Islamic Mutual Fun Industry In Pakistan

48

ISLAMIC MUTUAL FUND INDUSTRY IN PAKISTAN

description

This presentation include the brief history of Mutual funds in Pakistan, its present worth, future trends and prospects, Hopefully will help the interested students.

Transcript of Islamic Mutual Fun Industry In Pakistan

ISLAMIC MUTUAL FUND INDUSTRY IN PAKISTAN

GROUP MEMBERS

Wajid Ali3335Haifa Saleem3336Nabita Ishtiaq

3353Shakeel Aslam

3338Hassan Naseer

3328Rana Tassaduq

3316

PRESENTED TO:

Dr. Salman

Ahmad

Presented by:

Wajid Ali MBA-E9-3335

“INTRODUCTION”

A mutual fund is an investment vehicle that pools in the monies of several investors, and collectively invests this amount in either the equity market or the debt market, or both, depending upon the fund’s objective.

This means you can access either the equity or the debt market, or both, without investing directly in equity or debt.

CONCEPT OF A MUTUAL FUND A Mutual Fund is a trust that pools the savings of a

number of investors who share a common financial goal.

The money thus collected is then invested in capital market instruments such as shares, debentures and other securities.

The income earned through these investments and the capital appreciations realized are shared by its unit holders in proportion to the number of units owned by them.

How Mutual Fund works?

Pool their money with

INVESTORS

FUND MANAGERS

Passed back to

Generate

SECURITIES

Invest in

RETURNS

Mutual Funds

Mutual Funds

Professional Fund Managers

MBA’s

CA’s

CFA’s

The Investor

Investments Stocks Money Markets TFC’s Bank Deposits CFS

Income is earned from dividends on stocks and interest on bonds.

If the fund sells securities that have increased in price, the fund has a capital gain. Most funds also pass on these gains to investors in a distribution.

If fund holdings increase in price but are not sold by the fund manager, the fund's shares increase in price. You can then sell your mutual fund shares for a profit.

Continue……..

First modern day mutual fund was opened in North America in 1924.

The GREAT DEPRESSION of 1930s in USA has stalled the growth of mutual funds sector, like many other economic activities.

Yet it was, 1990s that mutual funds became mainstream investments in the USA and around the globe.

At the end of June 2013, total mutual fund assets all over the world were USD 30.05 trillion.

History and Inception of Mutual Funds

Worldwide Mutual Fund Industry

Presented by:

Haifa Saleem MBA-E9-3336

Islamic Mutual Fund Industry

The Islamic mutual funds market is one of the fastest growing sectors within the Islamic Financial System.

Yet when compared to the mutual fund industry at large, Islamic mutual funds are still in their infancy stage of growth and development.

The wider acceptance of equity funds by Shariah Scholars in early 1990s paved the way to launch Islamic mutual funds.

Currently there are over 600 Islamic Institutions in some 75 countries that are managing funds worth over USD 1.5 trillion by the end of June 2013.

Comparison of Islamic VS World Wide Mutual Fund Industry

Trillion USD

World Wide Mutual Funds

World Wide Islamic Mutual Funds95

.01%

4.99%

$ 1.5 trillion

$ 30.05 trillion

TYPES OF MUTUAL FUNDS ON THE BASES OF STRUCTURE

Open End:-Continuously offer and redeem their units to the investors.

Closed End:-One time issuance of certificates and then are traded in the secondary market.

Open Ended Funds

A type of mutual fund, where there are no restrictions on the amount of shares the fund will issue.

If demand is high enough, the fund will continue to issue shares no matter how many investors there are.

Open-end funds also buy back shares when investors wish to sell.

It's important to understand that each mutual fund has different risks and rewards.

In general, the higher the potential return, the higher the risk of loss.

Although some funds are less risky than others, all funds have some level of risk - it's never possible to diversify away all the risk. This is a fact for all investments.

Closed End Funds

Closed End Funds have a predetermined and fixed number of shares outstanding.

Closed-end funds behave more like stocks because they trade on an exchange and the price is determined by market demand after an initial public offering (IPO) process.

Closed-end funds can be traded below their net asset value or above.

The closed-end fund "company" still has its own stock, which is traded on an exchange and trades above or below its underlying value, or net asset value (NAV), in this case.

They also trade according to market demands. Every seller must have a buyer.

TYPES BY INVESTMENT OBJECTIVE

GROWTH / EQUITY ORIENTED SCHEMES

EQUITY FUNDS

INDEX FUNDS SECTOR FUNDS

INCOME / DEBT ORIENTED SCHEME

SPECIALIZED FUNDS

ISLAMIC FUNDS BALANCED FUND LIQUID FUNDS BOND FUNDS

Presented by:

Nabita Ishtiaq MBA-E9-3353

Benefits OF Mutual Funds

Professional Management:-Expertise to manage and reinvest interest or dividend income, or to investigate thousands of securities. Access to extensive research, market information, and skilled securities traders.

Liquidity:-Mutual fund can be bought and sold on any business day, so investors have easy access to their money. Many individual securities can also be bought and sold readily, others aren't widely traded.

Diversification:-Securities from hundreds or even thousands of issuers it reduces the risk of loss.

Convenience:-Mutual funds offer services that make investing easier. Mail, telephone, or the Internet. Automatic investments into a fund or automatic transfers from a fund to your bank account.

Tax Free Return:-The stock dividend from mutual funds are exempt from tax. Cash dividend taxable.

Continue……..

Comparison of Income Funds with Bank Deposits

TAX BENEFITS OF MUTUAL FUNDS

0%1.2%Tax Deduction

0%4.2%Tax Deduction

Bank Deposits Mutual Funds*

Corporate (35% Tax Bracket)

Pre tax return 12.0% 12%

After tax return 7.8% 12%

Individuals (10% Tax Bracket)

Pre tax return 12.0% 12%

After tax return 10.8% 12%

MARKET RISK: Sometimes prices and yields of all securities rise and fall. Broad outside influences affecting the market in general lead to this.

Inflation Risk: Inflation is the loss of purchasing power over time.

INTEREST RATE RISK: In a free market economy interest rates are difficult if not impossible to predict.

POLITICAL/GOVERNMENT POLICY RISK: Changes in government policy and political decision can change the investment environment.

LIQUIDITY RISK: Liquidity risk arises when it becomes difficult to sell the securities that one has purchased. 1

RISK FACTORS OF MUTUAL FUNDS

History of mutual funds in Pakistan

Mutual funds in Pakistan are registered and legally established in the form of a Trust, under the Trust Act of 1882.

The mutual fund industry is regulated by, the Securities and Exchange Commission of Pakistan (SECP) which licenses each Asset Management Company in strict compliance with the NBFC Rules, 2003 and requires all AMC’s to obtain an independent rating.

Mutual funds introduce in Pakistan in 1962, with the public offering of National Investment Trust followed by the establishment of the Investment Corporation of Pakistan (ICP) in 1966.

Rules Govern Mutual Funds in Pakistan

There are two rules govern mutual funds in Pakistan, which are:

Investment Companies and Investment Advisors' Rules, 1971. (Govern closed-end mutual funds)

2. Asset Management Companies Rules, 1995. (Govern open-ended mutual funds)

Comparison of Pakistan’s VS World Wide Islamic Mutual Funds

Trillion USD

Pakistan's Islamic Mutual Funds

World Wide Islamic Mutual Funds97

.33 %

2.66 %

$ 0.04 trillion

$ 1.50 trillion

Presented by:

Shakeel Aslam MBA-E9-3338

As the year 2013 draws to a close, the mutual fund industry appears to be undergoing a ‘consolidation’ phase. The number of asset management companies has gone down from 27 in 2012 to 24 by now.

In the year-ended June 30, there were about 175,000 individual investor accounts (not to be confused with number of individual investors), against about 171,000 in the prior year.

This seems to be the logical next step in the evolution of this industry, which is still in a developing stage, with less than Rs. 400 billion in total assets under management.

Continue……..

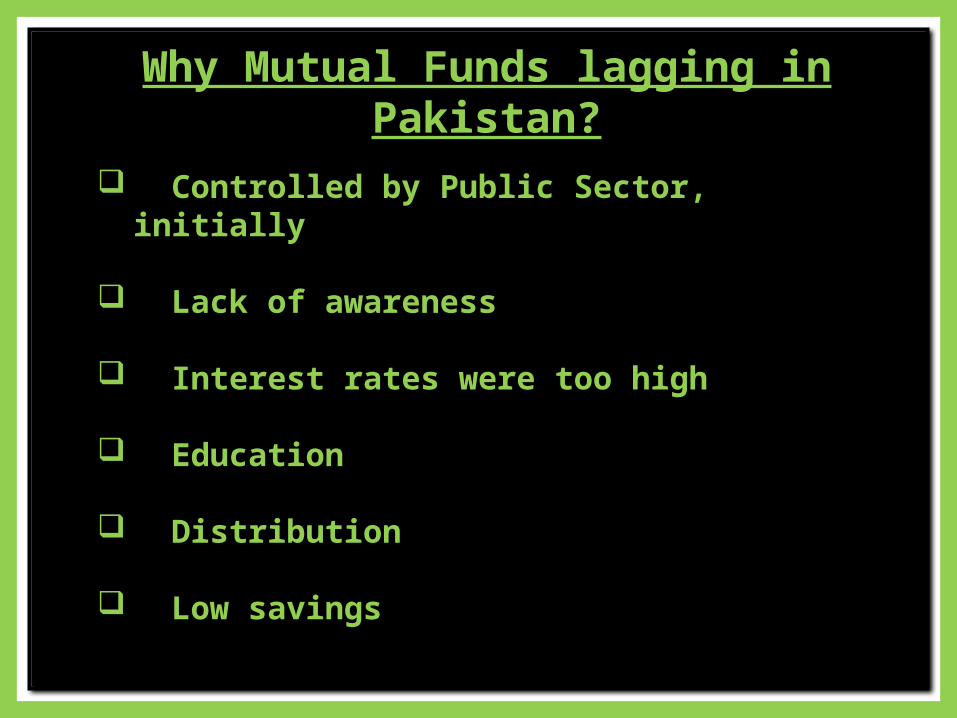

Why Mutual Funds lagging in Pakistan?

Controlled by Public Sector, initially

Lack of awareness

Interest rates were too high

Education

Distribution

Low savings

Mutual fund and Pakistan

MUFAP (mutual fund association of Pakistan) is the trade body for Pakistan's multi billion rupees asset management industry.

MUFAP role is to ensure transparency, high ethical conduct and growth of the mutual fund industry.

After the establishment of MUFAP in 1996, private and foreign firms were allowed to float open-ended funds for the general public.

. Mutual Funds were initially overseen by the Corporate Law Authority (“CLA”) under its Securities Wing.

The money that members manage is in a wide variety of investment vehicles including stocks, bonds, money market instruments, government securities and bank deposits.

Continue…….. The CLA, then a division of the Ministry of Finance, was gradually transformed

and made independent as the Securities and Exchange Commission of Pakistan (“SECP”) as part of the Capital Market Development Program (CMDP) initiative of the Asian Development Bank undertaken for Pakistan.

MUFAP’s role is to establish the essential codes and standards within the industry to ensure the trust and confidence of investors and build the industry as a whole.

The CMDP envisaged formation of four types of Self-Regulated Organizations (“SROs”) to function under the SECP

Stock Exchanges recognized as separate SROs; Mutual Funds Association of Pakistan (MUFAP); Leasing Association of Pakistan (LAP); and Modaraba Association of Pakistan (MAP).

Mutual Fund (Asset Management) Companies in Pakistan

NATIONAL INVESTMENT TRUST.

NBP FULLERTON ASSET MANAGEMENT LTD.

ABAMCO LTD.

AKD INVESTMENT MANAGEMENT LTD.

AL FALAH GHP INVESTMENT MANAGEMENT.

AL-MEEZAN INVESTMENT MANAGEMENT LTD.

AMZ ASSET MANAGEMENT LTD.

FAYSAL ASSET MANAGEMENT LTD.

FIRST CAPITAL INVESTMENTS LTD.

ARIF HABIB INVESTMENT MANAGEMENT LTD.

ASIAN CAPITAL MANAGEMENT (PVT.) LTD

ASKARI ASSET MANAGEMENT LTD.

ATLAS ASSET MANAGEMENT LTD.

BMA ASSET MANAGEMENT LTD.

HABIB ASSETS MANAGEMENT LTD.

HBL ASSET MANAGEMENT LTD.

KASB FUND LTD.

NATIONAL ASSET MANAGEMENT COMPANY LTD.

NATIONAL FULLERTON ASSET MANAGEMENT LTD - NAFA

Continue……..

Continue…….. NATIONAL IINVESTMENT TRUST LTD.

NBP CAPITAL LTD.

NOMAN ABID INVESTMENT MANAGEMENT LTD

PICIC ASSET MANAGEMENT COMPANY LTD.

PRUDENTIAL FUND MANAGEMENT LTD

SAFEWAY MANAGEMENT LTD.

UBL FUND MANAGERS LTD.

WE INVESTMENT MANAGEMENT LTD.

CROSBY ASSET MANAGEMENT LTD.

DAWOOD CAPITAL MANAGEMENT LTD.

Presented by:

Hassan Naseer MBA-E9-3328

Mutual fundExamples in

Pakistan

NATIONAL INVESTMENT TRUST LIMITED

The National Investment Trust Limited (NITL) is the first Asset Management Company of Pakistan, formed in 1962, had Funds under management of Rs.87 billion, with approximately 53,936 unit holders as on December 31, 2013.

NIT's distribution network comprises of 23 branches, various Authorized bank branches all over Pakistan.

The Trust constituted under the Trust Deed dated 12th November 1962, executed between National Investment Trust Ltd (NITL) as Management Company and National Bank of Pakistan as Trustee.

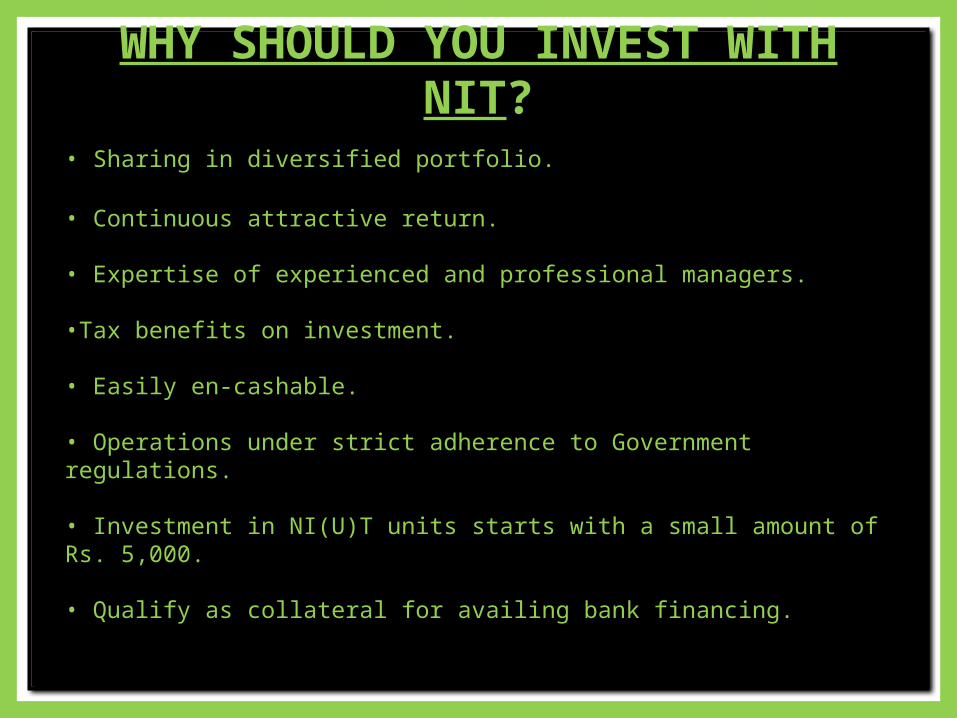

WHY SHOULD YOU INVEST WITH NIT?

• Sharing in diversified portfolio.

• Continuous attractive return.

• Expertise of experienced and professional managers.

•Tax benefits on investment.

• Easily en-cashable.

• Operations under strict adherence to Government regulations. • Investment in NI(U)T units starts with a small amount of Rs. 5,000.

• Qualify as collateral for availing bank financing.

• It minimizes the risk of investment as compared to individual investment in Stock Market.

• Investment decisions at NIT are based on company specific and sector related detailed analysis of information which may not be readily accessible to an individual.

• By investing in NIT units, the unit holder is indirectly investing in the shares quoted on stock exchanges and reaps the benefits of professional decision making.

• It helps to make ownership of the industrial projects more broad based.

Continue……..

Meezan Islamic Fund

Meezan Islamic Fund (MIF) is not only the largest Shariah compliant equity fund but also the largest Equity Fund in private sector in Pakistan.

MIF invests in combination of income and growth stocks of Shariah compliant companies with demonstrated track record of profitability and stable dividend payout history.

Incorporated on 27th February 1995, it is a group company of Meezan Bank Limited and Pakistan Kuwait Investment Company Private Limited and is currently managing assets of over Rs. 61 Billion.

Salient Features Of MIF Professional Management:-Our fund managers are trained investment professionals. Their knowledge provides you and opportunity to earn greater risk adjusted returns. Also by investing in MIF, you pass on the job of continuous monitoring and evaluation of investment opportunities to the Fund manager.

Healthy Return:-Apart from tax benefit, MIF also provides you a healthy return on your investment.

Tax Credit:-Investment in MIF enables you to get tax benefit up to Rs. 232,500/- in case of salaried person or up to Rs 272,250/- in case of non salaried person on investments up to Rs. 1,000,000/- under applicable tax laws, if investment is held for a period of two years.

Affordability:-A minimum investment of Rs. 5,000 makes MIF an affordable investment for small investors. Subsequent investments can be made with a minimum amount of Rs. 1,000. There is no cap on maximum amount of investment.

Impact of global funds sector on the Pakistani industry

Not much impact of global funds sector on the Pakistani industry because international funds who come to Pakistan don’t exactly invest in mutual funds.

Rather they invest in stocks directly, therefore We don’t see any direct link between the two, however Pakistani mutual fund industry can not remain isolated from developments taking place internationally and is adapting the international trends and best practices.

Presented by:

Rana TassaduqMBA-E9-3316

Current issues of funds management

Inadequate regulatory framework to cater for new products and growing needs of investors.

Limited investment options.

Lack of awareness among the general public

Future of Islamic mutual fund sector in Pakistan

The future outlook of the Islamic mutual funds industry in Pakistan is very promising and encouraging. The industry holds several exciting opportunities for both corporate and individual investors including the retired persons.

Islamic mutual fund industry in Pakistan is generating keen interest among a growing number of investors. It is attracting fund managers and leading players of industrial and corporate sector as sponsors

It has been providing versatile and attractive investment avenues to the general public while paying comparatively better returns based on dividend yields and capital gains.

Role of Government to promote Mutual Fund Sector

Mutual Funds Association of Pakistan is playing a pioneering role in the promotion of mutual fund sector in Pakistan by acting as a facilitator between the market participants and the regulators.

It disseminates essential information on various funds, the fund managers, the stock market as well as the regulatory environment under which open and closed-end.

Challenges for Mutual Fund Industry For Islamic mutual funds to progress in Pakistan, a variety of

challenges need to be overcome. The significant challenges are mentioned as following:

Lack of diversified products range

Understanding of investors’ need

Public awareness at mass level

Un-stability of Stock Market

Dearth of liquid debt instruments Protecting and maintaining the integrity and quality

Ensuring performance

Maintaining momentum to ensure viability

Providing competitive returns

Mitigating the Risk involved Inadequate Intellectual Capital Comforting & convincing with bad past investment experiences Budgetary constraints for Marketing activities. Low saving and Investment oriented society Information disclosure and transparency Choosing appropriate distribution network Right timing to launch funds In time after sale activities Strict monitoring of regulators

Continue……..

Recommendations

Team work for the growth of mutual fund industry. Mass awareness and education about mutual funds. Strengthening distribution network. Understanding the fact that related financial industries are not

a threat. Promoting healthy business practices and ethical code of

conduct. Disseminating timely information. Establishing affiliations with mutual funds associations in other

countries and promote one-to-one contacts. Media should play a more supportive and constructive role for

awareness and disseminating information.

Thank YOU …. !!!

“If you do not like any Rule , just Follow it , Reach the top and Change the rule” ........