Islamic Banker Magazines Chat with MM & Dr Munir

4

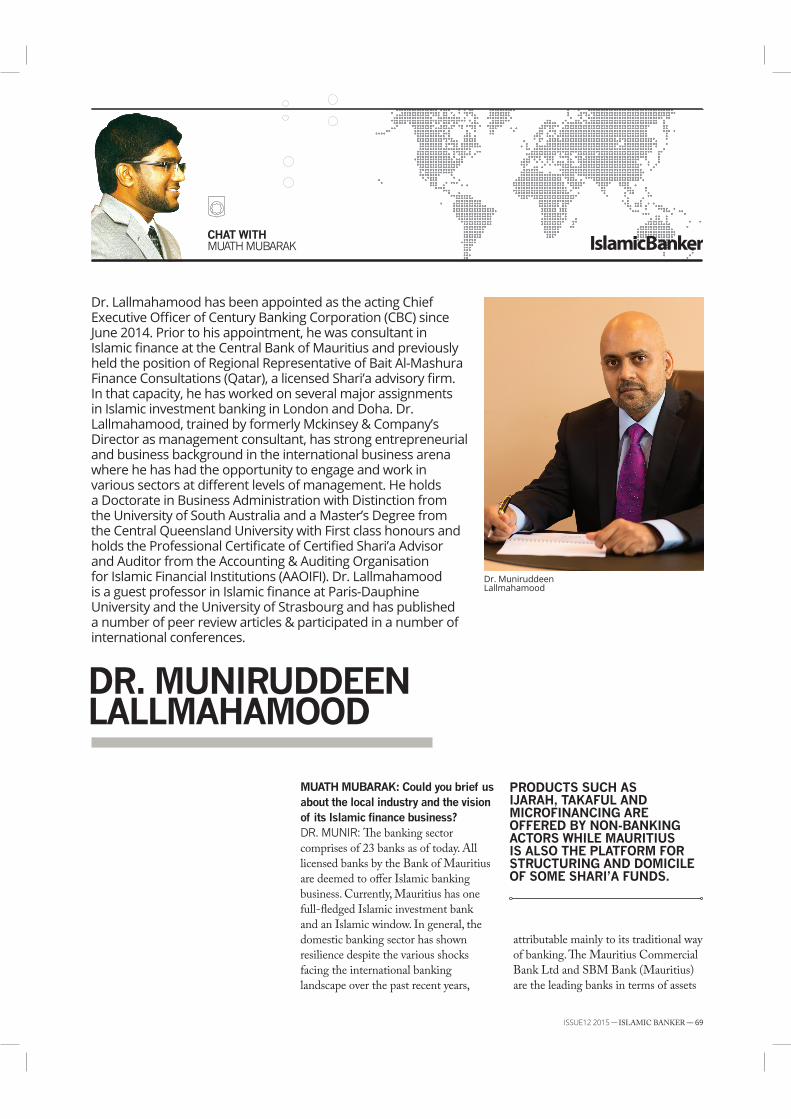

ISSUE12 2015 __ ISLAMIC BANKER __ 69 CHAT WITH MUATH MUBARAK PRODUCTS SUCH AS IJARAH, TAKAFUL AND MICROFINANCING ARE OFFERED BY NON-BANKING ACTORS WHILE MAURITIUS IS ALSO THE PLATFORM FOR STRUCTURING AND DOMICILE OF SOME SHARI’A FUNDS. DR. MUNIRUDDEEN LALLMAHAMOOD MUATH MUBARAK: Could you brief us about the local industry and the vision of its Islamic finance business? DR. MUNIR: e banking sector comprises of 23 banks as of today. All licensed banks by the Bank of Mauritius are deemed to offer Islamic banking business. Currently, Mauritius has one full-fledged Islamic investment bank and an Islamic window. In general, the domestic banking sector has shown resilience despite the various shocks facing the international banking landscape over the past recent years, attributable mainly to its traditional way of banking. e Mauritius Commercial Bank Ltd and SBM Bank (Mauritius) are the leading banks in terms of assets Dr. Lallmahamood has been appointed as the acting Chief Executive Officer of Century Banking Corporation (CBC) since June 2014. Prior to his appointment, he was consultant in Islamic finance at the Central Bank of Mauritius and previously held the position of Regional Representative of Bait Al-Mashura Finance Consultations (Qatar), a licensed Shari’a advisory firm. In that capacity, he has worked on several major assignments in Islamic investment banking in London and Doha. Dr. Lallmahamood, trained by formerly Mckinsey & Company’s Director as management consultant, has strong entrepreneurial and business background in the international business arena where he has had the opportunity to engage and work in various sectors at different levels of management. He holds a Doctorate in Business Administration with Distinction from the University of South Australia and a Master’s Degree from the Central Queensland University with First class honours and holds the Professional Certificate of Certified Shari’a Advisor and Auditor from the Accounting & Auditing Organisation for Islamic Financial Institutions (AAOIFI). Dr. Lallmahamood is a guest professor in Islamic finance at Paris-Dauphine University and the University of Strasbourg and has published a number of peer review articles & participated in a number of international conferences. Dr. Muniruddeen Lallmahamood

-

Upload

munir-daud -

Category

Economy & Finance

-

view

39 -

download

3

Transcript of Islamic Banker Magazines Chat with MM & Dr Munir

ISSUE12 2015 __ ISLAMIC BANKER __ 69

CHAT WITH MUATH MUBARAK

PRODUCTS SUCH AS IJARAH, TAKAFUL AND MICROFINANCING ARE OFFERED BY NON-BANKING ACTORS WHILE MAURITIUS IS ALSO THE PLATFORM FOR STRUCTURING AND DOMICILE OF SOME SHARI’A FUNDS.

DR. MUNIRUDDEEN LALLMAHAMOOD

MUATH MUBARAK: Could you brief us about the local industry and the vision of its Islamic finance business?DR. MUNIR: The banking sector comprises of 23 banks as of today. All licensed banks by the Bank of Mauritius are deemed to offer Islamic banking business. Currently, Mauritius has one full-fledged Islamic investment bank and an Islamic window. In general, the domestic banking sector has shown resilience despite the various shocks facing the international banking landscape over the past recent years,

attributable mainly to its traditional way of banking. The Mauritius Commercial Bank Ltd and SBM Bank (Mauritius) are the leading banks in terms of assets

Dr. Lallmahamood has been appointed as the acting Chief Executive Officer of Century Banking Corporation (CBC) since June 2014. Prior to his appointment, he was consultant in Islamic finance at the Central Bank of Mauritius and previously held the position of Regional Representative of Bait Al-Mashura Finance Consultations (Qatar), a licensed Shari’a advisory firm. In that capacity, he has worked on several major assignments in Islamic investment banking in London and Doha. Dr. Lallmahamood, trained by formerly Mckinsey & Company’s Director as management consultant, has strong entrepreneurial and business background in the international business arena where he has had the opportunity to engage and work in various sectors at different levels of management. He holds a Doctorate in Business Administration with Distinction from the University of South Australia and a Master’s Degree from the Central Queensland University with First class honours and holds the Professional Certificate of Certified Shari’a Advisor and Auditor from the Accounting & Auditing Organisation for Islamic Financial Institutions (AAOIFI). Dr. Lallmahamood is a guest professor in Islamic finance at Paris-Dauphine University and the University of Strasbourg and has published a number of peer review articles & participated in a number of international conferences.

12

ISSUE

ISSUE

12

ISSUE

12

ISSUE

12

IB

Dr. Muniruddeen Lallmahamood

70 __ ISLAMIC BANKER __ ISSUE12 2015 ISSUE12 2015 __ ISLAMIC BANKER __ 71

and profits in the domestic market; whereas Investec Bank (Mauritius) and HSBC Bank (Mauritius) are the top banks in the offshore market. As far as Islamic finance is concerned, products such as Ijarah, Takaful and microfinancing are offered by non-

PROFILE

DR. MUNIRUDDEEN LALLMAHAMOOD

NATIONALITY: Mauritian

QUALIFICATIONS: Among his many educational

qualifications is Doctor in Business Administration

from the University of South

Australia, a Master degree from

Central Queensland University

and a Professional Certificate of Certified Shari’a Advisor and Auditor from the Accounting

& Auditing Organisation for

Islamic Financial Institutions

(AAOIFI).

PROFESSIONAL GOAL: To build a strong foundation for

CBC as a reputable modern

Shari’a compliant bank in the region

FAVORITE SHARI’A SCHOLAR: Dr. Muhammad Daud Bakar / Dr. Osama Al Dereai

INSPIRING ISLAMIC FINANCE BOOK: Understanding Islamic finance by Muhd Ayub

ONE-LINE ADVICE: Strive for the best and be

passionate about everything

you do

What one would describe you? Objective and a problem

solver

What are you most passionate about you?

Broad understanding of the

various cultures, communities

and the world

What is your favourite journey? After travelling

to many of the world, I still

remember the details of the

land journey to perform Umrah

in 1986 from Kuwait.

What is your greatest achievement in life? This is yet to be fulfilled. I believe that there is always

something new to be learnt,

acquired and achieved. I aspire

to write and publish books that would contribute significantly to my area of expertise.

What is your motto in life? Do anything with a conscious mind, understand its impact

on your surroundings and

leave the rest to the Almighty

(tawakul)

ww

w.if

so-a

sso.

com

THIS YEAR WAS CHARACTERISED BY A MAJOR EVENT: THE 11TH ISLAMIC FINANCIAL SERVICES BOARD (IFSB) SUMMIT, THE FIRST OF ITS KIND TO BE HELD IN THE AFRICAN REGION.

banking actors while Mauritius is also the platform for the structuring and domicile of some Shari’a funds. Although Islamic finance business does not make up a significant proportion of the Mauritian financial sector, it is expected to play a bigger role in the future.

MM: As an Acting CEO of Century Banking Corporation (CBC) Mauritius, what are your aspirations for Islamic finance in the last quarter of 2014?DR. MUNIR: For long, Islamic finance has been waiting to take off fully in our beautiful island nation - ever since the Banking Act 2004 was amended in 2007, followed by several other amendments to the legislations and guidelines to incorporate Islamic finance in the Mauritian financial system. The local Islamic finance industry faced some resistance from licensed operators as well as consumers which, in my opinion, is mainly attributable to the word ‘Islamic’.As this year comes to an end, prospects for Islamic finance in Mauritius remain bright and promising. This year was characterised by a major event: the 11th

CHAT WITH MUAT MUBARAKDR. MUNIRUDDEEN LALLMAHAMOOD

12

ISSUE

ISSUE

12

ISSUE

12

ISSUE

12

IB

70 __ ISLAMIC BANKER __ ISSUE12 2015 ISSUE12 2015 __ ISLAMIC BANKER __ 71

Port Louis, capital city of the African island nation - Mauritius

Islamic Financial Services Board (IFSB) Summit, the first of its kind to be held in the African region. This Summit revived hopes, and objectives were set with the fervent willpower to uplift this nascent sector. About the same time, we saw the opening of an Islamic window by Pakistan based Habib Bank. I am personally confident that the year will end on a good note for Islamic finance in Mauritius. At CBC, our goal is to increase our market share in the local market and the region. We are already tapping the corporate segment and small & medium enterprises (SMEs) which predominantly consist of family businesses. This year, the bank is directing considerable efforts towards high net worth individuals (HNWI)through private banking products. The bank also serves international customers and provides bridge financing to foreigners interested in real estate projects in Mauritius.

MM: As one of the key industry leaders you have been actively engaged in many projects, could you brief the important projects that you are handling at the moment?DR. MUNIR: At this stage, my priority is building a highly reputable modern Shari’a compliant bank, which offers top class services to its investment, private banking and international clients and to foster long-lasting relationships. This, in itself, is a big challenge given that we are operating in an environment which is very much accustomed to conventional banking.

MM: You have been working as a consultant in Islamic finance at the Central Bank of Mauritius and also as a regional representative of Bait Al-Mashura Finance Consultations (Qatar), a licensed Shari’a advisory firm, how do you see the conduciveness of the market between

12

ISSUE

ISSUE

12

ISSUE

12

ISSUE

12

IB

72 __ ISLAMIC BANKER __ ISSUE12 2015 ISSUE12 2015 __ ISLAMIC BANKER __ 39

CHAT WITH MUAT MUBARAKDR. MUNIRUDDEEN LALLMAHAMOOD, ACTING CHIEF EXECUTIVE OFFICER OF CBC

Mauritius and the GCC?DR. MUNIR: Trade relationships between GCC and Mauritius are not significant except for Emirates Airline which operates two flights daily for the Mauritius-Dubai route. However, both Mauritius and the GCC are members of the Indian Ocean Rim Association. Mauritius also has tax treaties with Qatar, UAE, Kuwait and Oman, and is currently negotiating a tax treaty with Saudi Arabia. Given all the advantages that Mauritius has to offer (wide network of tax treaties, Islamic banking capabilities, favorable time zone, amongst numerous others), it can potentially become a jurisdiction of choice for GCC countries for investment and trade. Focusing on Africa has been the new agenda recently. This is evident because Mauritius has long trade relationships with Europe via Southern Africa that dates back to the 16th century.

MM: In your view, how do you see the progress of Islamic banking & finance globally? What are the pressing issues and challenges faced by the industry and how can they be resolved?

DR. MUNIR: In my view, we need to comprehend the fact that Islamic finance is acknowledged by many governments and international agencies (such as the World Bank, IMF, OECD and Basel Committee on Banking Supervision). Such a remarkable achievement evidences the exceptional performance and potential of this industry. The next move in Islamic finance, I would say Islamic Banking 3.0. This new phase does not mean a revolutionary approach to the Islamic banking industry: rather, it is about reviving the true essence of Islamic finance. To expound on this, I would say that Islamic banks should be more dynamic and proactive in the real economy instead of focusing only on mobilizing funds.

MM: What is your recommendation for the global Islamic finance industry and how do you see the local Islamic finance industry in 2015?DR. MUNIR: At the global level, we first need more coordination and policy synchronisation between authorities within and across jurisdictions, such as between the government (Ministry of Finance) and the central bank/monetary authority and the securities regulator of a country. Second, we would like to see a coordination and collaboration among the international Islamic agencies namely AAOIFI, IFSB, IDB, IFM and ISRA. Thirdly, the industry is in need of greater harmonisation and convergence across jurisdictions in terms of products and services, practices and systems. However, this could prove to be a daunting task owing to the diversity in Shari’a interpretations and opinions arising from the existence of different schools of thought in the Muslim world and the strive towards becoming the leading Islamic financial hub. I believe that 2015 has surprises in store for the local Islamic finance industry. I am very optimistic that Islamic finance will pick up, slowly but surely, in the next few years in Mauritius. IB

WE FIRST NEED MORE COORDINATION AND POLICY SYNCHRONISATION BETWEEN AUTHORITIES WITHIN AND ACROSS JURISDICTIONS, SUCH AS BETWEEN THE GOVERNMENT (MINISTRY OF FINANCE) AND THE CENTRAL BANK/MONETARY AUTHORITY AND THE SECURITIES REGULATOR OF A COUNTRY. SECOND, WE WOULD LIKE TO SEE A COORDINATION AND COLLABORATION AMONG THE INTERNATIONAL ISLAMIC AGENCIES NAMELY AAOIFI, IFSB, IDB, IFM AND ISRA.

One of the many exotic beaches of Mauritius.