Jan 2014 Natural Gas Update

9

1 Energy Report Storage Report Emptying Fast … page 5 Natural Gas Edition BC Energy Update Protect yourself next winter page 9 Natural Gas Spikes Why all the elements were there…page 3 Volume 1 Issue 1 January 2014 Long Term Outlook page 7

-

Upload

cascadiaenergy -

Category

Documents

-

view

218 -

download

3

description

Cascadia Energy , British Columbia

Transcript of Jan 2014 Natural Gas Update

1

Energy Report

Storage Report Emptying Fast … page 5

Natural Gas Edition

BC Energy Update

Why all the elements were there…

Protect yourself next winter

page 9

Natural Gas Spikes

Why all the elements were there…page 3

Volume 1 Issue 1 January 2014

Long Term Outlook page 7

2

energy report

Cascadia Energy Ltd.

Head Office

Suite 201 720 Beatty Str

Vancouver BC V6B 2M1

604-687-6663

Vancouver Island

#306 - 1095 Mckenzie Dr

Victoria BC V8P 2L5

250-704-4443

www.cascadiaenergy.ca

Nick Caumanns

604-961-8707

Steve Connelly

604-315-7009

Tom Barnes

250-704-4443

It’s hard to argue that natural gas is a great form of energy. It

burns easily and cleanly. It’s relatively abundant and easy to find

and release. It is also quite easy to transport, to move from place

to place, reasonably cheaply.

The resurgence in natural gas has been a dream from many.

Environmentalists love the carbon reductions. End users like the

low costs and clean easy combustion. Everyone likes that they can

get it piped to virtually anywhere they need.

Not all, however is rosy. Production, once a well has been

tapped, is reasonably steady, declining over time as the pressure

drops. For the same reason, you can’t just crank up the delivery of

natural gas at will so when we need more of it, such as in winter, it

has to come from somewhere.

That somewhere is usually a storage facility, underground or

LNG, or from increased deliveries through fixed diameter pipelines.

We all know what happens when high demand, limited availability,

and an open market place intersect.

If you didn’t, you probably found out this December. We

have, after years of a supply glut, a sudden resurgence of volatility.

Will it last? That depends on storage, new demand, production

restrictions, and other variables.

We’ll touch on some of those in this issue. We hope it’s

useful.

Nick Caumanns

Opening Note…

What’s with the cover photo?

Cascadia Energy Ltd. serves numerous greenhouse clients throughout BC. January is the

month of the big agricultural show in Abbotsford and, not least, greenhouses are large

consumers of natural gas. After all, if you live in a glass house you’d expect your gass bills to

be of concern. You could say that flowers are made of natural gas.

3

Low Temps,

High Prices

The intense volatility of natural gas

prices was on full display last

month with weather, exchange

rates and supply restrictions

combining to drive prices skyward

for BC customers.

While for now January prices

appear to be coming back to earth,

last month got off to a brutal start

with a rare yet wicked weather event

that gripped much of eastern Canada

and the US with record low

temperatures.

The so-called polar vortex

clamped down on much of eastern

Canada and the US placing heavy

burdens on storage draws as

consumers on both sides of the

border cranked up the heat to stay

warm or keep their businesses up and

running.

According to the US Energy

Information Association, 285 billion

cubic feet of gas was taken from

storage for the week of December

13—the largest withdrawal since

record keeping began in 1994. As a

consequence the Henry Hub

benchmark rose 60 cents higher than

the previous month. In BC similar

pressure was placed on reserves

triggering a decline in liquidity at

Sumas causing significant price

increases.

The unusually cold weather

continued to keep prices elevated

through the balance of the month

and early into the new year.

However, some analysts say that

even with more sub-zero

temperatures on the horizon for the

coming weeks the wild price spikes

that closed 2013 likely won’t

continue.

“Preceding the record high gas demand and prices during the polar vortex was an early start to winter, eight major winter storms resulting in multi-year high prices,” said Samantha Santa Maria from Platts, a

4

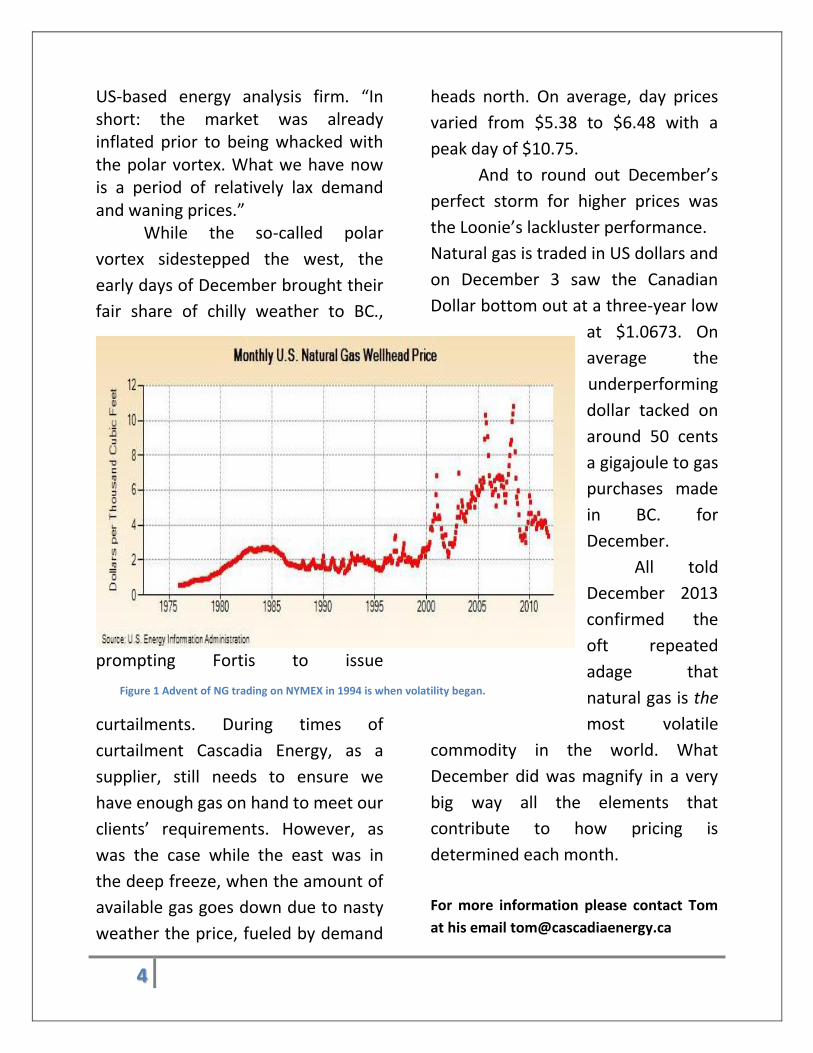

US-based energy analysis firm. “In short: the market was already inflated prior to being whacked with the polar vortex. What we have now is a period of relatively lax demand and waning prices.”

While the so-called polar

vortex sidestepped the west, the

early days of December brought their

fair share of chilly weather to BC.,

prompting Fortis to issue

curtailments. During times of

curtailment Cascadia Energy, as a

supplier, still needs to ensure we

have enough gas on hand to meet our

clients’ requirements. However, as

was the case while the east was in

the deep freeze, when the amount of

available gas goes down due to nasty

weather the price, fueled by demand

heads north. On average, day prices

varied from $5.38 to $6.48 with a

peak day of $10.75.

And to round out December’s

perfect storm for higher prices was

the Loonie’s lackluster performance.

Natural gas is traded in US dollars and

on December 3 saw the Canadian

Dollar bottom out at a three-year low

at $1.0673. On

average the

underperforming

dollar tacked on

around 50 cents

a gigajoule to gas

purchases made

in BC. for

December.

All told

December 2013

confirmed the

oft repeated

adage that

natural gas is the

most volatile

commodity in the world. What

December did was magnify in a very

big way all the elements that

contribute to how pricing is

determined each month.

For more information please contact Tom

at his email [email protected]

Figure 1 Advent of NG trading on NYMEX in 1994 is when volatility began.

5

What Storage

Means for

Prices

The extreme cold throughout

North America has begun to take a

toll on levels of underground

natural gas storage, drawing levels

lower than they have been for

years.

While it continues to be true

that the fundamentals for natural gas

look good, drilling, deliveries,

demand, etc, there is no doubt that

the market has responded to the

extreme weather with strong upward

price signals.

Although this says something

about supply and demand, it tells us

more about the nature of gas

marketing and trading. Prices go

down reluctantly, as they have over

the past few years in the face of

enormous new supplies coming to

the market, but at the sign of any, no

matter how seemingly short, crisis

6

prices tend to spike up and linger.

Of course a market driven by

speculative price setting mechanisms

will tend to factor in speculation and

in our current market the psychology

of betting on higher prices attracts

more activity than the other way

around.

We are now below the bottom

of the 5 year storage range. While

this in itself is somewhat

meaningless, it has an impact in how

traders approach the market.

Low spring storage levels imply

that there will be summer demand

for gas, which will tend to drive the

summer forward price upwards. On

the other hand, early storage refill

tends to make futures prices for the

next winter lower later on in the

summer.

Last spring we had normal

storage levels but, because of a small

difference between the spot price,

the rate the gas is put in, and the

future winter price, the price at which

gas would be taken out storage, refill

was slow early in the summer. This

resulted in low late summer storage

and high winter futures prices.

Given our current position in

terms of storage it is likely that we

will see strong summer pricing from

here on. That could mean storage

will refill quickly and possibly depress

winter prices in the back half of

summer.

All said though, there are so

many variables that the outcomes are

too unsure to predict. One thing is

certain, prices will likely stay strong

right through the spring and summer.

Figure 2 Sumas Day Price $ US before conversion @ $1.08

7

In the longer term…

While no one knows where prices will go in the next day, never mind the next

30 years, there are some long-term projections out there. They try to account for

long-term resources and demand estimates to see if we will either “run out” or

“be awash” in natural gas. It seems, from reading all of the reports, that over the

lonhg haul we will stay in good supply/demand balance and, as a result, no major

long-term price upheavals.

Prices in 2013, even barring the December anomaly, have been higher than 2012.

The price increases in the near term are due to growth of consumption in the

industrial and electric power sectors and growing demand for export at LNG

facilities. It is expected that 2014 onwards we will see a sustained increase in

production, which should lead to slower price growth over the longer term.

The U.S Energy information administration projects that the Henry Hub spot

natural gas will reach reache $4.80 in 2018, which is still less than 80 cents higher

than in 2013. The stronger near-term price growth is followed by an increase in

supply eventually causing prices to settle at $4.50 in 2020, which, while higher

than 2013, represents about a 10% shift over 7 years, hardly reason for worry.

After 2020, the EIA expects that increases in natural gas spot prices will be driven

by continued but slower growth in U.S. demand and exports to reach $7.65 in

2040, an increase of just iver $3.00 from 2020, but again covering quite a long

period of 20 years.

Regional spot price projections will follow the same general pattern as the Henry

Hub spot price. While this projection is for the US, it is generally understood that

the prices for Canadian gas will track quite closely to this.

None of this means that we won’t experience periods when prices are high due

to interim weather, political, or other factors but it does show an underlying

long term confidence in natural gas from the US government.

8

Market Overview

9

Fix Your Future

While one month of high prices

should not drive our behaviour, if

that event provides some new

information we shoud pay attention

to what it teaches.

The major factor that has changed

from the past few years duing which

we enjoyed low prices at Sumas

despite cold weather events is the

amount of freely available gas at the

Sumas market point. This is referred

to as liquidity.

Over the past few years producers

have slowly let their long-term

capacity from northern BC to the

lower mainland lapse. They then have

the option of shipping gas either

south or east based on price, without

having the sunk cost of a take or pay

pipeline contract. The gas then flows

on “IT” or interruptible transport

contracts.

Since IT contracts are less secure than

firm producers supplying gas at

Sumas who have “must supply”

contracts end up bidding for

increasingly shrinking supplies of

guaranteed firm gas. That of course

drives up the price for them but

what’s the real shame is that it drives

up the index, the price paid by

everyone else for their gas.

The simple analogy is that upon

booking a hotel room, you find there

is a convention in town and, even

though you booked a room, your

room rate will depend upon what

they charge the person getting the

last room. It’s likely to be a much

higher rate.

Going forward we would

recommend that clients always fix

winter pricing for at least 50% of

their volume. This should protect

against unreasonable price spikes

while allowing some opportunity to

participate in variable pricing should

the market remain soft during

warmer weather.