Irish Water: Phase 1 Report Appendices

79

Irish Water: Phase 1 Report Appendices

Transcript of Irish Water: Phase 1 Report Appendices

www.pwc.com/ie Draft

Irish Water: Phase 1 Report Appendices

Irish Water: Phase 1 Report

PwC Page 2 of 79

Table of Contents

Appendix 1: Terms of Reference ......................................................................... 3

Appendix 2: Water Policy Context ...................................................................... 5

Appendix 3: Legislative Summary ..................................................................... 7

Appendix 4: Water Organisation Charts ...........................................................13

Appendix 5: Public Sector Staffing Initiatives ................................................... 17

Appendix 6: Water Staffing .............................................................................. 19

Appendix 7: Review of International Experience ............................................. 20

Appendix 8: Definition of Options .................................................................... 63

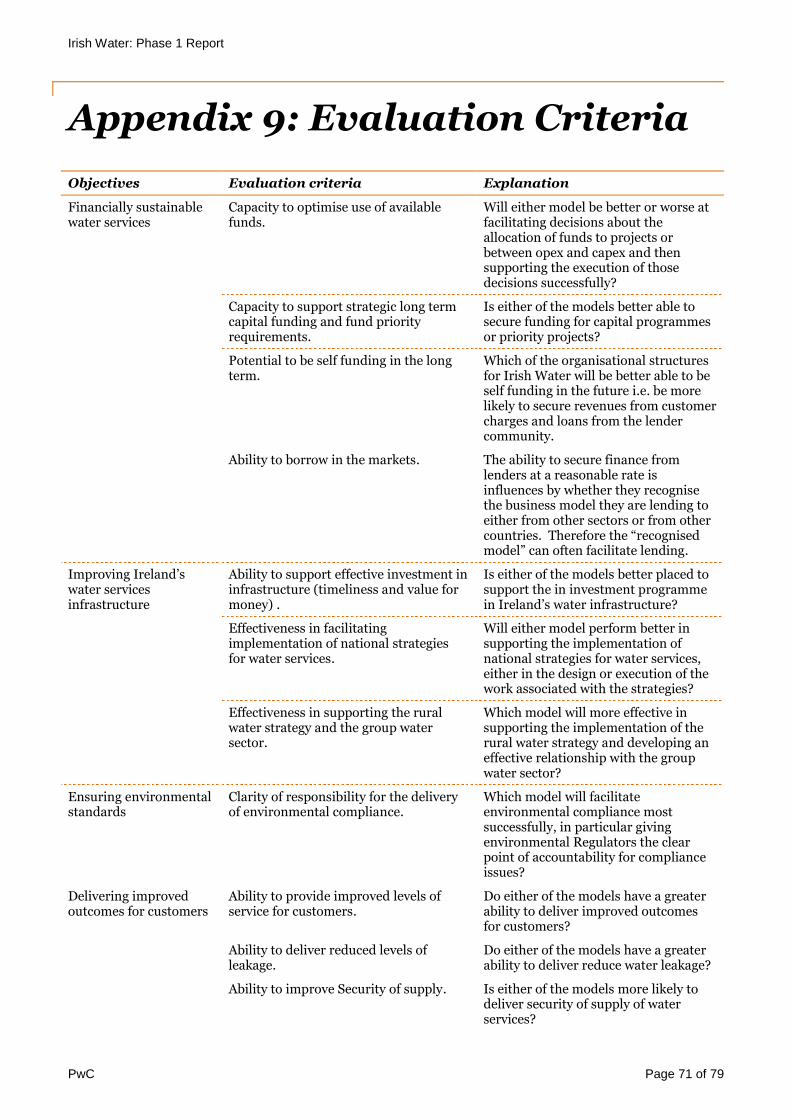

Appendix 9: Evaluation Criteria........................................................................ 71

Appendix 10: Performance Data for UK Water Companies ............................ 74

Appendix 11: Assessment of Options ................................................................. 76

Irish Water: Phase 1 Report

PwC Page 3 of 79

Appendix 1: Terms of Reference

Consultancy Services for Water Utility

Introduction The 34 city and county councils are responsible for the production, distribution and monitoring of drinking water from over 900 public water supplies and for the provision of public waste water services. The councils are also responsible for the supervision of any group and private water supplies in their areas and for the carrying out of various water-related inspection and enforcement activities.

The Programme of Financial Support for Ireland agreed between the Government and the EU/IMF requires, inter alia, that by the end of 2011, the Government will have undertaken an independent assessment of the transfer of responsibility for water services provision from the local authorities to a water utility. The Programme for National Recovery 2011-2016, indicates that the Government will create Irish Water, a new State company that will take over key water/waste water functions from the 34 existing local authorities.

This independent assessment, will guide the implementation of this strategy, identifying the optimum role and functions of the proposed company. Against the backdrop of the Government decision to establish Irish Water, the assessment should determine the most effective assignment of functions and structural arrangements for delivering high quality competitively priced water services to customers (domestic and non-domestic) and for infrastructure provision.

The study will be undertaken in two parts. Part I to identify the optimum organisational structure and Part II to examine in detail the legal, financial and organisational issues together with an implementation timetable.

Phase I – Options Consideration 1. The deliverable for Phase I of the study is an interim report indicating the recommended optimal

organisational form for water services delivery in Ireland, distinguishing if appropriate, between short-term, medium and longer term options.

2. In examining the optimal organisational structure for the sector, the study should have regard to the proposed structural reforms impacting on the sector, including the commitments in the Programme for National Recovery 2011-2016 including NewERA, the introduction of a fair funding model comprehending the metering of households and a charging regime to include a free allowance, the establishment of an independent Economic Regulator for water, the recommendations of the Local Government Efficiency Review Group and of the Value for Money Study of the Water Services Investment Programme1 as well as the governance requirements for the implementation of the River Basin Management Plans.

3. The study should consider two principal forms of potential company structure for Irish Water:

A water company which would be a self-financing water utility in a regulated environment, responsible for operation, maintenance and investment in all water services infrastructure, customer billing, charging; and

A company charged mainly with investment in the sector (strategic planning, delivery of projects of a regional/national priority, national metering programme) with local authorities operating as agents of the company, retaining their operational responsibilities and for delivery of smaller scale investment.

1 Unpublished – and outline of this report is attached at Appendix II

Irish Water: Phase 1 Report

PwC Page 4 of 79

The study should contrast these organisational forms, or variants thereof, with current arrangements across a number of parameters e.g. governance, value for money, financial viability, statutory compliance, efficiency, level of service, cost to consumers, infrastructure investment; leakage rates etc. Relevant examples of best practice internationally should be outlined. The examination should involve a SWOT analysis of the current delivery structures, including an examination of the performance of local authorities in recent years in the provision of water services - based largely on published information, including financial data, environmental reports (including inspection and enforcement activities) and other available service indicators.

4. The resulting recommendation should provide a broad indication of the role and functions that Irish Water should have and the rationale for assigning these functions to the company (e.g. water services infrastructure delivery, roll-out of metering programme, operation of existing plant, ownership of assets, implementation of river basin management plans, etc). The review should also consider the possibility/desirability of assigning responsibility for water services provision, or part thereof, to an existing state agency. The review will need to have regard to the outcome of a cost-benefit analysis of the funding options for the metering programme being carried out by the Department which is to be completed by end-April 2011.

Phase II – Implementation Strategy Phase II of the study will focus on the detailed implementation issues involved in the creation of a new company in line with recommendations made in Phase I of the study. It will recommend transitional arrangements together with a timeframe, taking account of the need for continued delivery of a critical public service during and following a restructuring process.

This will involve an examination of the issues that would arise from the consolidation of water services provision from the local authorities to a water company. This should include consideration of:

governance and organisational structures, including the relationship of the company with the Department, the proposed water Regulator, the Environmental Protection Agency, regional delivery structure, local authorities and the rural water sector, and staffing requirements;

the approach to future infrastructural delivery;

the approach to service delivery, having regard to, inter alia, the impact of regulation, environmental/public health standards and technological advances on service requirements;

primary legal issues arising including issues of ownership and control of assets, and an outline of main

legislative changes required to give effect to the recommended organisational form;

funding requirements of a new company, including the scope for accessing private finance, valuation of existing water services infrastructure and any further options of relevance to revenue generation; and

the re-assignment of the inspection and enforcement functions which currently rest with local authorities.

Irish Water: Phase 1 Report

PwC Page 5 of 79

Appendix 2: Water Policy Context

The Programme for Government contains a number of commitments in relation to reforming the institutional arrangements governing the water sector in Ireland. In addition, in preparing our report, we also had regard to the commitments in the agreement with the EU/IMF, the report of the Review Group on State Assets and Liabilities, and other government policies which are directly relevant and important in this regard.

Programme for Government The Programme for Government, published in March 2011 provides:

“To achieve better quality water and environment we will introduce a fair funding model to deliver clean and reliable water. We will first establish a new State owned water utility company to take over responsibility from the separate local authorities for Ireland’s water infrastructure and to drive new investment. The objective is to install water meters in every household in Ireland and move to a charging system that is based on use above the free allowance”.

There is a commitment to prepare a new National Development Plan for the period 2012-2017 setting down the public investment priorities over the period and this is expected to be published in September.

In order to ensure that public enterprise plays a full role in Ireland’s economic recovery, the Government has committed to creating a holding company to manage the state’s holdings of the semi-states, and to coordinate investment in key priority areas identified by the Government, including energy, water and forestry.

There is to be a Strategic Investment Bank that will become a provider of finance to large capital projects, a conduit for venture capital and a lender to SMEs.

New Economy and Recovery Authority (NewERA) The Programme for Government also contains the following which are relevant to the water sector:

The Government will put in place a parallel, commercially-financed investment programme in key networks of the economy to support demand and employment in the short-term, and to provide the basis for sustainable, export-led jobs and growth for the next generation.

Under the NewERA plan, streamlined and restructured semi-states will make significant additional investments, over and above current plans, over the next four years in “next generation” infrastructures in energy, broadband, forestry and water. These investments – and the accompanying semi-state restructuring process – will be financed and pro-actively managed by a New Economy and Recovery Authority (NewERA), which will absorb the National Pension Reserve Commission. Subject to finalisation in the National Development Plan, we propose to make additional investments in the following areas:

A new water network: The new Government will create Irish Water, a new State company that will take over the water investment maintenance programmes of the 34 existing local authorities. It will supervise and accelerate the planned investments needed to upgrade the State’s inefficient and leaking water network which proved so unreliable during the recent harsh weather conditions.

Irish Water: Phase 1 Report

PwC Page 6 of 79

EU/IMF Also of importance is the Programme of Financial Support for Ireland agreed between the Government and the EU/IMF( December 2010). The Programme requires, inter alia, that by the end of 2011, the Government will have undertaken an independent assessment of the transfer of responsibility for water services provision from the local authorities to a water utility.

The assessment is required to determine the most effective structure(s) for delivering high quality competitively priced water services to customers (domestic and non-domestic) and for infrastructure provision. In particular, the review is required to consider whether a national water utility would be more efficient and cost effective than the existing implementation and operation structures across the 34 city and county councils. This review is also to cover the legal framework and financial and economic dimensions as well as organisational issues, having regard to international experience and relevant examples of best practice.

Report of the Review Group on State Assets and Liabilities The report of Review Group on State Assets and Liabilities was issued by the Government in April 2011 and a large number of recommendations are being variously considered. The report contained the following references to the water sector:

“In 2009, the Special Group on Public Service Numbers and Expenditure recommended that the Irish water industry should be comprehensively restructured. The National Recovery Plan 2011-2014 provides for the introduction of a scheme for metering and charging for domestic water. A commercialised water industry that might eventually emerge from this reform would be a natural monopoly and would have to be subject to economic regulation.

It has been suggested that the Environmental Protection Agency (EPA), which currently has responsibility for water quality and compliance with EU directives, would be a suitable body to undertake this task. The Review Group feels that such an aggregation of responsibilities would not be appropriate and that responsibility for economic regulation in the water industry should be assigned to a body distinct from the EPA. In Northern Ireland, a single Regulator is responsible for electricity, gas and water. The technical challenges of regulation in these three sectors coincide to a large degree.

The Review Group recommended that, in the event that a customer financed water industry structure emerges, this monopoly should be regulated through expanding the role of the Commission for Energy Regulation rather than through the establishment of yet another sector Regulator."

The report also makes a number of recommendations in relation to economic regulation which are also relevant to designing new institutional arrangements for the water sector. The Group paid particular attention to questions of market design and the Regulatory reforms necessary to underpin competition and appropriate levels of investment, especially in those sectors where there are natural monopolies subject to statutory regulation. The water sector is also relevant in this regard. The Group indicated that recommendations are intended to enhance the competitiveness of the sectors of the economy where state bodies are active. They also recommended:(1) Changes in the governance of state bodies while they remain in public ownership to enhance efficiency and performance and (2) A review of Regulatory arrangements and a new structure for the oversight of Regulatory agencies.

At time of writing ,various measures to give effect to the recommendations in the Review Group’s report were being considered which when settled will further influence the shape of the sector.

Other Relevant Government Policies Other relevant Government policies on the public service relate to pay and numbers. Under these policies, any new agency will have to be set up in a way that ensures that:

No additional posts are created in the public service

There is no additional cost on the Exchequer.

Irish Water: Phase 1 Report

PwC Page 7 of 79

Appendix 3: Legislative Summary

1. Legislative Framework in respect of the Water Services Sector

The current legislative framework in respect of the water services sector is outlined briefly in this Appendix.

2. EU Legislative Framework

There is a comprehensive range of legislative provisions at EU level that require member states to implement national Regulatory frameworks for the planning and delivery of water services.

2.1 The Water Framework Directive

The Water Framework Directive (2000/60/EC) (the “Framework Directive”) establishes a framework for long-term sustainable water management through focusing on integrated planning and promoting sustainable water use.

A key innovation of the Framework Directive is the focus on river basins and requirements for river basin management plans, rather than a focus on arbitrary administrative or political boundaries. It applies to all waters, including rivers and lakes, estuaries (transitional waters), coastal waters and groundwater, and their dependent wildlife and habitats. The Framework Directive provides an overarching framework and programme to deliver long-term protection of water, and its objectives include the improvement and maintenance of water bodies of lesser status attaining “good status” by 2015, and those retaining good status or better where such status exists at present.

The Directive was transposed into Irish law by the European Communities (Water Policy) Regulations 2003, as amended (the “2003 Water Regulations”).

Key aspects of the Water Framework Directive include:

use of river basin management plans – river basin districts comprise the administrative areas’ for co-ordinated implementation of the Framework Directive. A total of eight river basin districts having been identified for the island of Ireland, three of which share cross-border waters with Northern Ireland, four of which are within the state of Ireland and one is entirely within Northern Ireland;

identification of an appropriate competent authority with responsibility for making river basin management plans setting out water quality objectives for each water body within the river basin district. This role is assigned to the constituent councils of each river basin district by the 2003 Water Regulations; in each case with one council designated to act as the coordinating authority for that district;

providing for a maximum of three river basin planning cycles up to 2027 to achieve the water quality objectives specified; and

requiring each river basin district to establish a programme of measures to ensure the water quality

objectives of the river basis management plans are met.

Irish Water: Phase 1 Report

PwC Page 8 of 79

2.2 The Drinking Water Directive

The Drinking Water Directive (98/83/EC) and related national regulations, set out the quality and monitoring requirements for portable water supplies. The objective of the Drinking Water Directive is to protect human health from the adverse effects of any contamination of water intended for human consumption by ensuring that it is wholesome and clean. It applies to water intended for drinking, cooking, food preparation or other domestic purposes supplied from a distribution network, from a tanker, in bottles or in containers which must comply with the standards set out in the Drinking Water Directive.2 Water providers have an information and advisory duty towards the public. Member States must monitor the quality of the drinking water mainly at the tap inside private and public premises and report the results at three yearly intervals to the EC.

The Drinking Water Directive is transposed into Irish law by the European Communities (Drinking Water) (No. 2) Regulations, 2007 (S.I. No 278 of 2007) (the “Drinking Water Regulations”). These regulations prescribe quality standards to be applied and related supervision and enforcement procedures in relation to supplies of drinking water, including requirements as to sampling frequency, methods of analysis, the provision of information to consumers and related matters. Under the Drinking Water Regulations a water service authority must:

ensure any water it provides is wholesome and clean and meets prescribed quality standards;

measure compliance with the parametric values in accordance with a prescribed sampling and analysis regime;

monitor compliance of all drinking water supplies in its functional area ; and

take appropriate remedial action (or ensure that action is taken) to restore the quality of non-compliant supplies.

2.3 Urban Waste Water Treatment Directive

The Urban Waste Water Treatment Directive (91/271/EEC) (“Waste Water Directive”) and related national regulations prescribe the collecting systems and treatment standards for waste water from centres of population based on the size of the centres and the sensitivity of the receiving waters to which treated waste water and storm overflows discharge. It requires biennial reporting to the EC on the disposal of waste water and sludge. Two key aspects of the Waste Water Directive are the requirement to have secondary treatment of wastewater in place in agglomerations above a certain size, and the need to provide nutrient reduction in addition to secondary treatment for discharges to designated sensitive waters.

The Waste Water Directive was transposed into Irish law by the Urban Waste Water Treatment Regulations 2001 (S.I. No 254 of 2001), as amended. These Regulations set specific standards to be achieved for waste water treatment plants, and set out a monitoring regime by local authorities of discharges from waste water treatment plants including the transmission of results to the EPA.

2.4 Other relevant European legislation

In addition to the directives mentioned above, there are a range of other European directives which also impact on the planning and delivery of water services in Ireland, including the Groundwater Directive (80/68/EEC)3, the Shellfish Directive (2006/113/EC), the Nitrates Directive (91/676/EEC), the Bathing Water Directive (2006/7/EC), the Dangerous Substances Directive (2006/11/EC), the Freshwater Fish Directive (2006/44/EC), the Sewage Sludge Directive (86/278/EEC), the Habitats Directive (92/43/EEC) and the Birds Directive (2009/147/EC).]

2 It does not apply to supplies serving less than ten cubic meters or 50 people unless the water is supplied as part of commercial or public

activity. Bottled spring and mineral waters are dealt with separately under Directive 80/777/EC and subsequent amendments relating to

the exploitation and marketing of natural mineral waters.

Irish Water: Phase 1 Report

PwC Page 9 of 79

3. Current national legislative framework

The Water Services Act 2007 (the “2007 Act”) sets out a legislative framework governing functions, standards, obligations, and practices in relation to planning, management and delivery of water services and practices in relation to planning, management and delivery of water services, waste water collection and treatment services.

3.1 Roles under the national legislative framework

The 2007 Act confers powers and responsibilities on different persons.

Role of the Minister under the 2007 Act

Under the 2007 Act, the Minister for Environment, Community and Local Government4 (the “Minister”) has a general duty to facilitate the provision of safe and efficient water services and water services infrastructure. As part of this high-level duty, the Minister has overall responsibility for:

the supervision and monitoring of the performance by water services authorities of their functions under the 2007 Act; and

the planning and supervision of investment programmes for the provision of water services.

The 2007 Act sets out the principles and policies to which the Minister shall have regard and of which he must take full account in carrying out his or her duties under the 2007 Act, including the principle of recovery of the costs of water services as provided for in the Framework Directive, development plans, regional or spatial guidelines and waste management plans and relevant river basin management plans or programmes of measures under the Framework Directive.

The 2007 Act confers a number of powers on the Minister to facilitate the provision of safe and efficient water services and water services infrastructure, including the power to:

provide guidance to water services authorities in relation to the performance of their functions under the 2007 Act;

to monitor and compare water services authorities in carrying out their functions;

specify standards, issue guidelines, codes of practice or directions in relation to the provision of water services (including in relation to pricing mechanisms and procurement) and grant or refuse approval to water services authorities to award contracts;

direct a water services authority in relation to, among other things, the drawing up or implementation of water services strategic plans, acquisition of land (for the purposes of its functions under the 2007 Act), procurement of water services infrastructure; the provision of water services jointly with one or more other water services authorities and licensing of water services providers; and

make regulations to require water services authorities to provide specified water services to specified classes of “agglomerations” (areas of sufficiently concentrated population or economic activities), areas or consumers.

4 Previously referred to as the Minister as the Minister for Environment, Heritage and Local Government.

Irish Water: Phase 1 Report

PwC Page 10 of 79

Role of water services authorities under the 2007 Act

Authority to provide water services is given to Ireland’s 34 City and County Councils (29 County and 5 City), each of which is designated as a water services authority under the 2007 Act.

A water services authority may provide water services, in accordance with prescribed standards and public policy, for domestic and non-domestic requirements in its functional area. Alternatively, water services authorities may, subject to the requirements of the 2007 Act and, if applicable, the State Authorities (Public Private Partnership Arrangements) Act 2002, enter into an agreement or arrangement with another person in relation to the provision of water services in part or all of its functional area. The 2007 Act also authorises two or more water services authorities to enter into an agreement or arrangement for the purpose of one or more of them or jointly carrying out any or all of their functions under the 2007 Act, in any or all of their respective areas or any part of them.

While the exercise of the powers conferred on water services authorities is generally at the discretion of the individual authority, water services authorities must comply with directions issued by the Minister and any regulations prescribed by the Minister requiring a water services authority to provide specified water services to specified agglomerations, areas or consumers.

Some important features of the 2007 Act relating to water services authorities are as follows:

water services authorities must ensure that their services are provided in a manner consistent with national policy and in accordance with prescribed standards. They are required to take full account of specified aspects of public policy when exercising powers, including planning and development, sustainable management of water resources, protection of human health and the environment and national and EU Regulatory requirements including a river basin management plan or programme of measures under the Water Framework Directive;

it provides a range of powers for a water services authority, such as metering, monitoring of water services, acquisition of premises and wayleaves and provides water services authorities with the power to deliver water supplies, i.e. to abstract water, store it, treat it and supply it for drinking or any other purpose, or to purchase it for onward supply;

it also provides for the provision, operation or maintenance of sewers, waste water collection networks and waste water treatment plants by water service authorities;

it provides for a strategic planning process to be carried out by water services authorities which when commenced, is intended to facilitate sustained improvement in the management and operation of water services infrastructure; and

it confers powers in relation to the licensing and supervision of group water schemes. In this context it should be noted that under the Drinking Water Regulations water services authorities supervise all other drinking water supplies in their functional area.

Role of the EPA in relation to water services

In addition to the general supervisory function conferred on the Minister under the 2007 Act, the EPA is tasked with:

reporting to the European Commission for the purpose of the Water Framework Directive and other coordination functions under the 2003 Water Regulations;

monitoring compliance of water intended for human consumption supplied by a “sanitary authority”

(meaning, since the enactment of the 2007 Act, a water services authority), or any person acting jointly with it or on its behalf, with the Drinking Water Regulations. Key features of the Drinking Water Regulations in this regard include that monitoring of all supplies is a function of water services authorities, but their monitoring programmes are subject to approval by the EPA, the EPA’s powers of

Irish Water: Phase 1 Report

PwC Page 11 of 79

enforcement to ensure that water services authorities comply with their monitoring obligations and the powers of the EPA and the water services authorities to intervene directly in the case of non-compliance to carry out remedial works and to recover costs from the supplier;

licensing or certifying discharges to aquatic environment from sewage systems owned, managed or operated by water services authorities under the Waste Water Discharge (Authorisation) Regulations 2007;

licensing trade discharges to waters under the Environmental Protection Agency Act 1992 (the “EPA Act”) and implementing regulations. Integrated Pollution Prevention Control (IPPC) licenses are issued by the EPA for designated categories of industry under the EPA Act and implementing regulations which includes trade effluent discharges from these industries. Water services authorities’ license discharge of trade effluents from non-IPPC licensed industries to public sewers within their functional area under the Water Pollution Acts.

Other water services providers under the 2007 Act

The 2007 Act contemplates the introduction of a licensing regime in respect of water services provided by persons other than a water services authority.5

Currently, any person can provide water services in Ireland provided that the water services provided comply with the applicable national and European quality standards6. On or after such date as the Minister may prescribe by regulations, a person (other than a water services authority or a person acting jointly with it or on its behalf) may not provide water for human consumption from a tanker or otherwise provide water services, except in accordance with a water services licence. An exception is made for bottled water provided in the ordinary course of business. Additionally, the Minister may, by regulations, specify a threshold below which a water services licence will not be required, either based on numbers of people to which water services are provided or a volumetric equivalent.

It will be an offence for any person other than a water services authority to provide services other than in accordance with the terms of a water services licence.

The water services authorities are designated as the licensing authorities and the 2007 Act prescribes the matters to which water services authorities must have regard when granting or reviewing a water services licence.

3.2 Other applicable national legislation

A wider national framework

Water services authorities operate within the broader framework of a range of national legislation which also impact on the planning and delivery of water services, which include:

the Planning and Development Act 2000, which provides for planning and sustainable development;

European Communities (Environmental Assessment of Certain Plans and Programmes) Regulations 2004 and the Planning and Development (Strategic Environmental Assessment) Regulations 2004 which require that the environmental consequences of certain plans and programmes, including developments plans and local area plans are identified and assessed during their preparation and before their adoption;

5 The relevant sections of the 2007 Act which provide for licensing of other water services providers have not yet been commenced.

6 For example, if water is supplied for human consumption it must be “wholesome and clean” and meet the requirements of the European

Communities (Drinking Water) (No. 2) Regulations 2007. However there is an exemption in relation to a supply of water which constitutes an individual supply of less than 10 cubic metres a day on average or serves fewer than 50 persons, and is not supplied as part of a commercial or public activity. An exemption also exists where a supply of water is used exclusively for purposes in respect of which the relevant supervisory authority is satisfied that the quality of the water has no influence, either directly or indirectly, on the health of the consumers concerned.

Irish Water: Phase 1 Report

PwC Page 12 of 79

the Waste Management Acts 1996 and 2001 and related regulations which prescribe the legal framework for the management of waste, for example the treatment and disposal of sludges arising from water and waste water treatment plants; and

Local Government (Water Pollution) Acts, 1977 and 1990 and supporting regulations which set out key provisions for the prevention of water pollution.

Other national legislation

Other legislation (much of which is transposing European legislation), which inform the statutory functions and powers of water services authorities, include the European Communities Environmental Objectives (Groundwater) Regulations, 2010, the European Communities (Good Agricultural Practice for Protection of Waters) Regulations 2010, the European Communities Environmental Objectives (Surface Waters) Regulations 2009, the Waste Water Discharge (Authorisation) Regulations 2007; the European Communities (Waste Water Treatment) (Prevention of Odours and Noise) Regulations 2005, the Urban Waste Water Treatment Regulations 2001 and 2004, the Waste Management (Use of Sewage Sludge in Agriculture) (Amendment) Regulations 2001, the Waste Management (Use of Sewage Sludge in Agriculture) Regulations 1998 and the European Communities (Quality of Surface Water Intended for the abstraction of Drinking Water) Regulations 1989.]

Irish Water: Phase 1 Report

PwC Page 13 of 79

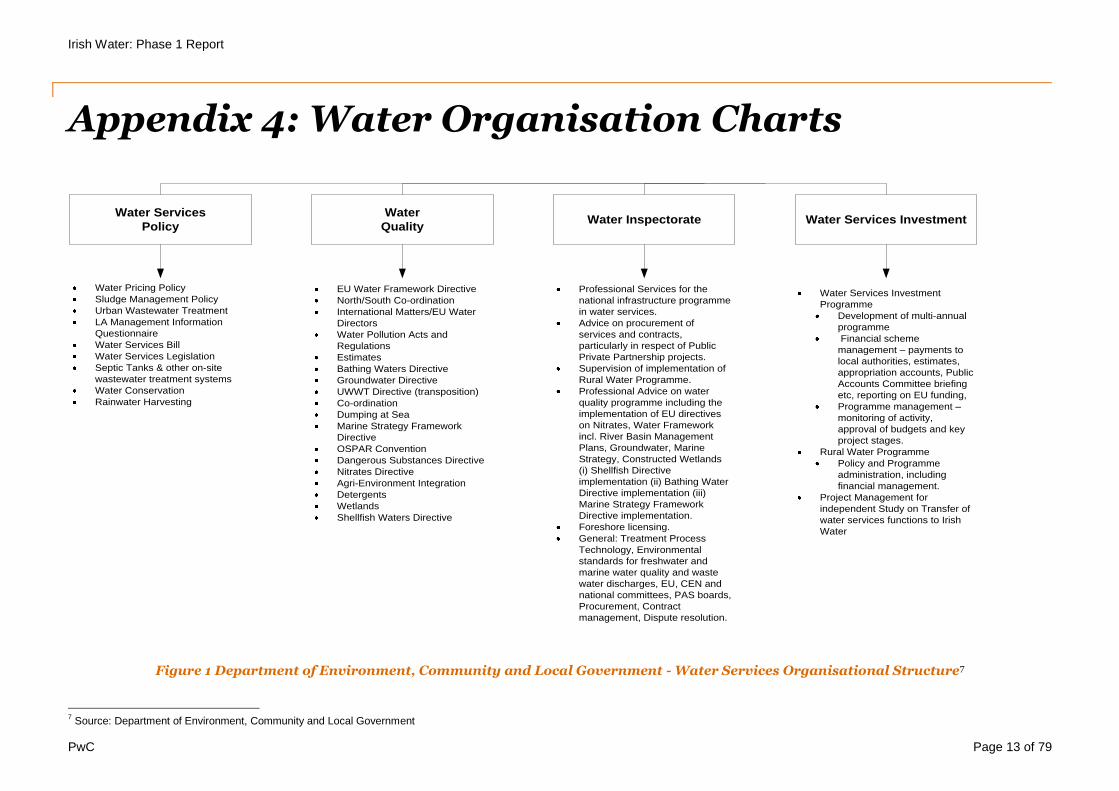

Appendix 4: Water Organisation Charts

Water Services

Policy

Water

QualityWater Inspectorate Water Services Investment

Water Pricing Policy

Sludge Management Policy

Urban Wastewater Treatment

LA Management Information

Questionnaire

Water Services Bill

Water Services Legislation

Septic Tanks & other on-site

wastewater treatment systems

Water Conservation

Rainwater Harvesting

EU Water Framework Directive

North/South Co-ordination

International Matters/EU Water

Directors

Water Pollution Acts and

Regulations

Estimates

Bathing Waters Directive

Groundwater Directive

UWWT Directive (transposition)

Co-ordination

Dumping at Sea

Marine Strategy Framework

Directive

OSPAR Convention

Dangerous Substances Directive

Nitrates Directive

Agri-Environment Integration

Detergents

Wetlands

Shellfish Waters Directive

Professional Services for the

national infrastructure programme

in water services.

Advice on procurement of

services and contracts,

particularly in respect of Public

Private Partnership projects.

Supervision of implementation of

Rural Water Programme.

Professional Advice on water

quality programme including the

implementation of EU directives

on Nitrates, Water Framework

incl. River Basin Management

Plans, Groundwater, Marine

Strategy, Constructed Wetlands

(i) Shellfish Directive

implementation (ii) Bathing Water

Directive implementation (iii)

Marine Strategy Framework

Directive implementation.

Foreshore licensing.

General: Treatment Process

Technology, Environmental

standards for freshwater and

marine water quality and waste

water discharges, EU, CEN and

national committees, PAS boards,

Procurement, Contract

management, Dispute resolution.

Water Services Investment

Programme

Development of multi-annual

programme

Financial scheme

management – payments to

local authorities, estimates,

appropriation accounts, Public

Accounts Committee briefing

etc, reporting on EU funding,

Programme management –

monitoring of activity,

approval of budgets and key

project stages.

Rural Water Programme

Policy and Programme

administration, including

financial management.

Project Management for

independent Study on Transfer of

water services functions to Irish

Water

Figure 1 Department of Environment, Community and Local Government - Water Services Organisational Structure7

7 Source: Department of Environment, Community and Local Government

Irish Water: Phase 1 Report

PwC Page 14 of 79

ProductionNetwork

Management

Maintenance/

Administration

Planning &

Asset

Management

Mainlaying

& Projects

Support

Systems

Ballymore

Eustace

(WTP)

Water Quality

Needs

Assessment

Forward

Planning

Pressure

Control and

Distribution

Demand and

Network

Management

Non-

Domestic

Metering

Network

Modelling

Maintenance

North City

Maintenance

South City

Maintenance/

Trades

Fleet

Management

Vocational

Training

3rd

Party Claims

Head Office

Building

Management

Administration

Local Admin

Health and

Safety

Planning

Development

Control

10 day GIS

Records

GIS

Records

Plumbing

Inspectors

Asset

Management

Mainlaying

Licence Work

Stores/

Materials

Fitters shop

Marrowbone

Lane Depot

Telemetry

GIS Systems

PC systems

Instrumentati

on

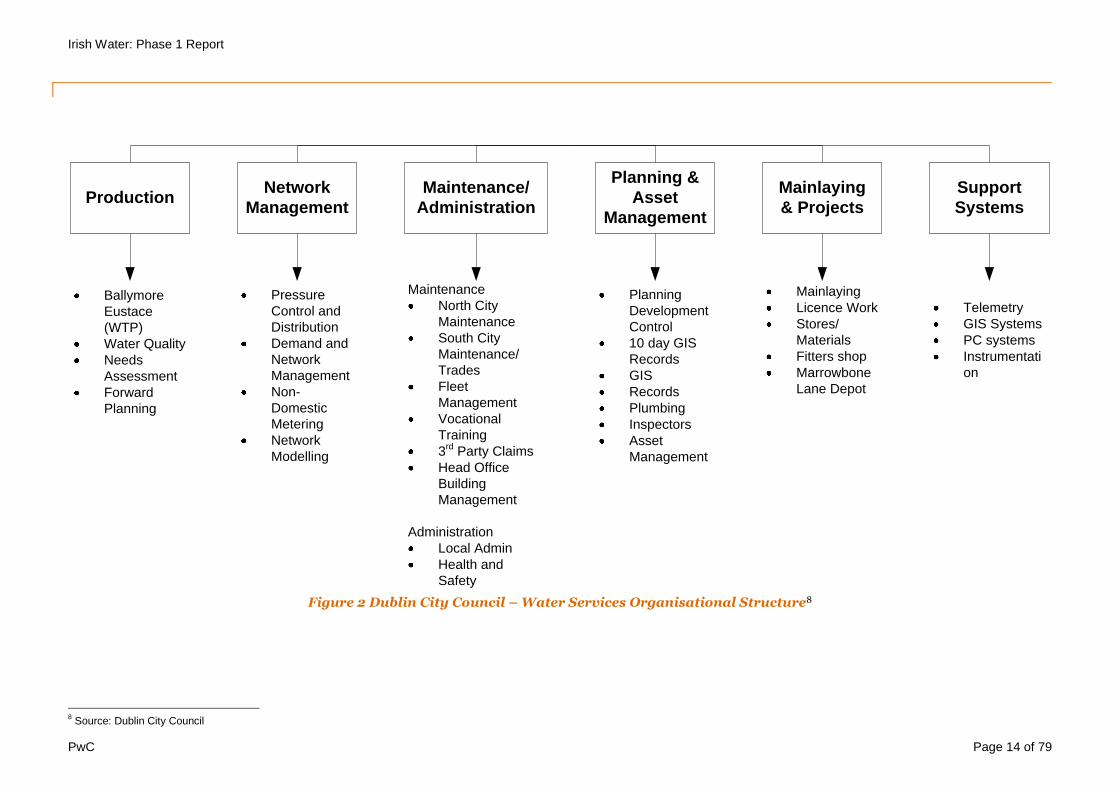

Figure 2 Dublin City Council – Water Services Organisational Structure8

8 Source: Dublin City Council

Irish Water: Phase 1 Report

PwC Page 15 of 79

Waste Water

Treatment

Network

Management

Planning

Service

Pollution

Control

Mechanical

SupportMainlaying

Manage

operations

contract

Maintenance

of public

network

River

cleaning

Rodent

Control

Road Gully

cleaning

Emergency

flood

response

Planning

applications

Development

Control

Policy

development

GDSDS

model

IT

EPA licence

ERBD

RMCEI

FOG

Trade

effluent

licences

Pollution

incidents

Flow

monitoring

Rainguages

Consolidated

charges

Tanker waste

Emergency

planning

Pumping

stations

Drainage

fleet

GPS

Signage

New sewers

Repairs to

pipes/gullies/

manholes

Minor flood

relief

schemes

Local

Admin

Senior

management

Health and

safety

Staff Training

Secretariat

Customer

Relations

Strategic

Planning &

Project

Management

Corporate

Support

WSIP

Project

support

Flood

Resiliance

Project

management

Design

ERBD

regional

coordination

PMDS

Corp.

emergency

planning

Project

procurement

Admin

Finance

HR

Legal

IT

CRM

Facilities

Fleet mgt.

Procurement

Rates

Loan

Charges

Central

Laboratory

Service

Support

Bad Debts

Accident/

Liability

Claims

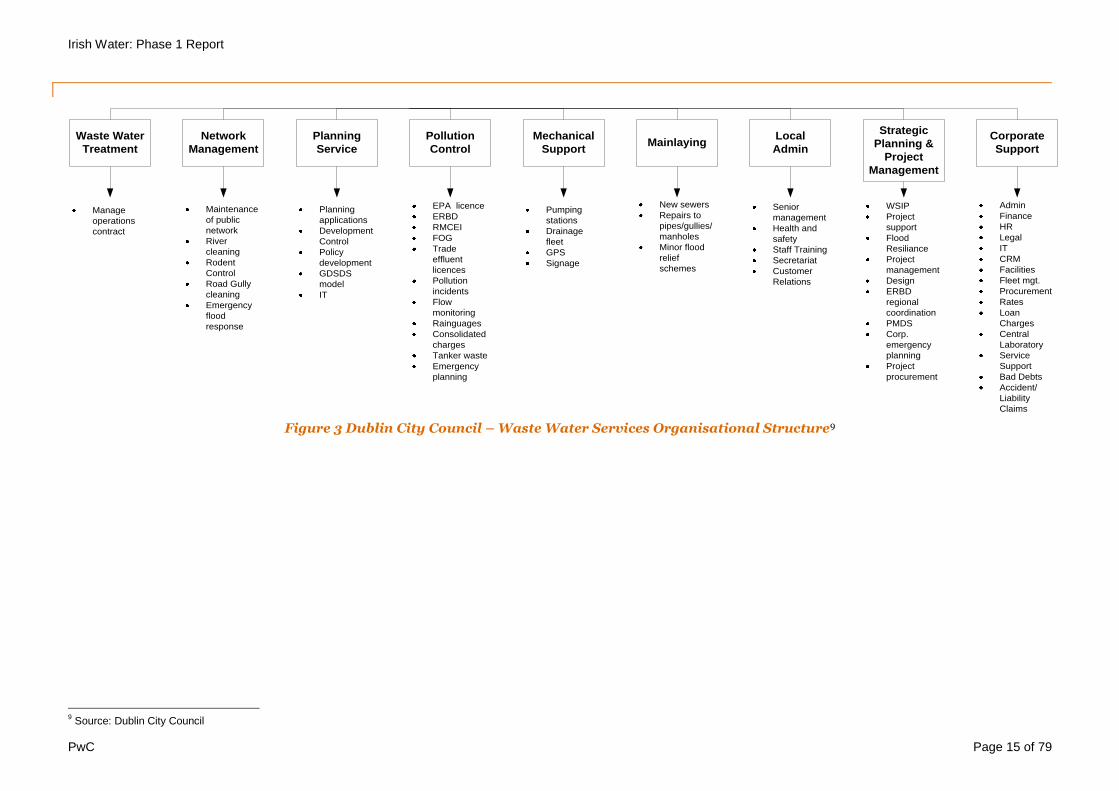

Figure 3 Dublin City Council – Waste Water Services Organisational Structure9

9 Source: Dublin City Council

Irish Water: Phase 1 Report

PwC Page 16 of 79

Capital Maintenance

Water

Services

Investment

Programme

Rural Water

Capital

Programme

Plant

Management

Water

Conservation

(incl. leak

detection)

Caretaking

Rural Water

Programme (incl.

Small Schemes

Water Metering

Water and Waste

Water

Laboratory/

Testing

Administration

Capital and

Maintenance

Programme

administration

Water Charges &

Collection

Rural Water

Administration

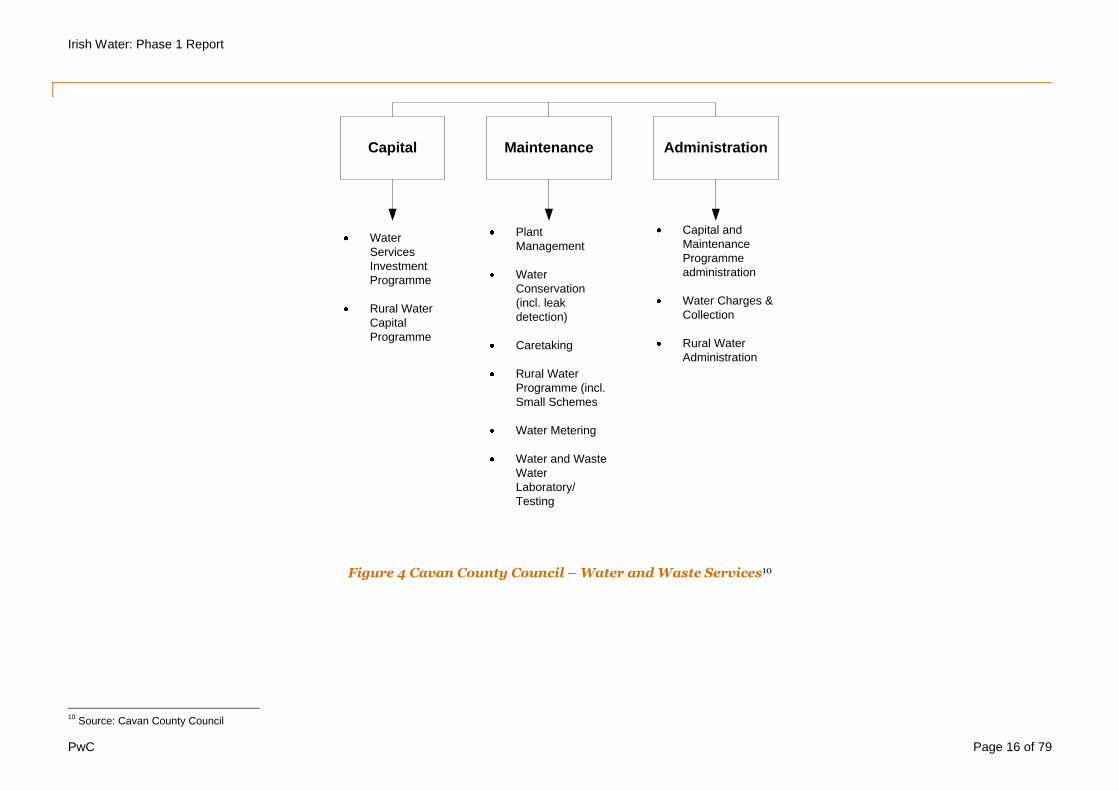

Figure 4 Cavan County Council – Water and Waste Services10

10

Source: Cavan County Council

Irish Water: Phase 1 Report

PwC Page 17 of 79

Appendix 5: Public Sector Staffing Initiatives

National and Local Government Initiatives to Reduce Staffing Costs and Improve Efficiencies Recent National and Local Government initiatives to reduce staffing costs and improve efficiencies include:

Suspension of Public Sector pay increases under “Towards 2016 – Review and Transitional Agreement” (September 2008);

Application of a pension levy for all public sector employees (March 2009);

Introduction of a moratorium on recruitment and promotion within the Public Service (March 2009);

Introduction of the Incentivised Scheme for Early Retirement (ISER) (April 2009);

Introduction of the Incentivised Career Break Scheme (September 2009)

The Public Sector Agreement 2010-2014 (June 2010); and

The Local Government Efficiency Review Group’s report and recommendations (July 2010).

The Pension Levy was introduced in March 2009 via the Financial Emergency Measures in the Public Interest Act 2009, which was originally enacted by the Oireachtas in February 2009. It applies to all persons in receipt of a government pension and is payable on all taxable income paid to that person from public funds. The rates at which the levy was charged at were revised in July 2009.

The Moratorium on Recruitment and Promotion with the Public Service was introduced in March 2009. The Moratorium provides for the filling of vacancies through staff redeployment and, in exceptional circumstances, through recruitment. Under both scenarios the sanction of the Minister for Finance is required.

The Incentivised Career Break Scheme (ISER) ISER was announced in April 2009. The purpose of the ISER was “to facilitate the permanent, structural reduction in the numbers of staff serving in the civil service, local authorities, health sector and non-commercial state bodies, with associated restructuring of organisation and operations, in as timely a manner as possible.” The scheme was open from May to September 2009.

The Public Sector Agreement (aka “Croke Park Agreement”) sets out a series of undertakings between the Public Service and the Government designed to “ensure that the Irish Public Service continues its contribution to the return to economic growth and economic prosperity to Ireland, while delivering excellence to the Irish People” 11. Chapter 5 of the Agreement relates to Local Government. Some key points made in the Agreement in relation to this sector include:

Rationalisation of State Agencies within the Local Government sector will be crucial in reducing internal boundaries and simplifying the delivery of services. There is also an expectation that there should be greater uptake of shared services, in particular in the areas of finance, payroll and HR. The objective of such organisational restructuring is to promote coherency in policy making and service delivery and to realise cost savings. 12

An agreed redeployment scheme is also set out. The scheme aims to absorb surplus staff across the

sector and provide career development opportunities for volunteering staff. In this regard, the Agreement states that “extremely flexible redeployment arrangements must be viewed as the corollary to arrangements that do not provide for compulsory redundancy”13. The specific terms of redeployment are also set out in the Agreement.

11

Public Service Agreement – 2010-2014, June 2010, page 2 12

Public Service Agreement – 2010-2014, June 2010, page 35 &36 13

Public Service Agreement – 2010-2014, June 2010, page 38

Irish Water: Phase 1 Report

PwC Page 18 of 79

With regards to improving productivity, the Agreement states “Better management and standardisation of annual and sick leave, and family friendly policies, including flexitime, will be necessary to manage continuity of service and peak demands and to effect pay bill savings. Other flexibility is possible through eliminating demarcation.”14

The development and implementation of a competency framework for all grades in Local Authorities and the recognition of performance (both good and poor) is also recommended.

The Local Government Efficiency Review Group was asked to review the cost base, expenditure of and numbers employed in local authorities. The Group reported its findings in July 2010. A selection of the report’s staffing and organisational related points are listed below:

The average Local Authority staffing ratio per 1000 population is 7.6 with urban authorities having higher staffing levels. The Review Group suggested that “A possible approach to realising such efficiencies might be to consider delivery of corporate service functions on a joint basis across two contiguous local authorities. A scale efficiency of 10% across selected local authorities through joint administrative arrangements or otherwise would release 170 WTEs for redeployment elsewhere.15”

The report also suggests the consideration of clustering of local authorities to achieve greater scale efficiencies. The list below illustrates the Review Group’s suggested clustering16:

- Mayo Roscommon - Sligo Leitrim - Waterford City & County

- North Tipp South Tipp

- Cavan Monaghan - Longford Westmeath - Limerick City & County

- Carlow Kilkenny

- Laois Offaly - Galway City & County

Delivery of water services along the River Basin Plan will, the Review Group believes, be challenging as the responsibility for implementation “is assigned amongst too many organisation and no single body has ultimate responsibility17.” However, the Review Group believes that there are advantages in taking this regional approach, including:

Improvements in efficiencies and cooperation;

Building and retaining expertise in identified areas which all water services can avail of

exploitation of economies of scale and potential cross boundary efficiencies;

Strengthening the capacity to plan and deliver strategically important projects and broaden the strategic context for locally delivered programmes;

Minimising duplication of resources and reducing the administrative burden; and

Improving service delivery.

14

Public Service Agreement – 2010-2014, June 2010, page 38 15

Local Government Efficiency Review Group, July 2010, page 62 16

Local Government Efficiency Review Group, July 2010, page 63 17

Local Government Efficiency Review Group, July2010, page 124

Irish Water: Phase 1 Report

PwC Page 19 of 79

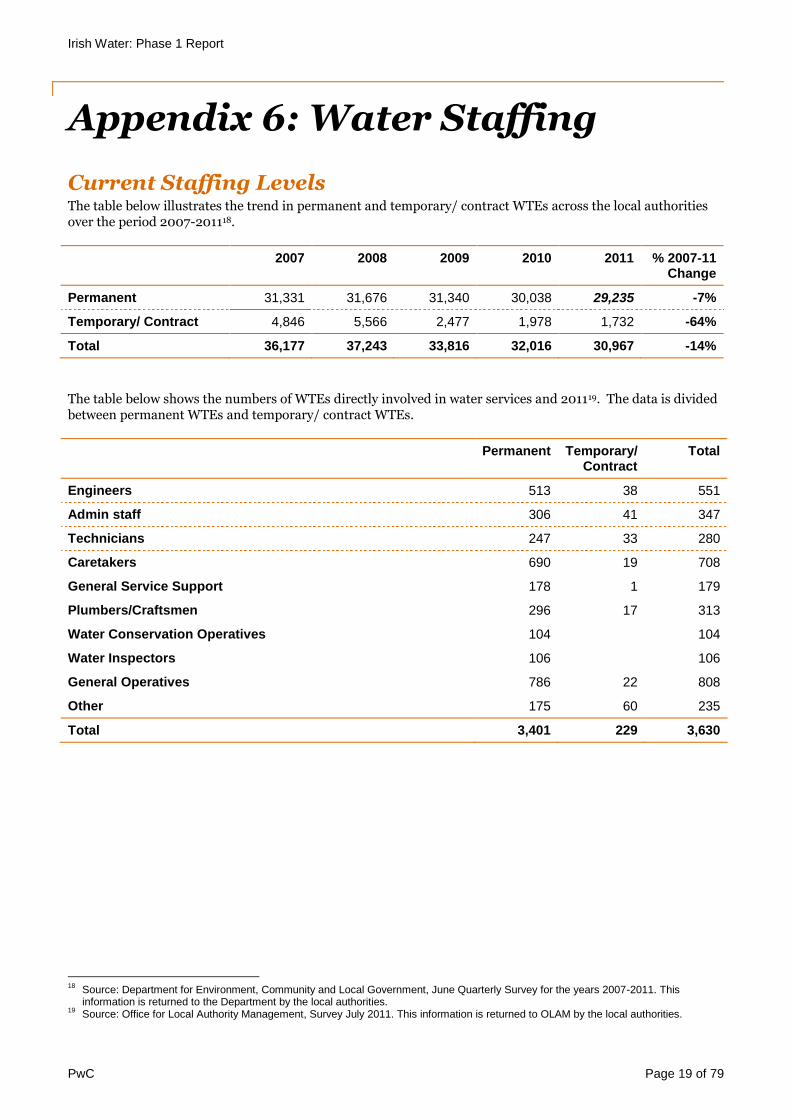

Appendix 6: Water Staffing

Current Staffing Levels The table below illustrates the trend in permanent and temporary/ contract WTEs across the local authorities over the period 2007-201118.

2007 2008 2009 2010 2011 % 2007-11 Change

Permanent 31,331 31,676 31,340 30,038 29,235 -7%

Temporary/ Contract 4,846 5,566 2,477 1,978 1,732 -64%

Total 36,177 37,243 33,816 32,016 30,967 -14%

The table below shows the numbers of WTEs directly involved in water services and 201119. The data is divided between permanent WTEs and temporary/ contract WTEs.

Permanent Temporary/ Contract

Total

Engineers 513 38 551

Admin staff 306 41 347

Technicians 247 33 280

Caretakers 690 19 708

General Service Support 178 1 179

Plumbers/Craftsmen 296 17 313

Water Conservation Operatives 104 104

Water Inspectors 106 106

General Operatives 786 22 808

Other 175 60 235

Total 3,401 229 3,630

18

Source: Department for Environment, Community and Local Government, June Quarterly Survey for the years 2007-2011. This information is returned to the Department by the local authorities.

19 Source: Office for Local Authority Management, Survey July 2011. This information is returned to OLAM by the local authorities.

Irish Water: Phase 1 Report

PwC Page 20 of 79

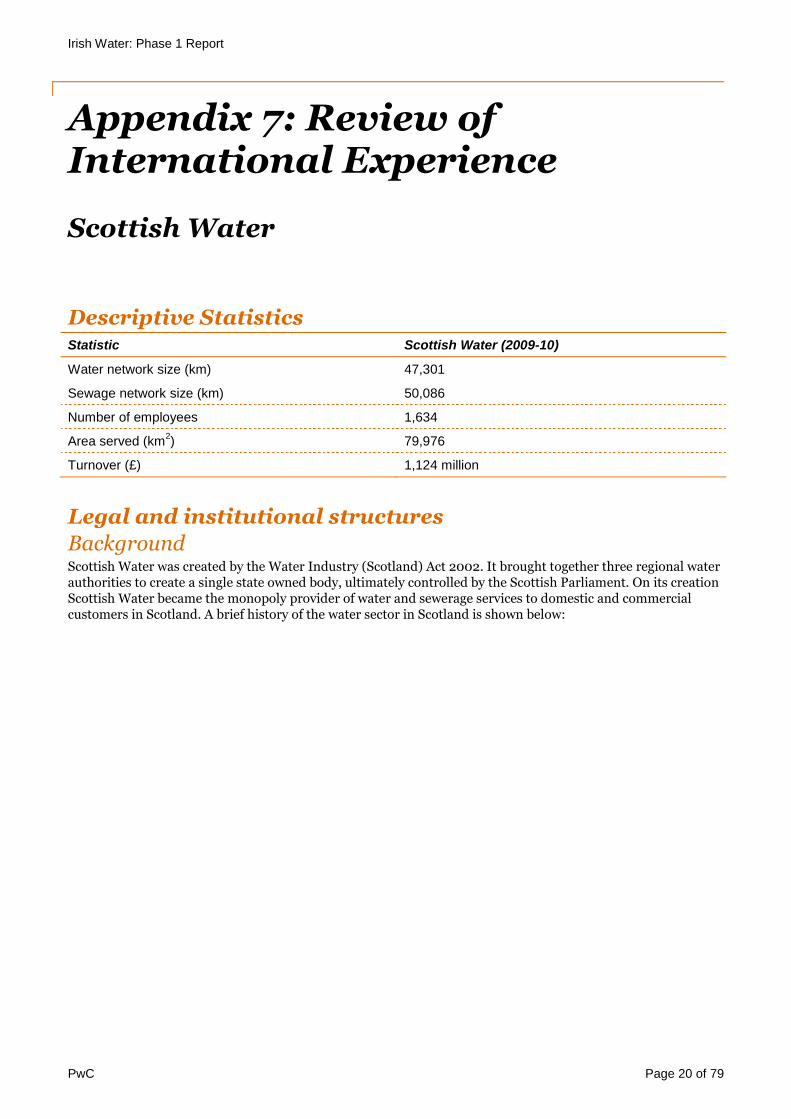

Appendix 7: Review of International Experience

Scottish Water

Descriptive Statistics Statistic Scottish Water (2009-10)

Water network size (km) 47,301

Sewage network size (km) 50,086

Number of employees 1,634

Area served (km2) 79,976

Turnover (£) 1,124 million

Legal and institutional structures

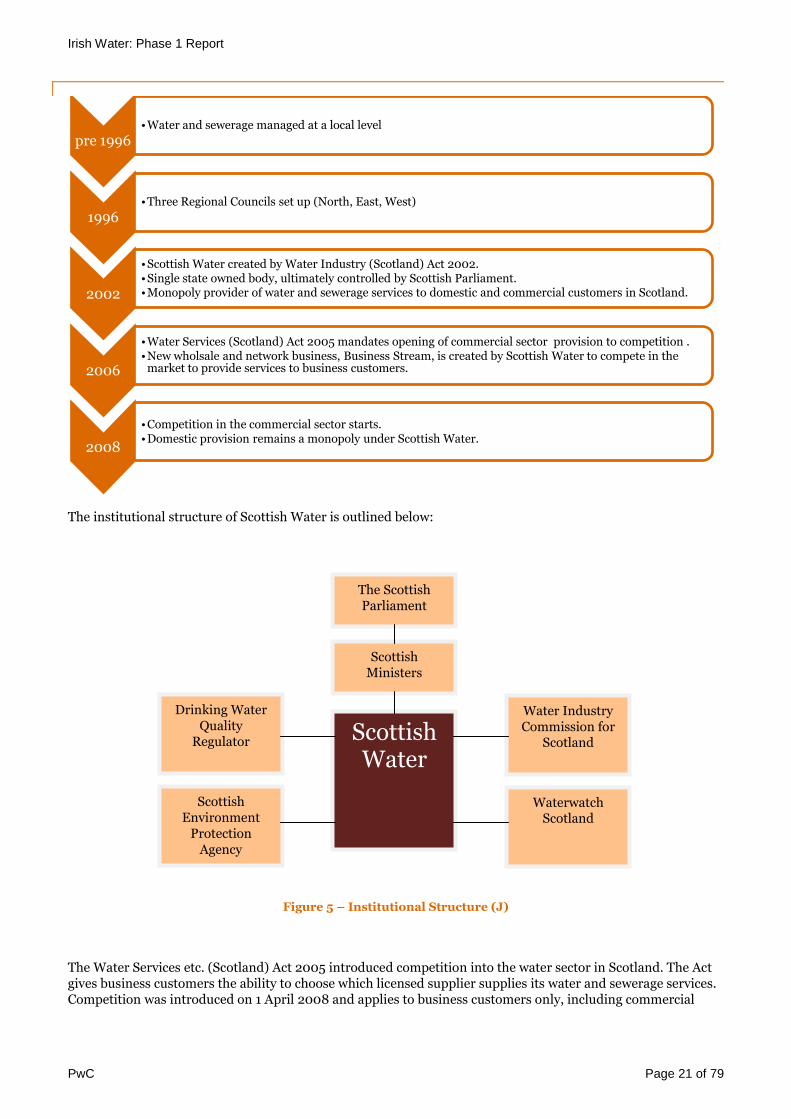

Background Scottish Water was created by the Water Industry (Scotland) Act 2002. It brought together three regional water authorities to create a single state owned body, ultimately controlled by the Scottish Parliament. On its creation Scottish Water became the monopoly provider of water and sewerage services to domestic and commercial customers in Scotland. A brief history of the water sector in Scotland is shown below:

Irish Water: Phase 1 Report

PwC Page 21 of 79

The institutional structure of Scottish Water is outlined below:

Figure 5 – Institutional Structure (J)

The Water Services etc. (Scotland) Act 2005 introduced competition into the water sector in Scotland. The Act gives business customers the ability to choose which licensed supplier supplies its water and sewerage services. Competition was introduced on 1 April 2008 and applies to business customers only, including commercial

pre 1996 •Water and sewerage managed at a local level

1996 •Three Regional Councils set up (North, East, West)

2002

•Scottish Water created by Water Industry (Scotland) Act 2002. •Single state owned body, ultimately controlled by Scottish Parliament. •Monopoly provider of water and sewerage services to domestic and commercial customers in Scotland.

2006

•Water Services (Scotland) Act 2005 mandates opening of commercial sector provision to competition . •New wholsale and network business, Business Stream, is created by Scottish Water to compete in the

market to provide services to business customers.

2008

•Competition in the commercial sector starts. •Domestic provision remains a monopoly under Scottish Water.

Scottish Water

Drinking Water Quality

Regulator

Waterwatch Scotland

Scottish Ministers

Scottish Environment

Protection Agency

The Scottish Parliament

Water Industry Commission for

Scotland

Irish Water: Phase 1 Report

PwC Page 22 of 79

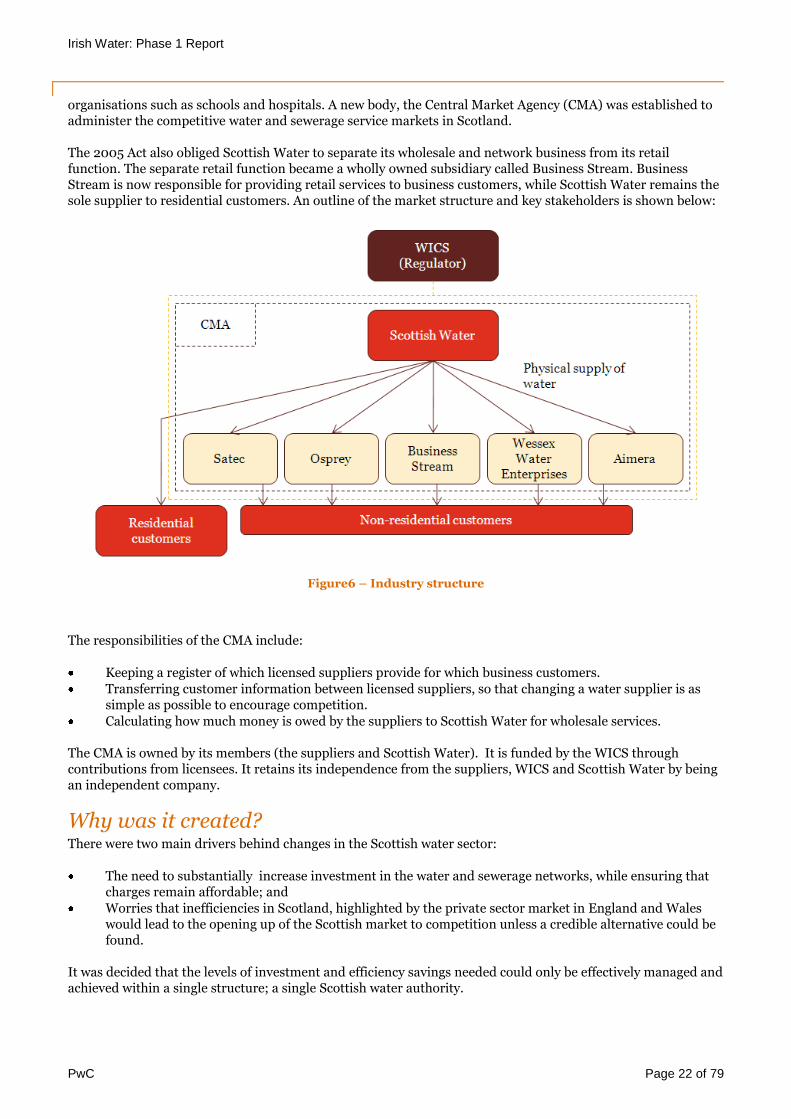

organisations such as schools and hospitals. A new body, the Central Market Agency (CMA) was established to administer the competitive water and sewerage service markets in Scotland.

The 2005 Act also obliged Scottish Water to separate its wholesale and network business from its retail function. The separate retail function became a wholly owned subsidiary called Business Stream. Business Stream is now responsible for providing retail services to business customers, while Scottish Water remains the sole supplier to residential customers. An outline of the market structure and key stakeholders is shown below:

Figure6 – Industry structure

The responsibilities of the CMA include:

Keeping a register of which licensed suppliers provide for which business customers.

Transferring customer information between licensed suppliers, so that changing a water supplier is as simple as possible to encourage competition.

Calculating how much money is owed by the suppliers to Scottish Water for wholesale services.

The CMA is owned by its members (the suppliers and Scottish Water). It is funded by the WICS through contributions from licensees. It retains its independence from the suppliers, WICS and Scottish Water by being an independent company.

Why was it created? There were two main drivers behind changes in the Scottish water sector:

The need to substantially increase investment in the water and sewerage networks, while ensuring that charges remain affordable; and

Worries that inefficiencies in Scotland, highlighted by the private sector market in England and Wales would lead to the opening up of the Scottish market to competition unless a credible alternative could be found.

It was decided that the levels of investment and efficiency savings needed could only be effectively managed and achieved within a single structure; a single Scottish water authority.

Irish Water: Phase 1 Report

PwC Page 23 of 79

The rationale behind the creation of Scottish Water was that it would:

Enable efficiencies in operating and capital investment expenditure to be achieved;

Provide a consistent approach to customers across Scotland in terms of charges and additional services;

Enable the organisation to compete for the retention of customers in border areas open to potential cross-border competition;

Allow a more consistent and strategic approach to investment planning and procurement so that environmental and quality objectives could be met more effectively.

It was also believed by the Scottish Executive that a larger body would be better placed than the three smaller authorities, in terms of economies of scale, critical mass and brand strength, to compete for business across Scotland and elsewhere in the UK. 20

During the process of creating Scottish Water, the Scottish Executive also identified the potential disadvantages that might arise from moving to a single authority. The most significant of these was the difficulty in regulating the authority in the absence of any direct comparisons in Scotland, and the risk that efficiency savings would not be achieved. As a result, Scottish Water is benchmarked, where possible, against water companies in England and Wales.

There was also a risk that local responsiveness would be lost. Local responsiveness is maintained through WaterWatch Scotland, which has regional panels based on local authority boundaries that represent consumer concerns, although Scottish Water itself does not operate on a regional structure.

Regulation

Obligations and duties The Scottish water industry is monitored and managed by a range of different bodies:

The primary role of the Water Industry Commission for Scotland (WICS) is to promote the interests of customers of the Scottish water authorities and to advise the Scottish Executive about levels of water charges. The Commissioner is responsible for regulating the economic and customer service performance of the water authorities.21

The Scottish Environment Protection Agency (SEPA) are responsible for environmental protection and improvement.

The Scottish Parliament holds Scottish Water and Ministers to account and regularly calls executives to its committees to give progress updates.

Scottish Ministers set the objectives for Scottish Water and appoint the Chair and Non-executive Directors.

Scottish Water are responsible for providing water and waste water services to household customers and wholesale Licensed Providers. They deliver the investment priorities of Ministers within the funding allowed by WICS.

The Drinking Water Quality Regulator (DWQR) is responsible for protecting the public by ensuring compliance with drinking water quality regulations. The DWQR is able to monitor drinking water, investigate possible breaches of regulations and enforce compliance.22

Waterwatch Scotland are responsible for representing the interests of Scottish Water customers.

20 A.The Scottish Executive. ‘Water Services Bill – The Executive’s Proposal’. (year unspecified). p1-12

21 A. The Scottish Parliament Information Centre. ‘Research Paper: Water Industry (Scotland) Bill’. 2001 (p6) 22 A. The Scottish Parliament Information Centre. ‘Research Paper: Water Industry (Scotland) Bill’. 2001 (p8)

Irish Water: Phase 1 Report

PwC Page 24 of 79

Scottish Water Minister

Price Control Process WICS has a statutory duty to promote the interests of customers. They set charge caps for water and sewerage services that deliver Ministers’ objectives for the water industry at the lowest reasonable overall cost.

The cap setting process, detailed in a Final Determination document, takes place every five years. It includes limits on the amount Scottish Water can charge households and limits on the amount Scottish Water can charge licensed retail suppliers in return for wholesale services. It also determines the price caps for retail suppliers when they supply services to non-domestic customers. The non-domestic cap is set at the price which customers would have been charged if Scottish Water was still providing services directly.

Price caps are set using the Retail Price Index (RPI), plus or minus a percentage that reflects the targets of efficiency and quality that have been set. In setting charge caps, WICS aims to give Scottish Water a level of revenue that covers all of its operating, capital and financing costs, taking account of the level of borrowing that is made available by the Scottish Government.

The factors that contribute to the price caps are:

Allowed rate of return;

PPP spend;

Allowed operational expenditure;

Growth and;

Chargeable customer base.

The Final Determination of price caps has been set for the period 2010-15. Prices are set to rise at 5% below the rate of inflation. The caps challenge Scottish Water to improve its efficiency further and deliver all of the charging and revised investment objectives of the Scottish Government. Objectives include Drinking water quality, Environmental improvement, Customer Service, Capital maintenance, Growth and an Efficiency challenge.

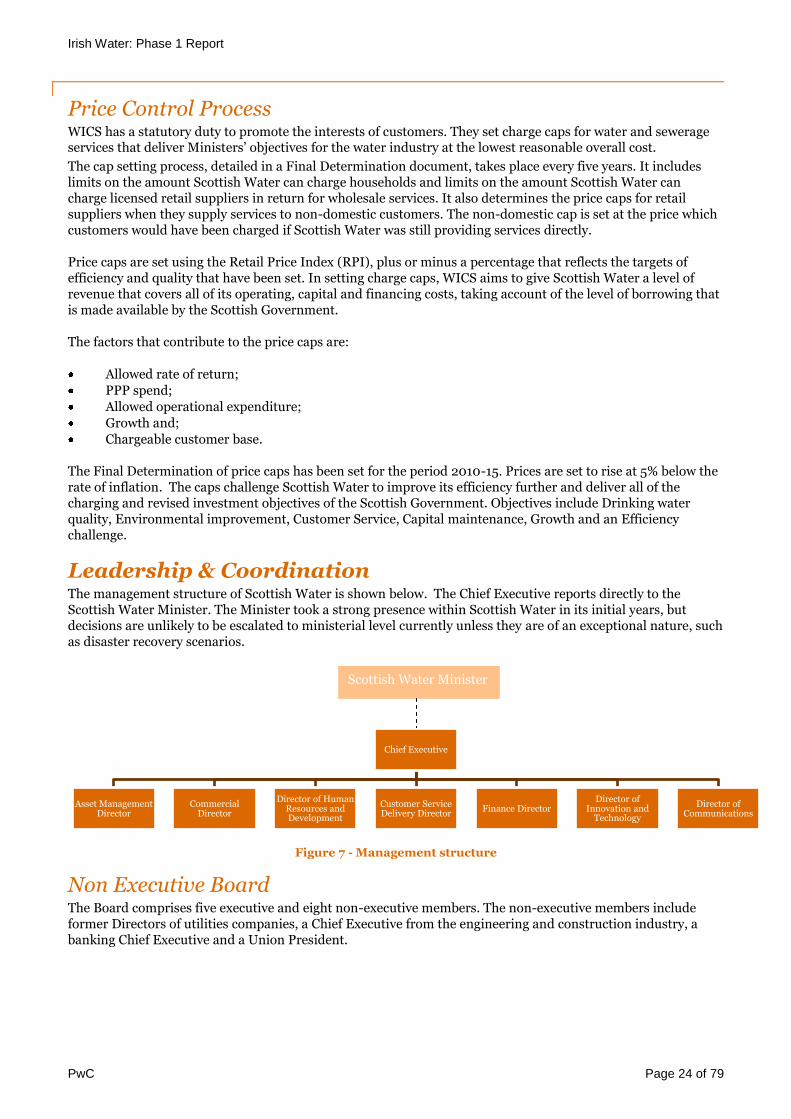

Leadership & Coordination The management structure of Scottish Water is shown below. The Chief Executive reports directly to the Scottish Water Minister. The Minister took a strong presence within Scottish Water in its initial years, but decisions are unlikely to be escalated to ministerial level currently unless they are of an exceptional nature, such as disaster recovery scenarios.

Figure 7 - Management structure

Non Executive Board The Board comprises five executive and eight non-executive members. The non-executive members include former Directors of utilities companies, a Chief Executive from the engineering and construction industry, a banking Chief Executive and a Union President.

Chief Executive

Asset Management Director

Commercial Director

Director of Human Resources and Development

Customer Service Delivery Director

Finance Director Director of

Innovation and Technology

Director of Communications

Irish Water: Phase 1 Report

PwC Page 25 of 79

Operations

Delivery Model The majority of Scottish Water’s operations are delivered in house. However, partnership structures and outsourcing are also used extensively. Operations are coordinated centrally, rather than within the original regional structures, and management is functionally driven, with separate teams working on water and sewerage.

Operating Costs Scottish Water was given an initial operating cost savings challenge of 40% in the period from 2001-2007. They claim to have met this challenge while improving overall service to customers. This was achieved primarily through a major IT restructuring (see IT section).

Scottish Water’s major goal is to reach the upper quartile water industry performance by 2013-14 by improving productivity. This will be achieved through:

Driving process compliance to the core of the business;

Championing first time resolution of customer issues, and;

Realising fully the benefits from the use of information and technology.23

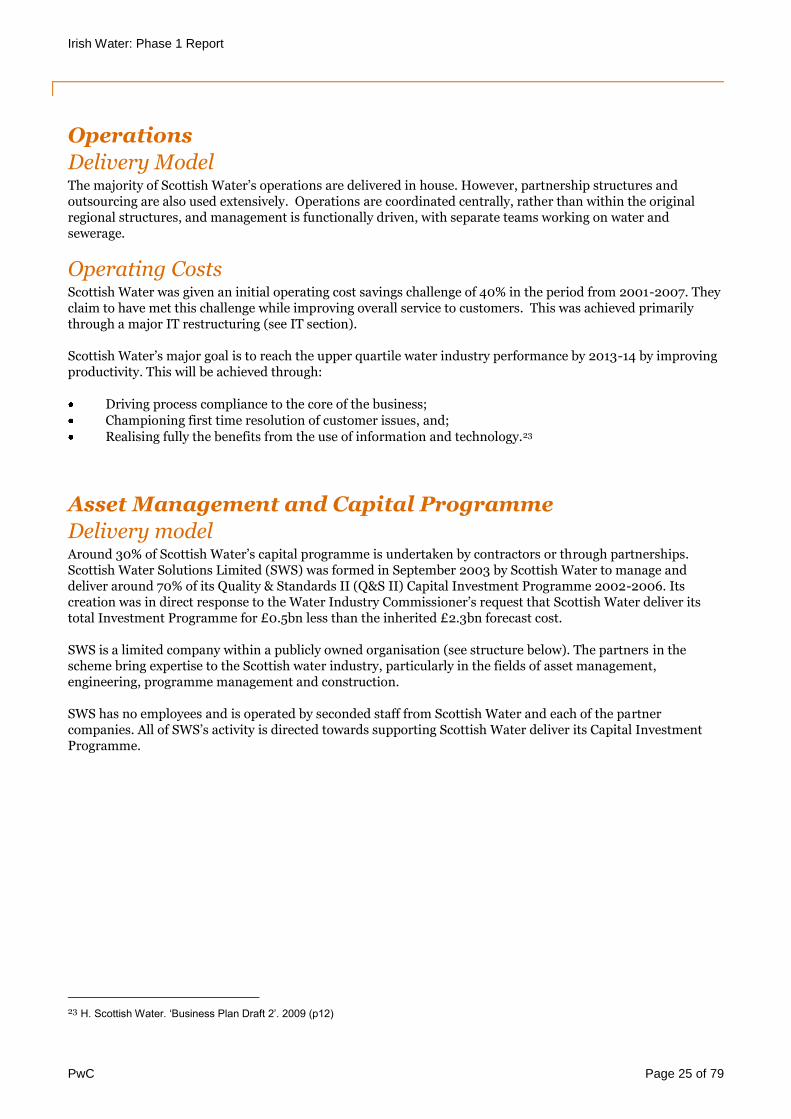

Asset Management and Capital Programme

Delivery model Around 30% of Scottish Water’s capital programme is undertaken by contractors or through partnerships. Scottish Water Solutions Limited (SWS) was formed in September 2003 by Scottish Water to manage and deliver around 70% of its Quality & Standards II (Q&S II) Capital Investment Programme 2002-2006. Its creation was in direct response to the Water Industry Commissioner’s request that Scottish Water deliver its total Investment Programme for £0.5bn less than the inherited £2.3bn forecast cost.

SWS is a limited company within a publicly owned organisation (see structure below). The partners in the scheme bring expertise to the Scottish water industry, particularly in the fields of asset management, engineering, programme management and construction.

SWS has no employees and is operated by seconded staff from Scottish Water and each of the partner companies. All of SWS’s activity is directed towards supporting Scottish Water deliver its Capital Investment Programme.

23 H. Scottish Water. ‘Business Plan Draft 2’. 2009 (p12)

Irish Water: Phase 1 Report

PwC Page 26 of 79

Figure 8 - Scottish Water Solutions ownership structure (SWS website)

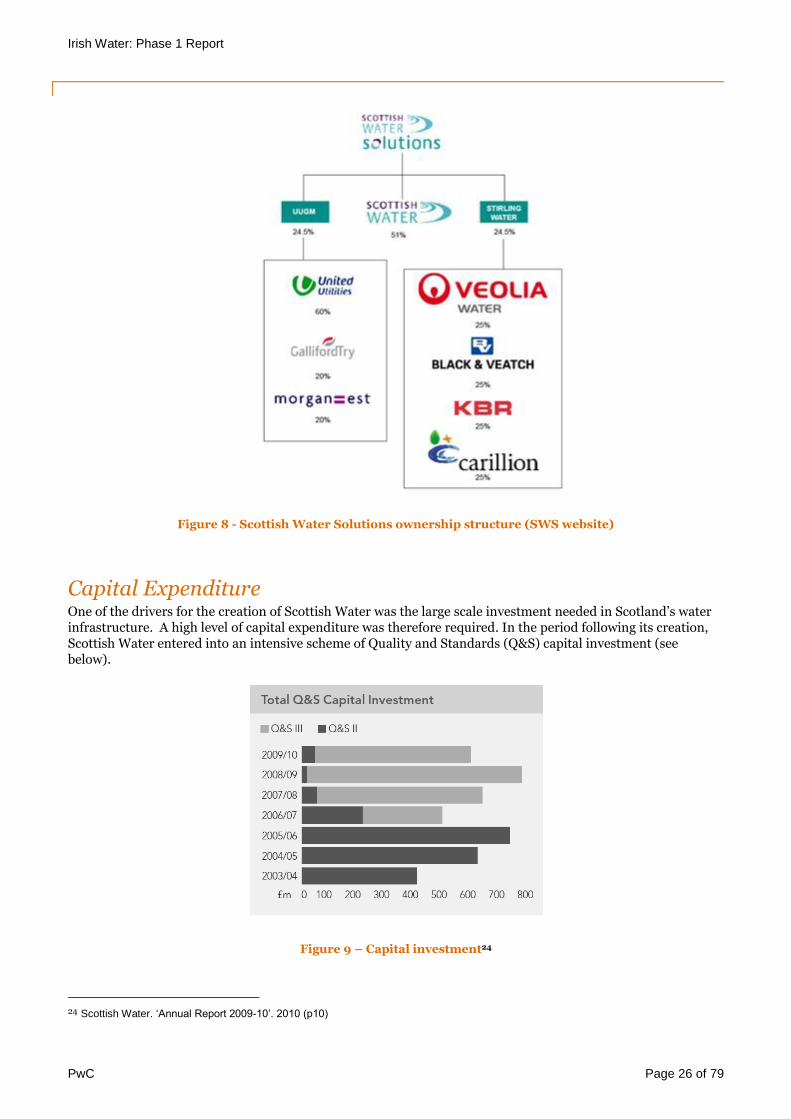

Capital Expenditure One of the drivers for the creation of Scottish Water was the large scale investment needed in Scotland’s water infrastructure. A high level of capital expenditure was therefore required. In the period following its creation, Scottish Water entered into an intensive scheme of Quality and Standards (Q&S) capital investment (see below).

Figure 9 – Capital investment24

24 Scottish Water. ‘Annual Report 2009-10’. 2010 (p10)

Irish Water: Phase 1 Report

PwC Page 27 of 79

During 2010-15, Scottish Water is expected to invest more than £2.5 billion in its assets. The investment is intended to improve drinking water quality and the environment, provide cleaner beaches and rivers, provide better service for customers and create a more sustainable water industry. Current and future capital investment is driven by requirements set out in the EU Directives on drinking water quality and on appropriate standards of treatment for wastewater discharges to the environment.25

During 2010-15 Scottish Water also aims to deliver their Q&SIIIb (capital investment) objectives including the delivery of an overall efficiency of £274m (12.3%) against the cost base that was used to build their estimates.

Scottish Water aims to achieve capital efficiencies by reducing both internal and contractor costs (management, feasibility, design and construction) as a result of the improved definition of maintenance and enhancement programmes.

Scottish Water’s capital projects are procured based on target cost with a pain/gain arrangement; the commercial arrangements ensure that continuous market testing of costs is undertaken through tendered projects and, where the target cost cannot be agreed within partnership contracts, projects are also let to the market. There are mechanisms in the procurement strategy to protect Scottish Water from losses in the event of non-delivered outputs through parent company guarantees.26

Customer Service & Billing

Background A 2001 Scottish Parliament research paper states that ‘the need for continued high investment in the Scottish water and sewerage infrastructure, and the implications of EU and UK competition rules mean that the ability for Scottish Water to generate new sources of funding is crucial.’ 27

The original three regional water providers in Scotland could only generate revenue through borrowing, directly charging their domestic and non-domestic customers for water and/or sewerage services supplied and central Government grants. Scottish Water has the power to levy charges on customers (levels as agreed by the Commissioner) or to make agreements with individual customers. This means that, for example, a company with nationwide outlets no longer has to negotiate charging agreements with three different organisations.

The Water Industry (Scotland) Bill enables Scottish Water to obtain information from local authorities which could help it develop a charging scheme. Such information includes council tax, council water charges, non-domestic water and sewerage rates and non-domestic rates.

When Scottish Water was formed there were large pricing differences across the country as a result of historic charging rates. One of the major initial targets of Scottish Water was to introduce a unified charging structure across the whole service area.

Charging Domestic customers are charged either on a metered or unmetered basis. Unmetered customers are charged a standard rate linked to their council tax band. Payment for unmetered customers is collected by local councils on behalf of Scottish Water.

Metered customers pay a fixed annual fee for their connection, based on the size of their connection pipe, and a fixed property and roads drainage charge based on their council tax band. They then pay volumetric rates for their water and waste water services. Only a very small number of properties are metered in Scotland, primarily due to the favourable non-metered rates and the public perception that metering is indicative of the private sector entering the water industry.

25 The Scottish Government. ‘Building a Hydro Nation – A Consultation’. 2010 (p2)

26 Scottish Water. ‘Business Plan Draft 2’. 2009 (p19)

27 The Scottish Parliament Information Centre. ‘Research Paper: Water Industry (Scotland) Bill’. 2001 (p15-22)

Irish Water: Phase 1 Report

PwC Page 28 of 79

Commercial water services can be provided by a range of businesses (see Figure ) that purchase on a wholesale basis from Scottish Water. Commercial customers receiving services from the Scottish Water owned company Business Stream may be metered or unmetered. Unmetered customer charges are based on council rates for their property. All payments are made directly to Business Stream rather than via councils.

Domestic customers For properties with non-metered supply the person liable for council tax is responsible for paying water bills. Local authorities collect the water and sewerage charges in their area on behalf of Scottish Water. Although council tax and water & sewerage charges are shown separately on household bills, the debt is combined such that people cannot pay their council tax but refuse to pay any water charges for which they are liable.28

A key feature of the arrangements for charging domestic customers is the link between charges and the Council Tax band of the property served. Those living in higher banded properties, who tend to be better off, pay more for their water and sewerage services than those in lower banded properties.

The Scottish Executive have proposed that regardless of how competition develops the principle of higher banded properties paying more than lower banded properties should be maintained. Similar provisions for meters are proposed, so that in future the standing and volumetric charges levied on those choosing to use meters are based on the combination of average charges and the Council Tax band ratio of the property served.29

Commercial customers Each licensed provider is charged by Scottish Water for the supply of water and sewerage services to the premises registered to the licensed supplier. The charging methodology varies depending on whether the premises is metered or un-metered.

Scottish Water is responsible for installing meters. The meter installation programme equipped all unmeasured non-household supply points with meters by April 2009. As a result of the meter installation programme, many customers moved from assessed charges based on the rateable value30 of their premises, to charges based on their actual usage. This change was undertaken on a phased basis.

In 2009/10, the phased introduction meant that the wholesale charge was based on a combination of:

Assessed meter size (related to the rateable value of the premises) and the assessed volume of

consumption (67% of the overall charge); and

Actual tariff meter size and the actual volume recorded on the meter (33% of overall charge).

In future years, the phasing did not apply. The overall charge is now entirely based on the actual tariff meter size and volume.

Where the licensed supplier believes that the assessed meter size and/or assessed volume consumption at a supply point are not reflective of usage, they may request a re-assessment provided they have sufficient supporting evidence.

Safety nets Exemption from Council Tax does not give exemption from water charges. Council Benefits do not currently pay for water charges, although the Scottish government has subsidised this in the past. The permanent Water Charges Reduction Scheme, a reduction of up to 25% introduced by the Scottish Government at 1st April 2006,

28 A.The Scottish Parliament Information Centre. ‘Research Paper: Water Industry (Scotland) Bill’. 2001 (p18)

29 The Scottish Executive. ‘Water Services Bill – The Executive’s Proposal’. (p22)

30 Rateable Value of a premises’ supply point: Each supply point will be assigned a Rateable Value based on the April 2000 rates

revaluation, although it may be re-valued depending on individual circumstances. The Rateable Value is the basis for levying Property

and Roads Drainage Charges, and also a basis for Water and Foul Sewerage Charges.

Irish Water: Phase 1 Report

PwC Page 29 of 79

is applied automatically to households with 2 or more adults which are in receipt of Council Tax Benefit and are not already in receipt of discounts. The Disabled Banding Reduction exists for properties that have been altered to meet the needs of a disabled person.

As mentioned above, whilst council tax and water & sewerage charges are shown separately on household bills, the debt is combined such that people cannot pay their council tax but refuse to pay any water charges for which they are liable. If people on 100% council tax benefit fall into arrears with their water charges, their arrears would still be classified as combined council tax and water charges debt.31

Customer service WICS monitors and reports on Scottish Water’s customer service performance in providing service to customers. It also sets targets for improvement. A points-based system, the Overall Performance Assessment (OPA), is used to monitor performance.

The OPA was originally developed by Ofwat to compare the customer service performance of the companies in England and Wales. Since 2002, Scottish Water's OPA score has more than doubled, increasing from 132 to 291 in 2009-10. They now aim to at least match the OPA scores of the leading companies in England and Wales by 2013-14.

England and Wales are to stop using the OPA as a performance indicator in 2011 in favour of an incentive driven system, the Service Incentive Mechanism (SIM). It is not clear whether Scotland plans to follow.

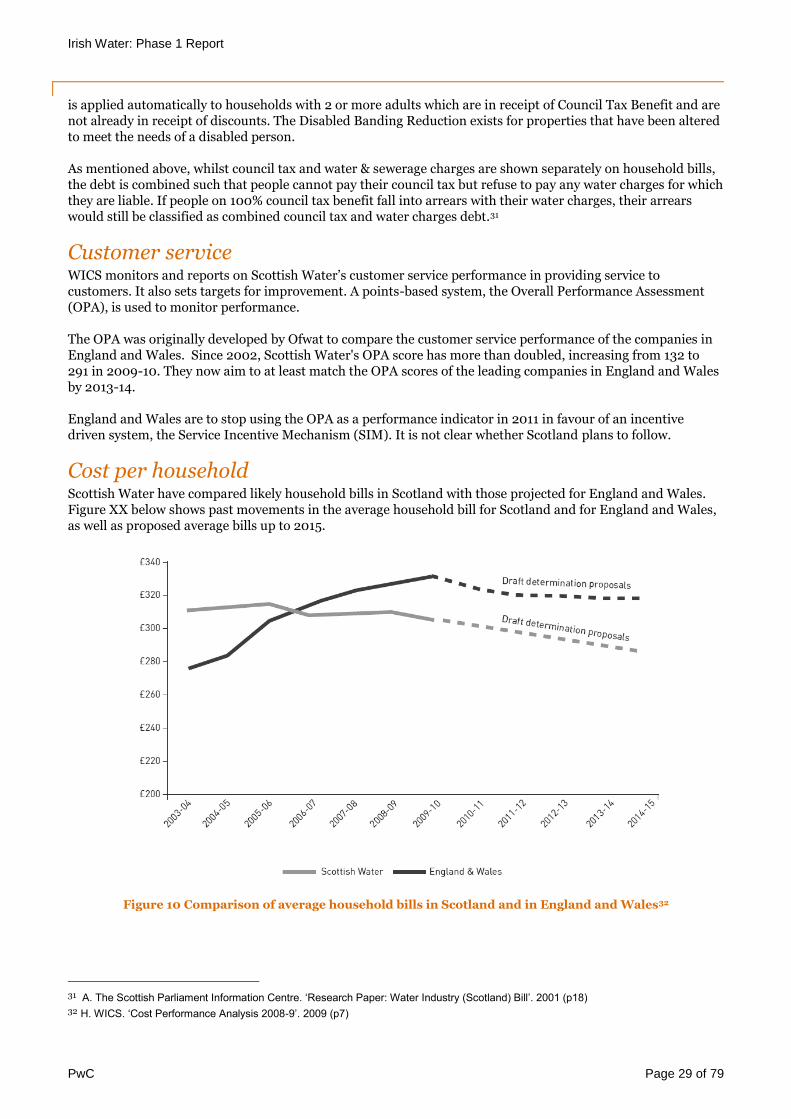

Cost per household Scottish Water have compared likely household bills in Scotland with those projected for England and Wales. Figure XX below shows past movements in the average household bill for Scotland and for England and Wales, as well as proposed average bills up to 2015.

Figure 10 Comparison of average household bills in Scotland and in England and Wales32

31 A. The Scottish Parliament Information Centre. ‘Research Paper: Water Industry (Scotland) Bill’. 2001 (p18)

32 H. WICS. ‘Cost Performance Analysis 2008-9’. 2009 (p7)

Irish Water: Phase 1 Report

PwC Page 30 of 79

Finance

Background The Water Industry (Scotland) Act states that ‘Scottish Water must exercise its functions so as to secure that, taking one year with another, its income is not less than sufficient to meet its expenditure.’ 33

Provisions were included in the Act to enhance water authority powers to enter into various forms of contractual agreements. These permit the water authority to enter into any form of Private Finance Initiative (PFI) and Public Private Partnership (PPP) agreements. It provides the power to enter into various types of joint venture, either with the intention to serve customers through the venture or to be part of a venture formed for the purposes of serving customers not currently served by the authority. It also provides a power for the authority to contract with third parties to lay water mains and service pipes.34

On the creation of Scottish Water a Regulatory Capital Value (RCV) was defined for the new body by a basic combination of the values of the three original organisations. These three values are unlikely to have been reached using the same methods.

Income Income from customers is of the order of £1bn/yr. Predicted increases are based on the Retail Price Index (RPI). However, Scottish Water have frozen their prices for domestic customers for the coming year.

Financeability Scottish Water has a £564m requirement for borrowing in the 2010-14 period, with annual increases of between £117 and £149m per annum. The profile of forecast borrowing is subject to an annual limit of available Scottish Government borrowing of less than £150m.35 The Scottish Government is, at present, the only provider of capital and the sole holder of equity.36

With increasing pressures on Scottish Government public expenditure, there is uncertainty over the level of borrowing that may be available for Scottish Water in 2010-14 and beyond. If funds cannot be secured through available Scottish Government borrowing, then Scottish Water will pursue other sources of finance.

During 2002-2009 Scottish Water had sufficient access to Scottish Government borrowing to finance their capital investment programme. However, their borrowing allowance for 2009/10 was limited such that the full costs of completing the current investment plan were planned to be financed by non-government borrowing from April 2010.

Scottish Water has the ability to take loans from its commercial arm, Scottish Water Business Stream (SWBS) Holdings Ltd. However, Scottish Water does not have access to the commercial equity market. It was therefore felt necessary to create a temporary government loan facility (up to £50m) to cover unexpected costs such as emergencies. In 2010 this was replaced by a growing savings account, or ‘gilts buffer’, financed by Scottish Water by outperforming their Regulatory targets.

The buffer is invested in index-linked, gilt-edged securities, in which excess cash arising from outperformance on capital or operating costs are held. This gilts buffer is intended to maintain the pressure on Scottish Water to improve its performance, by ensuring that good performance in one period could not be used to pay for poor performance in another period. Savings held in the buffer are to be returned to customers in the form of reduced prices if they are not used within four years.

33 C. Act of Parliament. ‘Water Industry (Scotland) Act 2002’. 2002 (p22)

34 A. The Scottish Executive. ‘Water Services Bill – The Executive’s Proposal’. (p15)

35 H. Scottish Water. ‘Business Plan Draft 2’. 2009 (p18)

36 http://www.watercommission.co.uk/UserFiles/Documents/Final%20Determination%20document.pdf

Irish Water: Phase 1 Report

PwC Page 31 of 79

WICS ensures that Scottish Water meets the appropriate industry investment grades as part of the Price Determination. The following financial ratios are used (2010-15 Price Determination):

Assumed range of financial ratios during Regulatory control period37

Financial ratio Average assumed value in this Final Determination

Norm for investment grade

Our intention to maintain

FFO/debt 12.5% Around 13.0% 11% to 13%

RCF/debt 12.5% Around 8.0% 11% to 13%

Cash interest cover 3.4 Around 3.0 >3.0

Cash interest cover I (capital charges: adjusted

1.6 Around 1.6 1.5 to 2.0

Cash interest cover II (actual capital maintenance expenditure)

2.1 Around 2.0 2.0 to 2.5

Forecast ratios 2010/11 2011/12 2012/13 2013/14

Cash interest cover 3.50 3.52 3.48 3.46

Funds from operations to debt 13.3% 13.3% 12.9% 12.7%

Gearing 55% 56% 56% 56%

PPPs/PFIs Scottish Water is dependent on PFI contracts for the performance of around 50% of its wastewater services. In some cases these contracts, established in the late 1990s, are inadequately incentivised and structured to ensure delivery of objectives.38 Total PFI costs are in the region of £140m/yr.

HR On the creation of Scottish Water, all employees of the three water boards became employees of the new entity. In the period between 2001 and 2002, generous voluntary redundancy packages were introduced, costing Scottish Water £80m. No compulsory redundancies were made as a matter of policy.

An Employee Council was created in ‘genuine partnership’ with Unions and employees to help manage change. As a result Scottish Water was able to reduced staff by over 2500 (from over 5600 employees in 2002) with no industrial action.

Scottish Water currently has over 1,634 employees (2010). Scottish Water Solutions has no employees- it has about 550 seconded staff from its partner bodies. Around 60 of these come from Scottish Water (2010).

The creation of Scottish Water removed previous constraints on outsourcing by giving the authorities and Scottish Water additional powers to make agreements with third parties.39 However Scottish Water state that they ‘only out source where (they) understood costs and outputs.’40

37 http://www.watercommission.co.uk/UserFiles/Documents/Final%20Determination%20document.pdf

38 Scottish Water. ‘Business Plan Draft 2’. 2009 (p20)

39 The Scottish Executive. ‘Water Services Bill – The Executive’s Proposal’. (year unspecified) (p15)

40 Dr Jon Hargreaves (CEO). ‘Organisational Change & the Transformation of Performance at Scottish Water’. 2007

Irish Water: Phase 1 Report

PwC Page 32 of 79

Marketing & Communications