Innovation & Commercialization Yigal Erlich Yozma Genève, April 2013.

Upload

jarvis-smallsCategory

view

227download

0

ISRAEL CREATIVE ECO-SYSTEM

Yigal ErlichYOZMA

September 2014

In tro d u c tio n

Yigal Erlich

• Former Chief Scientist of Israel’s Ministry of Industry, Trade and Labor

• Established the Technological Incubators Industry in Israel

• Founder & Manager of Israel’s anchor VC, Yozma

• Seed investor & active board member in technological startups such as

Biosense (acquired by J&J for $430M); Conduit (value: $1.35B) and Radiancy

(traded in Nasdaq with market cap of $340M).

•Chairman of Hadasit, TTO of Hadassah hospital; HBL – traded on TASE.

•Consultant to governments and VC on Private Public Partnerships and

investments (Russia, EEC, Canada, Portugal, New Zealand, Greece..).

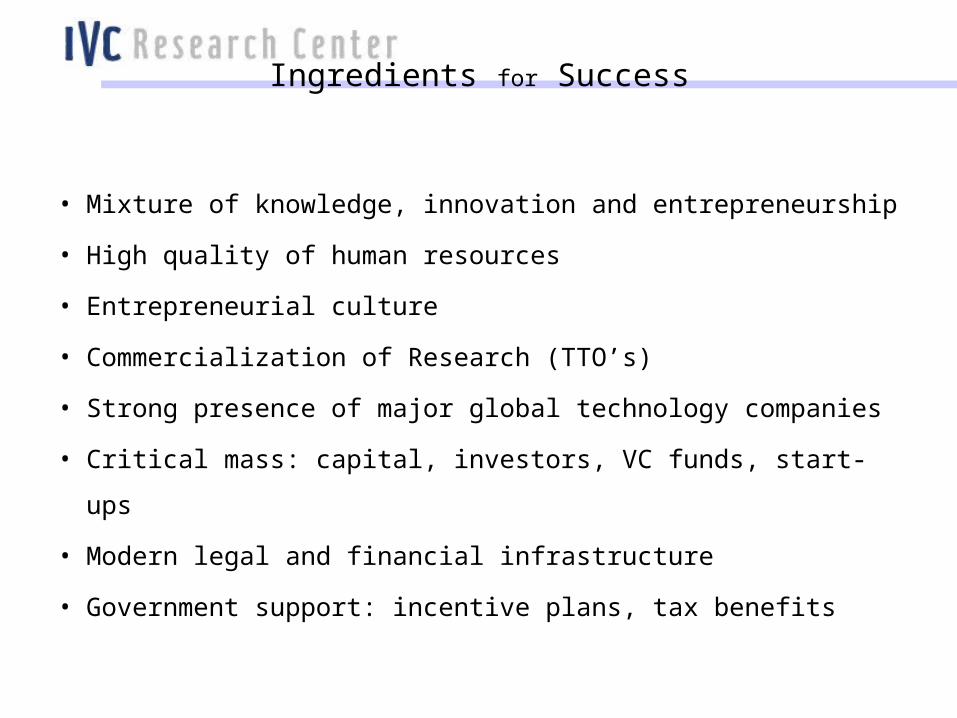

Ingredients for Success

• Mixture of knowledge, innovation and entrepreneurship

• High quality of human resources

• Entrepreneurial culture

• Commercialization of Research (TTO’s)

• Strong presence of major global technology companies

• Critical mass: capital, investors, VC funds, start-ups

• Modern legal and financial infrastructure

• Government support: incentive plans, tax benefits

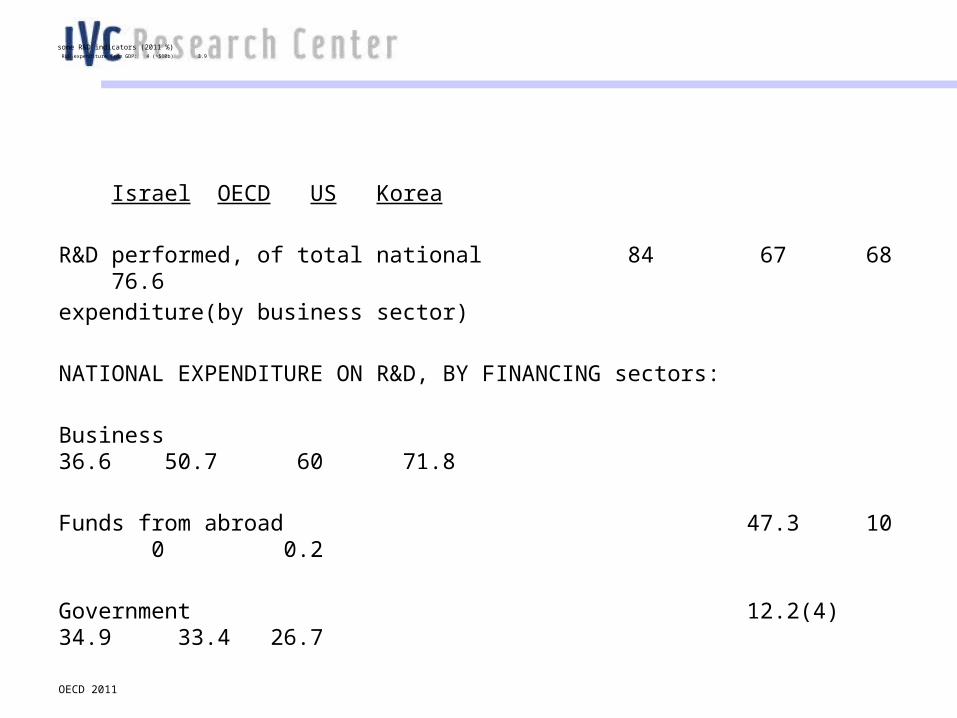

some R&D indicators (2011 %)R&D expenditure from GDP: 4 (~$10b) 3.9

Israel OECD US Korea

R&D performed, of total national 84 67 68 76.6expenditure(by business sector)

NATIONAL EXPENDITURE ON R&D, BY FINANCING sectors:

Business 36.6 50.7 60 71.8

Funds from abroad 47.3 10 0 0.2

Government 12.2(4) 34.9 33.4 26.7

OECD 2011

Israel VC “DNA” – Drivers of Entrepreneurship and Innovation

Forward

Informal

Creative

Ambitious

Non-Conventional

Communicative

Improvisation

Innovative

Experimental

Independent-thinking

“Chutzpah”

Going global from inception

Must-win attitude, Tolerance of failure

Question everything, Knock on any door

Using limited resources cost effectively

Solution-driven approach to real problems

Short history – past is not a constraint

Vision

IntegrityPersonal Example

Courage Out of the box

Capable

Persistent

Hard Working

Team

Family

Challenging

Action Driven

EducationCompetitive

Friendship

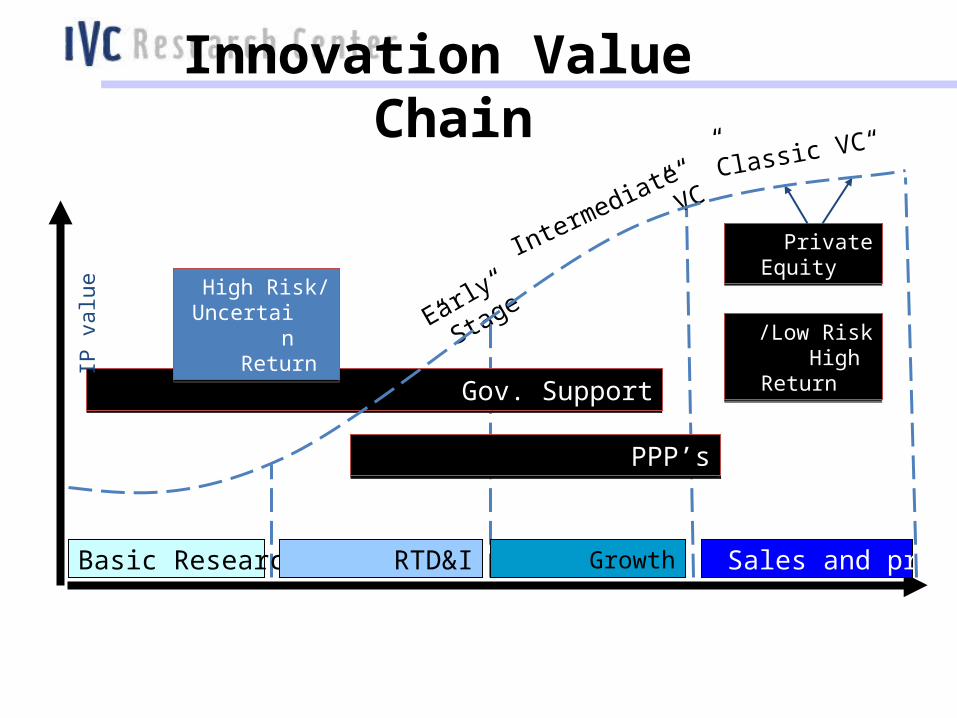

Innovation Value Chain

Basic Research RTD&I Growth Sales and profit

Gov. SupportGov. Support

PPP’sPPP’s

High Risk/ Uncertain

Return

High Risk/ Uncertain

Return Low Risk/ High Return

Low Risk/ High Return

Private EquityPrivate Equity

“

Early Stage

”

“

Intermediate VC

”

“Classic VC

”

IP v

alue

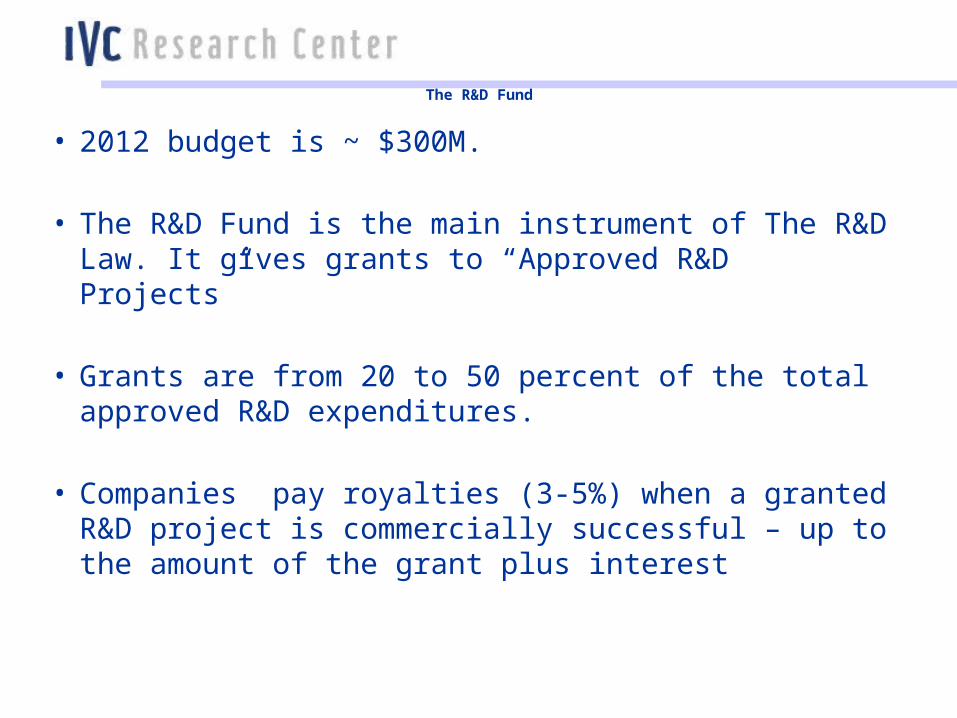

The R&D Fund

• 2012 budget is ~ $300M.

• The R&D Fund is the main instrument of The R&D Law. It gives grants to “Approved R&D Projects”

• Grants are from 20 to 50 percent of the total

approved R&D expenditures.

• Companies pay royalties (3-5%) when a granted R&D project is commercially successful – up to the amount of the grant plus interest

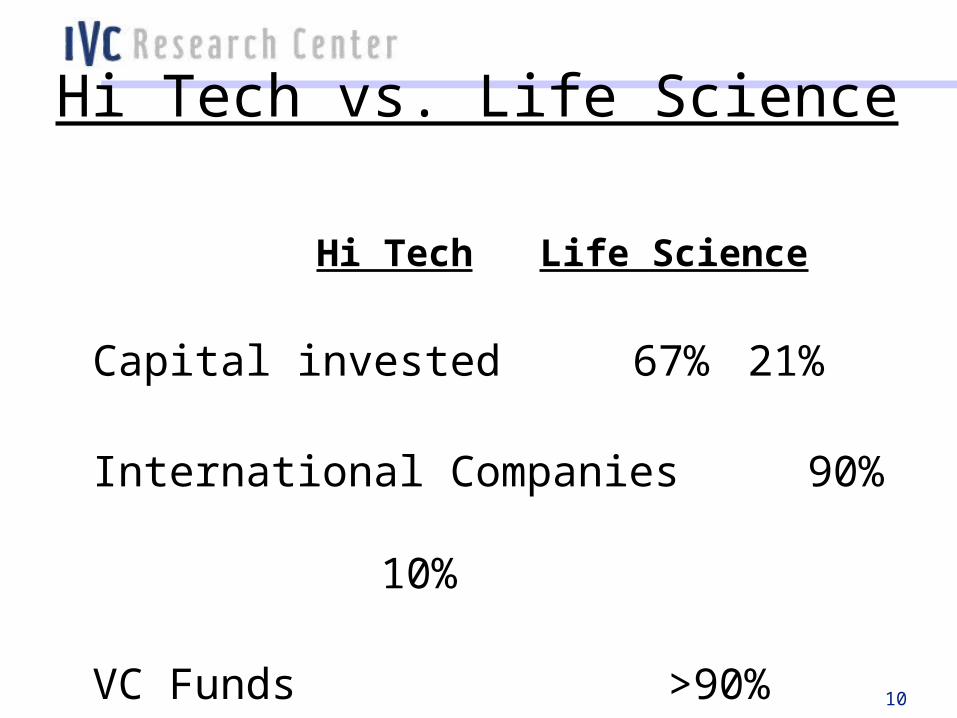

Hi Tech vs. Life Science

Hi Tech Life Science

Capital invested 67% 21%

International Companies 90% 10%

VC Funds >90% <10%

10

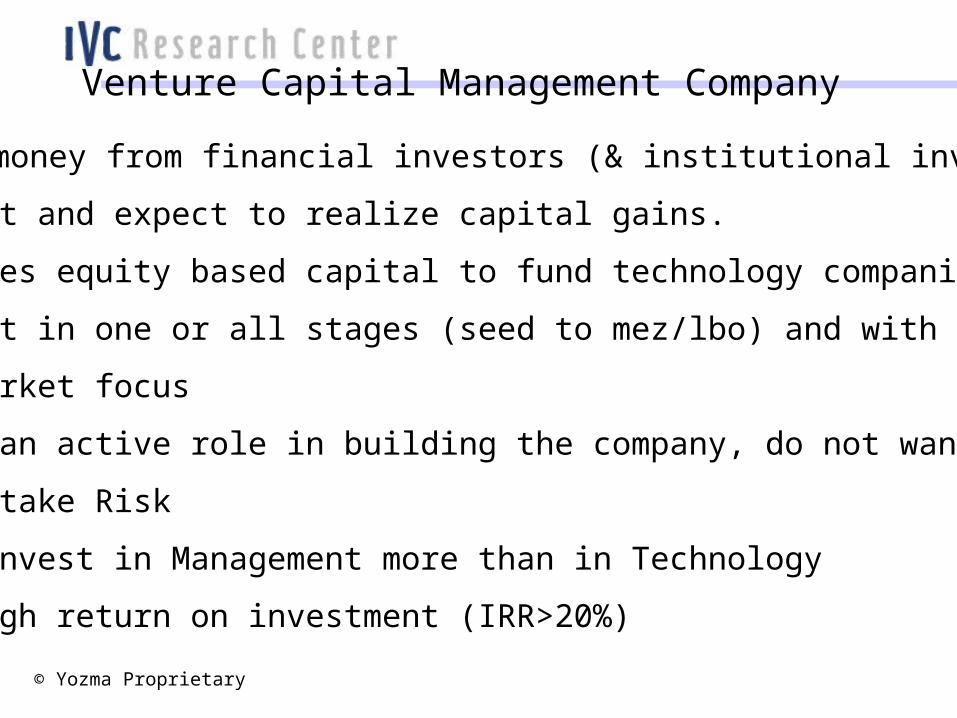

Venture Capital Management Company

•VC raises money from financial investors (& institutional investors)

Invest it and expect to realize capital gains.

• VC provides equity based capital to fund technology companies.

• VCs invest in one or all stages (seed to mez/lbo) and with or without

tech./market focus

• VCs take an active role in building the company, do not want to control

• Ready to take Risk

• Seek to invest in Management more than in Technology

• Expect high return on investment (IRR>20%)

© Yozma Proprietary

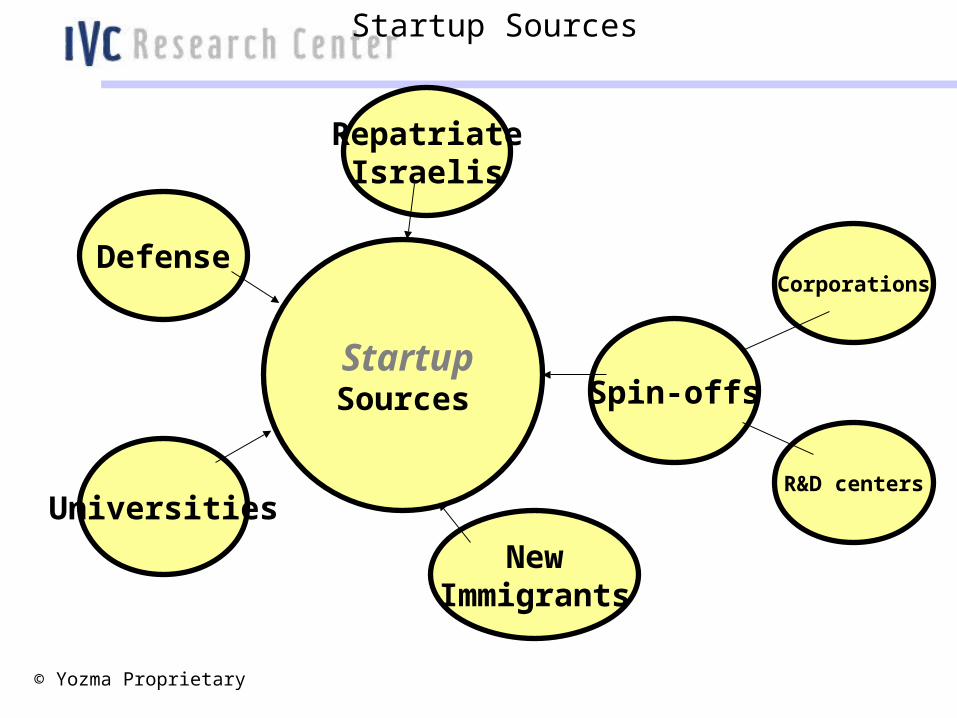

StartupSources

NewImmigrants

RepatriateIsraelis

Defense

Universities

Spin-offs

Corporations

R&D centers

Startup Sources

© Yozma Proprietary

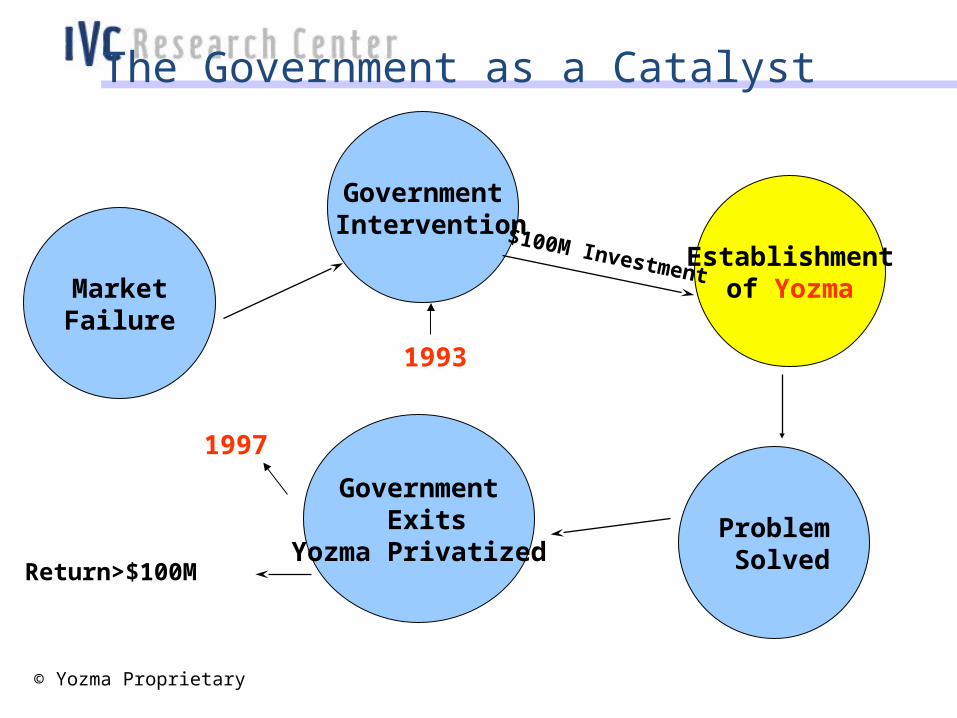

Yozma I Venture Capital (1993-98)

Mission: •To create a venture capital market in Israel

Policy: •Establish a $100M Government investment company.•Create professionally managed Funds.•Entice VC investments in Israeli early stage companies: (i) create and invest in new VC funds together with

experienced partners (from abroad).(ii) make direct investments in startup companies together with professional investors.

© Yozma Proprietary

The Government as a Catalyst

Return>$100M

MarketFailure

Government Intervention

Establishmentof Yozma

Problem Solved

Government Exits

Yozma Privatized

$100M Investment

1993

1997

© Yozma Proprietary

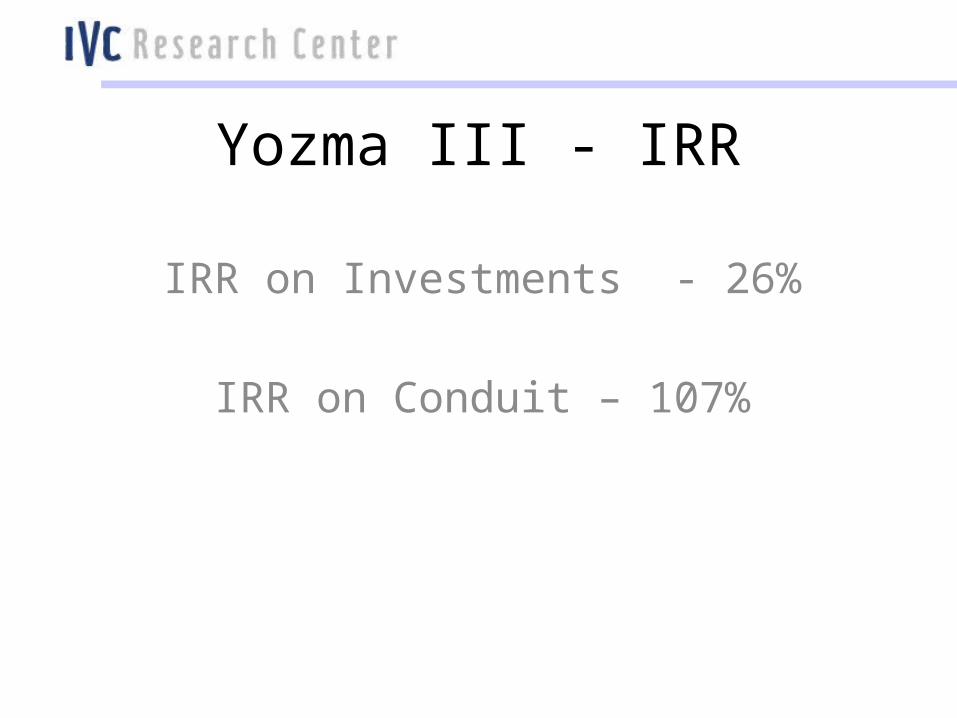

Yozma III - IRR

IRR on Investments - 26%

IRR on Conduit – 107%

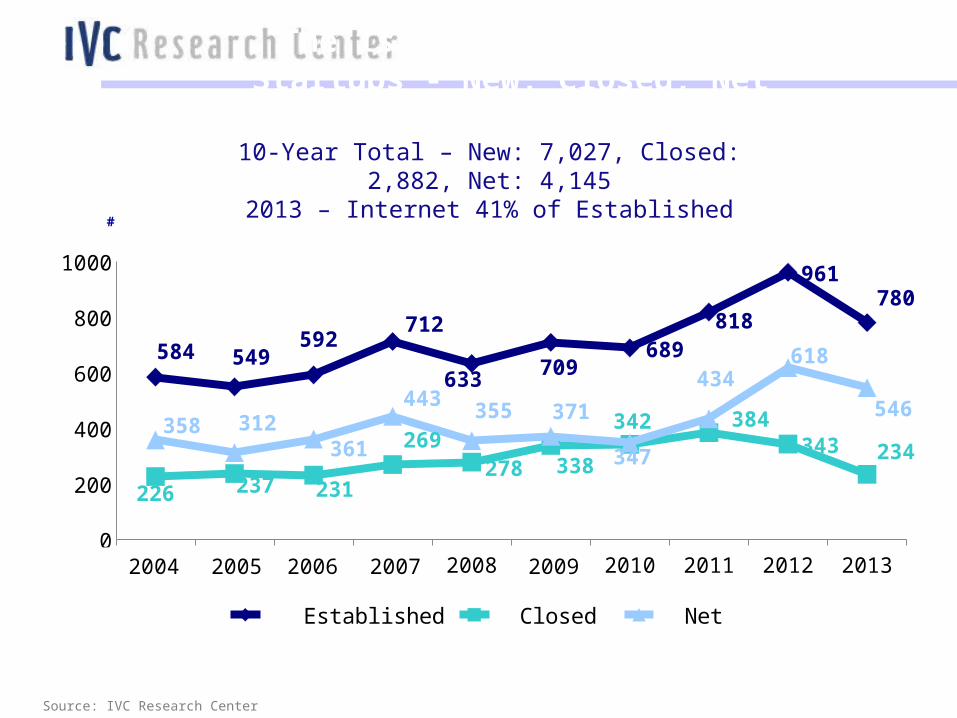

10-Year Total – New: 7,027, Closed: 2,882, Net: 4,1452013 – Internet 41% of Established

Source: IVC Research Center

2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

200

400

600

800

1000

584 549592

712

633 709689

818

961780

226 237 231

269278 338

342 384343 234

358 312361

443355 371

347

434618

546

Established Closed Net

20092007200620052004

#

The Israeli VC EcosystemStartups - New, Closed, Net

Source: IVC Research Center

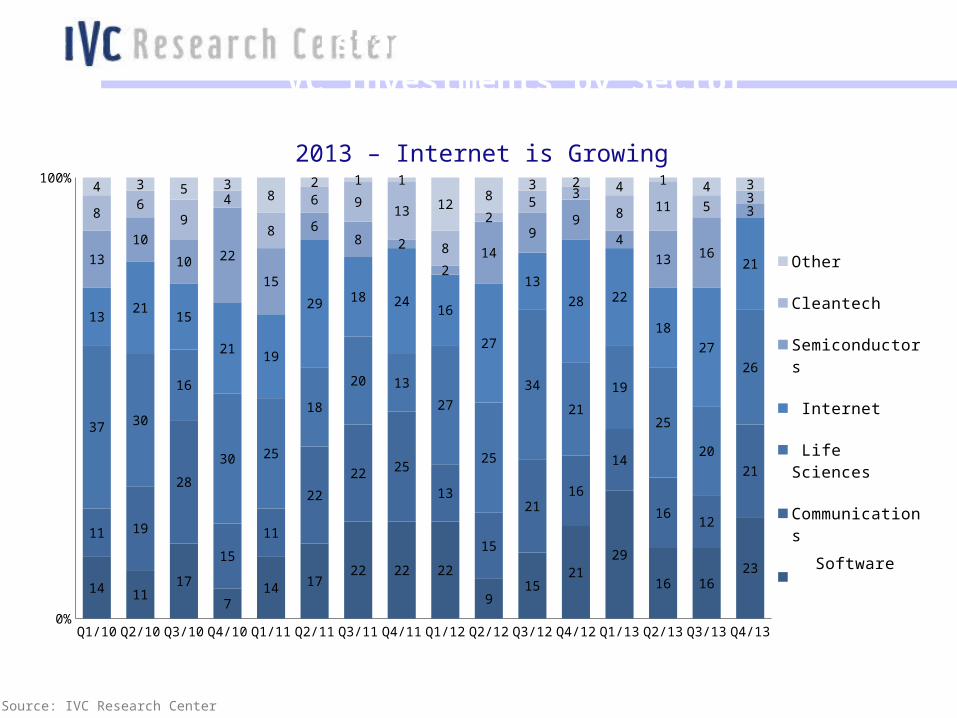

Israel VC Ecosystem VC Investments by Sector

2013 – Internet is Growing

Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11 Q3/11 Q4/11 Q1/12 Q2/12 Q3/12 Q4/12 Q1/13 Q2/13 Q3/13 Q4/130%

100%

14 1117

714 17

22 22 22

915

2129

16 1623

11 19

28

15

11

22

22 25

13

15

2116

14

1612

21

37 30

16

30 25

18

20 13

27

25

34

21

19

25

20

26

1321

15

21 19

29 18 2416

27

1328 22

1827

211310

10 22

15

68 2

214

99

413 16

386

94

8

6 913

8

25

38 11 5

34 3 5 3

82 1 1

128

3 2 4 1 4 3

Other

Cleantech

Semiconductors

Internet

Life Sciences

Communications

SoftwareSoftware

Internet Communications

Semiconductors Life Science

IT/SW

Cleantech

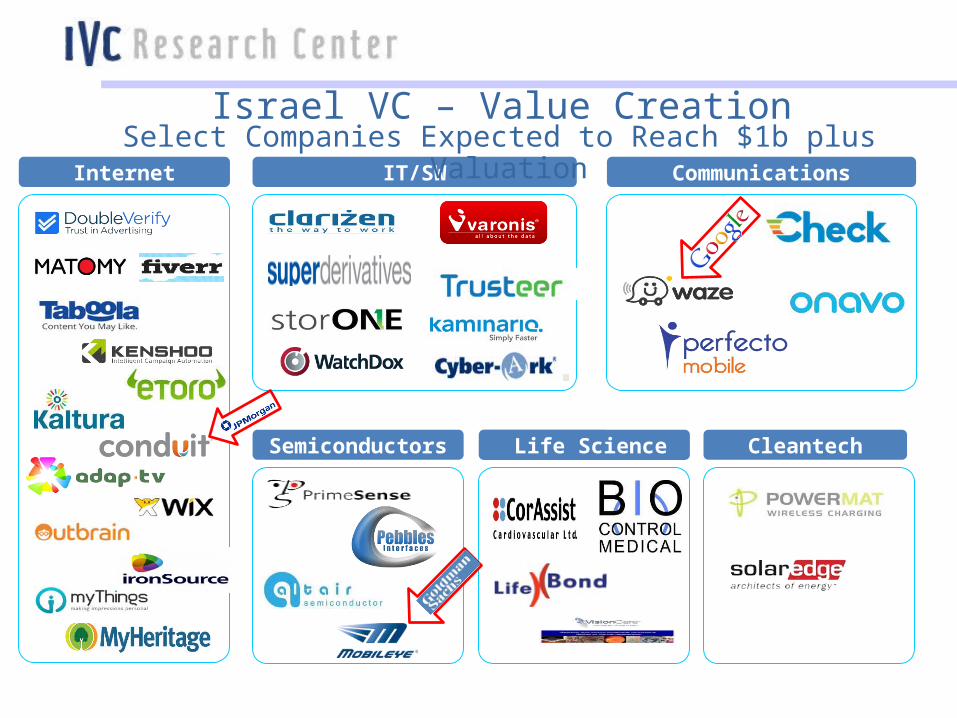

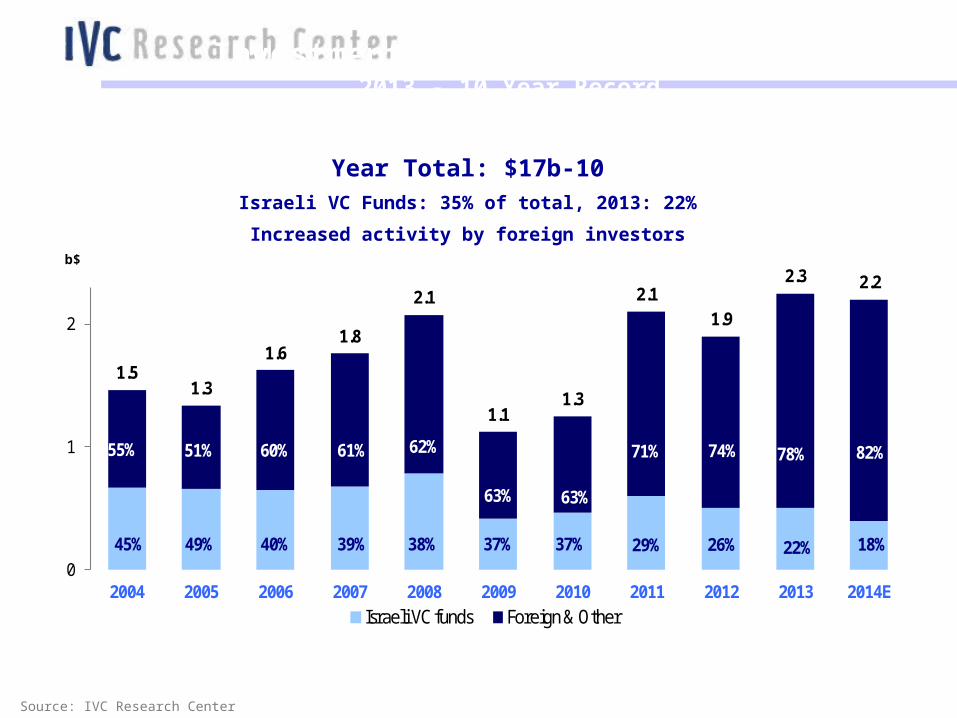

Israel VC – Value CreationSelect Companies Expected to Reach $1b plus Valuation

1.51.3

1.61.8

2.1

1.11.3

2.11.9

2.3 2.2

45% 49% 40% 39% 38% 37% 37% 29% 26% 22% 18%

55% 51% 60% 61% 62%

63% 63%

71% 74% 78% 82%

0

1

2

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E

Israeli VC funds Foreign & Other

Source: IVC Research Center

$b

10-Year Total: $17bIsraeli VC Funds: 35% of total, 2013: 22%

Increased activity by foreign investors

Investments in Israeli Startups2013 - 10 Year Record

Select Foreign Investors in Israeli Startups Increased Activities and Presence

Source: IVC Research Center

Select Investors Exposure/Mode of OperationSource of Capital

Type

Sequoia Israel, Greylock Israel, Orbimed Israel, DFJ – Tel Aviv, Credit Agricole Domestic team

Usually co-invest with Israeli funds

Israel-dedicated funds

VC Funds

Index, Bessemer, Accel, Highland, Battery, Lightspeed, HarbourVest, Canaan, Benchmark, Norwest, USVP, Crescent, SVB, Kima Ventures, Paul Capital, Kreos Capital, Blumberg Capital, Horizon Ventures, Fortrers, Mangrove

Israel is part of investment strategy Most have domestic presence Usually co- invest with Israeli funds

Allocation from main fund

VC Funds

Kleiner Perkins, New Leaf, NEA, Matrix, Mayfield, Opus, MPM, Storm, Charles River, RHO, JK&B, DAG, Globespan, Soffinova, Andresseen Horowitz, Union Square, Atlantic, Softbank, Coller Capital, Silver Lake, Goldman Sachs, JP Morgan, Vector, Apax, Francisco Partners, Susquehanna, Amadeus

Opportunistic approach No domestic presence Usually co-invest in Rounds B, C or later stage with Israeli funds

Allocation from main fund

VC FundsP/E Funds

Intel Capital, Motorola Ventures, ABB Ventures, Singtel, Siemens, T Ventures, GE, Samsung, J&J, Itouchu, Bosch, EMC, IBM, Cisco, BASF, Google, Microsoft, Qualcomm, Facebook, LG, Mitsui, SAP Ventures, AVG, Ebay, Huawei, Lenovu, Deautche Telekom Ventures, GM, Alcatel-Lucent, Vodaphone, HP Ventures, Nielsen Innovate Incubator

Strategic interest Most have domestic presence Usually co–invest with Israeli funds

Corporation nostro and VC Arms

CVC - Corporate Venture Capital

Innovation Endeavors, Tel Aviv Angel Group, Initial Capital, Jeff Pulver, Eric Schmidt, Zeev Oren, UpWest Labs, The Founders Fund, Yossi Vardi, Corporate Accelerators: Google, Microsoft, EMC, IBM

Added value approach Seed, pre Rounds A investors

Individuals, Family wealth

Super AngelsAcceleratorsIncubators

Source: IVC Research Center

Actively Seeking Technology InnovationSelect Multinationals Presence in Israel

Source: IVC Research Center

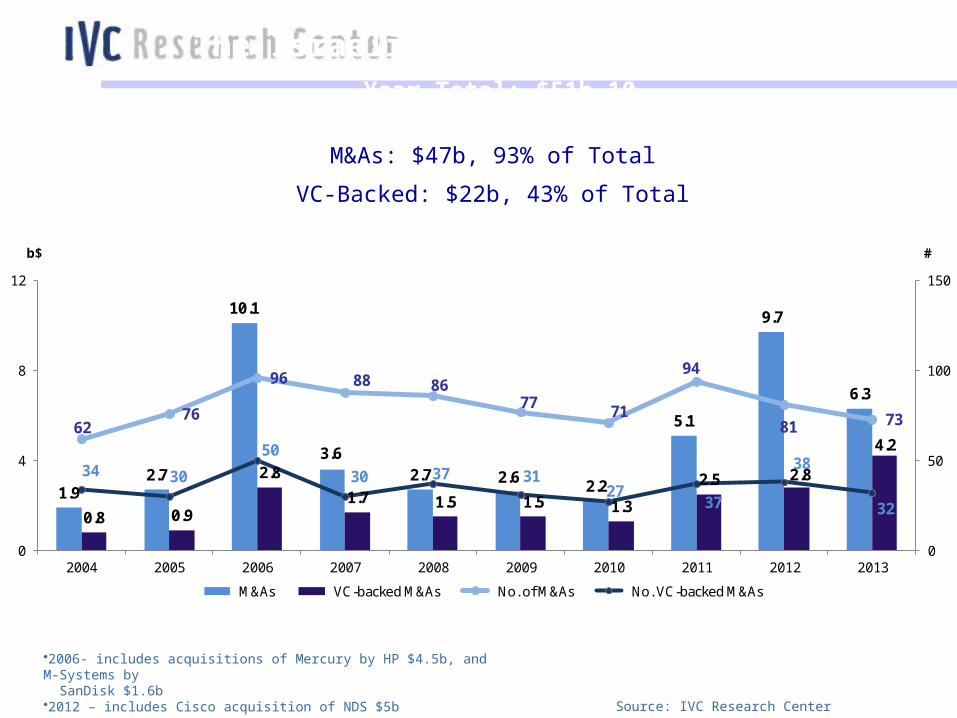

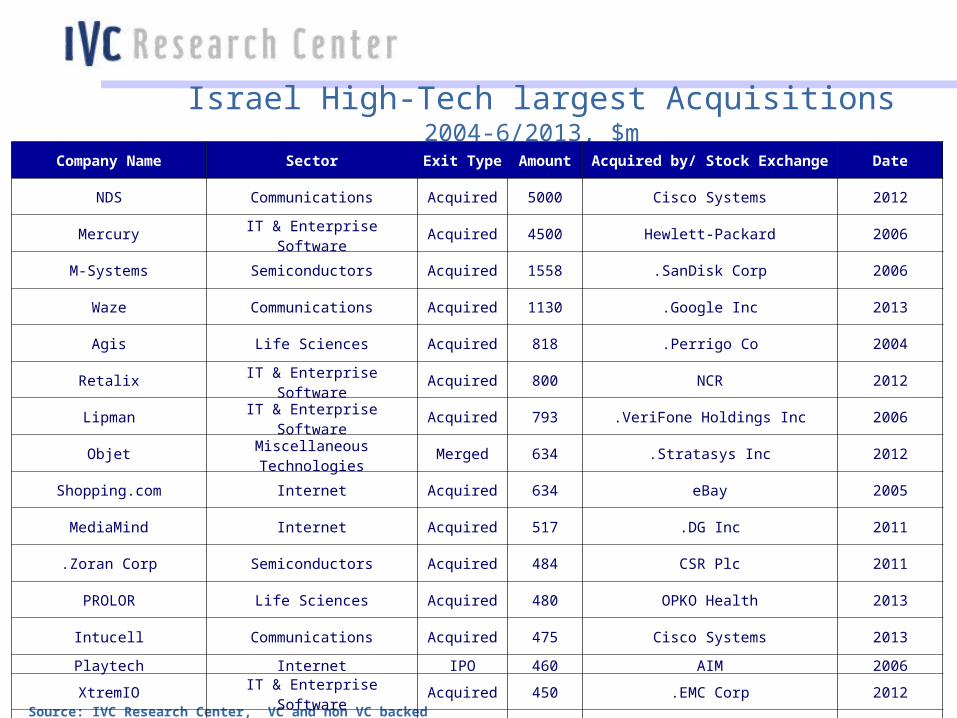

•2006- includes acquisitions of Mercury by HP $4.5b, and M-Systems by SanDisk $1.6b•2012 – includes Cisco acquisition of NDS $5b

The Israeli VC Ecosystem – Exits10-Year Total: $51b

1.92.7

10.1

3.62.7 2.6

2.2

5.1

9.7

6.3

0.8 0.9

2.8

1.7 1.5 1.5 1.3

2.5 2.8

4.262

76

96 88 8677

71

94

81 73

34 30

50

30 37 3127

37

38

32

0

50

100

150

0

4

8

12

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

M&As VC-backed M&As No. of M&As No. VC-backed M&As

#$b

M&As: $47b, 93% of Total

VC-Backed: $22b, 43% of Total

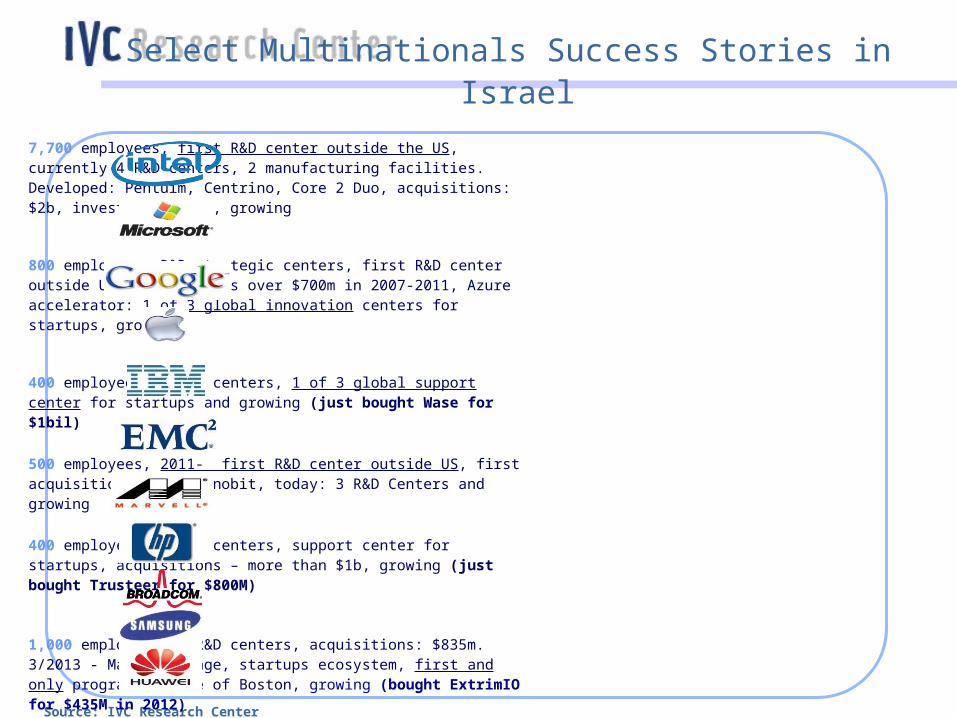

Select Multinationals Success Stories in Israel

Source: IVC Research Center

7,700 employees, first R&D center outside the US, currently 4 R&D centers, 2 manufacturing facilities. Developed: Pentuim, Centrino, Core 2 Duo, acquisitions: $2b, investment $7.3b, growing

800 employees, R&D strategic centers, first R&D center outside US, acquisitions over $700m in 2007-2011, Azure accelerator: 1 of 3 global innovation centers for startups, growing

400 employees, 2 R&D centers, 1 of 3 global support center for startups and growing (just bought Wase for $1bil)

500 employees, 2011- first R&D center outside US, first acquisition: $390m, Anobit, today: 3 R&D Centers and growing

400 employees, 4 R&D centers, support center for startups, acquisitions – more than $1b, growing (just bought Trusteer for $800M)

1,000 employees, 2 R&D centers, acquisitions: $835m. 3/2013 - MassChallenge, startups ecosystem, first and only program outside of Boston, growing (bought ExtrimIO for $435M in 2012)

1,200 employees, R&D center, manufacturing facility, acquisitions:Galileo:$2.7b, RADLAN: $195m,growing

3,600 employees, 2 R&D centers, largest software development site outside the US, growing

500 employees, 6 R&D sites, acquisitions – over $950m, growing

300 employees and growing, 2 R&D Centers, 2013- 1 out of 3 global innovation centers for startups, growing

200 employees and growing, R&D Center, growing

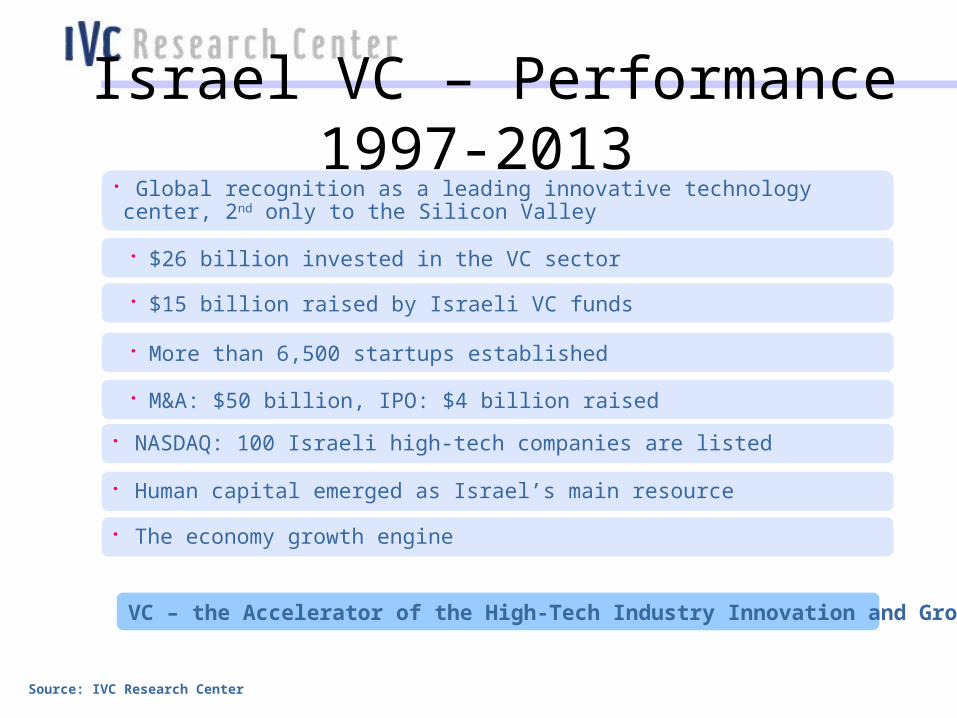

Israel VC – Performance 1997-2013

• More than 6,500 startups established

• NASDAQ: 100 Israeli high-tech companies are listed

• Human capital emerged as Israel’s main resource

• M&A: $50 billion, IPO: $4 billion raised

• $15 billion raised by Israeli VC funds

• $26 billion invested in the VC sector

• Global recognition as a leading innovative technology center, 2nd only to the Silicon Valley

Source: IVC Research Center

VC – the Accelerator of the High-Tech Industry Innovation and Growth

• The economy growth engine

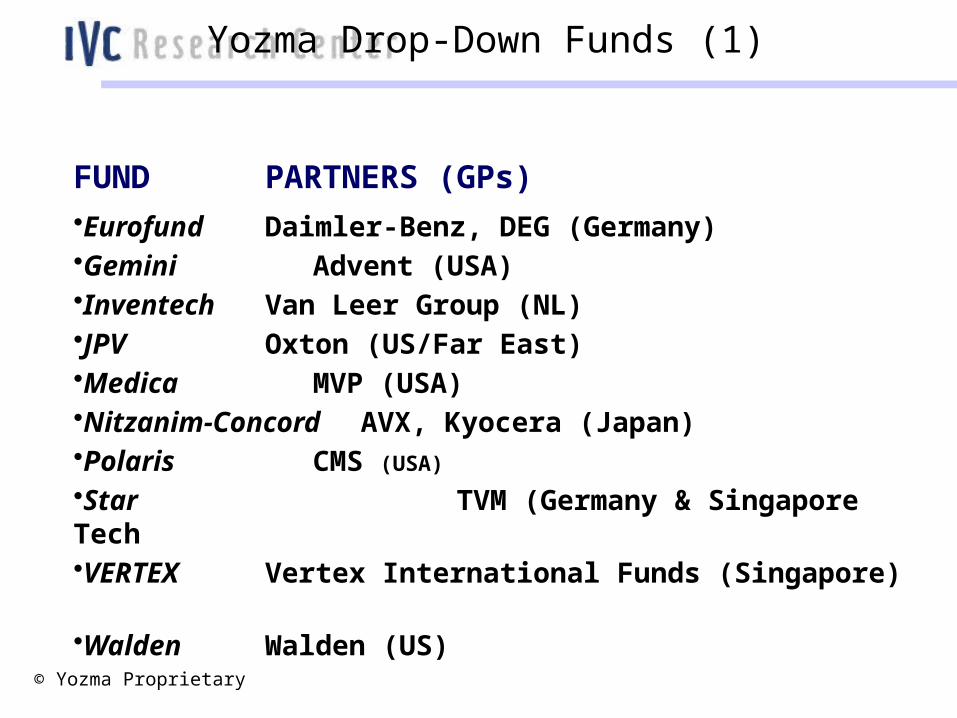

Yozma Drop-Down Funds (1)

© Yozma Proprietary

FUND PARTNERS (GPs)•Eurofund Daimler-Benz, DEG (Germany)•Gemini Advent (USA)•Inventech Van Leer Group (NL)•JPV Oxton (US/Far East)•Medica MVP (USA)•Nitzanim-Concord AVX, Kyocera (Japan)•Polaris CMS (USA) •Star TVM (Germany & Singapore Tech•VERTEX Vertex International Funds (Singapore)•Walden Walden (US)

27

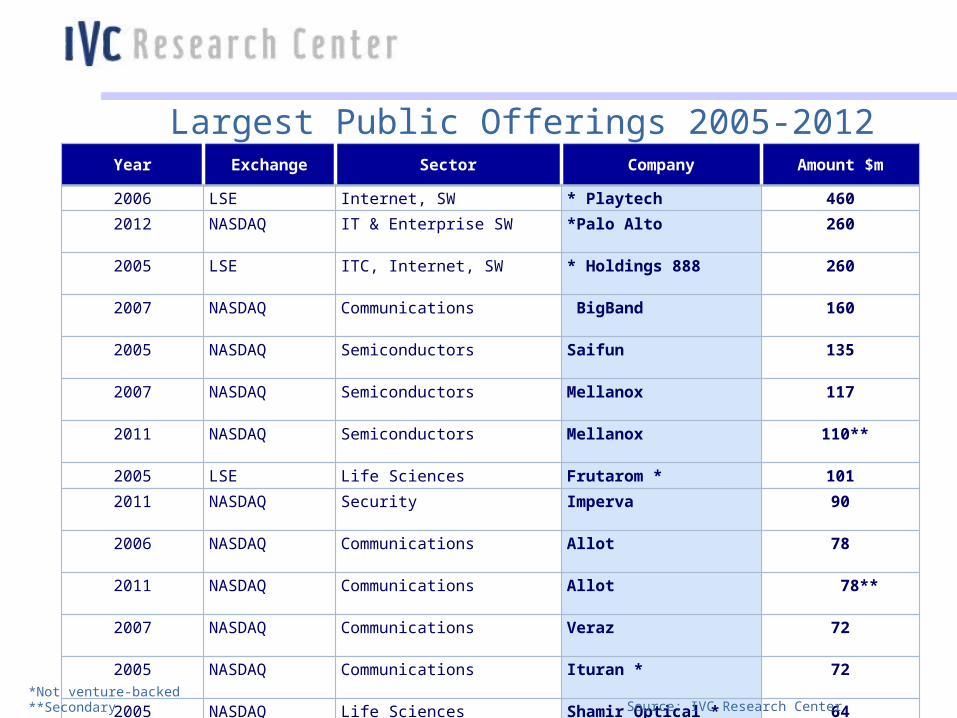

Year Exchange Sector Company Amount $m

2006 LSE Internet, SW Playtech* 460

2012 NASDAQ IT & Enterprise SW Palo Alto* 260

2005 LSE ITC, Internet, SW 888 Holdings* 260

2007 NASDAQ Communications BigBand 160

2005 NASDAQ Semiconductors Saifun 135

2007 NASDAQ Semiconductors Mellanox 117

2011 NASDAQ Semiconductors Mellanox 110**

2005 LSE Life Sciences Frutarom * 101

2011 NASDAQ Security Imperva 90

2006 NASDAQ Communications Allot 78

2011 NASDAQ Communications Allot 78**

2007 NASDAQ Communications Veraz 72

2005 NASDAQ Communications Ituran * 72

2005 NASDAQ Life Sciences Shamir Optical * 64

2010 NASDAQ Internet MediaMind 62

2007 NASDAQ Communications Voltaire 52

2007 TASE Life Sciences BioLine RX 50

2005 AIM ITC Visual Defence * 50

2007 AMEX Life Sciences Protalix 50

Largest Public Offerings 2005-2012

*Not venture-backed**Secondary Source: IVC Research Center

Israel High-Tech largest Acquisitions2004-6/2013, $m

Source: IVC Research Center, VC and non VC backed

Company Name Sector Exit Type Amount Acquired by/ Stock Exchange Date

NDS Communications Acquired 5000 Cisco Systems 2012

Mercury IT & Enterprise Software Acquired 4500 Hewlett-Packard 2006

M-Systems Semiconductors Acquired 1558 SanDisk Corp. 2006

Waze Communications Acquired 1130 Google Inc. 2013

Agis Life Sciences Acquired 818 Perrigo Co. 2004

Retalix IT & Enterprise Software Acquired 800 NCR 2012

Lipman IT & Enterprise Software Acquired 793 VeriFone Holdings Inc. 2006

Objet Miscellaneous Technologies Merged 634 Stratasys Inc. 2012

Shopping.com Internet Acquired 634 eBay 2005

MediaMind Internet Acquired 517 DG Inc. 2011

Zoran Corp. Semiconductors Acquired 484 CSR Plc 2011

PROLOR Life Sciences Acquired 480 OPKO Health 2013

Intucell Communications Acquired 475 Cisco Systems 2013

Playtech Internet IPO 460 AIM 2006

XtremIO IT & Enterprise Software Acquired 450 EMC Corp. 2012

Omrix Life Sciences Acquired 438 Johnson & Johnson Inc. 2008

Solel Cleantech Acquired 418 Siemens AG 2009

CyOptics Communications Acquired 400 Avago 2013

MobilEye Semiconductors Secondary 400 2013

Anobit (now HDC Apple) Semiconductors Acquired 390 Apple 2011

Quigo Internet Acquired 363 America Online (AOL) Inc. 2007

Amobee Communications Acquired 340 SingTel 2012

superDimension Life Sciences Acquired 300 Covidien 2012

Telmap Communications Acquired 300 Intel Corp. 2011

Actimize IT & Enterprise Software Acquired 282 NICE 2007

Cotendo (Now Akamai) Internet Acquired 268 Akamai Inc. 2011

888 Holdings IT & Enterprise Software IPO 260 LSE 2005

Palo Alto IT & Enterprise SW Acquired 260 IPO: NASDAQ 2012

ScaleIO IT & Enterprise Software Acquired 250 EMC Corp. 2013

Conduit Internet Secondary 100 2012

Summary – Israel’s High-Tech Sector

Within 65 leading years, Israel has evolved from a primarily agricultural economy to become a global technology center

The main growth engine of the economy, the magnet attracting foreign investors and leading multinational companies

Increased number and activities of global companies and investors seeking innovative technology, result in increased M&As activities

Strong, high-quality deal flow from new and experienced entrepreneurs

Shortage of capital result in favorable investment terms

The few active experienced and mature Israeli VC funds have the best exposure and right teams to leverage the current Israeli VC opportunity

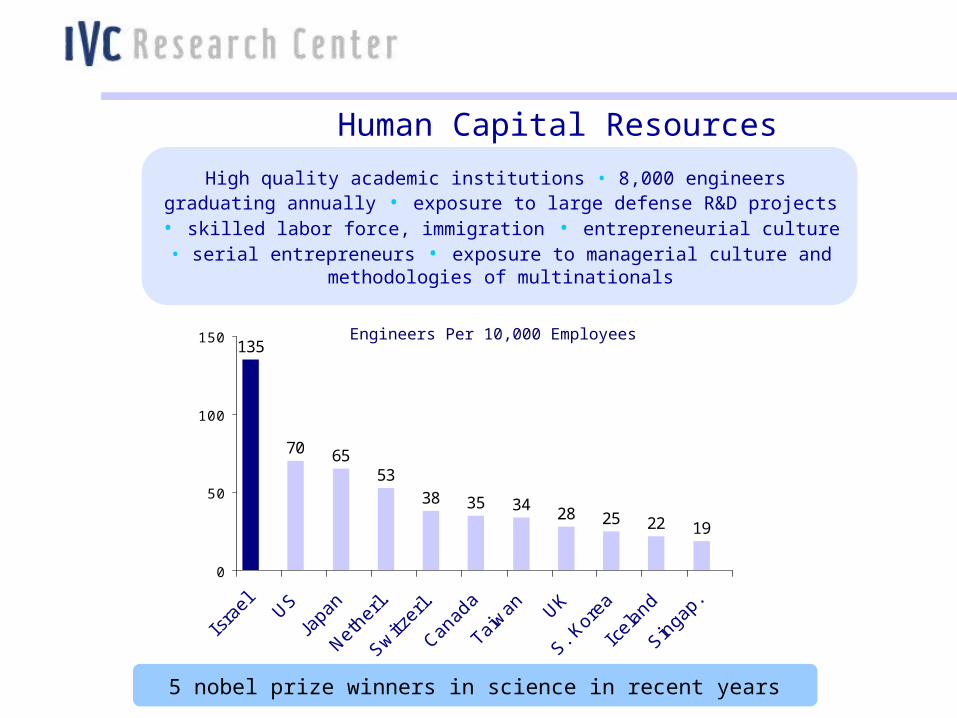

Human Capital Resources

135

70 6553

38 35 34 28 25 22 19

0

50

100

150 Engineers Per 10,000 Employees

5 nobel prize winners in science in recent years

High quality academic institutions • 8,000 engineers graduating annually • exposure to large defense R&D projects • skilled labor force, immigration • entrepreneurial culture • serial

entrepreneurs • exposure to managerial culture and methodologies of multinationals

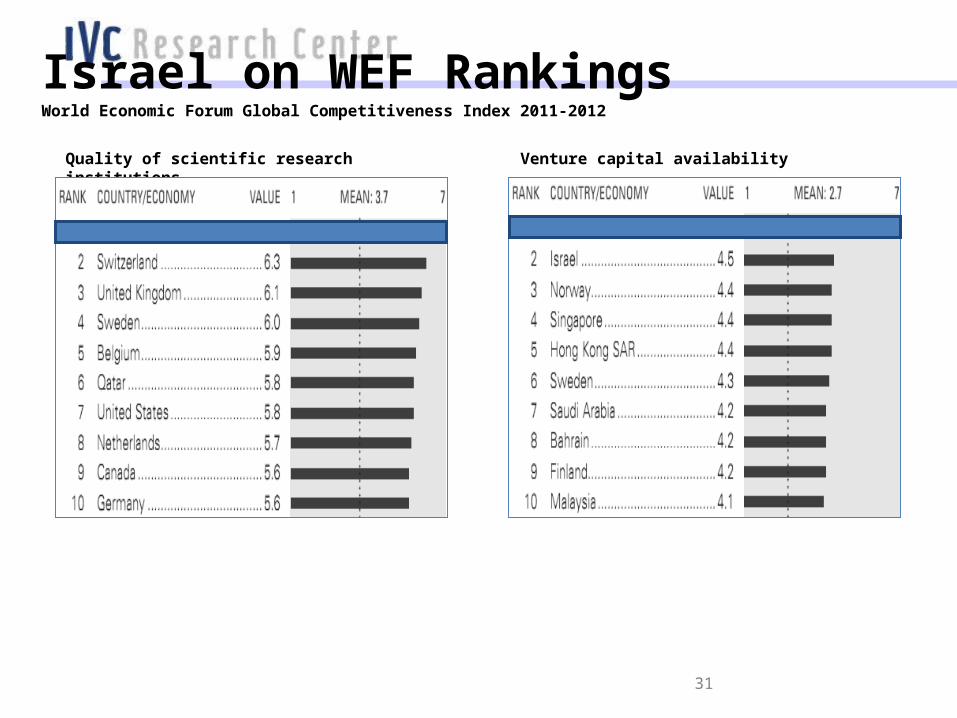

Quality of scientific research institutions Venture capital availability

Israel on WEF RankingsWorld Economic Forum Global Competitiveness Index 2011-2012

Additional Sources: World Economic Forum Global Competitiveness Index 2011-201231

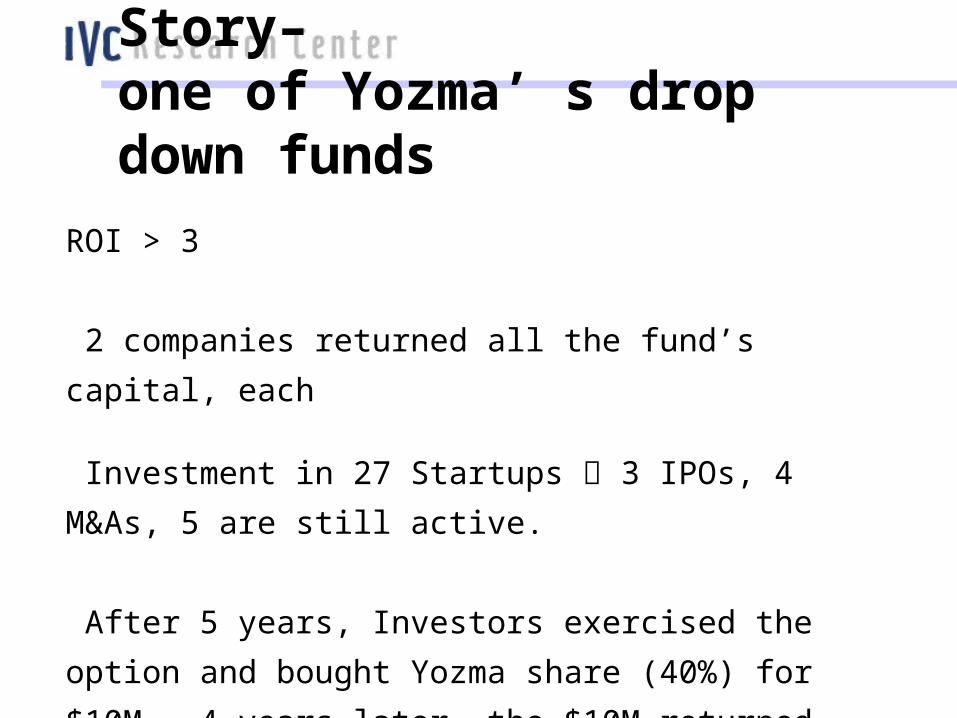

Success Story– one of Yozma’ s drop down funds

ROI > 3

2 companies returned all the fund’s capital, each

Investment in 27 Startups 3 IPOs, 4 M&As, 5 are still active.

After 5 years, Investors exercised the option and bought Yozma

share (40%) for $10M - 4 years later, the $10M returned $33M