JM Financial Capital Limited Annual Report 2019-20

119

Prudence Matters JM Financial Capital Limited Annual Report 2019-20

Transcript of JM Financial Capital Limited Annual Report 2019-20

Prudence Matters

JM Financial Capital LimitedAnnual Report 2019-20

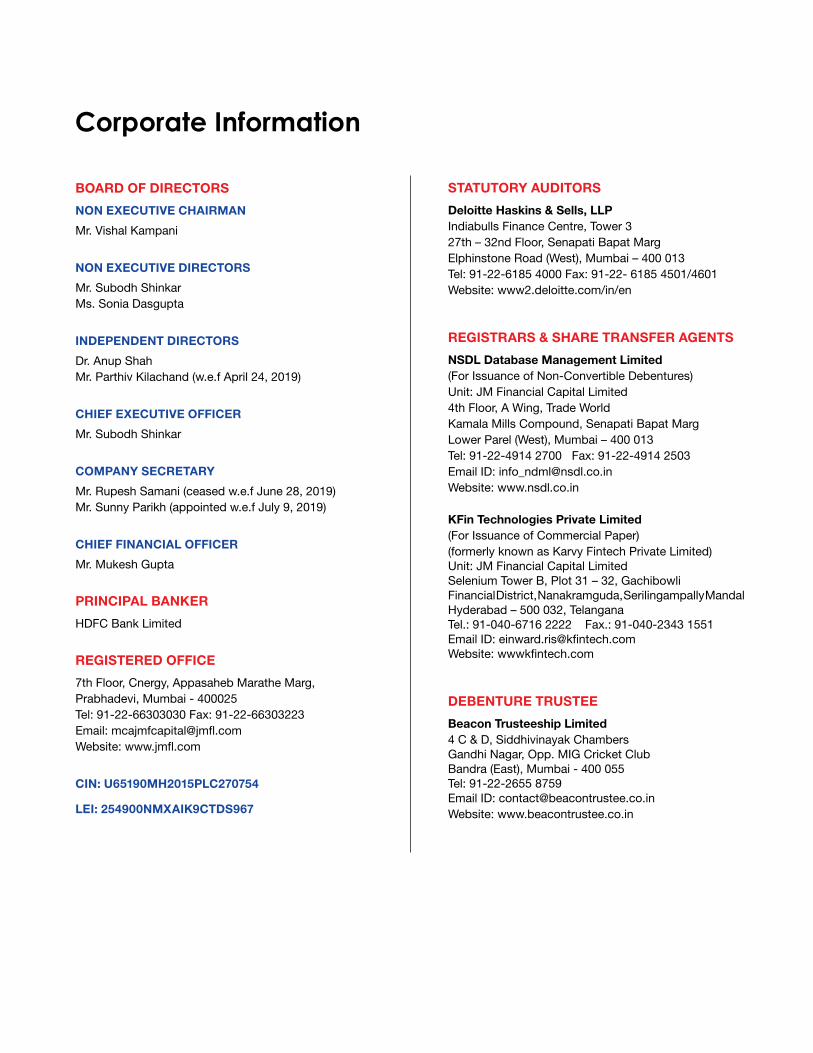

Corporate Information

BOARD OF DIRECTORS

NON EXECUTIVE CHAIRMAN

Mr. Vishal Kampani

NON EXECUTIVE DIRECTORS

Mr. Subodh ShinkarMs. Sonia Dasgupta

INDEPENDENT DIRECTORS

Dr. Anup Shah Mr. Parthiv Kilachand (w.e.f April 24, 2019)

CHIEF EXECUTIVE OFFICER

Mr. Subodh Shinkar

COMPANY SECRETARY

Mr. Rupesh Samani (ceased w.e.f June 28, 2019)Mr. Sunny Parikh (appointed w.e.f July 9, 2019)

CHIEF FINANCIAL OFFICER

Mr. Mukesh Gupta

PRINCIPAL BANKER

HDFC Bank Limited

REGISTERED OFFICE

7th Floor, Cnergy, Appasaheb Marathe Marg,Prabhadevi, Mumbai - 400025Tel: 91-22-66303030 Fax: 91-22-66303223Email: [email protected]: www.jmfl.com

CIN: U65190MH2015PLC270754

LEI: 254900NMXAIK9CTDS967

STATUTORY AUDITORS

Deloitte Haskins & Sells, LLP Indiabulls Finance Centre, Tower 327th – 32nd Floor, Senapati Bapat MargElphinstone Road (West), Mumbai – 400 013Tel: 91-22-6185 4000 Fax: 91-22- 6185 4501/4601Website: www2.deloitte.com/in/en

REGISTRARS & SHARE TRANSFER AGENTS

NSDL Database Management Limited(For Issuance of Non-Convertible Debentures)Unit: JM Financial Capital Limited4th Floor, A Wing, Trade WorldKamala Mills Compound, Senapati Bapat MargLower Parel (West), Mumbai – 400 013Tel: 91-22-4914 2700 Fax: 91-22-4914 2503Email ID: [email protected]: www.nsdl.co.in

KFin Technologies Private Limited(For Issuance of Commercial Paper)(formerly known as Karvy Fintech Private Limited)Unit: JM Financial Capital LimitedSelenium Tower B, Plot 31 – 32, GachibowliFinancial District, Nanakramguda, Serilingampally Mandal Hyderabad – 500 032, TelanganaTel.: 91-040-6716 2222 Fax.: 91-040-2343 1551Email ID: [email protected]: wwwkfintech.com

DEBENTURE TRUSTEE

Beacon Trusteeship Limited4 C & D, Siddhivinayak ChambersGandhi Nagar, Opp. MIG Cricket ClubBandra (East), Mumbai - 400 055Tel: 91-22-2655 8759 Email ID: [email protected]: www.beacontrustee.co.in

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

1Annual Report 2019-20

Notice

NOTICE IS HEREBY GIVEN THAT THE FIFTH ANNUAL GENERAL MEETING (“AGM”) OF THE MEMBERS OF JM FINANCIAL CAPITAL LIMITED (“THE COMPANY”) WILL BE HELD ON MONDAY, JULY 20, 2020 AT 11:30 A.M. THROUGH VIDEO CONFERENCING (“VC”)/OTHER AUDIO VISUAL MEANS (“OAVM”) TO TRANSACT THE FOLLOWING BUSINESS:

ORDINARY BUSINESS:

1. To receive, consider and adopt the Audited Financial Statements of the Company consisting of the Balance Sheet as at March 31, 2020, the Statement of Profit and Loss, Cash Flow Statement and Statement of Changes in Equity for the year ended on that date and the Explanatory Notes annexed to, and forming part of, any of the said documents together with the reports of the Board of Directors and the Auditors’ thereon; and

2. To appoint a Director in place of Mr. Vishal Kampani (DIN 00009079), who retires by rotation and being eligible, seeks re-appointment.

By Order of the Board

Place: Mumbai Sunny Parikh Date: June 24, 2020 Company Secretary

Registered Office:

7th Floor, Cnergy, Appasaheb Marathe Marg, Prabhadevi, Mumbai 400 025 (CIN: U65190MH2015PLC270754)Website: www.jmfl.comEmail: [email protected]

NOTES:

1. The Ministry of Corporate Affairs (“MCA”) has vide its Circular No. 14/2020 dated April 8, 2020, Circular No. 17/ 2020 dated April 13, 2020 and Circular No. 20/2020 dated May 5, 2020 (together referred to as “MCA Circulars”) has permitted to hold the Annual General Meeting (“AGM”) for the calendar year 2020 through Video Conferencing (“VC”) or Other Audio Visual Means (“OAVM”), without the presence of the Members at a common venue, due to outbreak of COVID-19 pandemic.

In due compliance with the above MCA Circulars, the Fifth AGM of the Company is being held through VC/OAVM.

2. Pursuant to the provisions of the Companies Act, 2013 (the “Act”), a member entitled to attend and vote at the AGM is entitled to appoint a proxy to attend and vote on his/her behalf and the proxy need not be a member of the Company. Since this AGM is being held through VC/OAVM, physical attendance of the members has been dispensed with. Accordingly, the facility for appointment of proxies by the Members will not be available for the AGM and hence the Proxy Form, Attendance Slip and Route Map are not annexed to this Notice.

3. In case if the member is a Body Corporate/Institution, then they are requested to send a scanned copy (PDF/JPG format) of its board or governing body resolution/authorisation, authorising its representative(s) to attend the AGM through VC/OAVM on its behalf and vote through show of hands. The said resolution/authorisation shall be emailed, through its registered email address to the Company Secretary at [email protected].

4. In compliance with the aforesaid MCA Circulars and other applicable provisions, if any, electronic copy of the Annual Report for the financial year 2019-20 is being sent to those Members whose email IDs are registered with the Company.

5. Members may also note that the Annual Report for the financial year 2019-20 including the Notice convening the Fifth AGM will also be available on the Company’s website viz., https://jmfl.com/who-we-are/group-companies.

6. Any document in connection with any of the items to be transacted in the Notice shall be made available for inspection and any member interested in obtaining a copy of the same may write to the Company Secretary at [email protected].

7. The relevant details as required clause 1.2.5 of Secretarial Standard - 2 on General Meetings issued by the Institute of Company Secretaries of India (SS-2), in respect of the persons seeking re-appointment as Director is given in annexure forming part of this Notice.

8. Members attending the AGM through VC/ OAVM shall be counted for the purpose of reckoning the quorum under Section 103 of the Act.

9. Since the AGM will be held through VC/OAVM, the Route Map is not annexed to the Notice.

Notice

2

Prudence Matters

JM Financial Capital Limited

INSTRUCTIONS FOR MEMBERS FOR ATTENDING THE AGM THROUGH VC/OAVM ARE AS UNDER:

1. Members will be able to attend the AGM through VC/OAVM through Microsoft Teams application. Members are requested to install/download the said application on their desktop/ laptop/ smartphone/ tablet through the below link:

https://www.microsoft.com/en-in/microsoft-365/microsoft-teams/download-app.

2. The invitation link for joining the meeting will be sent only to the Eligible Members who have registered their e-mail ID with the Company, the Depositories or with the depository participant.

3. Once the application is installed, members and eligible participants are requested to click on the link “Join Microsoft Teams Meeting” sent on their registered e-mail ID.

4. After you click on the link, it will take you to a page where you can choose to either ‘get the Teams application’ or ‘already have the Teams app? Launch it now’. Click on ‘already have the application’, the meeting window will then open automatically.

5. Please note that participants connecting from mobile devices or tablets, or through laptops via mobile hotspot may experience audio / video loss due to fluctuation in their respective networks. It is therefore recommended to use a good internet connection to mitigate any of the aforementioned glitches.

6. Facility of joining the AGM through VC / OAVM shall open 15 minutes before the time scheduled for the AGM. Further, an opportunity will be provided by Chairman to the shareholders attending the meeting through VC/OAVM whereby they may ask their questions.

7. Members who need assistance before or during the AGM, can contact Mr. Sunny Parikh, Company Secretary at + 91 7977990409 or email him at [email protected].

Notice (Contd.)

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

3Annual Report 2019-20

Notice

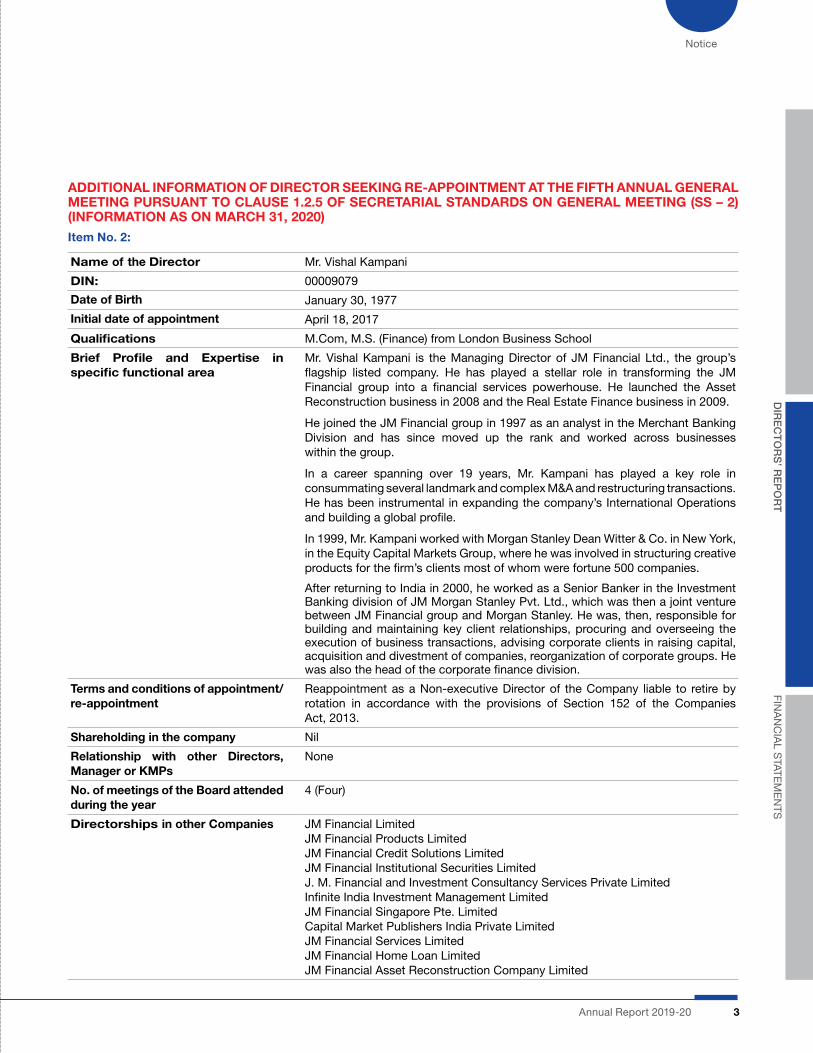

ADDITIONAL INFORMATION OF DIRECTOR SEEKING RE-APPOINTMENT AT THE FIFTH ANNUAL GENERAL MEETING PURSUANT TO CLAUSE 1.2.5 OF SECRETARIAL STANDARDS ON GENERAL MEETING (SS – 2) (INFORMATION AS ON MARCH 31, 2020)

Item No. 2:

Name of the Director Mr. Vishal Kampani

DIN: 00009079

Date of Birth January 30, 1977

Initial date of appointment April 18, 2017

Qualifications M.Com, M.S. (Finance) from London Business School

Brief Profile and Expertise in specific functional area

Mr. Vishal Kampani is the Managing Director of JM Financial Ltd., the group’s flagship listed company. He has played a stellar role in transforming the JM Financial group into a financial services powerhouse. He launched the Asset Reconstruction business in 2008 and the Real Estate Finance business in 2009.

He joined the JM Financial group in 1997 as an analyst in the Merchant Banking Division and has since moved up the rank and worked across businesses within the group.

In a career spanning over 19 years, Mr. Kampani has played a key role in consummating several landmark and complex M&A and restructuring transactions. He has been instrumental in expanding the company’s International Operations and building a global profile.

In 1999, Mr. Kampani worked with Morgan Stanley Dean Witter & Co. in New York, in the Equity Capital Markets Group, where he was involved in structuring creative products for the firm’s clients most of whom were fortune 500 companies.

After returning to India in 2000, he worked as a Senior Banker in the Investment Banking division of JM Morgan Stanley Pvt. Ltd., which was then a joint venture between JM Financial group and Morgan Stanley. He was, then, responsible for building and maintaining key client relationships, procuring and overseeing the execution of business transactions, advising corporate clients in raising capital, acquisition and divestment of companies, reorganization of corporate groups. He was also the head of the corporate finance division.

Terms and conditions of appointment/re-appointment

Reappointment as a Non-executive Director of the Company liable to retire by rotation in accordance with the provisions of Section 152 of the Companies Act, 2013.

Shareholding in the company Nil

Relationship with other Directors, Manager or KMPs

None

No. of meetings of the Board attended during the year

4 (Four)

Directorships in other Companies JM Financial Limited JM Financial Products Limited JM Financial Credit Solutions LimitedJM Financial Institutional Securities LimitedJ. M. Financial and Investment Consultancy Services Private LimitedInfinite India Investment Management LimitedJM Financial Singapore Pte. Limited Capital Market Publishers India Private LimitedJM Financial Services Limited JM Financial Home Loan LimitedJM Financial Asset Reconstruction Company Limited

4

Prudence Matters

JM Financial Capital Limited

Membership of Committees in other Companies (only the memberships of the Audit and Stakeholders Relationship Committee Shown)

Name of the Company Audit Committee Stakeholders’ Relationship Committee

JM Financial Credit Solutions Limited - Member

J. M. Financial and Investment Consultancy Services Private Limited

Member -

JM Financial Products Limited - Member

Notice (Contd.)

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

5Annual Report 2019-20

Directors’ Report

Directors’ Report

Dear Members,

The Directors of JM Financial Capital Limited (‘the Company’) are pleased to present their Fifth Annual Report together with the annual audited financial statements for the financial year ended March 31, 2020.

FINANCIAL PERFORMANCE

Financial Highlights

The summary of the Company’s financial performance for the financial year ended March 31, 2020 as compared to the previous financial year ended March 31, 2019 is given below:

(` in Lakh)

Particulars 2019-20 2018-19

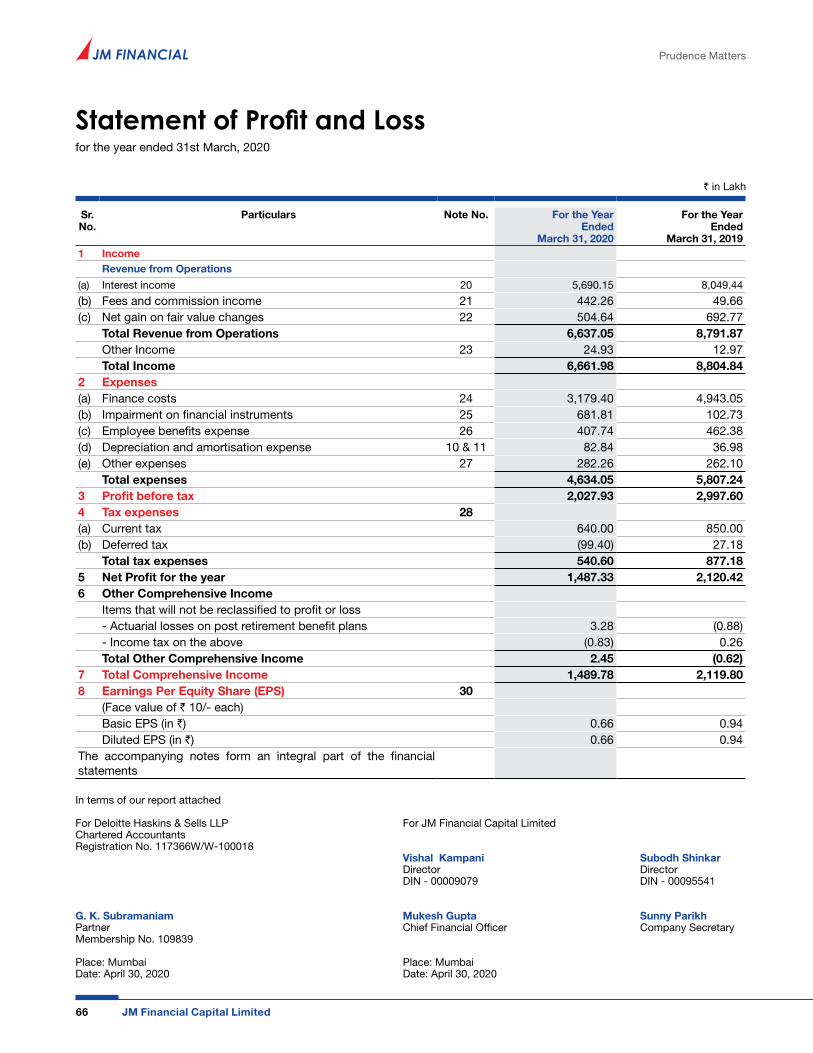

Gross Income 6,661.98 8,804.84

Less: Expenses 4,634.05 5,807.24

Profit before Tax 2,027.93 2,997.60

Current Tax 640.00 850.00

Deferred tax (99.40) 27.18

Net profit 1,487.33 2,120.42

Add/(Less): Other Comprehensive Income 2.45 (0.62)

Total Comprehensive Income 1,489.78 2,119.80

Appropriations

The following appropriations have been made from the available profits of the Company for the financial year 2019-20:

(` in Lakh)

Particulars 2019-20 2018-19

Net Profit 1,487.33 2,120.42

Add/(Less): Other Comprehensive Income 2.45 (0.62)

Total Comprehensive Income 1,489.78 2,119.80

Add: Balance profit brought forward from previous year 3,112.62 1,417.82

Profit available for appropriation 4,602.39 3,537.62

Less: Appropriations - -

Transferred to statutory reserve (300.00) (425.00)

Surplus carried to balance sheet 4,302.39 3,112.62

Overview of the Company’s Financial Performance

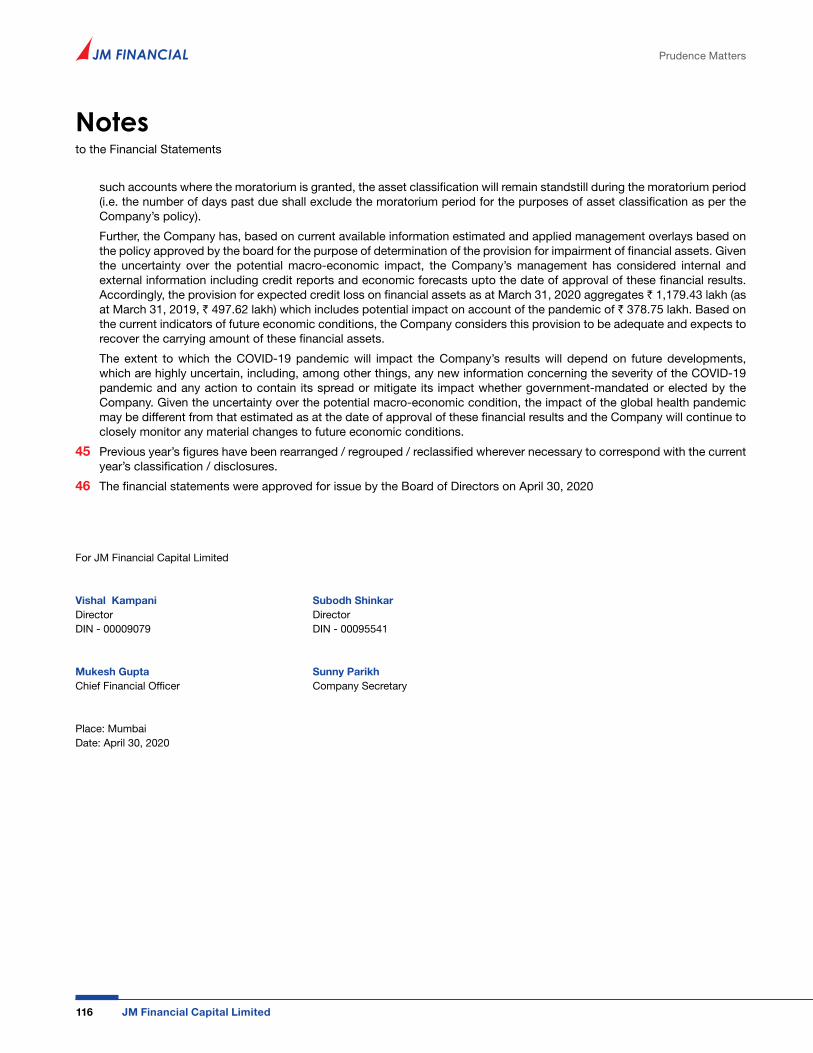

The outbreak of COVID-19 pandemic across the globe and in India has contributed to a significant decline and volatility in the global and Indian financial markets and slowdown in the economic activities. Reserve Bank of India (“RBI”) has issued guidelines relating to COVID-19 Regulatory Package dated March 27, 2020 and April 17, 2020 and in accordance therewith, the Company has proposed a moratorium of three months on the payment of all principal instalments and/or interest, as applicable, falling due between March 1, 2020 and May 31, 2020 to all eligible borrowers classified as standard, even if overdue as on February 29, 2020, excluding the collections made already made in the month of March 31, 2020. For all such accounts where the moratorium is granted, the asset classification will remain standstill during the moratorium period (i.e. the number of days past due shall exclude the moratorium period for the purposes of asset classification as per the Company’s policy).

6

Prudence Matters

JM Financial Capital Limited

Directors’ Report (Contd.)

Further, the Company has, based on current available information estimated and applied management overlays based on the Policy on Expected Credit Loss approved by the Board of Directors for the purpose of determination of the provision for impairment of financial assets. Given the uncertainty over the potential macro-economic impact, the Company’s management has considered internal and external information including credit reports and economic forecasts upto the date of approval of the financial results.

The extent to which the COVID-19 pandemic will impact the Company’s results will depend on future developments, which are highly uncertain, including, among other things, any new information concerning the severity of the COVID-19 pandemic and any action to contain its spread or mitigate its impact whether government-mandated or elected by the Company. Given the uncertainty over the potential macro-economic condition, the impact of the global health pandemic may be different from that estimated as at the date of approval of the financial results and the Company will continue to closely monitor any material changes to future economic conditions.

The Company has activated business continuity plan and mandated that large part of its employees to continue to work from home or remotely with effect from March 16, 2020 barring employees rendering essential services. COVID-19 has resulted in slow down of economic activities and has led to uncertainties and volatilities inter alia in the financial, capital and credit markets, which are expected to have an adverse impact on the business of the Company.

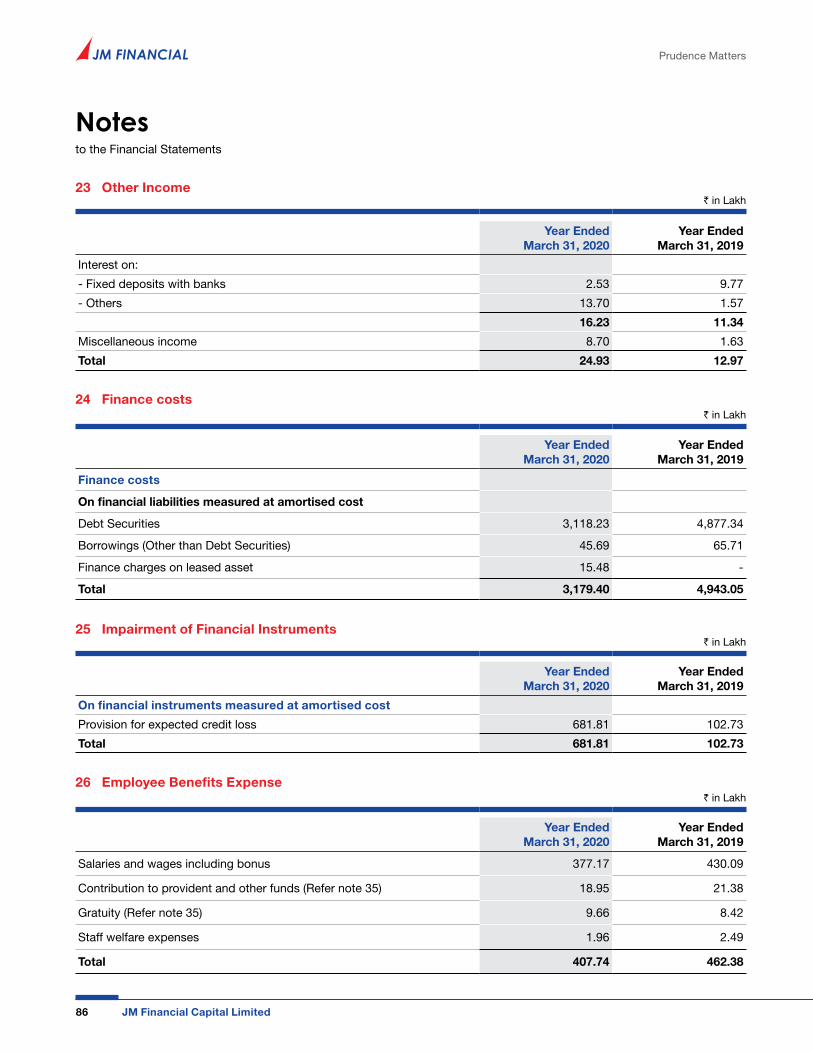

Gross Income

Total gross income earned by the Company during the financial year ended March 31, 2020 was ` 6,661.98 Lakh as compared to ` 8,804.84 Lakh during the previous financial year ended March 31, 2019.

Profit before tax

Profit before tax posted by the Company for the financial year ended March 31, 2020 was ` 2,027.93 Lakh as against ` 2,997.60 Lakh in the previous financial year ended March 31, 2019.

Profit after tax

Profit after tax was ̀ 1,487.33 Lakh for the financial year ended March 31, 2020 as against ` 2,120.42 Lakh in the previous financial year ended March 31, 2019.

DIVIDEND

The Board of Directors of the Company have decided to plough back the remaining profit after tax for business

activities and hence have not recommended any dividend on the equity share capital for the financial year ended March 31, 2020.

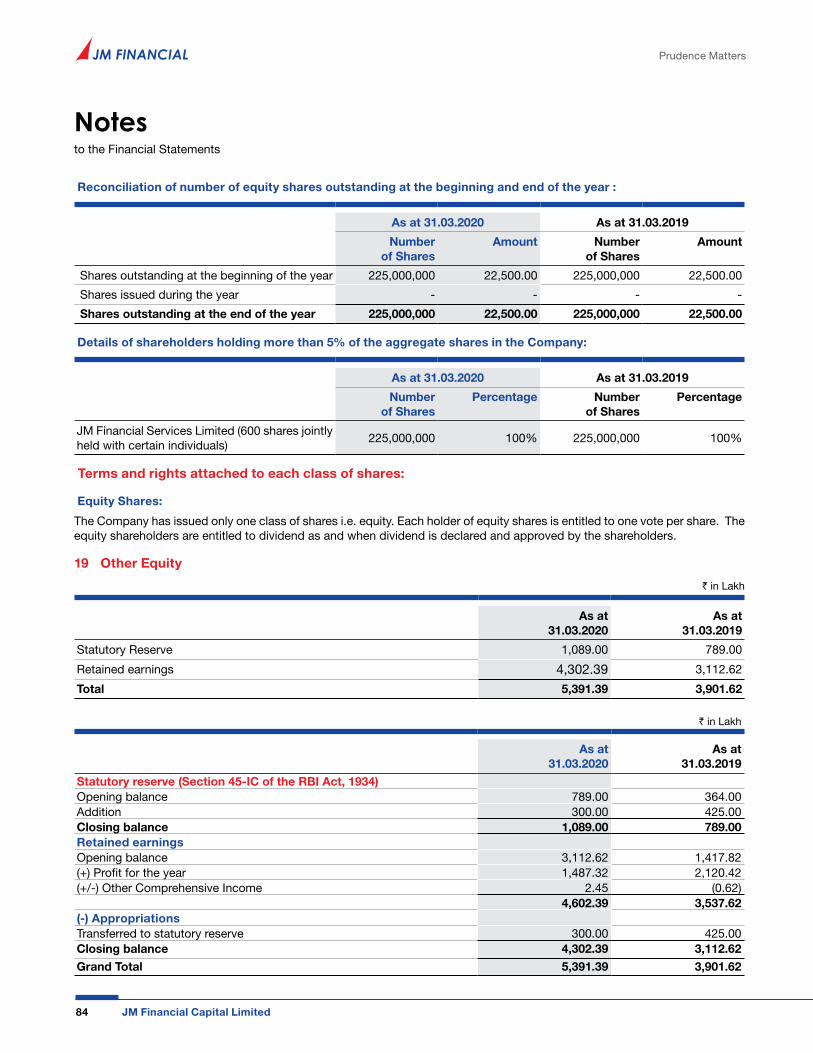

SHARE CAPITAL

(A) Authorised Share Capital

During the financial year under review, there has been no change in the authorised share capital of the Company. The authorised share capital of the Company as on March 31, 2020 stood at ` 300,00,00,000/- (Rupees Three Hundred Crore only) divided into (i) 22,50,00,000 Equity Shares of ̀ 10/- each aggregating to ` 225,00,00,000/- (Rupees Two Hundred and Twenty Five Crore only) and (ii) 7,50,00,000 preference shares of ̀ 10/- each aggregating to ̀ 75,00,00,000/- (Rupees Seventy Five Crore only).

(B) Issued and Paid-up Share Capital

The paid up share capital of the Company as on March 31, 2020 stood at ` 225,00,00,000/- (Rupees Two Hundred and Twenty Five Crore only) divided into 22,50,00,000 equity shares of ` 10/- each.

Other Equity

The reserves and surplus as at March 31, 2020 stood at ` 5,391.39 Lakh as against ` 3,901.62 Lakh as at March 31, 2019.

SUBSIDIARY COMPANY

As on March 31, 2020, the Company did not have any Subsidiary Company.

PUBLIC DEPOSITS

The Company being a “Systemically Important Non-Deposit taking Non-Banking Financial Company” has neither invited nor accepted or held any deposits from the public during the financial year ended March 31, 2020. Further, the Company will not accept any public deposits during the Financial Year 2020-21 without the prior written approval of Reserve Bank of India. As per the Master Direction - Non-Banking Financial Companies Acceptance of Public Deposits (Reserve Bank) Directions, 2016 issued by the Reserve Bank of India, a resolution in this regard has also been passed by the Board of Directors at its meeting held on April 30, 2020.

CREDIT RATING

The Company enjoys high credit ratings from the Rating Agencies. The credit ratings reflect the Company’s financial discipline and prudence.

During the financial year ended March 31, 2020, the Company avails the following credit rating facilities for the borrowing instruments of the Company from

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

7Annual Report 2019-20

Directors’ Report

ICRA Limited (ICRA), CRISIL Limited (CRISIL) and CARE Ratings Limited (CARE):

Facility ICRA CRISIL CARE

Commercial Paper Programme

ICRA A1+ CRISIL A1+ CARE A1+

Non-Convertible Debentures

ICRA AA/StableandPP-MLD ICRA AA/Stable

CRISIL AA / Stable

-

OVERVIEW OF BUSINESS PERFORMANCE OF THE COMPANY

The Company being Non-Banking Finance Company focuses on lending business offering products like loan against properties, loan against securities which inter-alia include margin funding, ESOP financing, loan against shares/bonds/mutual funds, financing clients for applications in select primary issuances in the equity and debt markets etc.

Operationally the processes and technology platform was put in place to ramp up the loan book. With the change in the CP Guidelines effective from August 10, 2017, the Company has obtained dual credit rating from ICRA Limited and CRISIL Limited with ratings assigned as “ICRA A1+” and “CRISIL A1+” for the Short Term Debt Programme (including Commercial Paper) for ` 1,000 Crore and ` 1,000 Crore respectively and “ICRA AA/ Stable” for Non-Convertible Debentures for ` 200 Crore & PP-MLD [ICRA AA] for ` 200 Crore for principal protected market linked Non-Convertible Debentures - from ICRA Limited.

The outbreak of the Covid-19 pandemic, created havoc and turmoil in the financial markets across the globe. The BSE SENSEX, which was at 41,254 as on December 31, 2019 closed at 29,469 as on March 31, 2020, a reduction of 29 %. This has seriously affected the capital market business and its exposure related NBFCs largely. The Covid-19 outbreak led panic sell-off in the global as well as domestic market. This has resulted in squaring off leveraged positions in the market largely, which was evident in the compressed loan book as well.

The overall capital market book stood at `144 Crore as at March 31, 2020. Corporate Funding as at March 31, 2020 stood at ` 57 Crore.

IPO financing though sluggish in the last quarter, totally 12 IPO’s (including 2 NCD issuance) were funded during the year aggregating to ` 6,144 Crore.

As on March 31, 2020 the total loan book stood at ` 200.75 Crore as compared to ` 425.56 Crore at the end of the previous financial year.

The overall closing FID funding book is ` 56.92 Crore as on March 31, 2020 as compared to ` 67.49 Crore as on March 31, 2019.

The Closing trading book of Institutional Fixed Income Division (IFID) stood at ` 26.91 Crore as on March 31, 2020. The fair value stood at ` 27.54 Crore as on March 31, 2020.

DEBT-EQUITY RATIO

The Debt Equity Ratio of the Company as at March 31, 2020 was 0.12.

EARNINGS PER SHARE (EPS)

The Earning per Share was ` 0.66 for the financial year ended March 31, 2020 as against ` 0.94 in the previous financial year ended March 31, 2019.

CAPITAL ADEQUACY

The Capital to Risk Assets Ratio of the Company is 90.92% as on March 31, 2020, as against the RBI norm of 15%. Out of the above, Tier I capital adequacy ratio stood at 90.43% and Tier II capital adequacy ratio stood at 0.49%.

NET OWNED FUNDS (TOTAL EQUITY)

The Net Owned Funds of the Company as at the financial year ended March 31, 2020 stood at ` 278.91 Crore as against ` 264.02 Crore in the previous financial year ended March 31, 2019.

LOAN BOOK

The total loan book of the Company for the financial year ended March 31, 2020 stood at ` 200.75 Crore as compared to ` 425.56 Crore as of March 31, 2019.

BOARD OF DIRECTORS AND KEY MANAGERIAL PERSONNEL

The composition of the Board of Directors of the Company is in accordance with Companies Act, 2013 (hereinafter referred to as “the Act”).

The Company has the following 5 (Five) Directors on its Board, two of them are Independent Directors.

Name of the Director Position held on the Board during the financial year 2019-20

Mr. Vishal Kampani Non-Executive Chairman

Mr. Subodh Shinkar Non-Executive Director

Ms. Sonia Dasgupta Non-Executive Director

Dr. Anup Shah Independent Director

Mr. Parthiv Kilachand Independent Director

8

Prudence Matters

JM Financial Capital Limited

Directors’ Report (Contd.)

Independent Director

The Board of Directors at its meeting held on April 24, 2019 appointed Mr. Parthiv Kilachand as an Additional Director (Non-Executive Independent) of the Company. Further, the appointment of Mr. Parthiv Kilachand as Non-Executive Independent Director of the Company was regularised and approved by the members of the Company at the Fourth Annual General Meeting of the Company held on July 9, 2019.

Cessation of Director

During the financial year ended March 31, 2020, none of the Director ceased their directorship.

Retirement of rotation of the Directors

In compliance with Section 152 of the Act read with the Articles of Association of the Company, Mr. Vishal Kampani (DIN 00009079), a Non-Executive Director retires by rotation at this Annual General Meeting of the Company. Being eligible, Mr. Kampani has offered himself for re-appointment as a Director. The brief details of Mr. Kampani, who is proposed to be re-appointed as required under Secretarial Standard 2 (“SS - 2”) is provided in the Notice convening the Annual General Meeting of the Company.

Key Managerial Personnel (“KMP”)

The details of the KMP in the Company as per Sections 2(51) and 203 of the Act are given below:

Name of the KMP Designation

Mr. Subodh Shinkar Chief Executive Officer

Mr. Mukesh Gupta Chief Financial Officer

Mr. Rupesh Samani* Company Secretary and Compliance Officer (till June 28, 2019)

Mr. Sunny Parikh# Company Secretary and Compliance Officer (w.e.f. July 9, 2019)

* Mr. Rupesh Samani resigned as Company Secretary and Compliance Officer with effect from June 28, 2019# During the financial year ended March 31, 2020, the Board has appointed Mr. Sunny Parikh, as Company Secretary and Compliance Officer of the Company with effect from July 9, 2019. Further, in accordance with the provisions of section 203 of the Act, Mr. Parikh has also been designated as the Key Managerial Personnel (hereinafter referred to as “KMP”) of the Company.

DECLARATION BY INDEPENDENT DIRECTORS

Dr. Anup Shah and Mr. Parthiv Kilachand have confirmed to the Board that they meet the criteria of independence as specified under Section 149 (6) of the Act and that they also qualify to be an Independent Directors pursuant to Rule 5 of the Companies (Appointment and Qualification of Directors) Rules, 2014.

The above confirmations were placed before the Board at its meeting held on April 30, 2020 and duly noted.

FIT AND PROPER DECLARATIONS GIVEN BY DIRECTORS

Pursuant to the ‘Fit and Proper’ Policy adopted by the Company under the Non-Banking Financial Companies – Corporate Governance (Reserve Bank) Directions, 2016 issued by the RBI, the Company has received the requisite declaration and undertaking from all the Directors of the Company.

The above declarations were placed before the Board at its meeting held on April 30, 2020 and duly noted.

BOARD MEETINGS

The Board meets at regular intervals to inter-alia discuss about the Company’s policies and strategy apart from other Board matters. The tentative annual calendar of the Board and Committee meetings is circulated in advance to enable the Directors to plan their schedule and to ensure participation in the meetings. The notice for the Board / Committee meetings is also given in advance to all the Directors.

During the financial year ended March 31, 2020, 4 (four) board meetings were held on April 24, 2019, July 9, 2019, October 16, 2019, and January 14, 2020. The maximum time period between the two Board Meetings did not exceed 120 days. The Company adheres to the applicable provisions of the Act and the Secretarial Standards on the Board and Committee Meetings as prescribed by the Institute of Company Secretaries of India. Agenda papers containing all necessary information / documents are made available to the Board /Committee Members in advance to enable them to discharge their responsibilities effectively and take informed decisions.

The attendance at the Board meetings during the financial year 2019-20 is given below:

Name of the Director Category No. of meetings

conducted

No. of meetings attended

Mr. Vishal Kampani Non-Executive Chairman

4 4

Mr. Subodh Shinkar Non-Executive Director

4 4

Ms. Sonia Dasgupta Non-Executive Director

4 4

Dr. Anup Shah Independent Director

4 4

Mr. Parthiv Kilachand Independent Director

4 4

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

9Annual Report 2019-20

Directors’ Report

POLICIES ON DIRECTORS’ APPOINTMENT AND REMUNERATION

Pursuant to sub-section (3) of Section 178 of the Act, the Board has formulated Policies on Directors’ appointment and remuneration. This Policy includes criteria for selection of Directors, determining their qualifications, positive attributes, remuneration and independence of Directors, evaluation process for performance of Directors, key evaluation criteria and other matters.

In accordance with the applicable provisions of the Act, these Policies are uploaded on the website of the Company, viz., www.jmfl.com.

EVALUATION OF THE BOARD OF THE DIRECTORS

Pursuant to the provisions of the Act, the Board has carried out an annual evaluation of its own performance and that of its committees including performance of the directors individually. Through a structured questionnaire, feedback from the directors were obtained as a part of performance evaluation. This was done in accordance with the Company’s policy on performance evaluation. The Nomination and Remuneration Committee of the Board has also carried out the evaluation of the performance of all the individual directors and the Chairman of the Company.

The performance evaluation of individual directors including the Chairman, inter alia, was done based on the criteria such as professional conduct, roles and functions, discharge of duties and their contribution to Board/Committees/Senior Management. The questionnaire prepared for evaluation of the board as a whole and its committees also covered various aspects such as structure and composition, effectiveness of the board process, information, roles and responsibilities and functioning of the Board and its Committees, establishment and determination of responsibilities of Committees, the quality of relationships between the Board and the management and professional development.

The performance evaluation of the non-independent Directors viz., the Chairman and the Board as a whole including Board Committees was carried out by the Independent Directors at their separate meeting held on March 20, 2020, taking into account the views of the executive director and the non-executive directors.

COMMITTEES

The Board committees and other committees play an important role in the governance and focus on specific areas and make informed decisions within the terms of reference and authority delegated. The Board committees and other committees comprising senior officials of the Company as the Members are guided by their respective terms of reference. The Board

has constituted/ re-constituted the following Committees to take informed decisions in the best interests of the Company:

The Board of Directors of the Company has constituted the following Committees:

AUDIT COMMITTEE

The Audit Committee comprises of well qualified Directors. The composition of the Audit Committee is in accordance with the RBI guidelines for NBFCs and the Act and the rules made thereunder. During the financial year ended March 31, 2020, the Audit Committee comprised of 3 (three) Members viz., Mr. Vishal Kampani, Mr. Parthiv Kilachand and is chaired by Dr. Anup Shah.

During the financial year ended March 31, 2020, 4 (four) Audit Committee meetings were held on April 24, 2019, July 9, 2019, October 16, 2019 and January 14, 2020.

The attendance at the Audit Committee meetings during the financial year ended March 31, 2020 is set out below:

Name of the Member Position No. of meetings

held

No. of meetings attended

Dr. Anup Shah Chairman 4 4

Mr. Vishal Kampani Member 4 4

Mr. Parthiv Kilachand* Member 4 3

Mr. Subodh Shinkar# Member 4 1

* Mr. Parthiv Kilachand was appointed as a member of the Audit Committee with effect from April 24, 2019. # Mr. Subodh Shinkar, ceased to be a member of the Audit Committee with effect from April 24, 2019.

Brief Scope and Function

The Audit Committee inter-alia:

l Overview of the Company’s financial reporting process and the disclosure of its financial information to ensure that the financial statements are correct, sufficient and credible;

l Recommending to the Board, the appointment, re-appointment including terms of appointment and re-appointment and, if required, the replacement or removal of the Statutory Auditor and Internal Auditors and the fixation of audit fees;

l Approval of payment to auditors for any services rendered by them;

l Review and monitor the auditor’s independence and performance, and effectiveness of audit process;

l examination of the financial statement and the auditors’ report thereon;

10

Prudence Matters

JM Financial Capital Limited

Directors’ Report (Contd.)

l Reviewing, with the management, performance of the Statutory and Internal Auditors, adequacy of the internal control systems;

l Reviewing the internal audit report and to discuss with the internal auditors of any significant findings and follow up action;

l Reviewing with the management, the un-audited financial statements and the annual audited financial statements before submission to the Board for approval;

l To review the functioning of the Whistle Blower mechanism;

l Approval or any subsequent modification of transactions of the Company with related parties;

l Scrutiny of inter-corporate loans and investments;

l Valuation of undertakings or assets of the Company, wherever it is necessary;

l Monitors the end use of funds raised through offers of securities and related matters; and

l Review of compliances with SEBI (Prevention of Insider Trading) Regulations, 2018 and to verify that the systems for internal control are adequate and are operating effectively, at least once in a financial year.

All members of the Committee are financially literate. The Company Secretary of the Company acts as the Secretary to the Committee. The Chief Financial Officer along with Internal Auditors and Statutory Auditors and other senior officials of the JM Financial Group are invited to attend the meetings of the Committee.

CORPORATE SOCIAL RESPONSIBILITY COMMITTEE

The Board of the Company has constituted a Corporate Social Responsibility (CSR) Committee in accordance with the provisions of Section 135 of the Act. During the financial year ended March 31, 2020, the Committee is comprised of 3 (three) Members viz., Dr. Anup Shah, Mr. Subodh Shinkar and it is chaired by Mr. Vishal Kampani.

During the financial year ended March 31, 2020 1 (one) CSR Committee meetings was held on October 1, 2019.

The attendance at the CSR Committee meeting during the financial year ended March 31, 2020 is set out below:

Name of the Member Position No. of meetings

held

No. of meetings attended

Mr. Vishal Kampani Chairman 1 -

Dr. Anup Shah Member 1 1

Mr. Subodh Shinkar Member 1 1

Brief Scope and Function

The CSR Committee inter-alia:

l formulates and recommends to the Board, CSR Policy which shall indicate the activities to be undertaken by the Company as specified in Schedule VII to the Act;

l recommends on the amount of expenditure to be incurred on CSR activities.

l institutes a transparent monitoring mechanism for implementation of the CSR activities to be undertaken by the Company.

NOMINATION AND REMUNERATION COMMITTEE

The Board of the Company has constituted a Nomination and Remuneration Committee (NRC) in accordance with the provisions of Section 178 of the Act and the RBI guidelines for Non-Banking Finance Companies (NBFCs). During the financial year ended March 31, 2020, the NRC Committee is comprised of 4 (four) Members viz., Mr. Vishal Kampani, Mr. Subodh Shinkar, Mr. Parthiv Kilachand and the Committee is chaired by Dr. Anup Shah.

During the financial year ended March 31, 2020, 2 (two) NRC Committee meetings were held on April 16, 2019 and July 9, 2019.

The attendance at the NRC Committee meetings during the financial year ended March 31, 2020 is set out below:

Name of the Member Position No. of meetings

held

No. of meetings attended

Mr. Subodh Shinkar Chairman 2 2

Mr. Vishal Kampani Member 2 2

Dr. Anup Shah Member 2 2

Mr. Parthiv Kilachand* Member 2 1

* Mr. Parthiv Kilachand was appointed as member of the NRC Committee with effect from April 24, 2019.

Brief Scope and Function

The NRC inter-alia:

l formulates the criteria for determining qualifications, positive attributes and independence of a director;

l identifying and recommending the Board of Directors, the appointment of persons considered capable and fit for the role of a director based on the criteria so formulated;

l evaluates the performance of Board, its Committees and all the individual directors including Chairman of the Company;

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

11Annual Report 2019-20

Directors’ Report

l recommends to the Board of Directors, a policy relating to the remuneration for the Directors, Key Managerial Personnel and other employees of the Company; and

l such other tasks as may be entrusted to it by the Board of Directors from time to time.

SPONSORSHIP AND CREDIT COMMITTEE

The Board has duly constituted its Sponsorship and Credit Committee. During the financial year ended March 31, 2020, the Sponsorship and Credit Committee is comprised of 2 (two) Members viz., Mr. Subodh Shinkar and Mr. Vishal Kampani. The Committee is chaired by Mr. Subodh Shinkar.

During the financial year ended March 31, 2020, 11 (Eleven) meetings of the Sponsorship and Credit Committee were held on May 2, 2019, May 31, 2019, June 18, 2019, July 16, 2019, August 13, 2019, September 30, 2019, November 11, 2019, December 20, 2019, January 15, 2020, February 24, 2020 and March 16, 2020.

The attendance at the Sponsorship and Credit Committee meetings during the financial year ended March 31, 2020 is set out below:

Name of the Member Position No. of meetings

held

No. of meetings attended

Mr. Vishal Kampani Member 11 11

Mr. Subodh Shinkar Chairman 11 11

Brief Scope and Function

The Sponsorship and Credit Committee inter-alia:

l scrutinizing the loan proposals and if satisfied approving the sanction of the loan proposal;

l scrutinizing the proposal for investment, disinvestment, subscription in shares, debentures etc. and if satisfied grant approval for the same;

l overviewing the Company’s financial position and fund requirements for extending the same to its clients;

l deciding the amounts to be borrowed by the Company through various borrowing instruments;

l scrutinizing the proposal of purchasing/selling loan portfolio, NPAs etc;

l perform such other allied functions including but not limited to reviewing the statement of overdues and NPAs as may be required from time to time.”

ASSET LIABILITY MANAGEMENT COMMITTEE

The Board of the Company has constituted an Asset Liability Management Committee (hereinafter referred to as “ALM Committee”) in accordance with the RBI Guidelines for NBFCs. During the financial year ended March 31, 2020, the ALM Committee comprised of 2 (two) Members viz., Ms. Sonia Dasgupta and is chaired by Mr. Subodh Shinkar.

During the financial year ended March 31, 2020, 4 (four) meetings of the ALM Committee were held on April 24, 2019, July 24, 2019, October 24, 2019 and January 13, 2020.

The attendance at the ALM Committee meetings during the financial year ended March 31, 2020 is set out below:

Name of the Member Position No. of meetings

held

No. of meetings attended

Mr. Subodh Shinkar Chairman 4 4

Ms. Sonia Dasgupta Member 4 4

Brief Scope and Function

The Asset Liability Management Committee inter-alia:

l Review of the asset-liability profile of the Company with a view to manage the market exposure assumed by the Company;

l Safeguarding the recovery positions at any point of time;

l Review of risk monitoring system, ensure payment of liability on its due dates, liquidity risk management, funding and capital planning, profit planning and growth projections, forecasting and analyzing different scenarios and preparation of contingency plans; and

l Performing such other functions in relation to the lending activities such as to check the credit worthiness of the client, to approve loan and disbursement of loan and to renew loans from time to time.

RISK MANAGEMENT COMMITTEE

The Board of the Company has constituted a Risk Management Committee in accordance with the RBI Guidelines for NBFCs. During the financial year ended March 31, 2020, the Risk Management Committee is comprised of 4 (four) Members viz., Mr. Vishal Kampani, Mr. Mukesh Gupta, Ms. Sanji Aswani and is chaired by Mr. Subodh Shinkar.

During the financial year ended March 31, 2020, 4 (four) Risk Management Committee meetings were held on June 18, 2019, August 13, 2019, November 11, 2019 and February 28, 2020.

12

Prudence Matters

JM Financial Capital Limited

Directors’ Report (Contd.)

The attendance at the Risk Management Committee meetings during the financial year ended March 31, 2020 is set out below:

Name of the Member Position No. of meetings

held

No. of meetings attended

Mr. Subodh Shinkar Chairman 4 4

Mr. Vishal Kampani Member 4 4

Mr. Mukesh Gupta* Member 4 1

Ms. Sanji Aswani* Member 4 1

* Mr. Mukesh Gupta and Ms. Sanji Aswani were appointed as members of the Risk Management Committee w.e.f January 14, 2020.

Brief Scope and Function

The Risk Management Committee inter-alia:

l identifying, monitoring and measurement of the risk profile of the Company (including market risk, operational risk and transactional risk);

l overseeing its integrated risk measurement system;

l reviewing the minutes of Meetings of the Asset Liability Management Committee;

l reviewing the following:

a. returns/ reports to the RBI; and

b. periodic investment portfolio.

l performing any other act, duty as stipulated by the Companies Act, Reserve Bank of India, Securities & Exchange Board of India, Stock Exchanges, and any other regulatory authority, as prescribed from time to time.

INFORMATION TECHNOLOGY STRATEGY COMMITTEE

The Board of the Company has constituted IT Strategy Committee in accordance with the Master Direction on Information Technology (IT) Framework for NBFCs issued by RBI.

During the financial year ended March 31, 2020, the IT Strategy Committee comprised of 3 (three) Members viz., Mr. Sriram Jayaraman, Mr. Subodh Shinkar and is chaired by Dr. Anup Shah.

During the financial year ended March 31, 2020, 2 (two) IT Strategy Committee meeting was held on April 30, 2019 and October 16, 2019.

The attendance of the members at the IT Strategy Committee meeting during the financial year ended March 31, 2020, is given below:

Name of the Member Position No. of meetings

held

No. of meetings attended

Dr. Anup Shah Chairman 2 2

Mr. Subodh Shinkar Member 2 2

Mr. Titus Gunaseelan* Member 2 1

Mr. Sriram Jayaraman# Member 2 1

# Mr. Sriram Jayaraman was appointed as member of IT Strategy Committee w.e.f. October 16, 2019.

* Mr. Titus Gunaseelan ceased to be member of IT Strategy Committee w.e.f August 9, 2019

Brief Scope and Function

The IT Strategy Committee inter-alia:

l reviews and amends the IT strategies in line with the corporate strategies, reviews Board Policy, cyber security arrangements and any other matter related to IT Governance and may place its deliberations before the Board;

l approves IT strategy and Policy documents and ensures that the management has put an effective strategic planning process in place;

l ensures that management has implemented processes and practices that ensure that the IT delivers value to the business;

l ensures IT investments represent a balance of risks and benefits and that budgets are acceptable;

l monitors the method that management uses to determine the IT resources needed to achieve strategic goals and provides high-level direction for sourcing and use of IT resources; and

l ensures proper balance of IT investments for sustaining NBFC’s growth and becoming aware about exposure towards IT risks and controls. approves the IT strategy and policy documents.

INFORMATION TECHNOLOGY STEERING COMMITTEE

The Board of Company had constituted an IT Steering Committee in accordance with the Master Direction on Information Technology (IT) Framework for NBFCs issued by the RBI.

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

13Annual Report 2019-20

Directors’ Report

During the financial year ended March 31, 2020, the IT Steering Committee comprised of 5 (five) Members viz., Mr. Sachchidanand Muchandi, Mr. Mukesh Gupta, Mr. Sunny Parikh, Ms. Sanji Aswani and Mr. Sriram Jayaraman,

During the financial year ended March 31, 2020, 2 (two) IT Steering Committee meetings were held on April 12, 2019 and October 11, 2019.

The attendance of the members at the IT Steering Committee meeting during the financial year ended March 31, 2020 is given below:

Name of the Member Position No. of meetings

held

No. of meetings attended

Mr. Sriram Jayaraman# Chairman 2 -

Mr. Sachchidanand Muchandi Member 2 2

Mr. Mukesh Gupta Member 2 2

Ms. Sanji Aswani Member 2 2

Mr. Sunny Parikh! Member 2 1

Mr. Rupesh Samani $ Member 2 1Mr. Titus Gunaseelan* Member 2 1

# Mr. Sriram Jayaraman was appointed as member of IT Steering Committee w.e.f. October 16, 2019.* Mr. Titus Gunaseelan ceased to be member of IT Steering Committee w.e.f August 9, 2019 ! Mr. Sunny Parikh was appointed as member of IT Steering Committee w.e.f. July 9, 2019.$ Mr. Rupesh Samani ceased to be member of IT Steering Committee w.e.f June 28, 2019

Brief Scope and Function

The IT Steering Committee inter-alia provides oversight and monitors the progress of the project, including deliverables to be realized at each phase of the project and milestones to be reached according to the project timetable.

ALLOTMENT COMMITTEE

The Board of the Company has constituted Allotment Committee. During the financial year ended March 31, 2020, the Committee comprised of 2 (two) Members viz., Ms. Sonia Dasgupta and it is chaired by Mr. Subodh Shinkar.

During the financial year ended March 31, 2020 1 (one) Allotment Committee meetings was held on July 22, 2019.

The attendance at the Allotment Committee meeting during the financial year ended March 31, 2020 is set out below:

Name of the Member Position No. of meetings

held

No. of meetings attended

Mr. Subodh Shinkar Chairman 1 1

Ms. Sonia Dasgupta Member 1 1

Brief Scope and Function

The Allotment Committee inter-alia:

l allots the securities issued by the Company from time to time;

l issues new certificates/duplicate certificates for Equity Shares, NCDs and such other securities that may be issued and allotted by the Company from time to time; and

l to do all such acts, deeds, matters and things as may be required to allot and issue certificates as above.

ASSET LIABILITY MANAGEMENT (ALM) SUPPORT GROUP

The Board of the Company has constituted an Asset Liability Management (ALM) Support Group on January 14, 2020, in accordance with point (d) of sub-clause (i) of clause A of Guidelines on Liquidity Risk Management Framework issued by RBI on November 4, 2019. The Support Group comprises of Mr. Mukesh Gupta (Chief Financial Officer), Mr. Sunny Parikh (Company Secretary and Compliance Officer), Mr. Y V ShivNarain (Part of Borrowing team), Mr. Hemant Kotak & Mr. Nishanth Shetty (Part of Controllers team) and Ms. Sanji Aswani (Head – Risk).

Brief Scope and Function

The Asset Liability Management (ALM) Support Group shall be responsible for analysing, monitoring and reporting the liquidity risk profile to the Asset Liability Management Committee.

Further, the ALM Support Group would also analyse and report the sources of the funds, the proposed avenues for the application of the funds, the borrowing maturity of the various instruments, the disbursements made and the disbursements in pipeline and the details of the repayments, to the members of the ALM Committee on quarterly basis.

SEPARATE MEETING OF INDEPENDENT DIRECTORS

The Independent Directors met on March 20, 2020, without the presence of the Non-executive Directors, Chairman and the Senior Management team. The meeting was attended by all the Independent Directors. The matters considered and discussed thereat, inter-alia, included those prescribed under Schedule IV to the Act.

DIRECTORS’ RESPONSIBILITY STATEMENT

Pursuant to the requirements under Section 134(3)(c) read with Section 134(5) of the Act with respect to Directors’ Responsibility Statement, the Directors hereby confirm that:

a. in the preparation of the annual accounts the applicable accounting standards have been followed and that no material departures have been made in following the same;

14

Prudence Matters

JM Financial Capital Limited

Directors’ Report (Contd.)

b. appropriate accounting policies have been selected and applied consistently by the Directors and the judgments and estimates made by them are reasonable and prudent so as to give a true and fair view of the state of affairs of the Company at the end of the financial year and of the profit and loss of the Company for that period;

c. proper and sufficient care for maintenance of adequate accounting records in accordance with the provisions of Act have been taken by the Directors for safeguarding the assets of the Company and for preventing and detecting fraud and other irregularities;

d. the annual accounts have been prepared by the Directors on a going concern basis;

e. internal financial controls to be followed by the Company had been laid down and such internal financial controls are adequate and were operating effectively; and

f. proper systems have been devised to ensure compliance with the provisions of applicable laws and that such systems were adequate and operating effectively.

POLICIES AND PROCEDURES

The Company conducts its business in a fair, transparent and ethical manner within the existing rules and regulations prescribed for NBFCs. The Board of the Company has inter-alia adopted following policies in accordance with the RBI guidelines for NBFCs /SEBI Regulations and/or the Act. Further, the Board of Directors review and amend the policies, to the extent applicable, at regular intervals.

Internal Guidelines on Corporate Governance

The Internal Guidelines on Corporate Governance is formulated to set best practices and facilitates greater transparency in operations, and to ensure that the long term interests of all stakeholders are served by adhering to and enforcing the principles of sound corporate governance.

Fair Practice Code

The Fair Practice Code is formed with the objective to act fairly and reasonably in all the dealings with borrowers, to assist its customers in understanding as to what are the broad features of its financial products, services and what are the benefits, risks involved in availing the same and to make every attempt to ensure that its customers would have trouble-free experience in dealing with it.

Interest Rate Policy

The Interest Rate Policy lays out appropriate internal principles and procedures in determining interest rates and processing and other charges.

Know Your Customer/Prevention of Money Laundering Policy

The Know Your Customer/Prevention of Money Laundering Policy is adopted to prevent the Company from being used, intentionally or unintentionally, by criminal elements for money laundering activities including committing financial frauds, transferring or deposits of funds derived from criminal activity or for financing terrorism and to have an adequate procedure to identify and report any suspicious fraud/transactions to the Regulatory Authority.

Asset Liability Management (ALM) Policy and Liquidity Risk Management Framework

The Asset Liability Management (ALM) Policy is formulated to establish guidelines to ensure prudent management of assets and liabilities for the Company. Further pursuant to Guidelines on Liquidity Risk Management Framework issued by RBI on November 4, 2019, the Board of Directors has also adopted Liquidity Risk Management Framework to strengthen ALM Policy and to have a sound and robust liquidity risk management system.

Loan Policy

The Loan Policy is formulated to act as a framework governing all lending transactions of the Company and inter alia prescribes broad outlines for loan processing, pricing, risk assessment, compliances etc. to be adhered for various loan products offered by the Company. Further, the Loan Policy also consists of a resolution plan for stressed assets adopted in accordance with the Prudential Framework for Resolution of Stressed Assets Directions 2019 issued by RBI on June 7, 2019.

Resource Planning Policy

The Resource Planning Policy lays down a broad framework for resource raising activities through various sources in a manner that ensures a strategic and smooth management of interest rate risk and liquidity risk.

Treasury and Investment Policy

The Treasury and Investment Policy lays down a framework for deployment of funds of the Company with a view to optimize return on investments.

Credit Information Policy

The Company, being a member of Credit Information Companies (CIC) namely, Credit Information Bureau (India) Limited, Equifax Credit Information Services Private Limited, Experian Credit Information Co. of India Private Limited and CRIF Highmark Credit Information Services Private Limited has in place a Credit Information Policy in accordance with the Credit Information Companies (Regulation) Act, 2005 and the Rules/Regulations made thereunder.

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

15Annual Report 2019-20

Directors’ Report

Outsourcing Policy

The Company has adopted an Outsourcing Policy in accordance with the RBI Master Direction, inter-alia containing the selection of outsourcing activities as well as service providers, delegation of authority depending on risks and materiality and systems to monitor and review the operations of these activities.

Fit and Proper Criteria Policy

The Company has adopted the Policy on Fit and Proper to lay down the fit and proper criteria for the Directors of the Company. It is prepared for ascertaining the fit and proper criteria for newly appointed Directors as well as for those Directors who are continuing on the Board of the Company.

Policy for Preservation of Documents

The Policy for Preservation of Documents define the guidelines to identify, classify, retain and protect all types of documents for sufficient length of time so as to comply with the regulatory requirements and also to have records for use in events of disputes, litigation, investigation, etc. This policy intends to provide necessary guidance for preservation, custody and disposal of documents maintained/filed by the Company.

Whistle Blower Policy

The Company has adopted a Whistle Blower Policy in accordance with Section 177 of the Act.

Code of Practices and Procedures for Fair Disclosure of Unpublished Price Sensitive Information and Code for Prevention of Insider Trading

In view of the SEBI (Prohibition of Insider Trading) (Amendment) Regulations, 2019, the Company has the following Codes in place:

l Code of Practices and Procedures for Fair Disclosure of Unpublished Price Sensitive Information (“Fair Disclosure Code”) to formulate a framework and policy for fair disclosure of events and occurrences.

l Code for Prevention of Insider Trading (‘the Code’) to outline the policies and procedures to be followed by the Designated Persons as defined in this Code for handling unpublished price sensitive information and for trading in the securities of the Company.

Corporate Social Responsibility (CSR) Policy

The Company has adopted a CSR Policy in accordance with Section 135 of the Act. The CSR Policy of the Company inter-alia contains the activities that can be undertaken by the Company for CSR, composition and meetings of CSR Committee, details of existing Charitable trusts within the JM Financial Group, annual allocation for CSR activities, areas of CSR projects, criteria for selection of CSR projects,

modalities of execution/implementation of CSR activities and the monitoring mechanism of CSR activities/projects.

Moratorium Policy due to COVID-19

The Company has adopted Moratorium Policy due to COVID 19 to provide moratorium to eligible borrowers on payments of instalments/interest on all term loans and/or working capital facilities extended the Company.

Policy on Expected Credit Loss

Pursuant to RBI guidelines dated March 13, 2020 on Implementation of Ind AS, the Company has adopted a policy for computation of Expected Credit Losses to cover the procedures and controls for assessing and measuring credit risk on all lending exposures, commensurate with the size, complexity and risk profile of the Company.

Information Technology Policies

The Company had adopted the following Information Technology Policies in view of the Master Direction issued by RBI dated June 8, 2017 numbered DNBS.PPD.No.04/66.15.001/2016-17, to ensure availability of sufficient, competent and capable human resources:

l Information Security Policy

The Information Security Policy is laid down to provide IS Framework with basic tenets like identification/classification of assets, segregation of duties and functions, role based access control, security (personal and physical), maker-checker system, incident management, trails and Public Key Infrastructure.

l Cyber Security Policy

The Cyber Security Policy is adopted to devise a strategy to combat cyber threats given the level of complexity of business and acceptable levels of risk.

l Cyber Crisis Management Plan

The Cyber Crisis Management Plan is laid down in order to be well prepared to face emerging cyber threats such as zero day attacks, remote access threats and targeted attacks. It addresses aspects like Detection, Response, Recovery, and Containment and is a part of overall Board approved strategy.

l Change Management Policy

The Change Management Policy is laid down to realign Information Technology systems on a regular basis in lines with the changing needs of our customers and business.

l Business Continuity Planning and Disaster Recovery

The Business Continuity Planning and Disaster Recovery is designed to minimize the operational, financial, legal, reputational and other material consequences arising

16

Prudence Matters

JM Financial Capital Limited

Directors’ Report (Contd.)

from any disaster. It has features like Business Impact Analysis and Recovery strategy/ Contingency Plan.

Other Policies

The Company has also adopted the following policies as recommended by the NRC of the Board:

l Policy on Selection of Directors;

l Policy on Performance Evaluation and Remuneration of Directors; and

l Policy on Performance Evaluation and Remuneration framework for the Key Managerial Personnel and other employees.

AUDITORS

STATUTORY AUDITORS

Deloitte Haskins & Sells LLP, Chartered Accountants, (Registration No. 117366W/W-100018), are the Statutory Auditors of the Company. They were appointed as the Statutory Auditors for a period of five years viz., 2016-17, 2017-18, 2018-19, 2019-20 and 2020-21 pursuant to the applicable provisions of the Act. The requirement to place the matter relating to appointment of auditors for ratification by the members at every AGM has been done away by the Companies (Amendment) Act, 2017. Accordingly, no resolution has been proposed for ratification of appointment of statutory auditors at the ensuing AGM.

Comments on Statutory Auditors’ Report

The Statutory Auditors have issued their unmodified opinion, both on the financial statements for the year ended March 31, 2020 and that they have not highlighted any qualifications, reservations, adverse remarks or disclaimers. The Statutory Auditors have not reported any incident of fraud to the Audit Committee of the Company during the financial year 2019-20. The notes to the Accounts referred to in the Auditor’s Report are self-explanatory and therefore do not call for any further explanation and comments.

SECRETARIAL AUDITORS

Pursuant to the provisions of Section 204 of the Act and Rule 9 of Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014, the Board of Directors of the Company had at their meeting held on April 24, 2019, appointed M/s. Naren Shroff & Associates, Company Secretaries, to undertake the Secretarial Audit of the Company for the financial year 2019-20. The Secretarial Audit Report for the financial year ended 2019-20, is appended as Annexure I to this Report.

Comments on Secretarial Auditors’ Report

The said report does not contain any qualifications, reservations or adverse remarks or disclaimers.

INTERNAL AUDITORS

Pursuant to the requirements of Section 138 of the Act and rule 13 of Companies (Accounts) Rules, 2014, the Board of Directors of the Company had at their meeting held on April 24, 2019, appointed M/s. CNK & Associates LLP, Chartered Accountants, as the Internal Auditors of the Company for the financial year ended March 31, 2020.

SECRETARIAL STANDARDS

The Company complies with the applicable Secretarial Standards issued by Institute of Company Secretaries of India.

DEBENTURE TRUSTEE

Beacon Trusteeship Limited acted as the Debenture Trustee for the Non-Convertible Debentures (NCDs) issued by the Company by way of private placement.

REGISTRAR AND SHARE TRANSFER AGENTS

NSDL Database Management Limited acts as the Registrar and Share Transfer Agent of the Company for the issuance of NCDs and KFin Technologies Private Limited (formerly known as Karvy Fintech Private Limited) acts as the Registrar and Share Transfer Agent of the Company for the issuance of Commercial Papers.

CORPORATE SOCIAL RESPONSIBILITY

The Board has constituted Corporate Social Responsibility (CSR) Committee in accordance with Section 135 of the Act.

The CSR Policy of the Company, inter alia, list the activities that can be undertaken or supported by the Company for CSR, composition and meetings of CSR Committee, details of existing Charitable Trusts within the JM Financial Group, annual allocation for CSR activities, areas of CSR projects, criteria for selection of CSR projects, modalities of execution/implementation of CSR activities and the monitoring mechanism of CSR activities/projects. The details of CSR activities undertaken by the Company are described in the prescribed format and are appended as Annexure II to this Report.

RISK MANAGEMENT

Risk management forms an integral part of our business operations and monitoring activities. The Company and its subsidiary are exposed to a variety of risks, including liquidity risk, interest rate risk, market credit risk, operational risk, regulatory and compliance risk, business and continuity risk and legal risk. Further, the Company convenes on periodical intervals Risk Management Committee meetings. The details of the risks faced by the Company and the mitigation thereof are discussed in detail in the Management Discussion and Analysis report.

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

17Annual Report 2019-20

Directors’ Report

INTERNAL FINANCIAL CONTROL SYSTEMS AND ITS ADEQUACY

The Board has adopted accounting policies which are in accordance with Section 133 of the Act read with the Companies (Indian Accounting Standards) Rules, 2015.

The internal financial control system of the Company is supplemented with internal audits, regular reviews by the management and checks by external auditors. It provides reasonable assurance in respect of providing financial and operational information, complying with applicable statues, safeguarding of assets of the Company, prevention and detection of frauds, accuracy and completeness of accounting records and ensuring compliance with the Company’s policies. The Audit Committee monitors this system and ensures adequacy of the same. The Statutory Auditors and the Internal Auditors of the Company also provides their opinion on the internal financial control framework of the Company.

During the year, no material or serious observations have been highlighted for inefficiency or inadequacy of such controls. The details of adequacy of Internal Financial Controls are given at length in the Management Discussion and Analysis Report.

RESOURCE MOBILIZATION

During financial year 2019-20, the Company met its funding requirements through a combination of Short Term debt (comprising Commercial Papers, Inter-Corporate Deposits (“ICDs”) and Bank Overdraft) and Long Term debt (comprising Non-Convertible Debentures (“NCDs”) ).

The Company’s total principal borrowing amounted to ` 35.30 Crore as at March 31, 2020 as against ` 270.00 Crore in the previous year.

The Company has been regular in servicing its debt obligations.

a) NON-CONVERTBLE DEBENTURES (NCDs)

Private Placement of Secured Rated Listed Redeemable Principal Protected Market Linked NCDs

During the financial year ended March 31, 2020, the Company has raised ` 35.30 Crores (Rupees Thirty Five Crore Thirty Lakh only) by way of issuance of 706 Secured Rated Listed Redeemable Principal Protected Market Linked NCDs (NCDs) of face value of ` 5,00,000/- each on Private Placement basis. The issued NCDs are listed on the Wholesale Debt Market Segment of BSE Limited.

b) BANK LINES

During the financial year ended March 31, 2020, the Company had overdraft against fixed deposit facility through HDFC Bank for an amount aggregating upto ` 9.50 Crore. As on March 31, 2020, there was no outstanding overdraft facility.

c) COMMERCIAL PAPERS

During the financial year ended March 31, 2020, the Company had issued CPs for an amount aggregating to ` 6,860 Crore and an amount aggregating to ` 7,130 Crore were duly redeemed upon their maturity.

The Company has been regular in repayment of its borrowings and payment of interest thereon.

d) INTER-CORPORATE DEPOSITS

The Company had taken an Inter-Corporate Deposit of ` 50 Crore which was duly repaid during the financial year ended March 31, 2020.

MATERIAL CHANGES AND COMMITMENTS AFFECTING THE FINANCIAL POSITION OF THE COMPANY

There have been no material changes and commitments affecting the financial position of the Company which have occurred between the end of the financial year of the Company to which the financial statements relate and the date of this Report.

DETAILS OF SIGNIFICANT AND MATERIAL ORDERS

During the financial year 2019-20, there were no significant and material orders passed by the regulators or courts or tribunals impacting the going concern status and Company’s operation in future. Further, no penalties have been levied by RBI/any other Regulators during the year under review.

REPORT ON MANAGEMENT DISCUSSION & ANALYSIS

The report on Management Discussion and Analysis for the year under review, as stipulated under the Non-Banking Financial Companies – Corporate Governance (Reserve Bank) Directions, 2015 issued by the RBI, forms part of this Report.

PARTICULARS OF REMUNERATION OF DIRECTORS/KMPS

The requisite disclosures in terms of the provisions of Section 197 of the Act read with Rule 5 of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 is appended to this Report as Annexure III.

As per the provisions of Section 136(1) of the Act, the reports and accounts are being sent to the Members of the Company excluding the information regarding employee remuneration as required pursuant to Rule 5(2) and Rule 5(3) of the said Rules. The same will be available for inspection up to the date of the Fifth AGM.

18

Prudence Matters

JM Financial Capital Limited

Directors’ Report (Contd.)

PARTICULARS OF LOANS, GUARANTEES AND INVESTMENTS

The particulars of loans, guarantees or investments under Section 186 of the Act are not furnished since the provisions of the said Section are not applicable to the Company, being an NBFC registered with the RBI.

PARTICULARS OF CONTRACTS OR ARRANGEMENTS WITH RELATED PARTIES DURING THE FINANCIAL YEAR ENDED MARCH 31, 2020

The Board of Directors of the Company has formulated a policy on dealing with Related Party Transactions, pursuant to the applicable provisions of the Act and RBI Master Directions. The same is displayed on the website of the Company at https://jmfl.com/who-we-are/group-companies.

The related party transactions that were entered into during the financial year ended March 31, 2020 were on arm’s length basis and in ordinary course of business. Pursuant to Section 134(3)(h) read with Rule 8(2) of the Companies (Accounts) Rules, 2014, there are no related party transactions that are required to be reported under Section 188(1) of the Act, as prescribed in Form AOC-2.

However, the details of the transactions with Related Party are provided in the Company’s financial statement in accordance with applicable Accounting Standard.

CONSERVATION OF ENERGY, TECHNOLOGY ABSORPTION, FOREIGN EXCHANGE EARNINGS AND OUTGO

The particulars regarding Conservation of Energy and Technology Absorption are not furnished since they are not applicable to the Company.

During the financial year ended March 31, 2020, the Company has not earned any foreign exchange.

ANNUAL RETURNPursuant to the requirements of Section 92(3) and Section 134(3) of the Act read with Rule 12 of Companies (Management and Administration) Rules, 2014, an extract of Annual Return as on March 31, 2020 in prescribed Form MGT-9 is given in this report as Annexure IV and also uploaded on the website of the Company as a part of the Annual Report.

VIGIL MECHANISM / WHISTLE BLOWER POLICYThe Company has established a vigil mechanism to provide appropriate avenues to the Directors and employees to bring to the attention of the Management, their genuine concerns about behavior of employees.

During the financial year ended March 31, 2020, no cases under this mechanism were reported to the Company.

POLICY FOR PREVENTION, PROHIBITION AND REDRESSAL OF SEXUAL HARASSMENT OF WOMEN AT WORKPLACEThe policy against sexual harassment is embodied both in the Code of Conduct of JM Financial Group as also in a specifically written policy in accordance with The Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013.

During the financial year ended March 31, 2020, no cases in the nature of sexual harassment were reported at any workplace of the Company.

MEANS OF COMMUNICATIONThe Company’s website keeps the investors updated on material developments in the Company by providing key and timely information such as Financial Results, Annual Reports, etc.

a. Half Yearly Results

The unaudited half yearly financial results are announced within forty-five days of the end of the half year. The audited annual financial results are announced within sixty days of the close of the financial year as per the requirements of the Regulation 52 of the SEBI (Listing Obligations and Disclosure Requirement) Regulations, 2015. The aforesaid financial results are sent to BSE Limited where the Company’s NCDs are listed. The unaudited half yearly results for the period ended September 30, 2019 was thereafter published within two calendar days in one English national daily newspaper (generally Business Standard). Also these unaudited and audited financial results were placed on the Company’s website viz., www.jmfl.com and are also available on the Stock exchange website. The Company also emails the unaudited half yearly and audited annual financial results to the NCD holders of the Company.

b. Website

The Company’s website www.jmfl.com provides information about the businesses carried on by the Company. It is the primary source of information to all the stakeholders of the Company and to general public at large. It also contains a Financial Results, Annual Reports, CSR, various Policies adopted by the Board and other general information about the Company is also available on its website. In accordance with the Liquidity Risk Management Framework for Non-Banking Financial Companies, the Company on a quarterly basis provided a public disclosure on liquidity risk as on its website.

c. Annual Report

Annual Report containing, inter alia, the Directors’ Report, Auditors’ Report and other important information is circulated to members of the Company and other stakeholders prior to the AGM. The Report on Management Discussion and Analysis forms part of the Annual Report.

Dir

ec

to

rs

’ re

po

rt

Fina

nc

ial S

tatem

en

tS

19Annual Report 2019-20

Directors’ Report

The Annual Report of the Company is also available on its website in a user friendly and downloadable format.

ACKNOWLEDGEMENTThe Directors acknowledges the support extended by the Reserve Bank of India, Securities and Exchange Board of India, Ministry of Corporate Affairs, Registrar of Companies, Maharashtra, Mumbai, other government and regulatory authorities.

The Directors also place on record the gratitude for the guidance and support extended by BSE Limited, National Securities Depository Limited, Central Depository Services (India) Limited.

The Directors also place on record their sincere appreciation for the continued support extended by the bankers, financial institutions, lenders and stakeholders, and trust reposed by them in the Company.

Recognising the challenging work environment, the Directors place on record, their appreciation for the dedication and commitment displayed by the employees of the Company across all levels.

For and on behalf of the Board

Vishal KampaniDate: April 30, 2020 ChairmanPlace: Mumbai (DIN 00009079)

20

Prudence Matters

JM Financial Capital Limited

Annexure I

FORM MR 3

SECRETARIAL AUDIT REPORTfor the Financial Year Ended 31St March, 2020

[Pursuant to section 204(1) of the Companies Act, 2013 and Rule No.9 of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014]

To,The Members,JM FINANCIAL CAPITAL LIMITED 7th Floor, Cnergy, Appasaheb Marathe Marg, Prabhadevi, Mumbai – 400 025.

We have conducted the secretarial audit of the compliance of applicable statutory provisions and the adherence to good corporate practices by JM FINANCIAL CAPITAL LIMITED (hereinafter called ‘the Company’). Secretarial Audit was conducted in a manner that provided us a reasonable basis for evaluating the corporate conducts/statutory compliances and expressing our opinion thereon.

Based on our verification of the Company’s books, papers, minute books, forms and returns filed and other records maintained by the Company, as produced before us, and also the information provided by the Company, its officers, agents and authorized representatives during the conduct of secretarial audit, we hereby report that in our opinion, the Company has, during the audit period covering the financial year ended on 31st March, 2020 complied with the statutory provisions listed hereunder, to the extent applicable to the Company, and also that the Company has proper Board-processes and compliance-mechanism in place to the extent, in the manner and subject to the reporting made hereinafter:

I. We have examined the Secretarial compliance based on the books, papers, minute books, forms and returns filed and other records maintained by the Company for the financial year ended on 31st March, 2020, as shown to us during our audit, according to the provisions of:

(i) The Companies Act, 2013 (the Act) and the rules made thereunder, as amended;

(ii) The Securities Contracts (Regulation) Act, 1956 (‘SCRA’) and the rules made thereunder, as amended and to the extent applicable;

(iii) The Depositories Act, 1996 and the Regulations and Bye-laws framed thereunder and to the extent applicable;

(iv) The following Regulations and Guidelines prescribed under the Securities and Exchange Board of India Act, 1992: -

(a) The Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 2015, as amended and to the extent applicable;

(b) The Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011, as amended and to the extent applicable;

(c) The Securities and Exchange Board of India (Issue and Listing of Debt Securities) Regulations, 2008, as amended and to the extent applicable; and

(d) The Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, as amended and to the extent applicable.

II. We further report that the Company has complied with the Secretarial Standards issued by The Institute of Company Secretaries of India.

III. During the year under review, the Company has complied with the applicable provisions of the Act, Rules, Regulations, Guidelines, Standards, etc. as mentioned above.

IV. We further report that, having regard to the compliance system prevailing in the Company and on examination of relevant documents and record, produced for our verification, in pursuance thereof, the Company has complied with the following Directions applicable specifically to the Company, in respect of submission / filing of various documents, returns, forms, information and other particulars with the prescribed authority;

• Non-Banking Financial Company – SystematicallyImportant Non – Deposit taking Company and Deposit taking Company (Reserve Bank) Directions, 2016, as amended and to the extent applicable.