JAIPUR RESIDENTIAL REAL ESTATE OVERVIEW … · 6 The Jaipur Residential Real Estate Overview...

23

1 JAIPUR RESIDENTIAL REAL ESTATE OVERVIEW January 2015

Transcript of JAIPUR RESIDENTIAL REAL ESTATE OVERVIEW … · 6 The Jaipur Residential Real Estate Overview...

1

JAIPUR RESIDENTIAL

REAL ESTATE OVERVIEW

January 2015

2

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY 3

2. JAIPUR CITY FACT FILE 4

3. JAIPUR REAL ESTATE 6

4. INFRASTRUCTURE GROWTH STIMULATORS 7

5. CITY SUPPLY AND ABSORPTION TRENDS 10

6. MAJOR LOCATIONS OF JAIPUR 13

7. CENTRAL JAIPUR 14

8. NORTH JAIPUR 16

9. WEST JAIPUR 17

10. SOUTH JAIPUR 19

11. EAST JAIPUR 21

12. LOCATION ATTRACTIVENESS INDEX 22

3

Jaipur is likely to become a Mega City by 2025 with a population of 10 million people covering an area of about 800 sq km. With flourishing tourism, manufacturing, export and educational infrastructure, Jaipur, the capital city of Rajasthan, is witnessing a booming real estate market. The city is strategically located at the confluence of three national highways, namely, NH-8 which connects Delhi to Mumbai, NH-12 which links Jaipur to Madhya Pradesh and NH-11 which links Bikaner to Agra. The Jaipur Residential Real Estate Overview highlights some of the key trends in the Jaipur residential real estate market. The report has been prepared based on a detailed market study by the ICICI PSG Research Team.

Some of the factors resulting in Jaipur’s popularity as a real estate destination include affordable investment options in comparison to NCR, rapid industrial and commercial development and a fast emerging IT sector leading to creation of employment opportunities. The plethora of socio-infrastructural developments such as the Jaipur Metro project, construction of Ring Road around Jaipur and major upcoming projects like Mahindra’s 3000-acre Special Economic Zone (SEZ), Reliance Medi-city and the Delhi Mumbai Industrial Corridor (DMIC) will be further strengthening the city’s real estate potential.

The realty market of Jaipur has witnessed maximum activity in suburban micro-markets of southern and

western Jaipur such as Jagatpura, Tonk Road, Vaishali Nagar, Patrakar Colony, etc. The roads and highways connecting Jaipur with neighboring locations both outside and within Rajasthan, such as Ajmer (Delhi-Mumbai) Road, Tonk Road, Sikar Road, Sirsi Road and Agra Road, have also been witnessing traction and various known developers have forayed into these regions seeing strong future growth potential along these corridors.

Jaipur residential real estate market is driven by a 60:40 mix of investors and end users respectively. The local

consumption of flats is comparatively low and the local investors prefer investing in plots as the business community which forms a major chunk of the local population comprising of marble traders, jewelers etc. view it as an easy exit option with the added advantage of flexibility to use the land if needed. The investor community consists of investors primarily from Delhi-NCR, UP, Kolkata and NRI investors from Dubai, Muscat, Kuwait, US etc.

Our in-depth analysis indicates than the maximum supply and absorption in the Jaipur market falls in the price

bracket of INR 2,000 – 4,000/sq. ft. and the most active configuration in terms new launches and absorption for the residential units has been the 3-BHK segment.

The report has been divided into following five distinct regions – Central, North, East, South and West based

on the geographical location and real-estate activity where we have analyzed the key trends in the markets and have provided a perspective of the prevailing market scenario.

Further, the report tracks the city absorption and supply trends and property price trends for each of these

micro-markets through the weighted average prices of the available supply of units.

The report concludes with a Location Attractiveness Index, which grades each micro-market on the basis of certain key parameters such as the current state of Infrastructure, Residential Cost, Proximity to Retail Establishments, Future Employment Generation Capacity etc.

EXECUTIVE SUMMARY

4

Overview

Jaipur is the capital and the largest city of the Indian state of Rajasthan. The city dates back to 1727. It was founded by and named after Maharaj Sawai Jai Singh II, the ruler of Amber. The city blushed in pink, is steeped in history and culture. Known for its handicrafts, gems and exports industry, this famous 'tourist spot' is also emerging as a favorable IT destination. Jaipur, an amalgamation of traditional and modern industries, is evolving well on the real estate development map. Jaipur is one of the earliest planned cities of India dating back to the 18th century. The city’s growth began from the Pink City area expanding primarily towards the western and southern Jaipur as the Nahargarh hills in the North and the East are physical barriers to the growth of the city. The setting up of Rajasthan Housing Board in 1970 with the objective of providing housing facilities to the citizens of 7 cities of the state, which has currently been expanded to 52 states, greatly enhanced the urban landscape and infrastructure of the city. The major transport corridors such as Tonk Road, Ajmer Road, Sirsi Road, Sikar Road etc. the have played a significant role in determining the urban form of the city. Geographical Location

Jaipur is situated in the east of Rajasthan state. The city is located approximately at 26.920N and 75.820E. Jaipur district has an area of 11,152 km2 and is surrounded by Sikar district in the north, the state of Haryana in the extreme north-east, Alwar and Dausa districts in the east, Sawai Madhopur district in south-east, Ajmer district in the west, Nagaur district in the north-west and Tonk district in the south. It lies 431 meters above the mean sea level. Moreover, east and north of Jaipur district are surrounded by the Nahargarh hills. The city is also very well connected to Delhi, Agra, Jodhpur, Udaipur and Jaisalmer through a network of roads, highways, railways and airways. Demographics (Census 2011 Highlights) As per provisional reports of Census India, population of Jaipur district in 2011 is 6,626,178; of which male and female are 3,468,507 and 3,157,671 respectively. In education section, total literates in Jaipur district are 4,300,965 of which 2,554,793 are males while 1,746,172 are females. Average literacy rate of Jaipur is 75.51 percent. Jaipur will soon join the club of top ten most populated cities of urban agglomerations in the country (Urban agglomeration is the population of main city added with the population of any suburbs). For Jaipur, it includes suburbs like Bassi, Sanganer, Shivdaspura, Ramgarh and Kanota.

Description 2011 2001

Population 6,626,178 5,251,071

Male 3,468,507 2,768,203

Female 3,157,671 2,482,868

Population Growth 26.19% 32.40%

Area Sq. Km 11,143 11,143

Density/km2 595 471

Proportion to Rajasthan Population 9.67% 9.29%

Sex Ratio (Per 1000) 910 897

Child Sex Ratio (0-6 Age) 861 899

Average Literacy 75.51% 69.90%

Literates 4,300,965 3,027,923

Male Literates 2,554,793 1,891,074

Female Literates 1,746,172 1,136,849

Child Proportion (0-6 Age) 14.03% 17.51%

Boys Proportion (0-6 Age) 14.40% 17.49%

Girls Proportion (0-6 Age) 13.63% 17.53% Source: Census-2011

JAIPUR FACT FILE

5

Economy The state and the city pay a substantial focus to the tourism, manufacturing, exports and education sectors. A variety of traditional as well as non-traditional items are exported from Rajasthan. These include precious and semiprecious stones, jewellery, ready-made garments, carpets, handicrafts, leather goods, chemicals, minerals, marbles, granite, engineering products etc. Jaipur's proximity to the National Capital Region is one of its biggest advantages. The nearby markets of Delhi and Gujarat have been both complementing and competing forces. The Delhi Mumbai Industrial Corridor (DMIC) will further strengthen Jaipur's development as an important economic hub. History Jaipur was founded in 1727 by Maharaja Sawai Jai Singh II, who ruled Jaipur State from 1699-1744. Initially his capital was Amber, which lies at a distance of 11 km from Jaipur. He felt the need of shifting his capital city with the increase in population and growing scarcity of water. Jaipur is the first planned city of India and the king consulted several books on architecture and architects before making the layout of Jaipur. After several battles with the Marathas, Maharaja Jai Singh became extremely concerned about the security aspects of the city. Due to this reason, he focused on his scientific and cultural interests to make a brilliant city. Being, a lover of mathematics and science, Jai Singh sought advice from Vidyadhar Bhattacharya, a Brahmin scholar of Bengal, to aid him design the city architecture. With a strategic plan, the construction of the city started in 1727. It took around 4 years to complete the major palaces, roads and square. The city was built following the principles of Vastu Shastra and was divided into nine blocks, out of which two consist of the state buildings and palaces, whereas the remaining seven blocks were allotted to the public. Administrative Framework Being a state capital, Jaipur has Legislative Assembly, Secretariat, State level offices of maximum Government departments with divisional and district level offices. There are 13 Tehsils and sub-divisions in the district which are named as Jaipur, Chomu, Amber, Sanganer, Shahpura, Bassi, Chaksu, Mojmabad, Jamwa Ramgarh, Phagi, Phulera, Kotputli, Viratnagar. Also, there are 13 Panchayat samitis and 2,369 villages. Infrastructure for Connectivity: Roads The city of Jaipur is centrally located and lies at the confluence of three National Highways. NH-8, one of the busiest highways in the subcontinent, links Delhi to Mumbai as well as important cities Gurgaon, Ajmer, Udaipur, Ahmedabad, Surat, Jaipur and Vadodara, NH-12 links to Jaipur (Rajasthan) to Jabalpur (Madhya Pradesh) via Kota and Bhopal and NH-11 links Bikaner to Agra, passing through Jaipur district with a total length of 366 km. City Bus Services RSRTC (Rajasthan State Road Transport Corporation) operates bus service to all the parts of Rajasthan and New Delhi, Uttar Pradesh, Haryana, Madhya Pradesh and Gujarat. City buses are operated by Jaipur City Transport Services Limited (JCTSL) of RSRTC under JNNURM (Jawaharlal Nehru National Urban Renewal Mission). The service operates more than 300 regular and low-floor buses. The three major bus depots are Vaishali Nagar, Vidyadhar Nagar and Sanganer. Railway Jaipur Railway Station (Jaipur Junction - JP) is the largest of all railway stations in Jaipur and the busiest railway station in Rajasthan. It has direct trains on the broad gauge network to all major cities in Rajasthan and India. One of India's most famous and luxurious trains 'The Palace on Wheels' also makes a scheduled stop in Jaipur. Other Railway Stations served by the Indian Railways network at Jaipur are:

Gandhinagar Railway Station

Gator Jagatpura Railway Station

Durgapura Railway Station Airway Jaipur is served by an International Airport, which is situated in its satellite town of Sanganer, at a distance of 10 km from city center and offers sporadic service to major Domestic and International locations. The Terminal 1 is used for both International and Domestic flights, while Terminal 2 is reserved for Domestic carriers. The up-gradation of airport has offered improved connectivity and wider choice of services to air travelers, boosting both International tourism and Economic development of the region.

JAIPUR FACT FILE

6

The Jaipur Residential Real Estate Overview highlights some of the key trends in the Jaipur residential real estate

market. The report has been prepared based on an in-depth market study by the ICICI PSG Research team with

detailed interactions with all the stakeholders of the real estate market.

Micro-market Overview: The Jaipur market has not witnessed much of a change in the realty absorption levels with the absorption hovering at around 1400-1600 units per quarter during the first three quarters of CY2014. The investors are willing to invest in the areas developing along the ‘spokes’ around the center of Jaipur such as Jagatpura, Tonk Road, Ajmer Road, Sanganer, Patrakar Colony etc.

The Jagatpura micro-market, with 25 residential projects coming up in this area, is attracting attention being

located around 6 kms away from Malviya Nagar which is a region that hosts good civic amenities such as schools, hospitals, multiplexes and malls that cater to the whole city. It is touted to become a major medical hub of Jaipur with Fortis Hospital, Apex Hospital, Narayan Hridayalaya falling in the vicinity of Jagatpura along with two proposed healthcare projects of Bombay Hospital and Reliance Mega Medicity. Investment in this market has seen an uptrend because of availability of regular rental income as it is a major educational hub due to the presence of various technical universities located in this area. The ticket size of in this area lies in the range of 30-90 lacs.

Patrakar Colony located in the proximity of Mansarovar colony which has developed a sustainable eco-

system due to its long history of inhabitation and its well-planned layout developed by the Rajasthan Housing Board, is a major factor driving the demand for Patrakar Colony. The proximity to the Mansarovar Metro station which is the starting point for the Phase I of the Jaipur Metro Rail Network will be an important driving factor for the real estate market in the area. Patrakar Colony is around 8 kms from the airport and the ticket size lies in the range of 20-80 lacs. It is the second most active micro-market in terms of absorption with around 400 units being absorbed till October 2014.

Tonk Road (beyond the B2 Bypass Road) is a micro-market where the builders are betting big on this area

due to the high sentimental value attached to it due to its proximity to Pratap Nagar, a well developed residential area, and good connectivity with other parts of Jaipur due to the availability of ample public transport facilities.

The investors who had invested in the Ajmer Road micro-market are still holding on to their investments as the resale market is virtually absent due to a low demand. The low demand can be gauged from the over-exploitation of the area with inadequate infrastructural support such as continuous water supply, electricity etc., thus skewing the demand-supply dynamics towards the supply side. The occupancy rates are currently only around 30% with very slim chances of any increment unless the basic amenities are taken care of. There are currently around 1 to 1.5 lac units being constructed which will further add to the woes of the region.

Special Economic Zone (SEZ) joint venture by Mahindra & Mahindra with

RIICO, the Mahindra City, spread across 3,000-acres, serves as a conduit between entire North India and the ports of the Western coast. It is divided into two zones – one zone being the IT zone and the other zone being dedicated to Export industries such as Gem stones, jewellery, handicrafts, garments etc. This will be a major driving factor for the Jaipur market as it is located on NH-8 which connects Delhi to Mumbai and is well connected to the Kandla Port in Gujarat being a major hub for exports. The Mahindra World City, Jaipur in its masterplan has planned to develop the social and residential infrastructure such as housing facilities, healthcare facilities, educational institutions, banks and ATMs etc. to enable a holistic living environment.

JAIPUR REAL ESTATE

7

Factors affecting Residential Market Development in Jaipur:

Employment generation opportunities: In 2008, Jaipur was ranked 31 among the 50 Emerging Global Outsourcing cities. Deutsche Bank Group Jaipur, Genpact and Infosys have their BPO in Jaipur and and many more indigenous and multi-national companies are exploring business opportunities in Jaipur. Mahindra World City in Jaipur, is India’s largest IT SEZ with 51 Companies who have signed the MoU for INR 13.6 billion and there is scope for further investment (Source: Invest North 2013, a CII-KPMG Study). The SEZ has a dedicated IT/ITeS zone spread over 750 acres which provides seamless telecom and broadband connectivity, quality satellite linkage and a range of voice and data solutions.

Good connectivity of Jaipur to the remaining parts of the country is a great advantage for the real estate market of Jaipur. Sirsi Road, Sikar Road and Kalwar Road merge in to the Ajmer road and connect Jaipur to West India. Tonk Road connects Jaipur to Central and South India, NH-8 passes through Jaipur and thus connecting it to Delhi and the rest of North India and Agra Road connects Jaipur to the UP and further to the East.

The local consumption of flats is low and the local investors prefer investing in plots as the business community forms a major chunk of the local population comprising of marble traders, jewelers etc. who view it as an easy exit option with the added advantage of flexibility to use the land if needed.

The end-users of Jaipur have become more acceptable to the concept of high-rise apartments and have

started moving into these structures.

A lot of investors are investing in Jaipur from Delhi-NCR, UP, Kolkata and NRI investors from Dubai, Muscat, Kuwait, US etc. which is aiding Jaipur’s real estate market in its course of improvement.

JAIPUR REAL ESTATE

8

Metro Rail Network: Rapid transit rail project 'Jaipur Metro' is expected to be one of the biggest growth stimulators for Jaipur realty market. The project is being handled and executed by Jaipur Metro Rail Corporation Limited (JMRC) that was setup by the Government of Rajasthan as a wholly owned company of the State Government. The project is planned along two corridors: The 'East West Corridor' and the 'North South Corridor'. The East West Corridor planned from Mansarovar to Badi Chaupar is being executed as Phase-I of the Project. The North South Corridor from Ambabari to Sitapura shall be taken up as Phase-II of the project. This project is currently undergoing the testing phase in the East West Corridor and is likely to be operational from March 2015. Once the metro becomes operational, rates of residential property in the areas on and near the metro route are expected to flare up. Bus Rapid Transit Service (BRTS): Jaipur BRTS has been proposed to cater to city's growing traffic needs in the

next 15-20 years. In Phase I, two corridors have been proposed: "North-South Corridor" from Sikar Road to Tonk

Road, and an "East-West Corridor" from Ajmer Road to Delhi Road.

Ring Road: The proposed Ring Road project launched by Jaipur Development Authority (JDA) will be a seminal project in terms of becoming the arterial road connecting the major areas of Jaipur together. Construction of Ring Road around Jaipur was conceived by PWD (Public Works Department) in December, 2000 on BOT (Build-Operate-Transfer) basis. In Phase I & II, a 47 km road will connect Ajmer Road, Tonk Road and Agra Road. In Phase III, a 97.75 km road will connect Agra Road, Delhi Road, Sikar Road and Ajmer Road. It will consist of a six-lane access controlled expressway with a three-lane service road on both sides. The Expressway will have investment zones for commercial as well as residential development on both the sides. The road is envisioned as a toll-free and signal-free expressway. Dedicated Freight Corridor running through Jaipur: Dedicated Freight Corridor (DFC) – a 1,483 km long rail corridor connecting Jawaharlal Nehru Port near Mumbai to Dadri near Delhi – will allow high-speed connectivity for high axle load wagons (25 tonnes) of double stacked container trains supported by high power locomotives. Delhi Mumbai Industrial Corridor (DMIC): A band of 150 km on both sides of the DFC has been chosen to be developed as the Delhi-Mumbai Industrial Corridor (DMIC). With nearly 39% of DFC passing through Rajasthan, opportunities for industrial establishment along the route are aplenty as the corridor will make Rajasthan easily accessible to western and northern markets. About 60% of the State's area (in 22 Districts including major districts such as Jaipur, Alwar, Kota and Bhilwara) falls within the project influence area of DMIC.

INFRASTRUCTURE GROWTH STIMULATORS

9

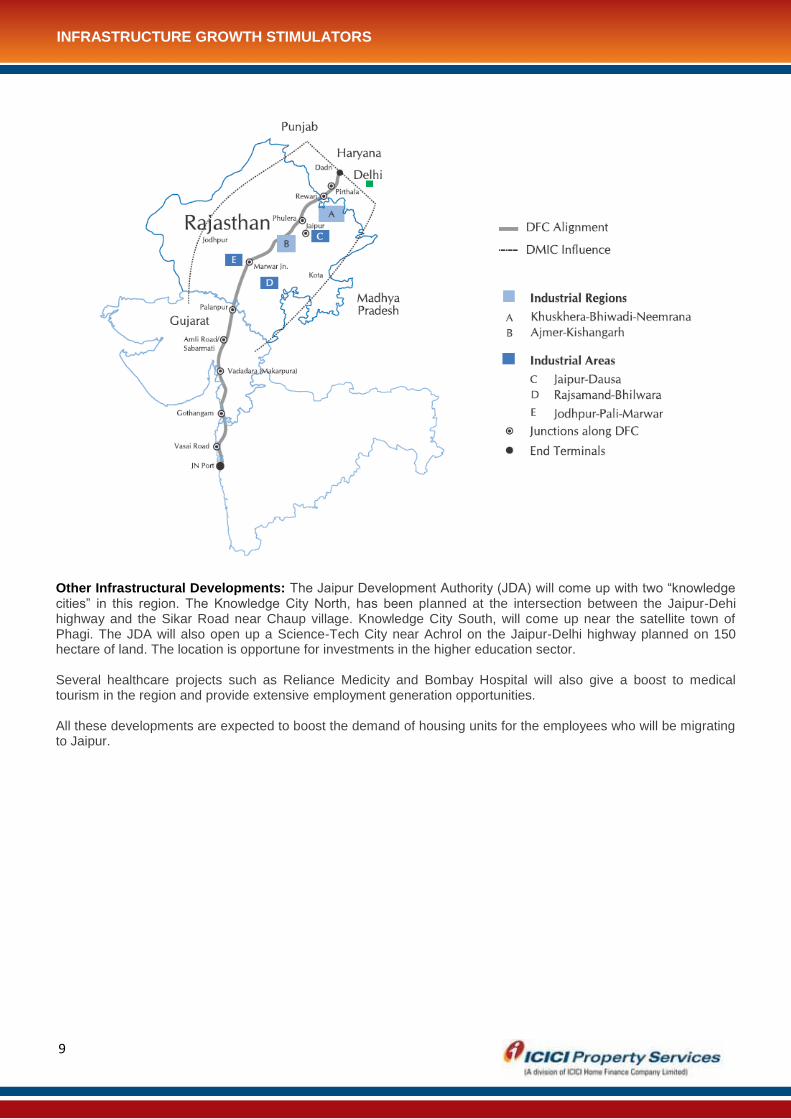

Other Infrastructural Developments: The Jaipur Development Authority (JDA) will come up with two “knowledge cities” in this region. The Knowledge City North, has been planned at the intersection between the Jaipur-Dehi highway and the Sikar Road near Chaup village. Knowledge City South, will come up near the satellite town of Phagi. The JDA will also open up a Science-Tech City near Achrol on the Jaipur-Delhi highway planned on 150 hectare of land. The location is opportune for investments in the higher education sector. Several healthcare projects such as Reliance Medicity and Bombay Hospital will also give a boost to medical tourism in the region and provide extensive employment generation opportunities. All these developments are expected to boost the demand of housing units for the employees who will be migrating to Jaipur.

INFRASTRUCTURE GROWTH STIMULATORS

10

A. Quarterly Trends:

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Q4-2012 Q1-2013 Q2-2013 Q3-2013 Q4-2013 Q1-2014 Q2-2014 Q3-2014

Un

its

New Launches New Launch Absorption Total Absorption Unsold Inventory

Source: PropEquity, ICICI Property Services Group. Note: Quarters as per CY2014

The number of new units launched has been following a downward trend in CY2014 and decreased by about 55%

in Q3-CY2014 over the previous quarter primarily due to the high amount of unsold inventory still available in

Jaipur. The total absorption levels have been around 1400-1600 units per quarter during CY2014.

B. Weighted Average Price Trend

2,000

2,200

2,400

2,600

2,800

3,000

3,200

3,400

3,600

3,800

4,000

Q4-2

012

Q1-2

013

Q2-2

013

Q3-2

013

Q4-2

013

Q1-2

014

Q2-2

014

Q3-2

014

INR

SqF

t

Available Units New Launches Absorbed Units

Source: PropEquity, ICICI Property Services Group. Note: Quarters as per CY2014

The weighted average price of the “Absorbed units”, which is at around INR 3500, has shown a healthy trend showing that the investors have an inclination to invest in the Jaipur housing real estate market.

CITY SUPPLY AND ABSORPTION TRENDS

11

C. Price-based Trends:

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

<2000 2000-4000 4000-6000 6000-8000 >8000

Un

its

New Launch Absorption Unsold Inventory

Source: PropEquity, ICICI Property Services Group. Note: Residential (Apartments, Villas and Floors) data for 2014 (from Jan-2014 to Sep-2014). Absorption is summation of new launches and unsold stock absorption.

D. Configuration-based Trends:

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1 BHK 2 BHK 3 BHK 4 BHK 5 BHK

Un

its

New Launch Absorption Unsold Inventory

Source: PropEquity, ICICI Property Services Group. Note: Residential (Apartments, Villas and Floors) data for 2014 (from Jan-2014 to Sep-2014). Absorption is summation of new launches and

unsold stock absorption.

BANGALORE RESIDENTIAL REAL ESTATE: SOUTH

CITY SUPPLY AND ABSORPTION TRENDS

12

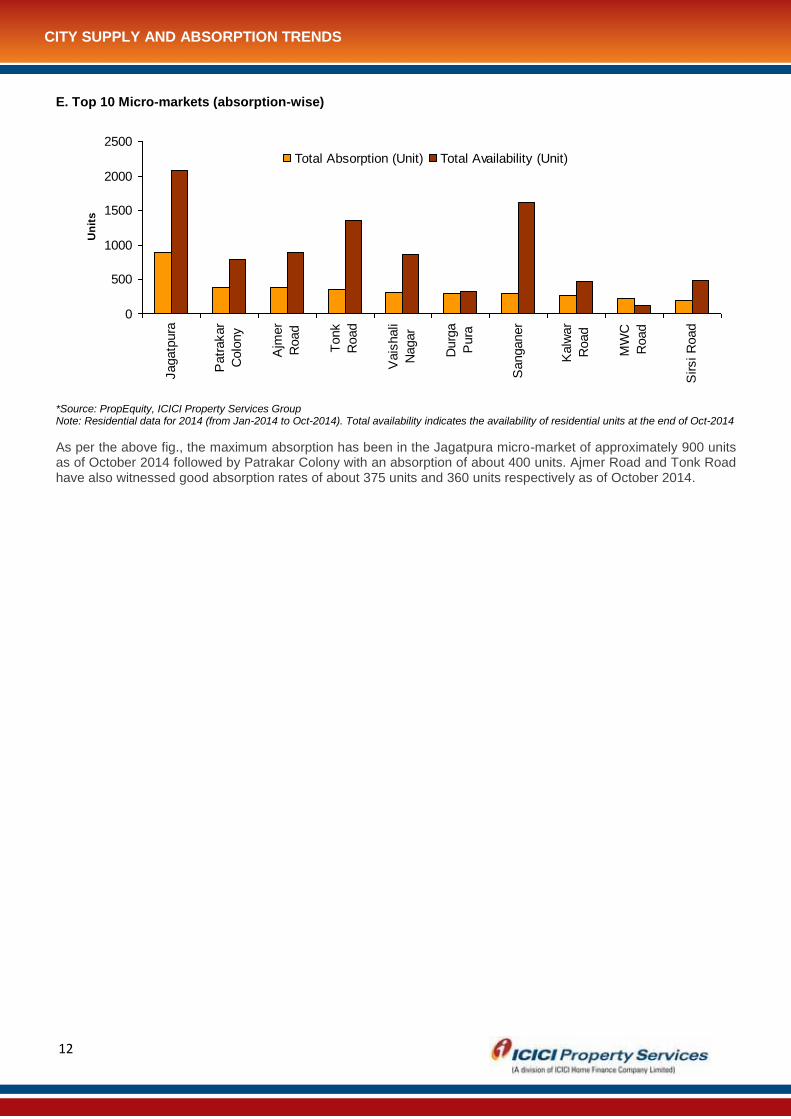

E. Top 10 Micro-markets (absorption-wise)

0

500

1000

1500

2000

2500

Jagatp

ura

Patr

akar

Colo

ny

Ajm

er

Road

Tonk

Road

Vais

hali

Nagar

Durg

a

Pura

Sanganer

Kalw

ar

Road

MW

C

Road

Sirsi R

oad

Un

its

Total Absorption (Unit) Total Availability (Unit)

*Source: PropEquity, ICICI Property Services Group Note: Residential data for 2014 (from Jan-2014 to Oct-2014). Total availability indicates the availability of residential units at the end of Oct-2014

As per the above fig., the maximum absorption has been in the Jagatpura micro-market of approximately 900 units as of October 2014 followed by Patrakar Colony with an absorption of about 400 units. Ajmer Road and Tonk Road have also witnessed good absorption rates of about 375 units and 360 units respectively as of October 2014.

CITY SUPPLY AND ABSORPTION TRENDS

13

For the purpose of this study, we have classified the real estate space in Jaipur into 5 distinct zones: Central, North, South, West and East based on the geographical location.

MAJOR LOCATIONS OF JAIPUR

14

Major Locations: Pink City, Adarsh Nagar, Bapu Nagar, C-Scheme, Civil Lines, M.I. Road, JLN Marg, Raja Park, New Sanganer Road, Panchsheel Colony, Shyam Nagar, Sodala, Tilak Nagar

Pink City is the old walled city built in pink stucco with well laid-out plan in 1727, and it is located towards the north-east of the city centre. All the old traditional shops and market places, various buildings of historical significance such as City Palace, Museum, Hawa Mahal and Jantar Mantar lie within this region. Residential development in this pocket is typically comprised of old independent houses, and no major residential up-gradation could be noticed here. The micro-market is end-user driven. This area primarily witnesses transactions in the secondary markets, and a lot of residential properties are being used for commercial purposes.

C-Scheme, one of the premium locations of Jaipur being located in the center of Jaipur and thus is well-

connected with other parts of Jaipur. The locality is primarily dominated by commercial development such as Axis Mall, Silver Square etc. From the residential development perspective, the micro-market has witnessed new constructions primarily being done on approximately 2000 sq. yards plots. It is an end-user driven micro-market and has witnessed a good price appreciation with the current rates hovering around 8,000 - 12,000/sqft.

Civil Lines is a prime location and is the residence of the Chief Minister of Rajasthan along with the other

important state dignitaries. Apart from premium independent houses, apartment complexes by renowned developers are also available in the price range of INR 8,000 to 10,000/sqft.

Bapu Nagar is situated to the south of the walled city. This area lies at the heart of Jaipur hence the real

estate costs typically lie on the higher side, in the range of INR 12,000 – 13,000/sqft. These areas are one of the oldest areas of Jaipur being the residence of mostly government employees (judges, IAS officers etc.) and generally comprise of smaller sized (1000 sq. yards to 2000 sq. yards) plots.

Adarsh Nagar is situated beyond the western walls of the Pink City. The place is an important commercial

centre in the city of Jaipur. The locality has good commercial / residential development and developer projects, though few, offer units priced at approximately INR 7,500 – 8,000/sqft.

The weighted average price of residential projects in the micro-markets of this region primarily lies on the

higher side lying in the price band of INR 8,000 – 12,500/sqft. Some of the key developers in this region are SDC, Pearl Spytech, Trimurthy, Om Group, Unique Builders, Unique Dream Builders, Mahima, Okay PLUS.

Source: PropEquity Note: Graph represents weighted average price of residential units available in the primary market. Missing line segments indicate unavailability of residential units in the primary markets during the specified time frame. *Quarters as per CY2014

CENTRAL JAIPUR

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

INR

/Sqft

Adarsh Nagar Bapu Nagar C Scheme Civil Lines Shyam Nagar

15

**Indicative mid-market segment Source: ICICI Property Services Group

Outlook Key: R - Rising F - Falling S - Stagnant SW - Stagnant but likely to weaken SS - Stagnant but likely to

strengthen

Locations Capital Values

(INR/sqft.)

Rental Values of 2 BHK

(INR/month)

Market Outlook

C-scheme 8000-12000 20,000-25,000 SS

Bapu Nagar 12000-13000 15,000-20,000 SS

Adarsh Nagar 7500-8000 8,000-10,000 SS

Civil Lines 8000-10000 15,000-20,000 R

Shyam Nagar 2800-3000 9,000-10,000 S

CENTRAL JAIPUR

16

Major Locations: Bani Park, Gopalbari, NH-11, Niwaru Road, Shastri Nagar, Sikar Road, Subhash Nagar, Sushant City, Vidhyadhar Nagar

Key Highlights:

Vidyadhar Nagar is one of the most prime localities of Jaipur due to its robust infrastructure structure

comprising of hospitals, schools, banking facilities, etc. This micro-market is primarily investment-driven with

the investments taking place in plots. The price lies in the range of INR 12,000 to 20,000 / sq. yard.

Sikar Road is primarily an industrial belt that witnesses some residential projects by local developers. It is

located along the Delhi Bypass connecting the heart of Jaipur to the Vishwakarma Industrial Area which is

the biggest operational RICCO industrial area of Rajasthan. This micro-market has the average ticket size (2

BHK) falling in the range of 30 – 35 lacs. The important driving factors for this micro-market are its proximity

to Vidyadhar Nagar and its good connectivity to the other parts of Jaipur through the Bus Rapid Transit

Service (BRTS) system.

Bani Park is a prime location of Jaipur, offering a mix of commercial and residential development. Various

Government offices, the collectorate and the civil court are located in this region. The region is predominantly

landscaped with independent houses but some apartment complexes can also be seen here. Average capital

values in this locality range from INR 6,000 to 7,500/sqft. approximately.

The weighted average price of residential projects in this region lies in the price band of INR 2000 – 4500/sqft

with the exception of Bani Park having a much higher weighted average price of INR 7000/sqft. Some key

developers are Vardhman Group, Siddha, Akshat, SDC Group, Ashiana, Mojika Group, GHP Group.

Source: PropEquity Note: Graph represents weighted average price of residential units available in the primary market. Missing line segments indicate unavailability of residential units in the primary markets during the specified time frame. *Quarters as per CY2014

Active Locations Capital Values

(INR/sqft.)

Rental Values of 2 BHK

(INR/month)

Market Outlook

Vidyadhar Nagar 4000-4500 10,000-15,000 R

Sikar Road 2500-3500 8,000-12,000 SS

Bani Park 6000-7500 12,000-15,000 SS

**Indicative mid-market segment Source: ICICI Property Services Group

Outlook Key: R - Rising F - Falling S - Stagnant SW - Stagnant but likely to weaken SS - Stagnant but likely to

strengthen

NORTH JAIPUR

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

INR

/sqft

Vidhyadhar Nagar Sikar Road Bani Park

17

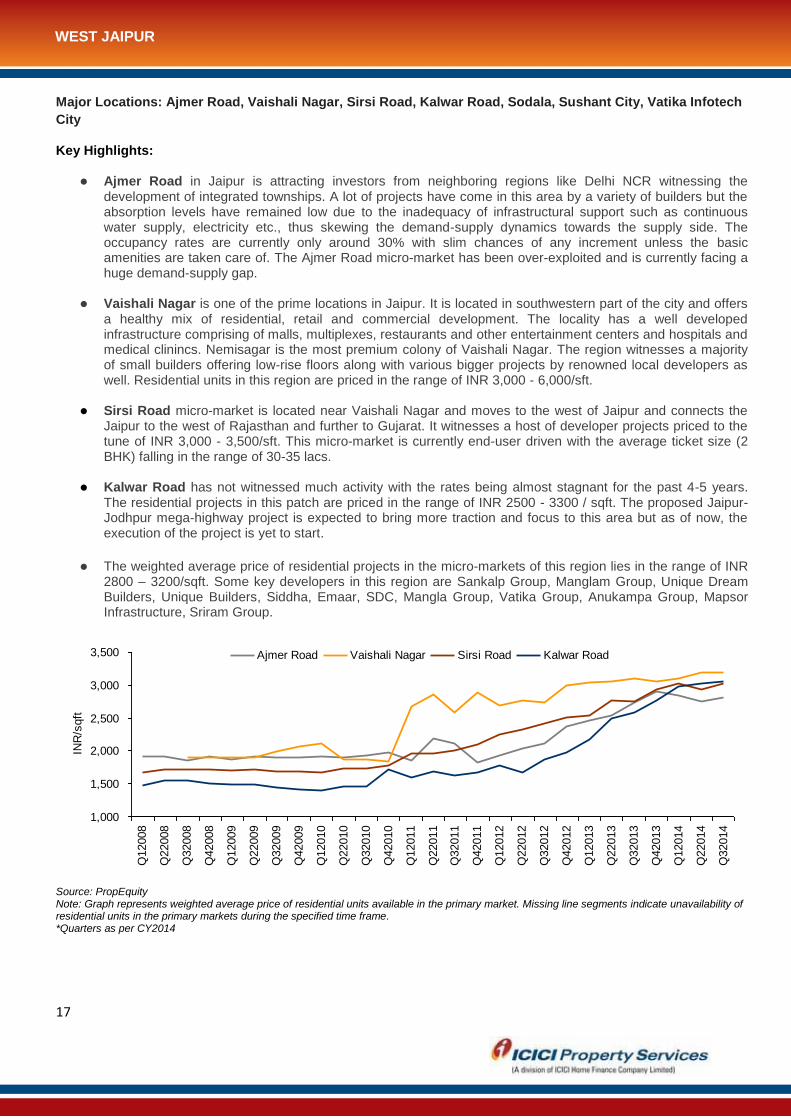

Major Locations: Ajmer Road, Vaishali Nagar, Sirsi Road, Kalwar Road, Sodala, Sushant City, Vatika Infotech

City

Key Highlights:

Ajmer Road in Jaipur is attracting investors from neighboring regions like Delhi NCR witnessing the development of integrated townships. A lot of projects have come in this area by a variety of builders but the absorption levels have remained low due to the inadequacy of infrastructural support such as continuous water supply, electricity etc., thus skewing the demand-supply dynamics towards the supply side. The occupancy rates are currently only around 30% with slim chances of any increment unless the basic amenities are taken care of. The Ajmer Road micro-market has been over-exploited and is currently facing a huge demand-supply gap.

Vaishali Nagar is one of the prime locations in Jaipur. It is located in southwestern part of the city and offers

a healthy mix of residential, retail and commercial development. The locality has a well developed infrastructure comprising of malls, multiplexes, restaurants and other entertainment centers and hospitals and medical clinincs. Nemisagar is the most premium colony of Vaishali Nagar. The region witnesses a majority of small builders offering low-rise floors along with various bigger projects by renowned local developers as well. Residential units in this region are priced in the range of INR 3,000 - 6,000/sft.

Sirsi Road micro-market is located near Vaishali Nagar and moves to the west of Jaipur and connects the

Jaipur to the west of Rajasthan and further to Gujarat. It witnesses a host of developer projects priced to the tune of INR 3,000 - 3,500/sft. This micro-market is currently end-user driven with the average ticket size (2 BHK) falling in the range of 30-35 lacs.

Kalwar Road has not witnessed much activity with the rates being almost stagnant for the past 4-5 years.

The residential projects in this patch are priced in the range of INR 2500 - 3300 / sqft. The proposed Jaipur-Jodhpur mega-highway project is expected to bring more traction and focus to this area but as of now, the execution of the project is yet to start.

The weighted average price of residential projects in the micro-markets of this region lies in the range of INR

2800 – 3200/sqft. Some key developers in this region are Sankalp Group, Manglam Group, Unique Dream Builders, Unique Builders, Siddha, Emaar, SDC, Mangla Group, Vatika Group, Anukampa Group, Mapsor Infrastructure, Sriram Group.

1,000

1,500

2,000

2,500

3,000

3,500

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

INR

/sqft

Ajmer Road Vaishali Nagar Sirsi Road Kalwar Road

Source: PropEquity Note: Graph represents weighted average price of residential units available in the primary market. Missing line segments indicate unavailability of residential units in the primary markets during the specified time frame. *Quarters as per CY2014

WEST JAIPUR

18

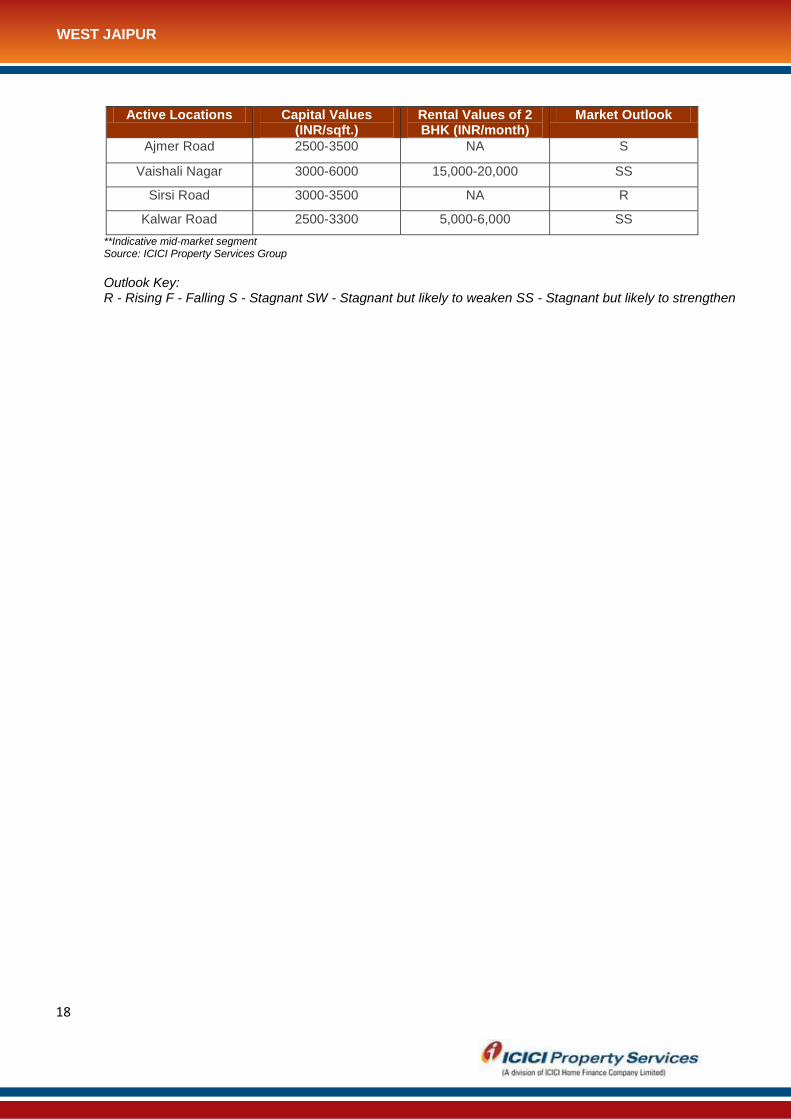

Active Locations Capital Values (INR/sqft.)

Rental Values of 2 BHK (INR/month)

Market Outlook

Ajmer Road 2500-3500 NA S

Vaishali Nagar 3000-6000 15,000-20,000 SS

Sirsi Road 3000-3500 NA R

Kalwar Road 2500-3300 5,000-6,000 SS

**Indicative mid-market segment Source: ICICI Property Services Group

Outlook Key: R - Rising F - Falling S - Stagnant SW - Stagnant but likely to weaken SS - Stagnant but likely to strengthen

WEST JAIPUR

19

Major Locations: Tonk Road, Sitapura, Jagatpura, Raj Aangan, NRI colony, Malviya Nagar, Milap Nagar, Jai Ambe Colony, Durga Pura, Jagatpura, Jawahar Circle Garden, Mansarover, Patrakar Colony, Pratap Nagar, Sanganer, Tonk Road, Mahindra World City Key Highlights:

Jagatpura is a well-planned area having the advantage of close proximity to the Sanganer Airport, the railway station and Sitapura industrial area. It is an upcoming location in the south-eastern part of Jaipur. The location is also set to become one of the major medical hubs in the region with Fortis Hospital, Apex Hospital, Narayan Hridayalaya falling in the vicinity of Jagatpura and two proposed healthcare projects of Bombay Hospital and Reliance Mega Medicity would further strengthen the healthcare landscape of the area. The area has witnessed price appreciation of approximately 40% in last two years. Investment in this market has seen an uptrend because of availability of regular rental income being a major educational hub due to the presence of various technical universities located in this area. This micro-market has been the focus of the present political establishment which can be gauged from the fact that approx. INR 55 crores have been sanctioned for constructing a dam to cater to the water needs of the area.

Tonk Road is an important connecting link of Jaipur that runs parallel to the Jagatpura micro-market. It is

well-connected with the central part of the city and the Tonk Road micro-market (beyond the B2 Bypass road) has good connectivity with other parts of Jaipur due to the availability of ample public transport facilities. The area has good potential of developing with a string of projects coming up in the area.

Malviya Nagar is a prime location in the southern precincts of Jaipur. Named after the noted freedom fighter

Madan Mohan Malviya, the location has a good mix of commercial, retail and residential development. The region hosts good civic amenities with schools, hospitals, multiplexes and malls that cater to the whole city. Jaipur International airport terminal 2 is located in vicinity to the region. The activity is present primarily in the secondary (resale) market in this area.

Mansarovar, touted as Asia's third largest colony, was established by the Rajasthan Housing Board and thus

is a well-planned market. The region caters to a mix of Low Income Group (LIG), Middle Income Group (MIG) and High Income Group (HIG) segments. The development has predominantly been low rise; however, there are plans to go vertical. Being the starting point of Phase 1 of the Jaipur Metro which is currently undergoing trial runs will be an important driving factor for the area. Currently, the micro-market is primarily driven by secondary (resale) market.

Patrakar Colony is placed approximately 2.5 km from the Mansarovar Colony and 5 km from the Sanganer

Airport. The region is also located in close proximity to the Mahindra SEZ. The region witnesses the presence of various good local developers. It has a high growth potential being close to the Mansarovar Metro Station. The occupancy in this area is currently of independent floors and low-rise apartments. The capital values lie in the range of INR 3,500 - 4,000 / sqft.

Durgapura is a densely populated residential area and having one of the best proximity and connectivity to

the major commercial/retail hubs of Jaipur. The good connectivity is due to the fact that it lies along the Tonk Road with the airport only a kilometer away and Durgapur Railway Station lying within the area itself. Investors are willing to invest in this area as it lies at the center of major developed hubs of Jaipur such as Mansarovar, Sanganer and Malviya Nagar.

Mahindra World City is likely to gain impetus from the huge employment opportunities generated because of

the Mahindra SEZ and act as a part of the infrastructure to support the upcoming employment opportunities. NRI Colony is dotted with bungalows and row houses with Jagatpura placed close to this location.

The weighted average price of residential projects in the micro-markets of this region primarily lies in the

range of INR 2500 – 4000/sqft. Some key developers in this region are Akshat, Ashiana, Mojika, SDC, Pearl Spytech, Trimurthy, Om Group, Unique Builders, Unique Dream Builders, Mahima Group.

SOUTH JAIPUR

20

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000Q

12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

INR

/sqft

Jagatpura Malviyanagar Tonk Road Durga pura

Patrakar Colony Mansarover Mahindra World City

Source: PropEquity Note: Graph represents weighted average price of residential units available in the primary market. Missing line segments indicate unavailability of residential units in the primary markets during the specified time frame. *Quarters as per CY2014

Location Capital Values (INR/sqft.)

Rental Values of 2 BHK (INR/month)

Market Outlook

Jagatpura 2500-3500 8000-10000 R

Tonk Road 2500-3200 12000-15000 R

Malviya Nagar 3000-3500 15000-20000 R

Patrakar Colony 3500-4000 8,000-10,000 R

Mansarovar NA 10,000-15,000 SS

Durgapura 5000-5500 NA S

Mahindra World City 3000-3200 NA R

**Indicative mid-market segment Source: ICICI Property Services Group

Outlook Key: R - Rising F - Falling S - Stagnant SW - Stagnant but likely to weaken SS - Stagnant but likely to strengthen

SOUTH JAIPUR

21

Major Locations: Agra Road, Amer Road, Goner Road, Ramgarh Road Key Highlights:

Agra Road: This is the only active micro-market of this region currently as the region is restricted due to

the Nahargarh Hills. The area has seen an uptrend in terms of the pricing. The proposed infrastructural projects in this area as it will prove beneficial for it in future as it will have good connectivity because of the Proposed Ring Road and being a part of the Golden Triangle connecting Jaipur-Delhi-Agra enhancing tourism and investment opportunities. As per Master Plan 2015, it is being developed as a Satellite Town of Jaipur and the Sector Road Plan for Agra Road has been launched.

The weighted average price of residential projects in this region primarily lies in the range of INR 2500 –

3000/sqft. Some key developers in this region are SDC, Pearl Spytech, PinkCity Infracon.

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

3,000

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

INR

/Sqft

Agra Road Goner Road

Source: PropEquity Note: Graph represents weighted average price of residential units available in the primary market. Missing line segments indicate unavailability of residential units in the primary markets during the specified time frame. *Quarters as per CY2014

Location Capital Values

(INR/sqft.) Rental Values of 2 BHK (INR/month)

Market Outlook

Agra Road 2500-3000 NA SW

**Indicative mid-market segment Source: ICICI Property Services Group

Outlook Key: R - Rising F - Falling S - Stagnant SW - Stagnant but likely to weaken SS - Stagnant but likely to strengthen

EAST JAIPUR

22

Jagatpura Tonk Road

Vaishali Nagar

C-scheme Bapu Nagar

Ajmer Road

Patrakar Colony

Kalwar Road

Sikar Road

Sirsi Road

Mahindra World City

Connectivity and Infrastructure

(Schools, markets, healthcare)

Residential Cost

Proximity to Organized Retail

Proximity to Commercial

Development

Scope of Future Infrastructure Development

Scope of Future Employment Generation

Good / low cost

Above Average / below average cost

Average / Medium Cost

Below Average / above average cost

Bad / High Cost

Source: ICICI Property Services Group

Explanatory Note: The C-Scheme micro-market scores above other locations in terms of infrastructure as it has been developed as one of the commercial hubs of Jaipur; Vaishali Nagar, Bapu Nagar, Jagatpura, Tonk Road, Sikar Road also have good civic infrastructure. Jagat pura, Ajmer Road, Tonk Road and Patrakar Colony are expected to have good infrastructure in future. The scope of future employment generation is highest in micro-markets of Jagatpura, Tonk Road, C-scheme, Sikar Road and Mahindra World City which will an important driving factor for them.

LOCATION ATTRACTIVENESS INDEX

23

ANALYST

TANAY AGARWAL Assistant Manager – Research ICICI Home Finance Ltd. [email protected] We acknowledge Gaurav Maheshwari, Manager, ICICI Bank for his contribution towards this report

For any further queries, please e–mail us at [email protected]

or

For more on our research reports & periodicals please log on to www.icicihfc.com

ICICI HFC DISCLAIMERS & DISCLOSURES

The information set out in this document has been prepared by ICICI HFC Ltd. based upon projections which have

been determined in good faith by ICICI HFC Ltd. There can be no assurance that such projections will prove to be

accurate. Past performance cannot be a guide to future performance.

The information in this document reflects prevailing conditions and our views as of this date, all of which are subject

to change. In preparing this document we have relied upon and assumed, without independent verification, the

accuracy and completeness of all information available from public sources or which was provided to us or which

was otherwise reviewed by us. ICICI HFC Ltd. does not accept any responsibility for any errors whether caused by

negligence or otherwise or for any loss or damage incurred by anyone in reliance on anything set out in this

document. No reliance may be placed for any purpose whatsoever on the information contained in this document or

on its completeness

The product(s)/service(s)/offer(s) as contained herein are provided /offered by third party and are subject to their

respective terms and conditions and not intended to create any rights or obligations.

The information set out in this document may be subject to change and such information may change materially.

This document is being communicated to you solely for the purposes of providing our views on current market trends on a

confidential basis and does not carry any right of publication or disclosure to any third party. By accepting delivery of this

document each recipient undertakes not to reproduce or distribute this presentation in whole or in part, nor to disclose any

of its contents (except to its professional advisers) without the prior written consent of ICICI HFC Ltd., who the recipient

agrees has the benefit of this undertaking. The recipient and its professional advisers will keep permanently confidential

information contained herein and not already in the public domain.

This document is not an offer, invitation or solicitation of any kind to buy or sell any product/ service and is not

intended to create any rights or obligations. Nothing in this document is intended to constitute legal, tax, securities

or investment advice, or opinion regarding the appropriateness of any investment, or a solicitation for any product

or service. The use of any information set out in this document is entirely at the recipient's own risk. Recipients of

this Information should exercise appropriate due diligence, including legal and tax diligence, prior to taking of any

decision.