, volatility in the Indian and global securities markets, results of operations and performance of the Company, performance of the competitors, developments in the construction and infrastructure segment, changes in perceptions in the market about investments in the construction and infrastructure sector, adverse media reports on the Company or on the sector in which the Company operates, changes in the estimates of performance of the Company, significant developments in India’s economic liberalization and deregulation policies and significant developments in India’s fiscal regulations.

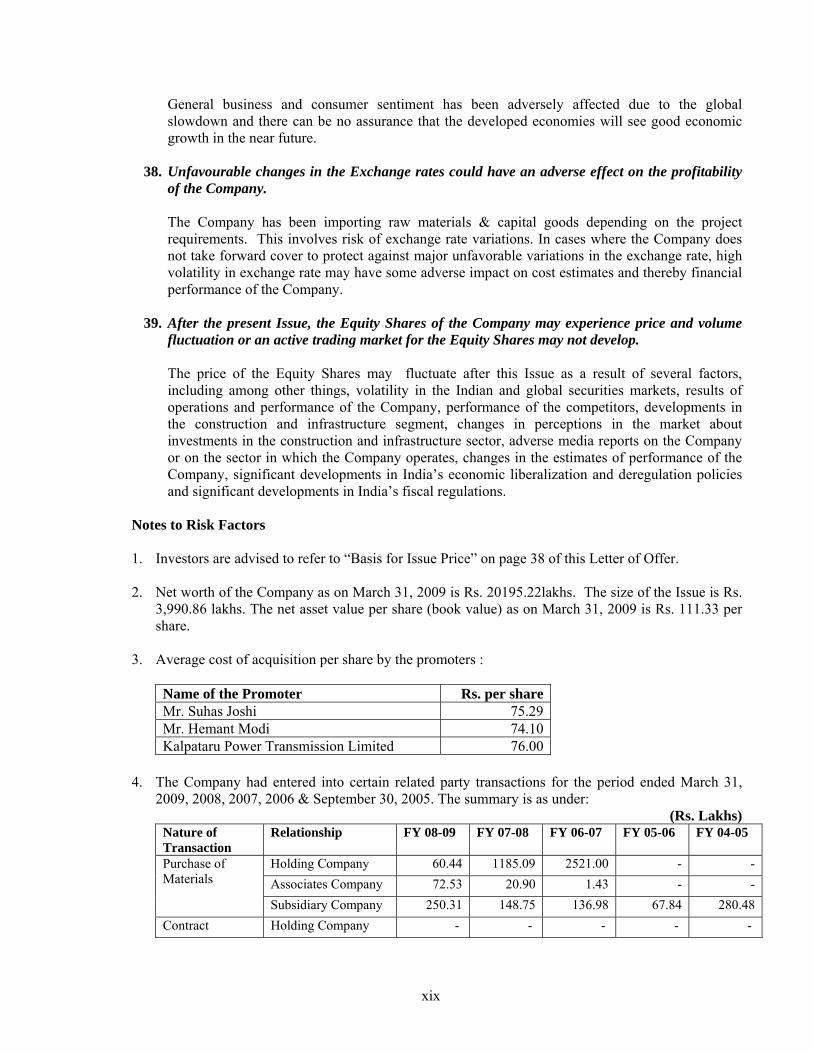

Notes to Risk Factors

1. Investors are advised to refer to “Basis for Issue Price” on page 38 of this Letter of Offer. 2. Net worth of the Company as on March 31, 2009 is Rs. 20195.22lakhs. The size of the Issue is Rs.

3,990.86 lakhs. The net asset value per share (book value) as on March 31, 2009 is Rs. 111.33 per share.

3. Average cost of acquisition per share by the promoters :

Name of the Promoter Rs. per shareMr. Suhas Joshi 75.29Mr. Hemant Modi 74.10Kalpataru Power Transmission Limited 76.00

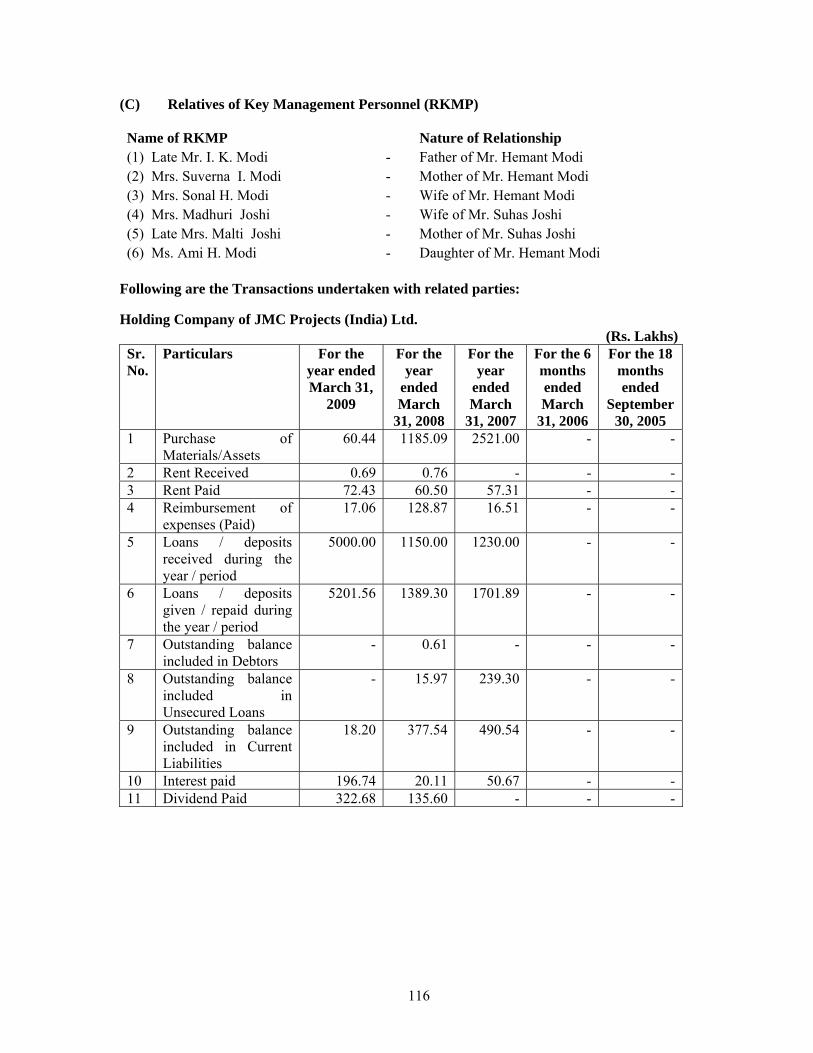

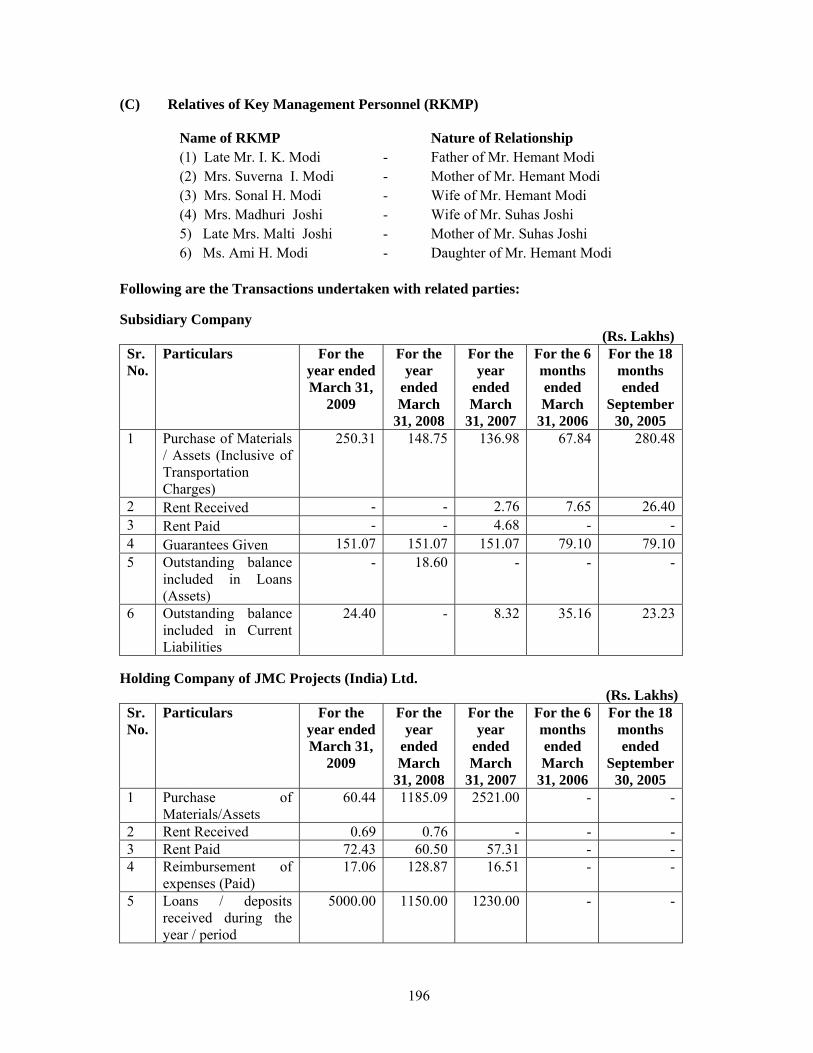

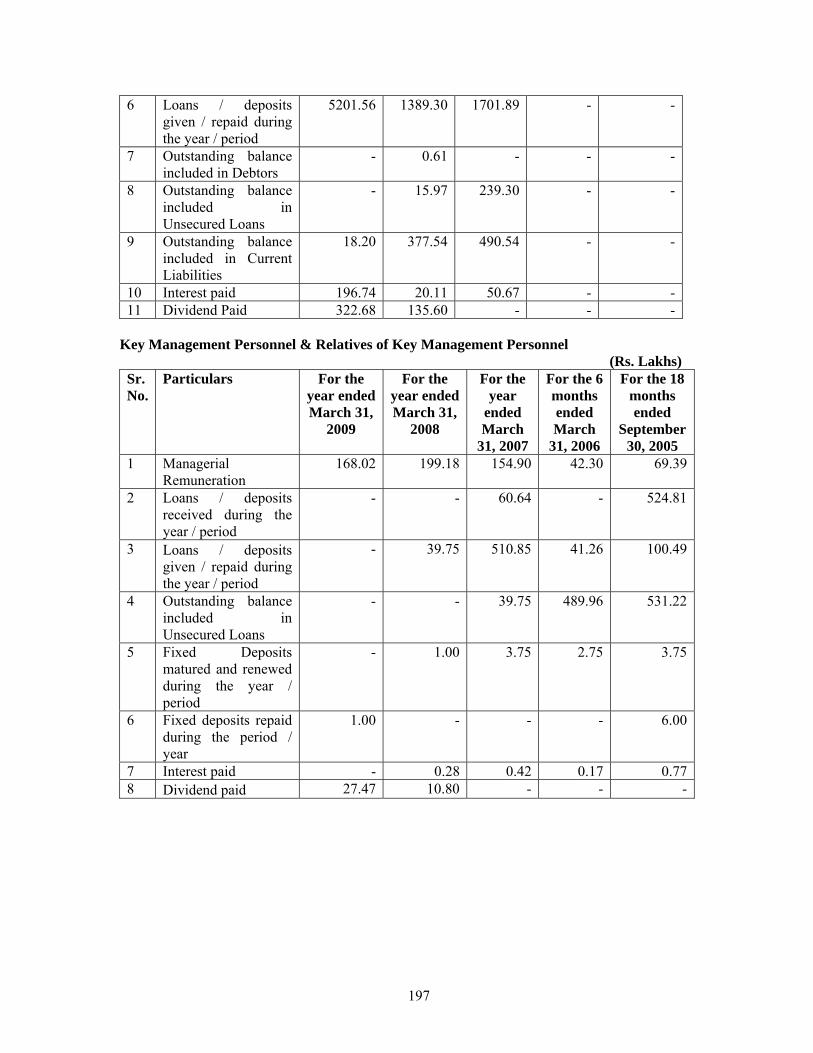

4. The Company had entered into certain related party transactions for the period ended March 31,

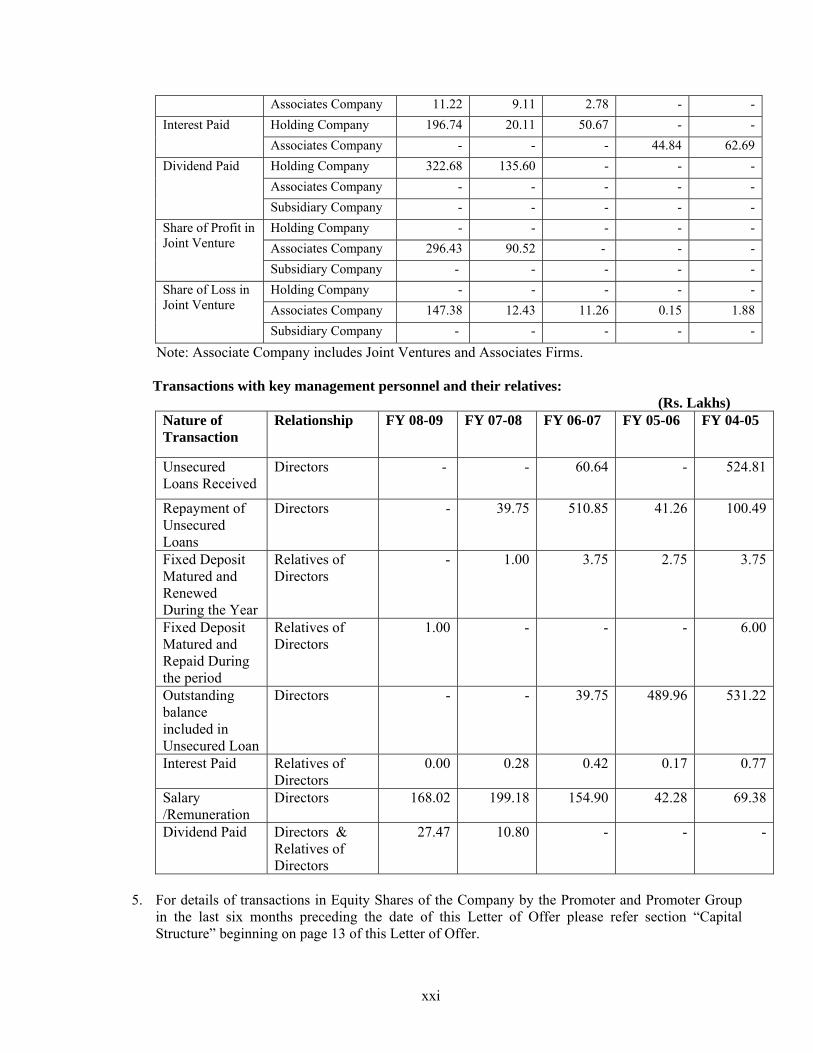

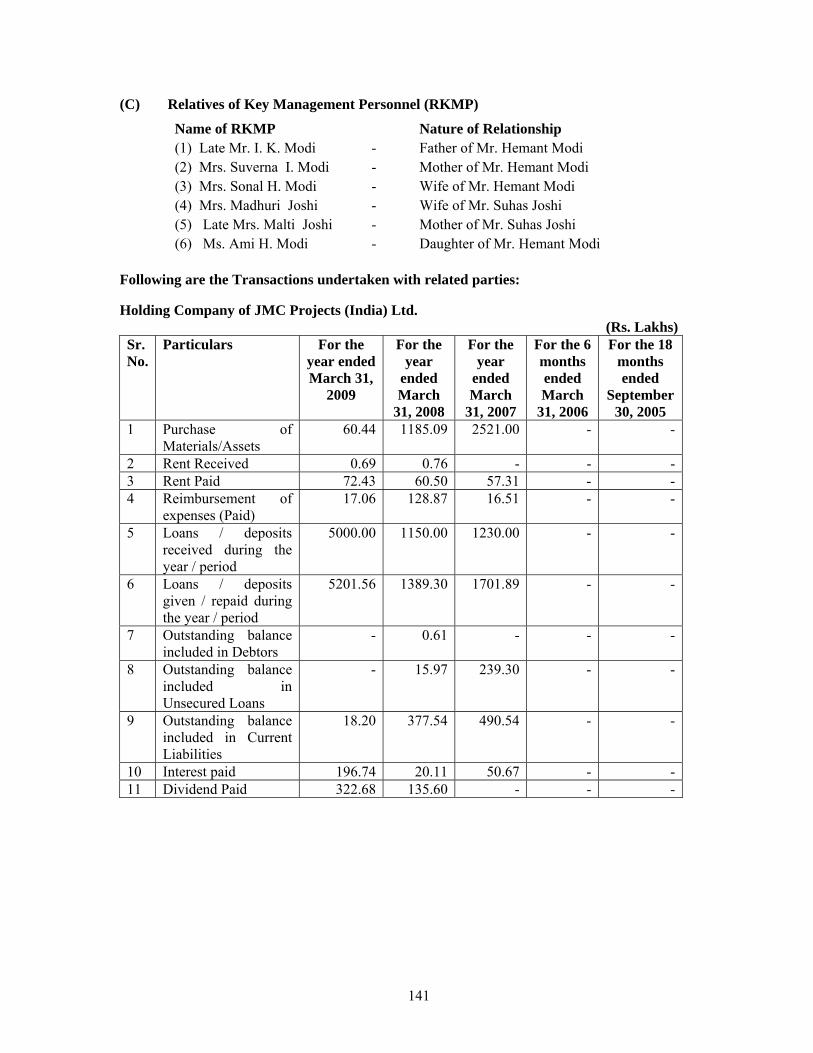

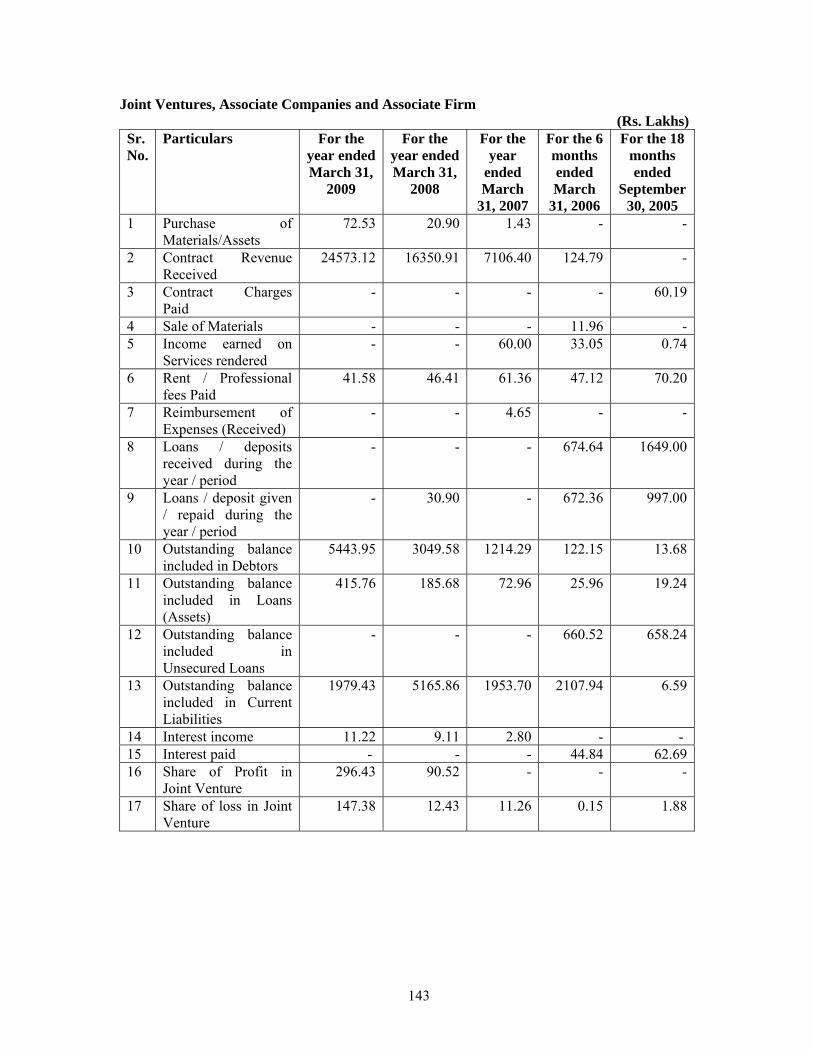

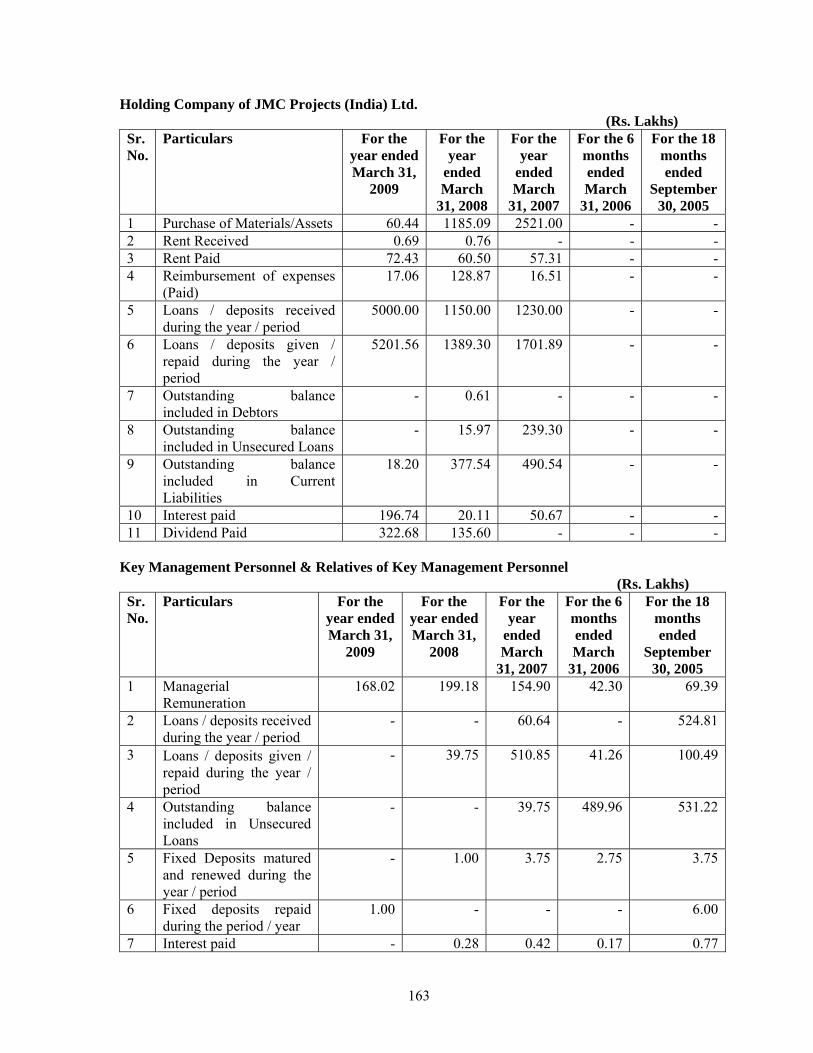

2009, 2008, 2007, 2006 & September 30, 2005. The summary is as under: (Rs. Lakhs)

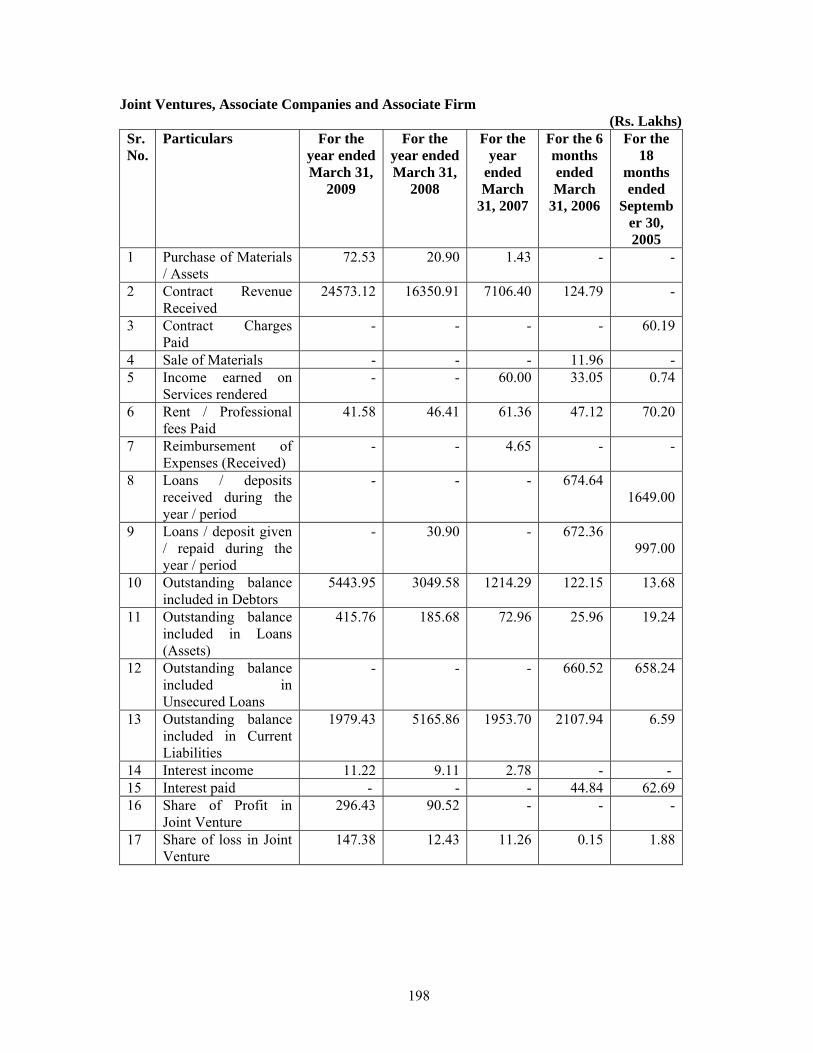

Nature of Transaction

Relationship FY 08-09 FY 07-08 FY 06-07 FY 05-06 FY 04-05

Purchase of Materials

Holding Company 60.44 1185.09 2521.00 - - Associates Company 72.53 20.90 1.43 - - Subsidiary Company 250.31 148.75 136.98 67.84 280.48

Contract Holding Company - - - - -

xx

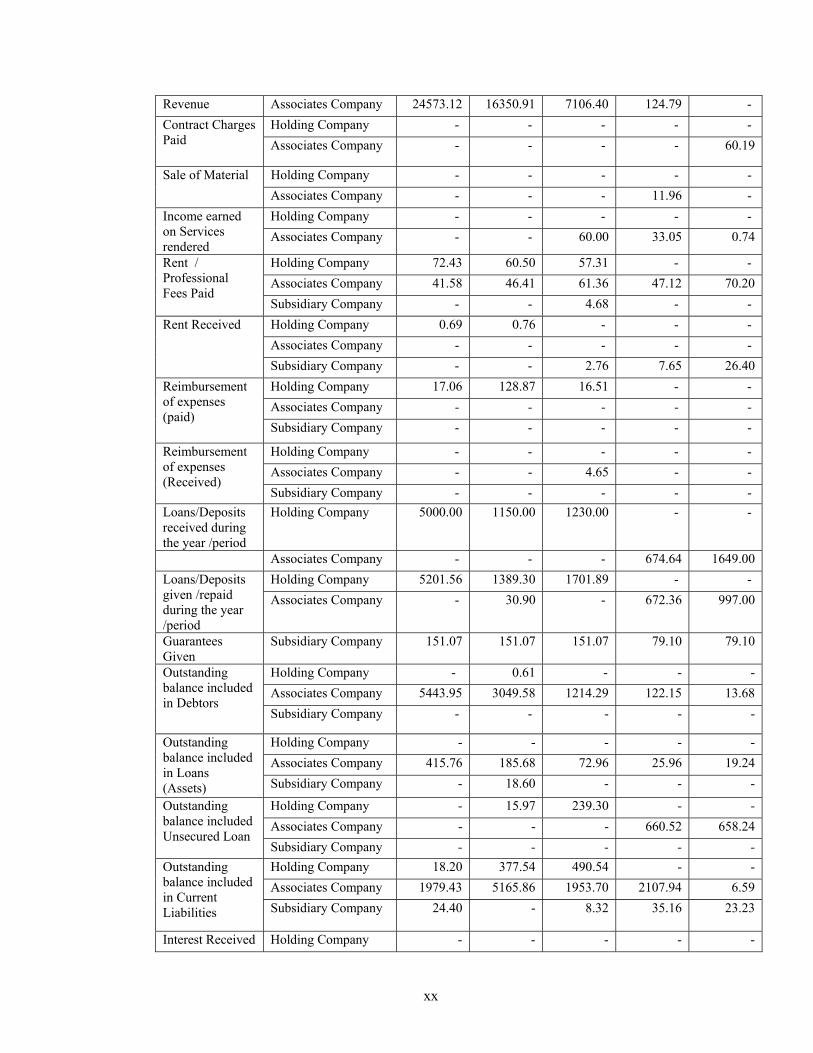

Revenue Associates Company 24573.12 16350.91 7106.40 124.79 - Contract Charges Paid

Holding Company - - - - - Associates Company - - - - 60.19

Sale of Material Holding Company - - - - - Associates Company - - - 11.96 -

Income earned on Services rendered

Holding Company - - - - - Associates Company - - 60.00 33.05 0.74

Rent / Professional Fees Paid

Holding Company 72.43 60.50 57.31 - - Associates Company 41.58 46.41 61.36 47.12 70.20 Subsidiary Company - - 4.68 - -

Rent Received Holding Company 0.69 0.76 - - - Associates Company - - - - - Subsidiary Company - - 2.76 7.65 26.40

Reimbursement of expenses (paid)

Holding Company 17.06 128.87 16.51 - - Associates Company - - - - - Subsidiary Company - - - - -

Reimbursement of expenses (Received)

Holding Company - - - - - Associates Company - - 4.65 - - Subsidiary Company - - - - -

Loans/Deposits received during the year /period

Holding Company 5000.00 1150.00 1230.00 - -

Associates Company - - - 674.64 1649.00 Loans/Deposits given /repaid during the year /period

Holding Company 5201.56 1389.30 1701.89 - - Associates Company - 30.90 - 672.36 997.00

Guarantees Given

Subsidiary Company 151.07 151.07 151.07 79.10 79.10

Outstanding balance included in Debtors

Holding Company - 0.61 - - - Associates Company 5443.95 3049.58 1214.29 122.15 13.68 Subsidiary Company - - - - -

Outstanding balance included in Loans (Assets)

Holding Company - - - - - Associates Company 415.76 185.68 72.96 25.96 19.24 Subsidiary Company - 18.60 - - -

Outstanding balance included Unsecured Loan

Holding Company - 15.97 239.30 - - Associates Company - - - 660.52 658.24 Subsidiary Company - - - - -

Outstanding balance included in Current Liabilities

Holding Company 18.20 377.54 490.54 - - Associates Company 1979.43 5165.86 1953.70 2107.94 6.59 Subsidiary Company 24.40 - 8.32 35.16 23.23

Interest Received Holding Company - - - - -

xxi

Associates Company 11.22 9.11 2.78 - - Interest Paid Holding Company 196.74 20.11 50.67 - -

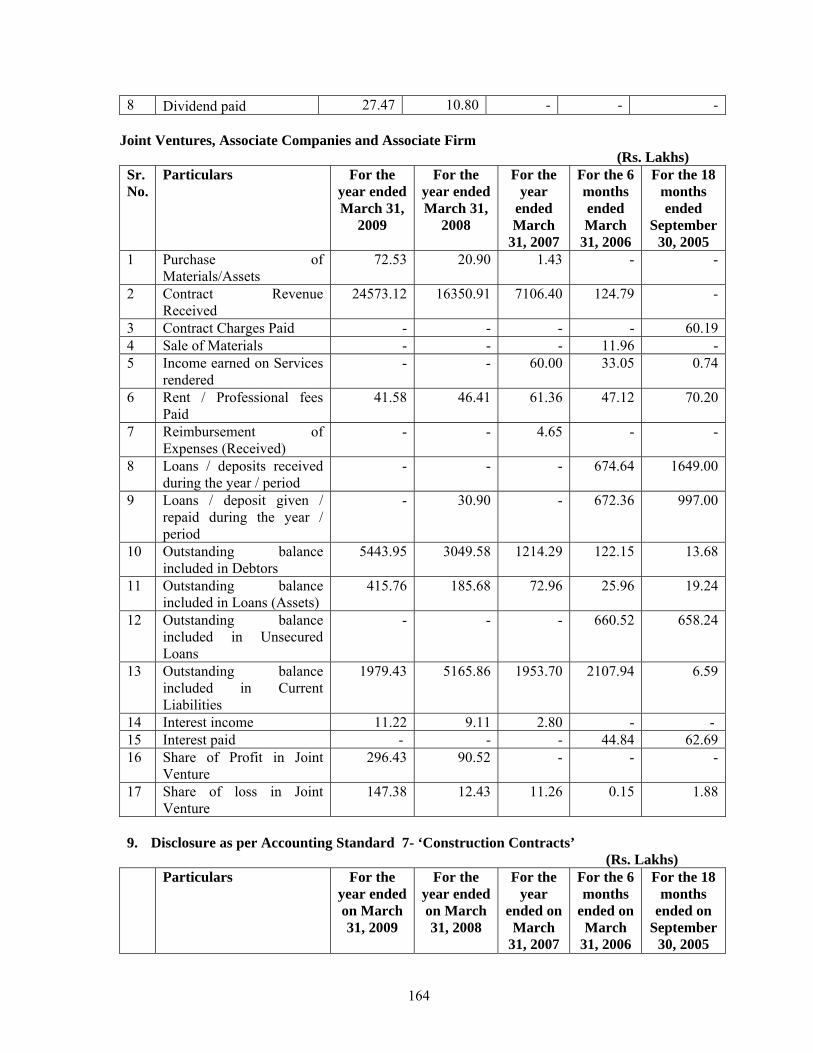

Associates Company - - - 44.84 62.69 Dividend Paid Holding Company 322.68 135.60 - - -

Associates Company - - - - - Subsidiary Company - - - - -

Share of Profit in Joint Venture

Holding Company - - - - - Associates Company 296.43 90.52 - - - Subsidiary Company - - - - -

Share of Loss in Joint Venture

Holding Company - - - - - Associates Company 147.38 12.43 11.26 0.15 1.88 Subsidiary Company - - - - -

Note: Associate Company includes Joint Ventures and Associates Firms.

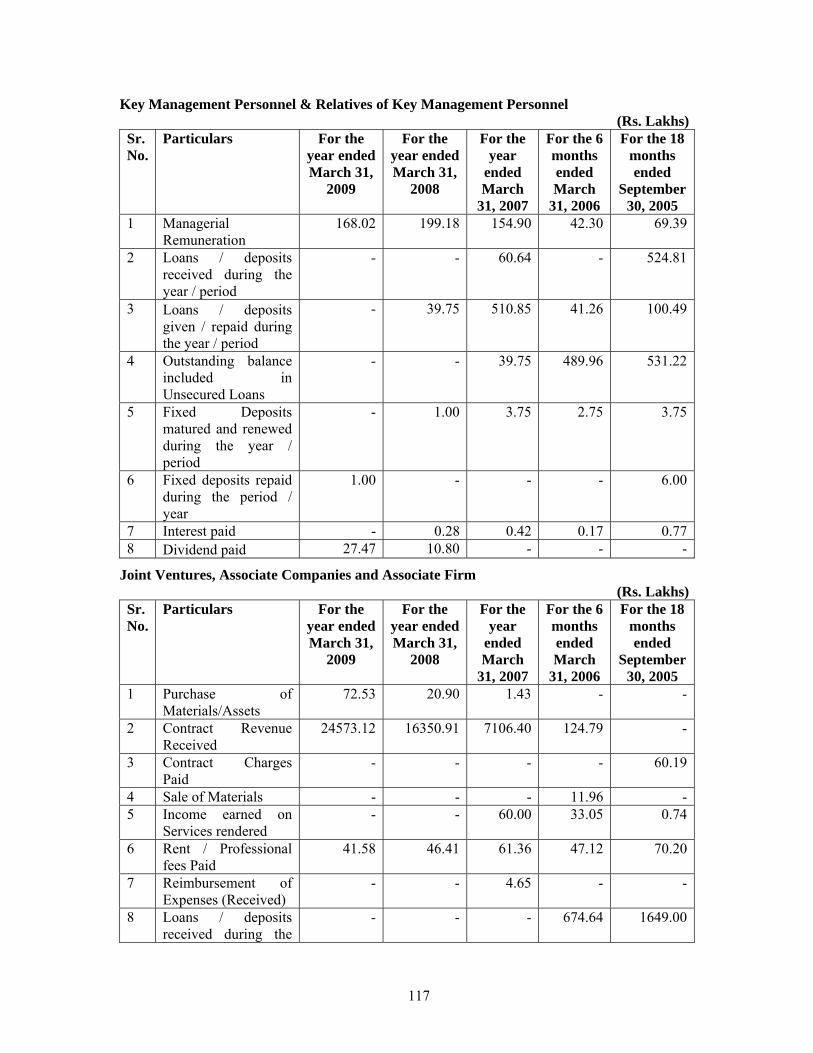

Transactions with key management personnel and their relatives: (Rs. Lakhs)

Nature of Transaction

Relationship FY 08-09 FY 07-08 FY 06-07 FY 05-06 FY 04-05

Unsecured Loans Received

Directors

- - 60.64 - 524.81

Repayment of Unsecured Loans

Directors - 39.75 510.85 41.26 100.49

Fixed Deposit Matured and Renewed During the Year

Relatives of Directors

- 1.00 3.75 2.75 3.75

Fixed Deposit Matured and Repaid During the period

Relatives of Directors

1.00 - - - 6.00

Outstanding balance included in Unsecured Loan

Directors - - 39.75 489.96 531.22

Interest Paid Relatives of Directors

0.00 0.28 0.42 0.17 0.77

Salary /Remuneration

Directors 168.02 199.18 154.90 42.28 69.38

Dividend Paid Directors & Relatives of Directors

27.47 10.80 - - -

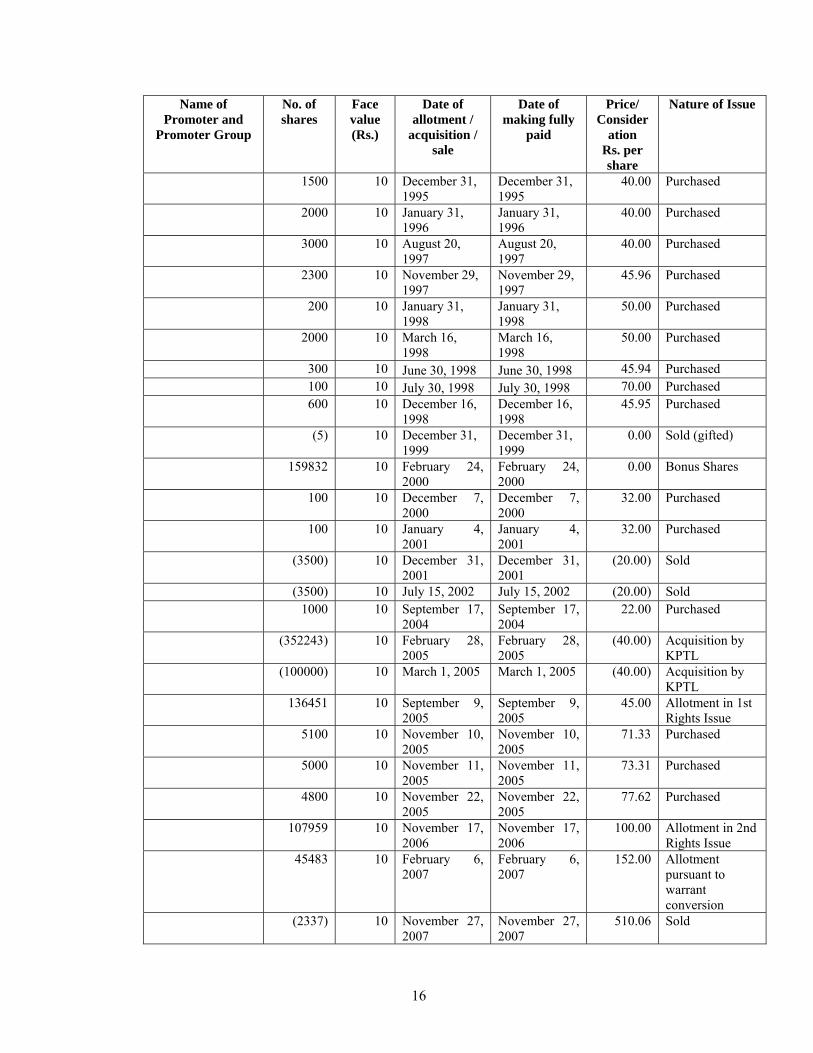

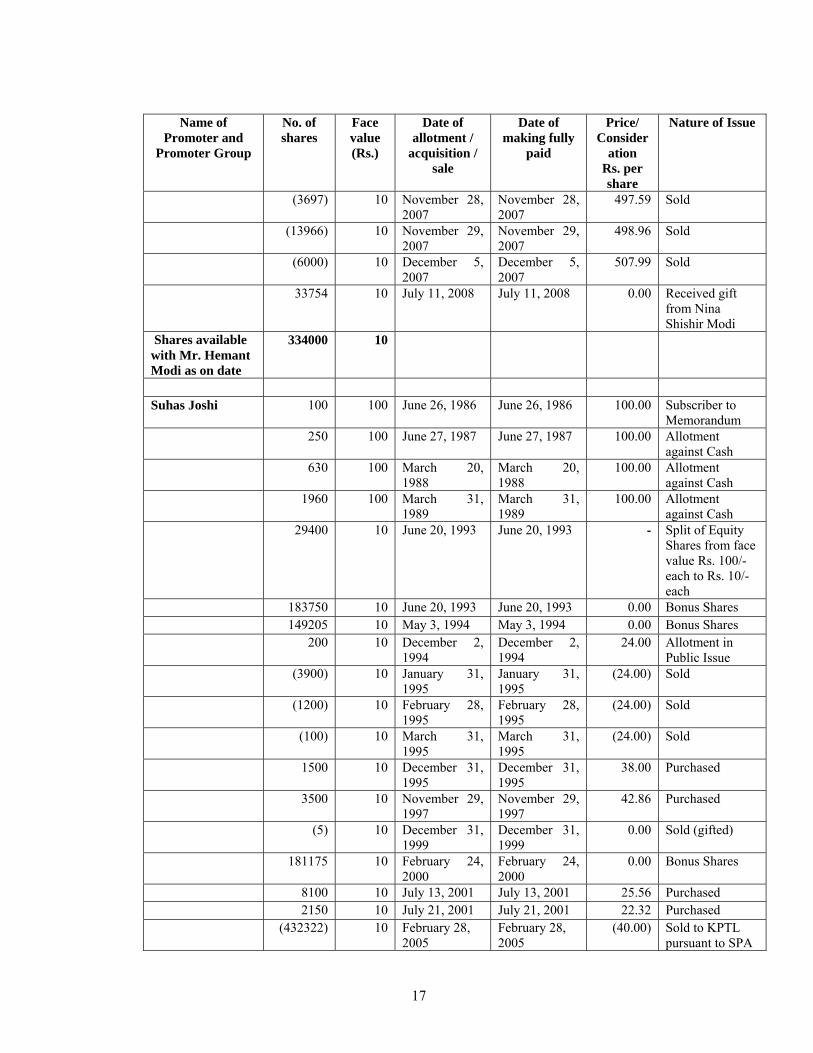

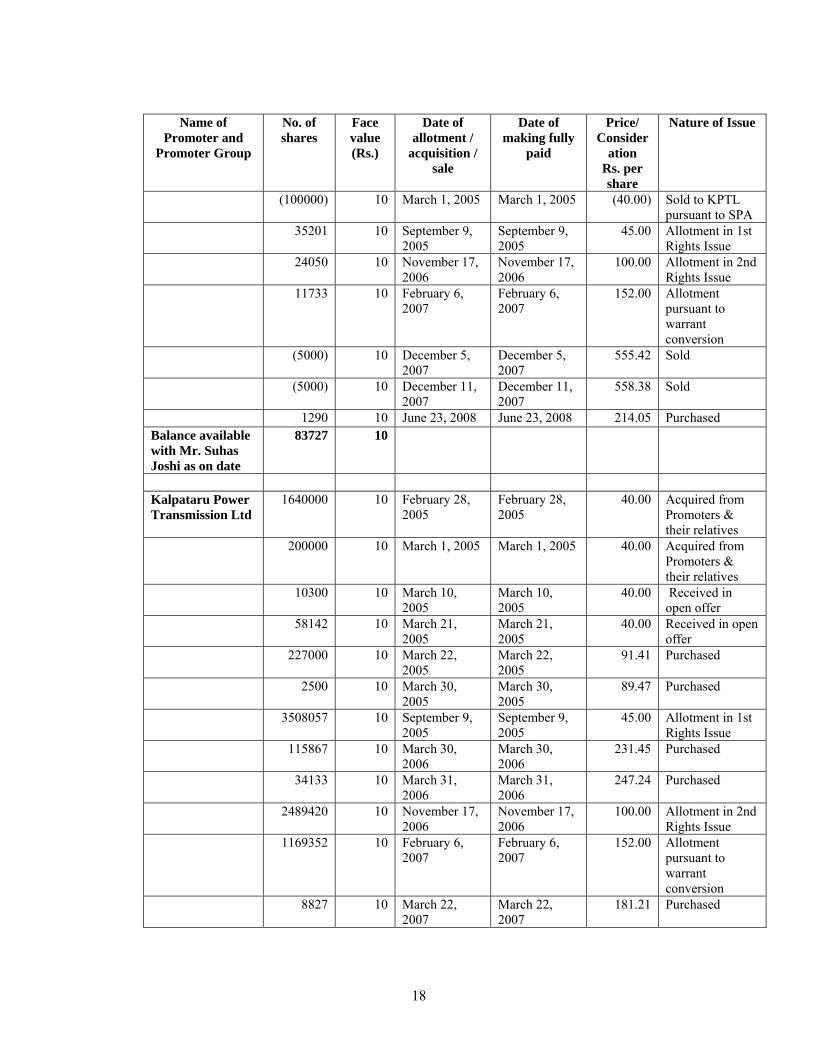

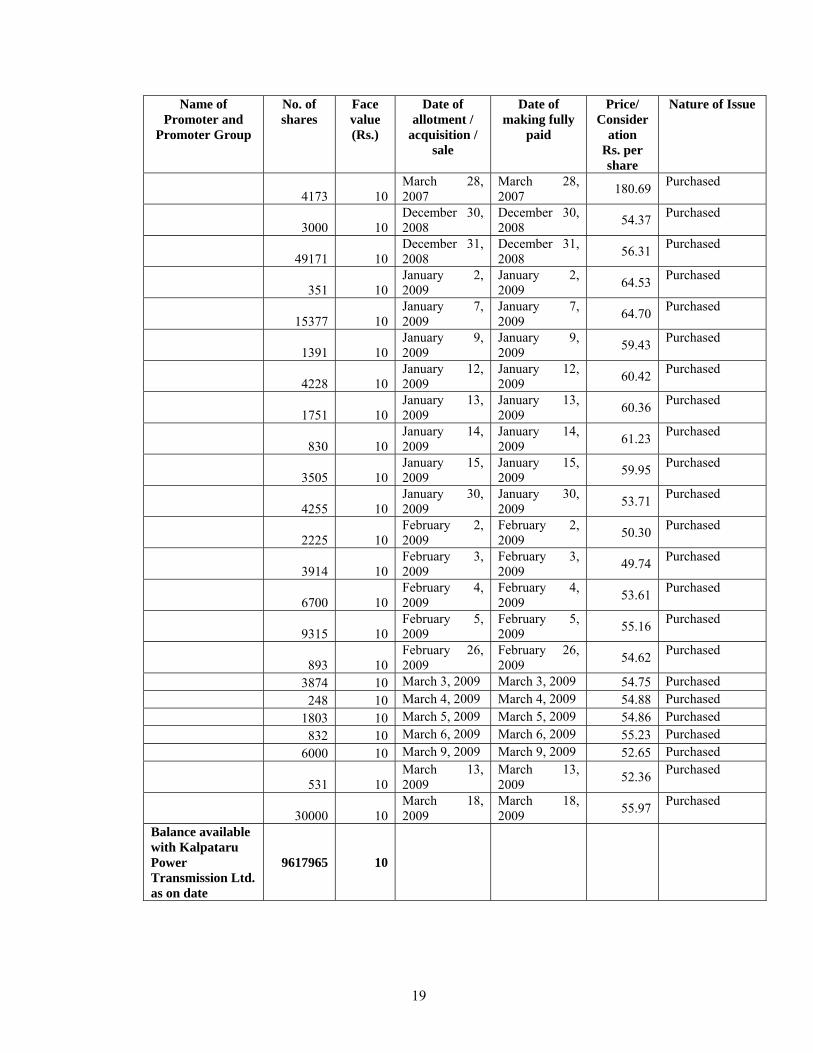

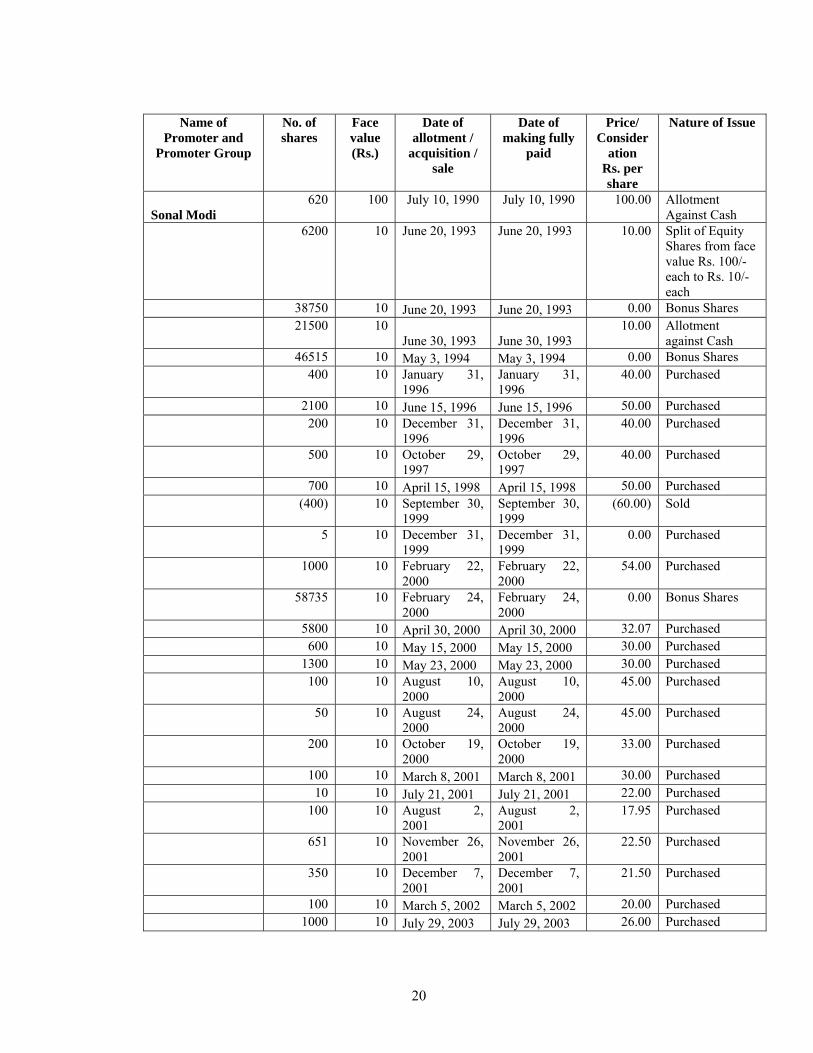

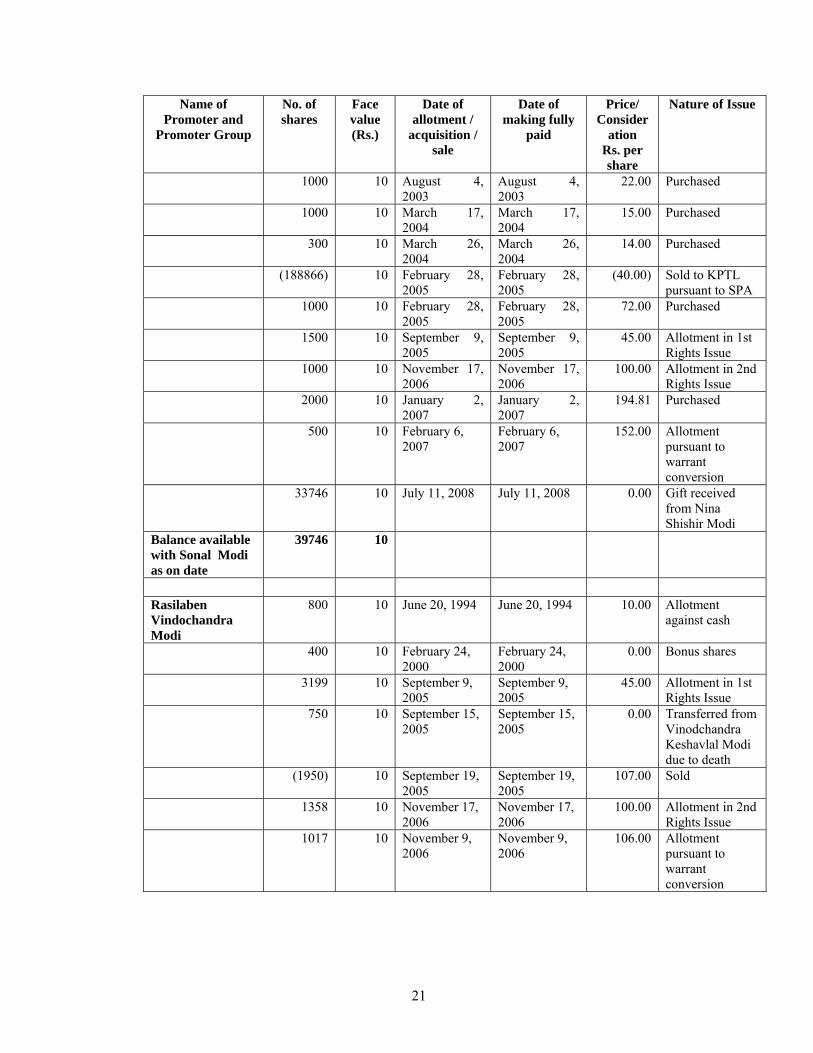

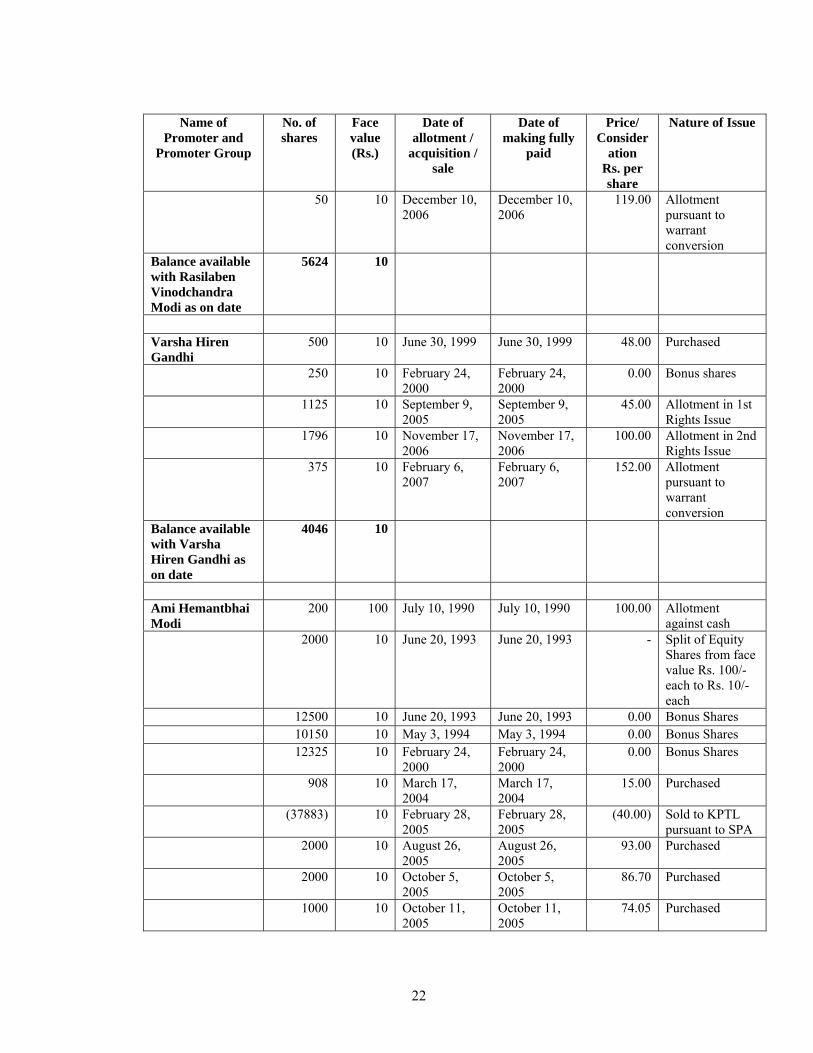

5. For details of transactions in Equity Shares of the Company by the Promoter and Promoter Group

in the last six months preceding the date of this Letter of Offer please refer section “Capital Structure” beginning on page 13 of this Letter of Offer.

xxii

6. For details of loans and advances made by the Company to companies in which the Directors are

interested please refer “Financial Statements” beginning on page 100 of this Letter of Offer.

7. For details of interests of Company’s Directors and key managerial personnel, please see the section “Management” beginning on page 68 of this Letter of Offer. For details of interests of the Promoters see the section “Promoters” beginning on page 95 of this Letter of Offer.

8. See section “Terms of the Issue” for details of Basis of Allotment begining on page 356 of this

Letter of Offer.

9. The Lead Manager and the Company are obliged to keep this Letter of Offer updated and inform the public of any material change/development until the listing and trading of Equity Shares offered under the Issue commences.

10. All information shall be made available by the Lead Manager and the Company to the public and

investors at large and no selective or additional information would be available only to a section of the investors in any manner whatsoever.

1

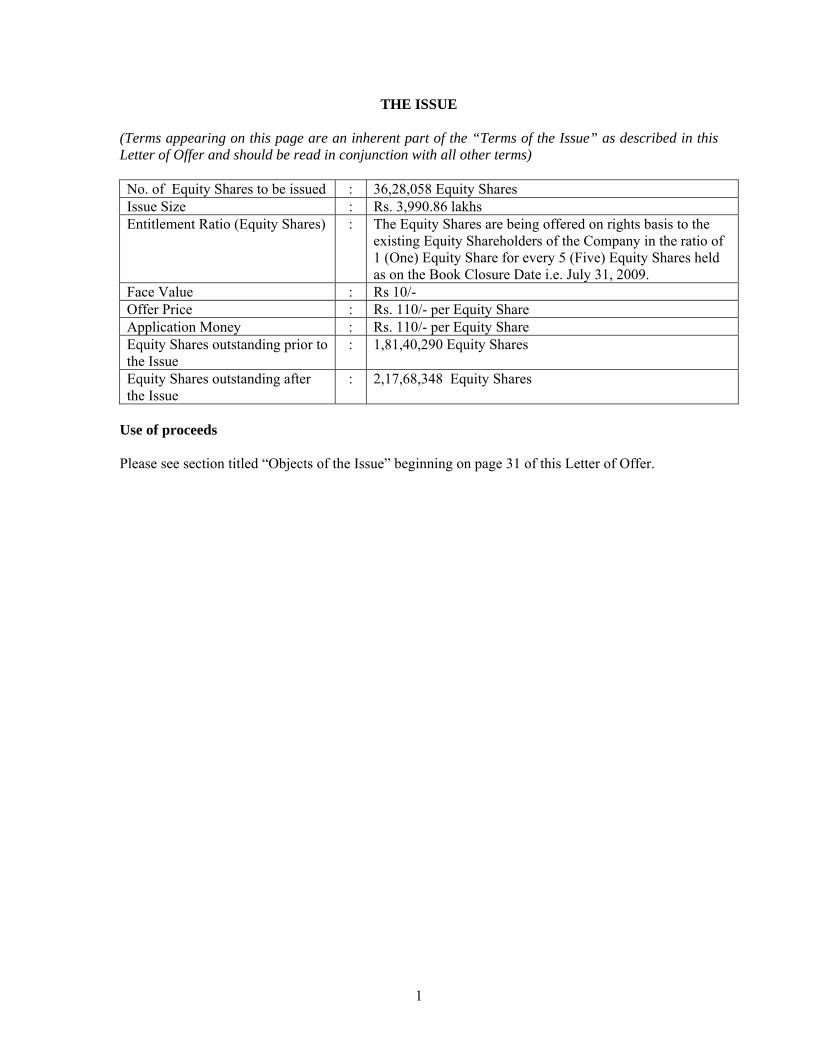

THE ISSUE

(Terms appearing on this page are an inherent part of the “Terms of the Issue” as described in this Letter of Offer and should be read in conjunction with all other terms) No. of Equity Shares to be issued : 36,28,058 Equity Shares Issue Size : Rs. 3,990.86 lakhs Entitlement Ratio (Equity Shares) : The Equity Shares are being offered on rights basis to the

existing Equity Shareholders of the Company in the ratio of 1 (One) Equity Share for every 5 (Five) Equity Shares held as on the Book Closure Date i.e. July 31, 2009.

Face Value : Rs 10/- Offer Price : Rs. 110/- per Equity Share Application Money : Rs. 110/- per Equity Share Equity Shares outstanding prior to the Issue

: 1,81,40,290 Equity Shares

Equity Shares outstanding after the Issue

: 2,17,68,348 Equity Shares

Use of proceeds Please see section titled “Objects of the Issue” beginning on page 31 of this Letter of Offer.

2

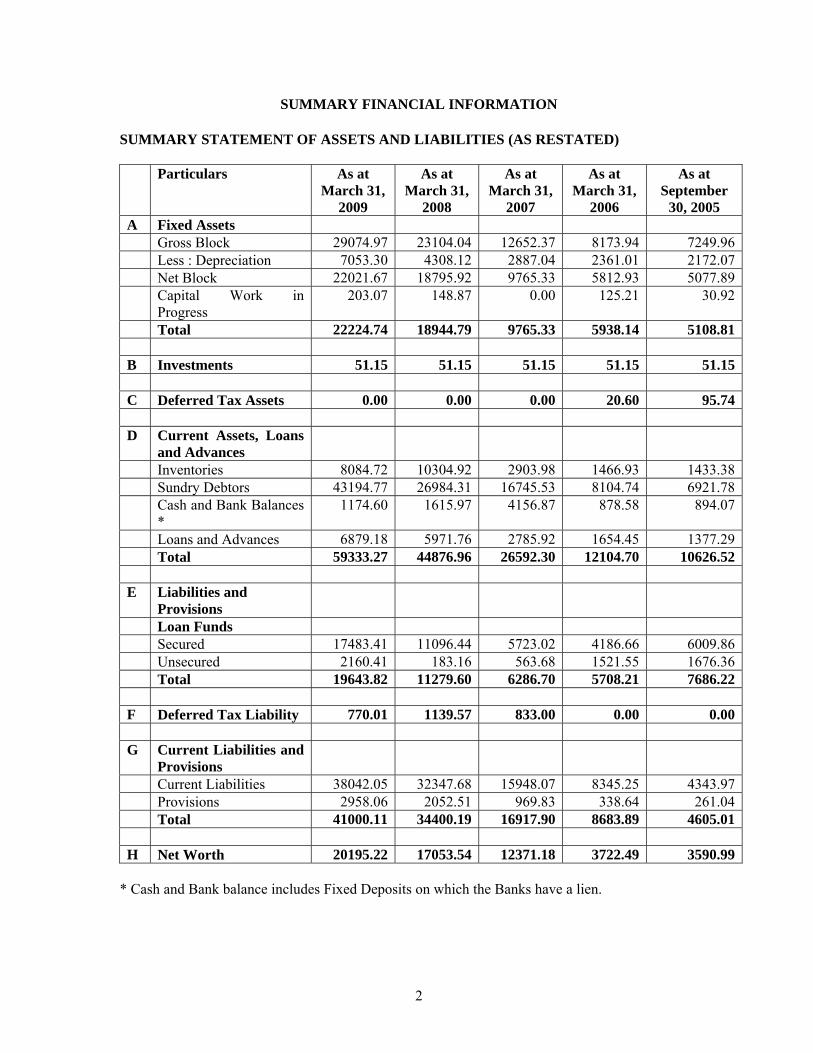

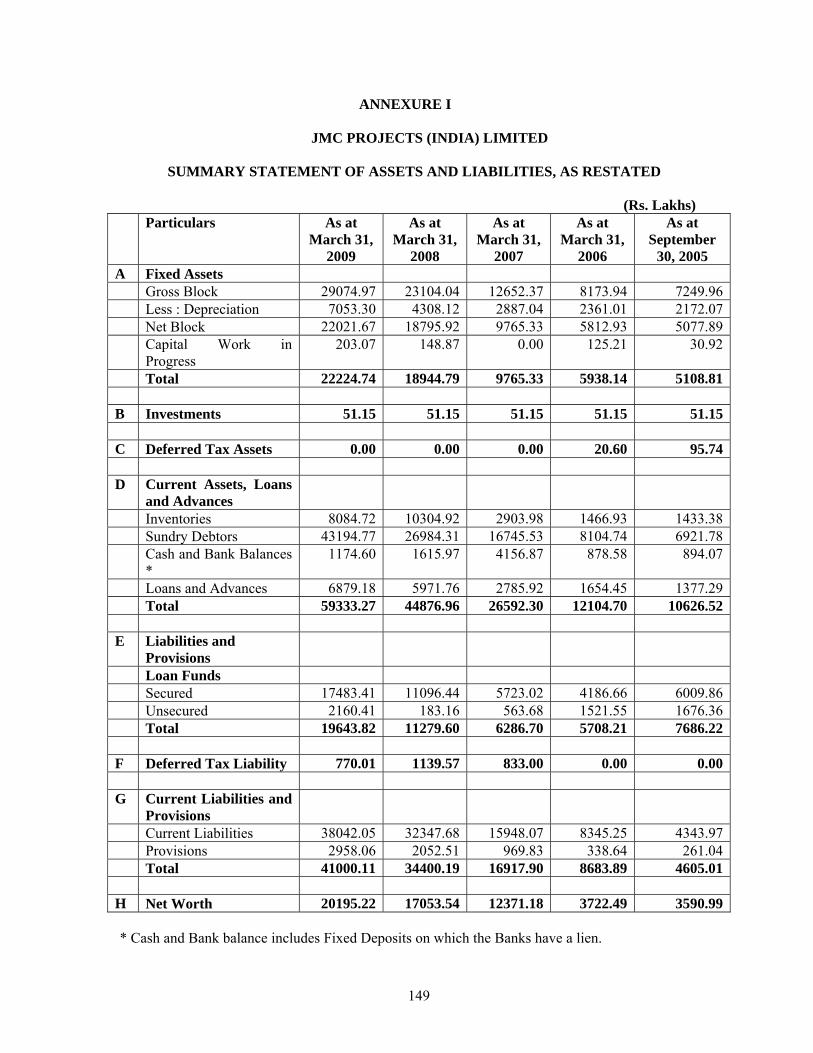

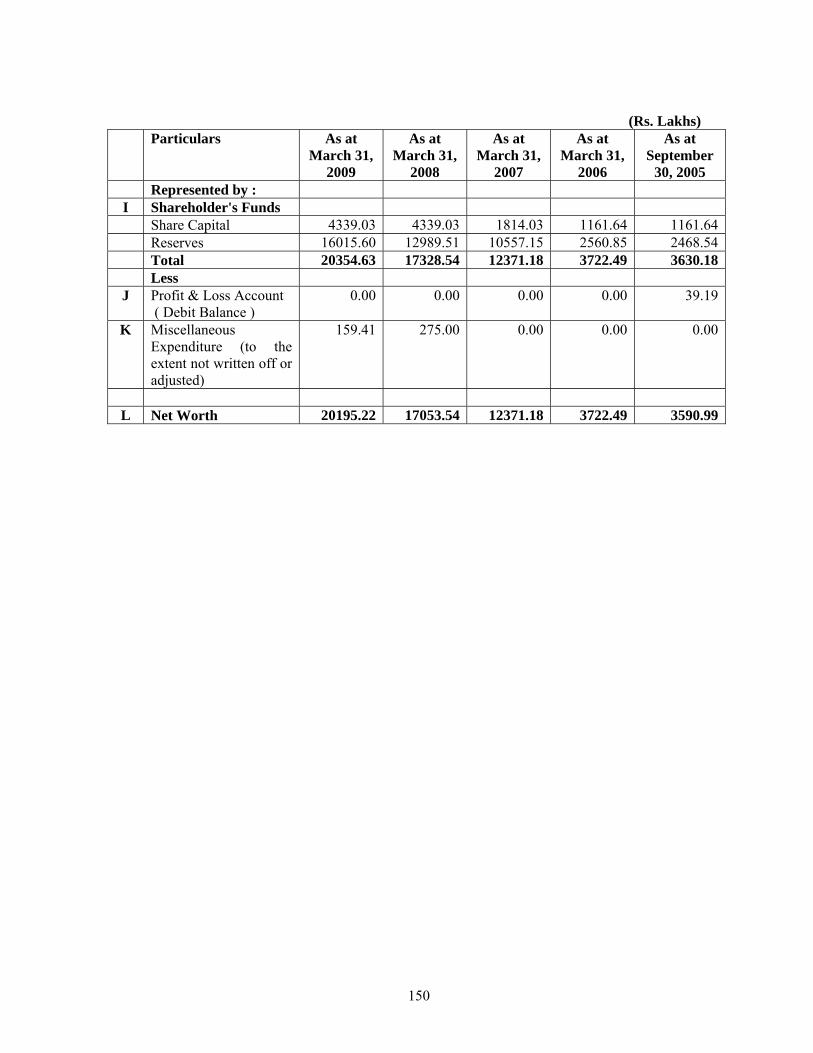

SUMMARY FINANCIAL INFORMATION SUMMARY STATEMENT OF ASSETS AND LIABILITIES (AS RESTATED)

Particulars As at

March 31, 2009

As at March 31,

2008

As at March 31,

2007

As at March 31,

2006

As at September

30, 2005 A Fixed Assets Gross Block 29074.97 23104.04 12652.37 8173.94 7249.96 Less : Depreciation 7053.30 4308.12 2887.04 2361.01 2172.07 Net Block 22021.67 18795.92 9765.33 5812.93 5077.89 Capital Work in

Progress 203.07 148.87 0.00 125.21 30.92

Total 22224.74 18944.79 9765.33 5938.14 5108.81 B Investments 51.15 51.15 51.15 51.15 51.15 C Deferred Tax Assets 0.00 0.00 0.00 20.60 95.74 D Current Assets, Loans

and Advances

Inventories 8084.72 10304.92 2903.98 1466.93 1433.38 Sundry Debtors 43194.77 26984.31 16745.53 8104.74 6921.78 Cash and Bank Balances

* 1174.60 1615.97 4156.87 878.58 894.07

Loans and Advances 6879.18 5971.76 2785.92 1654.45 1377.29 Total 59333.27 44876.96 26592.30 12104.70 10626.52 E Liabilities and

Provisions

Loan Funds Secured 17483.41 11096.44 5723.02 4186.66 6009.86 Unsecured 2160.41 183.16 563.68 1521.55 1676.36 Total 19643.82 11279.60 6286.70 5708.21 7686.22 F Deferred Tax Liability 770.01 1139.57 833.00 0.00 0.00 G Current Liabilities and

Provisions

Current Liabilities 38042.05 32347.68 15948.07 8345.25 4343.97 Provisions 2958.06 2052.51 969.83 338.64 261.04 Total 41000.11 34400.19 16917.90 8683.89 4605.01 H Net Worth 20195.22 17053.54 12371.18 3722.49 3590.99

* Cash and Bank balance includes Fixed Deposits on which the Banks have a lien.

3

(Rs. Lakhs)

Particulars As at March 31,

2009

As at March 31,

2008

As at March 31,

2007

As at March 31,

2006

As at September

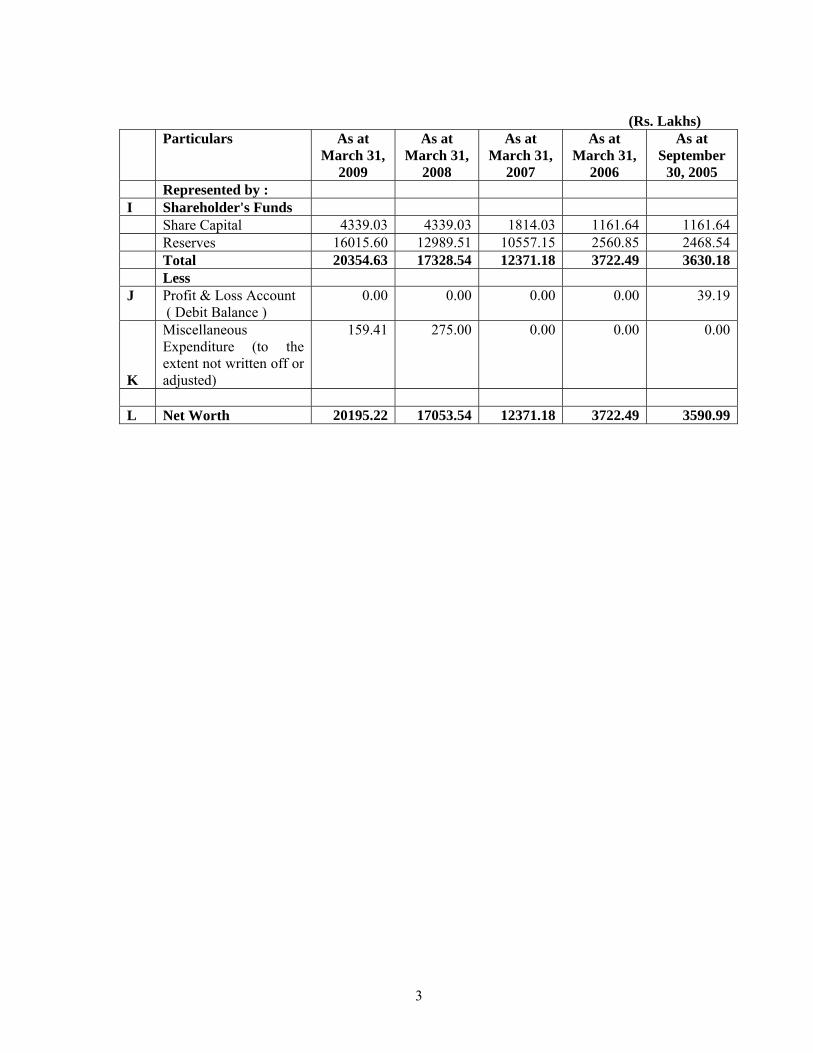

30, 2005 Represented by : I Shareholder's Funds Share Capital 4339.03 4339.03 1814.03 1161.64 1161.64 Reserves 16015.60 12989.51 10557.15 2560.85 2468.54 Total 20354.63 17328.54 12371.18 3722.49 3630.18 Less J Profit & Loss Account

( Debit Balance ) 0.00 0.00 0.00 0.00 39.19

K

Miscellaneous Expenditure (to the extent not written off or adjusted)

159.41 275.00 0.00 0.00 0.00

L Net Worth 20195.22 17053.54 12371.18 3722.49 3590.99

4

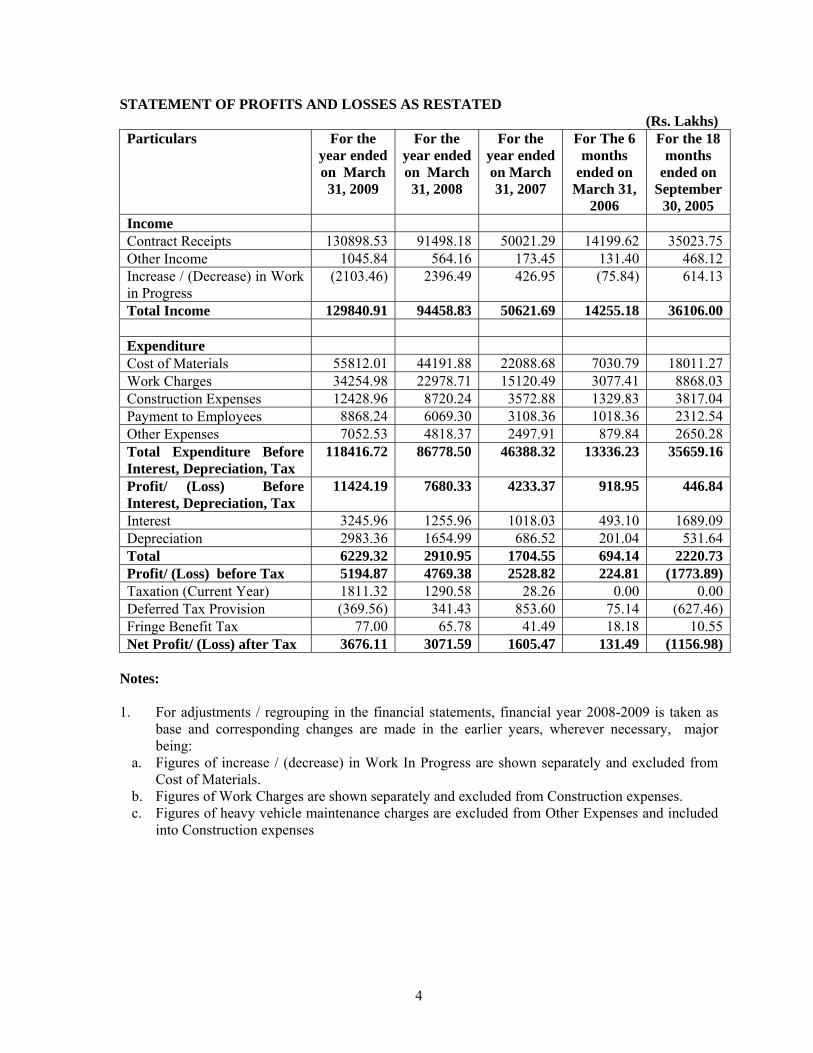

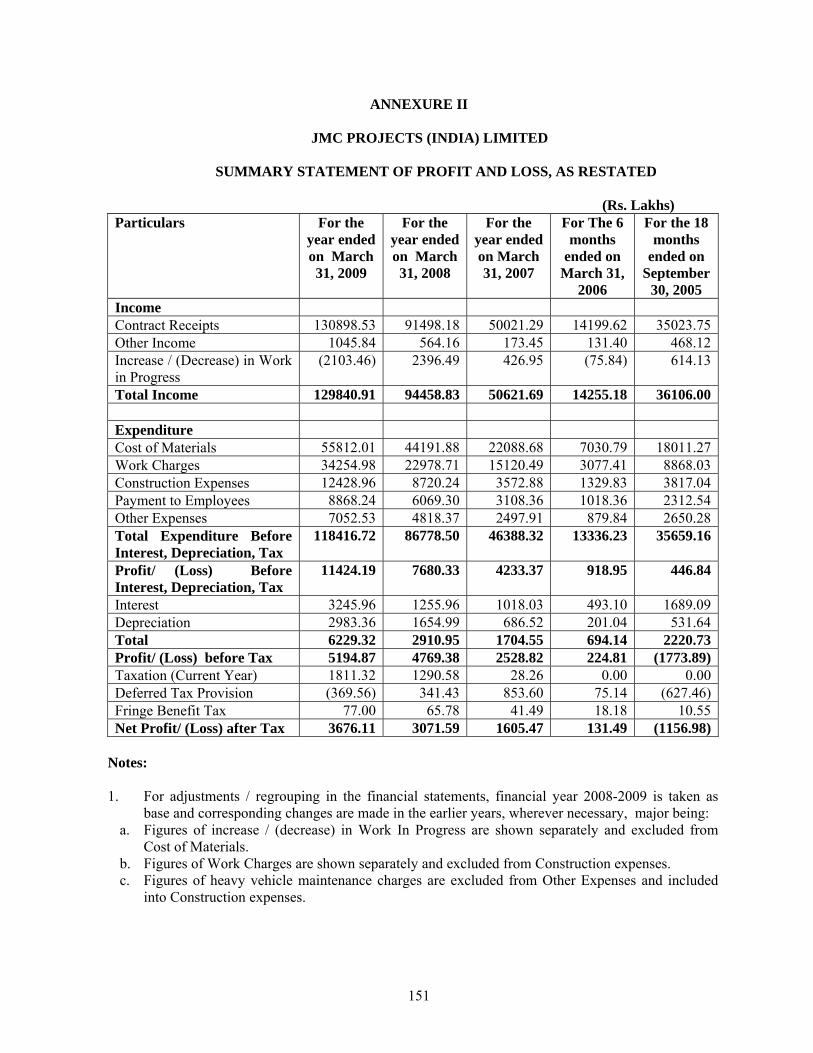

STATEMENT OF PROFITS AND LOSSES AS RESTATED (Rs. Lakhs)

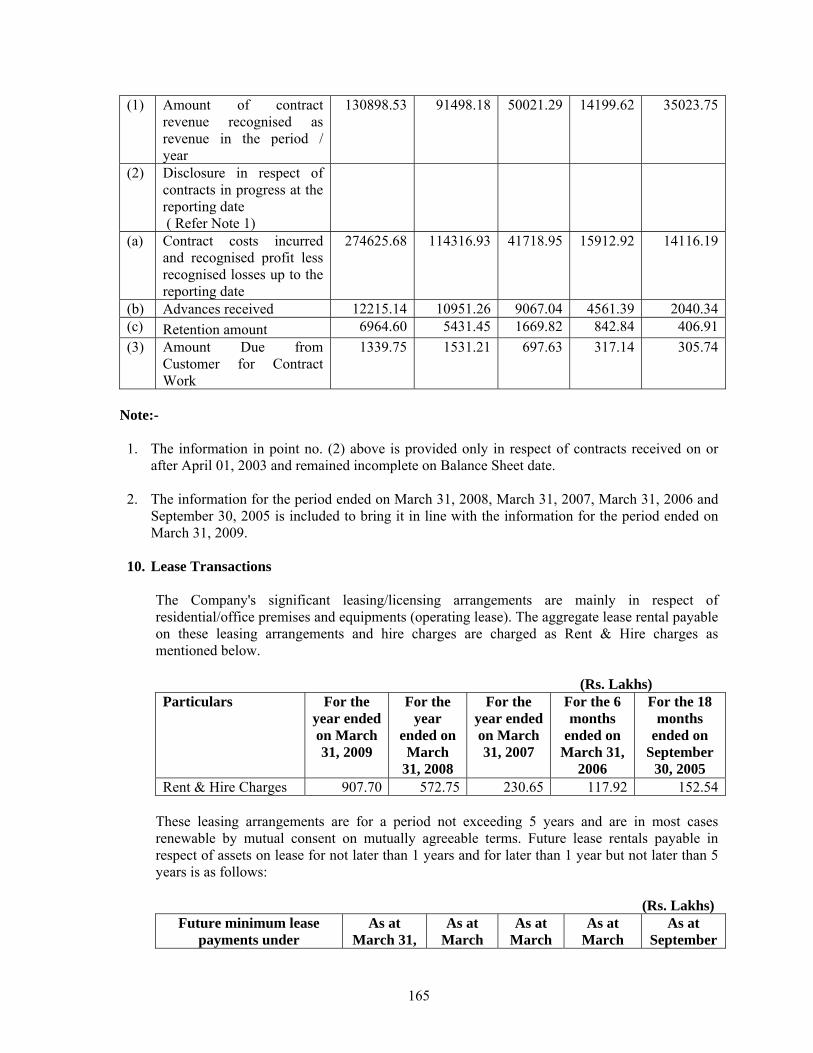

Particulars For the year ended on March 31, 2009

For the year ended on March 31, 2008

For the year ended on March 31, 2007

For The 6 months

ended on March 31,

2006

For the 18 months

ended on September

30, 2005 Income Contract Receipts 130898.53 91498.18 50021.29 14199.62 35023.75 Other Income 1045.84 564.16 173.45 131.40 468.12 Increase / (Decrease) in Work in Progress

(2103.46) 2396.49 426.95 (75.84) 614.13

Total Income 129840.91 94458.83 50621.69 14255.18 36106.00 Expenditure Cost of Materials 55812.01 44191.88 22088.68 7030.79 18011.27 Work Charges 34254.98 22978.71 15120.49 3077.41 8868.03 Construction Expenses 12428.96 8720.24 3572.88 1329.83 3817.04 Payment to Employees 8868.24 6069.30 3108.36 1018.36 2312.54 Other Expenses 7052.53 4818.37 2497.91 879.84 2650.28 Total Expenditure Before Interest, Depreciation, Tax

118416.72 86778.50 46388.32 13336.23 35659.16

Profit/ (Loss) Before Interest, Depreciation, Tax

11424.19 7680.33 4233.37 918.95 446.84

Interest 3245.96 1255.96 1018.03 493.10 1689.09 Depreciation 2983.36 1654.99 686.52 201.04 531.64 Total 6229.32 2910.95 1704.55 694.14 2220.73 Profit/ (Loss) before Tax 5194.87 4769.38 2528.82 224.81 (1773.89)Taxation (Current Year) 1811.32 1290.58 28.26 0.00 0.00Deferred Tax Provision (369.56) 341.43 853.60 75.14 (627.46)Fringe Benefit Tax 77.00 65.78 41.49 18.18 10.55 Net Profit/ (Loss) after Tax 3676.11 3071.59 1605.47 131.49 (1156.98)

Notes:

1. For adjustments / regrouping in the financial statements, financial year 2008-2009 is taken as

base and corresponding changes are made in the earlier years, wherever necessary, major being:

a. Figures of increase / (decrease) in Work In Progress are shown separately and excluded from Cost of Materials.

b. Figures of Work Charges are shown separately and excluded from Construction expenses. c. Figures of heavy vehicle maintenance charges are excluded from Other Expenses and included

into Construction expenses

5

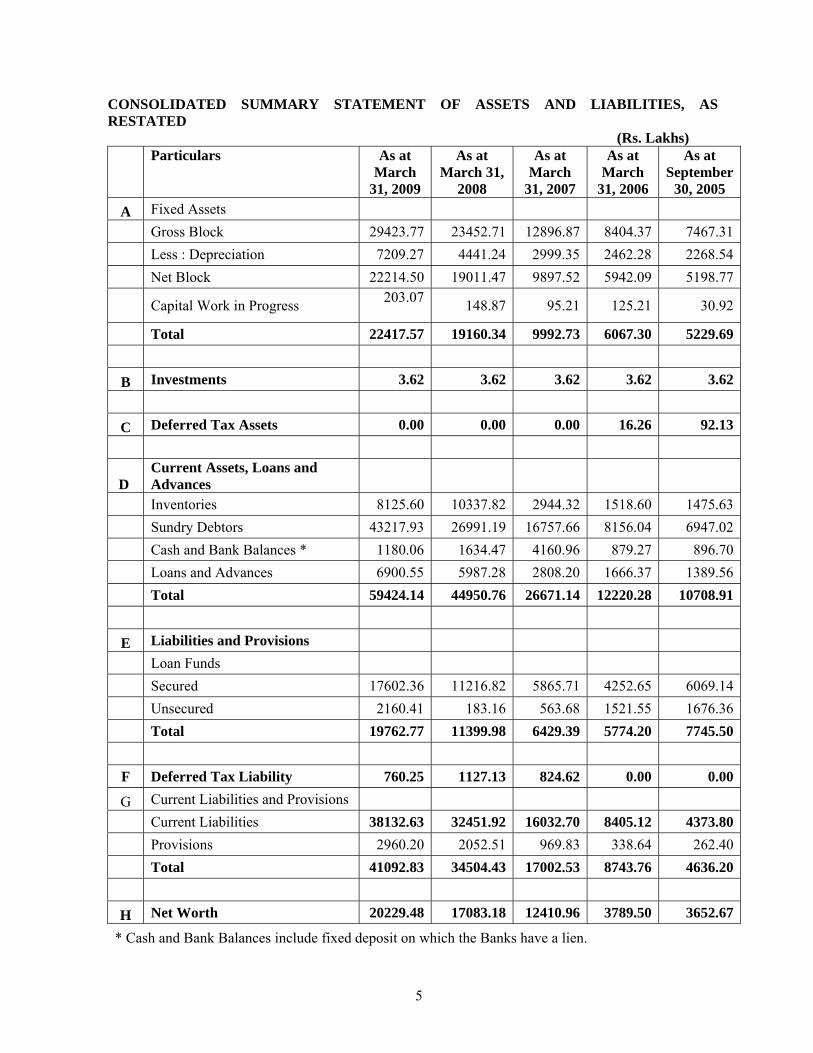

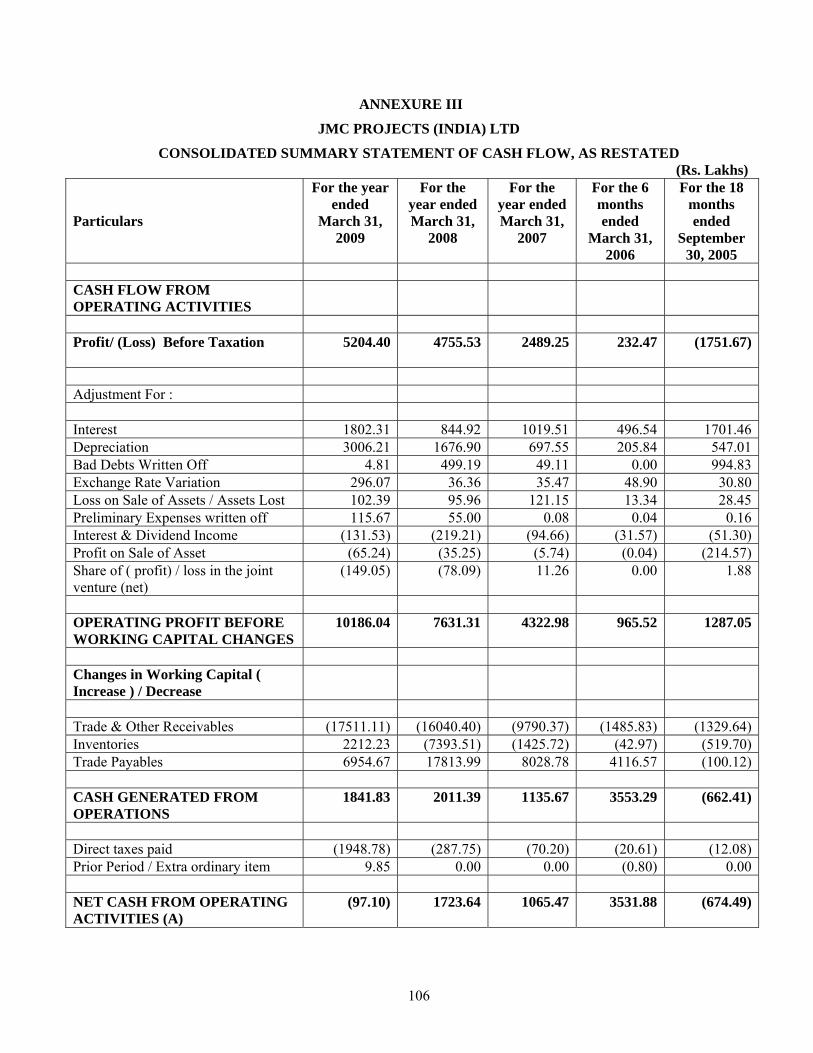

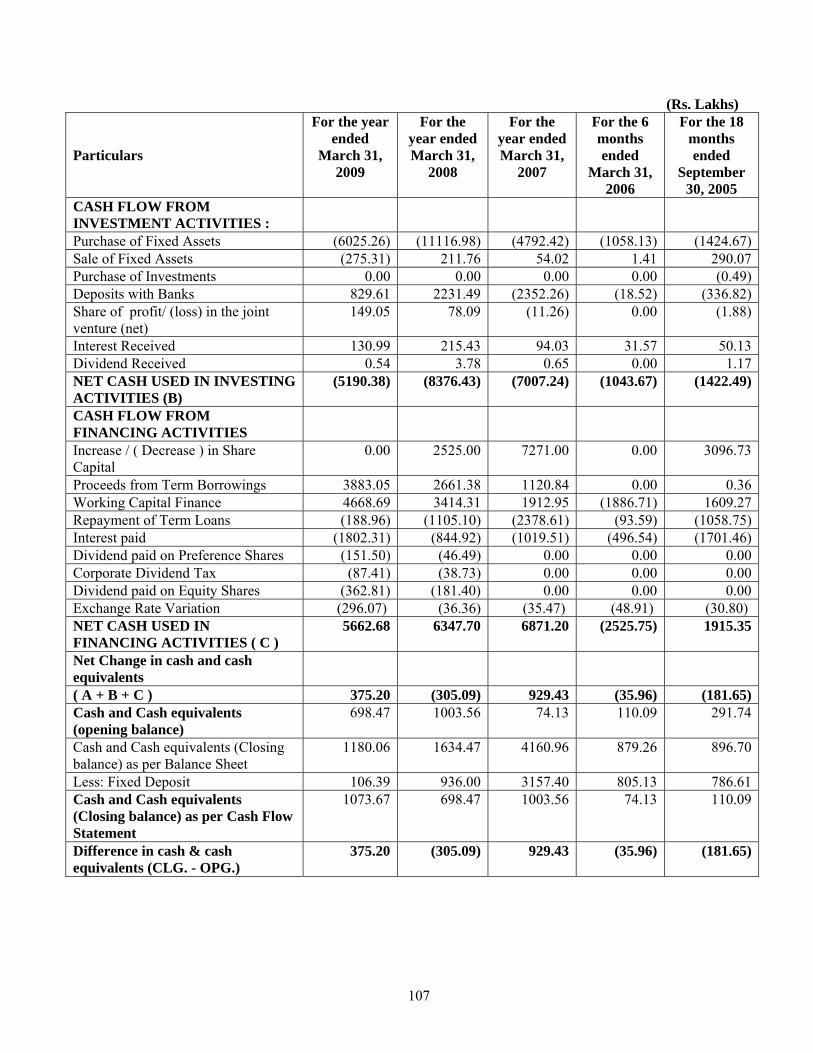

CONSOLIDATED SUMMARY STATEMENT OF ASSETS AND LIABILITIES, AS RESTATED

(Rs. Lakhs)

Particulars As at March

31, 2009

As at March 31,

2008

As at March

31, 2007

As at March

31, 2006

As at September

30, 2005 A Fixed Assets Gross Block 29423.77 23452.71 12896.87 8404.37 7467.31

Less : Depreciation 7209.27 4441.24 2999.35 2462.28 2268.54

Net Block 22214.50 19011.47 9897.52 5942.09 5198.77

Capital Work in Progress 203.07 148.87 95.21 125.21 30.92

Total 22417.57 19160.34 9992.73 6067.30 5229.69

B Investments 3.62 3.62 3.62 3.62 3.62

C Deferred Tax Assets 0.00 0.00 0.00 16.26 92.13

D Current Assets, Loans and Advances

Inventories 8125.60 10337.82 2944.32 1518.60 1475.63

Sundry Debtors 43217.93 26991.19 16757.66 8156.04 6947.02

Cash and Bank Balances * 1180.06 1634.47 4160.96 879.27 896.70

Loans and Advances 6900.55 5987.28 2808.20 1666.37 1389.56

Total 59424.14 44950.76 26671.14 12220.28 10708.91

E Liabilities and Provisions

Loan Funds

Secured 17602.36 11216.82 5865.71 4252.65 6069.14

Unsecured 2160.41 183.16 563.68 1521.55 1676.36

Total 19762.77 11399.98 6429.39 5774.20 7745.50

F Deferred Tax Liability 760.25 1127.13 824.62 0.00 0.00

G Current Liabilities and Provisions

Current Liabilities 38132.63 32451.92 16032.70 8405.12 4373.80

Provisions 2960.20 2052.51 969.83 338.64 262.40

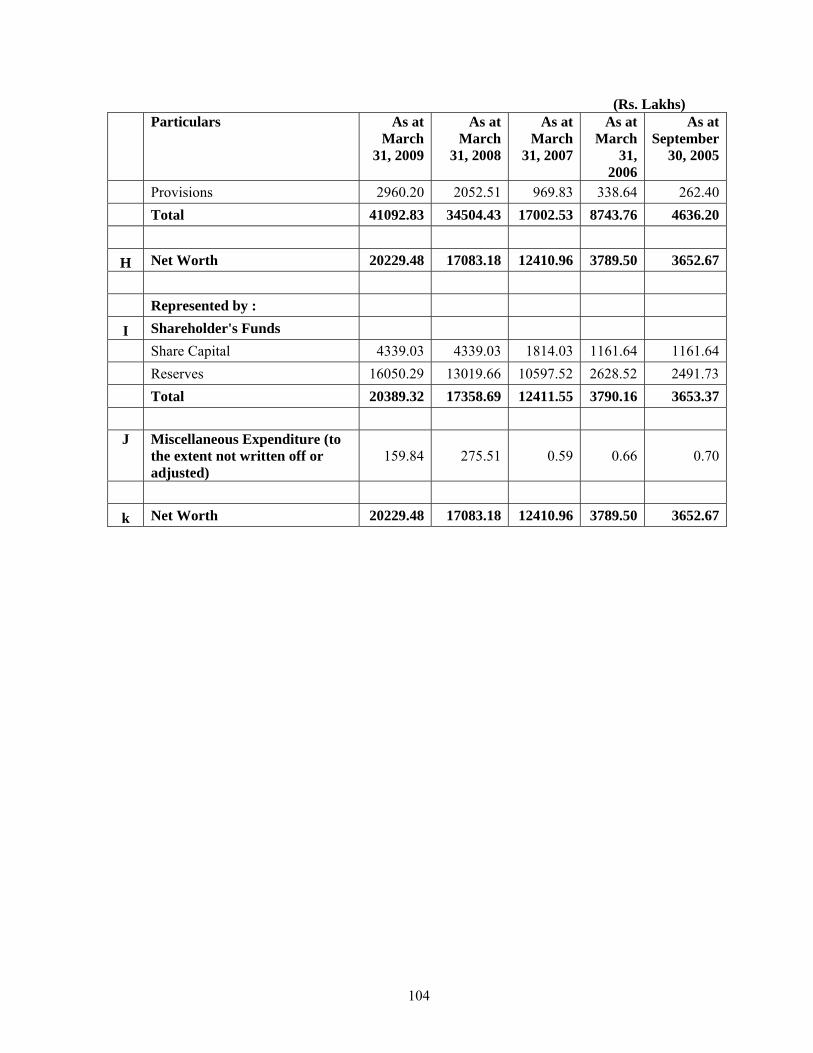

Total 41092.83 34504.43 17002.53 8743.76 4636.20

H Net Worth 20229.48 17083.18 12410.96 3789.50 3652.67

* Cash and Bank Balances include fixed deposit on which the Banks have a lien.

6

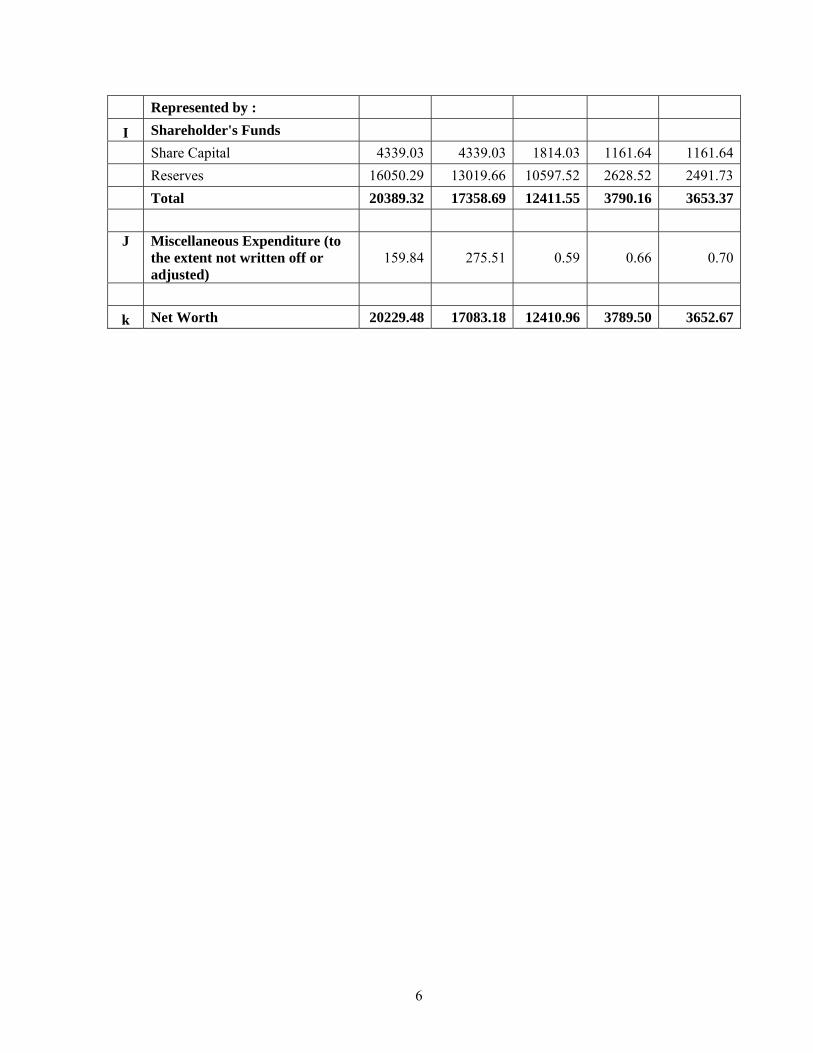

Represented by :

I Shareholder's Funds

Share Capital 4339.03 4339.03 1814.03 1161.64 1161.64

Reserves 16050.29 13019.66 10597.52 2628.52 2491.73

Total 20389.32 17358.69 12411.55 3790.16 3653.37

J Miscellaneous Expenditure (to

the extent not written off or adjusted)

159.84 275.51 0.59 0.66 0.70

k Net Worth 20229.48 17083.18 12410.96 3789.50 3652.67

7

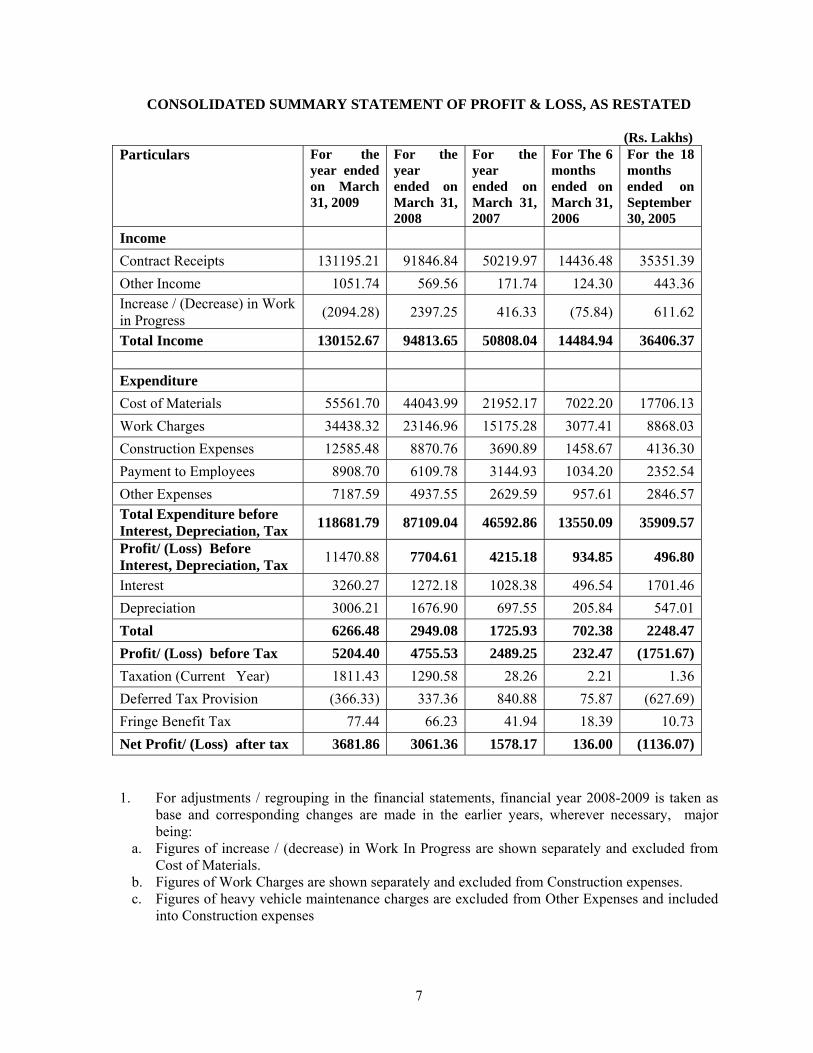

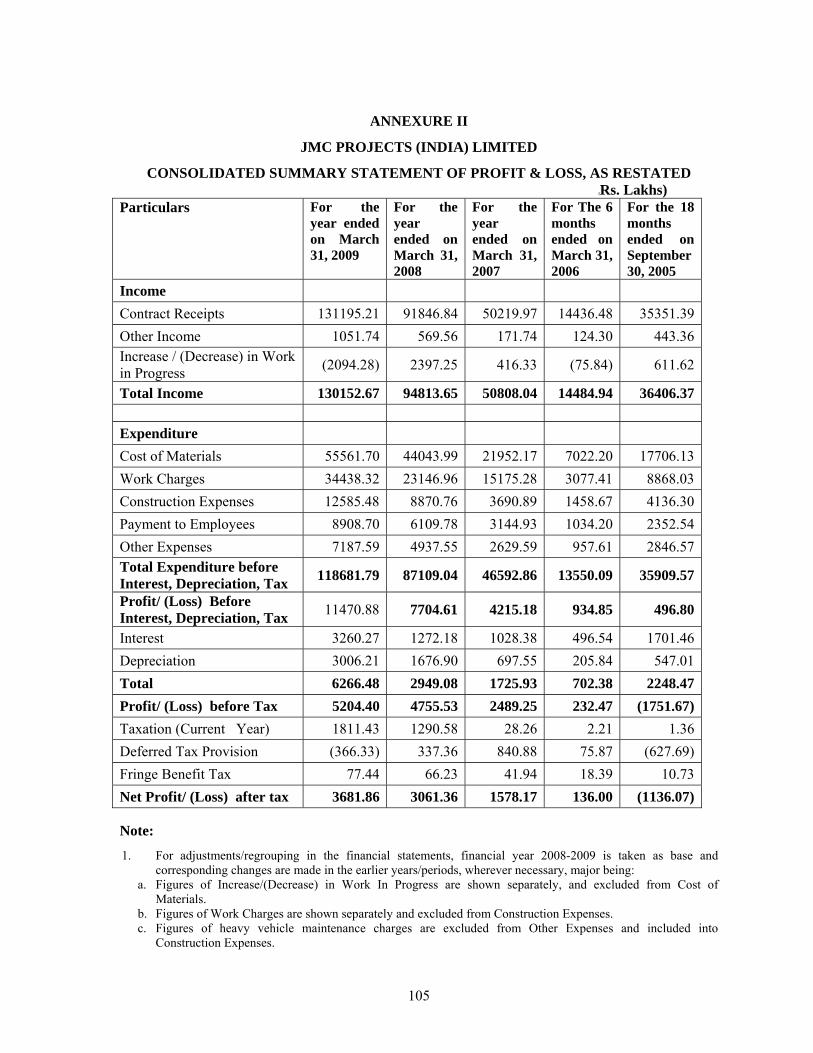

CONSOLIDATED SUMMARY STATEMENT OF PROFIT & LOSS, AS RESTATED

(Rs. Lakhs) Particulars For the

year ended on March 31, 2009

For the year ended on March 31, 2008

For the year ended on March 31, 2007

For The 6 months ended on March 31, 2006

For the 18 months ended on September 30, 2005

Income Contract Receipts 131195.21 91846.84 50219.97 14436.48 35351.39Other Income 1051.74 569.56 171.74 124.30 443.36Increase / (Decrease) in Work in Progress (2094.28) 2397.25 416.33 (75.84) 611.62

Total Income 130152.67 94813.65 50808.04 14484.94 36406.37 Expenditure Cost of Materials 55561.70 44043.99 21952.17 7022.20 17706.13Work Charges 34438.32 23146.96 15175.28 3077.41 8868.03Construction Expenses 12585.48 8870.76 3690.89 1458.67 4136.30Payment to Employees 8908.70 6109.78 3144.93 1034.20 2352.54Other Expenses 7187.59 4937.55 2629.59 957.61 2846.57Total Expenditure before Interest, Depreciation, Tax 118681.79 87109.04 46592.86 13550.09 35909.57

Profit/ (Loss) Before Interest, Depreciation, Tax 11470.88 7704.61 4215.18 934.85 496.80

Interest 3260.27 1272.18 1028.38 496.54 1701.46Depreciation 3006.21 1676.90 697.55 205.84 547.01Total 6266.48 2949.08 1725.93 702.38 2248.47Profit/ (Loss) before Tax 5204.40 4755.53 2489.25 232.47 (1751.67)Taxation (Current Year) 1811.43 1290.58 28.26 2.21 1.36Deferred Tax Provision (366.33) 337.36 840.88 75.87 (627.69)Fringe Benefit Tax 77.44 66.23 41.94 18.39 10.73Net Profit/ (Loss) after tax 3681.86 3061.36 1578.17 136.00 (1136.07)

1. For adjustments / regrouping in the financial statements, financial year 2008-2009 is taken as base and corresponding changes are made in the earlier years, wherever necessary, major being:

a. Figures of increase / (decrease) in Work In Progress are shown separately and excluded from Cost of Materials.

b. Figures of Work Charges are shown separately and excluded from Construction expenses. c. Figures of heavy vehicle maintenance charges are excluded from Other Expenses and included

into Construction expenses

8

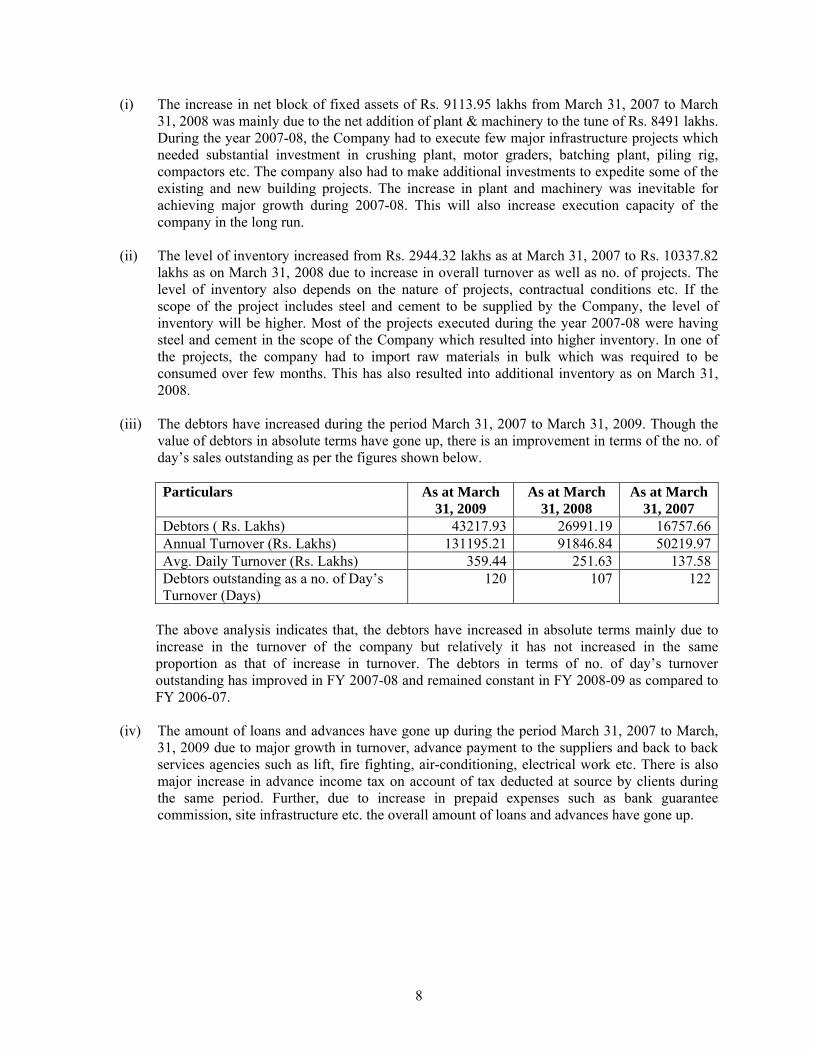

(i) The increase in net block of fixed assets of Rs. 9113.95 lakhs from March 31, 2007 to March 31, 2008 was mainly due to the net addition of plant & machinery to the tune of Rs. 8491 lakhs. During the year 2007-08, the Company had to execute few major infrastructure projects which needed substantial investment in crushing plant, motor graders, batching plant, piling rig, compactors etc. The company also had to make additional investments to expedite some of the existing and new building projects. The increase in plant and machinery was inevitable for achieving major growth during 2007-08. This will also increase execution capacity of the company in the long run.

(ii) The level of inventory increased from Rs. 2944.32 lakhs as at March 31, 2007 to Rs. 10337.82

lakhs as on March 31, 2008 due to increase in overall turnover as well as no. of projects. The level of inventory also depends on the nature of projects, contractual conditions etc. If the scope of the project includes steel and cement to be supplied by the Company, the level of inventory will be higher. Most of the projects executed during the year 2007-08 were having steel and cement in the scope of the Company which resulted into higher inventory. In one of the projects, the company had to import raw materials in bulk which was required to be consumed over few months. This has also resulted into additional inventory as on March 31, 2008.

(iii) The debtors have increased during the period March 31, 2007 to March 31, 2009. Though the

value of debtors in absolute terms have gone up, there is an improvement in terms of the no. of day’s sales outstanding as per the figures shown below.

Particulars As at March

31, 2009 As at March

31, 2008 As at March

31, 2007 Debtors ( Rs. Lakhs) 43217.93 26991.19 16757.66Annual Turnover (Rs. Lakhs) 131195.21 91846.84 50219.97Avg. Daily Turnover (Rs. Lakhs) 359.44 251.63 137.58Debtors outstanding as a no. of Day’s Turnover (Days)

120 107 122

The above analysis indicates that, the debtors have increased in absolute terms mainly due to increase in the turnover of the company but relatively it has not increased in the same proportion as that of increase in turnover. The debtors in terms of no. of day’s turnover outstanding has improved in FY 2007-08 and remained constant in FY 2008-09 as compared to FY 2006-07.

(iv) The amount of loans and advances have gone up during the period March 31, 2007 to March,

31, 2009 due to major growth in turnover, advance payment to the suppliers and back to back services agencies such as lift, fire fighting, air-conditioning, electrical work etc. There is also major increase in advance income tax on account of tax deducted at source by clients during the same period. Further, due to increase in prepaid expenses such as bank guarantee commission, site infrastructure etc. the overall amount of loans and advances have gone up.

9

GENERAL INFORMATION

Dear Shareholder(s) Pursuant to the resolution passed by the Board of Directors at their meeting held on January 29, 2009, it has been decided to make the following offer to the Equity Shareholders of the Company: ISSUE OF 36,28,058 EQUITY SHARES OF Rs. 10/- EACH AT A PREMIUM OF Rs. 100/- PER EQUITY SHARE AGGREGATING TO RS. 3,990.86 LAKHS TO THE EQUITY SHAREHOLDERS ON RIGHTS BASIS IN THE RATIO OF 1 (ONE) EQUITY SHARE FOR EVERY 5 (FIVE) EQUITY SHARES HELD ON THE BOOK CLOSURE DATE i.e. JULY 31, 2009 (“ISSUE”). THE ISSUE PRICE IS 11 TIMES THE FACE VALUE OF THE EQUITY SHARE. Registered Office of the Company: JMC Projects (India) Limited CIN No.: L45200GJ1986PLC008717 Registered Office: A-104, Shapath-4, Opposite Karnavati Club, S. G. Road, Ahmedabad – 380 051, India. Tel: +91-79- 3001 1500 Fax: +91-79-3001 1600/1700 E-mail: [email protected] Website: www.jmcprojects.com Address of the Registrar of Companies, Gujarat, Dadra & Nagar Haveli: ROC Bhavan, Opp. Rupal Park Society, Near Ankur Bus Stand, Naranpura, Ahmedabad – 380 013. The Equity Shares of the Company are listed on BSE and NSE. Board of Directors Name of the Director Designation Mr. D. R. Mehta Chairman Mr. Hemant Modi Vice Chairman & Managing Director Mr.Suhas Joshi Managing Director Mr.Kamal Jain Director Mr.Mahendra G Punatar Director Mr.Ramesh Sheth Director Mr.Manish Mohnot Director

For more details regarding the Directors please refer to “Management” beginning on page 68 of this Letter of Offer. Company Secretary & Compliance Officer Mr. Ashish Shah A-104, Shapath –4 Opposite Karnavati Club, S.G. Road Ahmedabad – 380 051 Tel: +91-79- 3001 1500 Fax: +91-79-3001 1600/1700 Email: [email protected]

10

Investors may contact the Compliance Officer for any pre-Issue/post Issue related matter. Legal Advisors to the Company Singhi & Co. Advocates, Solicitor & Notary 7-8, Premchand House Annexe Ashram Road Ahmedabad – 380 009. Tel: +91-79-2658 8336 Fax: +91-79-2658 7536 Email: [email protected] Bankers of the Company Oriental Bank of Commerce “Neel Kamal”, Opp: Sales India Ashram Road Ahmedabad – 380 009. Tel: +91- 79-2754 2029 Fax: +91-79-2754 1113 Email: [email protected] The Karur Vysya Bank Limited Sakar VII, B Block, Ashram Road Ahmedabad – 380 009. Tel: +91-79-2754 6247 Fax: +91-79-2754 6087 Email: [email protected] State Bank of India “Paramsiddhi Complex” Opp: V S Hospital, Ellisbridge Ahmedabad – 380 006. Tel: +91-79-2658 5623 Fax: +91-79-2658 1512 Email: [email protected] Indian Bank Ahmedabad Main Branch Mission Road Bhadra, Ahmedabad - 380 001. Tel: +91-79-2550 6641/7087 Fax: +91-79-2550 6583 Email: [email protected] Punjab National Bank Shastri Park Branch Nehrunagar Circle Ahmedabad - 380 015.

11

Tel: +91-79-2630 5447 Fax: +91-79-2630 9353 Email: [email protected] Axis Bank “Trishul”, Opp. Samartheshwar Mahadev Temple Law Garden Road Ahmedabad 380 006 Tel: +91-79-6630 6102 Fax: +91-79-6630 6109 Email: [email protected] Lead Manager to the Issue

Collins Stewart Inga Private Limited A-404, Neelam Centre Hind Cycle Road, Worli Mumbai – 400 030. Tel: +91-22-2498 2937/19/54 Fax :+91-22-2498 2956 Email: [email protected] Website: www.csinga.com Contact Person: Mr. Ashwani Tandon / Ms. Deepa Mutha Bankers to the Issue IDBI Bank Ltd. IDBI Complex Opp. Muni. Staff Quarters Nr. Lal Bungalow, Off. C. G. Road Post Bag No. 22 Ahmedabad - 380 006. Tel: +91-79-2656 3911/4149/4994 Fax: +91-79-2640 0814 Email: [email protected] Website: www.idbi.com Contact Person: Mr. S. G. Nadkarni Registrar to the Issue Link Intime India Pvt. Ltd. C-13, Pannalal Silk Mills Compound LBS Marg, Bhandup (West) Mumbai - 400 078. Tel: +91-22-2596 0320 Fax: +91-22-2596 0329 Email: [email protected] Website: www.linkintime.co.in Contact Person: Mr. Praveen Kasare

12

Auditors of the Company Sudhir N Doshi & Co. Chartered Accountants 22, Empire Tower, 2nd Floor, Adjoining Associated Petrol Pump, C. G. Road, Ellisbridge, Ahmedabad – 380 006 Tel: +91-79-2644 9403 Email: [email protected] Kishan M Mehta & Co. Chartered Accountants 6, Premchand House Annexe Ashram Road Ahmedabad - 380 009 Tel: +91-79-2658 1570 Fax: +91-79-2658 5229 Email: [email protected] Registrar to the Company Pinnacle Shares Registry Pvt. Ltd. Near Asoka Mills Naroda Road Ahmedabad – 380 025 Tel: +91-79-2220 0338 Fax: +91-79-2220 2963 Email: [email protected] Credit Rating This being an issue of Equity Shares, no credit rating is required. Minimum Subscription Clause

If the Company does not receive application money for atleast 90% of the Issued amount the entire subscription will be refunded to the Applicants within 15 days from the date of closure of the Issue. If there is a delay in the refund of application money by more than eight days after the Company becomes liable to pay the amount (15 days after closure of the Issue), the Company will pay interest for the delayed period at prescribed rates in sub-sections (2) and (2A) of Section 73 of the Companies Act, 1956.

13

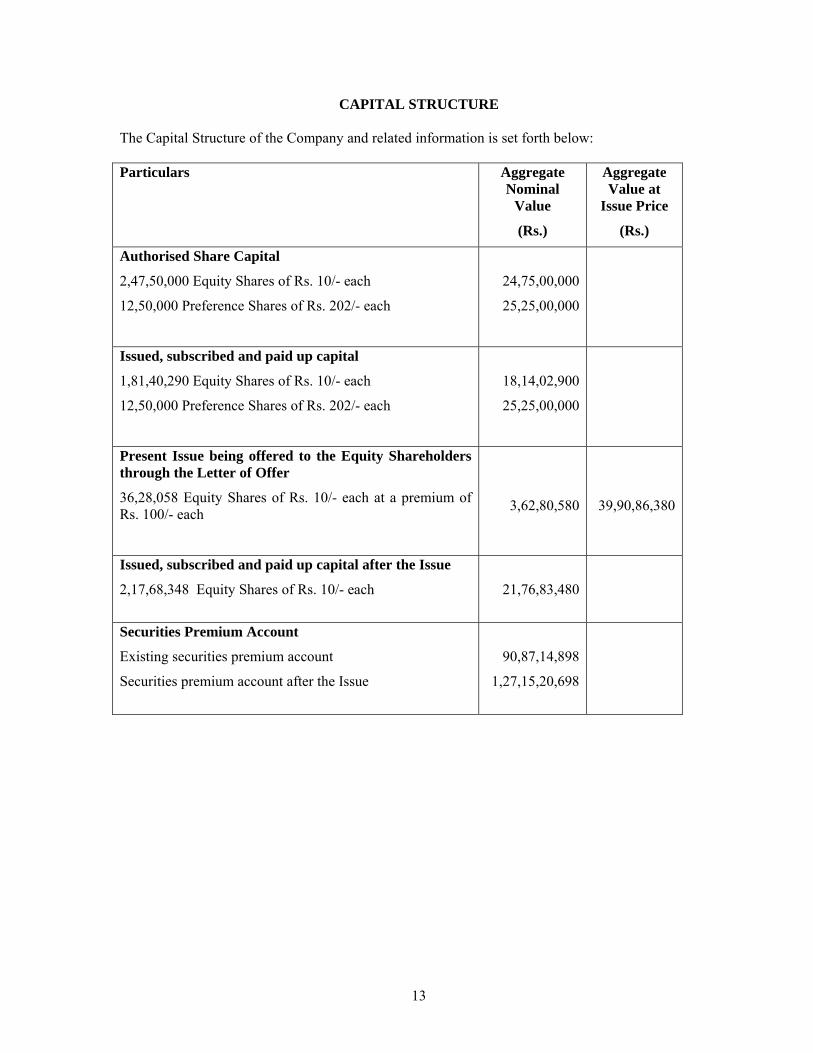

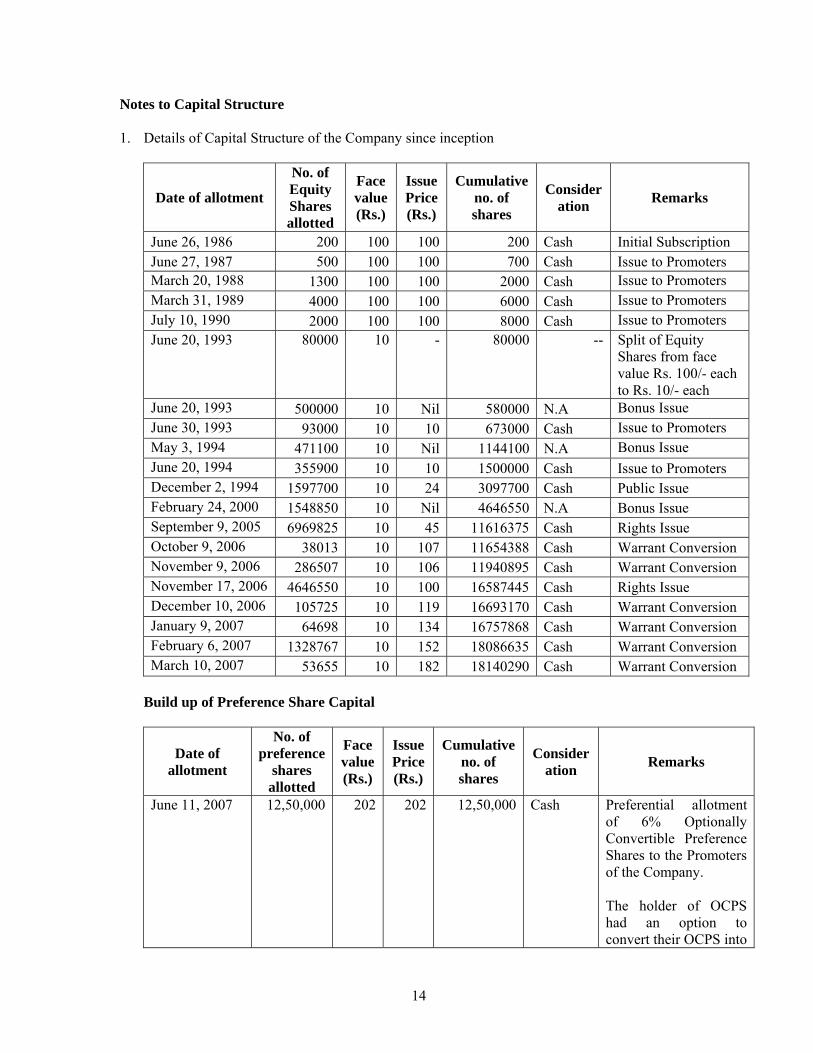

CAPITAL STRUCTURE

The Capital Structure of the Company and related information is set forth below: Particulars Aggregate

Nominal Value

(Rs.)

Aggregate Value at

Issue Price

(Rs.)

Authorised Share Capital

2,47,50,000 Equity Shares of Rs. 10/- each

12,50,000 Preference Shares of Rs. 202/- each

24,75,00,000

25,25,00,000

Issued, subscribed and paid up capital

1,81,40,290 Equity Shares of Rs. 10/- each

12,50,000 Preference Shares of Rs. 202/- each

18,14,02,900

25,25,00,000