Italian banking-foundations-2014-02-05-1

36

Italian Banking Foundations IMPORTANT DISCLOSURE FOR U.S. INVESTORS: This document is prepared by Mediobanca Securities, the equity research department of Mediobanca S.p.A. (parent company of Mediobanca Securities USA LLC (“MBUSA”)) and it is distributed in the United States by MBUSA which accepts responsibility for its content. The research analyst(s) named on this report are not registered / qualified as research analysts with Finra. Any US person receiving this document and wishing to effect transactions in any securities discussed herein should do so with MBUSA, not Mediobanca S.p.A.. Please refer to the last pages of this document for important disclaimers. 05 February 2014 Italian Reforms Stakes for CoCos: killing 3 birds with 1 stone Andrea Filtri Equity Analyst 2010-12 confirming the un-sustainability of the current model In Re-Foundation, 28 May 2012, we concluded that the crisis broke the symbiotic relationship between Foundations and banks, making it financially unsustainable. The latter required capital injections and reduced dividends, forcing the former to cut grants and distribute reserves. Updating our study for 2011-12 we reconfirm our diagnosis as events evolved more negatively than we had predicted. Asset value and grants are down 16% and 30% vs 2010, respectively, and cash flow has been negative for 4 consecutive years. Taking banks‟ consensus DPS and keeping other income sources stable, we calculate grants should fall by 39% to preserve capital levels. 1998 Parliament’s debate identified the risks but the law left some issues unresolved Digging in Parliament‟s archives, we retrace the debate which led to the Ciampi law which provided the Foundations‟ legal framework. The crux of the fight was on the powers of the regulatory authority (yet to be implemented), on forcing portfolio diversification, the disposal of bank stakes and outsourcing investment management. This confirms to us: a) MPs had already identified the crucial factors/risks of the new framework and; b) that the matters discussed are still very relevant today, suggesting the current law did not address all issues. IMF, ECB and Italian Treasury all pointing to a reform of Banking Foundations MPS, Carige, Banca Marche, CariFerrara, Tercas, BP Spoleto, Veneto Banca, Banca Cividale. These are only some of the many banks under special supervision as the surge in bad debts is jeopardising capital adequacy. They jointly hold over €300bn of assets or c.7% of industry‟s total stock; a potential systemic issue. Their peculiar governance is representing an obstacle for their recapitalisation. The issue is known abroad: Mario Draghi (ECB chairman), the IMF, Bank of Italy and the Finance Minister called for a reform of Foundations. The latter is reported to support a reform of the Foundations‟ law mandating portfolio diversification, prohibiting leverage and control of a bank and investing in hedge funds and derivatives. Converting equity stakes into CoCos: the transition towards full diversification Foundations‟ investments need to generate stable and growing cash flows to fund grants. In Re- Foundation we showed that bank stakes provided sub-optimal risk-adjusted returns vs a variety of alternatives, suggesting change is due. We acknowledge the difficulty for Foundations to abandon banks while these are still troubled and have depressed valuations. At the same time, Foundations are under pressure to return to giving more grants. We propose a transitory solution towards portfolio diversification: converting the Foundations‟ stakes into bank CoCos would: a) increase the visibility of investment yield while; b) upgrading the governance of the Foundation- bank model; c) leaving banks‟ capital adequacy unchanged. This is feasible as in Dec-13, Parliament allowed tax deductibility of CoCo coupons for banks. Win-Win-Win: EPS +14-30%, RoTE up 2-5 p.p., from buybacks below TE We see the CoCo for equity swap as a positive evolution for all stakeholders. While it is neutral to bailout risk, Foundations gain higher and visible yield (c.8.3%), banks gain on governance and profitability and minority shareholders gain EPS and DPS accretion. We simulate the operation on ISP and UCG, where Foundations own, on aggregate, 28% and 11% of ordinary shares. We calculate this would lead to: a) 14% EPS and 5 p.p. RoTE boost at ISP and 30% EPS and 2 p.p. RoTE hike at UCG, b) 1 p.p. higher div. yield, c) 3% investment yield premium for Foundations. The positive outcomes for all stakeholders derive from the below-BV valuation of shares allowing the accretive impact of the share buyback to more than compensate the earnings dilution from higher interest costs of CoCos. Higher valuations could provide less appealing financials, implying there is a window of opportunity to carry the swap out today, in our view. Had Foundations held CoCos since 2001, they would have made €22bn extra profits after costs and grants; 50% and 140% boost to the current total capital and 2001-12 cumulative grants. The deal would gear up bank balance sheets by 0.6-2 p.p. to 3.3-4.5% TE/TA, in line with EU retail peers and with no implications from bail-in regulation, hence at no compromise to the risk profile. +44 203 0369 571 [email protected] Antonio Guglielmi Equity Analyst +44 203 0369 570 [email protected] Andrea Carzana Equity Analyst +44 203 0369 576 [email protected] CoCo for equity swap simulation ISP UCG Foundations holding 28% 11% Buyback/CoCo, Eur m 13,820 6,885 Coupon, % 8.33% 8.33% Impact to 2015e adj. profits -18% -10% Shares cancellation (m) 3,297 3,490 2015e EPS change, % 14% 30% RoTE points change 5% 2% 2015e DPS change (unchanged payout) 23% 19% Yield change, % 1.2% 0.7%

-

Upload

lavoceinfo -

Category

News & Politics

-

view

79.420 -

download

0

Transcript of Italian banking-foundations-2014-02-05-1

Italian Banking Foundations

IMPORTANT DISCLOSURE FOR U.S. INVESTORS: This document is prepared by Mediobanca Securities, the equity research department of Mediobanca S.p.A. (parent company of Mediobanca Securities USA LLC (“MBUSA”)) and it is distributed in the United States by MBUSA which accepts responsibility for its content. The research analyst(s) named on this report are not registered / qualified as research analysts with Finra. Any US person receiving this document and wishing to effect transactions in any securities discussed herein should do so with MBUSA, not Mediobanca S.p.A.. Please refer to the last pages of this document for important disclaimers.

05 February 2014

Italian Reforms

Stakes for CoCos: killing 3 birds with 1 stone Andrea Filtri

Equity Analyst

2010-12 confirming the un-sustainability of the current model

In Re-Foundation, 28 May 2012, we concluded that the crisis broke the symbiotic relationship

between Foundations and banks, making it financially unsustainable. The latter required capital

injections and reduced dividends, forcing the former to cut grants and distribute reserves.

Updating our study for 2011-12 we reconfirm our diagnosis as events evolved more negatively

than we had predicted. Asset value and grants are down 16% and 30% vs 2010, respectively, and

cash flow has been negative for 4 consecutive years. Taking banks‟ consensus DPS and keeping

other income sources stable, we calculate grants should fall by 39% to preserve capital levels.

1998 Parliament’s debate identified the risks but the law left some issues unresolved

Digging in Parliament‟s archives, we retrace the debate which led to the Ciampi law which

provided the Foundations‟ legal framework. The crux of the fight was on the powers of the

regulatory authority (yet to be implemented), on forcing portfolio diversification, the disposal

of bank stakes and outsourcing investment management. This confirms to us: a) MPs had already

identified the crucial factors/risks of the new framework and; b) that the matters discussed are

still very relevant today, suggesting the current law did not address all issues.

IMF, ECB and Italian Treasury all pointing to a reform of Banking Foundations

MPS, Carige, Banca Marche, CariFerrara, Tercas, BP Spoleto, Veneto Banca, Banca Cividale.

These are only some of the many banks under special supervision as the surge in bad debts is

jeopardising capital adequacy. They jointly hold over €300bn of assets or c.7% of industry‟s total

stock; a potential systemic issue. Their peculiar governance is representing an obstacle for their

recapitalisation. The issue is known abroad: Mario Draghi (ECB chairman), the IMF, Bank of Italy

and the Finance Minister called for a reform of Foundations. The latter is reported to support a

reform of the Foundations‟ law mandating portfolio diversification, prohibiting leverage and

control of a bank and investing in hedge funds and derivatives.

Converting equity stakes into CoCos: the transition towards full diversification

Foundations‟ investments need to generate stable and growing cash flows to fund grants. In Re-

Foundation we showed that bank stakes provided sub-optimal risk-adjusted returns vs a variety

of alternatives, suggesting change is due. We acknowledge the difficulty for Foundations to

abandon banks while these are still troubled and have depressed valuations. At the same time,

Foundations are under pressure to return to giving more grants. We propose a transitory solution

towards portfolio diversification: converting the Foundations‟ stakes into bank CoCos would: a)

increase the visibility of investment yield while; b) upgrading the governance of the Foundation-

bank model; c) leaving banks‟ capital adequacy unchanged. This is feasible as in Dec-13,

Parliament allowed tax deductibility of CoCo coupons for banks.

Win-Win-Win: EPS +14-30%, RoTE up 2-5 p.p., from buybacks below TE

We see the CoCo for equity swap as a positive evolution for all stakeholders. While it is neutral

to bailout risk, Foundations gain higher and visible yield (c.8.3%), banks gain on governance and

profitability and minority shareholders gain EPS and DPS accretion. We simulate the operation

on ISP and UCG, where Foundations own, on aggregate, 28% and 11% of ordinary shares. We

calculate this would lead to: a) 14% EPS and 5 p.p. RoTE boost at ISP and 30% EPS and 2 p.p.

RoTE hike at UCG, b) 1 p.p. higher div. yield, c) 3% investment yield premium for Foundations.

The positive outcomes for all stakeholders derive from the below-BV valuation of shares allowing

the accretive impact of the share buyback to more than compensate the earnings dilution from

higher interest costs of CoCos. Higher valuations could provide less appealing financials,

implying there is a window of opportunity to carry the swap out today, in our view. Had

Foundations held CoCos since 2001, they would have made €22bn extra profits after costs and

grants; 50% and 140% boost to the current total capital and 2001-12 cumulative grants. The deal

would gear up bank balance sheets by 0.6-2 p.p. to 3.3-4.5% TE/TA, in line with EU retail peers

and with no implications from bail-in regulation, hence at no compromise to the risk profile.

+44 203 0369 571

Antonio Guglielmi

Equity Analyst

+44 203 0369 570

Andrea Carzana

Equity Analyst

+44 203 0369 576

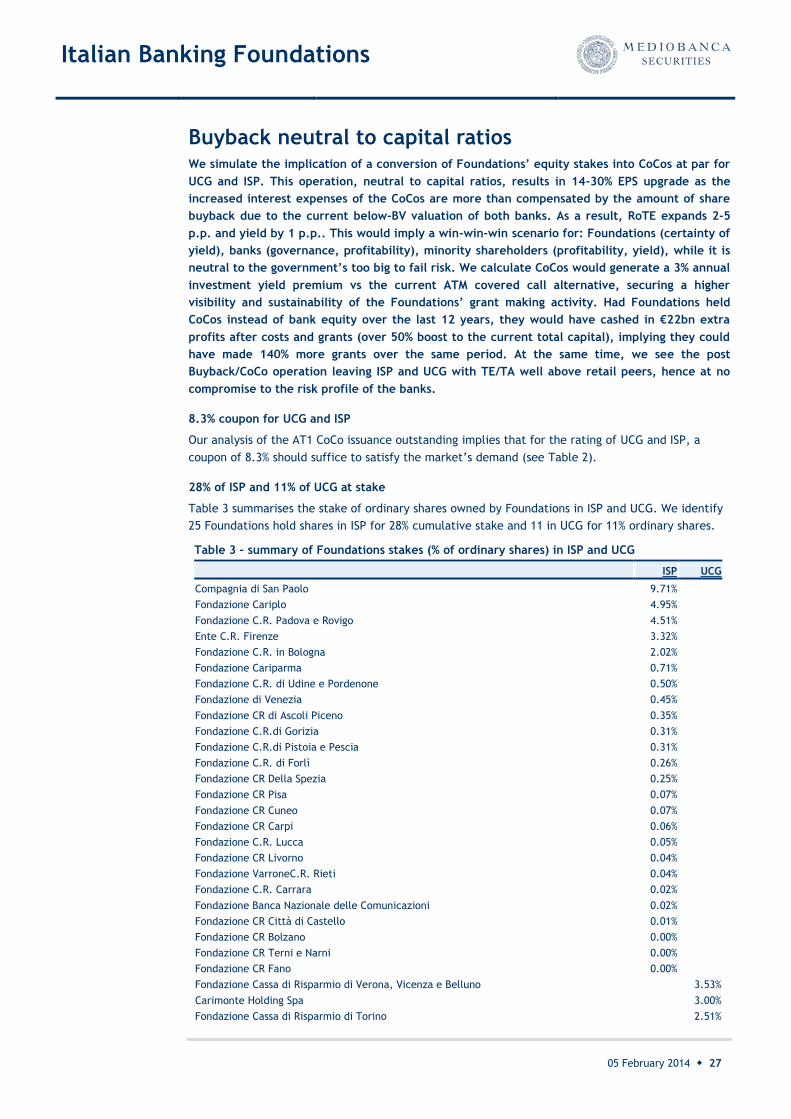

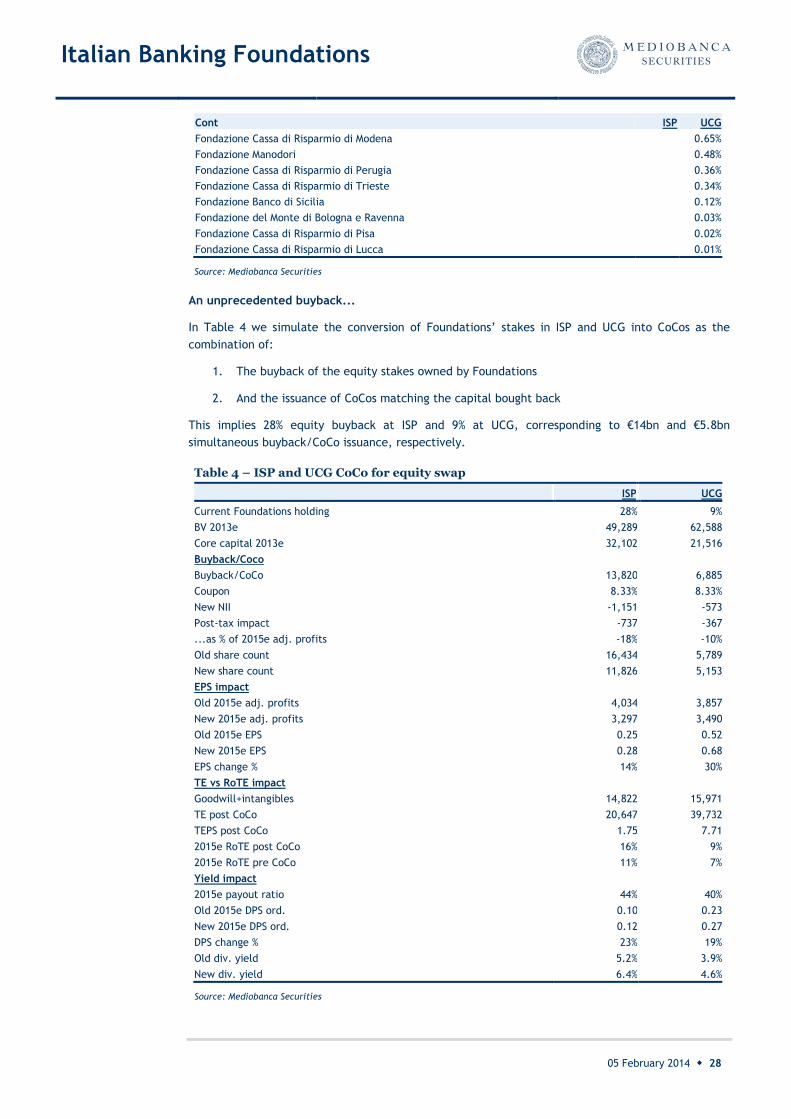

CoCo for equity swap simulation

ISP UCG

Foundations holding 28% 11%

Buyback/CoCo, Eur m 13,820 6,885

Coupon, % 8.33% 8.33%

Impact to 2015e adj. profits -18% -10%

Shares cancellation (m) 3,297 3,490

2015e EPS change, % 14% 30%

RoTE points change 5% 2%

2015e DPS change (unchanged payout)

23% 19%

Yield change, % 1.2% 0.7%

Italian Banking Foundations

IMPORTANT DISCLOSURE FOR U.S. INVESTORS: This document is prepared by Mediobanca Securities, the equity research department of Mediobanca S.p.A. (parent company of Mediobanca Securities USA LLC (“MBUSA”)) and it is distributed in the United States by MBUSA which accepts responsibility for its content. The research analyst(s) named on this report are not registered / qualified as research analysts with Finra. Any US person receiving this document and wishing to effect transactions in any securities discussed herein should do so with MBUSA, not Mediobanca S.p.A.. Please refer to the last pages of this document for important disclaimers.

Contents

Confirming the diagnosis 3

A very actual, old debate 14

Pressure (to reform) is all around 20

CoCo: transit to portfolio diversification 24

Buyback neutral to capital ratios 27

Appendix 32

Italian Banking Foundations

05 February 2014 ◆ 3

Confirming the diagnosis

In Re-Foundation, 28 May 2012, we highlighted how Italian Banking Foundations

needed to change to earn sustainable investment returns to fund their grants. In

essence, we concluded that the Foundations-Banks model - based on stable,

concentrated equity shareholdings in banks, in exchange for high dividends to fund

grants - was no longer sustainable. We suggested Foundations should diversify

investment portfolios by selling the banks’ shares. Our analysis based on data up to

2010. Two years on, little has changed. On aggregate, the main Foundations’ assets

(excl. MPS) have fallen a further 16% (50% due to the bank exposure), with grants

down 30% 2010-12 and implying 30% real contraction vs 2001. From 2009, underlying

cash flows turned negative, denting 4% of Foundations’ assets. 2011-12 reported

figures came below our projections made two years ago. Taking BBG consensus on

banks’s DPS and holding other income constant, we calculate Foundations should cut

grants by 39% to preserve capital. This confirms our thesis of unsustainability of the

current model and the need to diversify investment portfolios to recover higher and

more stable profitability.

Retracing our own footsteps

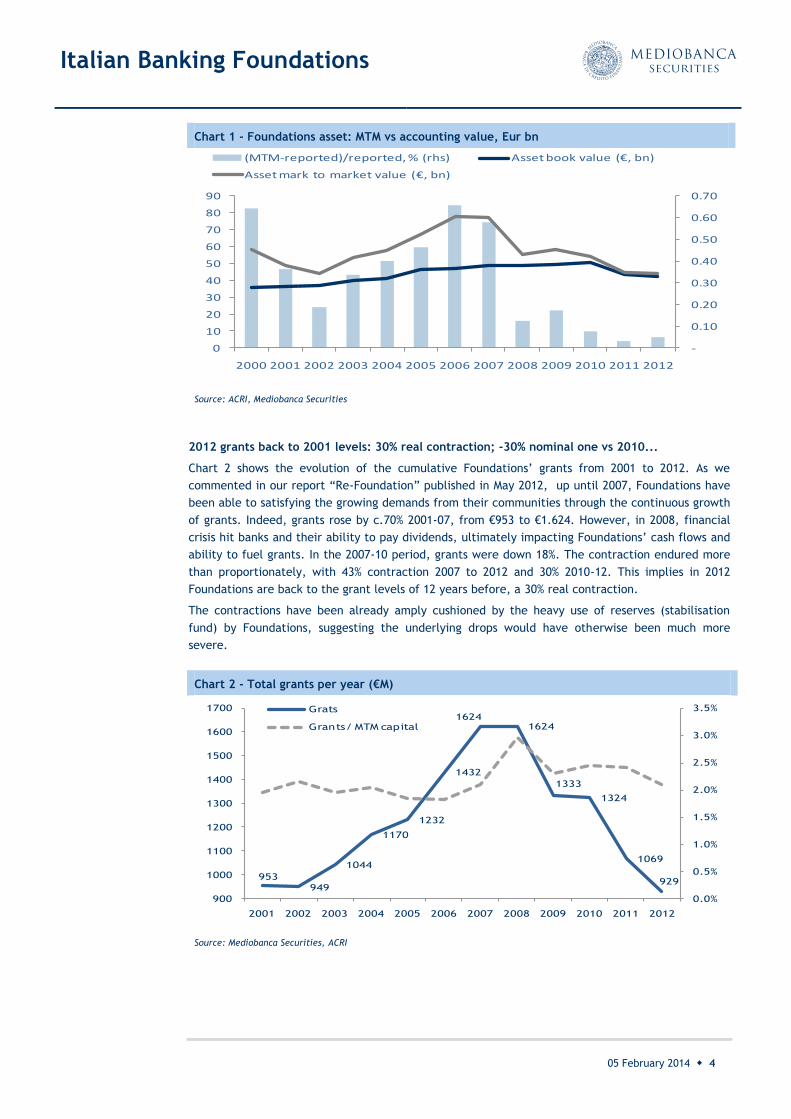

Fair value/mark to market convergence implies fair representation of reality

In our previous report Re-Foundation, published on May 28th 2012, we have broadly explained how

the absence of uniform FV/MTM principle has allowed Italian Banking Foundations (Foundations) to

smoothen results out in the past. We recall that for several years Foundation‟s profits did not

reflect the economic change in the value of the portfolio. Rather, they derived from the adoption

of different accounting principles for the different types of investments and for the various

investment operations. In general, annual profits embed all realised cash flows, regardless of what

investment generated them. So, all dividends/coupons received from any investment will enter the

annual profit and will contribute to the grant pool. As for the recognition of deltas in mark to

market (MTM), these will only translate in the P&L if the Foundation realises this through active

buying/selling. By their nature, strategic stakes, composing the majority of Foundations‟ portfolios

are hardly traded. This implies that for the purpose of their activity, Foundations consider the bank

holding as a perpetuity, mostly focussing on the dividend yield generated rather than looking at the

short term fluctuations in share price. To put it simply, a strong appreciation in share price would

not translate in any extra revenues (unless shares were sold). The same principle will hold for other

investments, with the exception of diversified investments which carry no intangible value as

strategic stakes do, and will therefore be more actively traded. This has two main implications for

Foundations: a) unrealised capital gains/losses have been used to smoothen annual grant pools. b)

de-touching of accounting from reality has led Foundations to over/under spend. As a consequence

of the two implications above, capital resources of Foundations have been overstated for a number

of years. However, the divergence between reported and real value of capital is now really thin as

the two have converged. Chart 1 shows the evolution of the total Foundations‟ capital from 2000 to

2012 compared to the equivalent amount classified according to MTM principles. Over the 2005-

2012 period, Foundations carried latent gains on their investments which progressively realigned to

their accounting values as markets retraced in recent years. The discrepancy between the two

methods reached a peak €31bn spread in 2006, i.e. 65% above the reported €47bn capital. This

positive gap progressively shrunk in the following years to almost 0% in 2011 and 4% in 2012. We can

therefore conclude that taking reported values is now a good starting point, as it closely reflects

the reality Foundations are facing in 2012.

Italian Banking Foundations

05 February 2014 ◆ 4

Chart 1 - Foundations asset: MTM vs accounting value, Eur bn

Source: ACRI, Mediobanca Securities

2012 grants back to 2001 levels: 30% real contraction; -30% nominal one vs 2010...

Chart 2 shows the evolution of the cumulative Foundations‟ grants from 2001 to 2012. As we

commented in our report “Re-Foundation” published in May 2012, up until 2007, Foundations have

been able to satisfying the growing demands from their communities through the continuous growth

of grants. Indeed, grants rose by c.70% 2001-07, from €953 to €1.624. However, in 2008, financial

crisis hit banks and their ability to pay dividends, ultimately impacting Foundations‟ cash flows and

ability to fuel grants. In the 2007-10 period, grants were down 18%. The contraction endured more

than proportionately, with 43% contraction 2007 to 2012 and 30% 2010-12. This implies in 2012

Foundations are back to the grant levels of 12 years before, a 30% real contraction.

The contractions have been already amply cushioned by the heavy use of reserves (stabilisation

fund) by Foundations, suggesting the underlying drops would have otherwise been much more

severe.

Chart 2 - Total grants per year (€M)

Source: Mediobanca Securities, ACRI

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0

10

20

30

40

50

60

70

80

90

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

(MTM-reported)/reported, % (rhs) Asset book value (€, bn)

Asset mark to market value (€, bn)

953

949

1044

1170

1232

1432

16241624

1333

1324

1069

929

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

900

1000

1100

1200

1300

1400

1500

1600

1700

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Grats

Grants/ MTM capital

Italian Banking Foundations

05 February 2014 ◆ 5

…as Foundations keep holding tight on ‘their’ banks...

The free fall of grants, which has reached the lowest level in twelve years, has once again

demonstrated our thesis of unsustainability of the Bank-Foundation model. Despite this, by looking

at how the relationship Bank-Foundation has developed in the past two years, little has changed.

Indeed, we notice that, after twenty years from the first reform, Foundations still have a firm grip

to „their‟ original banks. Chart 3 shows the distribution of the 88 Foundations in 2010 and in 2012:

15% is still over 50% control in 2012, vs. 17% in 2010;

31% is above the 20% stakeholding in 2012, vs. 40% in 2010;

50% is above the 5% stakeholding in 2012, vs. 56% in 2010;

25% has no stake in the saving banks in 2012, vs 20% in 2010.

The small decrease in the banks‟ stakes owned by Foundations is not the consequence of the active

selling of shares, but is mostly due to the dilution suffered in the banks‟ capital increases of 2011

and 2012 (UCG, ISP, PMI, UBI, Banco Popolare, MPS) imposed by the lack of free resources.

Chart 3 - Foundation’s stake into saving bank, 2010 (lhs) and 2012 (rhs)

Source: ACRI

…while on the other side, banks’ dependence on Foundations keeps on falling

Chart 4 shows the evolution of the capital of all Italian banks (light blue) and Foundations (dark

blue) and the incidence of the latter on the former. For Foundation-originated banks, the idea

underlying is that initially the two were one and the same; as time went by and banks emancipated

and grew, the two factors diverged. As we are using the total capital of all Italian banks, this

includes the one of Popolari, cooperative and private banks which did not originate from a

Foundation. Nevertheless, given the relative size of Foundation-originated banks, we believe the

relative evolution of the two factors still has some relevance for our analysis. The chart confirms

this intuition, showing:

High initial ratio – a decade ago, Foundations‟ capital stood at 1/3 of bank‟s capital, a

high ratio in relative and absolute terms suggesting, in our view, the relatively low degree

of emancipation of the banking sector at the time.

Banks lapping Foundations – from 2000 to 2012 banks have increased their capital by 98%

(92% from 2000 to 2010) and Foundations by only 19% (42% from 2000 to 2010). The

difference in Foundations‟ capital growth rate between 2000-10 and 2000-12 suggests that

in the last two years of our analyses Foundations have eroded a relevant part of their

capital, precisely 16% of €50bn 2010 capital.

15

18

21

14

20

Foundation with > 50% stake of the saving bank

Foundation with no stake of the saving bank

Foundation with <5% stake of the saving bank

Foundation with stake of the saving bank between 5% and

20%

Foundation with stake of the saving bank between 20%

and 50%

13

22

22

17

14

Foundation with > 50% stake of the saving bank

Foundation with no stake of the saving bank

Foundation with <5% stake of the saving bank

Foundation with stake of the saving bank between 5% and

20%

Foundation with stake of the saving bank between 20% and

50%

Italian Banking Foundations

05 February 2014 ◆ 6

Foreign acquisitions and crisis-driven rights issues diluting the link – we note significant

upward steps in the growth of banks capital, particularly in 2005 and 2011, and relatively

smoother growth for Foundations. Apart from the scale of the chart, the reason is that in

2005 UCG‟s acquisition of HVB brought the bank‟s capital within the „perimeter‟, while in

2009 and 2011 the banks‟ rights issues attracted new resources. In the latter case, while

banks reinforce capital, Foundations increase their equity and market risks in their

portfolios. Unless bank share prices significantly re-rate, the consequence of such

operations is a strengthening of banks‟ capital and the increase in risk of Foundation‟s

portfolios.

Chart 4 - Bank’s capital vs. Foundation’s capital (€bn)

Source: ACRI, Bank of Italy

Falling revenues and profits erode profitability

Chart 5 plots the evolution of the revenues on the Foundations‟ total assets and of the return on

assets (ROA) versus their respective adjusted versions (lhs) and the difference in the evolution of

revenue and profit margins reported and adjusted. Adjusted factors account for recurring items

only (core revenues: dividends, interest, pure trading profit; and core profits: core revenues minus

core costs and taxes) and for the market value of total assets (as opposed to reported assets). We

note:

Returns and profitability keep falling, 2011 the worst year – over the last twelve years,

Foundations reported average revenues/assets and profits/assets of 5.2% and 4.5%,

respectively. This result shows a deterioration in the last two years. Indeed, in the decade

2001-10 Foundations registered average revenue/assets of 5.6% and profits/assets of 5.1%.

By contrast, in the period 2011-12 the two profitability indicators collapsed to 3.1% and

1.3%, respectively.

Profits falling more than revenues – on the right hand side of the following chart, we

show how the gap between returns and profits has widened for Foundations, multiplying by

5-6 times in the last decade. This indicates that initially, returns from investments would

largely feed down to profits. The increase can theoretically be due to: a) growing costs

denting profitability, b) increasing provisions, c) increasing taxes. We exclude the latter

option as Foundations operate in a quasi-tax free regime. Years of banks‟ extra dividends

and years of particularly tough returns could require special provisions to be put on the

side and released to smoothen bottom line. Finally, higher cost absorption would impair

profitability explaining the delta.

0%

5%

10%

15%

20%

25%

30%

35%

-

50

100

150

200

250

300

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Italian Banks Capital Foundations capital Foundations capital/Bank capital (rhs)

Italian Banking Foundations

05 February 2014 ◆ 7

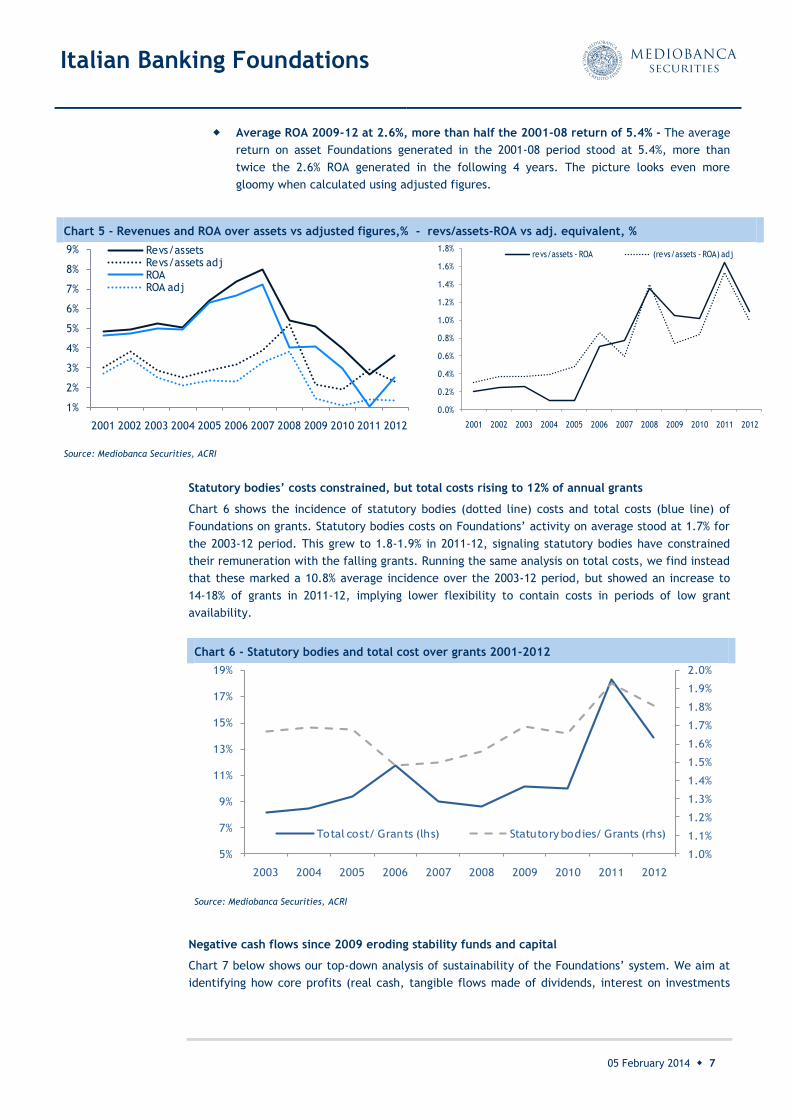

Average ROA 2009-12 at 2.6%, more than half the 2001-08 return of 5.4% - The average

return on asset Foundations generated in the 2001-08 period stood at 5.4%, more than

twice the 2.6% ROA generated in the following 4 years. The picture looks even more

gloomy when calculated using adjusted figures.

Chart 5 - Revenues and ROA over assets vs adjusted figures,% - revs/assets-ROA vs adj. equivalent, %

Source: Mediobanca Securities, ACRI

Statutory bodies’ costs constrained, but total costs rising to 12% of annual grants

Chart 6 shows the incidence of statutory bodies (dotted line) costs and total costs (blue line) of

Foundations on grants. Statutory bodies costs on Foundations‟ activity on average stood at 1.7% for

the 2003-12 period. This grew to 1.8-1.9% in 2011-12, signaling statutory bodies have constrained

their remuneration with the falling grants. Running the same analysis on total costs, we find instead

that these marked a 10.8% average incidence over the 2003-12 period, but showed an increase to

14-18% of grants in 2011-12, implying lower flexibility to contain costs in periods of low grant

availability.

Chart 6 - Statutory bodies and total cost over grants 2001-2012

Source: Mediobanca Securities, ACRI

Negative cash flows since 2009 eroding stability funds and capital

Chart 7 below shows our top-down analysis of sustainability of the Foundations‟ system. We aim at

identifying how core profits (real cash, tangible flows made of dividends, interest on investments

1%

2%

3%

4%

5%

6%

7%

8%

9%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Revs/assetsRevs/assets adjROAROA adj

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

revs/assets - ROA (revs/assets - ROA) adj

1.0%

1.1%

1.2%

1.3%

1.4%

1.5%

1.6%

1.7%

1.8%

1.9%

2.0%

5%

7%

9%

11%

13%

15%

17%

19%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Total cost/ Grants (lhs) Statutory bodies/ Grants (rhs)

Italian Banking Foundations

05 February 2014 ◆ 8

and trading profits, hence excluding cosmetic operations of sell and buyback ad other profit

management operations) compare to reported profits and to grants approved (cash outflows).

Looking at Chart 7 and comparing it with Re-foundation, in which we covered the time period 2001-

2010, we note:

€7.3bn over representation of cash flow in 2001-12, only +€0.3bn vs 2001-10 Over the

last 12 years, only in 2008 and 2011 reported profits undershot core profit. In every other

year, reported profits overshot resources available to spend. On the rhs chart below we

show in dark blue the annual spread between the two factors. We estimate €7.3bn from

2001 to 2012, up only €0.3bn in 2011-12.

Falling approved grants and increasing volatility – Grants approved have decreased in the

two-year period 2010-12 lowering the 2001-12 average at €1.22bn vs. €1.27 in 2001-10. In

addition, the volatility of grants approved has increased by 1% in the last two years

increasing the 2001-12 standard deviation/mean ratio to 20% vs. 19% in the period 2001-10.

Negative net cash flow since 2009 – In the right hand side chart we show in light blue the

spread between core profits and grants approved. Since 2009, when banks started to cut

dividends, the net cash flow has gone negative and it has remained so in the following

years. We calculate €0.7bn cumulative positive cash flow in 2001-12, half of what we have

calculated during the period 2001-10 (€1.5bn), and corresponding to 2% of the initial €36bn

total endowment of 2001. The picture is worse if we make the same analysis over the

period 2010-12. Since the cash flow has gone negative for the first time, Foundations

generated a cumulative negative cash flow of €2.1bn which translates in a 4% erosion of

the €49.4bn total endowment of 2009. Finally, 2011 and 2012 generated average annual

negative cash flows of €400m, comparing to +€361m in 2001-08 and €154m in 2001-10.

Chart 7 – Core profits vs reported profits and grants approved

Source: Mediobanca Securities, ACRI

Insufficient diversification dented the real value of endowments by 43 p.p in 12 years...

The lhs side of Chart 8 shows the comparison of cumulative performance of Foundations‟

comprehensive value of capital vs the major asset classes, rebased to 2000. Over the twelve years,

the MTM value of Foundations‟ assets was down c.25% v.s 7% underperformance in the decade 2000-

10 (2000-04 and 2011-12 estimated by MB, 2005-10 using the value provided by ACRI). By contrast,

Italian inflation was up 37 p.p., government bonds and R.E. 140 p.p., commodities 290 p.p.. We

believe the evolution of Foundations‟ asset values suggests a split in three segments:

1. 2000-05: equity and govies – Foundations performance is the average of the performance

of equity and government bonds, suggesting a balanced exposure to the two asset classes,

in our view.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Core profit/ MTM capital (rhs) Core profits

Reported profit (€ m) Grants approved (€ m)

Eur m

364 575

77

-109

164

161

822

835

-578

-767

-296

-504

221

110

702

849

1,2

53

1,4

15

917

-532

1,1

96

878

-200

482

-1,000

-500

-

500

1,000

1,500

2,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Core profits-grants approved Reported - core profits

Italian Banking Foundations

05 February 2014 ◆ 9

2. 2006-10: banks underperformance realign Foundations to equity – with the advent of

the financial crisis, the high exposure to the banking industry prevailed, with Foundations

asset value converging to the equities performance and underperforming it as banks lagged

behind other sectors.

3. 2010-12: low diversification led to underperformance vs. global equities – with the

improvement of global financial stability following the central banks‟ interventions, global

equities experienced a relief rally, which however, has only partially benefitted banks. As

shown in the rhs of Chart 8, Italian saving banks have underperformed the MS Global Equity

Index by c.50%. Given their high equity concentration of Italian banks in their portfolios,

Foundations partly missed the global equity rally.

From the above, we conclude that Foundations have not been able to keep to the mandate of the

law:

a. Real value destruction - overall Foundations have dented the real value of their assets,

underperforming the inflation rate by almost 43 p.p.. Only in 2006 and 2007, at the peak of

the financial bubble benefitting bank prices, Foundations showed a positive cumulative

performance vs Italian inflation. This betrays the law‟s goal of real value preservation.

b. Lack of diversification – the high correlation of Foundations‟ returns with equities and the

underperformance vs this riskier asset class during the financial crisis confirms Foundations

maintained a high overall portfolio concentration in the banks. This is the main factor

entailing the poor cumulative performance of Foundations and the high volatility of

returns, in our view.

Chart 8 - Returns comparison: Foundations vs asset classes– MS World Equity Index vs. ITA banks (2000=100)

Source: Mediobanca Securities, ACRI

* equity: MS World index

...coupled with highly volatile investment returns

Chart 9 shows the year on year evolution of the MB performance indicator aggregated for the five

largest Foundations (Cariplo, CSP, CRT, CRV, CRP) from 2002-12. From 2002 to 2007 Foundations

experienced growth in their MB performance indicator (see Appendix):

2008 has been the year of rupture with an average 30% real value destruction. 2009 and the

temporary euphoria of the national bailout of banks partially recovered the previous year‟s tragedy,

but 2010 and 2011 reiterated the 2008 issue. 2012 has returned a better MB performance indicator,

practically flat (-0.4%). This shows how volatile Foundations‟ investment performance has been over

a decade.

Foundations

Equity

Govies

R.E.

Cmmdty

IT infl

50

75

100

125

150

175

200

225

250

275

300

325

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

-

20

40

60

80

100

120

140

160

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Equity ITA banks

Italian Banking Foundations

05 February 2014 ◆ 10

Chart 9 – Evolution of the MB performance indicator*, 2002-12, % aggregate level

Source: Mediobanca Securities, company data

* see appendix

Bank stakes main culprit for Foundations’ loss in investments’ worth

In this analysis we estimate the split of the annual evolution of market value of investments of

Foundations between the bank stake, the net cash flow generated (revenues – costs – grants - taxes)

and the other investments. We adopt the following methodology:

1. We start from the first available market value of investments provided by the five largest

Foundations;

2. We then calculate the delta market value generated in each year as the sum of the delta

market values generated by the bank stakes and by other investments, plus the earnings

retention (net cash flow=NCF);

3. We then attribute performance to the different factors as follows:

We either take the reported change in value of the bank stake or we estimate the

average yearly holding of shares in the bank by dividing the Foundation‟s reported

market value of the bank stake by the average bank‟s share price;

We then apply the performance of the bank‟s share price in year t to the average

number of shares held and compare it to the same value in year t-1 to obtain the

performance contribution from the exposure to the bank;

We estimate the performance generated or lost by other investments by subtracting to

the overall delta in market value the performance generated by the saving bank and

the NCF.

We summarise the aggregate results as follows:

16% value destruction in 2011-12, half due to the banks stakes – we calculate the

aggregate MTM value fell by €3.7bn over 2011-12, for 18% fall on 2010 (-16% on reported

figures). A half of this is attributable to the banks‟ stakes, c.10% to negative cash flow and

40% to the evolution of other investments;

Bank stakes lost €8bn value since 2001, €1.9bn in the last two years...: the evolution of

the value of the cumulative bank stakes is in the light blue bars in Chart 10. We calculate

that cumulatively, the bank exposure meant €8bn loss in value for Foundations, i.e. 35% of

the €23bn market value of all investments in 2001YE. 2008 was the year of collapse, with

€9.6bn cumulative losses, aggravated by the increase in the concentration of portfolios

towards these assets through the capital increases launched by banks in the period.

other investments and NCF only compensated 23% of the bank value destruction: The

dark blue bars show the evolution in performance of non-bank investments. We calculate a

-30%

-20%

-10%

0%

10%

20%

30%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Italian Banking Foundations

05 February 2014 ◆ 11

cumulative gain of €0.6bn over the period 2001-12 vs €2bn over the 2001-10 period. This

sharp collapse has happened in 2011 where total other investments generated a loss of

€1.3bn. Given this negative performance in 2011, non-bank investments have offset only

8% of the losses taken through the bank exposure, vs. 25% offset during the period 2001-10.

Accounting also for the retained NCF, total offset of bank exposure amount to 23%, well

below the 55% level reached during the period 2001-10. We note a weak correlation

between the bank stake and other investments, implying other investments not only did

not offset the bank stake fluctuations, but partially magnified their impact to the

fluctuation of overall investments‟ worth.

2001-06 banks up €3.4bn, other investments up €5.8bn: we calculate that in the pre-

crisis period, banks generated cumulative performance for €3.4bn, i.e. 16% of the 2001

cumulative initial market value for Foundations; similarly, other investments grew by

€5.8bn.

2007-12 banks down €11bn, other investments down €5bn: the period 2007-12 saw

value destruction for €11bn on the banks stakes and €5bn for other investments, with a

total loss of €16bn, i.e. 47% of the peak aggregate market value of investments reached at

the end of 2006. The relative magnitude of losses reflects the risk concentration of

Foundations on banks during the crisis – increased through rights issues - and the sector

specific issues banks suffered from, in our view.

Chart 10 – Foundations’ aggregate market value evolution: banks vs other investments

Source: Mediobanca Securities, company data

23,2

84

17,1

42

1,000

6,000

11,000

16,000

21,000

26,000

31,000

36,000

41,000

Mkt

val

ue

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Ban

k

NC

F

Oth

er

Mkt

val

ue

01 02 03 04 05 06 07 08 09 10 11 12

€ m

Market value

Saving Bank

Other Investments

Italian Banking Foundations

05 February 2014 ◆ 12

Radical change is still needed

Replaying the simulation...

We learnt above that the Foundations‟ investment did not preserve their value in real terms over

the last decade, with a further deterioration in 2011-12. This confirms our conclusions on

Foundations‟ investments of Re-foundation. There, we estimated the alternative evolution of

Foundations‟ investments worth under three hypothetical scenarios of evolution of banks‟ dividend

streams. We showed the difficulty for Foundations to protect their assets with the status quo of

investments.

After two years, we re-run the same analysis to verify how reality has unfolded vs our three

hypothetical scenarios depicted two years ago.

We calculate the market value evolution under each DPS scenario by assuming:

a. flat evolution of non-DPS revenues vs 2010 values;

b. constant grants (those paid in 2010, therefore discounting a progressive fall in real grants,

after inflation) and compensating for the zero growth assumption on non-bank dividends;

c. 3% increase in annual operational costs.

On bank dividends, we contemplate the following three scenarios:

Flat dividend: this scenario assumed banks would keep on paying annual dividends in line

with those of 2010.

Consensus dividend: the dividend projection was based on the consensus estimates for the

2012-15 DPS. Later years assumed a 5% annual growth for the following two years and 3%

annual growth thereafter. This scenario resembled the slow recovery trajectory, in our

view.

Bull market: the „bull market‟ option was admittedly optimistic. We supposed banks would

revert to the golden years, when they paid high dividends to shareholders. This scenario

contemplated 2012 revenues at Foundations equal to peak revenues generated by

Foundations from 2005 to 2008. For later years, we projected 5% annual growth until 2015

and by 3% thereafter. This scenario implicitly assumed not only that banks would overcome

macro obstacles to profitability, but also that they would offset the additional regulatory

burdens that were progressively being introduced.

Our exercise admittedly excluded boosts to the market value of Foundations‟ assets from price

appreciation, and limited this to the „retained‟ portion of cashflows generated by the bank. Our

goal was in fact not to predict the actual evolution of the Foundations‟ worth, but rather to see if,

and under which circumstances, maintaining the asset allocation stale could support their statutory

goals.

...2011-12 proved harsher than our most cautious scenario

Chart 11 shows the projection in the evolution of the market value of Foundations we had shown in

the “Re-foundation” report with the addition of:

1) 2011 and 2012 MTM value of Foundations capital;

2) The potential 2013-16 scenario using DPS Bloomberg consensus as a rollover of the previous

„consensus‟ scenario.

We highlight the following:

Italian Banking Foundations

05 February 2014 ◆ 13

2011 and 2012 went below our worst case scenario – the evolution of the aggregate MTM

of Foundations‟ capital was below the 2010 level and it undershot the trajectory of the

most cautious „flat dividend‟ scenario we depicted two years ago.

2013-16 trajectory to confirm the hard times – we re-run the consensus exercise of two

years ago, updating it for the current market estimates on banks‟ DPS into 2016. The

trajectory depicted is below the previous „dividend flat‟ scenario and would confirm a

meagre cash inflow for Foundations going forwards.

Small dividends imply unsustainability of Foundations – the flat dividend scenario,

representing a Japanese-style evolution for the European economy, projects a relentless

fall in Foundations‟ worth into 2030 with a 2-3% annual loss in the absolute value of

Foundations‟ investments. This marks the unsustainability of the current asset allocation of

Foundations as the implications for Foundations‟ stakeholders would be either the full loss

in the support they have been used to receive, or a marked fall in the annual grants to the

local community, before the erosion of inflation.

39% decrease of grants in 2012-16 needed to preserve current capital level – We have

calculated the dividend Foundations will receive from banks in the period 2013-16 by

taking DPS Bloomberg consensus for the next four years. We maintained all the other

source of income (trading income, interests, etc..) stable at the 2012 level and applied a

3% increase in annual operational costs. This scenario would imply Foundations would need

to cut grants by 39% over 2013-16 to maintain their capital stable at the 2012 level.

This analysis suggests that the current portfolios of Foundations are not granting the recovery in

value of the assets, potentially putting at risk the financial sustainability or the one of future

grants. This suggests a change on the investment portfolios is required to preserve the Foundations‟

role as primary actors in the country‟s private, national welfare and charitable sector, in our view.

Chart 11 – Market value evolution from 3 bank DPS scenarios, 2001-30e

p

Source: Mediobanca Securities, Bloomberg ACRI

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Mkt Val avg 01-12 flat dividend

consensus dividend bull dividend

2013-16 consensus

consensus

Italian Banking Foundations

05 February 2014 ◆ 14

A very actual, old debate Digging into the Parliament’s archive we found that in 1998 - at the time of the discussion of

the Ciampi law on Foundations, which gave a definitive legal framework and a role to

Foundations - MPs debated harshly before approving the law. The private nature of Foundations

and their disposal of bank stakes was taken for granted. Much of the debate was about the

powers of control and guidance of the regulatory authority and on whether there should be

external monitoring and enforcement of portfolio diversification. Hot topics were: a) the forced

or incentivised divestment of bank stakes and the deployment of the proceeds, b) the degree of

independence in managing investments and the potential restrictions in certain investments

types, c) the powers of a potential regulating authority. The Lower House bill was tougher on

these matters, while the final agreement reflected a watered down compromise which included

the institution of a regulatory body which is yet to be formed, leaving the Finance Ministry as

the temporary, but still empowered authority of reference. We propose a summary of the two

year long debate to confirm that the issues we treated in this and in previous notes are deep

rooted, had already been identified in the debate 15 years ago and remain very actual. This

suggests the law did not resolve all the issues identified, in our view.

Ten years of legislative innovation behind today’s structure

The transformation of the Italian banking sector happened through a series of progressive

transformations of the legal framework regulating banks (see the table below).

1990 - Amato law: from public entities to joint stock companies - The privatisation of banking

Foundations was initiated in 1990 by Giuliano Amato. The Amato reforms produced a separation of

credit business from philanthropic activities. All banking business was spun off and passed to the

Savings Banks, already established as profit-making companies involved in private commerce and

regulated by the Civil Code and banking standards as applied to ordinary banks. The activities

concerned with social, cultural, civil and economic development remained with the newly-created

Foundations. The law conceived Foundations to be trustees for the capital raised from

privatisations and required them to maintain majority ownership of the banks.

1994 – Dini directive: incentives to reduce control on banks – introduced law 474/94. This

removed the requirement for Foundations to retain control of the banks and provided fiscal

incentives to Foundations which would diversify their portfolios by selling down their stakes.

1998-99 – Ciampi law: removing the umbilical cord - Law no. 461/98 (a.k.a. the "Ciampi" law),

together with decree, no. 153/99, required Foundations to relinquish any remaining control in their

respective banks - an obligation still in force today except for Foundations which have net assets

with a book value under €200m in 2002 or are located in special statute regions. The reform fully

defined the juridical framework of Foundations, providing their specifications under civil and fiscal

aspects. The decree also forbid Foundations from appointing their board members in the banks‟

boards and required them to have separate organs for their strategic, administrative and control

functions.

2001 vs 2003 – A definitive identity for Foundations – In 2001, Giulio Tremonti, minister of

Finance, sponsored law 448/01, which limited the private nature and the statutory autonomy of

Foundations. These reacted by appealing to the Constitutional Court which in September 2003

reaffirmed Foundations as "private, legal entities having statutory and management autonomy" and

as being "among the members of an organisation of a free society".

Italian Banking Foundations

05 February 2014 ◆ 15

Year Operation Banks % sold Seller Buyer Name @ date Today Foundations involved Management/ Shareholders 1990 Amato Law 1993 Privatization Credito Italiano 55% IRI market CI Unicredit 1994 Dini Directive 1994 Privatization COMIT 51% IRI market COMIT ISP 1996 Privatization IMI 7% Treasury block trade IMI ISP 1997 Privatization San Paolo 1 23% CSP market IBST ISP CSP 1998 Ciampi Law 1998 Privatization BNL 62% Treasury market BNL BNP 1998 M&A Ambroveneto & Cariplo Banca Intesa (BIN) ISP Cariplo, CRPa 1998 M&A San Paolo & IMI Sanpaolo IMI (SPI) ISP CSP 1998 M&A Unicredito & Credito Italiano Unicredito Italiano (UCI) UCG CRT, CRV, CM 1998 M&A UCI & CRTS CRTS UCI UCG CRT, CRV, CM, CRTS 1999 Privatization MPS 27% Fondazione MPS market MPS MPS 1999 Privatization Mediocredito Centrale 100% Treasury Banca di Roma Banco di Roma Unicredit BDR 1999 M&A BIN & COMIT BIN ISP Cariplo 1999 M&A UCI & CariTro CariTro Foundations UCI UCG CRT, CRV, CM, CRTS, CRTRO 1999 M&A MPS & BAM BAM MPS MPS

1999 M&A CR Roma Mediocredito Centrale & Savings

Banca di Roma (BdR) UCG CRR, BDS Libyan authorities buy a stake

2000 M&A SPI & Banco di Napoli Banco di Napoli SPI ISP CSP 2001 Tremonti law 2001 M&A SPI & Cardine Cardine Foundations SPI ISP CSP, CRPR, CRB, CRVe, CRUP, CRGo 2001 M&A UCI & Rolo Banca 1473 Cassamarca UCI UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte 2001 M&A BdR BIPOP-Carire Capitalia (CAP) UCG CRR, BDS,CRRE 2003 Constitutional Court ruling 300 and 301 2005 M&A UCI & HVB UniCredit (UCG) UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte 2006 M&A SPI & BIN Intesa Sanpaolo (ISP) ISP CSP, CRPR, CRB, CRVe, CRUP, CRGo, CARIPLO 2007 M&A ISP & Carifirenze ISP ISP CSP, CRPR, CRB, CRVe, CRUP, CRGo, CARIPLO, CRF 2007 M&A UCG & CAP UCG UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte, CRR, BDS, CRRE 2007 M&A MPS & Biverbanca CRBIVC MPS MPS MPS, CRBIVC 2008 RI: €3bn 'cashes' UCG UCG UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte, CRR, BDS, CRRE 2008 Shareholders UCG UCG UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte, CRR, BDS, CRRE Libya and Abu Dhabi buy stakes 2008 M&A MPS & Antonveneta Santander MPS MPS MPS, CRBIVC 2009 Zero cash DPS UCG UCG UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte, CRR, BDS, CRRE 2009 Zero cash DPS ISP UCG UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte, CRR, BDS, CRRE 2009 €0.01 DPS MPS MPS MPS MPS, CRBIVC 2009 RI: €4bn UCG UCG UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte, CRR, BDS, CRRE 2009 RI: €1.9bn T-bond MPS MPS MPS MPS, CRBIVC 2010 New mgt UCG UCG UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte, CRR, BDS, CRRE Piccini: Italy country head

2010 New mgt ISP UCG UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte, CRR, BDS, CRRE GM: Morelli for Micheli /

Chairman mgt board: Beltratti for Salza 2010 New mgt UCG UCG UCG CRT, CRV, CM, CRTS, CRTRO, CRMonte, CRR, BDS, CRRE CEO: Ghizzoni for Profumo 2011 RI: €5bn ISP ISP ISP CSP, CRPR, CRB, CRVe, CRUP, CRGo, CARIPLO, CRF 2011 RI: €2.1bn MPS MPS MPS MPS, CRBIVC * CSP= Compagnia di Sanpaolo, BDR= Banco di Roma, CRB= Cassa di Risparmio di Bologna, CRV= Cassa di Risparmio di Verona, CRVe= Cassa di Risparmio di Venezia, CRUP= Cassa di Risparmio di Udine e Perdenone, CRGo= Cassa di Risparmio di Gorizia, CRPa= CaRiParma, CRF=Ente Carifirenze, CM=Cassamarca, CRTS= Cassa di Risparmio di Trieste, CRTRO= Cassa di Risparmio di Trento e Rovereto, CRMonte=Carimonte, BDS= Banco di Sicilia, CRBIVC= Cassa di Risparmio Biella e Vercelli, IBST=Istituto Bancario Sanpaolo di Torino

Italian Banking Foundations

05 February 2014 ◆ 16

Ciampi law to fill the ambiguity of the Foundations’ role

The third legislative intervention in the process of definition of the Foundations‟ legal framework

became necessary to fill the normative gap of the Amato law. As per MP on.le Cambursano: “it

became evident that we were missing adequate instruments when, identified the no profit goal as

the sole raion d‟etre... the Italian legislative context could not provide adequate support”. The

Ciampi law defined Foundations as: legal entities of private nature, with full statutory and

managerial autonomy, only pursuing goals of social utility, temporarily supervised by the Finance

Ministry. This ended the dispute on the public nature of Foundations which was assigned in the

constituting law of 1990. In presenting to the Banking Association (ABI) in 1996, the then Finance

Minister, Ciampi said the Amato law separated banks from Foundations “but not completely

dethatching two souls which has been cohabitating in a single institute”. He continued saying the

Foundations-banks system required a second reform, the one on the “disposal from Foundations of

bank shares, so to allow to both entities to become permanently autonomous, both free to pursue,

according to their nature, their, very different, goals”. As Senator Debenedetti put it, Ciampi

acknowledged that “the Amato law, solving one problem, shed light on others: firstly the one of

ownership”.

Two years of Parliamentary gestation

On 12 February 1997 the then Finance Minister, Ciampi, presented a decree to reform the law

regulating Foundations. The lower House started the debate in March of the next year, approving a

draft on the 18th with 271 votes in favour, 212 against. On 12 May 1998 the bill then went to the

Senate, which approved it with significant changes on 11 November 1998 with 148 votes in favour,

11 against and 5 abstained. The Lower House then approved the new bill from the Senate a few

days later, converting into law on 23 December.

Government proposal: investment principles, regulatory authority

The governmental decree proposed that Foundations followed the principles of: 1) efficiency in the

management of funds, 2) capital preservation, 3) generation of adequate returns through portfolio

diversification. The decree also confirmed the institution of a regulatory authority with the power

to verify the management of assets, the adequate profitability and the conformity with statutory

goals. Also, the authority would authorise operations of concentration and transformation, could

commission the managing bodies and even dissolve the entities in case of irregularities in the

management.

From a harsh contrast in the Lower House...

The Lower House hosted a tough debate on the bill. There was wide agreement on the private

nature of Foundations and on the progressive disposal of bank shares. The contrast between

majority and opposition was more related to practicalities such as what would happen during and

post the sale process, how long it should take to carry this out, who if any would regulate and

supervise these entities and whether the management of assets should be regulated and controlled,

assigned to third parties or let in the full domain of the management of Foundations.

The majority, composed of the centre-left parties, proposed the institution of a regulatory

authority fixing parameters of adequacy of investment return and the monitoring of the principles

of preservation and prudent management of capital. Also, they proposed the disposal of bank stakes

over four years.

Regarding the regulatory authority, MP on.le Agostini said: “one of the powers of the authority is to

define the parameters linking the capital to the returns of the Foundation to devote defined

resources to the pursuit of statutory goals... as capital preservation is the fundamental scope of a

Foundation”.

Italian Banking Foundations

05 February 2014 ◆ 17

On the disposal process of bank stakes, MP on.le Agostini, sponsor of the proposal for the majority

group proposes that Foundations dispose of bank stakes within four years and that, at regime, they

dedicate their entire activity to the pursuit of the social good.

Very much opposed to this view, the conservative minority argued for a liberal solution, letting

Foundations free to manage their assets independently and without the supervision of any

authority. MP on.le Pace, in stating his opposition to the bill of the majority said: “there is the

attempt to attribute the power to fix the return on investments to the regulatory authority... the

higher the return, the higher normally will have to be the risk borne. The authoritarian

determination... of the investment return implies the acceptance of a degree of risk and this risk

is borne by Foundations, there is no aspect of the law which mentions what would happen in the

case of doing so and obliging Foundations to externalise the management of their investments,

depriving them from the possibility to manage it directly, these investments would go to

(colloquially speaking) „snafuz‟ (from Dictionary.com: „a badly confused or ridiculously muddled

situation‟)”.

On 18 March 1998, the Lower House approved a draft bill consisting essentially of:

Exclusive pursuit of social good – the bill approved indicated Foundations would

exclusively pursue goals of public good.

Indications on investments - the bill approved indicated the principles of efficiency,

capital preservation and portfolio diversification to grant an adequate profitability of the

invested capital and the conferral of asset management to authorised agents to grant

adequate transparency also to stake disposals.

Restriction of instrumental activities – the bill approved indicated Foundations could

control companies instrumental to fulfil statutory goals, exclusively in sectors like

scientific research, education, art, healthcare.

Regulatory authority - the bill approved indicated Foundations would be subject to a

regulatory authority which would verify the adherence to the law, the healthy and prudent

management, the profitability of the investment portfolio and the effective keeping of

statutory goals. This would have the power to remove administrative organs or even

dissolve a Foundation in case of grave irregularities, after having consulted with the

Foundation.

Fiscal treatment of bank stake disposals – the bill approved indicated that the privileged

fiscal regime on the disposal of bank shares would lapse after four years if Foundations still

held control on the bank.

...to a wide agreement on a compromise in the Senate

When the discussion of the matter went to the Senate, the harsh debate has been overcome, with

relevant amendments to the bill approved in the Lower House. In particular, the agreement

included:

The introduction of the local development among the scopes of Foundations;

A definition of return, net of operating costs and taxes, provisions to mandatory reserves;

The establishment of control as per the art. 2359 of the Civil Code of law;

The possibility for Foundations to buy stakes in the Bank of Italy;

The incompatibility for individuals to be part of Foundations‟ and banks‟ boards at once.

In essence the approved deal diluted the powers of the regulatory authority and the indications on

the investment activity.

The agreement is reflected in the final vote: 148 votes in favour, 11 against and only 4 abstained.

Italian Banking Foundations

05 February 2014 ◆ 18

Senator Debenedetti the main oppose to the compromise...

The opposition to the final bill came from Senator Debenedetti, notwithstanding his belonging to

the majority party. He was seeing the reform as a failed opportunity to provide the impulse to

diversify the shareholder base of banks, removing the strong links with Foundations. He had a very

clear idea of what to do: “it is now necessary that Foundations/associations overcome the identity

crisis, rediscovering a precise social or cultural vocation. Foundations/associations, clearly

belonging to the private sphere of law, will be able to construct the pendant of joint stock

companies: the latter pursuing profit maximisation, the former regulated as not for profit

entitites... Loyal to their origins, Foundations/associations will only invest their wealth with the

objective to generate returns to fund their institutional, not for profit and to allow lasting

interventions in the pursuit of their statutory goals. They will predominantly invest in a diversified

portfolio of financial assets. They will be allowed to maintain stakes in banks and companies, but

with no control. As guarantee, the management of financial resources of Foundations/associations

will happen through a professional manager and Foundations‟ management will be responsible for

how they have invested and how they have utilised the returns”. He also proposed a revision of the

concept of control related to the voting behaviour at AGMs as opposed to the number of shares

held, as per the art. 2359 of the Civil Code of law.

On Foundations-banks relationship, he added: “converting the stakes of Foundations/associations in

marketable securities, having separated the control from the ownership, having reoriented their

activity on the prudent portfolio diversification and on the spending of returns which derive from

it, will fall the main reason of the link with political power”.

On the link with politicians, he highlighted the importance of the ownership structure of

Foundations: “There is no doubt that a Foundation is a company: a company which does not

distribute profits but which can pursue, and this is the difference, surpluses. Also, they do not

receive contributions from private individuals, they originate from a separation, certainly not

from private donations provided by a universe of agents, so that the Foundation is an organisation

conceived for the wellbeing of the beneficiary of services which the Foundation offers and so it

does not have to report to its contributors... the fact that administrators are largely appointed by

politicians introduces for Foundations a particular category of agents which establish transactions

with Foundations: politicians... Foundations do not belong to anyone as nobody has the right on

their profits but they are controlled by administrators who are subject to their appointment by

politicians”.

He then linked the implication of the political influence on Foundations for financial markets: “it is

then necessary to pose this question: what is the propensity to risk of Foundations‟ administrators?

Low with respect to financial risk and low with respect to political risk... in conclusion, the

absence of contributors and the power of appointment from politicians are non- trivial on the

utility function of Foundations‟ administrators. If we introduce in financial markets operators who

formulate their demand not through a risk-return equation, we distance the market from a

condition of efficiency”.

He therefore proposed Foundations should sell the bank stakes, diversify their investment portfolios

to reap more stable returns to fund their grants and to remove the link with politicians. A

regulatory authority should monitor that investments are coherent with capital preservation and

diversification and they could remove administrators or even dissolve Foundations in case of

improper behaviour.

...together with a few more

Going through the Senate‟s documents, we also found a few individual proposals alternative to the

agreement between majority and minority.

Senator Sella di Monteluce proposed either the introduction of a fiscal incentive to dispose of bank

stakes or the transfer of voting rights on bank shares to the Finance Ministry if, after four years,

Italian Banking Foundations

05 February 2014 ◆ 19

these would not have sold the shares. Voting rights would be returned once the disposal would be

completed.

Senator Miglio proposed the partial utilisation of proceeds from the sale of banks‟ stakes into the

reduction of the Italian public debt and summarised his worries about the new law as follows:

“What will Foundations do with the colossal wealth they will administer with the disposals of bank

shares? Foundations are about to become a formidable power centre...the only certain fact is that

it will be about discretional decisions, made by party emissaries, not subject to any effective

democratic, direct or indirect control, a power as strong as irresponsible... the most formidable

instrument of influence-peddling and manipulation of consensus which has partitocracy has ever

has is being introduced”.

Lega Nord Padania and Rifondazione Comunista parties opposed the compromise. Senator Co‟

declared: “Foundations will be more and more destined to forget their goals of social welfare to

transform in power centres inside the banking sector”.

Today’s debate has not changed much

It has been an extremely formative experience to retrace the topics and the evolution of the

Parliamentary debate of the Ciampi law which is behind today‟s legal framework. We notice that

much of the Parliament‟s attention went to issues such as portfolio diversification, divestment of

banks shares, portfolio diversification, monitoring of capital preservation and adequacy of

investment returns, political interference, outsourcing of portfolio management, conflict between

investment goals and grant-making focus shows how:

1) The Parliament had already identified the crucial factors/risks 15 years ago;

2) Today‟s debate has not changed dramatically, implying the current framework did not

solve all the criticalities which had been identified.

Italian Banking Foundations

05 February 2014 ◆ 20

Pressure (to reform) is all around The IMF, the Bank of Italy and the Government have affirmed their support to a reform of

Foundations involving: 1) portfolio diversification; 2) leverage cap; 3) stricter governance. This

suggests that Foundations should: a) reduce their stakes in banks and diversify their investment

portfolios; b) reduce the risk of interference into the bank or from politicians. This shows the

level of the debate has raised from national to the international scene, increasing the pressure

on Italy to reform ahead of the implementation of the Common European Regulator.

IMF recommending a reform of Foundations...

The IMF 2013 Article IV Consultation published by the IMF last September included a chapter titled

„Reforming the corporate governance of Italian banks‟. This includes an analysis of the current

system of Foundations and provides recommendations of reform to foster corporate governance.

Lights and shadows of the Foundations’ system

The IMF analysis of the Italian banking system composes of the following points:

Concentrated ownership of Italian banks – Italian banks‟ ownership structure is

concentrated with the largest shareholder controlling on average 45% of the capital or 18%

when weighted by market capitalisation. This can facilitate decision making but in Italy

there are „minority shareholders that exercise control beyond their ownership through

legal devices such as joint lists, coalitions with other shareholders (formalized or not),

voting rights ceilings and cross-holdings. These shareholders are also often linked to non-

profit foundations, whose governance differs from a standard corporation‟.

Foundations propelled Italian banks forward... – Foundations supported two consolidation

waives, giving rise to three large banking groups. They also supported the recapitalisation

of banks in the crisis, providing 20% of the capital needs since 2008.

...but they have also dragged their feet – Foundations have dropped their bank ownership

to 40% in 2012 but they are still major shareholders in four of the top 10 banking groups.

Despite the indication of the law to lose control of banks, Foundations appoint the

majority of board members in the two largest banks.

Governance challenges – „Local politicians dominate the boards of several foundations‟.

„Foundations do not follow basic corporate governance practices. For example, the

appointment of governing bodies is often non-transparent and foundations do not follow

uniform accounting and disclosure rules. In addition, there has been little oversight of the

foundations, despite the law‟. „Despite provisions in law 461/98 that require

diversification of obligations, some large foundations still have portfolios heavily

concentrated in their ―original bank, with stakes varying from 30 to 90 percent. Some

foundations have also made use of bank credit (mortgages, credit lines) to fund

miscellaneous expenditures, such as capital increases, real estate acquisitions or

restructuring. Others have invested in risky derivative products‟.

Implications for banks of Foundations’ ownership – The concentrated, risky investments

mentioned in the above point „increased the riskiness of their portfolio and raised

pressure on banks to generate dividends to support the weak financial position of the

shareholder foundation. The IMF‟s FSAP stress test found that „banks influenced by

foundations are particularly vulnerable to slow growth or adverse macroeconomic

conditions. In the adverse scenario [...] the CET1 and Tier 1 capital shortfalls of this

category of banks would be respectively, €3.2 and €5.4 billion (0.2 and 0.3 percent of

GDP), accounting for 40–50 percent of the shortfall of all Italian banks in the test. Banks

Italian Banking Foundations

05 February 2014 ◆ 21

that have the highest proportion of foundation ownership display higher NPL ratios, lower

NPL provision coverage and lower capital ratios. This is confirmed by a BoI study that

indicates that bank performance has been negatively correlated to the proportion of

foundation ownership‟.

The report suggests the implementation of the following reforms for Foundations:

1. the introduction of strict divestment procedures for Foundations.

2. the diversification of investment portfolios and the requirement of minimum reserves

invested in safe assets to provide a buffer.

3. the introduction of a leverage cap to prevent levered acquisitions of risky assets.

4. the introduction of „term limits for foundation board members and of a cooling off period

between a political office and the appointment to a foundation – a provision currently left

to the „Code of Ethics‟‟.

5. „the implementation of strict oversight with prompt corrective actions‟.

...the government and BOI are on a similar page...

F. Saccomanni calling for unpleasant changes in the Foundation-Bank link in 2012...

In a speech to Foundations in June 2012, Fabrizio Saccomanni, then General Manager of the Bank of

Italy, provided the following recipe for the banking sector and for Foundations:

Foundations should diversify their investment portfolios;

Banks would need to cut costs to weather the storm of the crisis abandoning the federal

organisational model;

Banks should constrain remuneration and dividends to strengthen capital.

These measures would entail:

The dilution of Foundations‟ control over banks;

The absorption of the local banks pertaining to the larger groups into the parent company,

implying the removal of local brands, board seats and presence;

The structural fall of dividend yield for an investment in bank equity.

All the three above implications should have sounded unpleasant for Foundations whose presence in

the capital of banks aims at maintaining the attention of the company on the needs of local

households and SMEs and whose grant making activity requires cash generative investments.

...and for a reform of the Foundations’ law in 2013

In 2013, Saccomanni became Finance Minister in the Letta government. Over the year, a number of

Foundation-controlled banks went into problematic situations and a few scandals involving

Foundations broke out. The Italian press has reported his agreement with the Bank of Italy to

propose a reform of the law ruling Foundations based on four pillars:

1. Abolish the control of banks by Foundations;

2. Ensure effective portfolio diversification of investments through a cap of 30% of the total

portfolio in a single investment;

3. Forbid the underwriting of rights issues with leverage;

4. Forbid to invest in derivatives and hedge funds.

There has been little recent update on this, but if confirmed, it would pursue the recommendations

provided by the IMF last September.

Italian Banking Foundations

05 February 2014 ◆ 22

...in agreement with the Bank of Italy

In October 2013, Ignazio Visco, governor of the Bank of Italy, provided the following indications

when talking about Foundations: „Banking Foundations should have diversified their portfolios to

reduce their dependence on the results of their reference bank. Some have not done so, they will

have to adapt, taking market conditions into account‟.

This confirms the Bank of Italy‟s expectation that Foundations without diversified investment would

be potentially suffering from a financial standpoint as fixing the problem could imply the

recognition of financial losses or of material dilution in the equity stake in the reference bank.

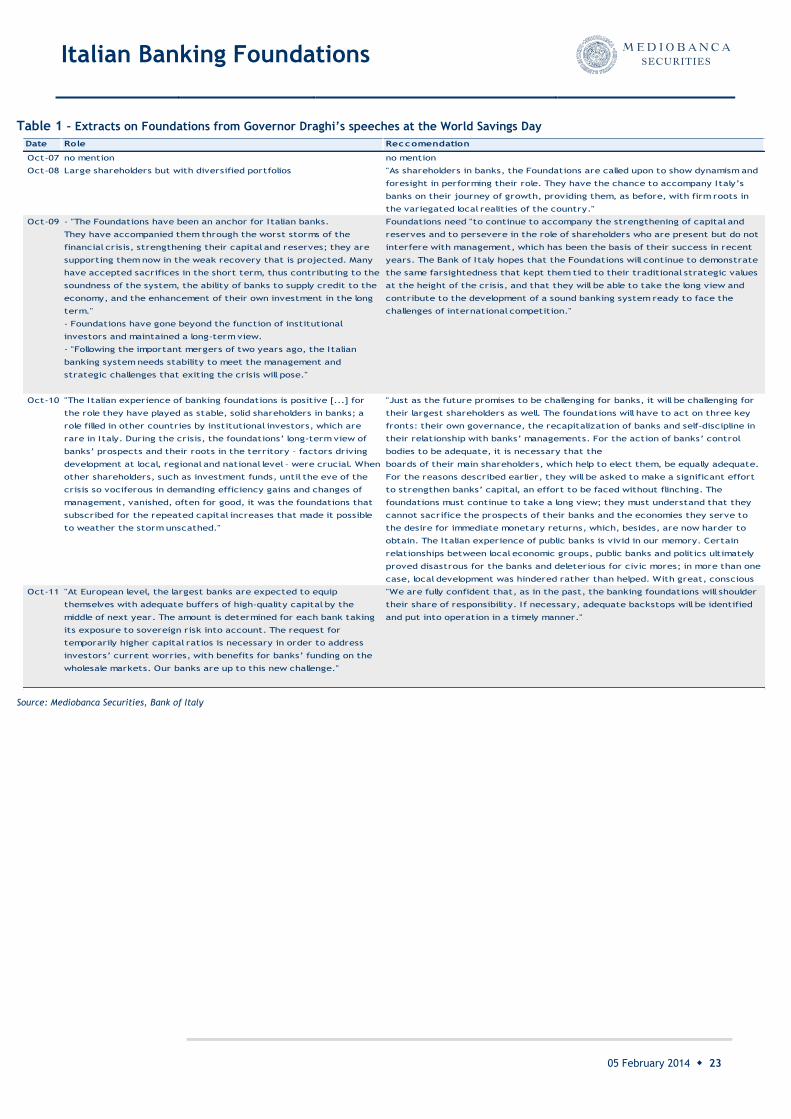

...and Draghi’s suasion were the prelude to today’s state

Mounting pressure for Foundations to put banks and the country before their interest...

Former BOI governor Mario Draghi exercised his moral suasion on the banks‟ as well as on

Foundations‟ management. Table 1 reports extracts from the Governor‟s speeches at the World

Saving Day, an annual event organised by ACRI, Italy‟ association of banking Foundations. The

beginning of the crisis marks the beginning of a recurring explicit reference made by the Governor

on the role Foundations should have in the banks. The Governor‟s requests and expectations from

the banks progressively escalated over the years:

2007 – No mention in the speech of Foundations and of their role in the banks.

2008 – The Governor‟s call is for a generic wish of having Foundations accompanying banks

on the journey of growth, providing them with firm roots. There is not explicit reference

to capital increases.

2009 - The Governor‟s request is explicitly to: support the upcoming capital increases,

refrain from interfering with management and take a long view on the return on their

investments. The tone has changed markedly on the previous year and is a call to arms, in

our view, with little gratification in exchange.

2010 – The Governor‟s intervention sets low expectations on the perspective of the

Foundations‟ investments in the banks; they are called to sacrifice and to suffer together

with „their‟ banks. Moreover, Foundations are asked to revise their governance on top of

putting further capital at the banks‟ disposal „without flinching‟. The Governor does not

envisage a good ROI but effectively warns that the alternative is the nationalisation of the

banks, recalling the poor luck of the country with state-owned banks.

2011 – The Governor anticipates that the EBA test will hit Italian banks on their sovereign

bond exposure and warns about further rights issues coming up. He once again exerts his