Jakarta Market Report 2010 - Colliers

29

COLLIERS INTERNATIONAL | JAKARTA Property Market Overview www.colliers.co.id MARKET OVERVIEW | MARCH | 2010 Our Knowledge is your Property INDONESIAN ECONOMIC INDICATOR 2005 2006 2007 2008 2009 Economic Growth (% YoY) 5.70 5.50 6.30 6.10 4.50 Inflation Rate (%) 17.11 6.60 6.59 11.06 2.78 1 Exchange Rate (Rp/US$) 9,695 8,980 9,124 9,672 10,325 1 Interest Rate - Central Bank Rate (%) 12.75 9.75 8.00 9.25 6.50 2 ECONOMIC INDICATORS Source: Statistics Indonesia, Finance Department, Bank Indonesia Notes: 1 January - December 2009 2 December 2009

-

Upload

endrohierarki -

Category

Documents

-

view

550 -

download

8

Transcript of Jakarta Market Report 2010 - Colliers

c o l l i e r s i n t e r n at i o n a l | J a K a rta

Property Market overview

www.colliers.co.id

M a r K e t oV e rV i e W | M a r c H | 2 0 1 0

Our Knowledge is your Property

INDONESIAN ECONOMIC INDICATOR

2005 2006 2007 2008 2009

economic Growth (% YoY) 5.70 5.50 6.30 6.10 4.50

inflation rate (%) 17.11 6.60 6.59 11.06 2.781

exchange rate (rp/Us$) 9,695 8,980 9,124 9,672 10,3251

interest rate - central Bank rate (%) 12.75 9.75 8.00 9.25 6.502

econoMic inDicators

Source: Statistics Indonesia, Finance Department, Bank Indonesia

Notes:1 January - December 2009 2 December 2009

colliers international2

The Knowledge Report | March | 2010 | Quarterly Research Report

BUilDinG naMe location eXPecteD coMPletion

in the CBD area

Bakrie tower rasuna said 2010

Menara Bidakara 2 Gatot subroto 2010

Graha 18 scBD 2010

equity tower scBD 2010

the oval (the office @Kuningan city) satrio 2011

sentral senayan 3 asia afrika 2011

eighty8 Kasablanka 2011

Menara allianz Kuningan 2011

tempo scan tower rasuna said 2011

ciputra office tower satrio 2012

office 8 senopati 2012

Wtc 2 sudirman 2012

in the outside CBD area

Grand Kebon sirih Kebon sirih 2010

Menara MtH Mt Haryono 2010

Kem tower Kemayoran 2010

central office Park s. Parman 2011

Gandaria 8 Gandaria 2011

Menara 165 tB simatupang 2011

Mt Haryono square cawang 2011

sovereign Plaza tB simatupang 2012

total space 782,830 sq m

list oF oFFice BUilDinGs UnDer constrUction

Source: Colliers International Indonesia - Research Department

Of all new buildings projected for the whole of 2009, only Bakrie Tower postponed opera-tion and will likely enter around March 2010; while Equity Tower, which was previously expected to finish in 2011, made speedy con-struction progress and will likely start operat-ing in May 2010. Therefore, the projection of office space in 2010, previously only two buildings (Menara Bidakara 2 dan Graha 18) is now four buildings (including the above-mentioned), adjusting the total supply from 64,000 to 210,800 sq m.

Thus, during 4Q2009, only Cyber 2 (located on Jalan HR Rasuna Said) was officially in op-eration. Cyber 2 was partly offered as strata-title office for sale and office space for lease.

Adding around 53,600 sq m, Cyber 2 brought 2009 annual supply to 281,140 sq m, or 53% higher than the total annual supply of 2008. All in all, the CBD now has a total of around 4.05 million sq m of office space.

Outside the CBD area, the office market did not register any new buildings. With no addi-tional stock within the area, cumulative sup-ply in this area hovered at around 1.66 mil-lion sq m. This year we shall see several office buildings placed in the market. Unlike supply in 2009, where only two buildings, totaling around 23,800 sq m, were the only supply, supply projection for 2010 would be around 121,000 sq m from six buildings.

oFFice sector

sUPPlY

colliers international 3

The Knowledge Report | March | 2010 | Quarterly Research Report

With around 281,140 sq m of office space entering during the whole of 2009, the YoY occupancy rate from 2008 to 2009 fell some-what, from 90.3% to 87.1% in the CBD area. The determinant factor in declining oc-cupancy level was not just significant supply but also the financial crisis early in the year, which impacted the pace of inquiries for office space. However, as mentioned in our previous report, the office market had begun to move forward from the third quarter of 2009. De-spite the slow growth, signs of recovery have become clear and will likely continue during 2010. Other than a sound economic perfor-mance, a smaller supply projection for the whole of 2010 could be the catalyst to balance supply and demand.

Meanwhile, the QoQ occupancy level moved only marginally, from 87.2% to 87.1%.

During the last quarter 2009, Cyber 2 has secured big tenants, such as Northstar Pa-cific, Marquee Executive Offices and Danone, totalling almost 25,000 sq m (not including other smaller tenants). With all the early pre-commitments, the commitment level of this building has reached more than 80%. Other buildings which were projected to complete this year have also registered high pre-com-mitment levels; in The Plaza, for example, a new building coming into operation during the “financial crisis” has secured significant transactions of around 5,000 sq m each by BMW and Sime Darby. During the reviewed

quarter itself, The Plaza has handed over more than 12,000 sq m to several companies. The resurrection of the office market was further seen in the acquisition of three major deals in Sental Senayan II. Other smaller transactions also emphasized that this sector is beginning to move forward.

With offices for sale, new strata-title office buildings have shown a sound performance. Bakrie Tower will be mostly occupied by tenants from their own group, while Equity Tower has secured a high pre-commitment level before really in operation.

From a business line perspective, the quarter’s active lessees include industries like banking, insurance and others. Our records show that most transactions were predominantly small- to medium-sized deals.

A similar trend was also seen in the outer CBD area, where occupancy levels shifted up moderately, by less than 1%, to 87.8%. Compared to the occupancy level at the year’s end, the YoY occupancy rate posed a posi-tive trend, moving from 86% in 2008. In this quarter, transactions in the non-CBD area were mostly due to the expansion of existing tenants. We also noticed the continuing relo-cation of big tenants, who decided to consoli-date their several office locations. In general, we did not notice a significant movement of tenants during the quarter and this helped maintain the current occupancy level.

DeManD

70%

75%

80%

85%

90%

95%

100%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2002 2003 2004 2005 2006 2007 2008 2009P 2010P 2011P 2012P

Demand Supply Occupancy Rate

cBD oFFice: cUMUlatiVe sUPPlY, DeManD anD occUPancY rate

Source: Colliers International Indonesia - Research Department

colliers international4

The Knowledge Report | March | 2010 | Quarterly Research Report

Source: Colliers International Indonesia - Research Department

While occupancy trends slightly declined, ask-ing rental rates by contrast posed a strength-ening YoY trend of 7%, while the QoQ trend recorded a 3% increase from Rp92,988/sq m/month previously to Rp95,611/sq m/month. The upward trend was mostly triggered by buildings which had just finished renovations and wanted to compete with newer build-ings in the neighbourhood. Most of the cases where rental rates were adjusted were due to management policy. Further, the influx of new buildings with high occupancy levels has also contributed to the increase in overall asking rental rates.

In the U.S. dollar-denominated buildings, the average asking rental rate remained the same as in the previous quarter. All buildings with US$ rents continued to maintain prices at the same level from quarter to quarter.

In the outer CBD area, no significant changes were made during the reviewed quarter and the average asking rental rates remained rela-tively flat, at Rp67,895/sq m/month. Likewise, average asking rental rates for U.S. dollar-de-nominated buildings did not change substan-tially, staying at US$11.94/sq m/month.

asKinG rental rates

serVice cHarGesAverage service charge for building in the CBD has increased only slightly, from Rp49,523 to Rp50,057/sq m/month. For some landlords who applied service charges adjustment in the quarter, the main reason was largely major refurbishment work, such as upgrading public equipment and facili-ties. On the other hand, buildings with U.S. dollar charges registered no change in the

maintenance tariff and maintained at around US$5.98/sq m/month.

The overall service charge tariff in the outer CBD area rose to Rp35,024, up by 2% com-pared to the previous quarter. Likewise, the average service charge cost in this area hov-ered at around US$4.66/sq m/month.

$10.37 $11.37 $12.37 $13.37 $14.37 $15.37 $16.37 $17.37 $18.37 $19.37 $20.37 $21.37 $22.37 $23.37

Rp0Rp10,000Rp20,000Rp30,000Rp40,000Rp50,000Rp60,000Rp70,000Rp80,000Rp90,000

Rp100,000Rp110,000Rp120,000Rp130,000Rp140,000

2004 2005 2006 2007 2008 2009

Rupiah US$

aVeraGe Gross rent annUallY

colliers international 5

The Knowledge Report | March | 2010 | Quarterly Research Report

The office sector will move forward, largely due to expectations of positive economic growth. For some periods we have found that economic growth has shown very strong cor-relation with the growth of the office sector, particularly in the rental and occupancy rates. This has been further emphasized by some indications such as continued higher office space absorption and controlled rental level resulting from space inquiries. Further to that, the relatively “in control” supply projection for 2010 will help regulate the balance be-tween supply and demand.

We anticipate that the pattern of office oc-cupiers will be similar to those in the previous period, when office leasing was dominated by small to medium transactions. In 2010 we still expect more companies to vacate older build-ings and relocate to newer buildings. This pat-tern would help buildings under construction or even those at the planning stage to secure pre-commitment level before being actually in operation.

In the period ahead, it is likely that asking rental rates would continue a positive trend. This will largely be contributed by relatively new buildings with decreasing vacancy rates.

oUtlooK

colliers international6

The Knowledge Report | March | 2010 | Quarterly Research Report

Shadowed by the global economic crisis, the apartment market experienced slowing activi-ties in early 2009. Supply grew by only 1.2% in the first three months of the year as most property players held a ‘wait and see’ view. Nevertheless, the relatively stable country’s economic indicators warmed up the develop-ers’ machine to continue developing their property in the remaining quarter of 2009. Tougher and tighter condition during the

year made apartment stock grow modestly by 13.4% y-o-y, with around 9,028 new ad-ditional units from a total of 14 projects, as compared to the previous year, when around 9,900 units entered the market from a total of 20 projects. One rusunami project of Me-nara Cawang, providing 3,000 units and a large-scale project of Thamrin Residence with 1,100 units, contributed the most to 2009’s annual supply.

aPartMent sector

aPartMent strata-title For sale

sUPPlY

DeVeloPMent location reGion

Kuningan Place (infinia and Ultima tower) Jalan Kuningan Madya 2010

Permata Hijau residence Jalan letjen. supeno 2010

the Boulevard Jalan Fachrudin 2010

sahid sudirman residence Jalan Jend. sudirman 2010

Grand surya Pegadungan, Kalideres 2011

Maple Park Golf View (tower a) Jalan Danau sunter Barat 2011

regatta (3 tower) Jalan Pantai Mutiara 2011

thamrin residence (tower c, D, e) Jalan Hr rasuna said 2011

Keraton Hyatt residence Jalan MH thamrin 2011

Menara cawang Jalan sMa 14, cawang 2012

Kebagusan city (tower a) Jalan Baung 2012

Gardenia Boulevard Warung Buncit 2012

the lavande Jalan supomo 2010

Best Western Mangga Dua Jalan Mangga Dua abdad 2010

total 9,028 unit

list oF ProJects enterinG tHe MarKet in 2009

Source: Colliers International Indonesia - Research Department

The East Jakarta area received the largest an-nual supply in 2009 from the completion of the Menara Cawang (rusunami project) with total of around 3,000 units. The CBD and

South Jakarta also had significant additional units, with 2,234 and 1,984 units, respec-tively.

colliers international 7

The Knowledge Report | March | 2010 | Quarterly Research Report

cUMUlatiVe aPartMent sUPPlY

Source: Colliers International Indonesia - Research Department

In the last quarter of 2009 around 1,418 ad-ditional units were recorded from three newly completed projects, bringing cumulative supply to 76,338 units as at the end of 2009. Around 9% of total supply was classified as rusunami units (the abbreviation of rumah

susun milik or low-cost multi-family residence subsidized by the government). Based on mar-ket segmentation, middle-low class apartment units dominated the market by 46%. These classes are found largely in West, North and Central Jakarta area.

DistriBUtion oF aPartMent For strata-title sale BaseD on MarKet seGMentation

Source: Colliers International Indonesia - Research Department

Low24.1%

Middle Low45.5%

Middle Upper19.3%

Upper7.9%

Luxury3.2%

Unlike the previous year, when it dominated market activities, during 2009 rusunami devel-opment was sluggish. Many ambiguous factors related to government support on rusunami-subsidized schemes and its regulation had re-strained the acceleration of development pro-cess and thus rescheduled completion targets. With changes in the projection we anticipate that future supply would include quite a few

from rusunami projects and other apartment projects. If all projects meet their schedule, there will be around 27,795 new units project-ed to enter the market in 2010, with 55% of them classified as rusunami units. Further, in 2011, the market anticipates another 18,400 new units, 25% of them rusunami. Supply pro-jection in 2012 will ease, with only 959 new units and with no rusunami projects.

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

CBD Central Jakarta South Jakarta North Jakarta East Jakarta West Jakarta

Tot

al U

nit

Existing 2008 Annual 2009

colliers international8

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2005 2006 2007 2008 2009 2010(p) 2011(p) 2012(p)

Tot

al U

nit

The Knowledge Report | March | 2010 | Quarterly Research Report

Source: Colliers International Indonesia - Research Department

FUtUre aPartMent For strata-title sale ProJects BY MarKet seGMentation

cUMUlatiVe sUPPlY oF aPartMents For strata-title sale UP to 2012(P)

Source: Colliers International Indonesia - Research Department

If we remove rusunami units from the future supply list, a total of 27,331 units are predicted to enter the market up to 2012. Middle-upper and middle-lower classes will be dominating the composition of future units, with 39%

and 35%, respectively, followed by upper-class units, with 20%. Luxury and low-class units will be in the minority, with 4% and 2% of the total additional units.

WitH rUsUnaMi Units WitHoUt rUsUnaMi Units

Demand for apartment units in Jakarta is still dominated by the investor type of buyers, as this sector continues to offer interesting returns. A relatively increasing capital gain becomes a major attraction for investor buy-

ers. However, given the fact that only selected projects are considered to have potential investment return, the overall market still indicated a downturn in the take-up rate.

DeManD

0

1,000

2,000

3,000

4,000

5,000

6,000

CBD Central Jakarta

South Jakarta

North Jakarta

East Jakarta

West Jakarta

Tot

al U

nit

Low Middle-Low Middle-Up Upper Luxury

0

1,000

2,000

3,000

4,000

5,000

CBD Central Jakarta

South Jakarta

North Jakarta

East Jakarta

West Jakarta

Tot

al U

nit

Low Middle-Low Middle-Up Upper Luxury

colliers international 9

The Knowledge Report | March | 2010 | Quarterly Research Report

Source: Colliers International Indonesia - Research Department

Source: Colliers International Indonesia - Research Department

Low class apartment units continued to be the most absorbed segment in the market in 2009. These kinds of units are easily found in West, North, Central and East Jakarta, where take-up rate achieved 76.7%. Upper-class

units that are mostly found in the CBD and South Jakarta area also managed to record a high take-up rate of 76.0%. Other apartment classes, except for middle-upper class, reported healthy take-up rates of above 70.0%.

cUMUlatiVe sUPPlY anD taKe-UP rate oF aPartMent For strata-title sale

Our survey revealed that the average take-up rate as at the end of 2009 had minor incre-ments, to 71.6%, from the average of 69.9% in the previous year. This translates into the market having a total of 21,702 unsold units. As shown in the chart, take-up rate is predict-ed to decline to around 62% in 2010 in antici-pation of upcoming completion of more than 25,000 new apartment units in the market.

The CBD area remained the favorite location in the market for apartments and this has re-sulted in a high take-up rate of 78.6%. Sound take-up rate performance was also recorded in the area of South, North and West Jakarta, while other areas in Jakarta managed to see a take-up rate of around 60%.

taKe-UP rate oF aPartMents For strata-title sale

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

20,000

40,000

60,000

80,000

100,000

120,000

2005 2006 2007 2008 2009 2010(p)

Tak

e U

p R

ate

Tot

al U

nit

Cumulative Supply Take-Up Rate

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

CBD Central Jakarta South Jakarta North Jakarta East Jakarta West Jakarta

Num

ber

of U

nit

Total Unit Sold Unit

colliers international10

The Knowledge Report | March | 2010 | Quarterly Research Report

Source: Colliers International Indonesia - Research Department

aVeraGe Price Per sQUare Meter oF JaKarta aPartMents For strata-title sale

taKe-UP rate BaseD on MarKet seGMentations

Source: Colliers International Indonesia - Research Department

The apartment asking price experienced a slight increment of 4.8% YoY, to an average of Rp11.6 million/sq m, from Rp11.0 million/sq m in 2008.

Adding to its image as a high-end area, South Jakarta area, which comprised projects target-

ing middle-upper to luxury class, managed to achieve a 1.4% increment YoY, to an average of Rp11.5 million/sq m. Apartments in the non-CBD area also registered an increase of 1.3% YoY, to Rp8.6 million/sq m in 2009, while those in the CBD area were stable at Rp15.9 million/sq m.

During the year, developers continue to use marketing gimmicks as effective tools to sell their projects. Regardless of lowering unit prices, developers prefer to provide flexible payment schemes for potential buyers. It is now very common for many developers to lengthen the instalment period and offer low interest rates to win in the competitive market. Further, with such a flexible scheme, transacted prices could be discounted up to 35% from the published price.

The range of offering price in the market was very wide. Low-class units were offered at an average price of Rp5 million/sq m, while mid-dle-class units were offered at an average price of Rp8.7 million/sq m for middle-low class and Rp12.7 million/sq m for middle-upper class. Higher prices were offered by upper-class projects with an average of Rp18.4 million/sq m and luxury class at an average of Rp23.4 million/sq m.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Low Middle Low Middle Up Upper Luxury

Tak

e U

p R

ate

Market Segmentation

asKinG Price

Rp0

Rp2,000,000

Rp4,000,000

Rp6,000,000

Rp8,000,000

Rp10,000,000

Rp12,000,000

Rp14,000,000

Rp16,000,000

Rp18,000,000

2006 2007 2008 2009

Pri

ce/s

q m

CBD South Jakarta Non CBD Average

colliers international 11

The Knowledge Report | March | 2010 | Quarterly Research Report

In 2009, apartments for lease in Jakarta grew slowly. With the trend of leasing units from secondary strata title units, developing a new purely leased apartment became a non-favor-ite option. Concentrating demand on leasing apartments only in certain areas has limited new leased apartment projects.

Apartments for lease only saw one new proj-ect in 2009, from the operation of the third tower of Golf Pondok Indah Apartment in the first half of the year. This apartment proj-ect offered 166 units for lease (non-service) in Pondok Indah, South Jakarta’s elite area. Within the same period, the market also wit-nessed the transformation of Puri Denpasar

apartments into a hotel scheme, thus reducing the cumulative supply by 36 units. Also, with-out additional units in the second half of the year, the market grew by 1.7% YoY, providing a total of 7,835 leasing units up to the end of 2009. Only 52% of these were leasing units with service.

Our survey up to the end of the year noted two new leasing apartments to enter the market in 2010, and probably another three develop-ments in 2011. These projects would provide a total of 381 serviced apartment units. And, for the first time since 1998, West Jakarta area would have new units, at around 55% of the above future units.

Source: Colliers International Indonesia - Research Department

ranGe Price BaseD on MarKet seGMentations

aPartMent For lease sUPPlY

Source: Colliers International Indonesia - Research Department

Rp0

Rp5,000,000

Rp10,000,000

Rp15,000,000

Rp20,000,000

Rp25,000,000

Rp30,000,000

Low Middle Low Middle Up Upper Luxury

Pric

e/ s

q m

Market Segmentation

aPartMent For lease (serViceD anD non serViceD)

sUPPlY

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2005 2006 2007 2008 3Q09 2009(p) 2010(p) 2011(p)

Serviced Apartment Non-Serviced Apartment

colliers international12

The Knowledge Report | March | 2010 | Quarterly Research Report

Location-wise, the CBD and South Jakarta area continue to dominate, providing 45% and 35% of the units, respectively. With dy-

namic business activities, apartments for lease with service were largely available in the CBD area, most classified as middle-upper class.

Source: Colliers International Indonesia - Research Department

sUPPlY oF aPartMents For lease BY location

serViceD aPartMent non serViceD aPartMent

CBD 35%

Central Jakarta

5%

South Jakarta50%

North Jakarta

2%

East Jakarta

1%

West Jakarta

7%

CBD 55%Central

Jakarta10%

South Jakarta20%

North Jakarta

9%

West Jakarta

6%

The demand for apartments for lease in 2009 was largely influenced by the global economic crisis. Tightened accommodation budgets applied by some multinational companies restrained business expansion plans, including expatriate allocations in the country. Thus, apartments at lower rates, or those providing flexible leasing terms, were in high demand. Benefiting from long-stay occupiers, apart-ments for lease (non-service) posted stable

occupancy rates and continued to show grad-ual improvement. In line with the fluctuating number of expatriates in the country, the apartments for lease with service also showed fluctuating occupancy levels during the year. All in all, however, the average occupancy rate of apartments for lease (both non-service and serviced) achieved 69.4%, down from 71.6% in the previous year.

DeManD

Source: Colliers International Indonesia - Research Department

aVeraGe occUPancY rate oF JaKarta aPartMents For lease

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009

Serviced Apartment Non-Serviced Apartment Average

At the end of the year, the South Jakarta area managed to achieve the highest occupancy level, with an average of 70.6%, leaving around 3,239 units vacant. The CBD and Non-CBD areas recorded a similar occupancy

rate, of 68.9%, in the reviewed year. With limited supply available, there were only 1,100 vacant units in the CBD area, with about 16,000 in the non-CBD area.

colliers international 13

The Knowledge Report | March | 2010 | Quarterly Research Report

During 2009, the average asking rental rate of apartments for lease was relatively stable. The minor QoQ discrepancy was more influenced by exchange rate volatility in the calculation process. In general, the average offering rental rate per square metre in 2009 was approxi-mately the same as the year before. Our survey

noted that the average rental rate stayed at an average of US$13.30/sq m/month. However, the average rent per unit registered a 6.4% YoY increment, to an average of US$2,121/unit/month, compared to the previous year’s US$1.994/unit/month.

asKinG rental rate

Source: Colliers International Indonesia - Research Department

Unit occUPieD oF aPartMent For lease (serViceD anD non-serViceD aPartMent)

0

10,000

20,000

30,000

40,000

50,000

60,000

CBD South Jakarta Non CBD

Tot

al U

nit

Total Unit Unit Occupied

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

$20.00

1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

Ren

tal R

ate

(US$

/sqm

/mon

th)

CBD SJ Non CBD Average

aVeraGe occUPancY rate oF JaKarta aPartMents For lease

Source: Colliers International Indonesia - Research Department

In terms of rental/unit/month, apartments for lease (non-service) recorded an average rent of US$1,830/unit/month. In the market, the range was from US$309/unit/month in the non-CBD area to US$8,000/unit/month in the CBD area. Meanwhile, serviced apart-

ments registered an average of US$2,920/unit/month. The lowest rent of this type of apartment was US$1,800/unit/ month, while the highest could reach US$7,000/unit/month.

colliers international14

The Knowledge Report | March | 2010 | Quarterly Research Report

asKinG rental/Unit/MontH

serViceD aPartMent non serViceD aPartMent

Source: Colliers International Indonesia - Research Department

Developers are very much waiting in the hope that new foreign ownership regulation will be released to further trigger apartment sales. In principle, the new regulation will only prolong ownership rights up-front, instead of periodic extension. However, such regulation would be the appetizer for apartment market to grow further against the threat of upcoming supply over the next two years.

Lower interest rates would also give hope for the apartment market to perform better, from the perspective of both buyers and developers. However, again the market should anticipate abundant future supply, which will put pres-sure on price growth. If this happens, develop-ers will continue to offer atractive package prices, such as longer term payment terms, reduced down payment amounts and more subsidies given to the mortgate rate.

oUtlooK

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

CBD South Jakarta Non CBD

Ren

tal (

US$

/uni

t/m

onth

)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

CBD South Jakarta Non CBD

Ren

tal (

US$

/uni

t/m

onth

)

colliers international 15

The Knowledge Report | March | 2010 | Quarterly Research Report

The average asking rental for expatriate hous-ing was relatively stable in the second half of 2009. During this period, the market saw small new houses being built, scattered in such areas as Kebayoran Baru, Pondok Indah, Cilandak and Cipete, which increased the maximum asking rental slightly. In 2H2009, houses available on the market were offered at the lowest rate of US$2,700 per month all the way up to the highest at US$4,400 per month. Large houses are commonly found in such areas as Menteng, Kuningan, Kebayoran Baru and Pondok Indah, and rental rates can reach above US$10,000 per month. For several

periods, landlords have continued to ask for a minimum leasing period of two years, with payment in advance.

In terms of location, expatriate housing con-tinued to be concentrated in South Jakarta, particularly in the areas of Pondok Indah, Ke-mang, Cilandak and Cipete. These areas pro-vide houses with an average asking rent rang-ing from US$2,800 to US$3,700 per month. Higher asking rents of around US$4,000 per month are seen in such areas as Menteng and Kebayoran Baru, which benefit from their vi-cinity to the CBD.

eXPatriate HoUsinG rental rates (1H2009)

Source: Colliers International Indonesia - Residential/Tenant/Investor Representation Services

In 2H2009, the expatriate housing market benefited from the recovery of the Indonesian economy following the global financial crisis that started in the same period. Nevertheless, as frequently occurs, the market at year-end was challenged with slowing leasing activity.

Meanwhile, the active demand in the market continued to be dominated by expatriates and their families looking for housing in the areas of Pondok Indah, Cilandak, Cipete and Kemang, with a budget of between US$3,000

and US$4,000 per month. The proximity to complete entertainment and education fa-cilities with good infrastructure and security within the area become key factors in location preference.

During the second half of the year, housing requests came from banking, oil and gas com-panies. In addition, demand for expat quality housing also came from the pharmaceutical sector.

eXPatriate HoUsinG anD aPartMents

eXPatriate HoUsinG

sUPPlY anD rental rates

DeManD

areaasKinG rates (Us$/Unit/MontH)* aVeraGe size (sQ M)

loW HiGH aVeraGe BUilDinG lanD

Menteng $2,000 $12,000 $4,148 762 960

Kuningan $2,000 $10,000 $3,563 475 758

Kebayoran Baru $2,000 $15,000 $4,413 574 658

Kemang $1,500 $8,000 $2,882 520 858

Pondok indah $2,000 $12,500 $3,707 539 645

Permata Hijau $2,000 $6,000 $3,413 629 757

lebak Bulus $1,500 $5,000 $2,700 580 1,158

Pejaten $1,500 $7,000 $3,106 534 1,000

cilandak $1,500 $7,500 $2,986 496 849

cipete $1,500 $5,500 $2,984 464 777

* Majority are Unfurnished

colliers international16

The Knowledge Report | March | 2010 | Quarterly Research Report

Several companies with limited budgets for their expatriate staff accommodation caused demand for apartments with reasonable rentals to rise. This trend among affordable accommodation triggered some projects to in-crease their asking rental rate, particularly for three-bedroom apartments. Thus, the asking rental rate for selected expatriate apartments recorded a moderate increase in 2H2009.

Individual owners commonly asked for a one year minimum lease period, with payment in advance. Shorter leasing periods could be obtained from apartments managed by deve-lopers.

Source: Colliers International Indonesia - Research Department

selecteD eXPatriate aPartMents

In general, the leasing apartment market saw a decrease in the occupancy rate in the second half of the year. The year-end period is usually the time when contracts expire/are terminated as short-term workers fly back to their home countries. The Jakarta market recorded an average occupancy rate of 69.4% in 2H2009, down from 71.3% in the previous half.

In the midst of this downward trend in oc-cupancy rate, selected expatriate apartments experienced only a minor decrease, with the average occupancy rate at 83.6%, down from 83.9% in the previous half.

Demand for apartments in this half of the year continued to come from individuals or couples with a need for efficiency and flex-ibility. These tenants mostly had a budget of between US$2,000 and US$3,500 per month for a three-bedroom apartment.

Similar to the previous half, The Pakubuwono Residence, which provides the most compre-hensive facilities in Jakarta, remained the most preferred option for expatriates. High demand was also seen for the new tower of Pondok In-dah Golf in South Jakarta.

aPartMentaVeraGe Us$ asKinG rent/MontH aVeraGe

occUPancY2Br 3Br 4Br

Dharmawangsa, sailendra na 3,500 - 5,000 3,500 - 6,500 80.00%

Four seasonsPlaza senayan, the Plaza residence

na2,200 - 4,500 3,500 - 5,000 5,000 - 6,500 88.33%

the residence, Golf Pondok indah, Bukit Golf, ascott, Menteng executive

2,200 - 3,500 2,500 - 4,000 4,600 - 5,000 85.00%

aston, Batavia, Pavillion Park, Permata Hijau, Puri casablanca, casablanca

1,200 - 3,000 1,500 - 3,500 2,500 - 4,000 75.00%

taman rasuna, semanggi, slipi, Kintamani, taman Pasadenia, Puri imperium

500 - 1,500 700 - 2,600 2,500 - 3,500 75.00%

all 500 - 4,500 700 - 5,000 2,500 - 6,500 83.60%

eXPatriates aPartMents

rental rates

occUPancY

DeManD

colliers international 17

The Knowledge Report | March | 2010 | Quarterly Research Report

selecteD aPartMents MarKeteD For sale

naMe location Price ranGe/Unit coMPletion Year

Kempinski residence cBD Us$300,000 - Us$700,000 2008

Kraton Grand Hyatt residence cBD Us$160,000 - Us$200,000 2009

the Pakubuwono View south Jakarta Us$290,000 - Us$420,000 2010

one at cik Ditiro central Jakarta Us$80,000 - Us$250,000 2010

Source: Colliers International Indonesia - Research Department

Note: US$1 is around Rp 10,000

With an optimistic projection for the economy in 2010, the expatriate house and apartment market is also expected to rise. Further, the soon-to-be-effective China Asian Free Trade Area (CAFTA) will cause the expatriate

residential market to increase as more expatri-ates move to Indonesia, particularly Jakarta. Given this, suppliers should prepare carefully in anticipation of the accommodation needed to meet this possible new demand.

oUtlooK

colliers international18

The Knowledge Report | March | 2010 | Quarterly Research Report

Although the country’s economy was af-fected by the impact of the global economic crisis during 2009, Jakarta’s retail market still recorded 8.9% YoY growth, well below the previous year’s growth of 16.7%. As listed in the table, 2009’s annual supply was mainly from North and Central Jakarta, entering the

market in the first and third quarters. Almost all centers, except for Koja Trade Mall, were developed by major retail players, e.g. Agung Podomoro Group, Summarecon Group, Plaza Indonesia Realty, Jaya Real Property and Lippo Group.

retail sector

sUPPlY

retail center naMe location MarKetinG scHeMe

DeVeloPer

central Park central Jakarta for lease agung Podomoro Group

emporium Pluit north Jakarta for lease agung Podomoro Group

Kelapa Gading Mall Phase V north Jakarta for lease Pt summarecon agung

Koja trade Mall north Jakarta for strata title sale Pt Maju sentosa cemerlang

Plaza indonesia extension central Jakarta for lease Pt Plaza indonesia realty

Pusat Grosir senen Jaya central Jakarta for strata title sale Pt Jaya real Property

PX Pavillion st Moritz West Jakarta for strata title sale lippo Group

season city West Jakarta for strata title sale agung Podomoro Group

total : 309,681 sq m

neW retail centers in 2009

Source: Colliers International Indonesia - Research Department

The operation of six new retail centers plus two mall extensions increased the cumula-tive retail space by 309,681 sq m, to a total of 3.77 million sq m, at end-2009. Around 65% of this is classified as retail center for lease, with most located in the non-CBD area, par-ticularly in the southern and northern areas. Central Jakarta, as the center of trading and business area, has the largest retail space for strata title sale.

By retail grade, the retail centers in Jakarta are predominantly Grade B centers, at around 48%. Generally, grade B centers were found in all Jakarta areas but most were concentrated in Central Jakarta. Premium centers were mostly found in the CBD area, while a few were also found in North, South and West Jakarta.

retail center DistriBUtion

BY MarKetinG scHeMe BY GraDe

Source: Colliers International Indonesia - Research Department

0

200,000

400,000

600,000

800,000

CBD Central Jakarta

South Jakarta

North Jakarta

East Jakarta

West Jakarta

Tot

al S

pace

(sq

m)

For Lease For Strata Title Sale

0

200,000

400,000

600,000

800,000

North Jakarta

East Jakarta

Central Jakarta

South Jakarta

West Jakarta

Ret

ail S

pace

(sq

m)

Premium Grade A Grade B Grade C

colliers international 19

The Knowledge Report | March | 2010 | Quarterly Research Report

retail sPace sUPPlY anD GroWtH

Source: Colliers International Indonesia - Research Department

A slowing supply trend also occurred in the Greater Jakarta area. Our survey recorded only two retail centers - Taman Topi Square in Bogor and Teraskota in Tangerang - operat-ing in the first half of 2009, with total space of 34,000 sq m. With no additional space in the second half of the year, the Greater Jakarta market grew 2.0% YoY. Stock was around 1.8 million sq m at end-2009. About 59% of total

stock was classified as retail space for lease. Located in populated areas and zoned as in-dustrial areas, Bekasi and Tangerang provided the largest retail space in Greater Jakarta area for both lease and strata title sale, with 33% and 32%, respectively, of total stock. In the south, on the other hand, intended mainly as a water conservation area, the total retail space is relatively small.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

2007 2008 2009 2010F 2011F 2012F

Ret

ail S

pace

(sq

m)

Existing Supply Annual Supply Average Growth

Ave

rage

Gro

wth

(%)

Slowing supply trend is projected to occur in 2010, with only two retail centers, such as Grand Paragon in Central Jakarta and Gan-daria Main Street in South Jakarta, prepared for operation. The last project will be part of

an integrated development consisting of office tower, apartment and hotel. Over the next two years, supply for retail space is projected to increase by from 4 to 6%, to achieve a total of 4.3 million sq m by the end of 2012.

Greater JaKarta retail sPace sUPPlY

BY MarKetinG scHeMe BY location

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Bekasi Bogor Depok Tangerang

Tot

al S

pace

(sq

m)

For Lease For Strata Title Sale

For Strata Title Sale

41%

For Lease59%

Source: Colliers International Indonesia - Research Department

All in all, we still expect supply to shrink over the next two years. The market registers growth of only 1.1% in 2010, from the com-pletion of Plaza Dua Raja in Bogor, and will

see no new supply in 2011. However, cumula-tive supply is projected to escalate by around 260,000 sq m in 2012 if six retail centers meet their schedules.

colliers international20

The retail market in Jakarta is still challenged. Consumers are more prudent in spending their money. A survey by a market research consultant showed that people are now more selective in buying their needs and focus on primary merchandise. Nevertheless, people in Jakarta still need a mall atmosphere as an al-ternative place in which to relax and socialize and this has become part of Jakarta’s lifestyle. Accordingly, food and beverage businesses continued to be the crowd pullers for a mall/shopping center. During the year, retail market was flooded by the opening of F&B outlets.

Several international restaurants opened their outlets in last quarter of 2009. In West Jakarta, May Star in Central Park and Dian Xiao Er in Taman Anggrek Mall were opened to serve Chinese food. Kemiri restaurant opened its 1,400-sq m open kitchen space at Pejaten Vil-lage South Jakarta. MOF Japanese sweets and coffee opened at Plaza Indonesia Extension, and J’Co and Bread Talk at Tamini Square were also seen to open in the period.

Besides F&B retailers, in the last quarter of the year Japanese retailer, Mujirushi Ryohin (muji), officially opened in Plaza Indonesia, offering a variety of food, fashion and acces-sories. Sophie Paris expanded its business in Plaza Semanggi, following previous outlets at Citraland and Tamini Square. Ace Hardware also started to open its 1,500-sq m space in Grand Indonesia. Pacific Place Mall added its F&B outlets with the opening of K-box res-taurant, Tutti Frutti Yogurt and Raffel’s Sand-wich. The mall also introduced the fashion outlets of Biyan and Lamborghini Boutique, as well as other tenants like Watch Time, Book Story, Kenko Reflexology, Grand Living Inte-rior and Erha Apothecary.

The retail occupancy rate showed a decreasing trend YoY. Our survey revealed that in 2009 the average occupancy rate of the Jakarta re-tail market hovered around 82% and achieved 82.6% in the last quarter of the year. This per-centage is 2% down from 2008 but overall the market is still performing well.

DeManD

Greater JaKarta retail sUPPlY anD GroWtH

-10%

0%

10%

20%

30%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2007 2008 2009 2010F 2011F 2012F

Annual Supply Existing Supply Growth

Source: Colliers International Indonesia - Research Department

The Knowledge Report | March | 2010 | Quarterly Research Report

colliers international 21

JaKarta retail center PerForMance

cUMUlatiVe sUPPlY anD DeManD occUPancY rate

Source: Colliers International Indonesia - Research Department

Premium malls continue to perform best, with a 98.6% average occupancy rate. Surprisingly, the middle to low market also recorded a great occupancy rate of 93.9%, higher than middle to upper malls.

A decreasing trend was also experienced by retail centers in the greater Jakarta area. The occupancy rate was recorded at 95% in 2007 and gradually fell to only 82.6% at end-2009. However, volatility remained healthy and

stabilized at between 80% and 90%. Retail centers in Tangerang and Bogor showed high average occupancy rates of 92% and 91%, respectively. However, in these two areas some shopping centers were still partially unoc-cupied, with vacancy rates of above 50%. In Bekasi, with large supply available, the occu-pancy rate was recorded lower at 78%, leaving more than 130,000 sq m of retail space vacant. Meanwhile, occupancy for retail market in Depok area stabilized at 86%.

Greater JaKarta retail center PerForMance

0

200,000

400,000

600,000

800,000

1,000,000

CBD Central Jakarta

South Jakarta

North Jakarta

East Jakarta

West Jakarta

Ret

ail S

pace

(sq

m)

cumulative supply cumulative demand

0%

20%

40%

60%

80%

100%

2005 2006 2007 2008 2009

Occ

upan

cy R

ate

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Depok Bogor Tangerang Bekasi

Ret

ail S

pace

(Sq

m)

cumulative supply cumulative demand

0%

20%

40%

60%

80%

100%

2005 2006 2007 2008 2009

Occ

upan

cy R

ate

cUMUlatiVe sUPPlY anD DeManD occUPancY rate

Source: Colliers International Indonesia - Research Department

Transactions in Greater Jakarta area include Read Bean and Mega Indo Electronic in Teraskota Tangerang, NAV Karaoke and TFY Yoghurt in Margo City Depok. Meanwhile,

the Ekalokasari mall in Bogor repositioned itself by reconfiguring their tenants to become a center for IT products.

The Knowledge Report | March | 2010 | Quarterly Research Report

colliers international22

With moderate retail performance within the year, the asking rental rate shown a minor increment of 0.6% YoY, to an average of Rp 343,355/sq m/month, from Rp341,143/sq m/month previously. Comprising several upper class retail centers, the average asking rental

rates of retail centers in the South, Central and North Jakarta areas indicated an incre-ment trend, while those in West and East Ja-karta were relatively stable, as quite a few cen-ters in the area target a middle-class market.

asKinG rental rate oF retail center in JaKarta

Rp0

Rp50,000

Rp100,000

Rp150,000

Rp200,000

Rp250,000

Rp300,000

Rp350,000

Rp400,000

Rp450,000

Rp500,000

2005 2006 2007 2008 2009

Ask

ing

rent

al R

ate/

sq m

/mon

th

Central Jakarta South Jakarta North Jakarta East Jakarta West Jakarta Average

Source: Colliers International Indonesia - Research Department

Based on class, premium retail centers were applying high asking rentals far above other classes. With only a few retail centers op-erating this kind of shopping centers, this indicated an increasing rental trend. Average rental rates for premium retail centers were of-

fered at an average of Rp683,000/sq m/month. At end-2009, middle- to upper-class centers were offered at Rp314,500/sq m/month, while middle- to lower- class were offered for Rp204,400/sq m/month.

Rp0

Rp100,000

Rp200,000

Rp300,000

Rp400,000

Rp500,000

Rp600,000

Rp700,000

Rp800,000

2005 2006 2007 2008 2009

Premium Middle Up Middle low

Source: Colliers International Indonesia - Research Department

asKinG rental rates anD serVice cHarGes

asKinG rental rates

The Knowledge Report | March | 2010 | Quarterly Research Report

colliers international 23

There were lower asking rental rates offered for retail centers in the greater Jakarta area. The average rent indicated an increasing trend from 2005 and experienced minor falls in 2008 and 2009. Our survey recorded that the aver-

age asking rental rate in Greater Jakarta area was Rp246,000/sq m/month. Stabilizing the rental rate was one of the strategies applied in the last two years to retain tenants.

Rp-

Rp50,000

Rp100,000

Rp150,000

Rp200,000

Rp250,000

Rp300,000

2005 2006 2007 2008 2009

Ask

ing

Ren

tal R

ate/

sq m

/mon

th

Source: Colliers International Indonesia - Research Department

The average service charge for retail centers in Jakarta was relatively stable within the first three quarters and posted a minor increment in the last quarter, due to new shopping cen-ters entering. In Jakarta, the service charge registered a modest decrease by 0.13% YoY, to Rp62,538/sq m/month, from Rp62,618/sq m/month previously.

Categorized by class, our survey revealed that premium and middle to low retail centers con-tinued to apply similar rates to the previous year, at Rp93,400/sq m/month and Rp51,750/sq m/month, respectively. Middle to upper centers posted a 6% increase, to Rp66,385/sq m/month, following the operation of some retail centers within the year.

serVice cHarGes

retail center serVice cHarGe BY class in JaKarta

Source: Colliers International Indonesia - Research Department

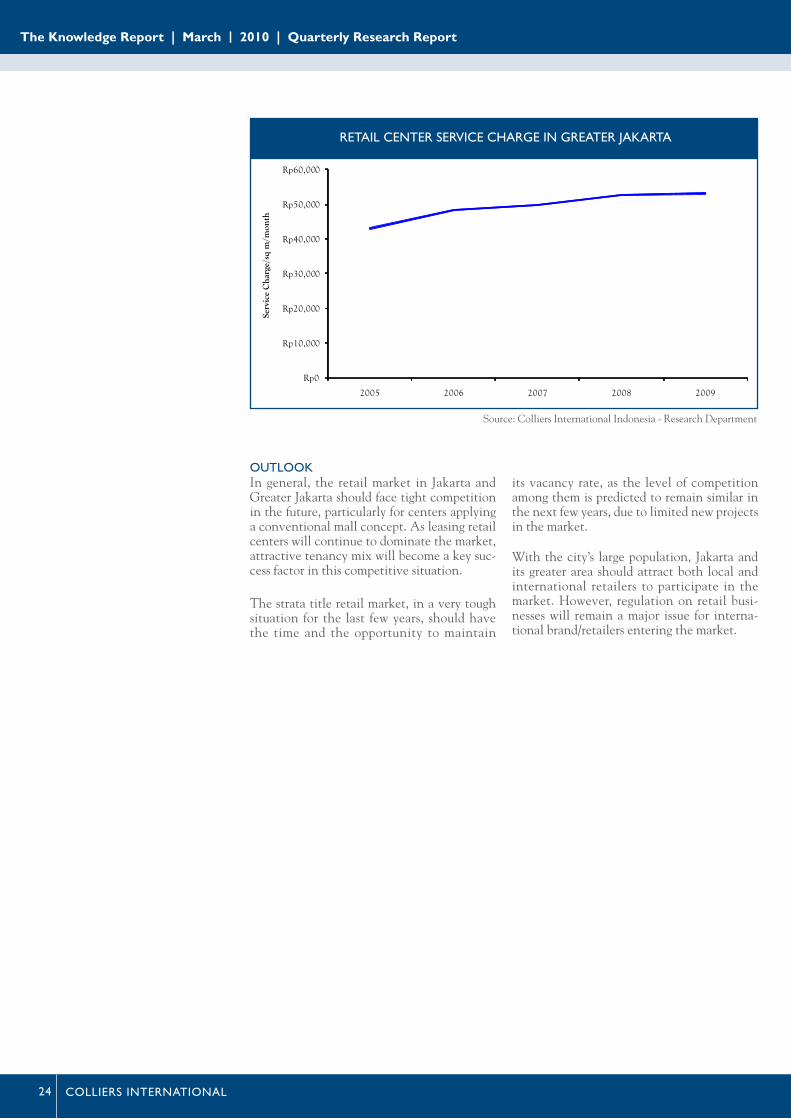

In greater Jakarta the average service charge recorded a minor increment of 0.8% YoY, to Rp53,071/sq m/month, compared to the previ-

ous year’s Rp52,651/sq m/month, due to the adjusted rate applied by some centers in the second half of the year.

Rp0

Rp10,000

Rp20,000

Rp30,000

Rp40,000

Rp50,000

Rp60,000

Rp70,000

Rp80,000

Rp90,000

Rp100,000

2005 2006 2007 2008 2009

Serv

ice

Cha

rge/

sq m

/mon

th

Premium Middle Up Middle low

The Knowledge Report | March | 2010 | Quarterly Research Report

colliers international24

retail center serVice cHarGe in Greater JaKarta

Rp0

Rp10,000

Rp20,000

Rp30,000

Rp40,000

Rp50,000

Rp60,000

2005 2006 2007 2008 2009

Serv

ice

Cha

rge/

sq m

/mon

th

Source: Colliers International Indonesia - Research Department

In general, the retail market in Jakarta and Greater Jakarta should face tight competition in the future, particularly for centers applying a conventional mall concept. As leasing retail centers will continue to dominate the market, attractive tenancy mix will become a key suc-cess factor in this competitive situation. The strata title retail market, in a very tough situation for the last few years, should have the time and the opportunity to maintain

its vacancy rate, as the level of competition among them is predicted to remain similar in the next few years, due to limited new projects in the market. With the city’s large population, Jakarta and its greater area should attract both local and international retailers to participate in the market. However, regulation on retail busi-nesses will remain a major issue for interna-tional brand/retailers entering the market.

oUtlooK

The Knowledge Report | March | 2010 | Quarterly Research Report

colliers international 25

During the reviewed quarter, neither of the existing industrial estates came with expan-sion plans, nor were future industrial estates openings announces . For some time, and likely for several periods ahead, the industrial estate market will not see any new industrial land, but expansion plans could possibly come from operating industrial estates with con-tinuing sales.

To date, we have heard no confirmation of the expansion of around 80 hectares land in Serang, nor the plan from prominent estates

in the Bekasi area. 2009 was seemingly the year of consolidation, wherein many industrial estates were working hard to focus on selling unsold units. Thus, during 2009 the industrial market registered no additional land, which helped take-up rate rise steadily.

As at the end of the year and up to the first quarter this year, supply of industrial land in the six different regions (Jakarta and greater Jakarta areas) did not change, remaining at 8,662 hectares.

inDUstrial estate sector

sUPPlY

Beyond expectations, the industrial market performed better, amidst the fear of a weak-ening economy in early 2009. At the begin-ning of the year quite a few of the industrial landlords we interviewed had moderate sales target during the year; but in fact, after one year under review, sales of industrial land were more than expected. Expansion activities from operating industrialists were dominant during the year and only a few new investments were seen during the year. However, we noted that the new investments acquiring industrial land were companies whose owners had long his-torical experience with the business environ-ment in Indonesia.

The number of total transactions during the quarter exceeded transactions during the pre-vious period. We recorded around 52 hectares of land being transacted in the quarter. Also, as mentioned earlier, total transactions dur-ing 2009 exceeded our expectations, and total industrial land sales in 2009 were recorded at around 214 hectares, which was slightly up compared to 2008’s total transactions, and this was much better than total transactions in 2006 and 2007.

Total sales recorded during the fourth quarter were registered by Modern Cikande, with a total of around 14.7 hectares; however, total sales recorded for the full year 2009 were registered by BFIE at a total of around 47.2 hectares. For the last four years, this was a his-torical high so far for total transactions made by one industrial estate in one year.

Delta Silikon ranked second after Modern Cikande in the total number of land and SFB sales during the quarter, with around 11.2 hectares, followed by Bekasi Fajar (BFIE) with a total of around 10.2 hectares. Modern Cikande, as the biggest contributor to the whole sales this quarter, received the biggest transaction from Mitsuba, Japanese automo-tive component makers, of around 7.3 hect-ares. This transaction was for the expansion of an existing factory, occupying four hectares of land. The second biggest transaction during the quarter also came from the same industry, in KIIC, which registered land transactions of around five hectares. Other significant trans-actions occurred during the quarter, including 4.9 hectares of land acquired by Taiwanese genuine leather tannery in Modern Cikande; PT. Kayaba Indonesia (automotive spare parts) in BFIE of 4 hectares; PT. Komatsu Indonesia (heavy equipment) in MM2100 taking around 3 hectares; a local steel-related industry taking around 3 hectares in KIEC; PT. Oh Sung E.I. (electronic components) from Korea in BFIE with transactions of around 2.6 hectares; a local aluminum manufacturer in Modern Ci-kande, with around 2.5 hectares; 2.4 hectares from a pharmaceutical company with transac-tions in Indotaisei and land transactions from PT. East Hope Agriculture Indonesia, a feed mill from China, taking around 2.4 hectares in Suryacipta.

DeManD

The Knowledge Report | March | 2010 | Quarterly Research Report

colliers international26

Source: Colliers International Indonesia - Research Department

annUal inDUstrial lanD sales

Source: Colliers International Indonesia - Research Department

cUMUlatiVe sUPPlY, DeManD anD taKe-UP rates

Source: Colliers International Indonesia - Research Department

inDUstrial lanD sales recorDeD in 4Q09

0

50

100

150

200

250

300

2004 2005 2006 2007 2008 2009

hect

are

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2004 2005 2006 2007 2008 1Q09 2Q09 3Q09 4Q09

hect

ares

Cumulative Supply (ha) Cumulative Demand (ha) Take-up Rate (%)

0 5 10 15 20 25 30 35 40 45 50

Sentul Industrial Estate

KBN

Kota Bukit Indah Intotaisei

Suryacipta

MM2100 Industrial Town

Jababeka Industrial Estate

KIIC

KIEC

Delta Silicon

Greenland (Kota Delta Mas)

Modern Cikande

Bekasi Fajar Industrial Estate

hectare

The Knowledge Report | March | 2010 | Quarterly Research Report

colliers international 27

inDUstrial lanD Prices anD Maintenance costOverall, prices are relatively stable but we have noted that some industrial estates have escalated their asking price. Continued in-quiries for one industrial estate have been the main reason for the developer to increase the offering price. Apart from that, the increas-ing Sale Value of the Tax Object (NJOP) was also a factor triggering the price hike. Besides, in anticipation of responding to the market, some developers tried to adjust their asking price to levels close to the market average.

One industrial estate in Bekasi has introduced a new price for their land in response to con-tinued demand and the land shortage. The new price was quite significant and beyond the market average.

In Serang one prominent industrial estate has come with a new quite significant offering price (up by 20%). Their confidence in con-tinued transactions, and the comprehensive facilities offered, have been the reasons behind the new price. Further, the price escalation was set to anticipate future plans to increase their own power plant capacity.

To equalize the market price, one industrial estate in Karawang has introduced new land prices during the reviewed quarter. This measure was taken in anticipation of growing demand.

Greater JaKarta inDUstrial lanD Prices

Source: Colliers International Indonesia - Research Department

Maintenance adjustment only occurred in Serang areas, with two prominent industrial estates introducing new maintenance tariff, rising by 13 to 18%. However, the mainte-nance tariff for Serang area was considered the

lowest compared to the other regions. It was registered that the climb in maintenance tariff ranged only from Rp30 to Rp50/sq m/month.

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

Bogor Tangerang Karawang Bekasi Serang

The Knowledge Report | March | 2010 | Quarterly Research Report

colliers international28

Greater JaKarta aVeraGe Maintenance costs

Source: Colliers International Indonesia - Research Department

$0.00

$0.01

$0.02

$0.03

$0.04

$0.05

$0.06

$0.07

$0.08

$0.09

1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

Bogor Tangerang Karawang Bekasi Serang

Source: Colliers International Indonesia - Research Department

reGionlanD Price (/sQ M) Maintenance cost (/sQ M/MontH)

loWest HiGHest aVeraGe (rp)

loWest HiGHest aVeraGe (rp)

Bekasi rp 500,000 Us$ 85.00 rp 637,225 Us$ 0.05 Us$ 0.07 rp 601

Karawang rp 300,000 Us$ 50.00 rp 391,779 Us$ 0.05 Us$ 0.06 rp 496

Bogor Us$ 45.00 rp 750,000 rp 653,105 Us$ 0.065 Us$ 0.1 rp 686

serang rp 350,000 rp 650,000 rp 551,776 rp 250 rp 330 rp 299

tangerang Us$ 60.00 rp 1.26 mill rp 616,322 Us$ 0.04 rp 1,000 rp 535

inDUstrial lanD Prices anD Maintenance cost

Starting 2010 with an historically good per-formance in 2009, the industrial market is expected to perform much better in 2010. With global financial crisis still evident at the beginning of the year, the industrial market was anticipated to dilute the hope of perform-ing better than the previous year. On the contrary, however, total sales recorded during 2009 even exceeded the totals of the preced-ing year. With plenty of ammunition for 2010, such as stabilized political conditions and the expectation of a growing economy, the indus-trial market in 2010 has met the requirement to perform even better.

We expect that the type of industries that acquire industrial land in the future will be the usual industries of auto spare parts, steel, ware-housing, packaging, food-related industries, printing, plastic moulding or pharmaceutical.

oUtlooK

The Knowledge Report | March | 2010 | Quarterly Research Report

colliers international 29

The Knowledge Report | March | 2010 | Quarterly Research Report

contact inForMation

this report and other research materials may be found on our website at www.colliers.com. Questions related to information herein should be directed to the research Department at the number indicated above. this document has been prepared by colliers international for advertising and general information only. colliers international makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. any interested party should undertake their own inquiries as to the accuracy of the information. colliers international excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damages arising there from. colliers international is a worldwide affiliation of independently owned and operated companies.

Our Knowledge is your Property

Colliers International IndonesiaWorld Trade Centre 10th floorJalan Jenderal Sudirman Kav 29 - 31Jakarta 12920Tel : 62 21 521 1400Fax : 62 21 521 1411

Mike BroomellManaging DirectorTel : 62 21 521 1400Fax : 62 21 521 1411Email : [email protected]

Ferry SalantoDivision Manager, Research ServicesTel : 62 21 521 1400Fax : 62 21 521 1411Email : [email protected]

293 oFFices in 61 coUntries on 6 continents

Usa 99 canada 19latin america 18 asia Pacific 62 eMea 95

$2.0 billion in annual revenue 868 million square feet under management

15,573 Professionals

www.colliers.co.id Our Knowledge is your Property