islamic banking

14

1 Awareness Of Islamic Banking In India- An Empirical Study Mohammad Faisal*, Asif Akhtar** and Asad Rehman*** Islamic banking is fast emerging as an alternative to the interest based conventional banking. It has registered exponential growth in last two decades. The recent global financial crisis and its impact on the conventional banking, has further given impetus to the concept of Islamic banking. India, with a Muslim population of over 180 million is the second largest Muslim population in the world. It remains an unexplored and a big market for Islamic Banking system. This study is an attempt to understand the awareness and attitude of Indians towards Islamic banking. For this purpose, a representative sample of the population is chosen and surveyed with the help of structured questionnaire developed for this purpose. The data collected is analyzed by applying appropriate statistical tools. Proper inferences are drawn and meaningful conclusions are made. This study will help us to identify the major areas of growth and challenges before Islamic finance in India. In the final part of the paper an attempt has been made to conduct a SWOT analysis of Islamic banking in India. Keywords: Islamic Banking, Sharia, Awareness, Attitude. Introduction Banking is an important financial intermediary and essential institution in the present global economic system. According to Oxford English dictionary 1 ‘bank’ is a financial establishment that uses money deposited by customers for investment, pays it out when required, makes loans at interest, and exchanges currency. The basic services a bank provides include receiving, collecting, transferring, paying, managing, exchanging, lending, investing, or safeguarding money for its customers. Now banking is not limited to supports business or commercial duties it also have social obligations towards society for development of any nation the role of its banking system is critically important, especially for a developing nation like India. Islamic banking is based on the principles of Islamic law (sharia) and guided by Islamic economies. Two basic principles behind such a banking system are the sharing of profit and loss and significantly; it prohibits the collection of interest, which is not permitted under Islamic law. Contrary to popular belief, Islamic banking is not just for Muslims. This system does not have any religious connotation .It aims to lay the foundations of an ethical and fair financial system, which consequently affects the socio-economic conditions of the market it is implemented in. Islamic banking provides services to everyone irrespective of religious beliefs, wealth, ethnicity, caste or creed. Half century 1 http://oxforddictionaries.com *Mohammad Faisal Research Scholar, Dept. of Business Administration FMSR, A.M.U. Aligarh, India **Asif Akhtar, Astt. Professor, Dept. of Business Administration FMSR, A.M.U. Aligarh, India *** Dr. Asad Rehman, Astt. Professor, Dept. of Business Administration FMSR, A.M.U. Aligarh, India

description

by geet

Transcript of islamic banking

1

Awareness Of Islamic Banking In India- An Empirical Study

Mohammad Faisal*, Asif Akhtar** and Asad Rehman***

Islamic banking is fast emerging as an alternative to the interest based conventional banking. It has registered exponential growth in last two decades. The recent global financial crisis and its impact on the conventional banking, has further given impetus to the concept of Islamic banking. India, with a Muslim population of over 180 million is the second largest Muslim population in the world. It remains an unexplored and a big market for Islamic Banking system. This study is an attempt to understand the awareness and attitude of Indians towards Islamic banking. For this purpose, a representative sample of the population is chosen and surveyed with the help of structured questionnaire developed for this purpose. The data collected is analyzed by applying appropriate statistical tools. Proper inferences are drawn and meaningful conclusions are made. This study will help us to identify the major areas of growth and challenges before Islamic finance in India. In the final part of the paper an attempt has been made to conduct a SWOT analysis of Islamic banking in India.

Keywords: Islamic Banking, Sharia, Awareness, Attitude.

Introduction Banking is an important financial intermediary and essential institution in the present global economic system. According to Oxford English dictionary1 ‘bank’ is a financial establishment that uses money deposited by customers for investment, pays it out when required, makes loans at interest, and exchanges currency. The basic services a bank provides include receiving, collecting, transferring, paying, managing, exchanging, lending, investing, or safeguarding money for its customers. Now banking is not limited to supports business or commercial duties it also have social obligations towards society for development of any nation the role of its banking system is critically important, especially for a developing nation like India. Islamic banking is based on the principles of Islamic law (sharia) and guided by Islamic economies. Two basic principles behind such a banking system are the sharing of profit and loss and significantly; it prohibits the collection of interest, which is not permitted under Islamic law. Contrary to popular belief, Islamic banking is not just for Muslims. This system does not have any religious connotation .It aims to lay the foundations of an ethical and fair financial system, which consequently affects the socio-economic conditions of the market it is implemented in. Islamic banking provides services to everyone irrespective of religious beliefs, wealth, ethnicity, caste or creed. Half century

1 http://oxforddictionaries.com

*Mohammad Faisal Research Scholar, Dept. of Business Administration FMSR, A.M.U. Aligarh, India **Asif Akhtar, Astt. Professor, Dept. of Business Administration FMSR, A.M.U. Aligarh, India *** Dr. Asad Rehman, Astt. Professor, Dept. of Business Administration FMSR, A.M.U. Aligarh, India

2

ago Islamic banking was virtually unknown. Now Islamic banking, is present is more than 75 countries worldwide. Globally, Islamic banking assets are said to be growing twice as fast as conventional banking assets and expected to reach $1.1 trillion (INR 61 trillion) in 2012, up 33 per cent from 2010, according to The World Islamic Banking Competitiveness Report 2011-12 Ernst & Young study. In considering the merit of Islamic banking in the context of India, we need to consider its demographics. The current Muslim population in India is over 180 million representing about 14% of the total population according to 2001 census. India is one of the largest Muslim populations in the world. Despite this demographic standing, Indian Muslims are mostly financially marginalized and excluded not just due to the unavailability of non-interest banking, but because a majority of them are poor, and hence, lack the requisite credit worthiness to engage in the modern financial and economic activities. There is also the question of historically entrenched disparities in India, in terms of region, religion, ethnicity, etc, which can be gainfully exploited to make a positive mark on the banking landscape of the country. This would definitely help to increase the size of the banking industry manifold, a development that would in turn lay the foundation for more innovations and healthy competition in the financial services industry in India, in the future. One may argue that Indian Muslims have been using existing conventional banking system for years. But this is because for many of them, there is no alternative, which indeed, compounds their financial exclusion. Our conventional banks, in the manner they are presently configured cannot address the financial needs of such a huge segment of the Indian population. There is no way we can deepen our financial markets under these circumstances. We must bear in mind, of course, that it is not only the majority of the Muslims that are financially excluded. A majority of the non-Muslim population too suffers the same fate. Both lack access to financial services. The bulk of Indian small- and medium-scale enterprises (SMEs) have no guaranteed access to credit, not to talk of small agricultural producers that will produce the raw-materials for these SMEs to thrive and survive. Now, we are still left with the question: what is the potential of Islamic banking for the Indian economy? What is the level of awareness of Indians about Islamic banking? What is the attitude of Muslims and non-Muslims towards Islamic banking in India? This study is an attempt to understand the awareness and attitude of Indians towards Islamic banking. For this purpose, a representative sample of the population is chosen and surveyed with the help of structured questionnaire developed for this purpose. The data collected is analyzed by applying appropriate statistical tools. In the final part of the paper an attempt has been made to conduct the SWOT analysis of Islamic banking in India.

3

Literature Review “Those who devour usury will not stand except as stands one whom the devil by his touch has driven to madness. That is because they say: Trade is like usury: but Allah has permitted trade and forbidden usury.... Allah will deprive usury of all blessing, but will give increase for deeds of charity, for He loves not any ungrateful sinner.... O you who believe, fear Allah and give up what remains of your demand for usury, if you are indeed believers. If you do it not, take notice of war from Allah and His messenger, but if you repent you shall have your capital sums; deal not unjustly, and you shall not be dealt with unjustly. And if the debtor is in difficulty, grant him time til it is easy for him to repay. But if you remit it by way of charity, that is best for you if you only knew.” [Surah al- Baqarah, verse 275-280]. Islamic banking is based upon the principle that the use of Riba (interest) is prohibited. This prohibition is based upon Sharia2 ruling. Since Muslims cannot receive or pay interest, they are unable to conduct business with conventional banks (Gerrard and Cunningham, 1997). To service this niche market, Islamic financial institutions have developed a range of halal3 interest-free financing instruments that conform to Sharia ruling, and therefore are acceptable to their clients (Malaysian Business, Dec. 16, 2001). Despite the prohibition of interest by four of the world’s major religions (Judaism, Christianity, Hinduism, and Islam), today’s international economic system is based on interest. However efforts are going on to replace the conventional interest-based banking system with the interest free banking and finance. Apart from religious dimension, the case against interest has been examined by many researchers (Aziz, 2011). The idea of Islamic banking goes back to as early as the 7th century, but it was only commercially implemented in the last century (Jonge, 1996). There is a common understanding among business management researchers that, the rapid growth of Islamic banking at the time when the ethical banking movement is gathering new momentum is not a matter of sheer coincidence. Most researchers including Dhumale and Sapcanin (2006), Lewison (1999), and Scott (2007) are of the view that Islamic banking actually rides on the crest of the world’s renewed interest in the ideas of ethical banking. Scott (2007) contends that Islamic banking has shown that it is financially sustainable because it is recording phenomenal growth rates across the world at a time when most businesses in the finance sector are struggling to survive. Taylor (2003) estimated that by 2002 Islamic banks accounted for around $250 billion in assets, and that this figure was expected to grow in the subsequent years. The Muslim population forms the niche market that Islamic banking targets and Zineldin (1996) reports that this is a powerful market for customized goods and services as it has the

2 Islamic laws

3 Products that fulfill the criteria laid out by Islam of being acceptable for use.

4

highest income outside the Western World, Australia and Japan. Furthermore, its population that currently stands at 25% of the global population is growing rapidly. All these factors indicate that, unless something unusually catastrophic happens, Islamic banking will continue to be financially viable business as it has a growing effective market. The spread of Islamic banking in other parts of the world, among non-traditional Muslim population puts this system of banking in stronger position regarding financial viability (Zaher and Hassan, 2001). Modern Islamic banking was started way back last decades of 19th century with establishments of some interest free banks in Egypt (Kahf, 2001). These organizations are not so successful due to various reasons. In first half of 20th century there are various academic initiatives by different scholars (like Naiem Siddiqi (1948) and Mahmud Ahmad (1952), Muhammad Hamidullah 1944, 1955, 1957 and 1962) across the globe to explore the concept of Islamic banking. A more elaborate explanation was given by Mawdudi in 1950. They have proposed an interest free banking system based on the concept of profit and loss sharing. A substantial literature on individual consumers’ attitudes towards conventional banking and services is already in place, especially concerning selection criteria (or patronage) and customer satisfaction. Moreover, most of this work is focused on banking. There are few studies on individual consumers’ attitudes towards Islamic banks. Erol and El-Bdour (1989) is considered to be the first study of individual consumers’ attitudes towards Islamic banking. A self-administered questionnaire was used to ascertain the attitudes, behavior and patronage factors of bank customers (both Islamic and conventional). The study found that bank customers (at least in Jordan) were generally aware of Islamic banks and their methods. Later, Omer (1992) surveyed 300 Muslims in the UK on their patronage factors and awareness of Islamic financing methods. At the time, Sharia-compliant products and services were primarily available though Islamic finance “windows” at conventional banks. The main finding was that a high level of ignorance prevailed among Muslims in the UK concerning Islamic finance principles. This is generally consistent with findings elsewhere in the literature that Muslims living in a notionally Muslim country have a greater awareness and knowledge of Islamic banking than immigrant Muslims. That said, although UK Muslims were largely ill informed about Islamic methods of finance, religious motivation comprised the most significant factor in their strong preference for Islamic banking services. Metwally (1996) also used factor analysis to study the attitudes of Muslims in three Arabic dual-banking systems (Kuwait, Saudi Arabia and Egypt) towards Islamic banking. The results indicated that Islamic banks did not significantly differ from conventional banks in the benefits and costs of bank products and services and that Islamic banks equaled conventional bank in terms of staff competency and speed of the services. On this basis, and similarly to Omer (1992), it was concluded that religion was the primary factor in the choice of an Islamic banking institution. In Egypt, Hegazy (1995) compared the demographic profiles of four hundred customers of two banks: the Faisal Islamic Bank and the (conventional) Bank of Commerce and

5

Development. The results showed that 98.8 percent of the Islamic bank’s customers were Muslims married with children, while 32.4 percent of the conventional bank’s customers were Christians and 54.3 percent were Muslims. This suggested that the choice of an Islamic bank is based, in part, on a religious motivation. Haron et al. (1994) likewise highlighted the differences in the patronage of Islamic and conventional banks in their study of Muslims and non-Muslims in Malaysia. Two subsequent studies also examined perceptions of Islamic banking in Malaysia – generally viewed as the largest centre for Islamic finance outside the Middle East. Hamid and Nordin (2001) focused on the awareness of Malaysian customers towards Islamic banking within the context of the wider promotion of Islamic education. They found that most Malaysians did not differentiate between Islamic and conventional bank products and services, though the majority had sufficient knowledge of the existence and services offered by Islamic banks in Malaysia. Moreover, even though half of respondents of this study dealt with Islamic banks, they were in need of extra understanding of Islamic banks’ products. In Singapore, Gerrard and Cunningham (1997) also considered attitudes towards Islamic banking, though in the context of a banking system where no Islamic banks were yet present. While the survey results showed, as expected, that non-Muslims were completely unaware of Islamic methods of finance, Muslims fared little better. Once again, fast and efficient service and confidentiality were the primary motivations for bank selection as in Haron’s et al. (1994) study of Malaysian bank customers. Metwally (2002) considered the role of socioeconomic and demographic characteristics in the process of bank selection in Qatar. Two studies on the perceptions and understanding of Islamic finance deserve special note. In the first, Bley and Kuehn (2004) surveyed business students’ knowledge of financial aspects of Islamic and conventional banks in the United Arab Emirates (Sharjah). A finding was that while Arabic Muslims displayed a high level of knowledge of Islamic financial terms and concepts, non-Arabic Muslims students had a higher level of knowledge of conventional banking. That said most students’ banking knowledge was generally at a low level. Recently a study by Akhtar and Akhter (2011) is about the differences in the perception of university employees about Islamic banking in India. Differences were found in the level of awareness about Islamic banking as an alternative to conventional banking.

Methodology for the Study As the main focus of this paper is to examine the level of perceived awareness and attitude of Indians towards Islamic banking, a questionnaire was formed contained questions in four sections. The first section listed eight terms (Riba, Sharia, Ijara, Mudharaba, Musharaka, Murabaha, Sukuk and Takaful, which are used in Islamic banking and finance. Six out of these eight terms are used by Gerrard and Cunningham (1997). Two terms Sukuk and Takaful are added for this study. The respondents were asked to indicate if they knew what the term meant on a four point scale where zero indicates fully unaware and three indicates that fully aware of the term. The second section contained a series of statements/questions that were styled in Likert scale

6

whereby a respondent had to indicate whether he/she “strongly disagree(1)”, “disagree(2)”, “neither agree nor disagree(3)”, “agreed(4)” or “strongly agreed(5)” with statements which were put to him or her. Initially there were 30 statements on which a pilot study was conducted and 11 statements are shortlisted after factor analysis. Out of these 6 statements are to meant to check level of awareness and 5 statements are related to attitude of respondents towards Islamic banking. The third section contains two situation specific questions to check the response of the respondents in those specific conditions. The fourth section contains standard demographic questions, such as gender, age and religion. For this study, data was collected through an exploratory sample survey of 152 respondents from four B class cities of northern India. For this study appropriate hypothesis were developed and tested by calculating mean values and conducting T test. Data analysis was carried out with the help of SPSS Version 17. Since the broad objective of the study is to understand the Indian customers regarding Islamic banking in India. The study has the following specific objectives:

To explore the awareness of Indians about Islamic banking

To explore the attitude of Indians about Islamic banking

To assess the behavior of respondents towards if an Islamic bank operates in India.

To explore the familiarity of respondents towards terms used in Islamic banking.

Hypotheses Following are the 4 hypotheses which are developed and tested for the study. Hypothesis similar to Ho3 and Ho4 are used by Gerrard and Cunningham (1997) in their study in Singapore. These hypotheses were considered because at that time Islamic banking was not introduced in Singapore and Muslims were in Minority in Singapore, very much similar to present condition in India. H01: There is significant variation in the mean value of awareness about Islamic banking among Indians across religion. H02: There is significant variation in the mean value of attitude towards Islamic banking among Indians across religion. H03: Muslims, in contrast to non-Muslims, are well aware of meaning of fundamental terms used in Islamic banking and finance. H04: Muslims, in contrast to non-Muslims, show a different reaction to the opening up of Islamic bank in India. Reliability of the Scale Reliability of the scale used in section II of the questionnaire is tested by calculating Cronbach’s Alpha of statements clubbed for awareness and attitude. As shown in table 1 Cronbach’s Alpha value is 0.912 for awareness and 0.859 for attitude shows high reliability of the scale.

7

Table 1: Reliability of scale

S.No Dimension Statements Cronbach’s Alpha

1

Awareness

In practice Islamic banking is different from conventional banking.

.912

2 Islamic banking is based on Sharia (Islamic Laws).

3 Islamic banking is a banking system for people of all faiths/religions.

4 If I put my money in Islamic banks, I am contended that my money will not be invested in unethical ventures like Alcohol, Gambling etc.

5 Islamic banking is strictly based on risk sharing model.

6 Islamic banks are more regulated form of banking as they are governed by regulatory bodies as well as by Sharia boards.

7

Attitude

Financing on the basis of profit-loss-sharing between the lender and the borrower will be advantageous to both.

.859

8 Financial matters and religion are inseparable.

9 Investments are more secure in Islamic banks

10 Islamic banking provides a solution to contemporary financial problems.

11 Islamic banking is at par with the principles of modern finance.

8

Results and Discussion 1. Descriptives of the sample

Table 2: Sample Profile

Sample distribution by

Frequency Percent

Religion Muslim 104 68.4

Non- Muslim 48 31.6

Educational Qualification

Less than Graduation 13 8.6

Graduation/Post graduation

37 24.3

M. Phil. /Ph.D. 28 18.4

Professional Qualification

47 30.9

Madarsa Education 27 17.8

Occupation

Government Service 47 30.9

Private Service 69 45.4

Self employed and business

20 13.2

Any other 16 10.5

Age group

Below 25 7 4.6

25 to 35 78 51.3

35 to 50 63 41.4

Above 50 4 2.6

Table no. 2 shows the descriptive statistics of the respondents on various demographic variables. As per the objectives of the study, the sample is subdivided on the basis of religion, educational qualification, occupation and age group. Sample populations have a mix of Muslims and non-Muslims of different age-group, educational qualification and occupation. 2. Hypothesis Testing

Awareness and Attitude

Table 3: Mean scores of the dimension

↓Religion/Dimension→

Muslim Non-

Muslim

Awareness 4.0881 2.5417

Attitude 4.0462 3.0125

9

Table 4: Independent Samples Test

F t df Sig.

Awareness 18.785 10.377 150 .000

Attitude 33.240 11.545 150 .000

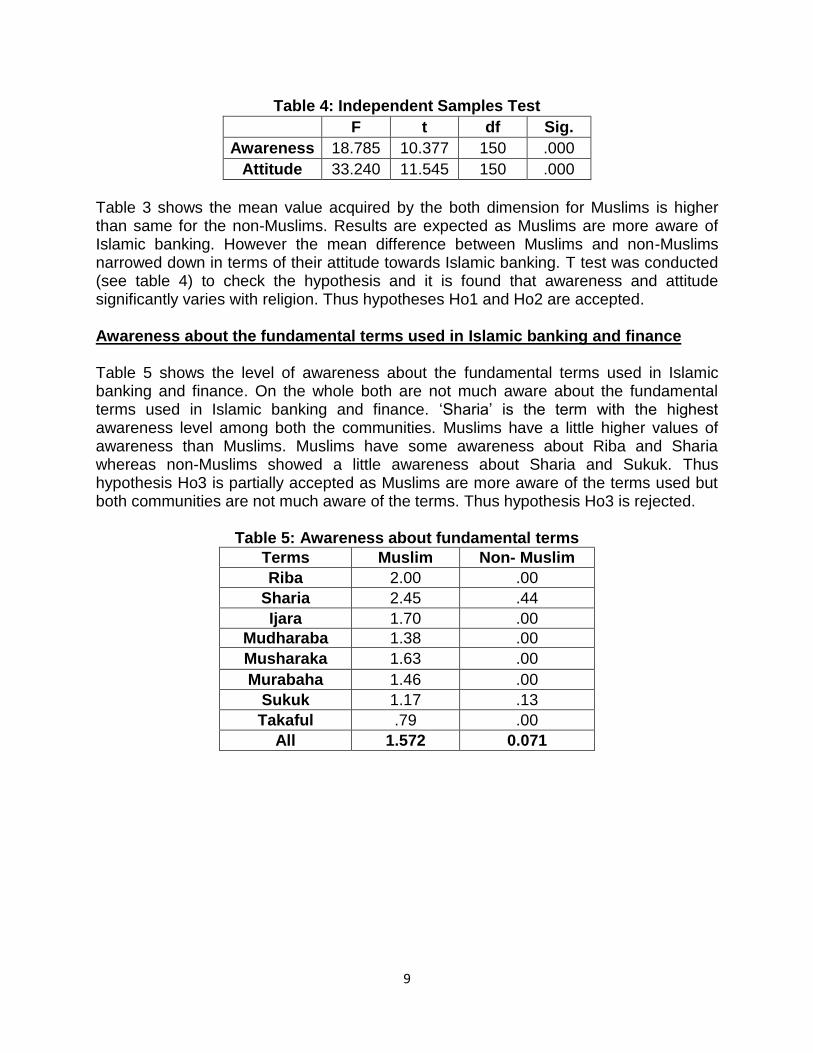

Table 3 shows the mean value acquired by the both dimension for Muslims is higher than same for the non-Muslims. Results are expected as Muslims are more aware of Islamic banking. However the mean difference between Muslims and non-Muslims narrowed down in terms of their attitude towards Islamic banking. T test was conducted (see table 4) to check the hypothesis and it is found that awareness and attitude significantly varies with religion. Thus hypotheses Ho1 and Ho2 are accepted. Awareness about the fundamental terms used in Islamic banking and finance Table 5 shows the level of awareness about the fundamental terms used in Islamic banking and finance. On the whole both are not much aware about the fundamental terms used in Islamic banking and finance. ‘Sharia’ is the term with the highest awareness level among both the communities. Muslims have a little higher values of awareness than Muslims. Muslims have some awareness about Riba and Sharia whereas non-Muslims showed a little awareness about Sharia and Sukuk. Thus hypothesis Ho3 is partially accepted as Muslims are more aware of the terms used but both communities are not much aware of the terms. Thus hypothesis Ho3 is rejected.

Table 5: Awareness about fundamental terms

Terms Muslim Non- Muslim

Riba 2.00 .00

Sharia 2.45 .44

Ijara 1.70 .00

Mudharaba 1.38 .00

Musharaka 1.63 .00

Murabaha 1.46 .00

Sukuk 1.17 .13

Takaful .79 .00

All 1.572 0.071

10

Response if Islamic banking introduced in India

Muslims Non-

Muslims No

(104)

Per cen

t

No (48)

Per cen

t 1

If an Islamic Bank opens its branch in India what will be your reaction to it?

a Open an account immediately with such type of bank.

81 77.8

3 6.2

b Wait for market response and open an account with such a bank if it is providing more benefits than existing commercial banks.

15 14.4

23 47.9

c Will continue banking with the traditional commercial banks.

3 2.8 8 16.6

d Can’t say 5 4.8 14

29.1

2

In case an Islamic bank announced that it had no profit to distribute on investment and savings deposits for any one year and if you were a depositor with this bank, would you:

No (104

)

Per cen

t

No (48)

Per cen

t

a Keep the deposit at the same or a different Islamic bank, because placing the deposit with a non-Islamic bank contravenes Islamic principles

58 55.7

0 0

b Withdraw all deposits at once and switch them to one or more banks which guarantee a return

2 1.9 10 20.8

c Remain a depositor at the Islamic bank because it could distribute high profits in subsequent years

31 29.8

6 12.5

d Consult relatives and colleagues and then decide what to do

9 8.6 18 37.5

e Can’t Say 4 3.8 14

29.1

A huge majority of Muslims respondents (77%) said that they will immediately open an account with this type of bank, while only a very small (6%) non-Muslim respondent will immediately open an account majority of non-Muslim respondent (47.9 %) will wait for market response and open an account if Islamic banks perform better. In case of non distribution of profit by an Islamic bank, a large majority (55.7 + 29.8 = 85.5%) of Muslims will remain depositor of the bank while only 20% of non-Muslims will transfer their account to traditional interest based banks. Thus, on basis of responses of these two questions hypothesis Ho4 is accepted.

11

Summary of hypothesis testing

S. No.

Hypothesis Result

Ho1 There is significant variation in the mean value of awareness about Islamic banking among Indians across religion.

Accepted

Ho2 There is significant variation in the mean value of attitude towards Islamic banking among Indians across religion.

Accepted

H03 Muslims, in contrast to non-Muslims, are well aware of meaning of fundamental terms used in Islamic banking and finance.

Rejected

H04 Muslims, in contrast to non-Muslims, show a different reaction to the opening up of Islamic bank in India.

Accepted

Discussion and Conclusions There is a general lack of awareness about Islamic banking in India. It is completely a new alternative banking system. People are less aware about Islamic Banking and its terminology. Both Muslims and non-Muslims show a positive attitude towards Islamic Banking. However, a good number of respondents said that they will prefer to put their savings in Islamic Banks if these banks provide better profit than existing commercial banks. Most of the Muslim respondents say that they will either keep the deposit in same or the different Islamic Banks, because placing a deposit with a non Islamic Bank contravenes Islamic principles. Further, they wished to remain a depositor at the Islamic Bank if it has no profit to distribute on investment and saving deposits for any one year because of their hope that it could distribute high profits in the subsequent years. The findings of the present study are in line with previous studies by Omer (1992) and Gerrard and Cunningham (1997) but deviate from the findings of Erol and El-Bdour (1989) and Bley and Kuehn (2004). This is may be because Erol and El-Bdour (1989) and Bley and Kuehn (2004) conducted their studies in Islamic nations Jordan and Qatar with a Muslims majority whereas Omer (1992) and Gerrard and Cunningham (1997) conducted their study in United Kingdom and Singapore where Muslims are in minority. Thus, the studies by Omer (1992) and Gerrard and Cunningham (1997) are closer in resemblance to the Indian context which also has a Muslims minority.

12

SWOT Analysis

Strength

Proved better banking system in recent global financial crisis.

Based on profit and loss sharing agreements.

Based on the principles of Sharia

People have positive attitude that Islamic banks are and based on equity, justice and ethics.

More controlled form of banking due to dual monitoring.

Weakness

Majority of people believe that this system is for Muslims only

Market share is negligible as compare to conventional banking

Major regulatory and legal framework need to be changed

There are some conflicts in Sharia laws among different school of thoughts.

Lack of awareness about Islamic Banking system

Opportunities

Biggest Muslim population in the world

An alternate to the conventional banking

Chances of innovation and reengineering in financial products are more

Positive attitude of Indian Muslims and non- Muslims towards Islamic banking.

Threats

Opposition by some political groups.

Stiff competition from conventional banks.

There is a perception that religion and financial matters are two separate things.

13

Recommendations and Managerial Implications There is no doubt that Islamic banking in India is in its nascent stage but there is tremendous scope for it because of a positive attitude of Muslims as well as non-Muslim toward it. Most of the respondents, as already discussed, are not aware of Islamic banking system. Hence there is a need to develop a marketing model accordingly and bring some path breaking modifications in the existing setups as being offered in different parts of the world. It is required to create awareness among people that it is not only for Muslims but also for all other people. It is rather an alternative banking system, rendered more effective by applying the risk sharing model based on interest free philosophy of banking. Similarities in the findings of this study with the studies conducted at Singapore and United Kingdom imply that the model adopted for introduction of Islamic banking in these countries may be adopted in India. Like Opening of special Islamic banking windows in existing commercial banks by accommodating some minor regulatory changes. Limitations of the Study Due to the time constraints and the breadth of scope of the study, it was not possible to research in depth every aspect of Islamic banking, most of which has been dealt with in other studies. The sample population of this study has been drawn from north Indian cities, which represents a different culture. The findings of this study therefore need to be generalized with care. This study also treats Indian Muslims as part of a single cultural entity. While this could be so at the macro level of retailing, cultural differences among the Indian Muslims could become an important variable at the micro level. More researches would be needed for generalizing the findings of the study at the micro level.

References Abdul-Gafoor, A. (2003), Islamic Banking, A.S. Noor Deen, Kuala Lumpur. Akhter, J. and Akhter, A. (2011), “Awareness and attitude of University Employees

towards Islamic banking in India”, International Journal of Business Swot. Bley, J. and Kuehn, K. (2004), “Conventional versus Islamic finance: student knowledge

and perception in the United Arab Emirates”, International Journal of Islamic Financial Services, Vol. 5 No. 4, pp. 17-30.

De Jonge, A. (1996) ‘Islamic law and the finance of international trade’, Monash University Working Paper,Melbourne.

De Jonge, A. (1996) ‘Islamic law and the finance of international trade, Monash University Working Paper, Melbourne.

El-Gamal, M. (2000), A Basic Guide to Contemporary Islamic Banking and Finance, available at: www.witness-pioneer.org/

Erol, C. and El-Bdour, R. (1989), “Attitudes, behaviour and patronage factors of bank customers towards Islamic banks”, International Journal of Bank Marketing, Vol. 7 No. 6, pp. 31-7.

14

Gerrard, P. and Cunningham, J. B. (1997) ‘Islamic banking: A study in Singapore’, International Journal of Bank Marketing, Vol. 15, No. 6, pp. 204 – 216.

Hamid, A. and Nordin, N. (2001), “A study on Islamic banking education and strategy for the new millennium-Malaysian experience”, International Journal of Islamic Financial Services, Vol. 2 No. 4, pp. 3-11.

Haron, S., Ahmad, N. and Planisek, S. (1994), “Bank patronage factors of Muslim and non-Muslim customers”, International Journal of Bank Marketing, Vol. 12 No. 1, pp. 32-40.

Hegazy, I. (1995), “An empirical comparative study between Islamic and commercial banks’ selection criteria in Egypt”, International Journal of Commerce and Management, Vol. 5 No. 3, pp. 46-61

Iqbal, M. and Llewellyn, D. (Eds). (2002), Islamic Banking and Finance: New Perspectives on

Iqbal, M. and Molyneux, P. (2005), Thirty Years of Islamic Banking: History, Performance, and Prospects, Palgrave Macmillan, New York, NY.

Lewis, M. and Algaoud, L. (2001), Islamic Banking, Edward Elgar, Cheltenham. Malaysian Business (2001), ‘A welcome alternative’, Malaysian Business, December

16. Metwally, M. (1996), “Attitudes of Muslims towards Islamic banks in a dual-banking

system”, American Journal of Islamic Finance, Vol. 6 No. 1, pp. 11-17. Metwally, M. (2002), “The impact of demographic factors on consumers’ selection of a

particular bank within a dual banking system: a case study”, Journal of International Marketing and Marketing Research, Vol. 27 No. 1, pp. 35-44.

Microfinance, Technical Note, Regional Bureau for Arab States, UNDP. Obaidullah, M. (2005), Islamic Financial Services, Islamic Economics Research Centre,

Jeddah. Omer, H. (1992), “The implication of Islamic beliefs and practice on Islamic financial

institutions in the UK”, PhD dissertation, Loughborough University, Loughborough. Profit-Sharing and Risk, Edward Elgar, Cheltenham. Rahul Dhumale and Amela Sapcanin (2006), An Application of Islamic Banking

Principles to Taylor, J. M. (2003). Islamic banking—the feasibility of establishing an Islamic bank in

the United States. American Business Law Journal, 40(2), 385-416. Warde, I. (2000), Islamic Finance in the Global Economy, Edinburgh University Press,

Edinburgh. Zaher, T. S. & Hassan, M. K. 2001. ‘A comparative literature survey of Islamic finance

and banking’, Financial Markets, Institutions and Instruments, 10(4): 155 – 199. Zineldin, M. (2002) "Managing in the @ age: Banking service quality and strategic positioning", Measuring Business Excellence, Vol. 6 Iss: 4, pp.38 - 43