January 21, 2009 Investment Outlook 2009: How to position your Portfolio Robert J. Tilden, CFA, CMA,...

27

January 21, 2009 Investment Outlook 2009: How to position your Portfolio Robert J. Tilden, CFA, CMA, ICD.D Partner

-

Upload

scarlett-wilkerson -

Category

Documents

-

view

217 -

download

1

Transcript of January 21, 2009 Investment Outlook 2009: How to position your Portfolio Robert J. Tilden, CFA, CMA,...

January 21, 2009

Investment Outlook 2009: How to position

your Portfolio

Robert J. Tilden, CFA, CMA, ICD.D

Partner

2

Agenda

• Review of 2008 – How bad was it?

• Outlook for 2009

• Positioning your portfolio for 2009

• Jarislowsky Fraser Limited

3

Oil Versus the Canadian Dollar (1994 – 2008)

Source: Bloomberg

Oil Price vs. the Canadian Dollar (1994-2008)

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

Oct-94 Jul-96 Apr-98 Jan-00 Oct-01 Aug-03 May-05 Feb-07 Nov-08

US$

/C$

$10

$25

$40

$55

$70

$85

$100

$115

$130

$145

US$

per

Bar

rel

C$

Oil (US$)

4

Market Returns - Periods ending December 31, 2008

(%) Q4 6 Mths 1 Yr 5 Yrs 10 Yrs

S&P/TSX -22.7 -36.8 -33.0 4.2 5.3

S&P 500 (C$) -9.8 -14.0 -21.9 -3.2 -3.6

S&P 500 (US$) -21.9 -28.5 -37.0 -2.2 -1.4

DJIA (C$) -6.6 -7.0 -18.0 -4.5 -2.7

DJIA (US$) -19.1 -22.7 -33.8 -3.4 -0.5

MSCI EAFE (C$) -7.5 -23.5 -29.4 1.0 -1.1

MSCI EAFE (US$) -19.9 -36.3 -43.1 2.1 1.2

Shenzhen (US$) China -9.6 -29.7 -58.7 13.8 6.9

BSE Sensex (US$) India -27.2 -36.1 -61.0 10.8 10.7

EAFE Emerging Mkts (US$) -27.6 -47.0 -53.2 8.0 4.3

Dex Bond Universe 4.5 4.1 6.4 5.5 6.0

91 Day T-Bills 0.7 1.5 3.3 3.3 3.7

C$/US$ -13.5 -16.8 -19.3 1.1 2.3

Converted to Canadian funds using Bank of Canada noon rates.

Returns are annualized for periods greather than 1 year.

55

Market Return Comparison

27.4

13.3

8.5

11.6

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

S&P/TSX S&P 500 MSCI EAFE MSCI World

Market Performance

(Periods Ending December 31, 2008)

GICS Energy Sector Weights by Market

as at December 31, 2008

S&P/TSX C$ S&P 500 C$ MSCI EAFE C$RUSSELL 2000 C$SCM BOND UNIVERSE C$

S&P 500 U.S.$MSCI EAFE U.S.$RUSSELL 2000 U.S.$

1 Year 4 Year

(%

)

66

S&P/TSX Sector Returns

Index IndexWeightings 1 Year Weightings 3 Months

(%) (%) (%) (%)

Consumer Staples 3.4 -6.1 Consumer Staples 3.4 3.3Utilities 1.9 -20.5 Utilities 1.9 -6.6

Telecommunication Services 6.0 -24.9 Health Care 0.4 -10.7

Industrials 6.1 -25.1 Consumer Discretionary 4.7 -12.2Materials 17.6 -26.5 Materials 17.6 -12.3

Health Care 0.4 -30.2 Telecommunication Services 6.0 -12.7

Industrials 6.1 -15.3S&P/TSX -33.0

S&P/TSX -22.7

Energy 27.4 -33.9Consumer Discretionary 4.7 -35.4 Energy 27.4 -27.2Financial Services 29.2 -36.5 Information Technology 3.3 -27.2

Information Technology 3.3 -54.2 Financial Services 29.2 -29.9

Bold type indicates sectors where JF was overweighted

Cyclical Sectors: 37.7 of index

For the periods ended December 31, 2008

7

S&P 500 Sector Returns

Index Index

Weightings 1 Year Weightings 3 Months

(%) (%) (%) (%)

Consumer Staples 12.9 5.8 Telecommunication Services 3.8 14.3

Health Care 14.8 -3.5 Utilities 4.2 3.3

Utilities 4.2 -11.2 Health Care 14.8 1.9Telecommunication Services 3.8 -13.1 Consumer Staples 12.9 1.0Consumer Discretionary 8.4 -16.8 Energy 13.3 -8.0

Energy 13.3 -18.5

S&P 500 -9.5S&P 500 -21.2

Consumer Discretionary 8.4 -10.6

Industrials 11.1 -24.9 Industrials 11.1 -11.8

Information Technology 15.3 -28.9 Information Technology 15.3 -13.9

Materials 2.9 -32.0 Materials 2.9 -19.8

Financial Services 13.3 -44.1 Financial Services 13.3 -26.9

Bold type indicates sectors where JF was overweighted

Canadian dollar sector returns have been calculated using the London 4pm rate.

Cyclical sectors: 41.5% of index

For the periods ended December 31, 2008 ($C)

8

MSCI EAFE Sector Returns

Index Index

Weightings 1 Year Weightings 3 Months(%) (%) (%) (%)

Health Care 9.8 1.9 Telecommunication Services 7.0 12.3Utilities 7.7 -9.8 Health Care 9.8 6.8Consumer Staples 10.3 -13.6 Utilities 7.7 6.1

Telecommunication Services 7.0 -15.0 Consumer Staples 10.3 0.5

Energy 8.5 -22.2 Energy 8.5 -1.3Industrials 11.5 -4.9

MSCI EAFE -28.8 Information Technology 5.1 -6.1

Industrials 11.5 -30.3 MSCI EAFE -7.0Information Technology 5.1 -30.8Consumer Discretionary 9.6 -31.4 Consumer Discretionary 9.6 -8.3

Materials 7.8 -40.9 Materials 7.8 -14.7

Financial Services 22.6 -43.5 Financial Services 22.6 -21.4

Bold type indicates sectors where JF was overweighted

Canadian dollar sector returns have been calcualted using the London 4pm rate.

Cyclical Sectors: 41.1% of index

For the periods ended December 31, 2008 ($C)

9

Bond Portfolio

• Continued turmoil in financial markets sparked a crisis of confidence in credit markets, effectively freezing them.

• Credit spreads widened to historic highs

• As liquidity and rationality return to credit markets, spreads should narrow, leading the portfolio to outperform

Q4/08 1 Year

(%) (%)

Universe 4.5 6.4

Federal Bonds 7.4 11.5

Provincial Bonds 5.1 5.3

Corporate Bonds -0.3 0.2

DEX Bond Universe Returns to December 31, 2008

10

Bond Portfolio Analysis - Performance

For the Quarter Ended December 31, 2008

4.3 4.3

5.2

4.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

(%)

Short

Term

Mid-Term Long Term DEX

Universe

8.6

7.0

2.7

6.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

(%)

Short Term Mid-Term Long Term DEX

Universe

For the Year Ended December 31, 2008

11

Mid Corporate Spread Widening

Source: PC Bond

12

Equity Valuations

Source: Bloomberg (as of January 12, 2009)

One Year Forward Price/Earnings Ratios One Year Forward Earnings Yield as a % of 10 Year Gov’t Yields

Russia

FranceGermany UKCanada India Mexico US

Japan

AustraliaChina

0

2

4

6

8

10

12

14

16

18

Nominal versus Real Yield on 10 Year Government Bonds

CanadaChinaFrance GermanyUS

JapanMexicoAustraliaUKIndia

Russia-6

-4

-2

0

2

4

6

8

10

Nom Yield Real Yield

JapanUS

ChinaGermanyCanada

UKFrance

RussiaAustralia

MexicoIndia

0

100

200

300

400

500

S&P 500 One Year Forward Operating Earnings Yield from IBES as a % of 10 Year Treasury Bond Yields

The 'Fed Model' JAN 2009

400

350

300

250

200

150

100

5082 84 86 88 90 92 94 96 98 00 02 04 06 08 10

Average

+1 Dev

-1 Dev

331.9

13

Equities Relative to Bonds

• The stock market declines of 2008 have created extremely attractive buying opportunities

• Monetary inflation remains a problem for the long term

• Major credit markets are quite disrupted and a return to more fluid credit markets will take time to orchestrate

14

Factors Affecting 2008 Performance

• Global economy moves from growth to slower growth/recession

• Growth constrained by liquidity crisis – bank lending constrained

• Negative returns in all equity categoriesBest Worst

Non Cyclical Sectors Emerging MarketsConsumer Cyclical

SectorsHealthcare Resources

• Spread widening continues in bond market

• Outstanding Issues• Recession – How long? How deep?• Consequences of massive liquidity injection for inflation – currencies• New Rules and Regulations

Portfolio holds no sub prime mortgage or asset backed securities

15

Investment Outlook … 2009

Economic Review

Investment Outlook

• The global economies are entrenched in a recession brought on by an over levered economy.

• A liquidity crisis (lack of lending) is exacerbating an already difficult recession.

• Unprecedented fiscal and monetary policy stimuli are being applied.

• Yields on government bonds are very low. Shorter term, high quality corporate bonds are preferred.

• Stocks are attractively valued and provide the best return potential in the coming years.

• Lower risk, higher dividend paying stocks in non-cyclical areas such as Health Care and Consumer Staples are preferred given uncertainty with regard to the length of the recession.

16

Consumer Credit and Mortgage DebtAs Percent of Disposable Income

Shaded Areas Represent U.S. Economic Recessions

130 130

120 120

110 110

100 100

90 90

80 80

70 70

60 60

50 501970 1975 1980 1985 1990 1995 2000 2005 2010

CanadaU.S. 126.3

123.1

Consumer Savings RateCanada( ) and U.S. ( )

Shaded Areas Represent Canadian Economic Recessions

NOV 2008

25 25

20 20

15 15

10 10

5 5

0 0

-5 -51970 1975 1980 1985 1990 1995 2000 2005

2.13.0

Economic Charts

Source: TD Securities

17

U.S. Single Family Housing StartsPer 1000 Population

Shaded Areas Represent U.S. Housing RecessionsM884 NOV 2008

7 7

6 6

5 5

4 4

3 3

2 2

1 11965 1970 1975 1980 1985 1990 1995 2000 2005 2010

1.44

Economic Charts

Source: TD Securities

18

U.S. Single-Family Housing StartsThousands

Shaded Areas Represent U.S. Economic RecessionsM10 NOV 2008

2000 2000

1800 1800

1600 1600

1400 1400

1200 1200

1000 1000

800 800

600 600

400 40082 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

12 Month Average

-46.0% Yr/Yr

Economic Charts

Source: TD Securities

19

Economic Charts

Source: TD Securities

Twelve Month Forward Real GDP GrowthConsensus Economics Survey

GDP aggregated using current exchange ratesM154 OCT 2008

6 6

5 5

4 4

3 3

2 2

1 1

0 0

-1 -193 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

North AmericaWestern EuropeAsia PacificLatin AmericaWorld

-0.200.02

3.57

2.98

1.35

20

Economic Charts

Source: TD Securities

Global InflationYear over Year %Change in CPI

M627 NOV 2008

6 6

5 5

4 4

3 3

2 2

1 1

0 0

-1 -1

-2 -297 98 99 00 01 02 03 04 05 06 07 08 09 10

Canada

U.S.

JapanGermany

U.K.

21

Economic Charts

U.S. Consumer In Global Perspective(percent share of Global GDP: 2007)

Source: Bureau of Economic Statistics, IMF, Merrill Lynch

2.6

3.9

4.7

5.2

6.1

6.1

8.1

18.2

0 5 10 15 20

Canada

Italy

France

U.K.

Germany

China

Japan

U.S. Consumer

22

Price-Earnings MultiplesBased On Trailing Operating Earnings

M968 JAN 2009

35 35

30 30

25 25

20 20

15 15

10 10

5 582 84 86 88 90 92 94 96 98 00 02 04 06 08 10

TSXS&P 500

9.8

12.8

Source: Citigroup

Note: Valuations reflecte the MSCI All Country World Index going back to 1995 and Citigroup estimates prior to that date

5

10

15

20

25

30

35

40

70 72 74 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

Global PE

Long Term Average

2000s Avg

1980s Avg1970s Avg

1990s Avg

5

10

15

20

25

30

35

40

Shaded Areas Represent Periods of Earnings Slumps

Price-Earnings MultiplesBased On Trailing Earnings

Source: TD Securities, Russell

Economic Charts

23

Portfolio Positioning for 2009

• Confirm your risk tolerance

• Ensure cash levels are sufficient to cover expenses for the next 2-3 years

• For fixed income (i.e. bonds) focus on short term, high quality corporate bonds as the yields on government bonds are very low.

• Stocks are attractively valued and should provide the best return potential in the coming years

• Ensure that your portfolio is properly diversified

• Three oil and two gas companies doesn’t count!

• Lower risk, higher dividend paying stocks in non-cyclical areas such as Health Care and Consumer Staples are preferred given uncertainty with regard to the length of the recession.

24

JFL Corporate Overview

• Jarislowsky Fraser Limited is a registered investment counseling firm, managing portfolios for clients in North America and Europe.

• The company was founded in 1955 as an investment research firm. In the 1960’s, the firm began to use this research material to counsel private investors and institutions.

• Our primary goal is growing capital for our clients in a low risk manner. Our firm is known for advocating shareholder rights and ensuring good corporate governance.

• Jarislowsky Fraser Limited is totally independent, with no corporate affiliations. The firm is owned by the partners.

25

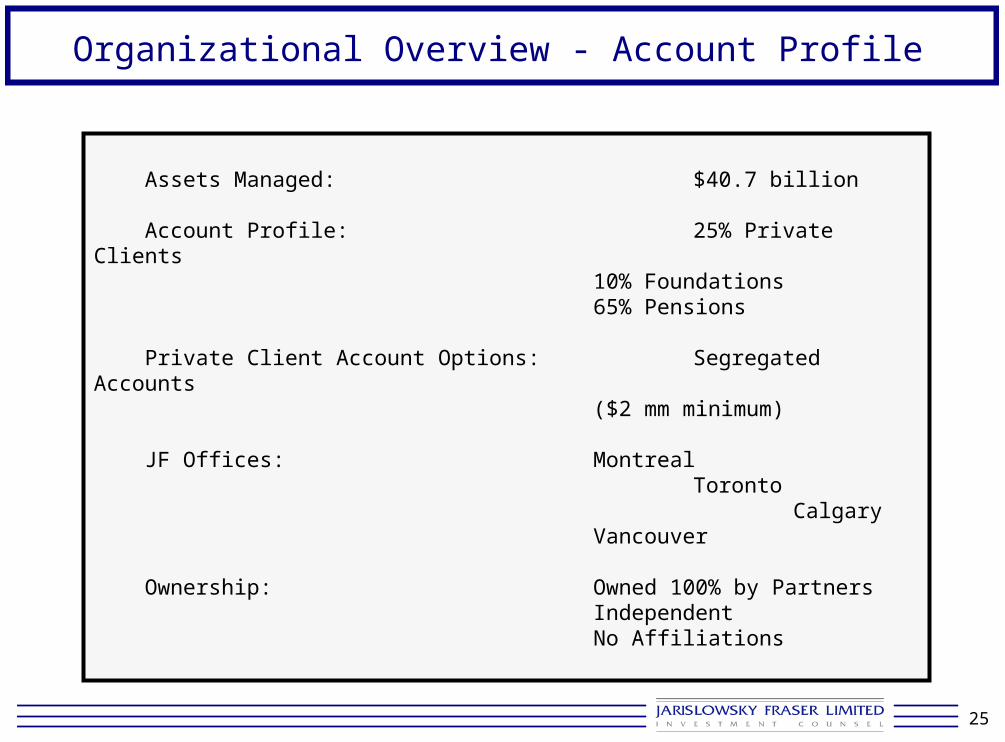

Assets Managed: $40.7 billion

Account Profile: 25% Private Clients 10% Foundations 65% Pensions

Private Client Account Options: Segregated Accounts ($2 mm minimum)

JF Offices: Montreal

Toronto Calgary

Vancouver

Ownership: Owned 100% by PartnersIndependent No Affiliations

Organizational Overview - Account Profile

26

Fee Schedule

First $ 5 Million .50 of 1%

Next $ 5 Million .35 of 1%

Next $ 15 Million .25 of 1%

Next $ 25 Million .20 of 1%

Next $ 50 Million .15 of 1%

Over $ 100 Million .10 of 1%

1. Excludes custodian fees and brokerage commissions2. JF fees are invoiced quarterly in advance, based on the ending

market value at the latest quarter end.

AmountFee Charged(Per Annum)

27

Contact Information

Calgary Office

Robert J. Tilden

Partner

Jarislowsky Fraser Limited

140 4th Avenue S.W.

Suite 1640

Calgary, Alberta

T2P 3N3

Telephone: (403) 233-9117

Fax: (403) 233-9144

Email: [email protected]