Issues Paper - Maximum fees and charges for cruise … · cruise ships in Sydney Harbour ......

72

Independent Pricing and Regulatory Tribunal Maximum fees and charges for cruise ships in Sydney Harbour Transport — Issues Paper March 2016

Transcript of Issues Paper - Maximum fees and charges for cruise … · cruise ships in Sydney Harbour ......

Independent Pricing and Regulatory Tribunal

Maximum fees and charges for cruise ships in Sydney Harbour

Transport — Issues PaperMarch 2016

Maximum fees and charges for cruise ships in Sydney Harbour

Transport — Issues Paper March 2016

ii IPART Maximum fees and charges for cruise ships in Sydney Harbour

© Independent Pricing and Regulatory Tribunal of New South Wales 2016

This work is copyright. The Copyright Act 1968 permits fair dealing for study, research, news reporting, criticism and review. Selected passages, tables or diagrams may be reproduced for such purposes provided acknowledgement of the source is included.

ISBN 978-1-925340-60-0 DP186

The Tribunal members for this review are:

Dr Peter J Boxall AO, Chairman

Ms Catherine Jones

Mr Ed Willett

Inquiries regarding this document should be directed to a staff member:

Melanie Mitchell (02) 9113 7743

John Smith (02) 9113 7742

Jenny Suh (02) 9113 7775

Independent Pricing and Regulatory Tribunal of New South Wales PO Box K35, Haymarket Post Shop NSW 1240 Level 15, 2-24 Rawson Place, Sydney NSW 2000

T (02) 9290 8400 F (02) 9290 2061

www.ipart.nsw.gov.au

Maximum fees and charges for cruise ships in Sydney Harbour IPART iii

Invitation for submissions

IPART invites written comment on this document and encourages all interested parties to provide submissions addressing the matters discussed.

Submissions are due by 22 April 2016.

We would prefer to receive them electronically via our online submission form <www.ipart.nsw.gov.au/Home/Consumer_Information/Lodge_a_submission>.

You can also send comments by mail to:

Review of cruise ship site occupation charges Independent Pricing and Regulatory Tribunal PO Box K35, Haymarket Post Shop NSW 1240

Late submissions may not be accepted at the discretion of the Tribunal. Our normal practice is to make submissions publicly available on our website <www.ipart.nsw.gov.au> as soon as possible after the closing date for submissions. If you wish to view copies of submissions but do not have access to the website, you can make alternative arrangements by telephoning one of the staff members listed on the previous page.

We may choose not to publish a submission—for example, if it contains confidential or commercially sensitive information. If your submission contains information that you do not wish to be publicly disclosed, please indicate this clearly at the time of making the submission. IPART will then make every effort to protect that information, but it could be disclosed under the Government Information (Public Access) Act 2009 (NSW) or the Independent Pricing and Regulatory Tribunal Act 1992 (NSW), or where otherwise required by law.

If you would like further information on making a submission, IPART’s submission policy is available on our website.

Contents

v IPART Maximum fees and charges for cruise ships in Sydney Harbour

Contents

Invitation for submissions iii

1 Introduction 1 1.1 What IPART has been asked to do 1 1.2 How we propose to conduct the review 2 1.3 The structure of this paper 3 1.4 Issues we seek comment on 4

2 Context for this review 6 2.1 The Port Authority’s roles, functions and cruise ship terminals 6 2.2 Cruise ship visits to Sydney Harbour 9 2.3 The Port Authority’s services and charges for cruise ships in Sydney

Harbour 11 2.4 Illustrative cost of the Port Authority’s charges for a typical cruise ship

visit 14

3 Our proposed approach 17 3.1 Overview of our proposed approach 17 3.2 Identify the services the Port Authority provides for cruise ships 18 3.3 Estimate the revenue required to recover efficient costs 18 3.4 Decide on forecasts of cruise ship visits 19 3.5 Assess the options for a pricing mechanism 19 3.6 Make our recommendations 20

4 Identifying the services provided by the Port Authority to cruise ships 21 4.1 Why it is important to consider all cruise ship services and charges 21 4.2 The Port Authority’s cruise ship services 22 4.3 Determine whether services should be contestable 23 4.4 Determine whether services should be charged separately 23

5 Estimating the revenue requirement 24 5.1 Building block method 24 5.2 Using a 5-year review period 26 5.3 Using separate building block models for the Port Authority’s different

services and berthing facilities 26 5.4 Estimating the allowance for operating expenditure 27 5.5 Estimating efficient capital expenditure 28 5.6 Estimating the allowance for a return on assets 29

Contents

vi IPART Maximum fees and charges for cruise ships in Sydney Harbour

5.7 Estimating the allowance for depreciation 35 5.8 Estimating the allowance for meeting tax obligations 35 5.9 Estimating the allowance for working capital 36

6 Forecasting cruise ship visits 37 6.1 Historical cruise ship visits 37 6.2 Forecast cruise ship visits 38

7 Assessing the options for price structure or pricing mechanism 39 7.1 Proposed criteria for assessing the options 39 7.1 Key issues the options need to address 40 7.2 Option 1: Current site occupation charge structure 41 7.3 Option 2: A two-part tariff 43 7.4 Option 3: An auction system 44

8 Making our recommendations 48 8.1 Commercial viability of the Port Authority 48 8.2 Total port costs and charges incurred per visit 49 8.3 Equivalent charges in other jurisdictions 50 8.4 Benefits of the cruise industry to the NSW economy 50 8.5 Changes to the regulatory framework and other reforms 51

Appendices 53 A Terms of reference 55 B More information on port charges 58 C IPART’s WACC methodology 62

1 Introduction

Maximum fees and charges for cruise ships in Sydney Harbour IPART 1

1 Introduction

Sydney is a popular destination for local and international cruise ships, and the number of ships visiting has grown strongly in recent years. In 2014-15, Sydney Harbour hosted 281 cruise ship visits1, more than any other port in Australia. An even greater number are scheduled to visit this year, including some of the world’s largest cruise ships.

The Port Authority of New South Wales (the Port Authority), a state-owned corporation, owns and operates two dedicated cruise passenger terminals in Sydney Harbour – the Overseas Passenger Terminal (OPT) in Circular Quay, and the White Bay Cruise Terminal (White Bay) near Balmain. The demand to use the OPT is increasing as larger cruise ships2 can’t fit under the Sydney Harbour Bridge to dock at White Bay. The OPT is now operating near full capacity during the peak cruising season.

In the context of this strong growth in cruise ship visits and limited passenger terminal capacity, it is important the prices the Port Authority charges cruise ships for occupying the terminals:

generate enough revenue to enable the Port Authority to operate the terminals efficiently and maintain their commercial viability over the long-term, and

send price signals to encourage the cruise industry to use the terminals efficiently.

At the same time, it is important that the impact of prices on the growth of cruise ship visits to Sydney is considered.

1.1 What IPART has been asked to do

The Premier of NSW has asked the Independent Pricing and Regulatory Tribunal of NSW (IPART) to conduct a review and make recommendations on the maximum site occupation charges the Port Authority should levy on cruise ships for using the OPT, White Bay and any other berths and moorings in Sydney Harbour.

1 Port Authority of NSW, Annual Report 2014-15, p 17. 2 Cruise ships over 80,000GT.

1 Introduction

2 IPART Maximum fees and charges for cruise ships in Sydney Harbour

Our terms of reference for this review ask us to recommend charges that:

Reflect the efficient capital and operating costs of providing the Port Authority’s existing site occupation services, and the scope for greater efficiency in providing these services so as to reduce costs, improve passenger experience and enhance efficiencies and turnaround times.

Include an appropriate price structure or other pricing mechanism that promotes the allocative efficiency of the Port Authority’s cruise ship infrastructure so as to maximise the economic benefits to the NSW economy, while avoiding cross-subsidies and overly complex pricing structures.

Take account of the need to maintain the commercial viability of the Port Authority’s cruise ship infrastructure.

We have also been asked to recommend an appropriate approach for updating the maximum site occupation charges annually. This approach should take account of administrative costs involved, be clear and simple, and provide certainty over the medium term for the cruise industry and the Port Authority.

In addition, the terms of reference ask us to have regard to a range of matters in making our recommendations. These include:

total port costs and charges incurred per visit by the cruise industry for each terminal/berth/mooring

equivalent charges applicable to the cruise industry in other national and international jurisdictions and the rates of return derived from these charges in these jurisdictions

the benefits of the cruise industry to the NSW economy and the effect any recommendations may have on the viability and growth of the industry

potential changes to the regulatory framework to encourage the efficient operation of the passenger cruise terminal facilities, and

potential reforms that could provide savings to business and the community, including net benefits for NSW, and budget implications for Government.

A copy of our terms of reference is provided at Appendix A.

1.2 How we propose to conduct the review

For this review, we will conduct a public consultation process, obtain expert advice, and undertake our own research and analysis. This paper is the first step in our consultation process, and identifies key issues on which we are seeking stakeholder input.

1 Introduction

Maximum fees and charges for cruise ships in Sydney Harbour IPART 3

We invite all interested parties to make submissions in response to the Issues Paper by 22 April 2016. (See page iii for information on how to make a submission.) We also plan to consult directly with the Port Authority and the cruise ship industry to gather further information.

We will release a Draft Report in June 2016 to explain our draft findings and recommendations, and seek submissions in response to this report. We will also hold a public forum in July 2016 to give stakeholders another opportunity to respond to the report. We will consider all submissions and public forum comments on the Draft Report before making our final recommendations and providing our Final Report to the Minister in September 2016.

Table 1.1 sets out an indicative timetable for the review. We will update this timetable on our website as the review progresses.

Table 1.1 Review timetable

Milestone Date

Release Issues Paper 21 March 2016

Submissions to Issues Paper due 22 April 2016

Release Draft Report June 2016

Public workshop July 2016

Submissions to Draft Report due July/August 2016

Release Final Report September 2016

1.3 The structure of this paper

The following chapters provide more information on the review, our proposed analytical approach and the issues we will consider:

Chapter 2 outlines the context for the review, including information on the cruise ship visits to Sydney Harbour and the Port Authority, the services it provides and the charges it levies.

Chapter 3 provides an overview of the analytical approach we propose to use to make our recommendations.

Chapters 4 to 8 discuss each of the key steps in this approach, including what we will consider in each step.

The issues on which we particularly seek stakeholder comment are highlighted in these chapters. For convenience, they are also listed below. Please feel free to comment on any or all of the issues, or provide other information or comments you consider relevant to the review and our terms of reference.

1 Introduction

4 IPART Maximum fees and charges for cruise ships in Sydney Harbour

1.4 Issues we seek comment on

The issues on which we particularly seek stakeholder comment are highlighted in the following chapters. For convenience, they are also listed below. Please feel free to comment on any or all of the issues, or provide other information or comments you consider relevant to the review and our terms of reference.

1 Do you agree with our proposed approach to the review? Are there any alternative approaches that would better meet the terms of reference, or any other issues we should consider? 20

2 What Port Authority services to cruise ships could be contestable? Are there any legislative or regulatory provisions that restrict the contestability of some services? 23

3 Would it be more efficient to include the compulsory charges outlined in Table 4.1 in the site occupation charge? Which charges should or should not be included in the site occupation charge? 23

4 Do you agree with our proposed approach to share supplementary revenue equally between the Port Authority and customers? 26

5 Do you agree with our proposed review period of five years? If not, what period do you prefer and why? 26

6 Should land at terminals and berthing precincts be valued based on existing use or most valuable use? 30

7 Do you agree with our proposed approach to valuing the initial asset base and allocating shared assets? Are there other approaches or issues we should consider? 32

8 Do you agree with our proposed approach to determining the industry-specific WACC parameters? Are there any other comparable businesses we should consider? 35

9 Do you agree with our overall proposed implementation of the building block model? Are there any other issues we should consider? 36

10 Are there other sources of information or other issues we should consider in deciding on forecasts of cruise ship visits? Is there a need for a mechanism to manage demand risk? 38

11 Do you agree with our proposed criteria for assessing the options for a price structure or pricing mechanism? Are there any other criteria we should consider? 40

1 Introduction

Maximum fees and charges for cruise ships in Sydney Harbour IPART 5

12 What are your views on the three preliminary options for a price structure or pricing mechanism – the current site occupation charge structure; a two-part tariff; and an auction system? Are there any other benefits or limitations we have not considered? Are there other alternatives you would like to see considered? 47

13 What sort of notice or transition period would be required to implement a new price structure or pricing mechanism? 47

14 Should bookings for slots be based on shorter time periods than the current 24-hour slot? Are there any other methods to increase the number of ships that can berth at a terminal in peak times? 47

15 What type of non-Port Authority charges are incurred by cruise ships for a typical visit to Sydney Harbour? How much are these charges? 50

16 What are the external costs and benefits of cruise ships in Sydney Harbour? 51

17 Are there any changes to the regulatory framework or reforms that would encourage more efficient operation of the passenger cruise terminals or provide savings or net benefits to the community? 51

2 Context for this review

6 IPART Maximum fees and charges for cruise ships in Sydney Harbour

2 Context for this review

IPART is reviewing the site occupation charges the Port Authority levies on cruise ships for using the passenger terminals in Sydney Harbour. We’ve been asked to recommend maximum site occupation charges that reflect the efficient costs of providing the terminals, promote the allocative efficiency of the infrastructure involved, and maintain the commercial viability of this infrastructure. To provide the context for this review, the sections below outline:

the Port Authority’s roles, functions and passenger terminals in Sydney Harbour

the number and growth in cruise ship visits to Sydney Harbour

the services the Port Authority provides to visiting cruise ships and the charges it levies for these services, and

the total cost of these services for a typical cruise ship.

2.1 The Port Authority’s roles, functions and cruise ship terminals

The Port Authority is a state-owned corporation that provides a variety of port and maritime services in Sydney Harbour, Port Botany, Port Kembla and the ports of Newcastle, Yamba and Eden. It was formed on 1 July 2014 when the Sydney, Newcastle and Port Kembla Port Corporations were amalgamated following the NSW Government’s long-term leasing of each corporation’s landside operations.

2.1.1 The Port Authority’s roles and functions

The Port Authority’s statutory objectives and functions are derived from the State Owned Corporations Act 1989, Ports and Maritime Administration Act 1995 and its Port Safety Operating Licence. In addition to operating the cruise ship terminals at Sydney Harbour, its responsibilities in all ports include:

the role of Harbour Master

management of harbour/port approaches and channels

safety of navigation and shipping movements

pilotage

2 Context for this review

Maximum fees and charges for cruise ships in Sydney Harbour IPART 7

port security

safety of operations

management of dangerous goods regulations

contingency planning and emergency response to marine-based incidents, and

clean-up of spills in the marine environment.3

The Port Authority provides these services for both cruise and non-cruise trade vessels. Around 10% of chargeable vessel movements in Sydney Harbour and Port Botany relate to cruise ships (Figure 2.1).

Figure 2.1 Chargeable vessel visits in Sydney, 2014-15

Note: Trade vessel visits include Sydney Harbour and Port Botany.

Data source: Port Authority of NSW, Annual Report 2014-15, p 17.

While the Port Authority owns many of the assets that are used to provide its services, the seabeds of Sydney Harbour, Botany Bay, Newcastle Harbour and Port Kembla and the channels and berthing boxes are owned by Roads and Maritime NSW (RMS). These are licensed to the Port Authority for its non-exclusive use.

2.1.2 The Port Authority’s passenger terminals in Sydney Harbour

The Port Authority owns and operates two dedicated passenger terminals – OPT and White Bay. The Port Authority resources each cruise terminal with an onsite Duty Manager of Operations supported by an asset manager who manages and oversees all aspects of terminal operations including ship day activities. In addition to these, it has non-dedicated passenger terminal White Bay 4, which is available, but infrequently used by cruise ships. 3 Port Authority of NSW, Annual Report 2014-15, p 9.

Chargeable cruise ship visits ,

281, 10%

Chargeable trade vessel visits ,

2476, 90%

2 Context for this review

8 IPART Maximum fees and charges for cruise ships in Sydney Harbour

Overseas Passenger Terminal

The OPT is located on Circular Quay, within sight of some of Sydney’s major tourist attractions and on the edge of the CBD. It has undergone several makeovers since it opened in 1960. The most recent upgrade, completed in 2014-15, improved the terminal’s efficiency and capacity to service the growing cruise market. This upgrade included a new mezzanine floor for passenger check-in, new lifts, escalators and a large travelator and more space for baggage. The new design and additional floor space enables passengers to embark and disembark at the same time reducing a ship’s turnaround time by up to 2.5-hours.4

At the same time as the terminal upgrade, the OPT wharf was extended by 60 metres so that it can host the increasing number of large cruise ships visiting Sydney. For example, this includes the Ovation of the Seas which is scheduled to berth at the OPT in December 2016. At close to 170,000 gross tonnes and 5,000 passengers, this will be the largest cruise ship to sail in Australian waters.

White Bay Cruise Terminal

This is a modern terminal located at White Bay 5. Officially opened on 19 April 2013, it features approximately 4,000 square meters of floor space, a dedicated baggage drop facility and short-term parking for up to 200 vehicles. The arrivals and departures halls can cater for up to 2,400 passengers at a time.5 It can also host functions or events on non-cruise days.

The White Bay Cruise Terminal is the designated ‘home port’ for cruise ships serving the domestic market.

Other berthing and mooring facilities

A non-dedicated passenger terminal can be provided adjacent to White Bay 5, at White Bay 4, by erecting temporary structures for customer clearance and baggage storage. This enables two cruise ships to berth at White Bay at the same time. It is also possible for two cruise ships to share the White Bay Cruise Terminal operational space, sharing the costs for security and cleaning, with no requirement for temporary infrastructure at White Bay 4.

4 Advice from the Port Authority of NSW. 5 Sydney Ports Corporation, Annual Report 2012-13, October 2013, p 29.

2 Context for this review

Maximum fees and charges for cruise ships in Sydney Harbour IPART 9

There are also berthing facilities at Glebe Island 1 and 2 that cruise ships could use if the OPT, White Bay Cruise Terminal and White Bay 4 are all occupied. However, the Port Authority has informed us that no cruise ship has docked at Glebe Island in the last 30 months and they have not forecast any cruise ships using those facilities in the future. Most of the time, these and other non-passenger berthing facilities6 are used for:

loading and unloading vessels transporting construction materials, other bulk materials and bulk liquids

refuelling cruise and other ships

undertaking emergency response and repairs to vessels.7

Additional mooring facilities are also available on the buoys at Athol Bay and Point Piper.

2.2 Cruise ship visits to Sydney Harbour

In 2014-15 Sydney Harbour hosted a record 281 cruise ship visits, making it the most visited cruise ship port in Australia. In line with the national trend, the number of cruise ship visits has grown steadily over the last five years.

These visits fall into several categories (see Box 2.1). Typically, they involve an arrival in the morning and departure in the afternoon or evening on the same day. However, some cruise ships stay in Sydney Harbour overnight.

The Port Authority publishes a cruise schedule on its website8 that enables cruise ship operators to see when the OPT, White Bay Cruise Terminal and White Bay 4 are available in the coming years. The schedule shows the projected arrival and departure times of cruise ships booked to berth at each facility. Currently, bookings are made on a first come first served basis, with established protocols around this process.9 The Port Authority is in the process of reviewing its booking system and is currently consulting with stakeholders independently of this review.

6 Including White Bay 3 and Glebe Island 7 and 8. 7 Port Authority of NSW, Annual Report 2014-15, p 17; Port Authority of NSW, Annual Report

2013-14, p 13. 8 The Port Authority cruise schedule is available at

http://www.sydneyports.com.au/port_operations/cruise_schedule. 9 The passenger vessel protocol is available at

http://www.sydneyports.com.au/__data/assets/pdf_file/0016/33226/Passenger_Vessel_Booking_Protocol_2016_Final.pdf.

2 Context for this review

10 IPART Maximum fees and charges for cruise ships in Sydney Harbour

Box 2.1 Cruise ship visit categories

Cruise ship visits can be categorised into:

Home port – these vessels are based in Sydney and their passengers are mainlyNSW-based. Their destinations are South Pacific islands, New Zealand, otherAustralian cities or days at sea. These cruises start and end in Sydney and take placeacross the year.

Seasonal – these vessels are deployed from the Northern Hemisphere during theiroff-season (October – April) to undertake Asia-Pacific cruises. The passengers areAustralian and international tourists.

Round the world/vessels in transit – these vessels are based overseas and Sydneyis one destination on a longer cruise through the South Pacific or around the world.The majority of visits are in peak summer months (January - February) and thepassengers are mostly international tourists.

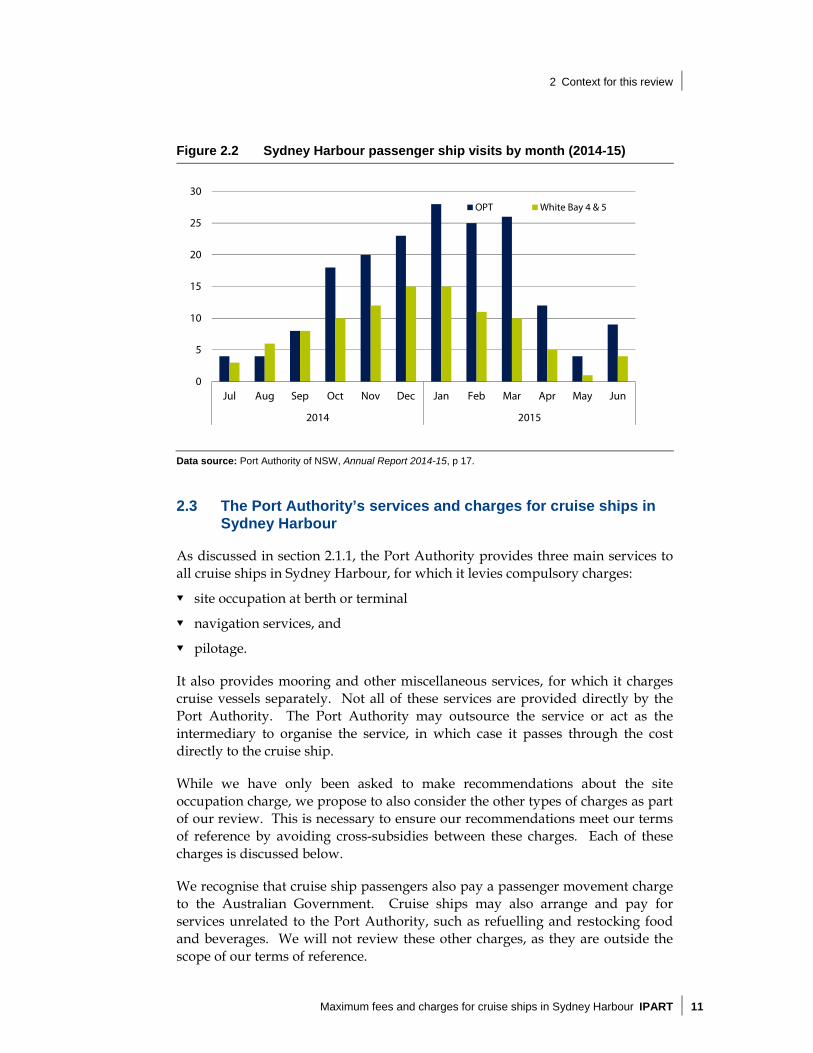

The majority of cruise visits take place in the summer months, and the OPT is the most frequently used berthing facility (Figure 2.3). However, the terminal is already operating near capacity during the peak season. In addition, there is a growing trend for larger cruise ships to visit Sydney. These larger ships can only use the OPT as they can’t fit under the Sydney Harbour Bridge to dock at White Bay. The NSW Government has committed to a Cruise Development Plan to address this and other issues related to the growth of the cruise industry.10 The Australian Government has also conducted a review of berthing facility options east of the Sydney Harbour Bridge.11

10 NSW Trade & Investment, Visitor Economy Industry Action Plan – The NSW Government Response

to the Final Report of the Visitor Economy Taskforce, December 2012, p 24. 11 Australian Government, Independent Review of the Potential for Enhanced Cruise Ship Access to

Garden Island Sydney, February 2012.

2 Context for this review

Maximum fees and charges for cruise ships in Sydney Harbour IPART 11

Figure 2.2 Sydney Harbour passenger ship visits by month (2014-15)

Data source: Port Authority of NSW, Annual Report 2014-15, p 17.

2.3 The Port Authority’s services and charges for cruise ships in Sydney Harbour

As discussed in section 2.1.1, the Port Authority provides three main services to all cruise ships in Sydney Harbour, for which it levies compulsory charges:

site occupation at berth or terminal

navigation services, and

pilotage.

It also provides mooring and other miscellaneous services, for which it charges cruise vessels separately. Not all of these services are provided directly by the Port Authority. The Port Authority may outsource the service or act as the intermediary to organise the service, in which case it passes through the cost directly to the cruise ship.

While we have only been asked to make recommendations about the site occupation charge, we propose to also consider the other types of charges as part of our review. This is necessary to ensure our recommendations meet our terms of reference by avoiding cross-subsidies between these charges. Each of these charges is discussed below.

We recognise that cruise ship passengers also pay a passenger movement charge to the Australian Government. Cruise ships may also arrange and pay for services unrelated to the Port Authority, such as refuelling and restocking food and beverages. We will not review these other charges, as they are outside the scope of our terms of reference.

0

5

10

15

20

25

30

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

2014 2015

OPT White Bay 4 & 5

2 Context for this review

12 IPART Maximum fees and charges for cruise ships in Sydney Harbour

2.3.1 Site occupation charge

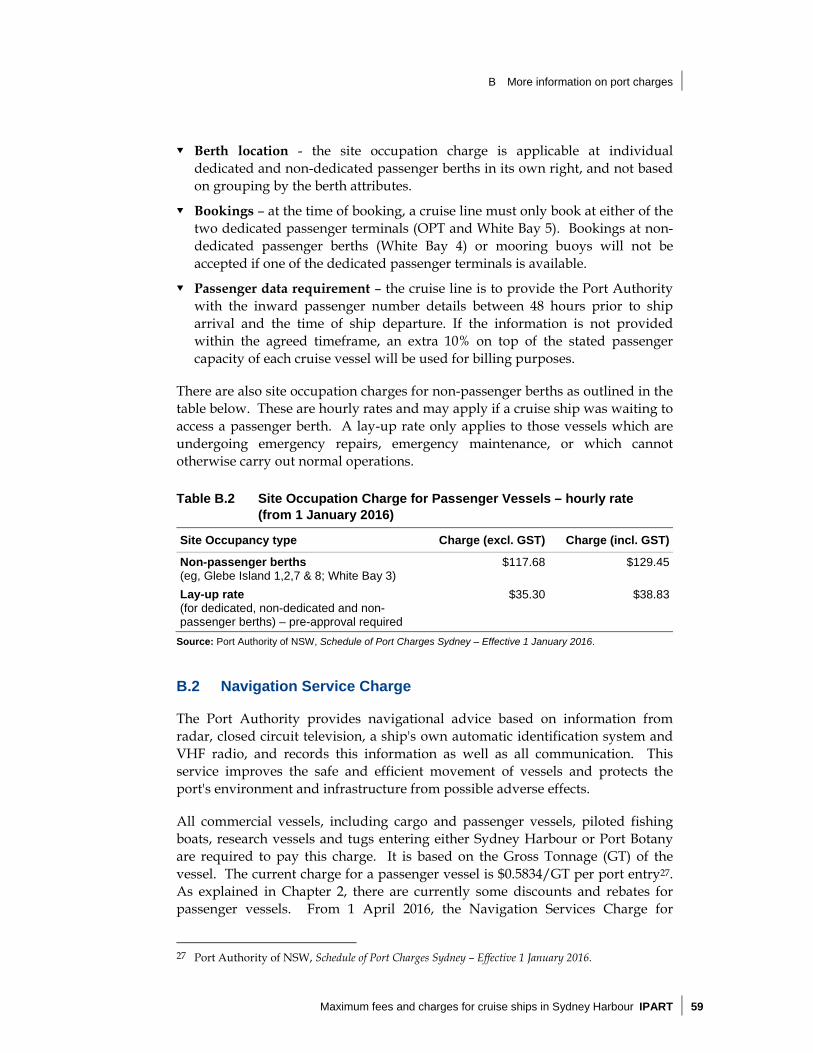

The site occupation charge is a fee for the use of a berthing facility. Currently, the site occupation charge is based on the number of incoming passengers arriving on the cruise ship12, and is charged per 24-hour slot. This means if a cruise ship’s stay at port is 12 hours, it pays for one 24-hour slot. If it stays 25 hours, it pays for two 24-hour slots. (Table 2.1 summarises the current level of these charges.)

Table 2.1 Site occupation charge for cruise ships in Sydney Harbour – per passenger, per 24-hour slot (from 1 January 2016)

Site type Charge (ex GST)

Dedicated passenger terminal (OPT and White Bay 5)

$30

Non-dedicated passenger terminal (White Bay 4)

$15

Source: Port Authority of NSW, Schedule of Port Charges Sydney - Effective 1 January 2016.

The site occupation charge for White Bay 4 is half the rate for the dedicated passenger terminals because, as discussed above, there are no permanent passenger facilities there. Temporary shelters are erected when it is used by a cruise ship, and the ship pays for the cost of this. Some cruise ships – for example vessels in transit – prefer to book White Bay 4 to take advantage of the lower charge.

Between 1992 and 2013, the site occupation charge was based on an hourly fee for all cruise ships using the dedicated passenger terminals. This fee was set at $670 between 1 July 1992 and 30 June 1997. From 1 July 1997 to 30 June 2013, the site occupation charge remained fixed at $250 per hour to support the growth of the cruise industry. From 1 July 2000 to 30 June 2013, the site occupation charge for all other non-passenger berths remained at $200 per hour. However, since 1 July 2013, the charge has been based on a per passenger fee and increased to assist with financing infrastructure upgrades and to provide a commercial return on NSW’s investment in cruise ship facilities.13 This fee was originally set at $20 per passenger per 24-hour slot on 1 July 2013, but was discounted to $18 following feedback from the industry that they would not be able to recoup the fee from passengers who had made bookings prior to the fee’s implementation. The fee was increased to $25 per passenger on 1 July 2014 and $30 per passenger on 1 July 2015.

As well as the different rates that apply to the dedicated passenger terminals and other berthing facilities, some rules apply to the site occupation charge. These are discussed in Appendix B.

12 As recorded in the ship’s Inward Passenger Manifest Declaration, excluding infants and crew. 13 Sydney Ports Corporation, Annual Report 2012-13, October 2013, p 20.

2 Context for this review

Maximum fees and charges for cruise ships in Sydney Harbour IPART 13

2.3.2 Navigation services charges

Navigation Services Charges are authorised by the Ports and Maritime Administration Act 1995, Part 5, Division 2 and are payable in respect of the general use by a vessel of a designated port and its infrastructure.

The charges relate to the provision of the following services and facilities to vessels:

Channels and Berthing Boxes (Maintenance Dredging).

Hydrographical Surveys.

Navigation Ads.

Ports Operations (Communications, Traffic Control and Integrated Vessel Surveillance System).

Port Safety.

Port Security.

Emergency Response Service.

Environmental Control (Protection and Pollution Control).

Harbour Master’s Duties and Responsibilities.

These services improve the safe and efficient movement of vessels and protect the port’s environment and infrastructure.

Cruise ships (and all other commercial vessels) entering Sydney Harbour are required to pay for these navigational services each time they enter the port. The charge for these services is based on the gross tonnage (GT) of the vessel. The current charge is $0.5834/GT (excl. GST) per port entry, which came into effect on 1 January 2016. However, the Port Authority has advised us that all cruise vessels have a 35% discount on this rate, and a further rebate of 9.64% since August 2014. The 9.64% rebate was granted to all ship companies on the basis that during the financial year 2014-15 the OPT was being upgraded and cruise ships would likely experience a measure of inconvenience during the reconstruction works. The 9.64% will be reduced to 7.00% on 1 April 2016. The rebate will gradually be eliminated now that the OPT upgrade is completed.

Additionally, the 35% concession can be increased by a further 15% (ie, a 50% concession in total) for all passenger vessel visits after the 29th visit in a financial year. This concession applies on a group basis such that one company that operates more than one cruise line will benefit as the concession will apply to all vessels after the 29th visit in aggregate for that company.

As noted above, RMS owns the channels and berthing boxes in Sydney Harbour. As these are required by the Port Authority to provide its services, channel fees are paid by the Port Authority to RMS based on a percentage of the navigation service charge revenue per annum. The channel fee is currently set at 13.8% of

2 Context for this review

14 IPART Maximum fees and charges for cruise ships in Sydney Harbour

the navigation service charge (excluding Maritime Security Charges and GST). Under a Channel Licence Agreement between the two parties, RMS grants the Port Authority a non-exclusive licence to not only use the channels and berthing boxes, but also to undertake maintenance dredging; and to repair, maintain, install and remove navigation aids.

2.3.3 Pilotage charge

Cruise ships (and all other commercial vessels) entering, leaving or moving within Sydney Harbour must take on board a marine pilot to conduct their movement. The pilotage charge is calculated on a tiered basis based on the gross tonnage of the ship. Cruise ships pay the charge, plus a boarding fee, for each inbound and outbound movement within the harbour. As with the navigation services charges, pilotage charges for cruise ship vessels have been granted a rebate of 9.64%, since August 2014, to all ship companies in connection with the OPT upgrade. This rebate will be reduced to 7% on 1 April 2016. The rebate will gradually be eliminated now that the OPT upgrade is completed. More information on pilotage charges is provided in Appendix C.

2.3.4 Miscellaneous charges

Cruise ships can also incur other fees for a range of miscellaneous services, including mooring (which apply if the ship moors on a buoy), security, cleaning, furniture hire and water usage (as applicable). More information on these charges is provided in Appendix C.

2.4 Illustrative cost of the Port Authority’s charges for a typical cruise ship visit

As Chapter 1 indicated, our terms of reference for this review require us to have regard to a range of matters in making our recommendations on the Port Authority’s site occupation charge. These include the total costs of the Port Authority’s charges per cruise ship visit to Sydney Harbour, and the equivalent charges applicable in other Australian and international ports.

While we will do further work on these costs and charges, we have conducted preliminary analysis of the main port charges for two different cruise ship visits at the OPT and White Bay 5 in comparison with those that would apply at the ports in Melbourne and Brisbane. Table 2.2 summarises our assumptions for the calculations.

2 Context for this review

Maximum fees and charges for cruise ships in Sydney Harbour IPART 15

Table 2.2 Assumptions for the main port charge calculations

Cruise ship A Cruise ship B

Terminal OPT WB 5 Terminal

Type of berth Dedicated passenger berth Dedicated passenger berth

Gross tonnage 167,800 70,310

Length 348 meters 245 meters

Chargeable passenger number

4,905 1,950

Number of pilot movements 2 2

Length of stay at passenger berth

12 hours 12 hours

Note: For a cruise ship visit from 1 April 2016.

As Figure 2.3 shows, Cruise ship A berthed at the OPT would incur approximately $217,847 in site occupation, pilotage and navigation service charges. The site occupation charge makes up about 68% of the total charges. Cruise ship B, which is of a much smaller size and berthed at White Bay 5, would incur a total port charge of $93,340. The site occupation charge represents about 63% of the total charges.

Figure 2.3 Example port charges at OPT and White Bay compared to other ports (ex-GST)

Note: In Melbourne, site occupation is referred to as ‘berth hire’ and navigation is included in ‘channel fees’. In Brisbane, navigation includes Harbour dues and conservancy fees.

Data source: Port Authority of NSW, Schedule of Port Charges Sydney - Effective 1 January 2016; Port of Melbourne, Reference Tariff Schedule - Effective 1 July 2015; Port Phillip Sea Pilots Pty Ltd, Pilotage Rates - Effective1st July 2015; Port of Brisbane, Schedule of Port Charges as at 1 July 2015; Maritime Safety Queensland, Fees and charges, available at http://www.msq.qld.gov.au/About-us/Current-fees.aspx#pilotage.

2 Context for this review

16 IPART Maximum fees and charges for cruise ships in Sydney Harbour

These charges take account of the current 35% discount on navigation fees and 7% rebate on navigation and pilotage fees offered by the Port Authority to cruise passenger vessels from 1 April 2016. The charges do not include the additional 15% discount on navigation fees for passenger vessels exceeding 29 visits in a financial year (as it is not available to all vessels). We have based our calculations for Melbourne and Brisbane on published fees and charges, which do not include any unpublished discounts or rebates that may be available to passenger vessels at those ports.

In terms of the structure of these charges, there are some similarities and some differences between Sydney, Melbourne and Brisbane:

in Melbourne, cruise ships are charged a flat rate to use a port berth for the first 24 hours and an hourly rate thereafter (the charge is not based on passenger numbers)

in Brisbane, they are charged a flat rate per 24-hour period to use a multi-user terminal

also in Brisbane, pilotage charges are based on the length of the vessel, not the gross tonnage as in Sydney and Melbourne, and

at each of these ports, the navigation fees are based on the gross tonnage of the vessel.

3 Our proposed approach

Maximum fees and charges for cruise ships in Sydney Harbour IPART 17

3 Our proposed approach

We have developed an approach we propose to use to guide our analysis and decision-making for this review. The approach ensures we will consider all the matters specified in our terms of reference outlined in Chapter 1, and take account of the contextual issues discussed in Chapter 2.

Our proposed approach is similar to one we use in determining prices in some of the industries we regulate, such as the water industry. It makes use of key methodologies we have developed and tested over time. However, there is also an important difference between this review and our regulatory reviews. The prices we determine for regulated businesses are generally binding on these businesses. In this review, we are only making recommendations. The NSW Government will make the final decisions on the site occupation charge and associated charging arrangements.

The sections below provide an overview of our proposed approach and each of its key steps. Chapters 4 to 8 discuss each step in more detail, including our preliminary analysis and views where we have them.

3.1 Overview of our proposed approach

Our proposed approach involves five steps:

1. Identify all services for cruise ships provided by the Port Authority and determine whether any of these should be contestable and whether they should be levied separately or included in the site occupation charge.

2. Estimate the revenue required to recover the efficient costs of providing all the Port Authority’s cruise ship services over the price-setting period using our ‘building block’ methodology.

3. Decide on the forecast cruise ship visits over this period.

4. Assess the options for the price structure or pricing mechanism for the Port Authority’s cruise terminal and berthing services (ie, the services for which site occupation charges currently apply) by considering how well they would:

a) recover the efficient costs of providing the cruise terminal and berthing services given expected demand for them, and

b) promote the efficient use of infrastructure related to these services.

3 Our proposed approach

18 IPART Maximum fees and charges for cruise ships in Sydney Harbour

5. Make our recommendations based on the findings from the first three steps and having regard to the other matters in our terms of reference.

3.2 Identify the services the Port Authority provides for cruise ships

As discussed in Chapter 2, the Port Authority carries out a number of functions in addition to managing terminals and berthing facilities and cruise ships may incur a number of miscellaneous charges for these services in addition to site occupation, navigation and pilotage.

Our first step is to identify all the services that the Port Authority provides for cruise ships and review whether these services should be:

contestable – whether the cruise operator should be able to choose whether to procure the services from the Port Authority or another external provider, and

charged separately – whether the charges that apply should be levied separately or included in the site occupation charge

Currently, all primary (site occupation, navigation and pilotage) and miscellaneous services are either provided by or procured through the Port Authority. However, it may be more efficient for cruise vessels to procure some of these services directly through a third party. This may reduce costs and improve efficiency for both the Port Authority and the cruise operator.

For services that we determine are either more efficiently procured through the Port Authority, or must be procured through the Port Authority for other legislative or regulatory reasons (eg, for security reasons), we will examine whether these services are optional or compulsory – that is, whether the service is something that only some or all cruise ships undertake when they dock at the terminal or berth.

We will then determine whether it is more efficient for the Port Authority to charge for these services separately or bundled together (ie, as part of the site occupation charge).

3.3 Estimate the revenue required to recover efficient costs

In most industries where we determine prices, we use a building block method to estimate how much revenue the business needs to generate from prices over the determination period to recover the efficient costs of providing the regulated services to the required standard. This approach involves ‘building up’ this revenue requirement by calculating and adding individual ‘cost blocks’ such as the efficient operating costs, a return on assets and depreciation for each year of the determination period.

3 Our proposed approach

Maximum fees and charges for cruise ships in Sydney Harbour IPART 19

For this review, we propose to use this building block method to estimate the Port Authority’s revenue requirement to recover the efficient costs of providing each of its cruise ship services over a 5-year period (2016-17 and 2020-21).14 We will consider the Port Authority’s historical and projected operating and capital costs. We also propose to engage an external consultant to review the Port Authority’s historical and projected costs and provide advice to us on their efficiency.

Chapter 5 provides a more detailed description of the building block method and how we propose to apply it. It also discusses some of the key issues we will consider in this step and seeks comment from stakeholders.

3.4 Decide on forecasts of cruise ship visits

Once we have estimated the revenue requirement, the next step in our proposed approach is to decide on the forecast chargeable cruise ship visits to Sydney Harbour over the 5-year review period. We will use these forecasts to calculate the price levels needed to recover the revenue requirement for the Port Authority’s cruise terminal and berthing services over this period.

3.5 Assess the options for a pricing mechanism

The next step in our proposed approach is to assess the options for the price structure or other pricing mechanism. In line with the terms of reference for this review, we need to identify which option will best recover the efficient costs of the Port Authority’s cruise terminal and berthing services and send price signals that promote more efficient use of the infrastructure used to provide these services.

At this stage, we propose to investigate the merits of three options:

the current site occupation charge levied by the Port Authority as a single, variable charge on a per passenger basis

a two-part site occupation charge, comprising a fixed charge and a variable charge that could be based on passengers, tonnes or time, and

an auction system for booking slots at each cruise terminal or berthing facility.

We will also consider an appropriate approach to updating prices annually that considers administrative costs, promotes a clear and simple pricing structure and provides certainty over the medium term for the cruise industry and the Port Authority.

14 We will only estimate the efficient costs of services provided by the Port Authority in this step.

As Chapter 2 noted, the charges cruise ships pay for services from other parties are outside the scope of our review.

3 Our proposed approach

20 IPART Maximum fees and charges for cruise ships in Sydney Harbour

3.6 Make our recommendations

The final step in our proposed approach is to make our recommendations based on the findings from the first four steps and having regard to other matters in our terms of reference, including:

the effect of our recommendations on the commercial viability of the Port Authority

equivalent charges on cruise ship visits to other national and international ports and the rates of return derived from these charges

the benefits of the cruise industry to the NSW economy and the effect our recommendations on the viability and growth of the industry

changes required to the regulatory framework to encourage the efficient operation of the passenger cruise terminal facilities, and

potential reforms that could provide savings to business and the community, including net benefits for NSW, and budget implications for the NSW Government.

IPART seeks comments on the following

1 Do you agree with our proposed approach to the review? Are there any alternative approaches that would better meet the terms of reference, or any other issues we should consider?

4 Identifying the services provided by the Port Authority to cruise ships

Maximum fees and charges for cruise ships in Sydney Harbour IPART 21

4 Identifying the services provided by the Port Authority to cruise ships

The first step in our proposed approach is to identify all the services the Port Authority provides for cruise ships and determine whether any of these should be:

contestable – whether the cruise operator should be able to choose whether to procure the services from the Port Authority or another external provider, and

charged separately – whether the charges that apply should be levied separately or included in the site occupation charge.

This chapter discusses the relevant cruise ship services for which charges are levied by the Port Authority. It explains how we will determine whether the service should be contestable and charged separately or bundled in with the site occupation charge.

4.1 Why it is important to consider all cruise ship services and charges

Our terms of reference ask us to recommend charges that reflect the scope for greater efficiency in supply of existing services so as to reduce costs and enhance efficiencies and turnaround times. It also asks us to avoid cross-subsidies in our pricing structure. As such, we need to identify whether the services provided by, or procured through, the Port Authority are being provided at least cost. If the service could be provided directly by a third party at a lower cost or in a shorter timeframe, then this could reduce costs, improve efficiencies and reduce turnaround times for operators and passengers.

If the service is routinely provided to all (or a majority of) cruise ships, then it is a standard operating cost for the Port Authority that can be forecasted in advance. As such, it may be more efficient to include those costs in the site occupation charge, rather than administer multiple separate charges. If the service is provided on an ad hoc basis to some cruise ships, it may be more efficient to charge separately so that only the users of that service pay for it.

4 Identifying the services provided by the Port Authority to cruise ships

22 IPART Maximum fees and charges for cruise ships in Sydney Harbour

For all services we will consider whether the current charge reflects the efficient cost of providing that service. If charges do not reflect the efficient cost of providing a service it means that there may be some cross-subsidisation of these costs through other charges, such as the site occupation charge or vice versa. How we propose to determine efficient costs is discussed further in Chapter 5.

4.2 The Port Authority’s cruise ship services

Currently, all the services provided to cruise ships are not contestable. They must be provided by, or procured through, the Port Authority.15 Not all of these services are provided directly by the Port Authority. The Port Authority may outsource the service or act as the intermediary to organise the service, in which case it passes through the cost to the cruise ship. Some of these services are compulsory – they are undertaken by all cruise vessels that dock in Sydney Harbour – and some are optional – they are undertaken by only some cruise vessels. Table 4.1 summarises the current cruise ship services and how they are provided.

Table 4.1 Current services and charges for cruise ships in Sydney Harbour

Charge type Service type Contestable

Site occupation Compulsory No

Navigation services Compulsory No

Pilotage Compulsory No

Buoy (per vessel, per hour) Optional No

Navigation light handling fee (flat rate per vessel, per use)

Optional No

Security Compulsory No

Cleaning Charges (per Vessel Call) - OPT Compulsory No

Cleaning Charges (per Vessel Call) - WB5 Compulsory No

Standard Furniture Hire Compulsory No at WB5 or OPT

Non-Standard Furniture Hire Optional No at WB5 or OPT

Hose Handling Fee Optional No if required

Additional Hours Gangway(s) Hire (per hour) - From 8:00pm to 6:00am

Optional No

Water per KL Optional No

Berthing facility insurance surcharge (per vessel, per hire, per period)

Compulsory No

Source: As advised by the Port Authority of NSW.

15 Except for furniture hire at White Bay 4.

4 Identifying the services provided by the Port Authority to cruise ships

Maximum fees and charges for cruise ships in Sydney Harbour IPART 23

4.3 Determine whether services should be contestable

If a service could be provided directly to the cruise ship by another provider in the market, then the service is considered to be ‘contestable’. In this case a cruise operator can shop around to find the best service and price for their needs.

Services that may only be provided by or procured through the Port Authority are not contestable. The cruise ship does not have a choice in who provides or how much it pays for the service. For example, all ships entering Sydney Harbour must be guided by an experienced pilot, except in limited circumstances where a ship’s captain has the necessary skills and experience and has applied for an exemption. Currently, the Port Authority provides pilotage services on an exclusive basis.

Services may be non-contestable because of regulatory or legislative restrictions. For example, for safety or security reasons, the Port Authority may be the only provider currently authorised to provide the service.

IPART seeks comments on the following

2 What Port Authority services to cruise ships could be contestable? Are there any legislative or regulatory provisions that restrict the contestability of some services?

4.4 Determine whether services should be charged separately

Many of the services listed in Table 4.1 are compulsory – that is, they are routinely provided to all cruise ships. This means that a charge is levied for that service for every chargeable call. This may not be the most efficient way of charging for the service as it incurs additional administrative costs on behalf of the Port Authority and the cruise operator.

Services that are routinely performed should be able to be forecast in advance as a standard operating cost for the Port Authority. As such, it may be more efficient to include those costs in the site occupation charge, rather than through multiple separate miscellaneous charges.

If the service is optional – that is, it is undertaken for only some cruise ship visits, it may be more efficient to charge separately so that only the users of that service pay for it. For example, gangway hire, furniture hire and water.

IPART seeks comments on the following

3 Would it be more efficient to include the compulsory charges outlined in Table 4.1 in the site occupation charge? Which charges should or should not be included in the site occupation charge?

5 Estimating the revenue requirement

24 IPART Maximum fees and charges for cruise ships in Sydney Harbour

5 Estimating the revenue requirement

The next step in our proposed approach is to estimate the total revenue that is required to recover the efficient costs of providing the Port Authority’s cruise ship services. As Chapter 3 discussed, we propose to use the building block method for this step. The sections below:

provide an overview of the building block method

discuss our preliminary views on how we will apply this method, including:

– using a 5-year review period, and

– using separate building block models to estimate the efficient costs of providing pilotage services, navigational services, and cruise terminal and berthing services at each of the different passenger terminals and berthing facilities

outline how we propose to calculate each of the cost building blocks, including the key issues we will need to consider in doing so.

5.1 Building block method

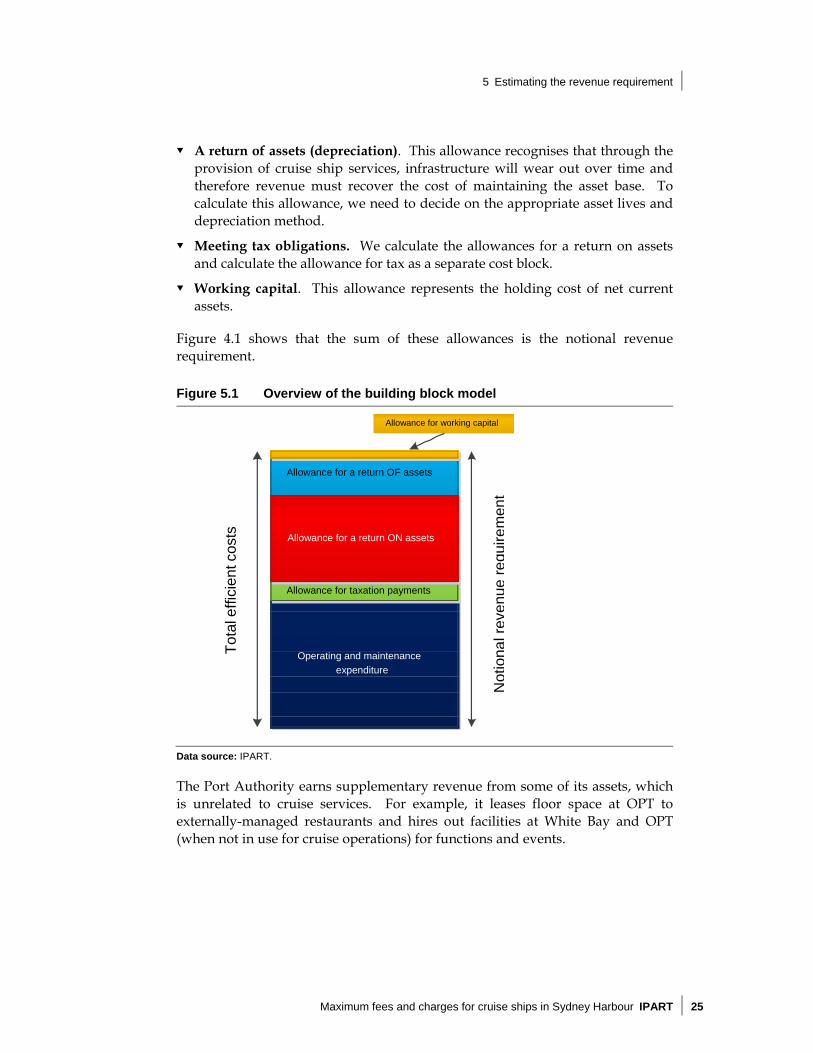

5.1.1 Overview of the building block method

Under the building block method we build up the total revenue required to cover the total efficient costs of providing cruise ship services, which includes an allowance for:

Operating expenditure, which represents our estimate of forecast efficient operating, maintenance and administration costs associated with providing cruise ship services.

A return on assets used by the Port Authority to provide cruise ship services. This represents our assessment of the opportunity cost of the capital invested by the Port Authority, and ensures that it can continue to make efficient investments in capital in the future. To calculate it, we need to decide on the value of the initial asset base, and the appropriate rate of return.

5 Estimating the revenue requirement

Maximum fees and charges for cruise ships in Sydney Harbour IPART 25

A return of assets (depreciation). This allowance recognises that through the provision of cruise ship services, infrastructure will wear out over time and therefore revenue must recover the cost of maintaining the asset base. To calculate this allowance, we need to decide on the appropriate asset lives and depreciation method.

Meeting tax obligations. We calculate the allowances for a return on assets and calculate the allowance for tax as a separate cost block.

Working capital. This allowance represents the holding cost of net current assets.

Figure 4.1 shows that the sum of these allowances is the notional revenue requirement.

Figure 5.1 Overview of the building block model

Data source: IPART.

The Port Authority earns supplementary revenue from some of its assets, which is unrelated to cruise services. For example, it leases floor space at OPT to externally-managed restaurants and hires out facilities at White Bay and OPT (when not in use for cruise operations) for functions and events.

Allowance for a return OF assets

Operating and maintenance

expenditure

Allowance for taxation payments

Allowance for a return ON assets

Allowance for working capital

Not

iona

lrev

enue

requ

irem

ent

Tot

al e

ffici

ent c

osts

5 Estimating the revenue requirement

26 IPART Maximum fees and charges for cruise ships in Sydney Harbour

Consistent with other price reviews we conduct, we propose to deduct a proportion of this revenue from the revenue requirement in recognition that this revenue offsets some of the cost of holding assets used to service cruise operations. Our standard approach has been to deduct 50% of supplementary revenue, where assets in the asset base are being used to generate this revenue. This seeks to strike a balance between passing the benefits of this supplementary revenue to customers through lower prices, and providing the business with incentives to pursue opportunities to earn supplementary revenue from spare capacity.

IPART seeks comments on the following

4 Do you agree with our proposed approach to share supplementary revenue equally between the Port Authority and customers?

5.2 Using a 5-year review period

We propose to apply the building block model over a 5-year period, between 2016-17 and 2020-21. This means we could also recommend prices for this period.

There are advantages and disadvantages of longer and shorter review periods. For example, a longer review period would provide greater stability and predictability in site occupation prices. However, it would also involve increased risk associated with inaccuracies in the forecast data we used to recommend these prices, and the risk that changes in the industry will impact the effectiveness of our recommendations.

In our view, a 5-year period provides a reasonable balance between these competing factors, and is similar to the period we use in other industries.

IPART seeks comments on the following

5 Do you agree with our proposed review period of five years? If not, what period do you prefer and why?

5.3 Using separate building block models for the Port Authority’s different services and berthing facilities

We propose to estimate the efficient costs of providing all the Port Authority’s cruise ship services, and to use separate building block models for pilotage services, navigational services, and for services provided at each terminal and berthing facility. This is consistent with our terms of reference, which require that our recommendations reflect the efficient costs of providing existing cruise services, avoid cross-subsidies between these services, and have regard to total port costs and charges incurred by the cruise industry.

5 Estimating the revenue requirement

Maximum fees and charges for cruise ships in Sydney Harbour IPART 27

5.3.1 Separate building block models for pilotage and navigational services

Given that the assets involved in providing pilotage and navigational services are mostly discrete, we propose to use a separate building block model for each of these services. This will enable us to avoid including cross-subsidies in our recommended site occupation charges. It will also indicate the extent to which the current pilotage and navigational services charges are cost-reflective, and allow us to assess the impact of our recommendations on site occupation charges on the Port Authority’s overall cost recovery. Our ability to do this will depend on how accurately we can allocate these costs.

5.3.2 Separate building block models for the different terminals and berthing facilities

As Chapter 2 discussed, the assets used to provide the Port Authority’s cruise terminal and berthing services include the OPT, the White Bay Cruise Terminal and, to a lesser extent, berthing facilities at White Bay 4. White Bay 4 is not a dedicated passenger facility and is also used for other purposes.

In our view, using separate building block models for each terminal or berthing facility (or group of facilities) will enable us to recommend charges that better reflect the quality and quantity of services provided at each facility. This is consistent with the terms of reference, which ask us to consider whether there should be different charging schedules and arrangements for the use of different berthing facilities.

5.3.3 Charges for assets owned by other government entities

In general, our building block methodology takes account of all costs incurred to provide the relevant services. As Chapter 2 noted, RMS owns the channels and berthing boxes in Sydney Harbour that are used by the Port Authority to provide its services. The Port Authority pays a fee to RMS for use of the channel, which is 13.8% of its navigation revenue (excluding Maritime Security Charges and GST). This forms part of the Port Authority’s operating costs. We will consider the efficiency of the fees that the Port Authority pays to RMS as part of our review of efficient operating costs (see section 5.4).

5.4 Estimating the allowance for operating expenditure

The allowance for operating expenditure reflects our view of the efficient level of operating costs the Port Authority will incur in providing its cruise services over the review period. These costs include, among others, costs of labour, service contractors, utilities, maintenance and equipment.

5 Estimating the revenue requirement

28 IPART Maximum fees and charges for cruise ships in Sydney Harbour

We will estimate these costs based on detailed information provided by the Port Authority on its historical and projected operating and maintenance costs. This information will be separated by function – navigation, pilotage or cruise terminal and berthing facilities. Where costs are shared between functions, we propose to allocate them using our proposed methodology for allocating shared assets to the initial asset base (see section 4.6.1 below).

Only efficient costs will be included in the allowance for operating expenditure. Efficient costs may vary from the Port Authority’s actual costs in providing the service. Efficient costs represent what an efficient service provider would incur in providing the services at the quantity and level demanded by the industry, and subject to any external legislative requirements and regulatory standards over which the Port Authority has no control.

We propose to engage an external consultant to review the Port Authority’s actual and forecast costs and advise us on their efficiency. Some of the factors that we will ask the consultant to consider include:

the legislative requirements and regulatory standards associated with the provision of cruise ship services (eg, safety standards, OHS, award wage rates paid by the Port Authority)

benchmark costs of similar businesses where available

the quantity and level of cruise ship services and facilities, including whether there is need for spare or additional capacity.

We will ask the consultant to identify where any cost savings could be made through efficiency gains. We will take this advice into consideration when forming our judgement on the level of efficient operating costs to include in the building block models.

5.5 Estimating efficient capital expenditure

Under the building block method, there is no explicit allowance for capital expenditure in the notional revenue requirement. Instead, efficient capital expenditure is added to the asset base and recovered through the allowances for a return on assets and depreciation (discussed below).

To decide how much capital expenditure to add to the asset base in each year of the review period, we will review the Port Authority’s forecast capital expenditure and apply an efficiency test to this expenditure over the period. This test examines whether the forecast capital expenditure represents (over the life of the asset) the best way of meeting customers’ needs, subject to meeting any regulatory requirements. We propose to engage a consultant to assist us in applying the test.

5 Estimating the revenue requirement

Maximum fees and charges for cruise ships in Sydney Harbour IPART 29

We will incorporate efficient capital expenditure into the value of the asset base, and then use this value in calculating the allowances for a return on assets and depreciation.

5.6 Estimating the allowance for a return on assets

The allowance for return on assets represents the cost of capital invested in a benchmark efficient business through equity and debt investments. Including a return on assets ensures that efficient investment in infrastructure continues into the future to meet growth in demand and maintain the business’ long-term viability. In capital-intensive businesses like the Port Authority’s, this allowance typically represents a large proportion of the total revenue requirement.

To estimate the allowance for a return on assets, we propose to:

determine the value of the initial asset base

decide on an appropriate rate of return, and

multiply the value of the asset base by the rate of return.

5.6.1 Valuing the initial asset base

The asset base refers to the value of a business’ assets used to provide the relevant services, which are funded by shareholders.16 The asset base is valued in real terms and adjusted for CPI annually. Once the value of the initial asset base is established, this value is ‘rolled forward’ at the end of each year in a price setting period. That is, it is adjusted to reflect capital expenditure, asset disposals, depreciation and CPI over the year.

As this is the first time we are applying a building block model to the Port Authority’s cruise ship services, we need to determine an initial asset base for the Port Authority’s for each of these services.

The primary assets associated with providing the services include land, buildings, furniture at terminals, roadways, bridges, wharves, jetties, pilot cutters and breakwaters, plant and intangibles such as software, etc. The Port Authority engages external experts to update the value of its assets every three to five years, depending on the asset.

We propose to review the Port Authority’s asset valuations and consider a number of other valuation techniques, depending on whether the asset is land or any other asset class. We also propose to allocate shared assets between cruise and non-cruise services.

16 In this instance the NSW Treasurer and NSW Minister for Finance and Services are equal

shareholders.

5 Estimating the revenue requirement

30 IPART Maximum fees and charges for cruise ships in Sydney Harbour

Valuing the Port Authority’s land assets

The land on which the terminals and other assets are built is a valuable asset and the Port Authority is entitled to a reasonable return. When considering the value of land for the initial asset base, we will review the Port Authority’s valuations and the Valuer General’s methodology for determining land values as outlined in the Valuation of Land Act 1916 (NSW). We also propose to consider valuations for surrounding sites with different zoning, such as residential, to develop a measure of the opportunity cost of the land used for providing cruise ship services.

The Port Authority values land at current market prices for existing use. This is done on a direct comparison basis with some adjustments to reflect differences between the parcel of land in question and comparable properties. Where land is restricted in the nature of its use by zoning, as is the case for land around the Glebe Island and White Bay precincts, a discount is applied.

The Valuer General’s methodology for land valuation takes into account:

the location of the land

soil type and land surface (such as slope)

town planning controls and constraints on use (such as heritage restrictions and Crown lease restrictions)

land size and shape, and

nearby development and amenities (such as parks, views, public transport and main roads).

This methodology requires that land be valued in relation to its highest and best permitted use. In most cases, this is based on the current zoning and planning restrictions.17 Generally, restrictions over the use of land (eg, due to terrain, heritage listing, Crown lease restrictions, etc), will lower its value. Valuations of land do not take into account the value of buildings or structures on the land, or other improvements. However, land improvements, such as the reclamation of land by draining or filling, are included in the valuation.

IPART seeks comments on the following

6 Should land at terminals and berthing precincts be valued based on existing use or most valuable use?

Valuing the Port Authority’s non-land assets

We will review the Port Authority’s valuations of all non-land assets, including buildings, roads, wharves and jetties. The Port Authority values buildings at current market prices for existing use, and land based on its existing use. Roads, wharves and jetties are valued at depreciated replacement costs.

17 NSW Government, Valuation of Land Act 1916, section 6A(1).

5 Estimating the revenue requirement

Maximum fees and charges for cruise ships in Sydney Harbour IPART 31

We propose to also consider the following valuation methods:

Optimised replacement cost method values the asset at the cost of replacing it with a modern equivalent available asset. This method removes excess capacity through ‘optimisation’ and values the asset based on the most efficient way to deliver the required services.

Depreciated optimised replacement cost (DORC) method recognises limited remaining life of the existing asset and depreciates the optimised replacement cost to reflect the current, partly worn-out state and limited service potential of the existing assets.

Depreciated historic/actual cost method values the asset at the cost at which they were originally purchased and applies appropriate deductions for accumulated depreciation.

Allocating shared assets between cruise and non-cruise segments

We are interested in the efficient costs of providing cruise ship services, as opposed to services provided to non-cruise commercial operators. Where assets are utilised by both cruise and commercial operators we will need to consider how to allocate the value of these shared assets to the cruise sector. This is relevant for both pilotage and navigation building blocks, and terminals which service both cruise passengers and non-cruise commercial vessels (eg, White Bay 4).

Figure 5.2 below outlines the process we will use to do this.

Figure 5.2 Allocating assets to cruise and non-cruise services

5 Estimating the revenue requirement

32 IPART Maximum fees and charges for cruise ships in Sydney Harbour

This approach takes into account the reality of the Port Authority’s business, which incorporates both cruise and commercial operations. There are economies of scale in catering for both segments – that is, it costs less to use the same assets to service both segments, than to build separate assets to service each individually. Both segments benefit from this shared cost arrangement. If we considered the value of assets used to service the cruise segment as a stand-alone business, it is likely that building block costs would be much higher and the Port Authority may over-recover its actual costs, given the existing charges for commercial operators.

IPART seeks comments on the following

7 Do you agree with our proposed approach to valuing the initial asset base and allocating shared assets? Are there other approaches or issues we should consider?

5.6.2 Deciding on the appropriate rate of return

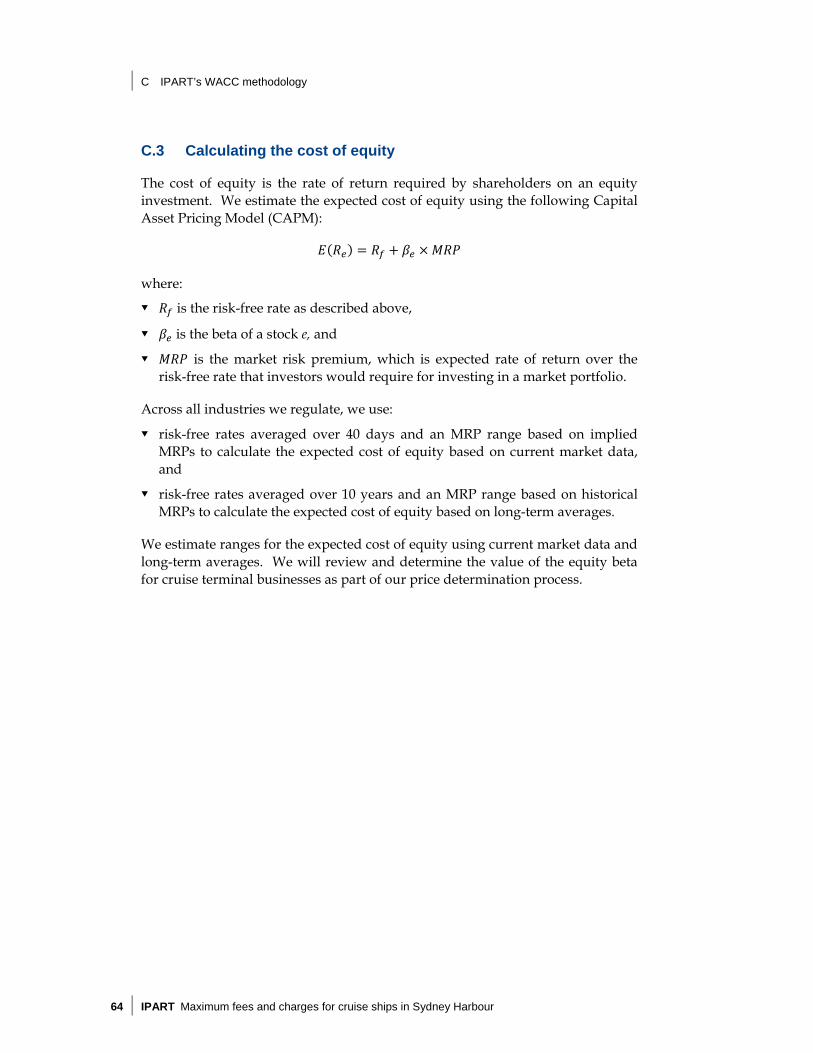

We propose to decide on the appropriate rate of return by using our standard weighted average cost of capital (WACC) methodology. The parameters underlying the WACC calculation can be grouped into two categories:

Market-based parameters, which include risk-free rate, debt margin, inflation rate and MRP. These parameters are common to businesses in all industries.

Industry-specific parameters, which include equity beta and gearing ratio. These parameters are specific to the business’ particular industry.

Estimating the market-based parameters

Risk-free rate

The risk-free rate is used as a point of reference in determining both the cost of equity and the cost of debt within the WACC. It is used as a base rate to which an equity or debt risk premium is added to reflect the riskiness of the specific business for which the rate of return is being derived.

In line with our current WACC methodology, we will estimate the risk-free rate as:

The 40-day average of the 10-year Commonwealth Government Security yields published by Bloomberg. This will be used to estimate the cost of debt and cost of equity using current market data.

The 10-year average of the 10-year Commonwealth Government Security yields published by Bloomberg. This will be used to estimate the cost of debt and cost of equity using long-term averages.

5 Estimating the revenue requirement

Maximum fees and charges for cruise ships in Sydney Harbour IPART 33

Debt margin

The debt margin represents the cost of debt a company has to pay above the nominal risk-free rate. Following our current WACC methodology, we will estimate the debt margin as:

The two-month average18 of the RBA’s monthly estimates of the credit spreads for 10-year corporate bonds rated as BBB. This is used to estimate the cost of debt using current market data.

The 10-year average of the RBA’s monthly estimates of the credit spreads for 10-year corporate bonds rated as BBB. This is used to estimate the cost of debt and cost of equity using long-term averages.

Inflation rate

The inflation rate is used to convert the nominal post-tax WACC into a real post-tax WACC. For this parameter we will use a 10-year geometric average of the 1-year RBA inflation forecast and the middle of the RBA’s target band of inflation (currently at 2.5%) for the remaining nine years.

Market risk premium

The market risk premium (MRP) is the expected rate of return over the risk-free rate that investors would require for investing in a market portfolio. The MRP is an expected return and is not directly observable. Therefore, it needs to be estimated through proxies. In line with our current WACC methodology, we will use both current market data and long-term averages. For the:

current market data we will establish an MRP range using our six MRP methodologies to estimate the cost of equity, and

long-term averages we will use an MRP range of 5.5% to 6.5% with a midpoint of 6.0%, based on the historical arithmetic average of the excess market return over the risk-free rate, to estimate the cost of equity.

Estimating the industry-specific parameters

Equity beta

The equity beta measures the extent to which the return of a particular security varies in line with the overall return of the market. It represents the systematic risk of a security that cannot be avoided by holding it as part of a diversified portfolio. The equity beta does not take into account business-specific or diversifiable risks.

18 This is as an approximation for the 40-day average.

5 Estimating the revenue requirement

34 IPART Maximum fees and charges for cruise ships in Sydney Harbour

In each price review we conduct, we determine the value of the equity beta for the relevant business. We do this by estimating the equity betas of (listed) comparable firms, and considering the equity betas that other regulators have applied to comparable businesses.

Subject to data availability, we propose to estimate equity betas for listed international ports that provide similar services to the Port Authority. This will most likely include businesses that provide mixed services to cruise and commercial ships, such as ships anchoring services, handling cargo, loading and unloading passengers, goods storage and car transportation services. This is because it may be difficult to isolate a suitable number of comparable businesses that earn revenues from cruise ship services only.

We will also consider equity betas for international airports. There are some similarities between airports and seaports in that they both provide passenger terminal services, handle cargo, and earn revenues from leasing of food and beverage spaces and retail spaces. There are likely to be many more listed airports than seaports, and this will allow more robust estimation of equity beta.

Lastly, we will consider regulatory decisions on the equity beta for ports and airports in other jurisdictions. For example, we will look at decisions made by the Essential Services Commission, which is responsible for regulating ports in Victoria; Civil Aviation Authority of UK, which regulates charges for various airports in the UK; and the New Zealand Commerce Commission, which determines the appropriate equity beta for Wellington International Airport.

Gearing ratio

The gearing ratio is the proportion of debt to total assets in the business’ capital structure. Regulators commonly adopt a benchmark capital structure rather than the actual capital structure of the regulated entity, to ensure that customers will not bear the costs associated with an inefficient capital structure.

Similar to our proposed approach for determining the equity beta, we propose to estimate the gearing ratio by considering:

gearing ratios of listed international ports

gearing ratios of listed international airports, and

past regulatory decisions on the gearing ratio for ports and airports.