Javed Siddiqi

33

Credit Risk Modelling for IFRS -9 Javed H. Siddiqi Head of Risk Management Division Soneri Bank -Pakistan 23-25 May 2016 Singapore

-

Upload

jhsiddiqi2003 -

Category

Documents

-

view

84 -

download

2

Transcript of Javed Siddiqi

Credit Risk Modell ing for IFRS -9

Javed H. S idd iq i

Head o f R isk Management D iv is ion

Soner i Bank -Pakistan

23-25 May 2016 Singapore

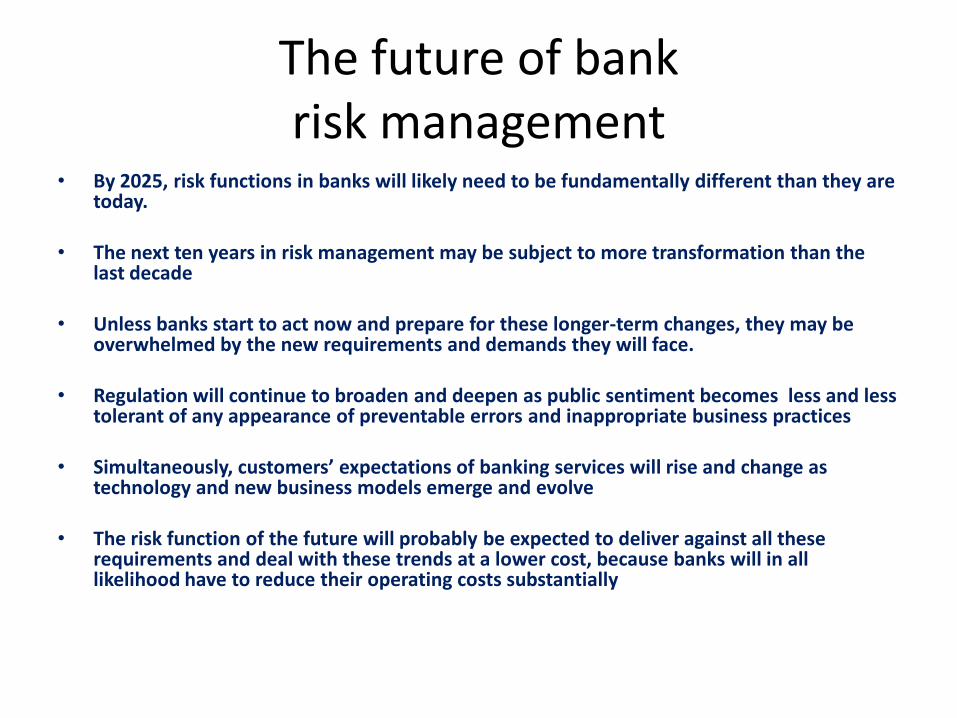

The future of bank risk management

• By 2025, risk functions in banks will likely need to be fundamentally different than they are today.

• The next ten years in risk management may be subject to more transformation than the last decade

• Unless banks start to act now and prepare for these longer-term changes, they may be

overwhelmed by the new requirements and demands they will face.

• Regulation will continue to broaden and deepen as public sentiment becomes less and less tolerant of any appearance of preventable errors and inappropriate business practices

• Simultaneously, customers’ expectations of banking services will rise and change as technology and new business models emerge and evolve

• The risk function of the future will probably be expected to deliver against all these requirements and deal with these trends at a lower cost, because banks will in all likelihood have to reduce their operating costs substantially

What will the risk function look like in 2025?

• It is likely to have broader responsibilities, to be very engaged at a strategic level, and to have much stronger, collaborative relationships with other parts of the bank.

• Banks talent pool will probably have experienced a massive shift in expertise toward better analytics and greater collaboration, and away from operating processes

• IT and data will likely be much more sophisticated, often employing big data and complex algorithms.

• The risk function may be able to make better risk decisions at lower operating costs while creating superior customer experiences.

• If banks want their risk functions to thrive during this period of fundamental transformation, they need to rebuild them during the next decade.

The leading institutions will be

distinguished by their intelligent management of risk.

In the future . . .

Rational for Change (IAS 39 to IFRS 9)

• During the financial crisis, the incurred loss model of IAS 39 for accounting of

credit losses associated with loans and other financial instruments was identified as one of the main weakness of existing accounting standards

• The current IAS 39 uses an incurred loss model to recognize impairment loss of a financial asset only after a trigger loss event has occurred.

• Incurred loss mode is “too little too late” because the model delays the recognition of a credit loss event unit there is objective evidence of impairment.

• Incurred loss model only consider those losses that arises from past events and effect of future credit loss events cannot be considered, even when they are expected.

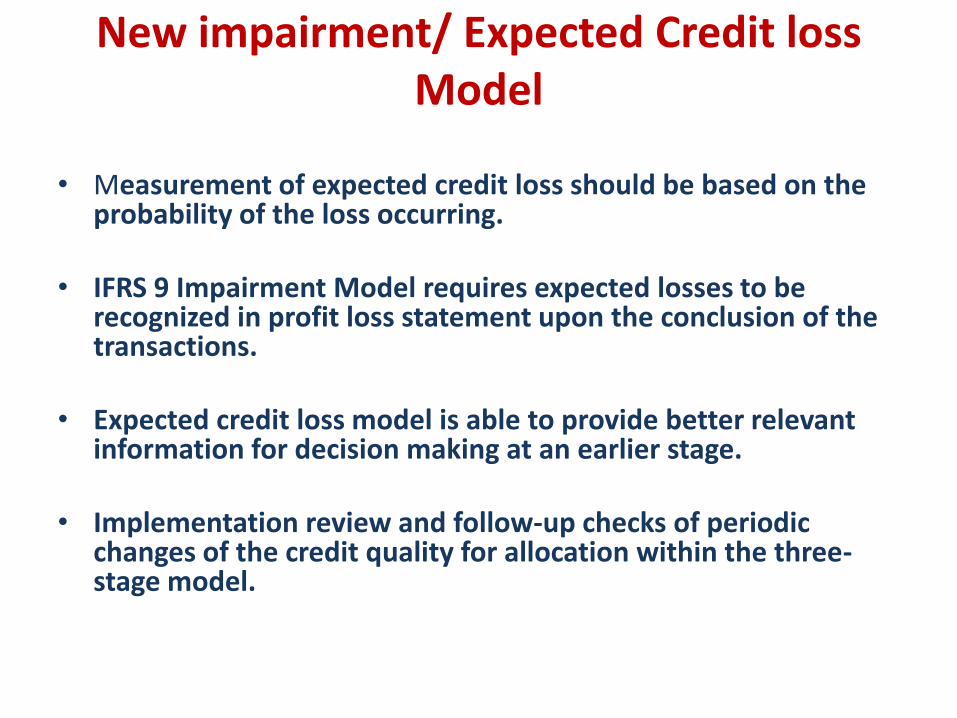

New impairment/ Expected Credit loss Model

• Measurement of expected credit loss should be based on the

probability of the loss occurring.

• IFRS 9 Impairment Model requires expected losses to be recognized in profit loss statement upon the conclusion of the transactions.

• Expected credit loss model is able to provide better relevant information for decision making at an earlier stage.

• Implementation review and follow-up checks of periodic changes of the credit quality for allocation within the three-stage model.

Challenges and complexities: Integration with risk management model

• The primary challenge of implementing this ECL impairment

model of accounting is integrating the model with the existing risk management system of the banks.

• This forward looking ECL impairment model requires a lot of estimations including Exposure at default (EAD), probability of defaults (PD) and loss given default (LGD) which can be pulled from existing credit models with some essential

adjustments as required.

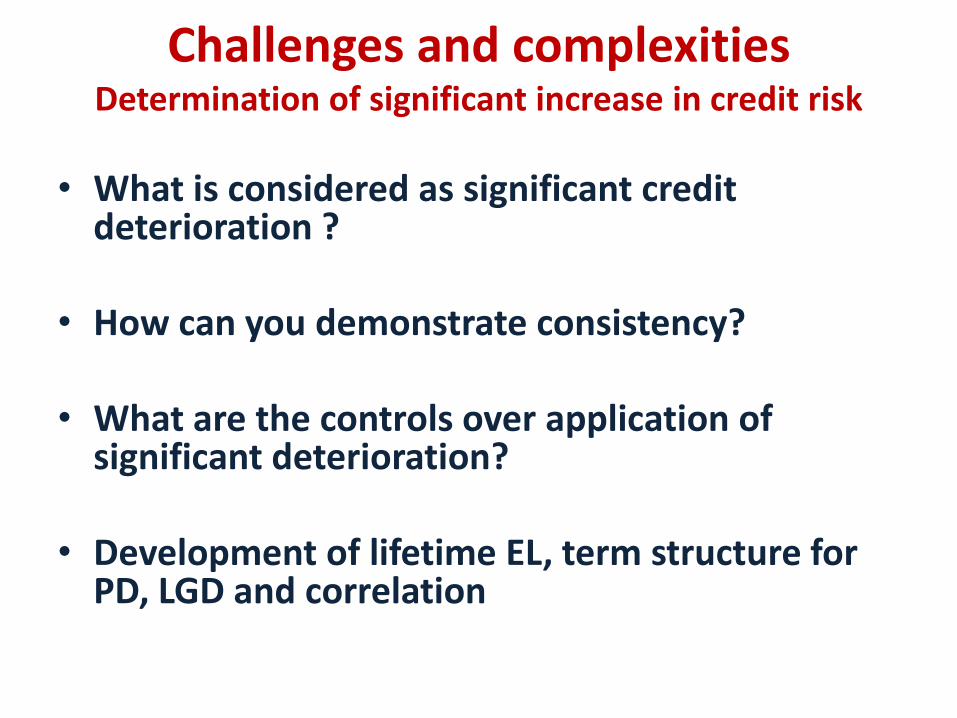

Challenges and complexities Determination of significant increase in credit risk

• What is considered as significant credit

deterioration ?

• How can you demonstrate consistency?

• What are the controls over application of significant deterioration?

• Development of lifetime EL, term structure for PD, LGD and correlation

Challenges and complexities Incorporating forward looking information:

• One of the major change in IFRS 9 from IAS 39 is the consideration of forward looking information and macro-economic factors to forecast future economic condition in the expected credit loss estimation

• The standard also mentions that the measurement should reflect reasonable and supportable information available

• Though the standard does not prescribe any particular method of measurement, the entity would require to judge individual or group of assets considering a wide range of quantitative and qualitative information

• The Basel committee guidelines published in February 2015 recognized that the implementation of forward looking information will be costly but this cost should not be avoided and the bank’s experienced credit judgment must be documented in their credit risk methodology.

Leveraging existing Basel II/III Methodologies In use Probability of Default -PD

IFRS 9 Basel II/III

PD estimates over 12-month horizon for Stage 1; Lifetime Loss calculation for Stage 2 and 3

12-month PD estimation

PD estimates are “point-in-time” measures

PD estimates is mostly based on “through-the-cycle” measure

Definition of default-may adopt regulatory definitions

Regulatory overrides

Considers forward looking estimates at balance sheet date.

Routine use of stress testing and scenario analysis for calibration

Leveraging Existing Basel II/III Methodologies In Use Loss Given Default Model-LGD

IFRS 9 Basel II/III

Current LGD Downturn LGD estimates

Discount rate should be at effective interest rate

Consideration of certain costs and LGD floors

Collateral valuation and disclosures for financial instruments with inherent objective evidence of impairment

Discount rate based upon weighted average cost of capital or risk-free rate

Treatment of collateral is subject to detailed rules, haircuts etc.

IFRS 9: Potential Impact & Challenges

• Business Related Challenges

• Methodical Challenges

• Technical Challenges

• Process Related Challenges

• Strategic Challenges

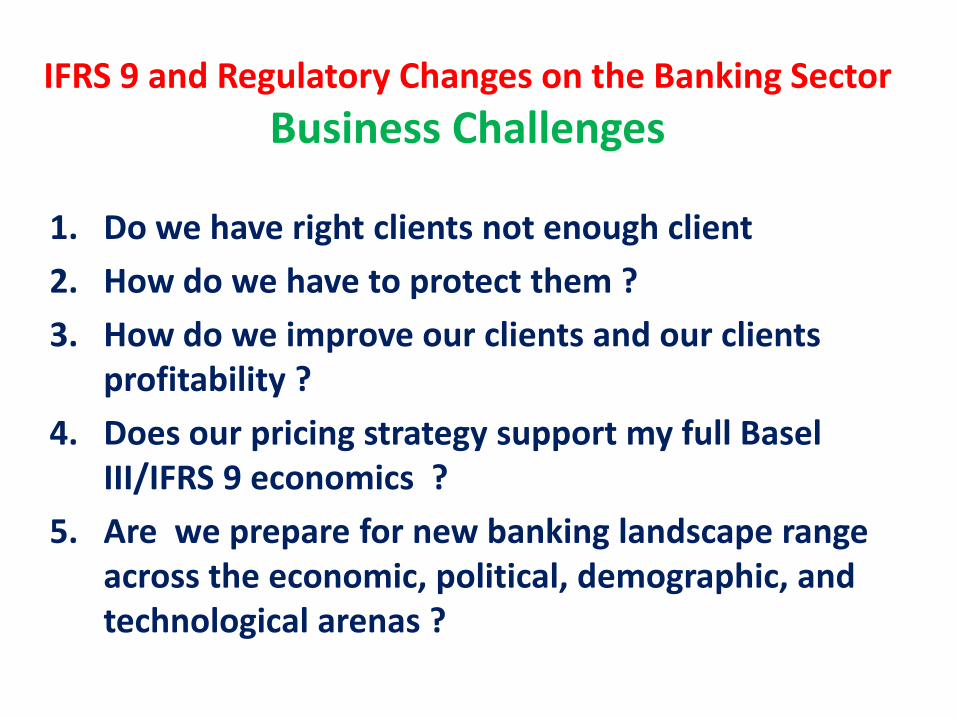

IFRS 9 and Regulatory Changes on the Banking Sector

Business Challenges

1. Do we have right clients not enough client

2. How do we have to protect them ?

3. How do we improve our clients and our clients profitability ?

4. Does our pricing strategy support my full Basel III/IFRS 9 economics ?

5. Are we prepare for new banking landscape range across the economic, political, demographic, and technological arenas ?

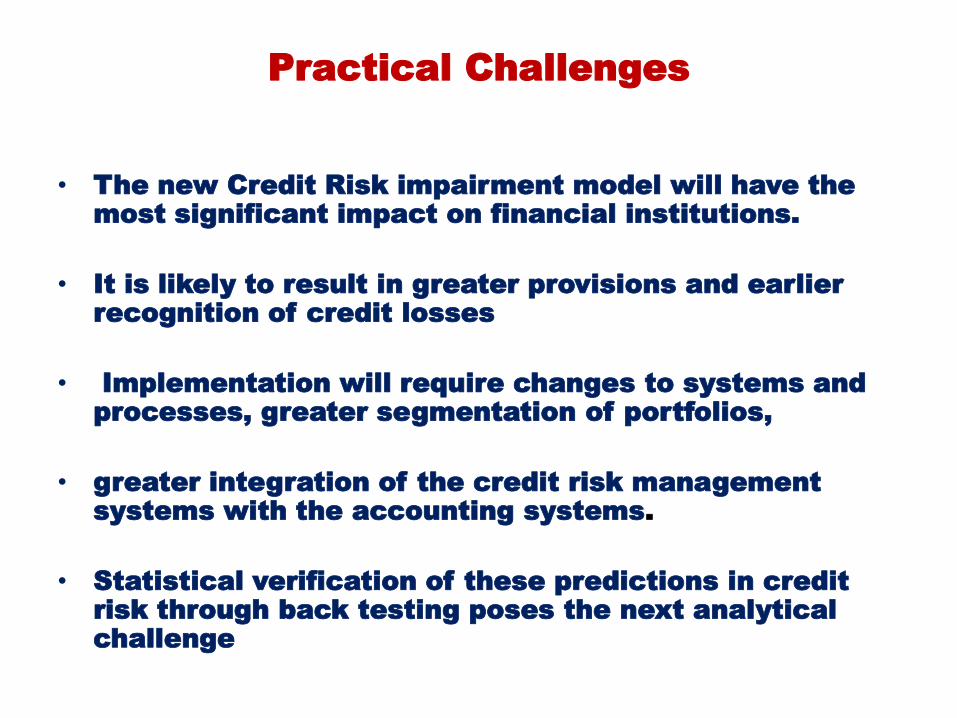

Practical Challenges

• The new Credit Risk impairment model will have the

most significant impact on financial institutions.

• It is likely to result in greater provisions and earlier

recognition of credit losses

• Implementation will require changes to systems and

processes, greater segmentation of portfolios,

• greater integration of the credit risk management

systems with the accounting systems.

• Statistical verification of these predictions in credit

risk through back testing poses the next analytical

challenge

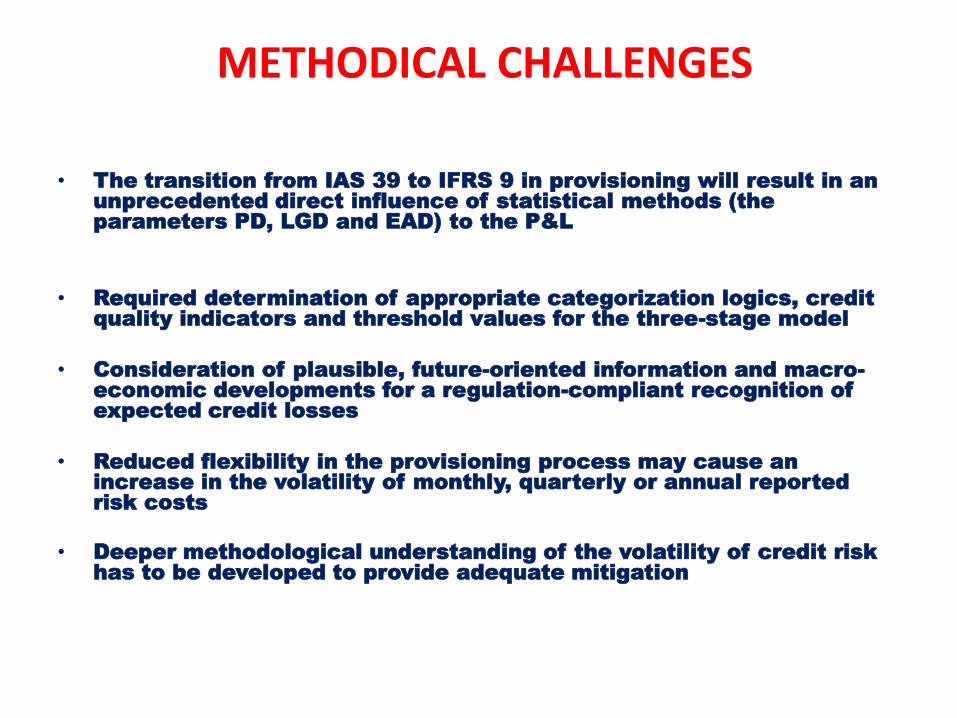

METHODICAL CHALLENGES

• The transition from IAS 39 to IFRS 9 in provisioning will result in an

unprecedented direct influence of statistical methods (the

parameters PD, LGD and EAD) to the P&L

• Required determination of appropriate categorization logics, credit

quality indicators and threshold values for the three-stage model

• Consideration of plausible, future-oriented information and macro-

economic developments for a regulation-compliant recognition of

expected credit losses

• Reduced flexibility in the provisioning process may cause an

increase in the volatility of monthly, quarterly or annual reported

risk costs

• Deeper methodological understanding of the volatility of credit risk

has to be developed to provide adequate mitigation

TECHNICAL CHALLENGES

• Review and follow-up checks of periodic changes

of the credit quality for purposes of (re-)allocation

within the three-stage logic

• Definition system-related implementation of

rights of choice regarding trading and leasing

requirements

• Selection and implementation of appropriate

technical impairment solutions, taking the

cost/benefit ratio and the integration into the

existing system environment into account

PROCESS-RELATED CHALLENGES

• The selection and implementation of suitable IT impairment solutions, taking both cost/benefit factors and integration into existing system and environment.

• Ensuring that the impairment results can be reconciled to regulatory and other internal credit risk measurement results

• Prospective PDs and cash shortfalls must be dependent from future macroeconomic outcomes e.g.. unemployment rates, GDP, benchmark interest rate, inflation and technology.

STRATEGIC CHALLENGES

• The need to identify suitable measures to reduce the size of impairment provisions and P&L volatility.

• Handling the expected reduction of the equity ratio due to initial application effects

• Review of the product catalogue and ensuring competitiveness

• Audit assurance for the applied methods or simplifications

• Consistency of methods compared to other areas such as risk or regulatory

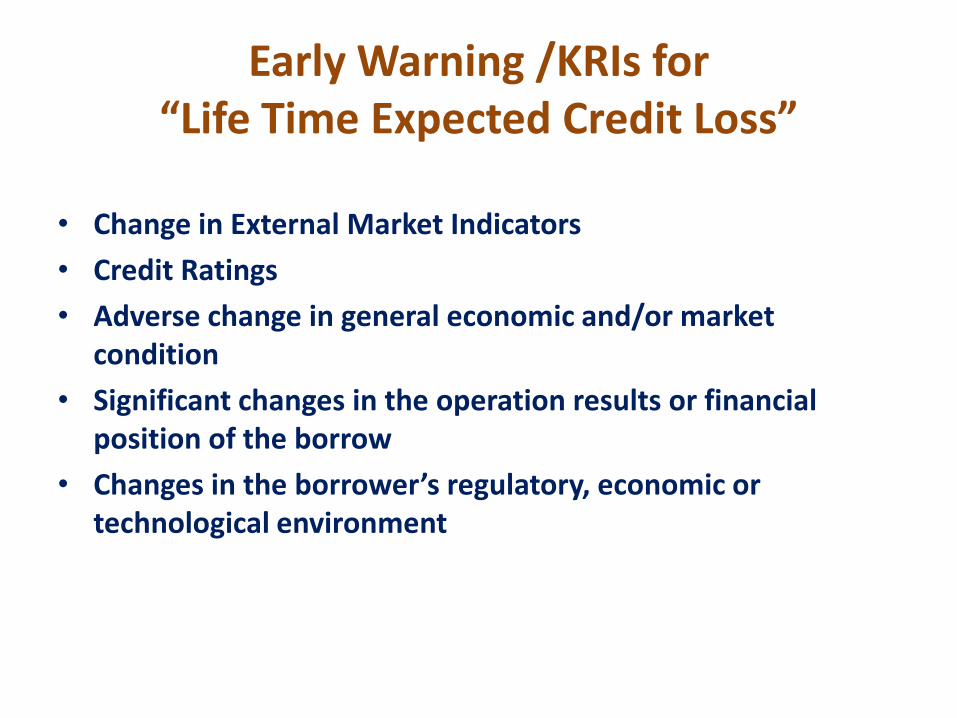

Early Warning /KRIs for “Life Time Expected Credit Loss”

• Change in External Market Indicators

• Credit Ratings

• Adverse change in general economic and/or market condition

• Significant changes in the operation results or financial position of the borrow

• Changes in the borrower’s regulatory, economic or technological environment

Early Warning /KRIs for “Life Time Expected Credit Loss

• Change in the value of collateral or guarantees

• Expected or potential breaches of covenants

• Changes in the expected behavior of the borrower and past due information

• Material documentation problems

• Inability to clean-up the facilities as per terms and conditions.

• Diversion of loan proceeds/Excessive inter-company lending(s)

Early Warning /KRIs for “Life Time Expected Credit Loss

• Industry-specific, economic, and/or political problems, affecting the obligor’s performance

• Significant declining revenues / profitability • Severe liquidity crunch or cash flow or late payment of Interest/mark-up

/Installment due or considerable increase in days payable • Increase leverage and /or weakening net-worth • Concerns about the obligor’s management competence , emergence of

succession risk • An inability to obtain current financial information

Early Warning /KRIs for “Life Time Expected Credit Loss

• Exhibit of adverse trend in sales and cost of good sold

• Significant increase in receivable and inventory build-up with decline sales

• Negative cash flow from operations during last two years

• No movement/slow movement in pledged stocks

• Shortage in pledge Stock/margin or pilferage or unauthorized stock lifting.

• Dispute among the sponsors/partners

Early Warning /KRIs for “Life Time Expected Credit Loss

• An actual or expected internal credit rating downgrade for the borrower or decrease in behavior scoring used to assess credit risk internally

• A significant credit determination on the other financial instruments of the same borrower

• A Significant change in the borrower’s ability to meet its debt obligations, such as a decline in the demand for borrower’s sales product because of shift in technology

• A Significant expected reduction of the borrower’s economic incentive to make scheduled contractual payments.

• Contractual payments are more than 30 days past-due information.

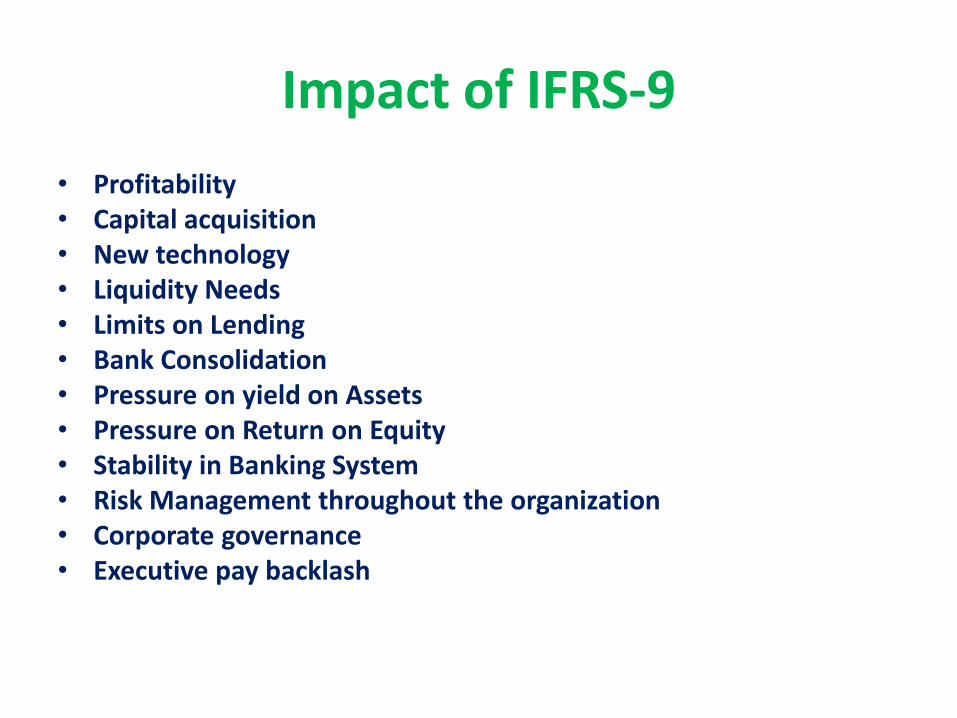

Impact of IFRS-9

• Profitability • Capital acquisition • New technology • Liquidity Needs • Limits on Lending • Bank Consolidation • Pressure on yield on Assets • Pressure on Return on Equity • Stability in Banking System • Risk Management throughout the organization • Corporate governance • Executive pay backlash

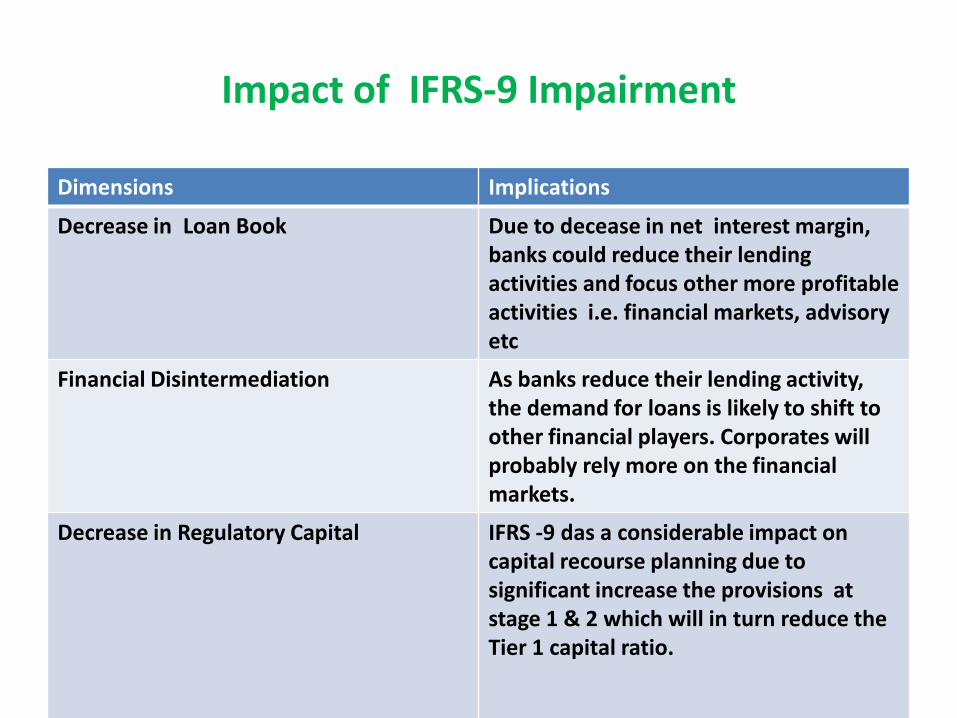

Impact of IFRS-9 Impairment

Dimensions Implications

Decrease in Loan Book Due to decease in net interest margin, banks could reduce their lending activities and focus other more profitable activities i.e. financial markets, advisory etc

Financial Disintermediation As banks reduce their lending activity, the demand for loans is likely to shift to other financial players. Corporates will probably rely more on the financial markets.

Decrease in Regulatory Capital IFRS -9 das a considerable impact on capital recourse planning due to significant increase the provisions at stage 1 & 2 which will in turn reduce the Tier 1 capital ratio.

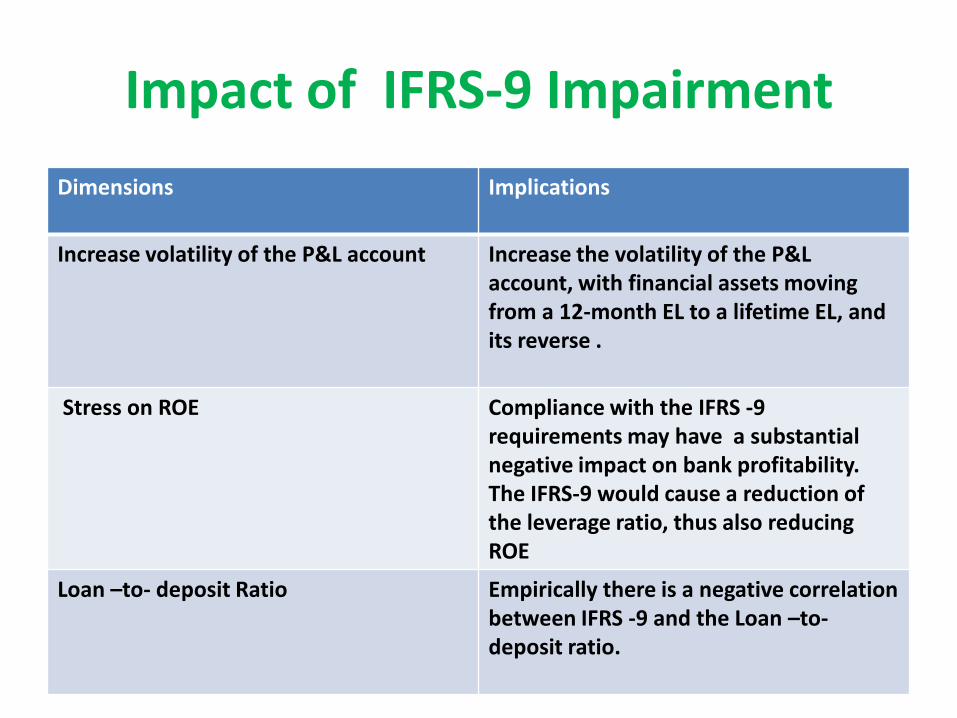

Impact of IFRS-9 Impairment

Dimensions

Implications

Increase volatility of the P&L account

Increase the volatility of the P&L account, with financial assets moving from a 12-month EL to a lifetime EL, and its reverse .

Stress on ROE Compliance with the IFRS -9 requirements may have a substantial negative impact on bank profitability. The IFRS-9 would cause a reduction of the leverage ratio, thus also reducing ROE

Loan –to- deposit Ratio

Empirically there is a negative correlation between IFRS -9 and the Loan –to- deposit ratio.

Impact of IFRS-9 Impairment :

Dimensions

Implications

Impact on GDP In order to meet the IFRS-9 , banks will will cause a reduction in profitability, which banks will tend to restore via an upward pressure on lending margin

Interbank lending and borrowing Both interbank lending and borrowings facility will also affect a bank’s IFRS-9 Implementation

Global banks

Global banks with lower capital buffer or higher leverage ratio and excessive structural funding mismatches were likely to fail.

Tuning of Basel II/III Credit Risk Models for IFRS 9

Factors Basel II IFRS 9

Time Horizon One year (for 12 moths) PD 12 months PD or Lifetime PD

Observation period Five years for retail exposure and seven years for corporate , bank and sovereign exposure

No specific

Statistical approach Hybrid of point-in-time to through-the –cycle to get the historical long-run average default rates

Point –in time

Default if obligor 90 days past due or earlier No specific definition, nut usually not beyond 90 days past due

Floor PD and LGD are subject to floors No floor prescribed

Expected Loss (EL) PD*LGD*EAD PD*PV of cash shortfalls (PD is 12 months or lifetime)

Conclusion

The banking sector must serve as a stabilizing force and not as an amplifier of the shocks. Challenge on delivering on the promise for the next decade – ‘think global and act local’ IFRS 9 implementation, is a journey not the destination, is a road not a end of the road.

29

30

Effective Management of IFRS 9 Credit Risk Modelling benefits the bank..

• Efficient allocation of capital to exploit different risk / reward pattern across business

• Better Product Pricing

• Early warning signals on potential events impacting business

• Reduced earnings Volatility

• Increased Shareholder Value

No Gain! No Risk …

To Summarise….

“We have no future because our present is too volatile. We have only risk management. The spinning of the given moment’s scenario. Pattern recognition.”

--- Willian Gibson

• References

• [1] “Basel III: A global regulatory framework for more resilent banks and banking systems,” Basel Committe on Banking Supervision, pub., Dec. 2010, (rev June 2011).

• [2] Edward Wyatt (December 20, 2011). “Fed Proposes New Capital Rules for Banks”, New York Times.

• [3] (July 21, 2010). “Dodd-Frank Wall Street Reform and Consumer Protection Act”, Public Law 111-203.

• [4] (December, 2012). “Commission Delegated Regulation (EU)”, No 149/20, Official Journal of the European Union, European Market Infrastructure Regulation (EMIR) Technical Standards.

• [5] J. Gregory, Counterparty Credit Risk and Credit Value Adjustment: A Continuing Challenge for Global Financial Markets, 2nd ed. Wiley, 2012.

• [6] S. H. Zhu and M. Pykhtin, “A guide to modeling counterparty credit risk,” in GARP Risk Review, Jul./Aug. 200