ISSUES FOR AMEDA DEPOSITORIES IN MANAGING RISK IN THE CURRENT ENVIRONMENT April 2010.

17

ISSUES FOR AMEDA DEPOSITORIES IN MANAGING RISK IN THE CURRENT ENVIRONMENT April 2010

-

date post

22-Dec-2015 -

Category

Documents

-

view

218 -

download

4

Transcript of ISSUES FOR AMEDA DEPOSITORIES IN MANAGING RISK IN THE CURRENT ENVIRONMENT April 2010.

ISSUES FOR AMEDA DEPOSITORIES IN MANAGING RISK IN THE CURRENT

ENVIRONMENT

April 2010

© 2010 Thomas Murray Ltd.Page 2 PRIVATE AND CONFIDENTIAL

Agenda

TM Depository Risk Definitions & Country Categories

Risk Comparisons: AMEDA vs Rest of the World with Key Issues

© 2010 Thomas Murray Ltd.Page 3 PRIVATE AND CONFIDENTIAL

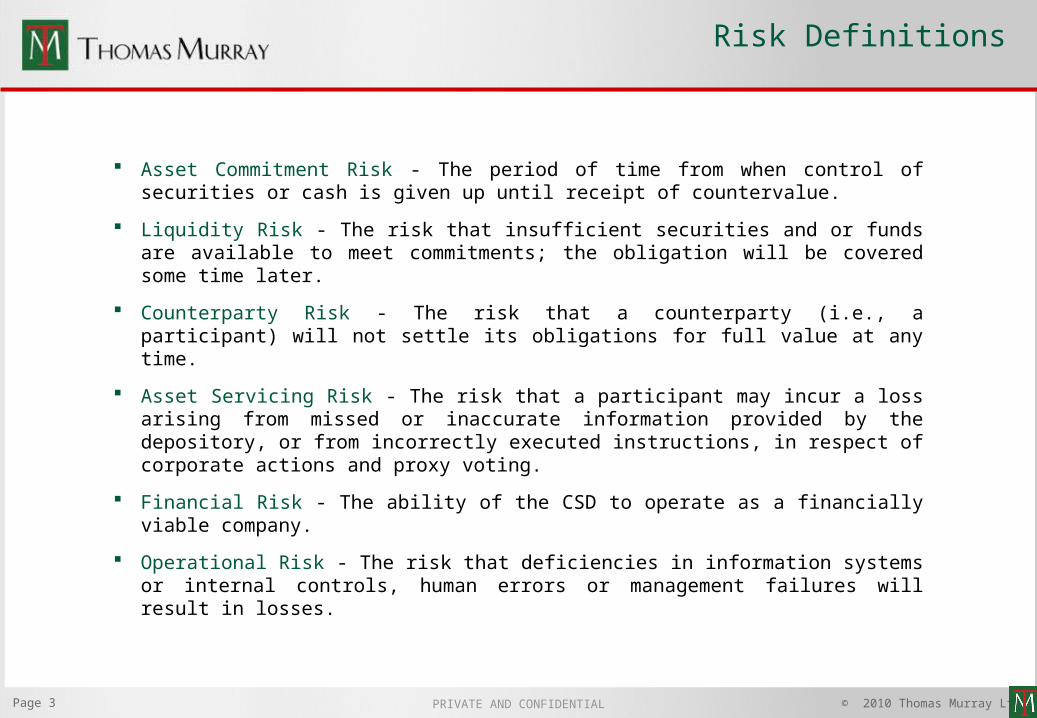

Risk Definitions

Asset Commitment Risk - The period of time from when control of securities or cash is given up until receipt of countervalue.

Liquidity Risk - The risk that insufficient securities and or funds are available to meet commitments; the obligation will be covered some time later.

Counterparty Risk - The risk that a counterparty (i.e., a participant) will not settle its obligations for full value at any time.

Asset Servicing Risk - The risk that a participant may incur a loss arising from missed or inaccurate information provided by the depository, or from incorrectly executed instructions, in respect of corporate actions and proxy voting.

Financial Risk - The ability of the CSD to operate as a financially viable company.

Operational Risk - The risk that deficiencies in information systems or internal controls, human errors or management failures will result in losses.

© 2010 Thomas Murray Ltd.Page 4 PRIVATE AND CONFIDENTIAL

Country Categories

Middle East Countries and CSDs Bahrain – CDS Egypt – MCDR Israel – TASECH Jordan – SDC Kuwait – KCC Lebanon – Midclear Morocco – Maroclear Oman – MDSRC Palestine – CDS Qatar – Qatar Exchange Saudi Arabia – Tadawul Tunisia – Sticodevam UAE – DFM UAE Nasdaq Dubai

Additional CSDs in Country Average Lebanon – CBL

African Countries and CSDs Kenya – CDSC Mauritius – CDS Nigeria – CSCS South Africa – Strate

Additional CSDs in Country Average Kenya – CBK Mauritius – BOM West Africa – DCBR Zambia – LuSE Zambia – BoZ

AMEDA CSDs Under preparation Ghana – GSD UAE - ADX

© 2010 Thomas Murray Ltd.Page 5 PRIVATE AND CONFIDENTIAL

Overall Risk

Average Rating - ACSDAAverage Rating – EU/EEAAverage Rating – Eurasia

Average Rating – Asia PacificAverage Rating – AfricaAverage Rating – Middle East

Key Issues What is the role of market infrastructure, and CSDs in

particular in protecting investors against the next Lehmans or Madoff?

What lessons have been learnt from the financial crisis?

If market infrastructure is to take on more responsibility for asset protection, should their business model change?

Key Variants: AMEDA vs ROW Some AMEDA markets are still in the emerging zone

and are yet to adopt the more recent standards of best market practice

Overall systems and approach to risk mitigation is less sophisticated than in developed markets

However, most CSDs weathered the global financial storm well both from a revenue and a risk perspective

AAA

AA+

AA

AA-

A+

A

A-

BBB

BB

B

CCC

CC

C

Rating

© 2010 Thomas Murray Ltd.Page 6 PRIVATE AND CONFIDENTIAL

Asset Commitment Risk

Key Issues RTGS (normally with optimisation cycles) is now

common in developed market settlement systems

Often combined with overnight and or daytime batch routines to maximise liquidity efficiency

This flexibility gives participants the choice of optimising liquidity or asset availability

Key Variants: AMEDA vs ROW Still a prevalence exists for batch processing rather

than real time processing

Most central banks are using RTGS but not linked real time to SSS (8 CSDs have linkage)

Significant blocking or prefunding in contrast to other regions.(10 CSDs block securities on Trade Date)

AAA

AA+

AA

AA-

A+

A

A-

BBB

BB

B

CCC

CC

C

Rating

Average Rating - ACSDAAverage Rating – EU/EEAAverage Rating – Eurasia

Average Rating – Asia PacificAverage Rating – AfricaAverage Rating – Middle East

© 2010 Thomas Murray Ltd.Page 7 PRIVATE AND CONFIDENTIAL

Liquidity Risk

AAA

AA+

AA

AA-

A+

A

A-

BBB

BB

B

CCC

CC

C

Rating

Key Issues Pressure on liquidity has intensified, and margin and

collateral requirements may have tightened. Has this been an issue for AMEDA markets?

Widespread bans or restrictions on short selling

Tightening of credit leads to higher funding costs

Key Variants: AMEDA vs ROW No AMEDA markets banned short selling (mainly

Europe & AP)

Some AMEDA markets lack developed fails management processes

Some AMEDA markets lack a critical mass of issued securities under custody leaving a significant proportion of the market physical

Some restrictions on credit facilities for foreign investors and the lack of a developed interbank lending market

Average Rating - ACSDAAverage Rating – EU/EEAAverage Rating – Eurasia

Average Rating – Asia PacificAverage Rating – AfricaAverage Rating – Middle East

© 2010 Thomas Murray Ltd.Page 8 PRIVATE AND CONFIDENTIAL

0

5

10

15

20

25

30

35

Asia Pacif ic Americas Europe Africa Middle East Eurasia

Region

Nu

mb

er o

f co

un

trie

s

Ban in place

Ban removed

No Ban applied

Not practised

Short Selling Bans By Region

CSDs & the Global Financial Crisis

© 2010 Thomas Murray Ltd.Page 9 PRIVATE AND CONFIDENTIAL

Counterparty Risk

AAA

AA+

AA

AA-

A+

A

A-

BBB

BB

B

CCC

CC

C

Rating

Key Issues Counterparty Risk is now back on top of the agenda for

institutional investors

How do CSDs that commingle CSD and CCP roles in the same legal entity manage to ring-fence the CCP risk?

How have risk models been adapted since the global financial crisis? Has surveillance been improved? Has stress-testing been developed?

Key Variants: AMEDA vs ROW Few CCPs exist in the region (3) in contrast to Europe.

Most AMEDA markets have a guarantee fund in place

Still a lack of true DVP especially for off-market/ client-side settlement in some AMEDA markets

Real-time monitoring of participants’ exposures (and their collateralisation) is uncommon in AMEDA markets

Stress testing is rare.Average Rating - ACSDAAverage Rating – EU/EEAAverage Rating – Eurasia

Average Rating – Asia PacificAverage Rating – AfricaAverage Rating – Middle East

© 2010 Thomas Murray Ltd.Page 10 PRIVATE AND CONFIDENTIAL

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

Uni

ted

Arab

Emira

tes

Saud

i Ara

bia

Nig

eria

Pale

stin

e

Egyp

t

Isra

el

Om

an

Jord

an

Qat

ar

Tuni

sia

Bahr

ain

Kuw

ait

Leba

non

Keny

a

Mor

occo

Region

Num

ber o

f cou

ntrie

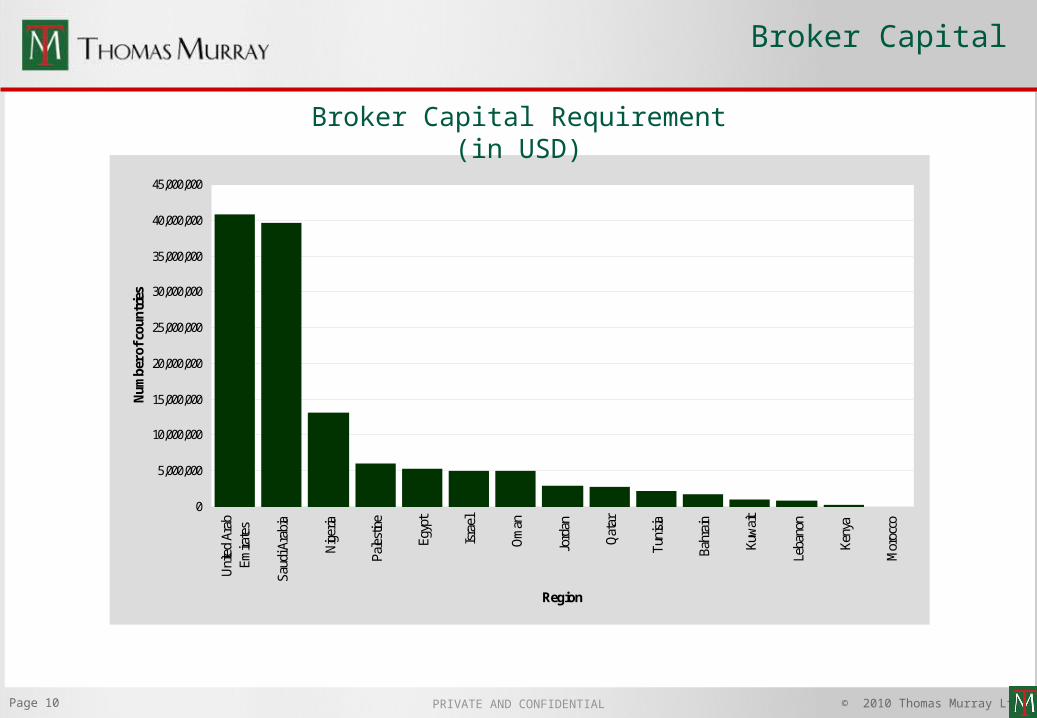

sBroker Capital Requirement (in USD)

Broker Capital

© 2010 Thomas Murray Ltd.Page 11 PRIVATE AND CONFIDENTIAL

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

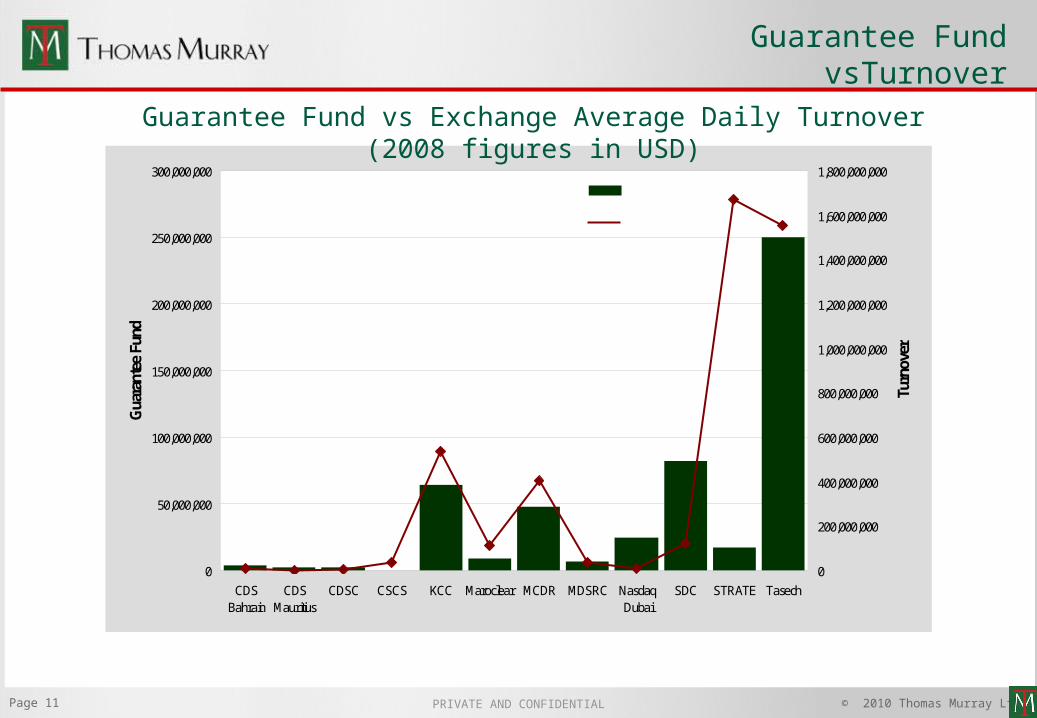

CDSBahrain

CDSMauritius

CDSC CSCS KCC Maroclear MCDR MDSRC NasdaqDubai

SDC STRATE Tasech

Gua

rant

ee F

und

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1,800,000,000

Turn

over

Guarantee Fund

Turnover

Guarantee Fund vs Exchange Average Daily Turnover (2008 figures in USD)

Guarantee Fund vsTurnover

© 2010 Thomas Murray Ltd.Page 12 PRIVATE AND CONFIDENTIAL

Asset Servicing Risk

Average Rating - ACSDAAverage Rating – EU/EEAAverage Rating – Eurasia

Average Rating – Asia PacificAverage Rating – AfricaAverage Rating – Middle East

AAA

AA+

AA

AA-

A+

A

A-

BBB

BB

B

CCC

CC

C

Rating

Key Issues An expanding business sector for CSDs - gaining

ground on custodians

Does the removal of commercial banking capital from asset servicing disadvantage market participants and investors?

How have markets ‘de-risked’ corporate actions processing?

Key Variants: AMEDA vs ROW Not all AMEDA members are involved in Asset

Servicing to a degree that they are taking on risk exposure

Where AMEDA members are engaged in Asset Servicing, some have relatively low capital backing this business

Few AMEDA members have moved up the value chain enough to threaten to compete with their participants (Only one offers proxy voting)

© 2010 Thomas Murray Ltd.Page 13 PRIVATE AND CONFIDENTIAL

CSD Role in Corporate Actions

CSD Participation In Corporate Actions(As at July 2009)

0

5

10

15

20

25

30

35

Asia Pacific Americas W. Europe (incl.EU)

Africa Middle East Eurasia

Region

Nu

mb

er o

f co

un

trie

s

Not Involved in CAs

Only Mandatory Cas

Involved in CAs

© 2010 Thomas Murray Ltd.Page 14 PRIVATE AND CONFIDENTIAL

Financial Risk

Average Rating - ACSDAAverage Rating – EU/EEAAverage Rating – Eurasia

Average Rating – Asia PacificAverage Rating – AfricaAverage Rating – Middle East

AAA

AA+

AA

AA-

A+

A

A-

BBB

BB

B

CCC

CC

C

Rating

Key Issues Adequacy of financial resources was a key concern

during the recent financial crisis

Many CSDs’ profit margins slumped in 2008/9. How have CSDs responded in the short and medium-term?

How have business models adapted to the crisis and what lessons have been learnt?

Key Variants: AMEDA vs ROW Massive diversity in financial resources amongst

AMEDA members

AMEDA members’ profit margins not as hard-hit as ECSDA and ACG

Still, few AMEDA members have real diversity in revenue streams

Some independent CSDs in the region susceptible to horizontal or vertical consolidation

© 2010 Thomas Murray Ltd.Page 15 PRIVATE AND CONFIDENTIAL

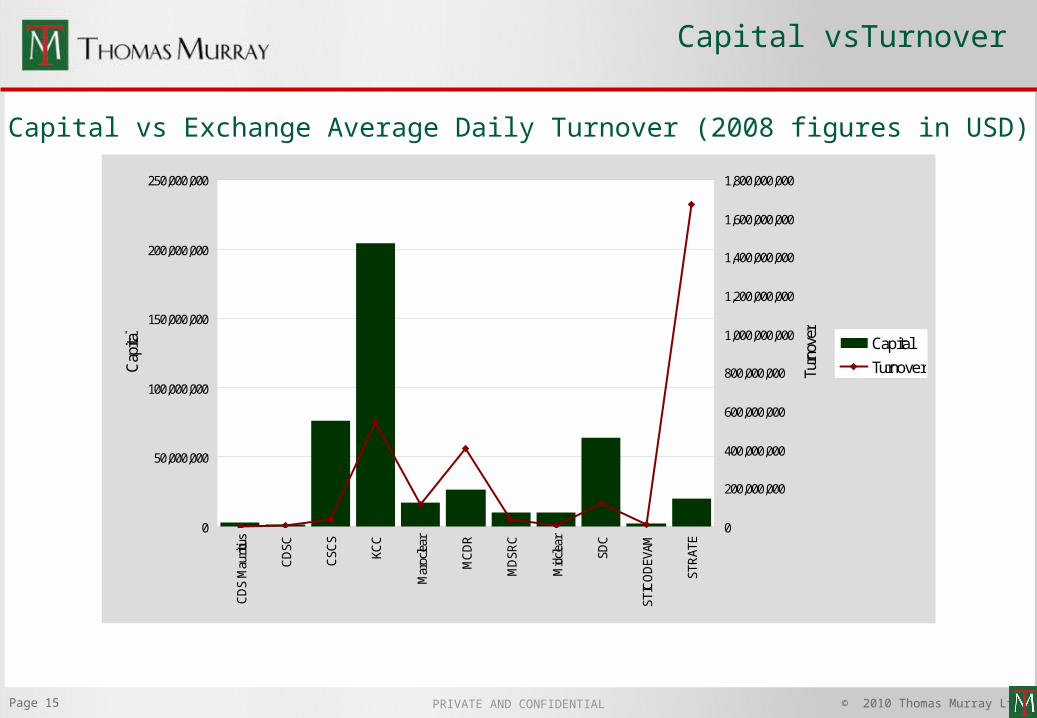

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

CD

S M

aurit

ius

CD

SC

CSC

S

KCC

Mar

ocle

ar

MC

DR

MD

SRC

Mid

clear

SDC

STIC

OD

EVAM

STR

ATE

Cap

ital

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1,800,000,000

Turn

over Capital

Turnover

Capital vs Exchange Average Daily Turnover (2008 figures in USD)

Capital vsTurnover

© 2010 Thomas Murray Ltd.Page 16 PRIVATE AND CONFIDENTIAL

0

50,000,000

100,000,000

150,000,000

200,000,000

CDSMauritius

CDSC CSCS KCC Maroclear MCDR MDSRC Midclear SDC STRATE

Capital

Net Profit

Capital vs Profit of CSDs (2008 figures in USD)

Capital vs Profit

© 2010 Thomas Murray Ltd.Page 17 PRIVATE AND CONFIDENTIAL

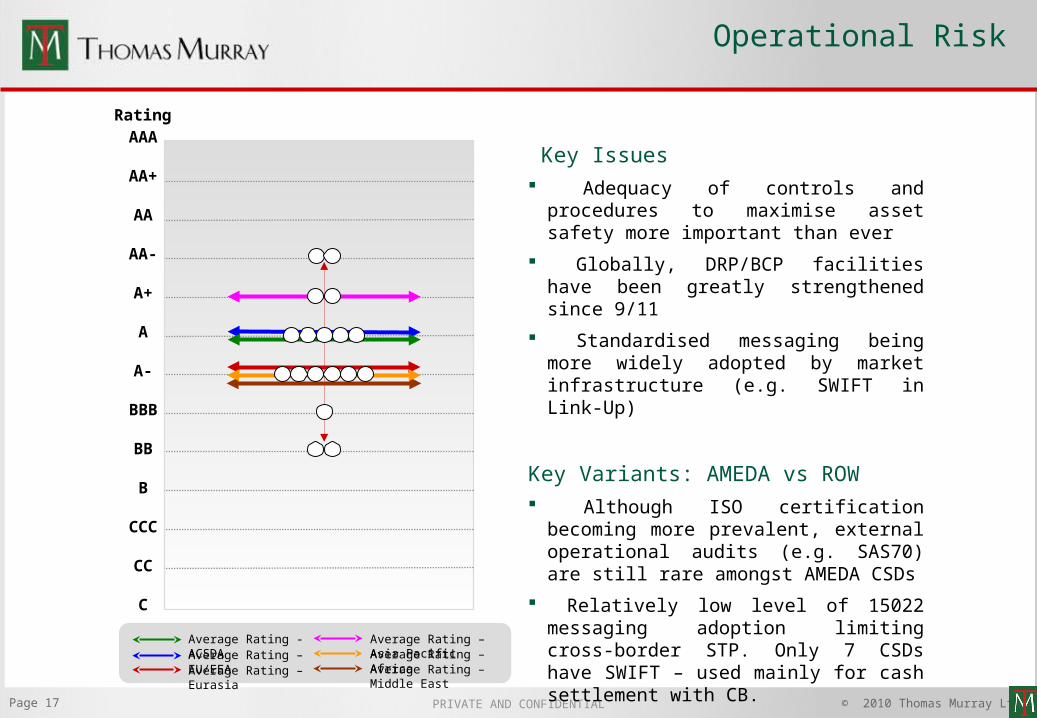

Operational Risk

Average Rating - ACSDAAverage Rating – EU/EEAAverage Rating – Eurasia

Average Rating – Asia PacificAverage Rating – AfricaAverage Rating – Middle East

AAA

AA+

AA

AA-

A+

A

A-

BBB

BB

B

CCC

CC

C

Rating

Key Issues Adequacy of controls and procedures to maximise

asset safety more important than ever

Globally, DRP/BCP facilities have been greatly strengthened since 9/11

Standardised messaging being more widely adopted by market infrastructure (e.g. SWIFT in Link-Up)

Key Variants: AMEDA vs ROW Although ISO certification becoming more prevalent,

external operational audits (e.g. SAS70) are still rare amongst AMEDA CSDs

Relatively low level of 15022 messaging adoption limiting cross-border STP. Only 7 CSDs have SWIFT – used mainly for cash settlement with CB.

DRP/BCP strategies in some markets still need further development.