Itu - Airline Strategies and Business Models Alex...

73

Airline Strategies and Business Models Alex Philip & Bruce Tecklenburg Fundamentals of Airline Management Module 4: 13 October 2015 Istanbul Technical University Air Transportation Management M.Sc. Program

Transcript of Itu - Airline Strategies and Business Models Alex...

Airline Strategies and Business ModelsAlex Philip & Bruce Tecklenburg

Fundamentals of Airline Management

Module 4: 13 October 2015

Istanbul Technical University

Air Transportation Management

M.Sc. Program

2

Objectives

Connect market segments and passenger expectations

Connect potential airline business models with

passenger expectations

Connect deregulation and potential airline business

models

Connect partnering strategies and alliances with both

deregulation and airline business models

Connect cargo strategy impact on airline success

Regulatory

Environment

Technology

Airline and

Industry

Strategies

Passenger

Expectations

The passenger is at the center

4

Passenger market is segmented

Business

30% Travel

40-50%

Revenue

Personal

70% Travel

50-60% Revenue

Short-Haul

65% Travel

Long-Haul

35% Travel

Long-haul

business

Long-haul

personal

Short-haul

business

Short-haul

personal

5

Business

30% Travel

40-50% Revenue

Personal

70% Travel

50-60% Revenue

Short-Haul

65% Travel

Long-Haul

35% Travel

Long-haul

business

Long-haul

personal

Short-haul

business

Short-haul

personal

Table exercise/discussion questions

1. What are three key passenger expectations for your market segment?

2. How are these passenger expectations changing?

6

Market forecast drivers and considerations

Infrastructure Economicgrowth

Marketliberalization

Emergingmarkets

Fuelprice

Airlinestrategies &

businessmodels

Airplanecapabilities Environment

Highspeed

rail

CurrentMarketOutlook

2015-2034

Regulatory

Environment

Technology

Airline and

Industry

Strategies

Passenger

Expectations

The passenger is at the center

Copyright © 2015 Boeing. All rights reserved.

History

International air transportation is

mostly negotiated between two

countries (bilateral)

Under the framework first

introduced in the 1944 Chicago

Convention

Increasing liberal agreements over

last twenty years

Open Skies deals are the most

liberal

Chicago Convention framework is

still being used

Ownership remains to be nationally

based

9

A typical bilateral (except Open Skies)

Negotiated between two sovereign nations

Specified type of traffic allowed (traffic freedoms)

May specify: airlines, airports, capacity, frequency & fares

Typically includes a “nationality” clause

Reciprocity

Any changes have to be approved by both governments

Typical Example:

• Total 18 frequencies per day

allocated to specific route groups

• No gauge restrictions

• Fare: no restrictions

• Must be Chinese controlled airlines

10

Open Skies Agreement

What’s different:

Agreement can be bilateral, multi-

lateral, or by joint political entity

(e.g., EU)

Typically no traffic restrictions

other than domestic (Cabotage)

No limitations on airline

designations, points served,

service levels (frequencies &

seats), nor fares

Changes in services do not have to

be approved by both governments

What remains:

“Nationality” clause

Reciprocity

11

Current model Open-Skies agreement

Reference: http://www.state.gov/e/eb/rls/othr/ata/114866.htm

12

Traffic rights

13

4 Nothing in this article shall be deemed to confer on the airline or airlines of one Party the

rights to take on board, in the territory of the other Party, passengers, baggage, cargo, or mail

carried for compensation and destined for another point in the territory of that other Party.

- No Cabotage (Eighth & Ninth Freedoms)

(i) for airlines of the United States, from points behind the United States via

the United States and intermediate points to any point or points in

[country] and beyond; [and for all-cargo service, between [country] and

any point or points - Seventh Freedom

Traffic rights

(a) the right to fly across its territory without landing - First Freedom

(b) the right to make stops in its territory for non-traffic purposes - Second Freedom

(i) for airlines of the United States, from points behind the United States via

the United States and intermediate points to any point or points in

[country] and beyond; [and for all-cargo service, between [country] and

any point or points - Sixth Freedom

(i) for airlines of the United States, from points behind the United States via

the United States and intermediate points to any point or points in

[country] and beyond; [and for all-cargo service, between [country] and

any point or points - Fifth Freedom

(i) for airlines of the United States, from points behind the United States via

the United States and intermediate points to any point or points in

[country] and beyond; [and for all-cargo service, between [country] and

any point or points - Third & Fourth Freedoms

14

Freedoms of the Air

15

Perth

Cairns

Melbourne

Sydney

Brisbane

Christchurch

Auckland

Wellington

Adelaide

Gold Coast

Trans-Tasman

Nonstop Services

April 2006

Palmerston

Dunedin

Hamilton

Queenstown

Analysis of Growth in Major Markets vs. Non Major Markets

1994 - 2004

Australian Bureau of Transport and Regional Economics

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

To

tal P

assen

gers

- M

ajo

r M

ark

ets

-

100,000

200,000

300,000

400,000

500,000

600,000

To

tal P

assen

gers

- N

on

Majo

r M

ark

ets

Major Markets Non Major Markets

CAGR for Non

Major Markets -

14.45%

CAGR for Major

Markets 7.10%

Source: Australian Bureau of Transport and Regional Economics, International City Pair Data

Major Markets includes all routings between main New Zealand markets (Auckland, Christchurch, Wellington) and Australian markets

(Sydney, Melbourne, Brisbane)

Open Skies can stimulate growth

even in mature markets

Australia – New Zealand Trans-Tasman Open Skies Agreement 2000

16

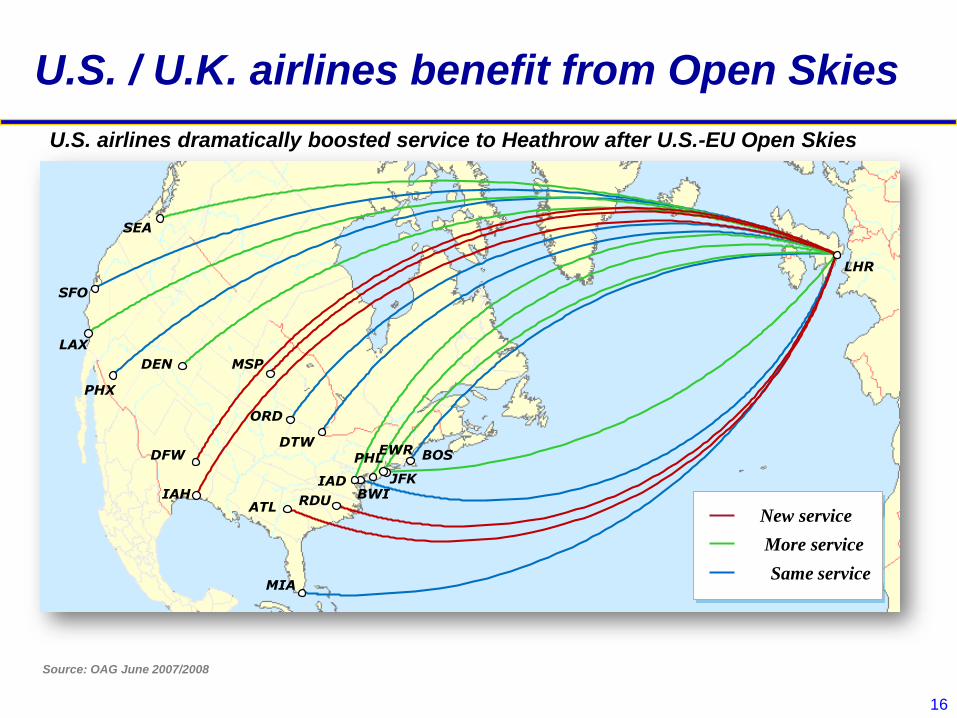

U.S. / U.K. airlines benefit from Open Skies

Source: OAG June 2007/2008

LHR

ATL

DEN

DFWDTW

IAH

LAX

MSP

ORD

PHX

RDU

SEA

SFO

BOS

BWI

EWR

IAD JFK

PHL

MIA

New service

More service

Same service

U.S. airlines dramatically boosted service to Heathrow after U.S.-EU Open Skies

17

US-EU Open Skies transformed market landscapeTrans-Atlantic traffic share of ATI JVs now 75%

Traffic share measured by ASK

18

Ownership

19

But Ownership Restrictions Remain

a. Substantial ownership and effective control of that airline are vested in the other Party,

nationals of that Party, or both

20

Airlines are pursuing more cross-

border ownership arrangements

Chicago Convention introduced sovereignty concept but left to

each nation to define criteria for national carriers

Uncommon to see restrictions allowing above 49% foreign ownership

Recent cross-border investments have focused on

consolidation of network airlines and LCCs

Air France/KLM, IAG, Latam for example

JetStar, Air Asia, Lion Air, Tiger, Indigo Partners

Various legal structures have been used to meet national

ownership and control requirements

21

Many factors drive strategic plans

Airline Business Models

Business Personal

Short-Haul

Long-Haul

Regulatory

Environmen

t

Technology

Airline and

Industry

Strategies

Passenger

Expectations

22

Low cost carriers have changed the industry

Business

30% Travel

40-50%

Revenue

Personal

70% Travel

50-60% Revenue

Short-Haul

65% Travel

Long-Haul

35% Travel

LCCs

23

Southwest was designed to serve

short-haul markets

Capitalized on underserved

short-haul markets

Business shuttle focus

Low fare traffic stimulation

Southwest Airlines in 1971 – “Texas Triangle”

DAL

SAT HOU

24

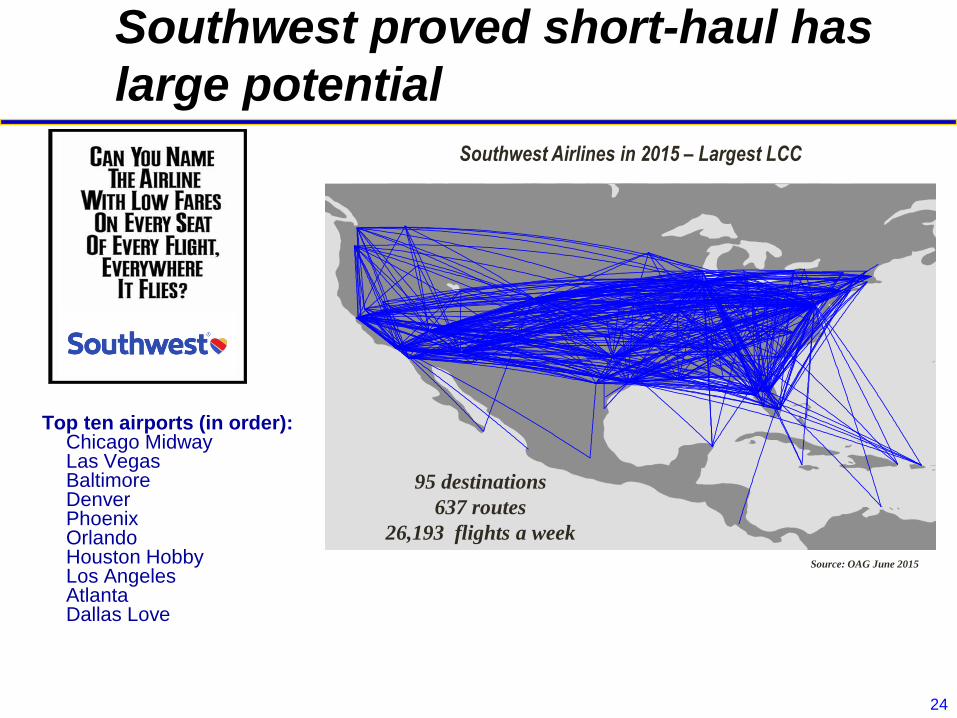

Southwest proved short-haul has

large potential

Top ten airports (in order):Chicago MidwayLas VegasBaltimoreDenverPhoenixOrlandoHouston HobbyLos AngelesAtlantaDallas Love

Source: OAG June 2015

Southwest Airlines in 2015 – Largest LCC

95 destinations

637 routes

26,193 flights a week

2525

Traditional LCC business model characteristics

Traditional LCC business model highly successful, but evolving

• Network/Schedule

• Simplified network (P2P)

• Secondary airports; multiple bases

• Relatively short-haul

• Fare/Product Mix

• One-cabin class

• No seat assignments

• Basic service (reduced frills)

• Ancillary revenues

• No frequent flier program

• Operations

• Common fleet

• High utilization

• Avoidance of global distribution system

• Low labor / avoid unions

• Stand-alone airline (no subsidiaries)

26

19.4

13.711.9

10.3 9.8

02468

101214161820

Avg. of USmajor

networkcarriers

Southwest JetBlue Allegiant Spirit

LCC unit cost advantage is critical

Unit costs in US cents/ASM, 2013

Source: US DOT Form 41

Stage length adjusted to system average

LCCs must achieve at least 20-40% lower cost

than network carriers

27

Low costs and fares stimulate growth

Local traffic and average yields in three Minneapolis

markets before and after LCC entry

Source: Sabre ADI, 2009-20110

150,000

300,000

450,000

600,000

750,000

Denver (DEN) Chicago (MDW) St. Louis (STL)

Before SWA After SWA

22¢

27¢

48¢

30¢

42¢A

nn

ua

l O

&D

Pa

ssen

ger

s

75¢

60¢

45¢

30¢

15¢

16¢

28

LCC websites are powerful tools

Majority of reservations are

via the websites

Cost benefits:

– No commissions

– No GDS fees

Revenue benefits:

– Up-selling opportunities

– Fees for letting other

companies use the website

Relationship benefits:

– Millions of visitors

– Direct, on-going customer

contact

29

LCC business model origin1990: U.S. LCCs growing/emerging in E.U.

Source: Aug 1990 OAG

LCCs in 1990

30

LCC business model has gone worldwide

Oceania

Flights/week: 2,640

km/flight: 1,640

Today LCC’s operating in most regions

SE Asia

Flights/week: 19,740

km/flight: 1,160

NE Asia & China

Flights/week: 11,900

km/flight: 1,040

S Asia

Flights/week: 7,150

km/flight: 1,060

Middle East

Flights/week: 3,250

km/flight: 1,600

Europe & CIS

Flights/week: 39,500

km/flight: 1,190

Latin America

Flights/week: 13,400

km/flight: 980

Source: 2014 Diio/Innovata

Africa

Flights/week: 960

km/flight: 1,080

North America

Flights/week: 39,450

km/flight: 1,400

31| 31

54%

50%

36%

33%

29%

28%

26%

16%

12%

9%

9%

1%

SE Asia

S Asia

Europe

Lat America

N America

World

Oceania

NE Asia

Middle East

Africa

China

Former CIS

Source: Diio/Innovata 2015, jets only

Only Selected Regions Have Low LCC

Penetration2014 LCC market share - measured in annual seats

(by airline domicile)

32

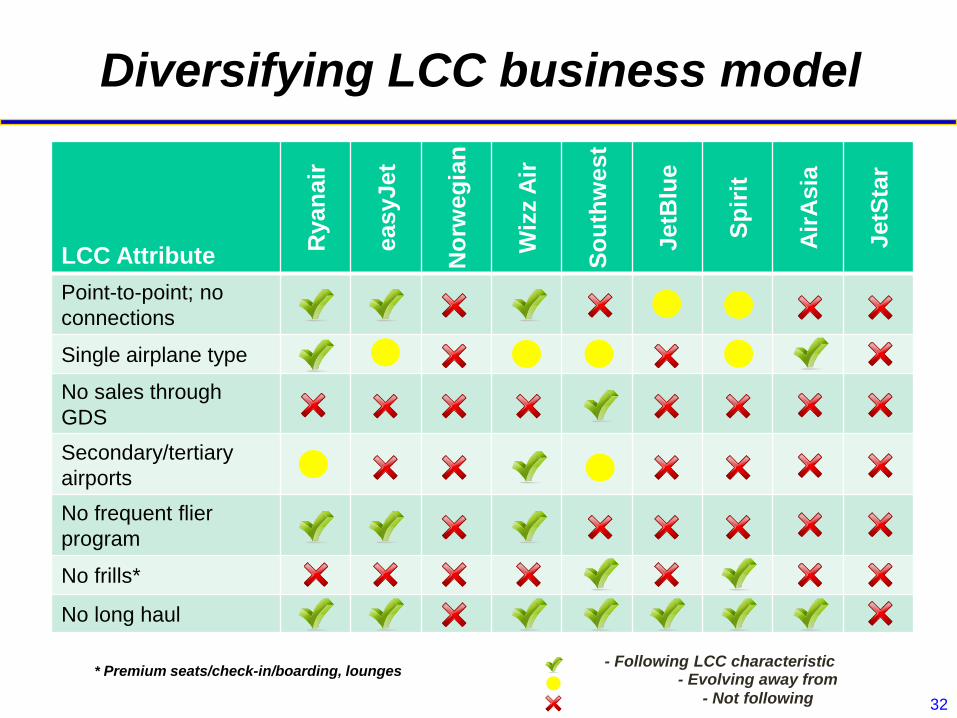

Diversifying LCC business model

LCC Attribute

Ryan

air

easyJet

No

rweg

ian

Wiz

z A

ir

So

uth

west

JetB

lue

Sp

irit

Air

Asia

JetS

tar

Point-to-point; no

connections

Single airplane type

No sales through

GDS

Secondary/tertiary

airports

No frequent flier

program

No frills*

No long haul

* Premium seats/check-in/boarding, lounges- Following LCC characteristic

- Evolving away from

- Not following

33

Medium-Haul LCCs

Asia pacific is center of Medium-haul LCCs

OAK-ARN

(8583km)

LAX-CPH

(9024km)

OSL-BKK

(8668km) ARN-BKK

(8291km)

MCO-VCP

(6799km)

RUH-

MNL

(7772km)

JED-KUL

(7060km)

DXB-MNL

(6902km) NRT-OOL

(7237km)

MEL-HNL

(8871km)

SIN-AKL

(8406km)

Source: 2014 Diio/Innovata – for wide-body service from Norwegian, AirAsia X (incl. Thai, Indonesia), Jetstar, Cebu Pacific, Scoot, Azul, Pal Express

35

Global Network business model

Business

30% Travel

40-50%

Revenue

Personal

70% Travel

50-60% Revenue

Short-Haul

65% Travel

Long-Haul

35% Travel

Focus on multiple passenger segments

36

Global network carriers are large

Rank Airline RPK(billions)

1 American Airlines & US Airways 350.7

2 United Airlines 330.9

3 Delta Air Lines 326.6

4 Emirates 230.9

5 Air France-KLM 229.3

6 Lufthansa Group 214.6

7 IAG 202.6

8 Southwest Airlines :LCC 173.9

9 China Southern Airlines 166.6

10 Air China 154.7

Top airlines by RPKs - 2014

Source: ICAO, IATA, airline annual reports, Boeing analysis

RPKs Share

Global

Network

Top 9:34%

37

Common characteristics with Global

Network model

Large complex fleets

Major hub operations

Domestic and Int’l markets

Bilaterally controlled environment

Long haul & short haul routes

Broad range of service levels

First class, airport lounges, onboard meals

and IFE

Economy, buy on board, ancillary fees

Alliance membership

Serving multiple segments increases complexity

38

Hubs increase reach of Network airlines

The connecting hub and spoke network has become

the dominant airline business model

City A

City B Hub

City D

City C

City E

City F

3 airplanes : 15 city pairs

39

Hubs must create value

ATH

LHR

DUBMAN

EDI

MIA

LAX

SFO

YVR

ORDYYZ BOS

JFK

IAD

PHL

Example London (LHR) to Athens (ATH)

Other 10

45

10

10

9

8

76

6

65

4

3

3

2

LOCAL PAX 45

CONNECTING PAX 89

134 TOTAL PAX

Collect traffic at one point to create volume for non-stop service

40

Networks are best for serving small markets

0%

2%

4%

6%

8%

10%

12%

14%

16%

<6 <12 <25 <50 <100 <200 <400 <800 <1600 1600+

O&D Passengers per Day

Sh

are

of

Wo

rld

RP

Ks

Connecting Markets Nonstop Markets

Source: Boeing Hub Development Analysis

98% of all of the World’s markets have less than 10 PDEW

41

Gulf 3 success: one stop to everywhere

20

04

20

14

EmiratesQatarEtihad

• 6th Freedom business model

but with differentiation

• Prime location

• Supportive governments

• Efficient operation

• Strong brands

• Enabled by 8000NM aircraft

42

An 8 hour flight is within reach of…

~15% of the World’s Population >80% of the World’s Population

Gulf 3 business model is strategically located to serve more than 80% of the world’s population

within an 8 hour flight of Dubai

www.gcmap.com : Range circles at 4,000 mi

43

Airport congestion can impede network

airline growth

Work to maximize convenience and minimize hassles

44

Business travel is vital to most network airlines

Burning questions

Will business travel keep growing?

How can airlines prevent business

travelers “buying down” to

economy?

Long-haul business travelers value

comfort, convenience, and reliability,

but how much?

Short-haul business travelers

value convenience and reliability,

but are increasingly price sensitive.

What will they value in the future?

Business traveler expectations can change

45

Differentiation for different market

segments

Airport

Boarding pass on

mobile devices

Automated boarding

Lounges

On board

First

Business

Premium Economy

Economy

Value analysis: revenue benefits vs associated costs

46

Non-global Network Carriers face

challenges

Business

30% Travel

40-50%

Revenue

Personal

70% Travel

50-60% Revenue

Short-Haul

65% Travel

Long-Haul

35% Travel

Global Network

Non-global Network

47

How do non-global network carriers

differ from global network carriers?

• Typically lower fleet complexity

• Typically just one key hub

• Can be domestic only or both

domestic and international

• Long-haul might just be Transcon

• Business travel remains key

• Partnering levels vary

48

Charter Carriers evolving due to LCC

competition

Business

30% Travel

40-50%

Revenue

Personal

70% Travel

50-60% Revenue

Short-Haul

65% Travel

Long-Haul

35% Travel

Global Network

Charter

49

Charter carrier characteristics

• Targets leisure travelers

• Often inclusive tour

packages

• Seasonal markets

• High load factors and

utilization rates

• In direct competition with

LCCs

50

LCC

Business Personal

Short-Haul

Long-Haul

Non-global Network Charter

Global Network

Class exercise

Global Network Carrier Non-global Network Carrier LCC

1 2 3

For the segments shown below:

• What are the challenges in capturing these passengers?

• What strategies/tactics might be used?

Business

Short-Haul

Business

Long-Haul

Business

Short-Haul

51

LOW

HIGH

Limited cooperation on specific routes

Expanded cooperation to develop joint

network

Anti-trustjoint venture

Airline cooperation takes different forms

52

Code sharing routes have increased at a

7.8% CAGR over the last decade

OAG August

Over half of worldwide ASKs are code sharing

-

20

40

60

80

100

120

140

160

180

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Billio

ns

Worldwide weekly ASK

Code Sharing

Non code sharing

Code sharing

40.9%

Code sharing

57.1%

Example: Qantas had 134 airport pairs in 2014 flying their own metal

― Own metal ― Partner metal OAG Aug,2014Network (2014)

<Airport-pairs>

Own Partner Total

134

Qantas’s airport pairs 4X with code sharing

― Own metal ― Partner metal OAG Aug,2014Network (2014)

Own Partner Total

134 346 480

<Airport-pairs>

Turkish Network

― Own metal ― Partner metal Innovata Sep 2015Network (Sep 2015)

<Airport-pairs>

Own Partner Total

335 614

Turkish with codeshare

― Own metal ― Partner metal Innovata Sep 2015Network (Sep 2015)

<Airport-pairs>

Own Partner Total

335 279 614

57

Alliances have become a powerful tactic

Expand network / enhance revenue / reduce costs

58

0

5

10

15

20

25

30

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

One World Sky Team Star

0%

10%

20%

30%

40%

50%

60%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Source: OAG, BCA Analysis

Alliances are maturing

Number of Airlines

% of Global Scheduled ASM

59

Star Alliance oneworld SkyTeam Major Unaligned

U.S./Canada

Europe

Asia Pacific

Other

Airline alliances members as of December 2014

60

Deeper partnering and ownership strategies

Subsidiaries

Acquisitions

Mergers

61

Airlines are creating subsidiaries for

many purposes

Broadening customer base

Offering multiple brands

Serving customers in different

regions

Often required by foreign

ownership limits that prevent

full consolidation

Diversifying airline business

activities

Examples

50/50

62

Airlines invest in other airlines for multiple

reasons

40% 21.2%24%

4%

49%

33.3%

29%49%

To gain access to

restricted markets

To gain needed

network feed

To overcome

alliance weakness

To gain valuable

airport slots

Note: Darwin Airline was renamed to

49% 2.98%3.5%

10%

5% 29.9%

63

Airline mergers

Mergers can provide multiple

benefits

Rationalization of costs (including

capacity discipline)

Expand market access and global

reach

Ability to compete with competitor

mergers

Recent major carrier mergers have

been important to remain

competitive

Cross-border mergers can be

highly creative in working with

foreign ownership restrictions

Major mergers

64

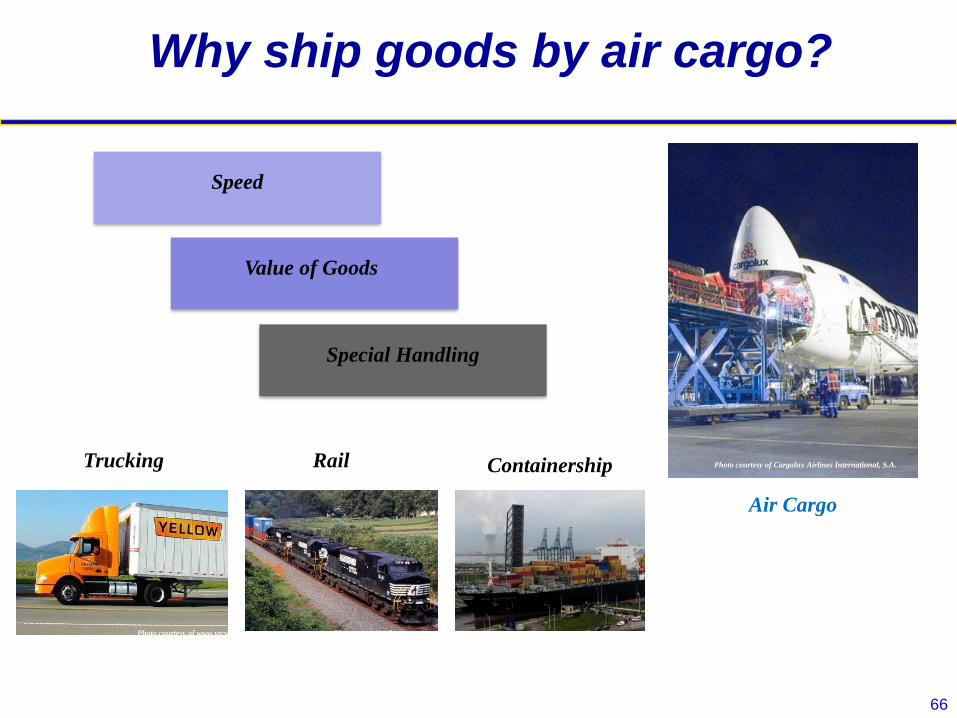

Air Freight Express Mail

Air Cargo

65

Two major business models

1. Panalpina

2. Expeditors

3. DB Schenker

4. Kuehne+Nagel

5. Hellmann

Freight forwarders act as intermediaries between airlines and shippers

Express Carrier/Integrators

General Cargo Carrier

66

Why ship goods by air cargo?

Photo courtesy of www.yrcw.com Photo courtesy of www.nscorp.com

Photo courtesy of Cargolux Airlines International, S.A.Trucking Rail Containership

Air Cargo

Speed

Value of Goods

Special Handling

67

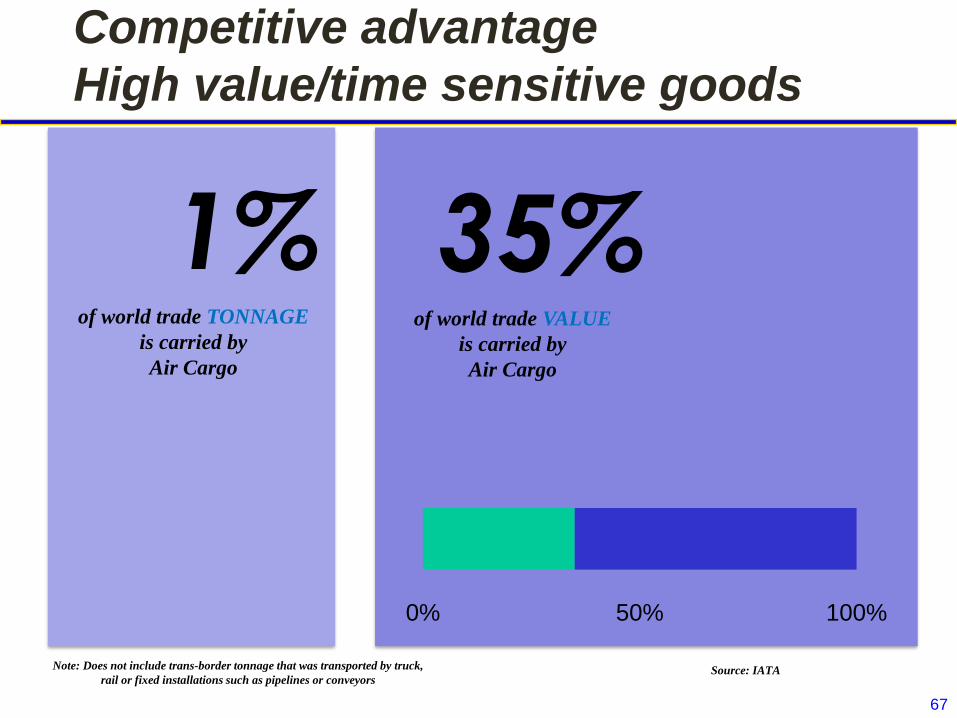

Competitive advantage

High value/time sensitive goods

1%of world trade TONNAGE

is carried by

Air Cargo

35%of world trade VALUE

is carried by

Air Cargo

0% 50% 100%

Note: Does not include trans-border tonnage that was transported by truck,

rail or fixed installations such as pipelines or conveyorsSource: IATA

68

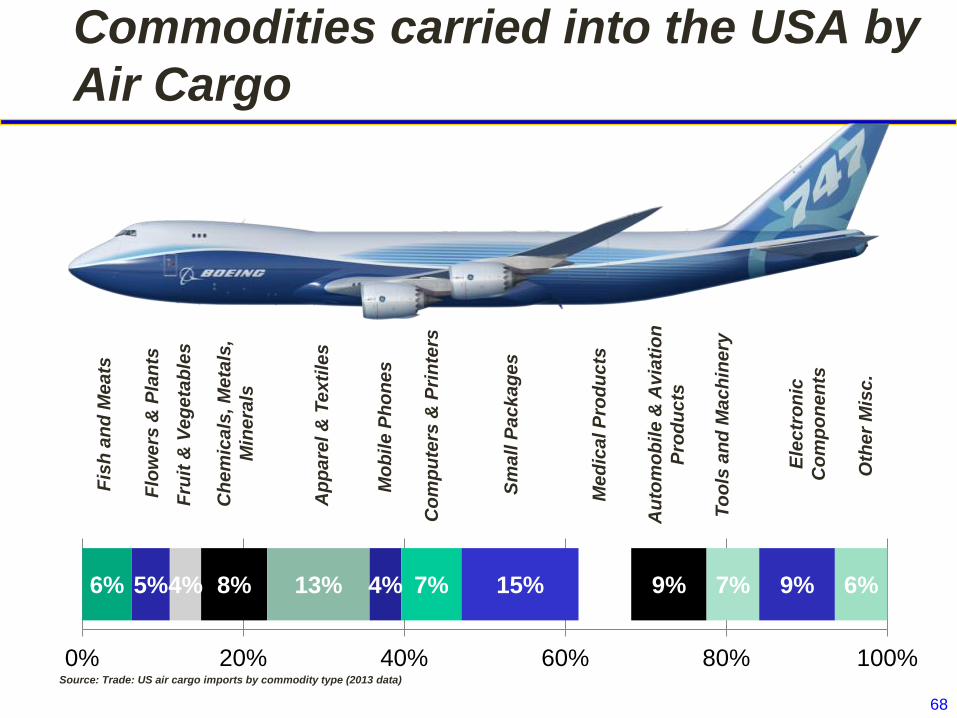

6% 5%4% 8% 13% 4% 7% 15% 7% 9% 7% 9% 6%

0% 20% 40% 60% 80% 100%

Fis

h a

nd

Me

ats

Flo

we

rs &

Pla

nts

Fru

it &

Ve

ge

tab

les

Ch

em

ica

ls, M

eta

ls,

Min

era

ls

Ap

pa

rel &

Te

xti

les

Mo

bil

e P

ho

ne

s

Co

mp

ute

rs &

Pri

nte

rs

Sm

all

Pa

ck

ag

es

Me

dic

al P

rod

uc

ts

Au

tom

ob

ile

& A

via

tio

n

Pro

du

cts

To

ols

an

d M

ac

hin

ery

Ele

ctr

on

ic

Co

mp

on

en

ts

Oth

er

Mis

c.

Source: Trade: US air cargo imports by commodity type (2013 data)

Commodities carried into the USA by

Air Cargo

69

Total air cargo industry revenue by business model

Express carriers

38%

Combination carriers

41%

All cargo11%

Passenger belly only

10%

World air cargo revenue

$92.6 billion

Express

carriers$35.1B

Combination

carriers

$38.3B

Passenger

belly only$9.5B

All cargo$9.7B

Sources: Air Transport Intelligence, U.S. DOT F41, Boeing estimates, and airline reports. (2012

Data)

Freighters, directly or indirectly, contribute to 90% of total air cargo industry revenue

70

80% AsiaN America Cargo Carried on Maindeck

Daily Flights

Pax

flights

Converting

lower hold

capacity to

equivalent

freighter flights

logistic/

destination

range

LF

regulations

Source: Innovata, DOT T-100, 2013, Boeing Analysis

60-7050-60

10

150

Equivalent

freighter

flights

Total

freighter

flights

Freighter

flights

71

Freighter service advantages over passenger belly

Cargo focus and control

Timing and routing

Capacity (volume, weight, hazmat & dimensional)

Handling location and ramp proximity

Reliability and predictability

Freighters will remain the leading cargo capacity provider

72

Key Takeaways

A good strategy is critical for success

Customers (passengers) need to be at the center of

your plan

Relentless focus on many external factors

The regulatory environment is a key external factor

No one airline business model is “right”

No specific partnering level is “right”

Good strategy is also key for air cargo success

73

MonteCristoAir Case Study Connection

What is MonteCristoAir’s current strategy?

Given the key factors MonteCristoAir is facing, does their

strategy need updating?

What are the key regulatory issues facing them?

What is their current business model?

How should they adapt their business model to fit their

environment?

What partnering level is right for MonteCristoAir?

Should air cargo be part of their operations?